Zinc Polycarboxylate Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

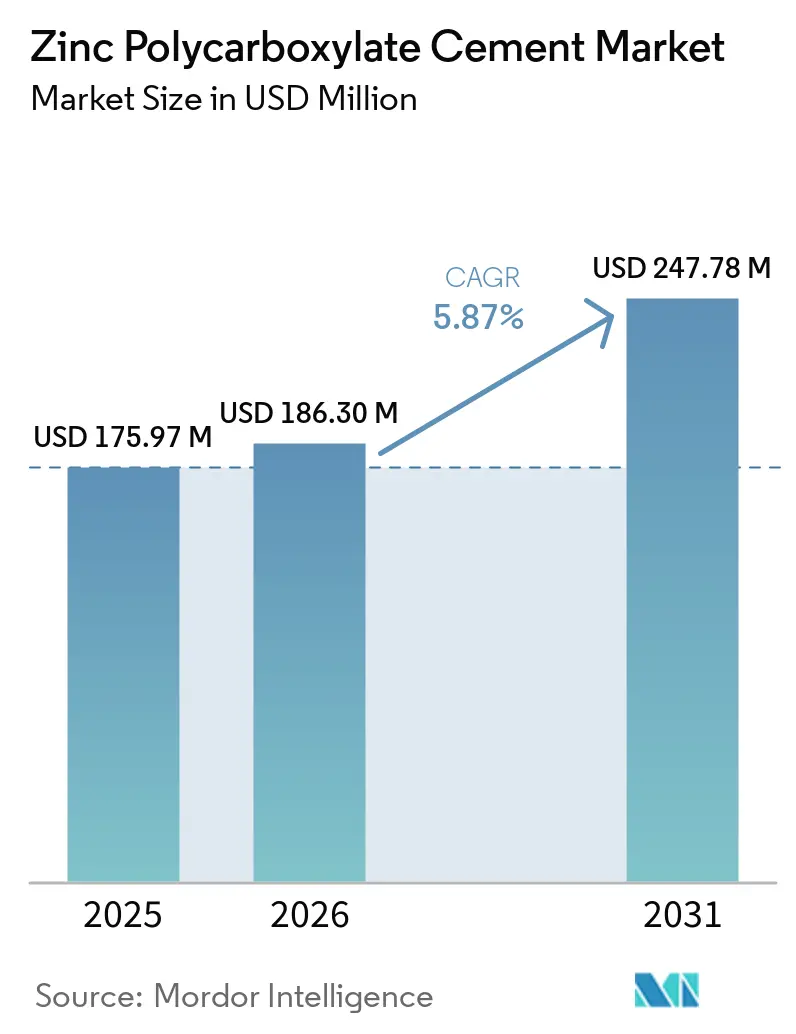

| Market Size (2026) | USD 186.30 Million |

| Market Size (2031) | USD 247.78 Million |

| Growth Rate (2026 - 2031) | 5.87% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zinc Polycarboxylate Cement Market Analysis by Mordor Intelligence

The Zinc Polycarboxylate Cement Market size is projected to expand from USD 175.97 million in 2025 and USD 186.30 million in 2026 to USD 247.78 million by 2031, registering a CAGR of 5.87% between 2026 to 2031.

Demand is holding firm because hospitals and dental clinics in cost-sensitive nations still prefer proven acid-base chemistries that bond without light curing, while premium practices migrate to resin-modified glass ionomers and self-adhesive resin cements. Pediatric and geriatric protocols that avoid allergenic monomers continue to lean on zinc polycarboxylate cements, reinforcing steady volumes despite substitution threats. Manufacturers are shortening setting times and adding self-adhesive features, helping the material defend its niche in orthodontic banding and in single-unit zirconia crown workflows. Procurement officers in emerging Asia and Latin America are also contracting directly with regional toll plants, leveraging the material’s 3-4× cost advantage over resin alternatives to expand restorative coverage under tight reimbursement ceilings.

Key Report Takeaways

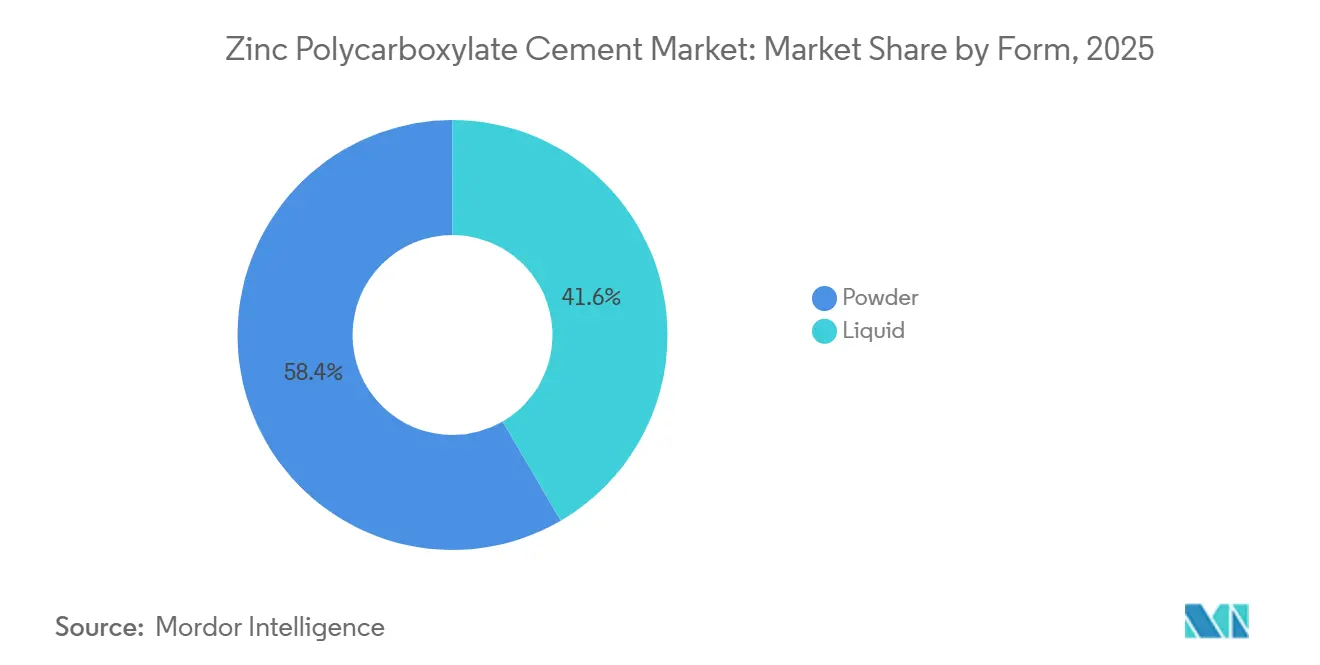

- By form, powder commanded 58.40% of zinc polycarboxylate cement market share in 2025, while the liquid segment is projected to advance at a 5.98% CAGR through 2031.

- By application, crown and bridge cementation led with 41.34% revenue share in 2025; orthodontic band and bracket luting is forecast to expand at a 6.99% CAGR to 2031.

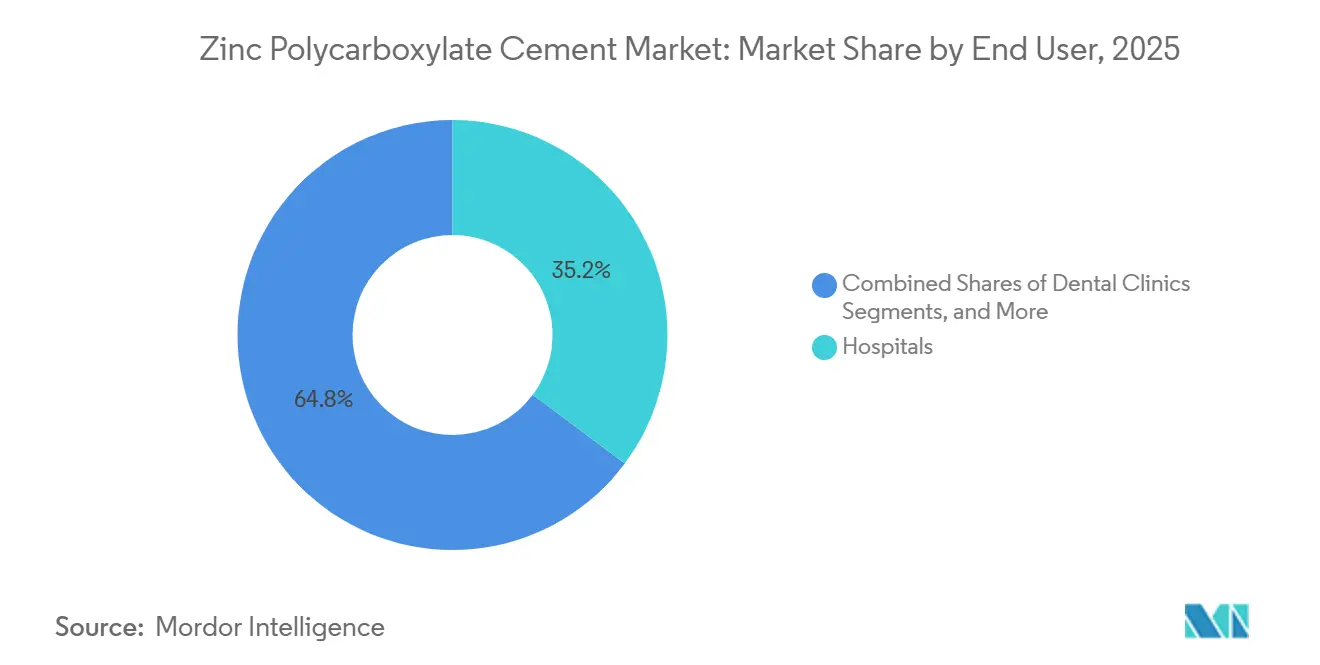

- By end user, hospitals held 35.20% of the zinc polycarboxylate cement market size in 2025, whereas dental clinics are growing at a 6.45% CAGR through 2031.

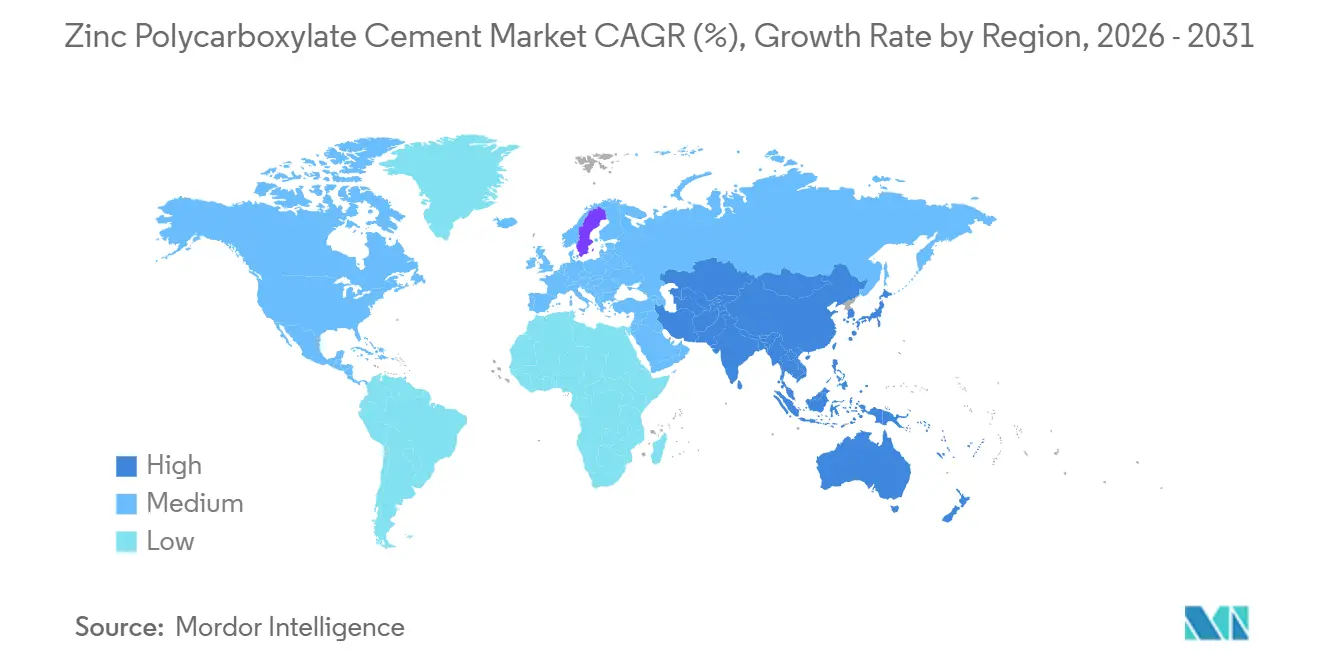

- By geography, North America accounted for 39.67% share of the zinc polycarboxylate cement market in 2025, while Asia-Pacific exhibits the fastest regional CAGR at 6.15% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Zinc Polycarboxylate Cement Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising volume of single-unit metal and zirconia restorations | +1.2% | North America, Europe, global tourism hubs | Medium term (2-4 years) |

| Accelerating adoption in pediatric & geriatric dentistry | +1.5% | Asia-Pacific, Latin America, global | Long term (≥ 4 years) |

| Cost advantage over resin-based cements in emerging markets | +1.3% | Asia-Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Demand for self-adhesive, faster-setting ZPC formulations | +0.9% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| OEM outsourcing by global brands to Asian toll manufacturers | +0.7% | Asia-Pacific core, global spill-over | Medium term (2-4 years) |

| Regulatory shift toward BPA-free materials | +0.8% | Europe, North America, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Single-Unit Metal and Zirconia Restorations

The increasing chairside production of zirconia and metal crowns is driving growth in the zinc polycarboxylate cement market. This cement chemically bonds without requiring separate primers, offering significant time savings in high-throughput environments. Zirconia's low translucency effectively conceals the slightly opaque cement line, and clinicians can seat units under moderate moisture, providing a practical advantage over hydrophobic resin cements. Dental tourism hubs such as Thailand and Mexico prefer ISO 9917-compliant products, which eliminate the need for light-curing lamps in remote outreach clinics. In the United States, group purchasing organizations bundle zinc polycarboxylate cements with stainless-steel crown kits for Medicaid children's programs, demonstrating the niche's resilience. As CAD/CAM workflows expand, the cement's low film thickness continues to meet marginal gap requirements, ensuring its relevance in the digital era.

Accelerating Adoption in Pediatric & Geriatric Dentistry (Hypersensitivity to Resin Cements)

Clinical protocols for pediatric and geriatric patients increasingly favor biocompatible cementation methods that avoid bisphenol A and other sensitizing monomers, contributing to the steady growth of the zinc polycarboxylate cement market. Stainless-steel crowns on primary molars exhibit a five-year survival rate of 93-97% when seated with conventional acid-base cements, significantly outperforming composite alternatives. Among U.S. adults aged 65 and older, root caries prevalence reaches 60%, making the cement's fluoride release and moisture tolerance particularly suitable for these cases.[1]U.S. Food and Drug Administration, “Recognition of Consensus Standards—ISO 9917-1:2025,” fda.gov Additionally, xerostomia caused by polypharmacy further limits the effectiveness of resin-based cements, reinforcing the preference for traditional chemistries. The European Union's pediatric BPA ban has further accelerated this trend, with suppliers emphasizing BPA-free labeling to attract family clinics.

Cost Advantage Over Resin-Based Cements in Emerging Markets

Zinc polycarboxylate cements, priced at approximately one-quarter of resin cements, remain the preferred choice in resource-constrained health systems across regions such as India, Indonesia, and parts of Africa. In China, the localization of dental device production is channeling stimulus financing toward domestic cement lines that meet ISO radiopacity standards without relying on expensive resin technologies. Similarly, Latin American ministries are leveraging cost savings to expand universal oral-health campaigns, maintaining steady demand despite currency fluctuations.

Demand for Self-Adhesive, Faster-Setting ZPC Formulations

Manufacturers are developing polyacrylic acid chains that enhance hydroxyapatite chelation, reducing intraoral setting times to under five minutes and eliminating the need for conditioners. These advancements are helping the zinc polycarboxylate cement market maintain its position in orthodontic banding, where faster lock-in times minimize chairside delays. Liquid-capsule delivery systems are also gaining traction, reducing operator variability and aligning with infection-control requirements. Shofu's integration of Smart Dentistry Solutions in January 2026 highlights the industry's focus on chemistry upgrades that support digital brackets and clear aligner accessories.[2]Prevest DenPro, “Poly Zinc+ Product Information,” prevestdenpro.com Fast-setting formulations are particularly appealing to high-volume community clinics, where patient chairs are rotated every 15 minutes.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Substitution by resin-modified glass ionomers & resin cements | -1.8% | North America, Europe, global premium clinics | Medium term (2-4 years) |

| Higher water solubility & marginal leakage concerns | -0.9% | Humid climates worldwide | Long term (≥ 4 years) |

| Stringent radiopacity & biocompatibility testing raising costs | -0.6% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Supply volatility of high-purity zinc oxide feedstock | -0.5% | North America, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Substitution by Resin-Modified Glass Ionomers & Resin Cements

Resin-hybrid cements now deliver a shear bond strength of 1.39 MPa to zirconia, outperforming the 0.85 MPa bond strength of conventional glass ionomers. These cements also exhibit strong resistance to washout under occlusal stress. Digital milling centers have standardized the use of these resins to ensure retention on CAD/CAM onlays, capturing higher-value cases that were previously dominated by the zinc polycarboxylate cement market. In a notable development, GC America’s collaboration with SprintRay in March 2026 has streamlined production by linking CAD files directly to a press capable of producing ten units optimized for resin bonding in just ten minutes. With insurers now reimbursing digital crowns at parity, clinicians are increasingly transitioning to these solutions, reducing the volume of legacy cements.

Higher Water Solubility & Marginal Leakage Concerns

Although the hydrophilic matrix of the cement enhances bonding, it also dissolves gradually in saliva, increasing the risk of leakage under subgingival margins. To comply with ISO 9917 standards, which require radiopacity above 100% of aluminum, additional barium fillers are incorporated. However, this can weaken the compressive strength of the cement. In hot and humid regions, oral fluids accelerate the dissolution process, prompting practitioners to limit their use to temporary crowns or pediatric stainless-steel cases. Resin-modified glass ionomers, strengthened with HEMA, effectively address these challenges and are increasingly replacing zinc polycarboxylate cements in long-term restorations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Powder Takes the Lead with Bulk Purchases and Shelf Stability

In 2025, the powder segment held a dominant 58.40% share of the zinc polycarboxylate cement market, driven by hospitals and teaching institutions that mix chairside for varied viscosities. These organizations procure kilogram drums through long-term contracts, effectively managing budgets and reducing losses due to product expiration. Additionally, powder-liquid kits help avoid plastic capsule waste, aligning with sustainability objectives in healthcare facilities.

Liquid capsules, however, are growing at a steady 5.98% CAGR as clinics increasingly prefer single-dose consistency and faster cleanup, particularly under stringent infection-control protocols introduced after the COVID-19 pandemic. The capsulated delivery system minimizes operator mixing errors and is particularly appealing to mobile dental units that lack glass slabs. In India, emerging brands are introducing foil-pouch powders that dissolve directly in proprietary liquids, further narrowing the distinction between segments and enhancing market penetration.

By Application: Crown & Bridge Cementation Dominates, Orthodontic Luting Grows

Crown and bridge cementation accounted for 41.34% of the 2025 revenue, supported by bulk crown programs in government insurance and international dental tourism packages. Clinics favor the cement’s low film thickness, which ensures a passive fit on metal copings. This segment serves as a foundation for baseline demand and acts as a key price benchmark during tender negotiations.

Orthodontic band and bracket luting is driving growth, expanding at a 6.99% CAGR. This growth is fueled by the increasing use of temporary attachment cements in clear aligner hybrids, which must withstand salivary seepage during extended appointments. Liquid capsules that set in under five minutes reduce chairside failures and align with the operational needs of clinics offering evening and weekend hours. This trend ensures the zinc polycarboxylate cement market remains relevant, even in practices that primarily use resin for definitive restorations.

By End User: Hospitals Dominate, Dental Clinics Expand Their Footprint

In 2025, hospitals captured 35.20% of the zinc polycarboxylate cement market. Centralized purchasing strategies enable hospitals to secure volume discounts and support workflows across multiple specialties, ranging from pediatric crowns to maxillofacial splints. The absence of curing lights in many inpatient units makes self-setting cement a practical choice.

Dental clinics are experiencing a 6.45% CAGR, driven by the expansion of franchises and dental service organizations that implement standardized cost-containment formularies across numerous operatories. Capsules that eliminate the need for weighing ensure consistent application, addressing challenges associated with high associate dentist turnover. Although academic centers contribute a smaller share of revenue, they play a critical role in validating new glass fillers and influencing textbook protocols, which downstream users adopt, thereby supporting the continuity and development of the zinc polycarboxylate cement market.

Geography Analysis

In 2025, North America captured 39.67% of the zinc polycarboxylate cement market share, supported by Medicaid and Veterans Affairs contracts that require ISO-compliant, BPA-free cements. Integrated delivery networks secure multiyear tenders, ensuring consistent supply and reducing risks associated with off-label resin use in pediatric applications. The United States dominates the region, contributing approximately 85% of sales, while Canada and Mexico account for the remainder through public benefit plans and cross-border clinics.

Asia-Pacific is projected to experience the fastest growth, with a 6.15% CAGR from 2026 to 2031. This growth is driven by localization initiatives in China and India, which lower import tariffs and accelerate product registration. Increasing disposable incomes in Indonesia and Vietnam are boosting out-of-pocket spending on restorative treatments. Additionally, government dental programs in rural India prefer powder kits due to their ability to withstand tropical storage conditions. Japan's aging population is driving consistent demand for atraumatic restorative treatments, leveraging the cement's fluoride release properties.

Europe, South America, and the Middle East & Africa collectively account for the remaining market demand. Europe is witnessing moderate growth as clinicians adapt to BPA bans and prefer traditional chemistries for pediatric applications. Brazil's public SUS network procures domestically blended powders to meet ISO 9917 radiopacity standards while managing costs. In Dubai, private clinics alternate between premium resins and conventional powders based on patient payment methods. South Africa's mobile outreach programs rely on foil-pack powder kits for their portability, maintaining steady demand across provinces in the zinc polycarboxylate cement market.

Competitive Landscape

The zinc polycarboxylate cement market is moderately fragmented. Five major players—3M, Dentsply Sirona, GC Corporation, Shofu, and VOCO account for the majority of global revenue, while numerous regional brands cater to price-sensitive segments. Competition is increasingly focused on packaging innovation, BPA-free labeling, and digital workflow integration rather than solely on bond strength. In January 2026, Shofu completed the integration of Smart Dentistry Solutions to enhance logistics in the U.S. and promote upgraded cements alongside CAD/CAM blocks.

In March 2026, GC America formed a partnership with SprintRay to incorporate its cements into a rapid press-and-print system capable of producing ten zirconia restorations in ten minutes. Dentsply Sirona expanded its collaboration with Benco Dental, increasing showroom visibility for its cementation products and aligning promotions with chairside mills and imaging equipment. Asian OEMs, such as Shanghai Rong Xiang and Prevest DenPro, secure tenders by offering ISO-compliant white-label powders at prices up to 40% lower than those of multinational competitors.

Supply risks related to high-purity zinc oxide create moderate barriers to entry, as smelter shutdowns can constrain inventories. Leading brands mitigate this risk by sourcing from multiple suppliers. Smaller firms rely on forward contracts to hedge against cost fluctuations but still face margin pressures. The market favors companies with strong regulatory compliance and extensive distribution networks, while also providing opportunities for agile regional players that tailor packaging and pricing to local market needs.

Zinc Polycarboxylate Cement Industry Leaders

3M Company

Dentsply Sirona Inc.

GC Corporation

Shofu

VOCO GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: GC America and SprintRay announced a strategic partnership to link GC materials with SprintRay’s MIDAS digital press, enabling up to ten indirect restorations in less than ten minutes and launching a 40-city clinician education tour.

- January 2026: Shofu Dental Corporation finalized the merger of Smart Dentistry Solutions into its U.S. arm, transferring all product supply and invoicing to the combined entity from 5 January 2026.

- January 2026: Dentsply Sirona and Benco Dental broadened their alliance to distribute restorative materials, orthodontics, and digital equipment across North American outlets, expanding channel penetration for zinc polycarboxylate cement lines.

Global Zinc Polycarboxylate Cement Market Report Scope

As per the scope of the report, zinc polycarboxylate cement is a dental luting agent that provides true chemical adhesion to enamel, dentin, and stainless steel, primarily used for permanent restoration cementation, ortho bands, and dental bases. Composed of zinc oxide powder and polyacrylic acid liquid, it is highly biocompatible with low pulpal irritation.

The Zinc Polycarboxylate Cement Market is segmented into form, application, end user, and geography. By form, the market is segmented into powder and liquid. By application, the market is segmented into crown & bridge cementation, orthodontic band/bracket luting, cavity base/liner, and temporary/pediatric restorations. By end user, the market is segmented into hospitals, dental clinics, academic & research institutes, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Powder |

| Liquid |

| Crown & Bridge Cementation |

| Orthodontic Band/Bracket Luting |

| Cavity Base / Liner |

| Temporary / Pediatric Restorations |

| Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Form | Powder | |

| Liquid | ||

| By Application | Crown & Bridge Cementation | |

| Orthodontic Band/Bracket Luting | ||

| Cavity Base / Liner | ||

| Temporary / Pediatric Restorations | ||

| By End User | Hospitals | |

| Dental Clinics | ||

| Academic & Research Institutes | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the zinc polycarboxylate cement market be by 2031?

The zinc polycarboxylate cement market size is forecast to reach USD 247.78 million by 2031, advancing at a 5.87% CAGR from 2026 to 2031.

Which region is growing the fastest for zinc polycarboxylate cements?

Asia-Pacific is projected to record a 6.15% CAGR, driven by Chinese and Indian production scale-ups and rising restorative spending.

What application area leads revenue?

Crown and bridge cementation led with a 41.34% share in 2025 owing to long-standing use in metal and zirconia crowns.

Which form factor dominates sales?

Powder formulations captured 58.40% zinc polycarboxylate cement market share in 2025 because hospitals favor bulk kits with long shelf life.

Who are the key suppliers in this space?

3M, Dentsply Sirona, GC Corporation, Shofu, and VOCO together hold roughly 55% of global revenue, with regional players filling cost-sensitive niches.

What is driving orthodontic demand for the cement?

Orthodontic band and bracket luting is advancing at a 6.99% CAGR as the materials moisture tolerance and faster-setting capsules reduce appliance debonding.

Page last updated on: