Zirconia Based Dental Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

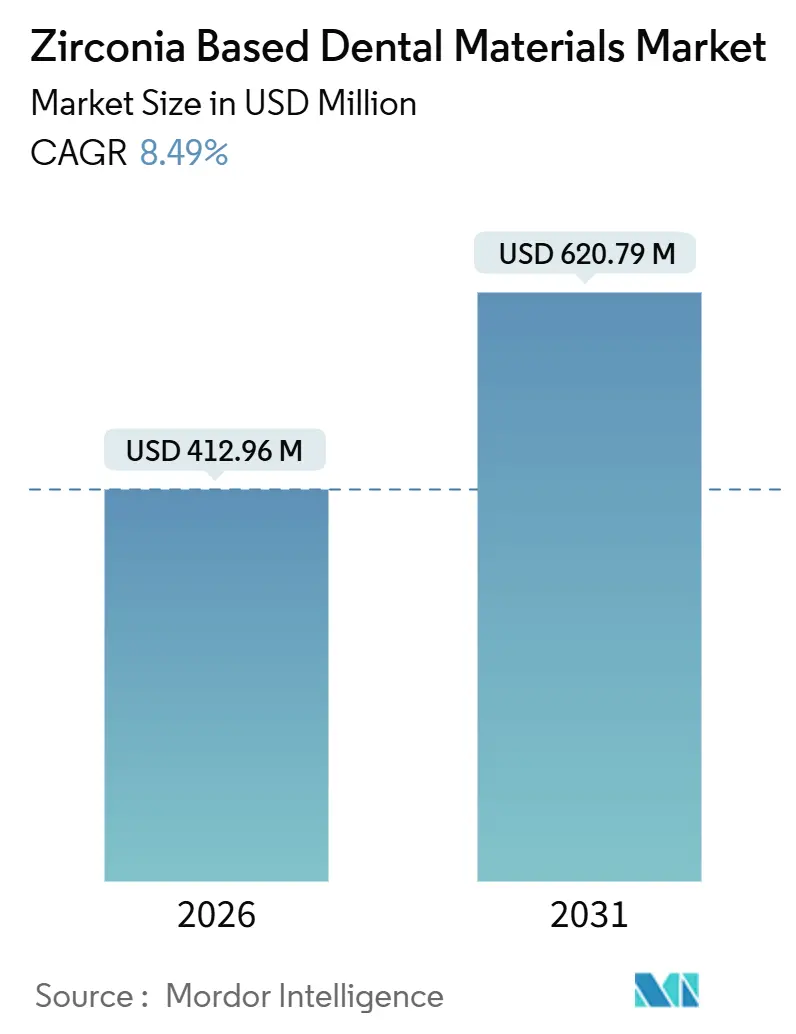

| Market Size (2026) | USD 412.96 Million |

| Market Size (2031) | USD 620.79 Million |

| Growth Rate (2026 - 2031) | 8.49% CAGR |

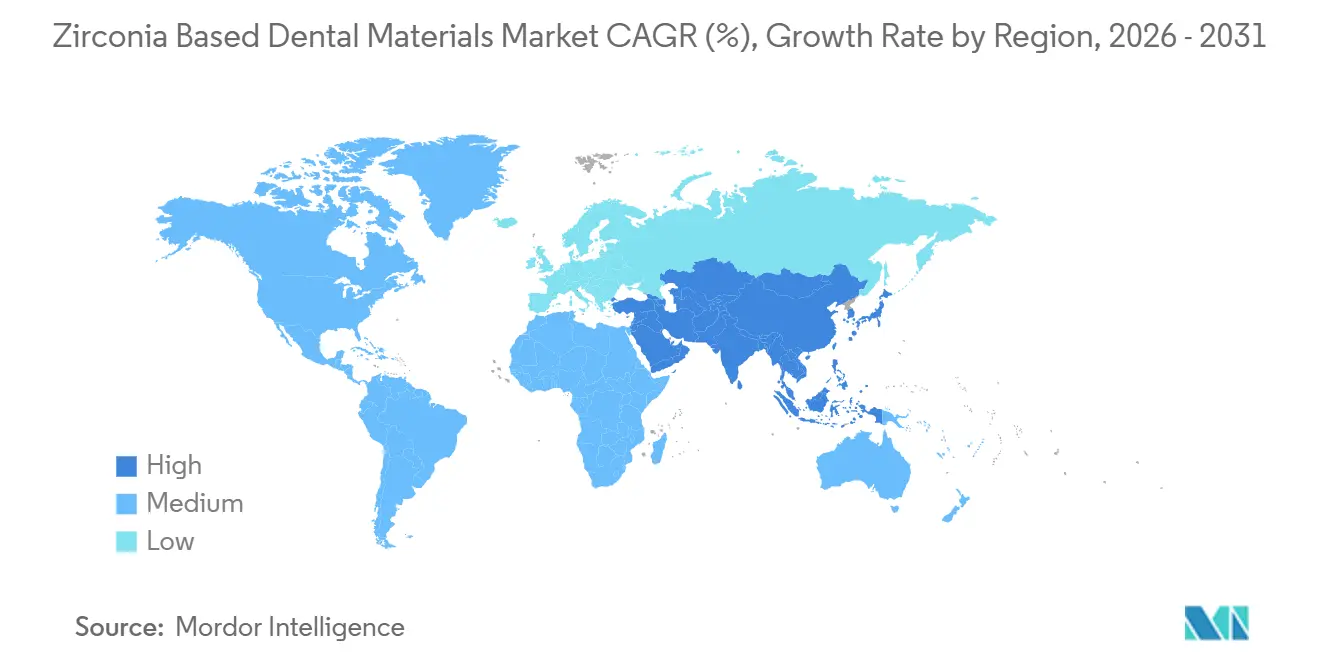

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

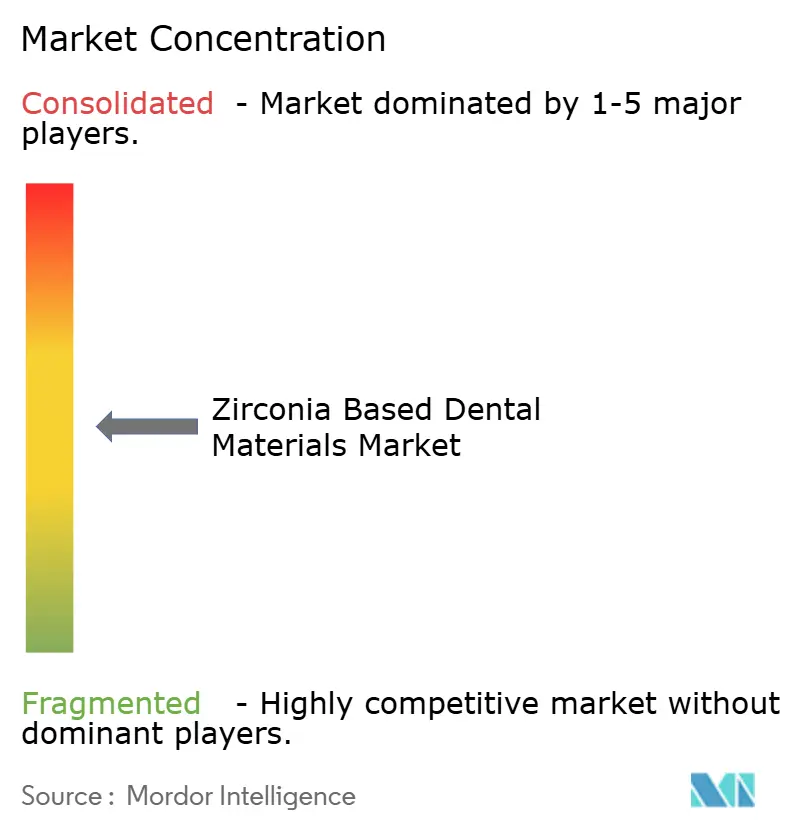

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zirconia Based Dental Materials Market Analysis by Mordor Intelligence

The Zirconia Based Dental Materials Market size is estimated at USD 412.96 million in 2026, and is expected to reach USD 620.79 million by 2031, at a CAGR of 8.49% during the forecast period (2026-2031).

Current growth rests on steady laboratory demand for pre-shaded discs, rising clinic adoption of chairside workflows, and a shift toward multi-layered blanks that balance strength with translucency. Competitive pricing from vertically integrated Chinese suppliers is widening access, while established European and Japanese brands protect premium niches through R&D in gradient and nano-structured ceramics. Growing penetration of 3D-printed powders, reimbursement expansion for all-ceramic crowns, and rapid furnace cycles that enable same-day dentistry collectively reinforce an upbeat five-year outlook for the zirconia based dental materials market

Key Report Takeaways

- By product type, zirconia dental discs led with 59.46% revenue share in 2025; zirconia powders for 3D printing are projected to expand at a 12.53% CAGR through 2031.

- By application, dental crowns accounted for 44.13% share of the zirconia based dental materials market size in 2025 and implant abutments are advancing at an 11.43% CAGR through 2031.

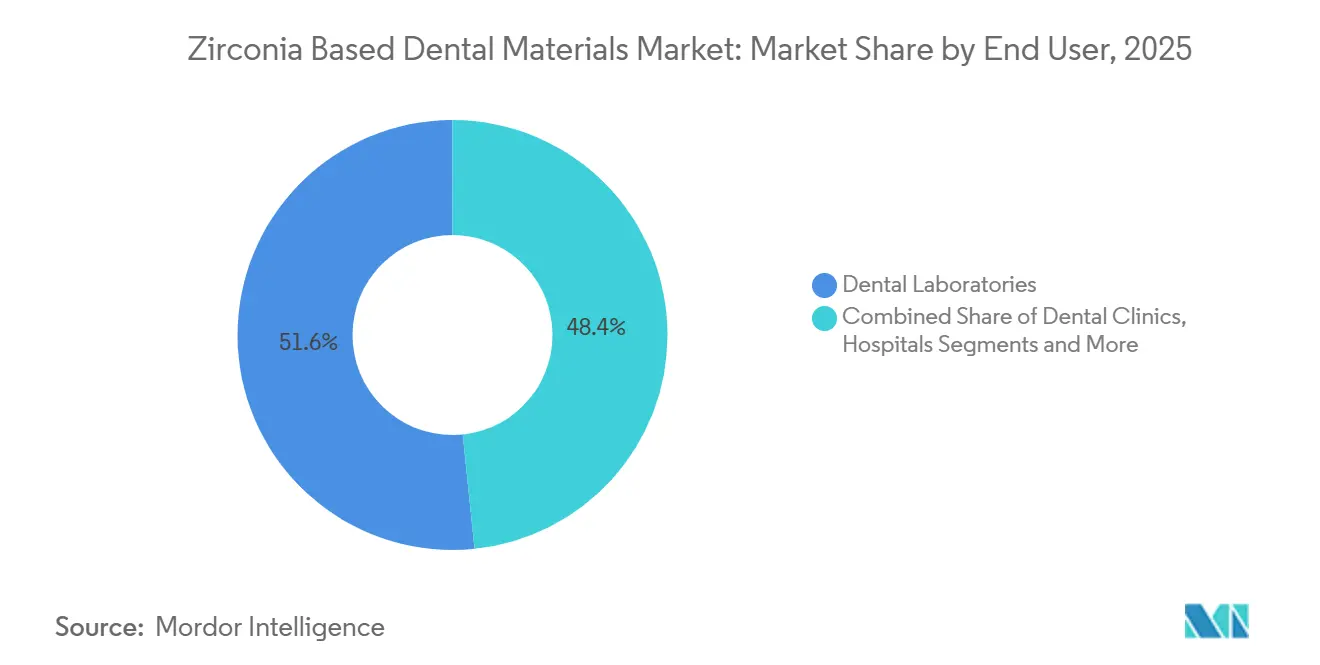

- By end user, dental laboratories held 51.64% of the zirconia based dental materials market share in 2025, while dental clinics record the highest projected CAGR at 10.68% through 2031.

- By material grade, high-strength 3Y-TZP commanded 43.22% share in 2025 and multi-layered gradient formulations are forecast to post a 12.54% CAGR through 2031.

- By geography, North America generated 37.72% revenue in 2025; Asia-Pacific is poised to grow at a 10.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Zirconia Based Dental Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-Dentistry (CAD/CAM) Adoption Accelerates Zirconia Demand | 2.3% | Global, with early penetration in North America, Western Europe; rapid catch-up in China, South Korea | Medium term (2-4 years) |

| Rising Preference for Aesthetic, Metal-Free Restorations | 1.7% | Global, strongest in urban centers of North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Global Ageing Population & Caries Prevalence Increase Restorative Volumes | 1.9% | Global, with pronounced impact in Japan, Germany, United States | Long term (≥ 4 years) |

| Speed-Sintering Furnaces Enabling Chair-Side Same-Day Zirconia Restorations | 1.1% | North America, Western Europe, urban Asia-Pacific | Short term (≤ 2 years) |

| AI-Driven CAD Workflows Cutting Design/Milling Cost & Waste | 0.9% | Global, concentrated in high-volume laboratories and dental-service organizations | Medium term (2-4 years) |

| Regional Localization of Zirconia Manufacturing Prompted by Tariff & Supply-Risk Mitigation | 0.7% | North America, European Union, with emerging capacity in India, Mexico | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital-Dentistry (CAD/CAM) Adoption Accelerates Zirconia Demand

Laboratories and clinics continue replacing analog impressions with intraoral scanners and integrated milling systems. 3Shape’s Automate AI platform processed more than 3 million zirconia cases during 2025 and trimmed design time to under three minutes. Dentsply Sirona reported 18% year-over-year growth in Primemill and inLab unit sales in the same period, directly lifting zirconia blank consumption. Standardized thresholds in ISO 13356 and ISO 6872 reassure buyers that CAD/CAM-graded blanks meet minimum 800 MPa flexural strength, facilitating predictable restorative outcomes.[1] International Organization for Standardization Editorial Staff, “ISO 13356: Implants for Surgery—Y-TZP,” ISO, iso.org Heightened throughput and lower per-unit costs make zirconia the default option in centralized milling hubs, especially within dental-service organizations that manage hundreds of daily cases. These fundamentals underpin a robust contribution to the wider zirconia based dental materials market.

Rising Preference for Aesthetic, Metal-Free Restorations

Consumers increasingly reject metal margins in favor of tooth-colored crowns and bridges. A 2024 patient survey revealed 78% preference for all-ceramic solutions over metal-ceramic alternatives.[2]Luis Jiménez-Castellanos, “Patient Preferences for All-Ceramic Versus Metal-Ceramic Crowns,” Journal of Prosthetic Dentistry, journals.elsevier.com High-translucency 5Y-TZP now achieves light transmission above 40%, narrowing the optical gap with natural enamel. Ivoclar Vivadent’s IPS e.max ZirCAD Prime combines a 3Y core with a 5Y veneer and exceeds 750 MPa flexural strength, eliminating manual porcelain layering in many anterior cases. Regulatory pathways under EU MDR 2017/745 and the FDA 510(k) process oblige manufacturers to demonstrate biocompatibility, ensuring long-term safety. Aesthetic demand feeds directly into volume gains for the zirconia based dental materials market.

Global Ageing Population & Caries Prevalence

United Nations projections show the 65-plus cohort reaching 1.6 billion by 2050, boosting restorative volumes worldwide. WHO data confirm that untreated caries affects 2.5 billion people, sustaining demand for durable crowns and bridges.[3]Benoit Varenne, “Global Oral Health Status Report 2024,” World Health Organization, who.int Japan’s latest dental survey records 25.0 remaining teeth per 80-year-old, up from 24.1 in 2017, yet restorative treatments continue to rise. Zirconia’s low plaque affinity and high fracture resistance suit geriatric patients who often struggle with oral hygiene. These demographic and clinical factors reinforce long-run expansion of the zirconia based dental materials market.

Speed-Sintering Furnaces Enabling Chair-Side Same-Day Restorations

Rapid furnaces such as Dentsply Sirona’s SpeedFire complete densification in 14 minutes compared with legacy eight-hour cycles. Same-visit delivery increases patient satisfaction and reduces temporary crown costs. Early adopters report that faster turnaround boosts clinic throughput by up to 25%, a tangible driver of zirconia blank consumption. Urban practices in the United States, Germany, and South Korea illustrate the strongest near-term uptake. As pricing declines, rapid sintering will influence wider segments of the zirconia based dental materials market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Material & Equipment Costs Versus Alternative Ceramics/Metal-Ceramic Options | 1.4% | Global, most acute in price-sensitive markets of South Asia, Latin America, Eastern Europe | Medium term (2-4 years) |

| Requirement For Specialized Technical Expertise & Training | 0.9% | Global, with acute shortages in emerging markets and rural regions | Long term (≥ 4 years) |

| Volatility In Zirconium-Oxide Powder Supply Chain | 0.7% | Global, with supply concentrated in Australia, South Africa, China | Short term (≤ 2 years) |

| Clinical Misuse From 3Y/4Y/5Y Grade Confusion Causing Early Failures | 0.5% | Global, particularly in markets with limited continuing-education infrastructure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Material & Equipment Costs

Zirconia discs sell at 30-50% premiums over lithium-disilicate blanks, and entry-level five-axis mills cost USD 80,000–150,000. A 2024 cost analysis pegged all-in crown production at USD 62 versus USD 48 for lithium disilicate. Speed-sintering furnaces list above USD 25,000, and capital recovery hinges on sufficient daily cases. Price sensitivity hampers adoption in India, Brazil, and Eastern Europe, tempering the near-term pace of the zirconia based dental materials market.

Requirement For Specialized Technical Expertise & Training

Only 38% of U.S. general dentists feel “very confident” selecting the correct zirconia grade, according to the ADA’s 2024 workforce survey. Training programs cost USD 1,500–3,000 and remain concentrated in North America and Western Europe. Limited expertise prolongs learning curves and heightens risk of fabrication errors, restraining the zirconia based dental materials market in underserved regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Discs Dominate, Powders Surge

Zirconia dental discs accounted for 59.46% of 2025 revenue, reflecting seamless integration with five-axis milling units and automated loading systems. High-volume laboratories cut per-unit labor to under five minutes, reinforcing disc leadership within the zirconia based dental materials market. Blocks remain essential for small chairside mills, while powders for 3D printing are set to grow at a 12.53% CAGR. The ability to nest multiple restorations in one build and avoid bur wear offsets powder prices near USD 200 per kg. The zirconia based dental materials market size for 3D-printed powders is predicted to expand rapidly as FDA guidance clarifies validation protocols.

Powder suppliers such as 3D Systems report layer resolutions of 50 microns and densities above 99% for NextDent Zirconia, meeting ISO 6872 Class 5 strength requirements. Austrian player Lithoz revealed 41% year-over-year powder growth in 2024 as labs print implant bars and surgical guides. These additive advances promise fresh momentum for the zirconia based dental materials market.

By Application: Crowns Lead, Implant Abutments Accelerate

Dental crowns held 44.13% revenue in 2025, illustrating their ubiquity across single-tooth restorations. Monolithic crowns eliminate veneering risk and streamline lab labor, entrenching crown dominance within the zirconia based dental materials market. Bridges follow, leveraged by high flexural strength for posterior spans. Implant abutments carry an 11.43% CAGR through 2031, buoyed by zirconia’s soft-tissue compatibility. A randomized trial found 18% lower plaque accumulation on zirconia versus titanium abutments. Straumann’s Pure Ceramic line is experiencing double-digit sales gains in Europe and North America.

Minimal-prep inlays and onlays are gaining share as preservation-focused dentistry spreads, while zirconia dentures remain niche yet promising in geriatric populations. Collectively, these trends extend growth in the zirconia based dental materials market.

By End User: Laboratories Retain Majority, Clinics Gain Speed

Dental laboratories contributed 51.64% of revenue in 2025, processing up to 200 daily cases and unlocking scale economies on blanks and burs. Clinics, however, are expanding at a 10.68% CAGR as rapid sintering furnaces enable same-day crowns. Dentsply Sirona shipped more than 1,200 SpeedFire units during 2025, with 68% of buyers citing same-visit workflows. Hospitals use zirconia mainly in oral-maxillofacial surgery, while universities push research on nano-structured variants. This evolving mix sustains momentum in the zirconia based dental materials market.

By Material Grade: 3Y-TZP Leads, Gradient Formulations Surge

High-strength 3Y-TZP held 43.22% material-grade revenue in 2025, favored for posterior load-bearing restorations. 5Y-TZP offers enhanced translucency for anterior use but sacrifices some strength. Multi-layered blanks marrying 3Y cores with 5Y veneers are projected to grow 12.54% CAGR, making them the fastest rising contributor to the zirconia based dental materials market. Kuraray Noritake’s Katana UTML features a four-zone yttria gradient that boosts translucency from 38% to 49% across the blank. Research at the University of Zurich hints that nano-structured zirconia may eventually combine 3Y-level strength with 5Y-level translucency.

Geography Analysis

North America generated 37.72% of global revenue in 2025 as U.S. practices invested heavily in scanners and mills. The ADA found that 62% of general offices owned intraoral scanners by 2024. The FDA’s streamlined 510(k) pathway supports brisk launch cycles, sustaining leadership in the zirconia based dental materials market.

Europe ranks second, anchored by German manufacturing clusters and strict CE-mark requirements. The U.K.’s NHS began reimbursing posterior monolithic crowns in 2024, widening patient access. Southern Europe progresses more slowly, but cosmetic clinics in Milan and Barcelona are lifting regional uptake.

Asia-Pacific is the fastest growing region at 10.67% CAGR. China’s regulator approved 22 domestic blanks in 2024, and local producers price discs 20–30% below European imports. Japan expanded reimbursement to include molar zirconia crowns, tapping its aging population. India’s dental-tourism sector and Korea’s digital-dentistry ecosystem add further upside, cementing Asia-Pacific as a pivotal growth engine for the zirconia based dental materials market.

Middle East & Africa and South America contribute smaller shares yet show steady progress. Dubai licensed more than 1,200 dental clinics in 2024 and mandates CE or FDA-cleared materials. Brazil’s first domestic blank approval in 2025 signals a turn toward localized production. These developments gradually enlarge the global footprint of the zirconia based dental materials market.

Competitive Landscape

The zirconia based dental materials market is moderately concentrated. European and Japanese leaders defend premium slices with gradient innovation, while Chinese suppliers like Upcera and SINOCERA leverage integrated feedstock to undercut prices by up to 30%. Dentsply Sirona’s CEREC ecosystem bundles mills, furnaces, and proprietary blanks, and consumables reached 38% of its CAD/CAM revenue in 2025. Ivoclar Vivadent mirrors this approach via the PrograMill platform and IPS e.max ZirCAD range. Straumann expanded into materials through Createch Medical and now markets Pure Ceramic abutments.

Chinese entrants are establishing overseas plants—Upcera plans a Mexican facility by 2026—to sidestep tariffs and shorten delivery times. Smaller innovators such as Lithoz and 3D Systems target additive manufacturing niches with printer-powder pairs certified to ISO 13356. Competitive intensity fosters rapid R&D cycles, ensuring that the zirconia based dental materials market remains dynamic.

Zirconia Based Dental Materials Industry Leaders

Dentsply Sirona

Ivoclar Vivadent

Kuraray Noritake Dental

Zirkonzahn

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Kuraray Noritake Dental launched KATANA Zirconia ONE For IMPLANT, a pre-sintered block that supports hybrid abutment crowns in CEREC systems.

- June 2025: ClearChoice introduced Endura Elite, a full-arch restoration fabricated from premium zirconia to enhance esthetics and longevity.

- May 2025: Dentsply Sirona unveiled CEREC Cercon 4D multidimensional abutment blocks and Calibra Abutment resin cement for chairside workflows.

Global Zirconia Based Dental Materials Market Report Scope

Zirconia-based dental materials are high-strength, bioinert ceramics made from zirconium dioxide, used for durable and aesthetic dental restorations like crowns, bridges, and implants. Known for toughness, wear resistance, and radiopacity, they are stabilized with yttrium oxide (yttria) and fabricated using CAD/CAM technology for precise, biocompatible applications.

The Zirconia Based Dental Materials Market Report is segmented by Product Type, Application, End User, Material Grade, and Geography. By Product Type, the market is segmented into Zirconia Dental Discs, Zirconia Dental Blocks, and Zirconia Powders for 3D Printing. By Application, the market is segmented into Dental Crowns, Dental Bridges, Inlays & Onlays, Dentures, Implant Abutments, Veneers, and Orthodontic Brackets. By End User, the market is segmented into Dental Laboratories, Dental Clinics, Hospitals, and Academic & Research Institutes. By Material Grade, the market is segmented into High-Strength 3Y-TZP, High-Translucency 5Y, Multi-Layered/Gradient, Zirconia-Toughened Alumina, and Nano-Structured. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Zirconia Dental Discs |

| Zirconia Dental Blocks |

| Zirconia Powders (3D-printing grade) |

| Dental Crowns |

| Dental Bridges |

| Inlays & Onlays |

| Dentures |

| Implant Abutments |

| Veneers |

| Orthodontic Brackets |

| Dental Laboratories |

| Dental Clinics |

| Hospitals |

| Academic & Research Institutes |

| High-Strength (3Y-TZP) Zirconia |

| High-Translucency (5Y) Zirconia |

| Multi-Layered / Gradient Zirconia |

| Zirconia-Toughened Alumina (ZTA) |

| Nano-structured Zirconia |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Zirconia Dental Discs | |

| Zirconia Dental Blocks | ||

| Zirconia Powders (3D-printing grade) | ||

| By Application | Dental Crowns | |

| Dental Bridges | ||

| Inlays & Onlays | ||

| Dentures | ||

| Implant Abutments | ||

| Veneers | ||

| Orthodontic Brackets | ||

| By End User | Dental Laboratories | |

| Dental Clinics | ||

| Hospitals | ||

| Academic & Research Institutes | ||

| By Material Grade | High-Strength (3Y-TZP) Zirconia | |

| High-Translucency (5Y) Zirconia | ||

| Multi-Layered / Gradient Zirconia | ||

| Zirconia-Toughened Alumina (ZTA) | ||

| Nano-structured Zirconia | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the zirconia based dental materials market today?

The zirconia based dental materials market size reached USD 412.96 million in 2026 and is projected to grow to USD 620.79 million by 2031.

Which product type leads global revenue?

Zirconia dental discs hold 59.46% of 2025 revenue thanks to compatibility with five-axis milling systems.

What segment is expanding the fastest through 2031?

Powders for 3D printing are forecast to post a 12.53% CAGR as additive workflows gain traction.

Which region shows the highest growth outlook?

Asia-Pacific is set to expand at 10.67% annually on expanding local manufacturing and rising aesthetic demand.

Why are implant abutments a high-growth application?

Clinicians favor zirconia abutments for superior soft-tissue aesthetics and lower plaque accumulation, supporting an 11.43% CAGR through 2031.

What is the main barrier to wider adoption in emerging markets?

Higher material and equipment costs versus alternative ceramics and metal-ceramic options remain the most cited hurdle.

Page last updated on: