Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

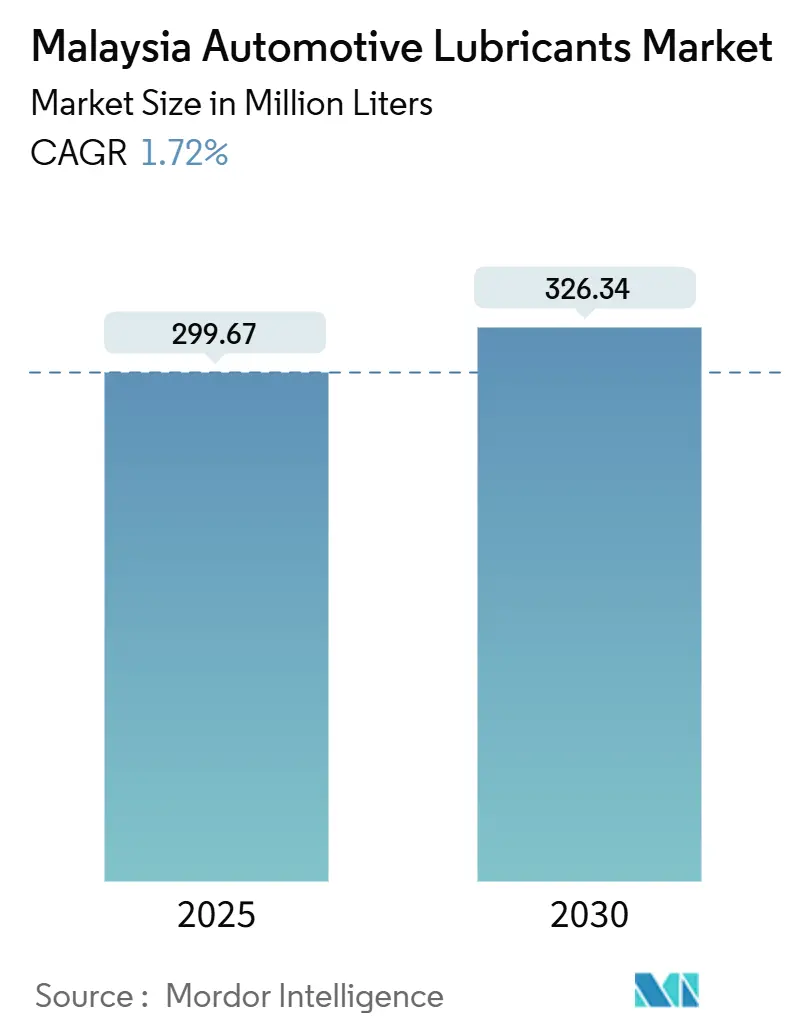

| Market Volume (2025) | 299.67 Million liters |

| Market Volume (2030) | 326.34 Million liters |

| Growth Rate (2025 - 2030) | 1.72% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malaysia Automotive Lubricants Market Analysis by Mordor Intelligence

The Malaysia Automotive Lubricants Market size is estimated at 299.67 million liters in 2025, and is expected to reach 326.34 million liters by 2030, at a CAGR of 1.72% during the forecast period (2025-2030). The sector is transitioning from pure volume growth toward premium, higher-value products as stricter certification, domestic base-oil investments, and fuel-subsidy reforms reshape buyer preferences. Engine oil replacements continue to drive demand as the vehicle parc expands, while automatic transmissions and low-viscosity synthetics gain momentum as modern drivetrains become more prevalent. Commercial fleets increase lubricant consumption as Malaysia’s logistics expansion boosts average mileage, while organized quick-lube chains elevate product quality expectations. Competitive intensity remains moderate, as leading multinationals and PETRONAS leverage their compliance capabilities, distribution reach, and domestic Group III supply to defend their share, even as smaller blenders face certification headwinds.

Key Report Takeaways

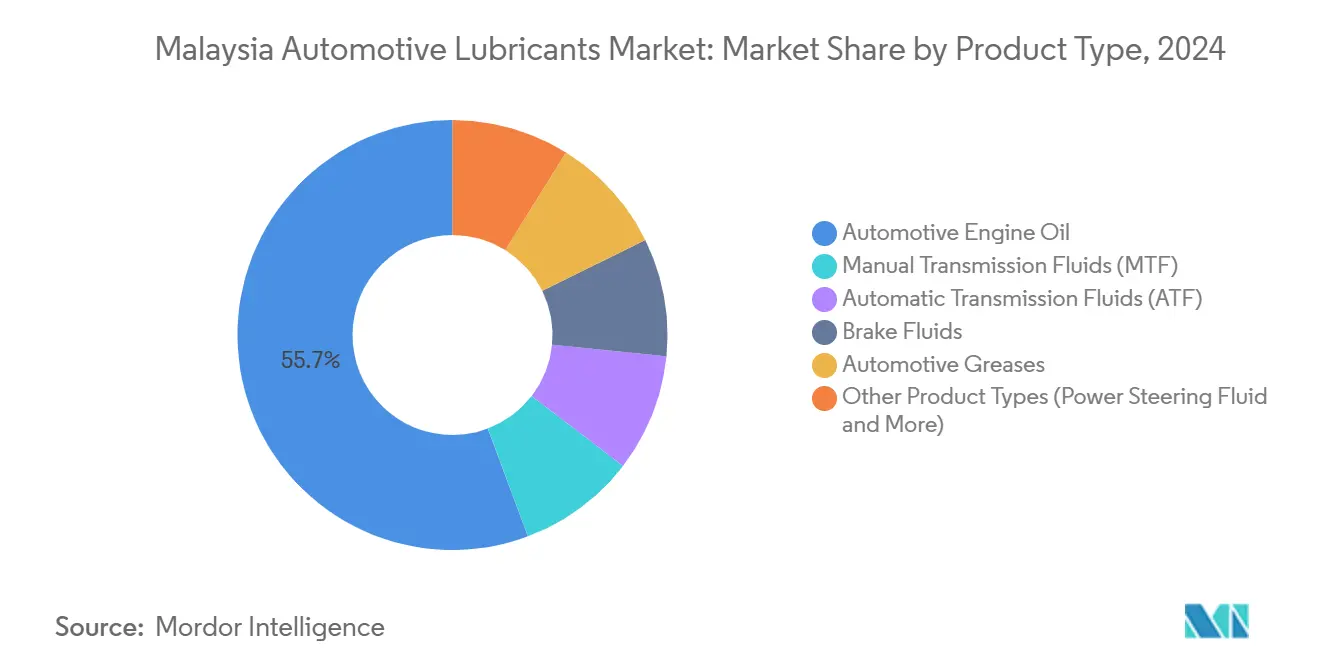

- By product type, automotive engine oils led with 55.72% of Malaysia automotive lubricants market share in 2024. Automatic transmission fluids (ATF) are forecast to expand at a 1.89% CAGR to 2030.

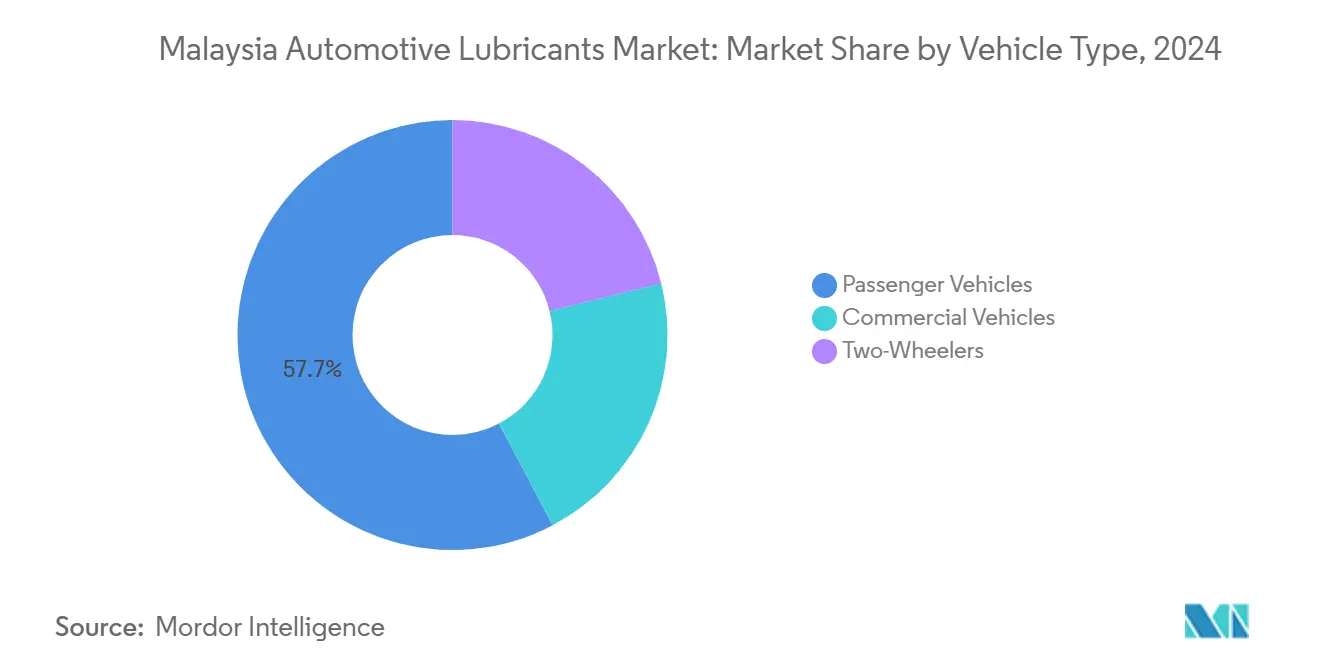

- By vehicle type, passenger vehicles captured 57.71% of Malaysia automotive lubricants market share in 2024. Commercial vehicles are projected to post the fastest 1.95% CAGR through 2030.

Malaysia Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle-parc growth and high motorisation | +0.3% | National, concentrated in Klang Valley and Johor | Medium term (2-4 years) |

| Acceleration of quick-lube chains and OEM service centres | +0.2% | Urban centers, expanding to secondary cities | Short term (≤ 2 years) |

| Shift to low-viscosity synthetics post-diesel subsidy reform | +0.3% | National, fleet-heavy regions leading adoption | Medium term (2-4 years) |

| Mandatory Engine-Oil Certification Order curbing counterfeits | +0.3% | National enforcement, rural areas most impacted | Short term (≤ 2 years) |

| Palm-oil bio-lubricant R&D bolstering domestic feedstock | +0.2% | Peninsular Malaysia, plantation regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising vehicle-parc growth and high motorization

Vehicle registrations reached 202,245 units between January and March 2024, up 5% year-over-year, reinforcing a robust link between parc size and lubricant consumption. Newer cars enter the maintenance cycle requiring premium synthetic oils, while aging vehicles increase replacement demand. Secondary urban centers, such as Johor Bahru and Penang, witness an increasing density, opening up white space for organized service formats that push certified products. Domestic assembly volumes—210,431 units in the same period—further support OEM factory-fill as well as aftermarket sales. As average vehicle age rises, adherence to scheduled maintenance becomes more critical, driving sustained lubricant turnover.

Acceleration of quick-lube chains and OEM service centers

PETRONAS AutoExpert has announced 100 outlets nationwide, using standardized servicing to assure lubricant quality and strengthen brand loyalty[1]PETRONAS, “AutoExpert Franchise Expansion,” petronas.com. Partnerships with digital retailers enable rapid market roll-out and access to established customer pools. OEM initiatives such as Sime Darby Motors’ Drivecare highlight automakers’ intent to own the maintenance journey and capture high-margin fluid sales. Chain formats utilize centralized procurement and technician training to outperform independent workshops in terms of price-to-service value. The trend supports premiumization because warranty compliance favors exact-spec lubricants over generic mineral grades.

Shift to low-viscosity synthetics after diesel subsidy reform

The removal of diesel subsidies in June 2024 increased pump prices by 56%, forcing fleet operators to optimize their total costs. Demand for 0W-20 and 5W-30 synthetics that deliver fuel-economy gains rose sharply, aided by PETRONAS Syntium X in July 2024. Domestic ETRO+ Group III output allows local blenders to supply these grades competitively, replacing imports. Extended drain intervals reduce the frequency of yearly oil changes but increase the value per liter, shifting the revenue mix toward higher-margin SKUs. New API SP and ILSAC GF-6 specifications reinforce the move because mineral oils cannot meet performance thresholds cost-effectively.

Mandatory engine-oil certification order curbing counterfeits

The Trade Descriptions Order, enforced from October 2025, requires SIRIM QAS certification and tamper-evident marking on every engine oil pack. Fines reach MYR 200,000 per corporate offence, prompting distributors to audit inventories. Since 2019, authorities have confiscated MYR 1.1 million in counterfeit stock, most recently through a 13-suspect sting in April 2025. Compliance costs favor large brands that possess testing laboratories and traceable supply chains. Consumer education by FOMCA encourages retail buyers to opt for certified labels, thereby consolidating market volumes through the formal channel.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising HEV/BEV penetration compressing engine-oil volumes | -0.3% | Urban centers, government fleet adoption leading | Long term (≥ 4 years) |

| Cost-driven drain-interval stretching after fuel-subsidy cuts | -0.2% | National, commercial fleets most affected | Medium term (2-4 years) |

| Grey-/illicit oils undercutting branded players | -0.1% | Rural areas, independent workshop channels | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising HEV/BEV penetration compressing engine-oil volumes

Electric and hybrid vehicles accounted for roughly 2–3% of 2024 sales, but policy targets of 15% by 2030 will reduce internal-combustion lubricant demand. Federal allocations totaling MYR 2.4 billion back charging corridors and local assembly incentives. Suppliers respond by introducing EV thermal-management fluids, as seen in UMW Grantt’s brake fluid and coolant line released in July 2024. Although these new products carry a higher unit value, they cannot fully offset the displacement of high-volume engine oil. Fleet electrification, especially in last-mile logistics, adds downward pressure because high mileage amplifies the lost demand.

Cost-driven drain-interval stretching after fuel-subsidy cuts

Commercial operators faced an immediate surge in operating costs once diesel prices rose to MYR 3.35 per liter in June 2024. Many adopted synthetic oils that allow extended intervals, stretching kilometers per change by 30–40%. In contrast, synthetics raise revenue per liter, overall liters per vehicle decline, softening volume growth. Lubricant makers contend with elevated additive and packaging costs simultaneously, squeezing their margins. To offset this, they bundle analysis services that predict optimal change intervals, retaining value through data rather than the number of liters sold.

Segment Analysis

By Product Type: Engine-oil scale faces a premium shift

Engine oil retained a 55.72% share of the Malaysian automotive lubricants market in 2024, as internal-combustion engines still dominate the national vehicle parc. Certification rules effective in 2025 raise barriers for parallel imports, helping established suppliers defend volumes. Nevertheless, growth tapers as the category matures, prompting producers to shift toward value-added synthetics. Automatic-transmission fluids, in contrast, are expected to expand at a 1.89% CAGR as multi-speed gearboxes become more prevalent across both passenger sedans and pickups. Local Group II refines from Pentas Flora, trimming costs and closing the feedstock loop, enabling competitively priced premium ATF formulations.

Domestic blenders utilize Formula 1 transfer technology to produce shear-stable synthetics, suitable for stop-and-go urban duty cycles. Manual-transmission and brake fluids hold steady replacement demand but lack volume lift because manual transmissions are in secular decline. Specialty segments—power steering fluids, greases, and hydraulic oils—grow from a smaller base, driven by vehicle electrification that requires dedicated coolant and dielectric fluids. Over the forecast period, premiumization lifts average selling price faster than liters, so product-mix upgrades become the principal driver of revenue.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: Commercial fleets set the growth tone

Passenger cars consumed 57.71% of lubricant volumes in 2024, driven by the dominance of private ownership; however, their expansion is slowing as urban congestion and mobility-as-a-service alternatives gain traction. Turbocharged downsized engines require low-SAPs synthetics compliant with API SP, reinforcing the push toward premium formulations. Commercial vehicles provide the strongest uplift, with volumes advancing at a 1.95% CAGR, thanks to intensified e-commerce logistics and the pan-Borneo highway freight. Fleet managers emphasize total-cost-of-ownership, adopting synthetic 10W-40 in heavy-duty diesel engines to extend drain intervals from 20,000 km to 40,000 km, which supports the Malaysian automotive lubricants market share for synthetics in this segment.

Light-duty vans and pickup trucks bridge the gap between private and freight needs, drawing blended product demand that mirrors passenger-car specs yet faces rougher duty cycles. Motorcycle lubricants remain a resilient niche, tied to the growth of food delivery and rural mobility. PETRONAS offers tropical-climate 4T oils engineered for high ambient temperature and humidity, defending share against Japanese OEM brands. Looking ahead, commercial-fleet transformation outweighs the drag from electrification in passenger cars, sustaining aggregate market growth.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Peninsular Malaysia accounts for the bulk of consumption due to dense vehicle ownership, industrial clustering, and highway connectivity, which underpin fast service intervals. The Klang Valley tops regional demand, housing major assembly plants and accounting for around one-third of registered vehicles. Johor ranks second; its cross-border freight with Singapore, along with a new Mercedes-Benz logistics center announced in November 2024, elevates lubricant pull-through[2]Mercedes-Benz Group AG, “Johor Logistics Centre Investment,” mercedes-benz.com. Northern states Penang and Kedah add stable volumes through component production and heavily trafficked expressways.

East Malaysia (Sabah and Sarawak) lags in absolute liters but records above-average growth as infrastructure spending opens new transport corridors. PETRONAS targets 20% sales growth there by widening distributor coverage and offering packaged synthetics suited to long haulages where service points are sparse. Resource industries such as palm-oil plantations and offshore gas employ heavy equipment that consumes large-capacity diesel engine oils and hydraulic fluids, complementing on-road demand.

Rural districts wrestle with counterfeit imports, prompting regulators to intensify roadside checks and retailer audits under the Trade Descriptions Order. Certified supply chains are extending beyond cities via quick-lube franchising, which promises consistent pricing and warranty-compliant service. Organized chains also pilot mobile units that service agricultural machinery, unlocking fresh revenue pockets. Over the forecast horizon, regional parity narrows as infrastructure upgrades and stricter enforcement drive organized-channel penetration in under-served markets.

Competitive Landscape

The Malaysia automotive lubricants exhibit moderate concentration. Margin pressure from additive inflation and shipping bottlenecks triggers diversification into services. PETRONAS offers fluid analytics platforms that predict drain intervals, adding subscription revenue. Shell partners with fleet-telemetry providers, integrating lubricant condition into vehicle-health dashboards. Sustainability also differentiates Pentas Flora’s rerefined Group II base oil, which appeals to ESG-focused fleets, while its palm-ester R&D positions Malaysia as a source of renewable feedstock.

Malaysia Automotive Lubricants Industry Leaders

-

BP p.l.c.

-

Chevron Corporation

-

Exxon Mobil Corporation

-

Shell plc

-

PETRONAS Lubricants International

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Petron Malaysia has received the SIRIM Genuine Product License under the 2024 Certification and Marking of Engine Oils (for Motor Vehicles) Order. This license authorizes the company to obtain SIRIM Genuine Product Labels for its engine oils in the Malaysian market.

- March 2025: Hextar Oiltech Sdn Bhd, a subsidiary 60% owned by Hextar Global Berhad, has been appointed as the exclusive distributor for Petromin’s premium lubricant in Malaysia. This strategic partnership is expected to strengthen the availability of high-quality lubricants in the Malaysian market, potentially driving growth and enhancing competition within the industry.

Malaysia Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is Malaysia’s automotive lubricants demand in 2025 and where is it headed by 2030?

Volume reached 299.67 million liters in 2025 and is projected to rise to 326.34 million liters by 2030, supported by a 1.72% CAGR.

Which product category holds the biggest share of national lubricant consumption?

Engine-oil replacements account for 55.72% of 2024 volumes because the vehicle parc is still dominated by internal-combustion engines.

What segment is expanding fastest in the next five years?

Automatic-transmission fluids show the strongest five-year momentum, advancing at a 1.89% CAGR as modern drivetrains gain share.

How are diesel-subsidy reforms influencing lubricant purchasing?

The 56% diesel-price jump in June 2024 pushed commercial fleets toward low-viscosity synthetics that extend drain intervals and improve fuel economy.

What role do certification rules play in supplier strategy?

The October 2025 SIRIM QAS mandate raises entry barriers, favoring brands that can fund testing labs, secure traceability systems, and roll out tamper-evident packaging.

Page last updated on: