Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

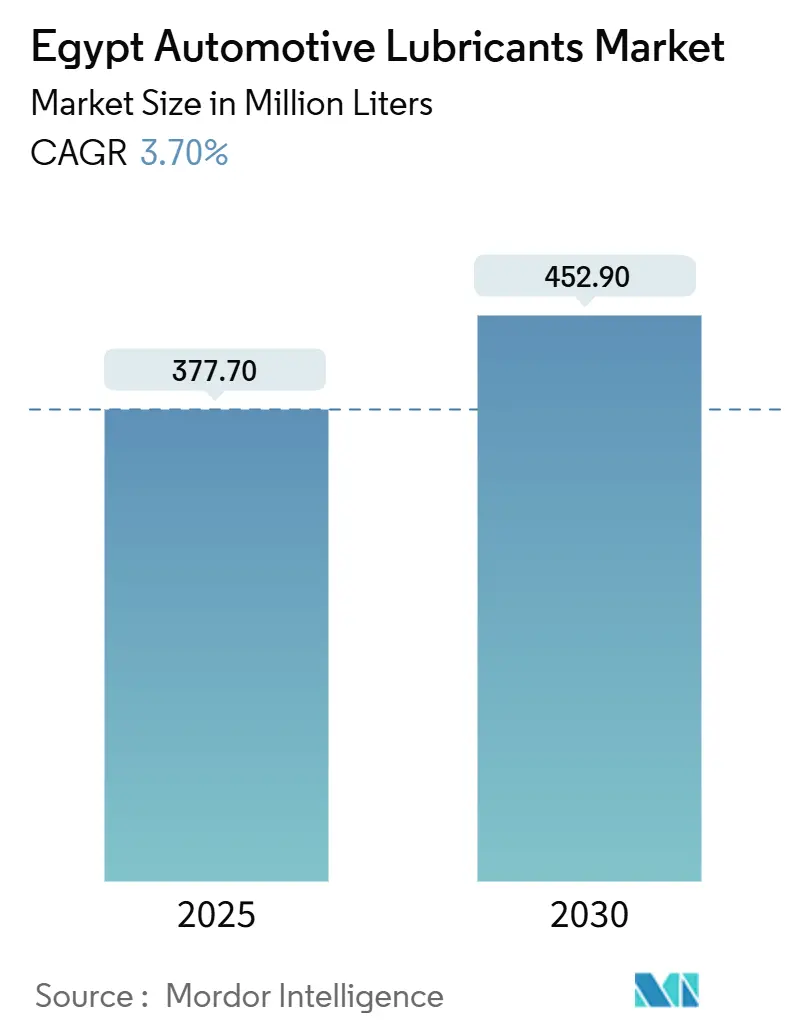

| Market Volume (2025) | 377.70 Million liters |

| Market Volume (2030) | 452.90 Million liters |

| Growth Rate (2025 - 2030) | 3.70% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Egypt Automotive Lubricants Market Analysis by Mordor Intelligence

The Egypt Automotive Lubricants Market size is estimated at 377.70 million liters in 2025, and is expected to reach 452.90 million liters by 2030, at a CAGR of 3.70% during the forecast period (2025-2030). Egypt’s expanding vehicle parc, ambitious infrastructure program, and the OEM-led shift toward higher-spec multigrade and synthetic blends are the chief volume drivers. Multinationals are investing in local blending to counter currency-driven import cost inflation and to tailor products for Egypt’s hot climate and heavy-duty operating cycles. Digital channels, both e-commerce storefronts and app-based mechanic platforms, continue to open fresh retail corridors for premium products, especially among tech-savvy urban consumers. Regulatory enforcement by the Egyptian Organization for Standardization (EOS) is lifting baseline quality and gradually squeezing counterfeit supply, a trend expected to reinforce consumer trust in branded lubricants.

Key Report Takeaways

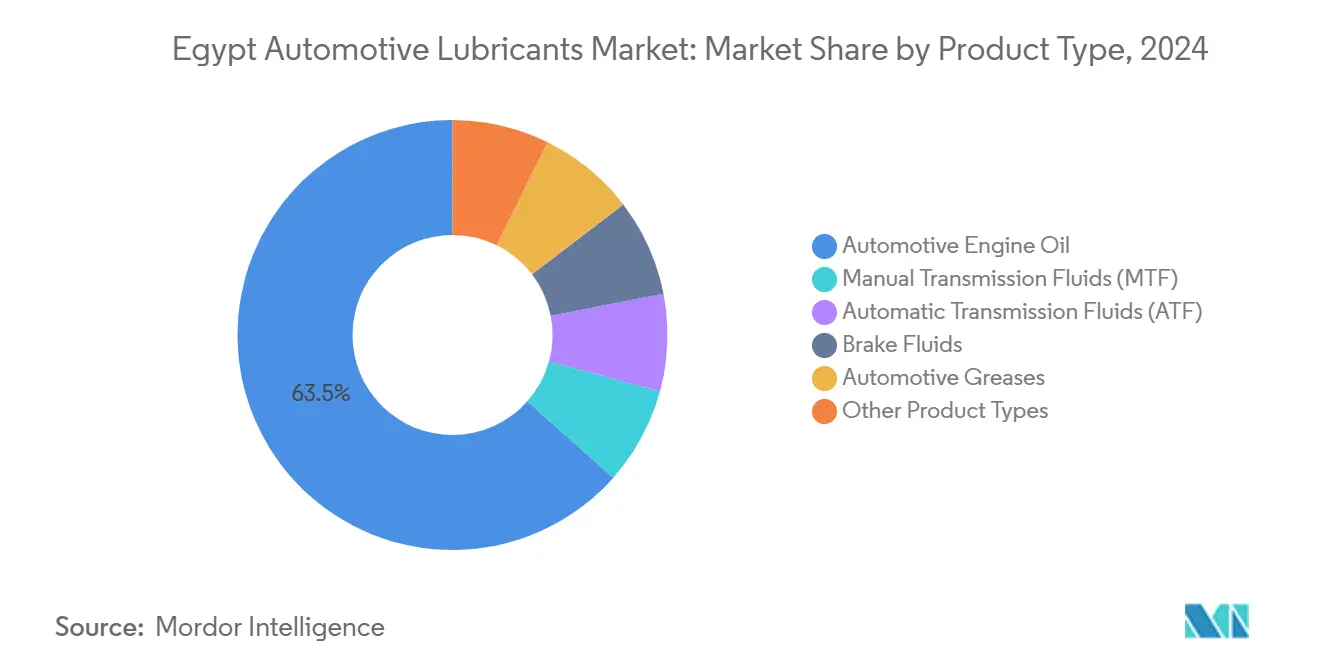

- By product type, automotive engine oils held 63.45% of the Egypt automotive lubricants market share in 2024, while automatic transmission fluids are forecast to expand at a 3.95% CAGR through 2030.

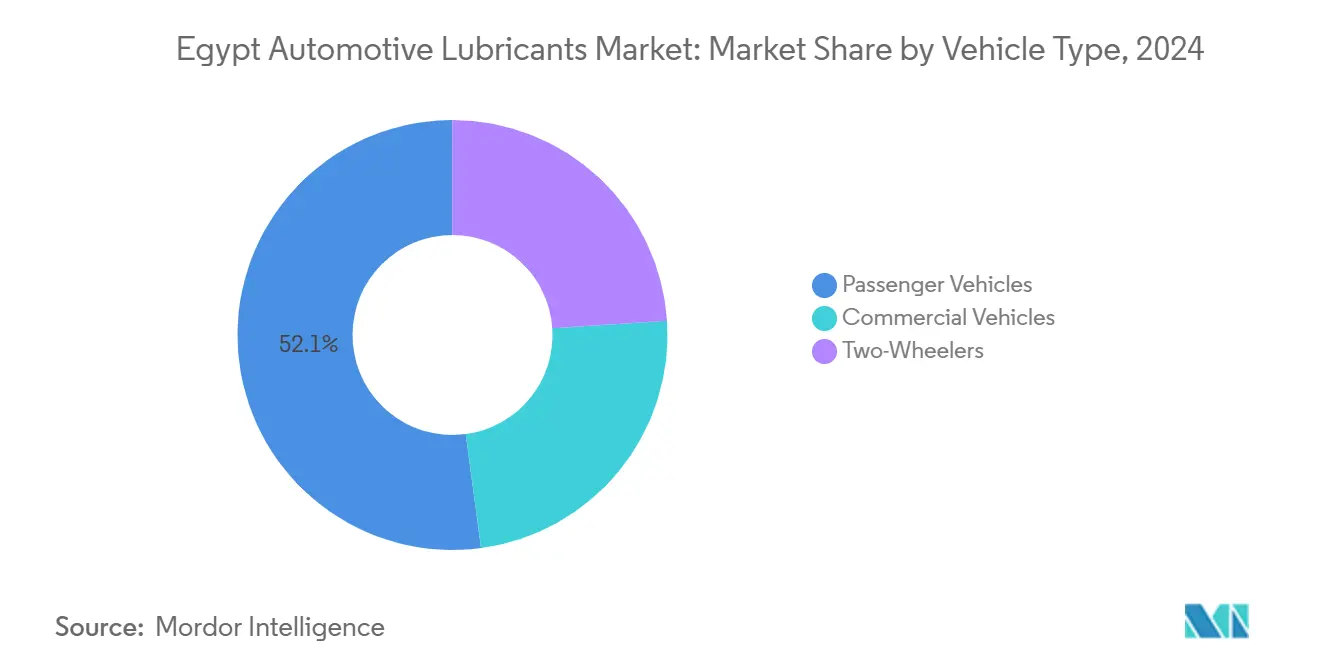

- By vehicle type, passenger cars led the Egypt automotive lubricants market with a 52.12% share in 2024; two-wheelers are projected to post the highest CAGR of 3.81% from 2025 to 2030.

Egypt Automotive Lubricants Market Trends and Insights

Drivers Impact Analysis

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising vehicle parc and ownership expansion | +1.2% | National, concentrated in Greater Cairo, Alexandria, Giza | Medium term (2-4 years) |

| Infrastructure boom driving commercial-fleet oil demand | +0.8% | National, with early gains in New Administrative Capital, Suez Canal Economic Zone | Long term (≥ 4 years) |

| OEM shift to higher-spec multigrade and synthetic oils | +0.6% | Global OEM influence, strongest in urban centers | Medium term (2-4 years) |

| Local blending capacity upgrades by multinationals | +0.5% | Concentrated in Cairo, Alexandria, Suez industrial zones | Short term (≤ 2 years) |

| E-commerce and digital mechanic platforms pushing retail volumes | +0.4% | Urban centers, expanding to secondary cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Vehicle Parc and Ownership Expansion

Egypt operated more than 5 million internal-combustion vehicles in 2024, a base that now requires regular engine oil and drivetrain fluid service intervals that average 6,000 kilometers for passenger cars. Middle-class households in Cairo and Alexandria benefit from accessible financing and locally assembled models that qualify for lower customs duties, encouraging first-time car ownership. Government incentives for assembly plants spur OEM-approved factory fills, which then lock consumers into branded aftermarket choices. Fleet renewals toward newer models with tighter tolerances further accelerate demand for low-viscosity multigrades that meet API SN Plus or ACEA C3 guidelines. Commercial truck registrations linked to megaproject construction increase heavy-duty engine oil consumption, and workshop operators increasingly recommend semi-synthetics for extended drain intervals. This convergence of private and fleet demand highlights the long-term growth trajectory of the Egyptian automotive lubricants market.

Infrastructure Boom Driving Commercial-Fleet Oil Demand

The USD 58 billion New Administrative Capital alone engages thousands of dump trucks, concrete mixers, and cranes that consume high-TBN diesel oils every 250 operating hours. The deepening of the Suez Canal port and berth extensions requires marine-grade trunk piston engine oils with enhanced detergency under high-sulfur fuel conditions. Highway upgrades that connect Upper Egypt to coastal hubs increase demand for lubricants for asphalt pavers, graders, and maintenance fleets that rely on multi-purpose hydraulic fluids. Mining and oil exploration in the Eastern Desert require extreme-pressure gear oils for rigs operating in abrasive sand environments. The national roads agency mandates equipment service records, which fuels consumption of OEM-backed lubricants from Shell, TotalEnergies, and Misr Petroleum. Infrastructure, therefore, injects sustained commercial-fleet volumes into the Egyptian automotive lubricants market.

OEM Shift to Higher-Spec Multigrade and Synthetic Oils

Local assembly lines for BMW, Mercedes-Benz, and Hyundai specify 5W-30 and 0W-20 synthetic oils that conform to ACEA C3 and API SP standards, thereby reducing fuel consumption while extending oil-change intervals to 15,000 kilometers. Transmission builders now endorse full synthetic ATFs compatible with GM DEXRON VI and Volvo 97342, exemplified by Mobil ATF Multi-Vehicle. Workshops follow OEM service bulletins, driving retail upsell from monogrades to premium multigrades. Synthetic penetration of passenger-car engine oil is expected to rise, a trend that boosts the value per liter in the Egyptian automotive lubricants market. Tribology research from the Egyptian Society of Tribology suggests that the addition of 20% solid additives can reduce wear scar diameters by 18%, encouraging domestic formulators to explore additive innovation[1]Journal of the Egyptian Society of Tribology, “Effect of Solid Additives,” ekb.eg.

Local Blending Capacity Upgrades by Multinationals

ADNOC Distribution and TotalEnergies operate a blending plant in Borg El Arab, which supplies Voyager-branded products to 240 fuel stations and independent retailers. Misr Petroleum and Al-Manar provide base-stock flexibility for API Group I and Group II formulations. Currency devaluation in 2024 and 2025 widened the cost gap between imported finished lubricants and locally blended alternatives, making Egypt a hub for exporting lubricants to North Africa. Multinationals install in-line blending control and bulk additive dosing to deliver OEM-approved batches quickly, shortening lead times to local distributors. These upgrades anchor supply security and improve margins in the Egyptian automotive lubricants market.

Restraints Impact Analysis

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency devaluation inflating imported base-oil costs | -0.9% | National, affecting all import-dependent operations | Short term (≤ 2 years) |

| Counterfeit and low-grade lubricants eroding premium share | -0.6% | National, concentrated in rural and price-sensitive segments | Medium term (2-4 years) |

| Gradual CNG/EV penetration reducing engine-oil volume | -0.3% | Urban centers, government fleets, public transportation | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Devaluation Inflating Imported Base-Oil Costs

Base-oil imports account for a major portion of Egypt’s requirements, so a decline in the pound's value increases the landed cost per barrel, thereby squeezing blender margins. Formulators respond by renegotiating long-term supply contracts and switching to Group I stocks sourced from local refineries, including the Assiut hydrocracker expansion. Some brands employ cost-down reformulations that blend Group I with synthetic base stocks yet retain OEM approvals. Others pass along cost increases, causing retail prices on 4-liter packs to rise. Persistent volatility threatens volume in low-income segments and tempers short-term growth prospects for the Egyptian automotive lubricants market.

Counterfeit and Low-Grade Lubricants Eroding Premium Share

Regulators seized counterfeit lubricant containers in 2024, indicating the presence of an illicit market. Counterfeits are sold at up to 50% discounts compared to genuine products, attracting price-sensitive consumers in rural governorates. Substandard oil can shorten engine life, but detecting it remains difficult for untrained buyers. EOS mandates conformity testing, yet spot checks cover only 15% of retail outlets each quarter, allowing counterfeit channels to regroup quickly[2]Egyptian Organization for Standardization and Quality, “EOS,” iso.org. Brand owners deploy tamper-evident seals and QR code authentication, yet awareness remains uneven. These factors dilute demand for verified premium brands, shaving 0.6 percentage points from the projected CAGR of the Egyptian automotive lubricants market.

Segment Analysis

By Product Type: Engine Oils Remain Dominant Amid ATF Acceleration

Automotive engine oils accounted for 63.45% of 2024 consumption. Multigrade formulations, such as 5W-30 and 10W-40, combine shear stability with high detergent levels, supporting drain intervals of up to 15,000 kilometers in passenger cars operating under Egypt’s dusty conditions. Synthetic penetration has increased as OEM warranties increasingly require API SN Plus or ACEA C3 oils. Group III base-oil availability from regional import hubs linked to the Suez Canal underpins this trend, and local blenders have added nitrogen blanketing and in-line viscosity control to meet tighter specifications. Semi-synthetic blends attract mass-market buyers while still meeting OEM requirements.

Automatic transmission fluids are projected to register a 3.95% CAGR through 2030, the fastest pace among products and a significant contributor to the growth of the Egyptian automotive lubricants market. OEM factories fill demand for low-viscosity, friction-modified ATF compatible with wet-clutch systems, increasing value per liter. Manual transmission fluids and gear oils continue to serve commercial fleets that prefer 80W-90 viscosities for durability under high load. Brake fluids, greases, power steering fluids, and coolants are rising steadily in line with vehicle counts and maintenance schedules. EOS mandates the use of DOT 4 brake fluid on new cars, fueling incremental demand. Across product types, counterfeit penetration is highest in monograde engine oils and lowest in ATF, due to the more complex packaging and product-level strategies required within the Egyptian automotive lubricants market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Vehicle Type: Passenger Vehicles Lead, Two-Wheelers Accelerate

Passenger cars accounted for 52.12% of the 2024 volume in the Egyptian automotive lubricants market. Urban middle-income consumers favor branded engine oils endorsed by OEM manuals, reinforcing multinationals’ premium positioning. Service frequency averages twice a year because desert dust and stop-and-go traffic can quickly cause oil oxidation. Workshops are increasingly installing sticker reminders and SMS alerts to support lubricant pull-through. Consumer preference for extended-warranty packages sold by dealerships drives the adoption of synthetic blends, further increasing the value per service.

Logistics, construction, and intercity transport corridors primarily drive commercial vehicle demand. Fleet managers weigh lubricant choice against total cost of ownership and downtime risk, often opting for high-base-number diesel oils with 25,000-kilometer drain intervals. Bulk supply contracts linked to fuel-station networks allow tiered pricing based on monthly volume, stabilizing revenue streams for suppliers in the Egyptian automotive lubricants market.

Two-wheelers are projected to grow at a 3.81% CAGR through 2030. Food delivery and ride-hailing apps like Mrsool and Talabat add thousands of motorcycles monthly, which operate in hot-idle cycles that rapidly degrade their oil. Two-stroke demand declines as four-stroke models dominate sales, aligning with OEM calls for JASO MA2-certified 10W-40 oils that protect wet clutches. Assemblers such as Benelli Egypt require factory-fill lubricants, forging direct supplier agreements that widen market access. Together, the vehicle-mix dynamics help maintain balanced volume growth and reinforce the resilience of the Egyptian automotive lubricants market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Nile Delta and Valley account for a major share of the lubricant volume, thanks to their dense population, industrial clusters, and the highest vehicle ownership rates. Alexandria’s port and logistics operations support commercial-vehicle lube demand, while tourism traffic to the North Coast bolsters seasonal sales of passenger-car oils. Suez Canal Economic Zone attracts tanker fleets and container traffic that rely on marine and heavy-duty engine oils, adding incremental barrel volumes and enhancing geographic diversity inside the Egyptian automotive lubricants market.

Upper Egypt, stretching from Assiut to Aswan, is outpacing the national average thanks to mining and agricultural mechanization projects that operate fleets of excavators, harvesters, and irrigation pumps. The Assiut hydrocracker expansion improved local base-oil access, reducing freight cost to blenders serving nearby governorates. Workshop density remains low, so oil change intervals often exceed OEM recommendations, creating an opportunity for awareness programs led by suppliers. New urban communities such as the New Administrative Capital and New Alamein consume high volumes of construction equipment lubricants during build-out phases, then transition to passenger-car and commercial-fleet service demand post completion.

Sinai Peninsula and Red Sea coastal towns experience niche but strategic demand, primarily from tourism buses, fishing fleets, and heavy equipment servicing mineral extraction projects. Suppliers route deliveries through the Suez corridor, leveraging bonded warehouses for duty-free marine lubricants. Retail footprint is thinner, so e-commerce channels bridge gaps by delivering engine-oil packs to end consumers in Sharm El-Sheikh and Hurghada within 48 hours. This digital penetration illustrates the omnichannel evolution of the Egypt automotive lubricants market.

Competitive Landscape

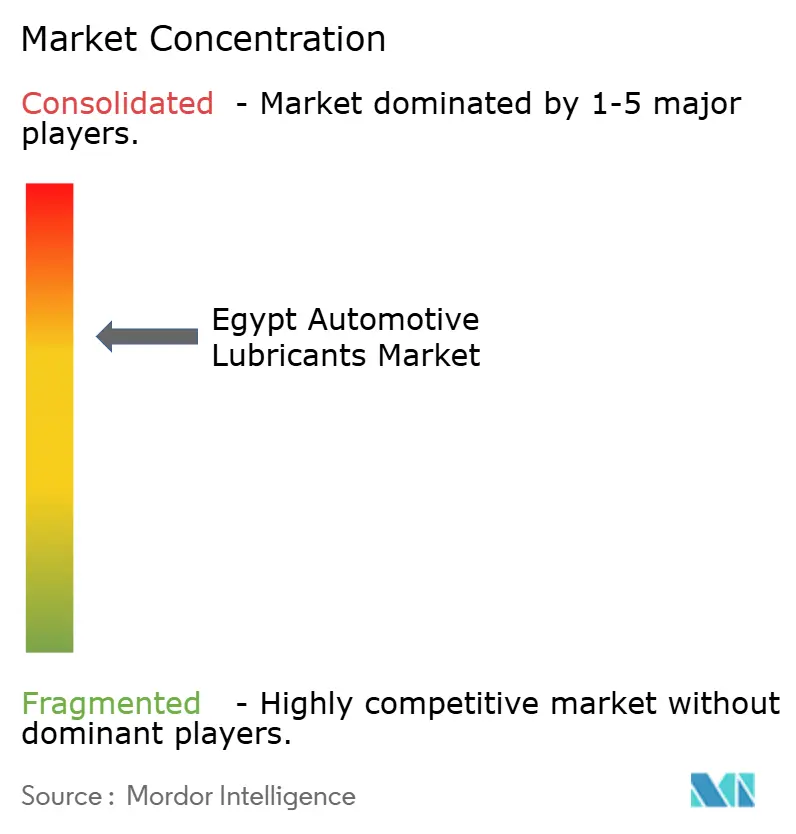

Egypt Automotive Lubricants is moderately consolidated. Shell, TotalEnergies, ExxonMobil, and BP collectively held a major share of premium-segment volume in 2024, supported by their fuel-station networks, OEM endorsements, and technical service teams. Local champions offer competitive pricing and secure government contracts, serving both rural and industrial customers through their filling stations. They tap into the domestic base-oil supply, which partly insulates them from foreign currency swings and enables them to make aggressive tenders for public-sector fleets. Regional entrants seek footholds through partnerships with independent retailers. White-space opportunities exist in EV fluids, biodegradable hydraulic oils, and factory-fill agreements for new assembly plants, with early pilots underway. Competitive strategy now extends into digital territory. ExxonMobil collaborates with fintech firm Octane to integrate Mobil lubricant purchase rewards into a fleet-management wallet. TotalEnergies promotes QR-code authentication to fight counterfeits, while Shell pilots on-site lubricant condition monitoring via IoT sensors in haul-truck fleets. Vendors also sponsor mechanic training through EOS-approved curricula, cementing mindshare at the point of service. These initiatives collectively elevate switching costs and consolidate loyalty within the Egyptian automotive lubricants market.

Egypt Automotive Lubricants Industry Leaders

-

Exxon Mobil Corporation

-

Shell plc

-

TotalEnergies

-

BP plc

-

Misr Petroleum

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: ExxonMobil Egypt partnered with fintech firm Octane to digitize vehicle services, integrating Mobil lubricants with a fleet-management digital wallet.

- June 2025: ADNOC Distribution and TotalEnergies Marketing Egypt launched Voyager lubricants with local production at Borg El Arab, marking ADNOC’s entry into third-party retail sites

Egypt Automotive Lubricants Market Report Scope

By Product Type

| Automotive Engine Oil | 0W-XX |

| 5W-XX | |

| 10W-XX | |

| 15W-XX | |

| Monogrades | |

| Other Grades | |

| Manual Transmission Fluids (MTF) | |

| Automatic Transmission Fluids (ATF) | |

| Brake Fluids | |

| Automotive Greases | |

| Other Product Types (Power Steering Fluid etc.) |

By Vehicle Type

| Passenger Vehicles |

| Commercial Vehicles |

| Two-Wheelers |

| By Product Type | Automotive Engine Oil | 0W-XX |

| 5W-XX | ||

| 10W-XX | ||

| 15W-XX | ||

| Monogrades | ||

| Other Grades | ||

| Manual Transmission Fluids (MTF) | ||

| Automatic Transmission Fluids (ATF) | ||

| Brake Fluids | ||

| Automotive Greases | ||

| Other Product Types (Power Steering Fluid etc.) | ||

| By Vehicle Type | Passenger Vehicles | |

| Commercial Vehicles | ||

| Two-Wheelers |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current volume of Egypt’s automotive lubricants consumption?

The Egypt automotive lubricants market size stands at 377.70 million litres in 2025.

How fast is demand expected to grow over the next five years?

Volume is forecast to reach 452.90 million litres by 2030, reflecting a 3.70% CAGR.

Which product category dominates sales?

Engine oils account for 63.45% of 2024 volume, far ahead of other lubricant types.

Which vehicle class contributes the most lubricant demand?

Passenger cars held 52.12% of 2024 consumption and remain the largest contributor.

What major factor could restrain near-term growth?

Ongoing currency devaluation inflates imported base-oil costs, pressuring margins and prices.

Page last updated on: