Argentina Lubricants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

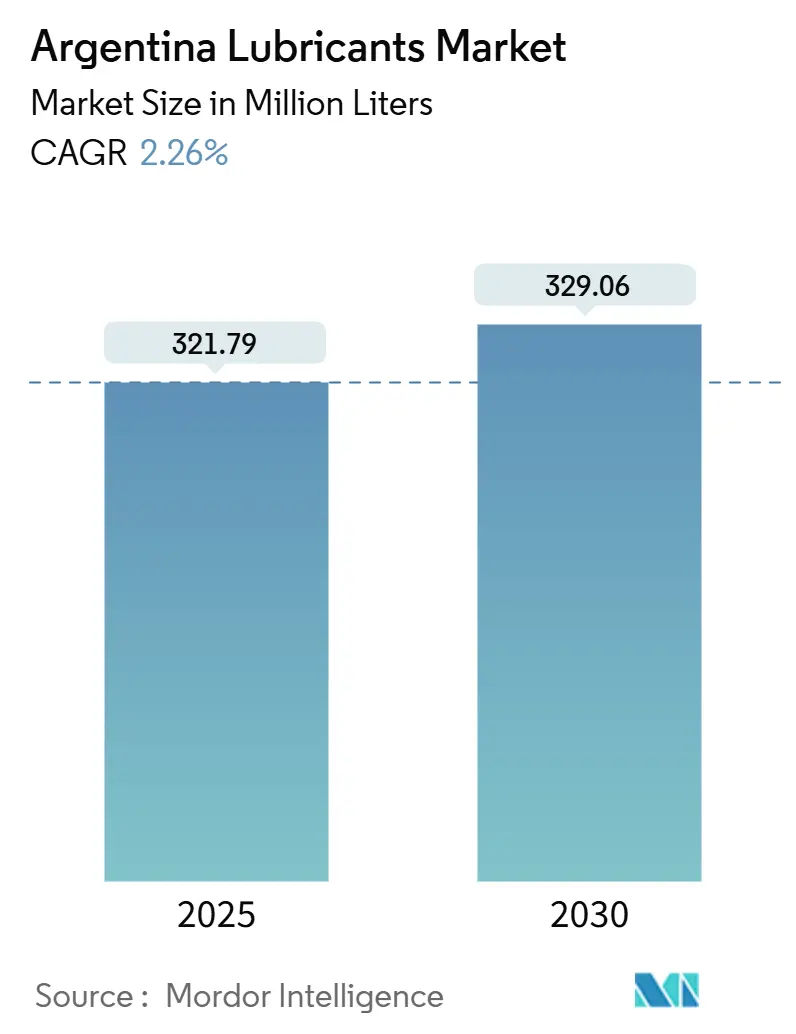

| Market Volume (2025) | 321.79 Million liters |

| Market Volume (2030) | 329.06 Million liters |

| Growth Rate (2025 - 2030) | 2.26% CAGR |

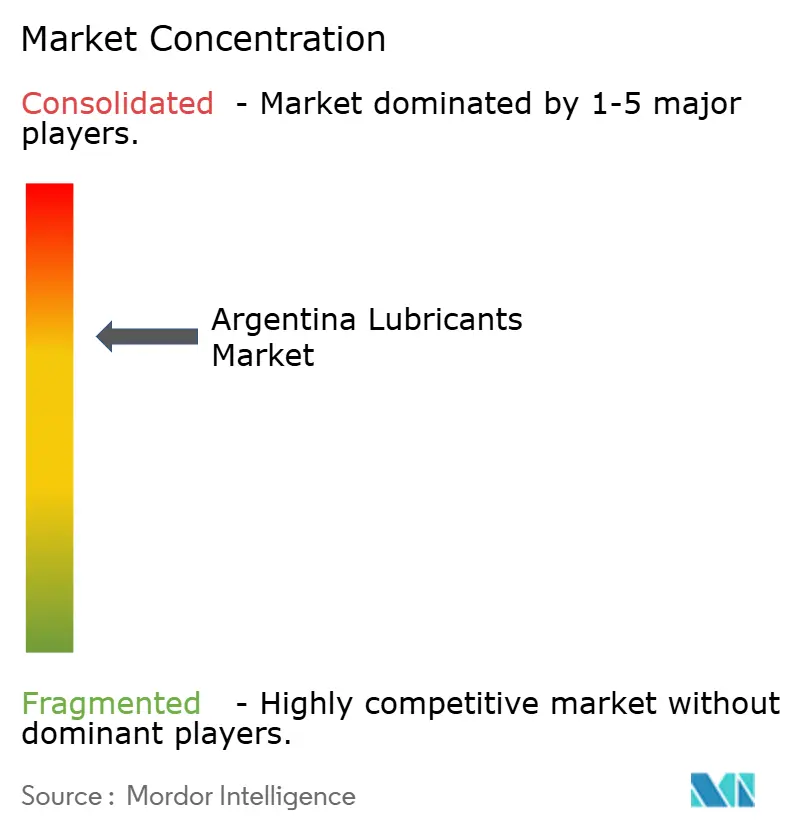

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Argentina Lubricants Market Analysis by Mordor Intelligence

The Argentina Lubricants Market size is estimated at 321.79 million liters in 2025, and is expected to reach 329.06 million liters by 2030, at a CAGR of 2.26% during the forecast period (2025-2030). The measured expansion is underpinned by a gradual economic stabilization, rising vehicle registrations, new biofuel mandates, and industrial activity tied to the Vaca Muerta shale play. Demand growth is strongest in synthetic formulations that can tolerate higher biofuel blends, while mineral oils still dominate volumes due to price-sensitive consumer behavior. Currency volatility, counterfeit products, and early electric-vehicle (EV) adoption temper near-term momentum, yet industrial projects in mining and unconventional oil support baseline consumption. Overall, the Argentine lubricants market benefits from a balanced mix of automotive after-sales demand and emerging heavy-duty requirements across the mining, construction, and energy infrastructure sectors.

Key Report Takeaways

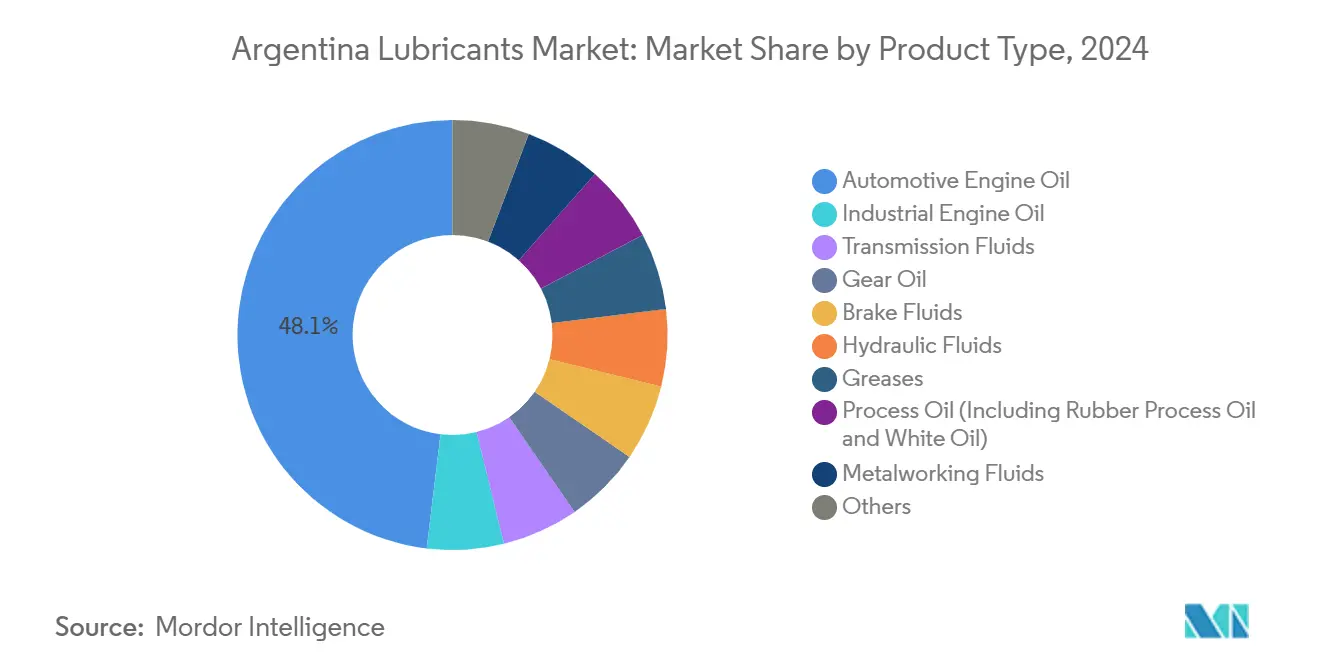

- By product type, automotive engine oil led with 48.10% of the Argentina lubricants market share in 2024, while hydraulic fluids are projected to expand at a 4.18% CAGR through 2030.

- By end-user industry, the automotive segment accounted for 56.04% of the Argentina lubricants market size in 2024, whereas heavy equipment is advancing at a 3.48% CAGR through 2030.

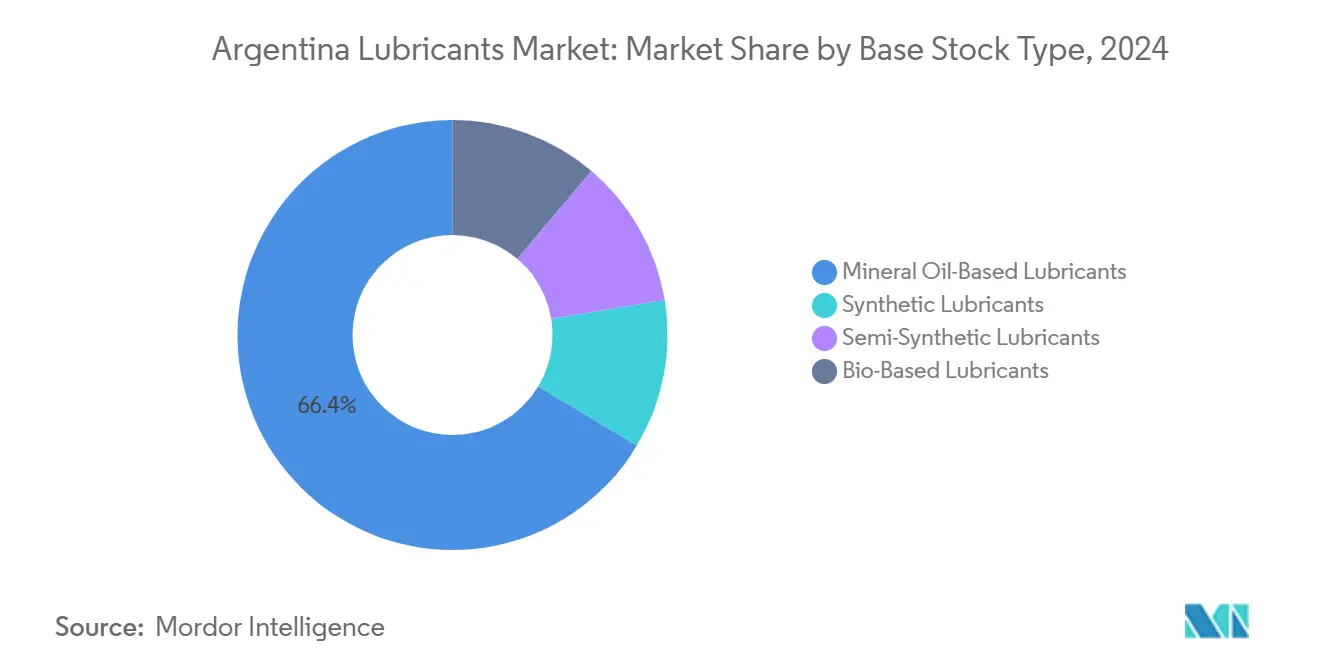

- By base stock type, mineral oil-based products held 66.40% share of the Argentina lubricants market in 2024, and synthetic oils are growing at a 4.53% CAGR through 2030.

Argentina Lubricants Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Argentina's expanding vehicle fleet boosts engine oil consumption | +0.8% | National, concentrate in Buenos Aires, Córdoba, Santa Fe | Medium term (2-4 years) |

| Resurgence of large-scale mining projects spurs demand for heavy-duty lubricants | +0.6% | Northwestern provinces (Salta, Jujuy, Catamarca) | Long term (≥ 4 years) |

| Vaca Muerta shale ramp-up increases industrial lubricants off-take | +0.5% | Neuquén province, spillover to Río Negro | Medium term (2-4 years) |

| Government bio-fuels blending mandate accelerates shift to high-performance synthetics | +0.3% | National, with early adoption in major urban centers | Short term (≤ 2 years) |

| Rapid growth of lithium-processing equipment drives specialty-grease usage | +0.4% | Northwestern provinces (Salta, Jujuy, Catamarca) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Argentina’s Expanding Vehicle Fleet Boosts Engine-Oil Consumption

Vehicle production increased in 2024, marking a rebound that helped restore assembly lines after pandemic-related slowdowns. Domestic sales recovered as financing conditions improved under macroeconomic reforms, and commercial registrations increased as logistics firms upgraded their fleets to handle the rising trade flows. Frequent service intervals for trucks and buses result in higher turnover of premium-grade lubricants, helping to stabilize the Argentine lubricants market even when discretionary car replacement cycles lengthen. Parts retailers and quick-lube chains in Buenos Aires report double-digit volume growth for OEM-approved 5W-30 synthetics, reflecting shifts toward tighter engine tolerances. Higher bio-fuel blends also require upgraded additive packages, nudging fleet operators away from legacy mineral formulations.

Resurgence of Large-Scale Mining Projects Spurs Heavy-Duty Lubricant Demand

Argentina’s lithium output is projected to triple by 2030 as the provinces of Salta, Jujuy, and Catamarca fast-track the development of brine evaporation ponds and direct-lithium-extraction (DLE) pilots[1]U.S. Geological Survey, “Mineral Commodity Summaries 2024: Lithium,” usgs.gov. Off-highway haul trucks, loaders, and drill rigs in these high-altitude sites consume hydraulic fluids, gear oils, and greases specifically designed for extreme temperature fluctuations. The World Bank’s USD 300 million Northern Argentina Mining Development Program is upgrading roads and power lines, facilitating equipment mobilization, and increasing demand for ancillary lubricants. Copper and gold prospects in San Juan and Mendoza add further opportunities. Lubricant suppliers respond with on-site filtration units and oil-condition monitoring services that extend drain intervals and lower total operating costs, reinforcing loyalty among mine operators.

Vaca Muerta Shale Ramp-Up Increases Industrial Lubricant Off-Take

Crude output from the Vaca Muerta play reached 442,000 barrels per day in April 2025, up 28% from early 2024, as producers capitalize on simplified export rules and long-term tax stability. More than 200 active rigs each consume specialized drilling fluids and hydraulic oils every month, creating a steady industrial base for the Argentine lubricants market. The USD 3 billion Vaca Muerta Sur pipeline transports crude to Atlantic ports and relies on compressor-station gear oils formulated for a wide viscosity range. Local SME suppliers receive technical assistance to qualify their products under new national content rules, thereby widening the competitive options for operators seeking quick turnaround times.

Government Bio-Fuel Blending Mandate Accelerates Shift to High-Performance Synthetics

Law 27.640 establishes minimum blends of 12% biodiesel and 7.5% bioethanol in transport fuels, while Resolutions 140/2025 and 141/2025 define the pricing and supply mechanisms. Higher oxygenate content increases oxidation risk and seal-swelling tendencies in engines, prompting a rapid shift toward synthetic and semi-synthetic lubricants with enhanced antioxidant and dispersant formulations. Major fuel retailers now bundle premium 0W-20 or 5W-30 synthetics with bio-fuel compatible service packages, boosting value per service visit and cushioning volume pressures from longer drain intervals. OEMs also align warranty policies with advanced lubricant specifications, thereby reinforcing adoption among fleet managers who are concerned about downtime.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic peso-driven inflation inflates base-oil import costs | -0.4% | National, with acute impact on import-dependent regions | Short term (≤ 2 years) |

| Unpredictable export tax policy on base oils curtails investment | -0.3% | National, particularly affecting Buenos Aires industrial zones | Medium term (2-4 years) |

| Growing preference for EVs lowers long-term ICE-oil demand | -0.2% | Urban centers (Buenos Aires, Córdoba, Rosario) | Long term (≥ 4 years) |

| Counterfeit lubricant proliferation erodes branded volumes | -0.2% | National, concentrated in price-sensitive rural markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Peso-Driven Inflation Inflates Base-Oil Import Costs

The peso lost value against the USD in 2024, while headline inflation reached 211%, increasing landed costs for base oils sourced abroad. Importers stagger their purchases to manage working-capital swings, yet discretionary buyers often gravitate toward low-priced alternatives that frequently bypass quality controls. Domestic refiners cannot meet the additive requirements for high-performing synthetics, so blender margins compress when price ceilings fail to keep pace with input costs. Some distributors now quote prices in hard currency to hedge, but the practice remains limited to B2B contracts. Retail buyers experience frequent price adjustments, eroding loyalty and encouraging gray-market imports that undercut branded products.

Growing Preference for EVs Lowers Long-Term ICE-Oil Demand

EV sales climbed 127% in 2024 to 3,200 units, aided by reduced import tariffs and a charging-station program led by YPF Luz. Although penetration is still below 1%, ride-hailing fleets and last-mile delivery firms in Buenos Aires run pilot programs that showcase lower operating costs than comparable diesel vans. Each full battery electric vehicle eliminates routine oil changes, trimming addressable volume for the Argentine lubricants market in high-mileage urban duty cycles. Component suppliers counter by promoting thermal-management fluids and specialty greases for e-motors, but these niches only partly offset the loss of engine oil barrels in the medium term.

Segment Analysis

By Product Type: Engine Oils Retain Scale as Hydraulic Fluids Accelerate

Automotive engine oils accounted for 48.10% of the total volume in 2024, driven by extensive service-station coverage and entrenched brand preferences. The large installed vehicle base ensures repeat purchases even when new-car sales fluctuate, supporting baseline demand within the Argentine lubricants market. Engine-oil marketers focus on API SP and ACEA C-grade formulations that withstand bio-fuel dilution, nudging average selling prices upward and cushioning currency-linked cost swings. Franchise workshops nationwide promote bundled oil-filter packages that reinforce OEM specifications and reduce leakage to unbranded vendors.

Hydraulic fluids post the fastest 4.18% CAGR through 2030 on the back of mining, construction, and unconventional oil drilling. New equipment for lithium extraction utilizes high-pressure pumps and sophisticated motion-control systems, which require zinc-free or ashless formulations to ensure longer component life under abrasive brine conditions. Suppliers provide field-side testing units to monitor viscosity and contamination, converting spot buyers into long-term contracts. As rigs and excavators in Neuquén and Jujuy rotate every 500-600 hours, rather than the traditional 250-hour cycle, fluid consumption rises proportionally, strengthening the Argentine lubricants market despite its mature status.

Note: Segment shares of all individual segments available upon report purchase

By End-User Industry: Automotive Dominance Faces Industrial Rotation

Automotive applications accounted for 56.04% of the 2024 volume, reflecting regional vehicle assembly hubs and extensive aftermarket channels. Service garages in Córdoba and Santa Fe handle multi-brand fleets, driving steady sales of 15W-40 and 5W-30 grades. However, unit growth moderates toward 2030 as electric drivetrain adoption gains traction and extended drain intervals reduce workshop visits. Consequently, suppliers diversify into shock-absorber fluids and e-transmission greases to maintain wallet share within the Argentine lubricants market.

Heavy equipment demand grows at a 3.48% CAGR, led by mining fleets that operate 24/7 in the Lithium Triangle. High-horsepower excavators, haul trucks, and crushing lines consume gear oils, greases, and engine oils that are capable of withstanding high-altitude and high-salinity environments. Construction machinery linked to Vaca Muerta pipelines further broadens industrial consumption, requiring low-temperature hydraulic systems for winter operations. Power-generation sets in drill pads and remote camps also add niche turbine-oil requirements, diversifying the Argentinian need for lubricants beyond consumer channels.

By Base Stock Type: Mineral Oils Prevail as Synthetics Gain Traction

Mineral oil-based products delivered 66.40% of total volume in 2024, buoyed by local refining capacity and widespread availability through YPF forecourts. Competitive pricing shields mineral lines from rapid share loss; however, technical ceilings prompt premium buyers to upgrade to semi-synthetic or full-synthetic options for extended drain intervals and improved cold-crank properties. Lead-acid battery recyclers also favor conventional hydraulic oils in material-handling equipment, preserving baseline demand in the Argentine lubricants market.

Synthetic oils expand at a 4.53% CAGR, propelled by biofuel compatibility needs and high-load industrial duty cycles. Fleet managers in Buenos Aires and Neuquén report longer engine life using low-SAPS 0W-20 synthetics, and OEMs now validate warranty coverage only when API SP-plus lubricants are recorded in service logs. Multinationals invest in local blending hubs to shorten lead times; FUCHS allocated BRL 220 million for a regional plant that will supply PAO-based engine oils and advanced greases[2]FUCHS Petrolub SE, “Annual Report 2024,” fuchs.com . Advances in polyalkylene-glycol chemistry also open avenues for high-efficiency worm-gear applications in renewable energy equipment, adding incremental volume to the Argentine lubricants market size forecast.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Buenos Aires, Córdoba, and Santa Fe jointly consumed the majority of lubricant volumes in 2024, thanks to concentrated vehicle ownership, assembly plants, and port-linked logistics networks. Service stations around Buenos Aires’ metropolitan ring road handle dense commuter traffic and last-mile delivery fleets that demand quick-lube services every 5,000–7,000 km. Retail shelf space favors 4-liter packs of 10W-40 synthetic oils, reflecting a shift in consumer preferences toward higher-specification products among middle-income consumers. Industrial clusters in Rosario and the Paraná corridor also draw gear and hydraulic oils for grain-handling machinery, ensuring steady seasonal peaks that align with harvest periods.

Neuquén Province is emerging as the fastest-growing pocket within the Argentine lubricants market, posting annual gains since 2024, as rig counts, pipeline projects, and midstream facilities proliferate. Distributors set up depots near Añelo to reduce transit times and maintain inventory for 48-hour call-outs. Local authorities run supplier development programs that certify small blenders able to meet API CK-4 standards, injecting competition into what was once a branded-majors stronghold. Cross-provincial supply chains also benefit trucking firms that backhaul lubricants toward Buenos Aires, employing consolidated freight rates that lower delivered costs.

Salta, Jujuy, and Catamarca are registering accelerating lubricant uptake due to lithium brine expansions and World Bank-funded road improvements. High-altitude conditions mandate lubricants with pour points below -40 °C and strong rust-preventive additives to counter saline spray. Mining contractors utilize on-site micro-labs that extend oil life through filtration and spectrographic analysis, reducing waste disposal while maintaining throughput. Equipment OEMs conduct joint workshops with lubricant suppliers to train operators on contamination control, thereby reinforcing the stickiness of their products. Although absolute volumes remain smaller than those of populous Pampas provinces, double-digit growth supports a vibrant secondary distribution network in northern Argentina.

Competitive Landscape

The Argentine lubricants market is moderately consolidated. International brands compete on product performance. Regional firms carve out a niche in the agricultural and small-industrial sectors by offering flexible pack sizes and localized after-sales support. Technical service emerges as the main differentiator rather than label loyalty. Quaker Houghton transitioned from a distributor model to a wholly owned Argentine subsidiary, which provides on-site metalworking-fluid management for auto-parts machining lines. Mergers and acquisitions chatter intensifies as global majors recalibrate portfolios. BP placed its Castrol business under strategic review in mid-2025, signaling potential divestments that could reshape the brand's positioning across Latin America. Local independents watch for carve-out opportunities to license established trademarks and broaden product breadth. In parallel, suppliers are exploring bio-lubricant options for agricultural machinery to align with the Ministry of the Environment’s cleaner production guidelines, although cost remains a barrier to mass adoption within the Argentine lubricants market.

Argentina Lubricants Industry Leaders

-

YPF

-

Shell plc

-

ExxonMobil Corporation

-

BP plc (Castrol)

-

TotalEnergies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP plc (Castrol) initiated the sale of its Castrol lubricants division, valued at up to USD 10 billion, as part of a broader USD 20 billion divestment plan by 2027.

- October 2024: Texaco and Mobil 1 formally returned to Argentina, each naming new official importers to re-enter the premium segment after prior exits linked to import restrictions.

Argentina Lubricants Market Report Scope

Lubricants are fluids designed to minimize friction between surfaces, thereby preventing wear and tear. Tailored for specific end users, these lubricants are crafted using distinct additives and base oils. Typically, base oils constitute 75% to 90% of a lubricant's formulation, endowing the final product with essential lubricating properties.

The Argentina lubricants market is segmented by product type and end-user industry. By product type, the market is segmented into engine oil, transmission and gear oils, hydraulic fluids, metalworking fluids, grease, and other product types. By end-user industry, the market is segmented into passenger vehicles, motorcycles, commercial vehicles, and industrial (mining, marine, oil and gas, agriculture, and other industrial applications). For each segment, the market sizing and forecasts have been done on the basis of volume (million liters).

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

What is the current volume of lubricants consumed in Argentina?

The Argentine lubricants market size reached 321.79 million liters in 2025.

How fast will lubricant demand grow in Argentina through 2030?

Consumption is projected to rise to 329.06 million liters by 2030, reflecting a 2.26% CAGR.

Which product category is expanding the quickest?

Hydraulic fluids are projected to post the fastest growth with a 4.18% CAGR through 2030, fueled by mining and Vaca Muerta construction activity.

Why are synthetic lubricants gaining share?

Mandatory 12% bio-fuel blends under Law 27.640 require formulations with higher oxidation stability, encouraging a shift to synthetics.

Which province shows the highest lubricant demand growth?

Neuquén leads in growth due to the development of Vaca Muerta shale and related infrastructure projects.

How are macroeconomic factors affecting lubricant prices?

Peso depreciation and high inflation raise imported base-oil costs, forcing blenders to adjust prices frequently and compress margins.

Page last updated on: