X-linked Retinitis Pigmentosa Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

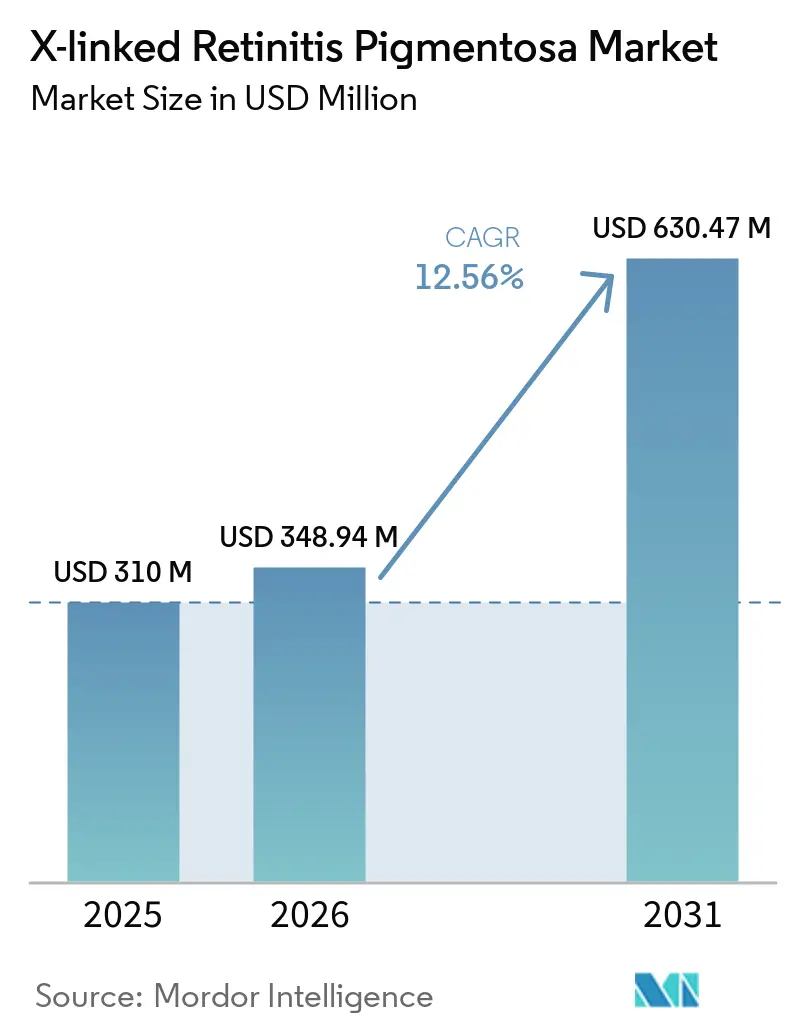

| Market Size (2026) | USD 348.94 Million |

| Market Size (2031) | USD 630.47 Million |

| Growth Rate (2026 - 2031) | 12.56% CAGR |

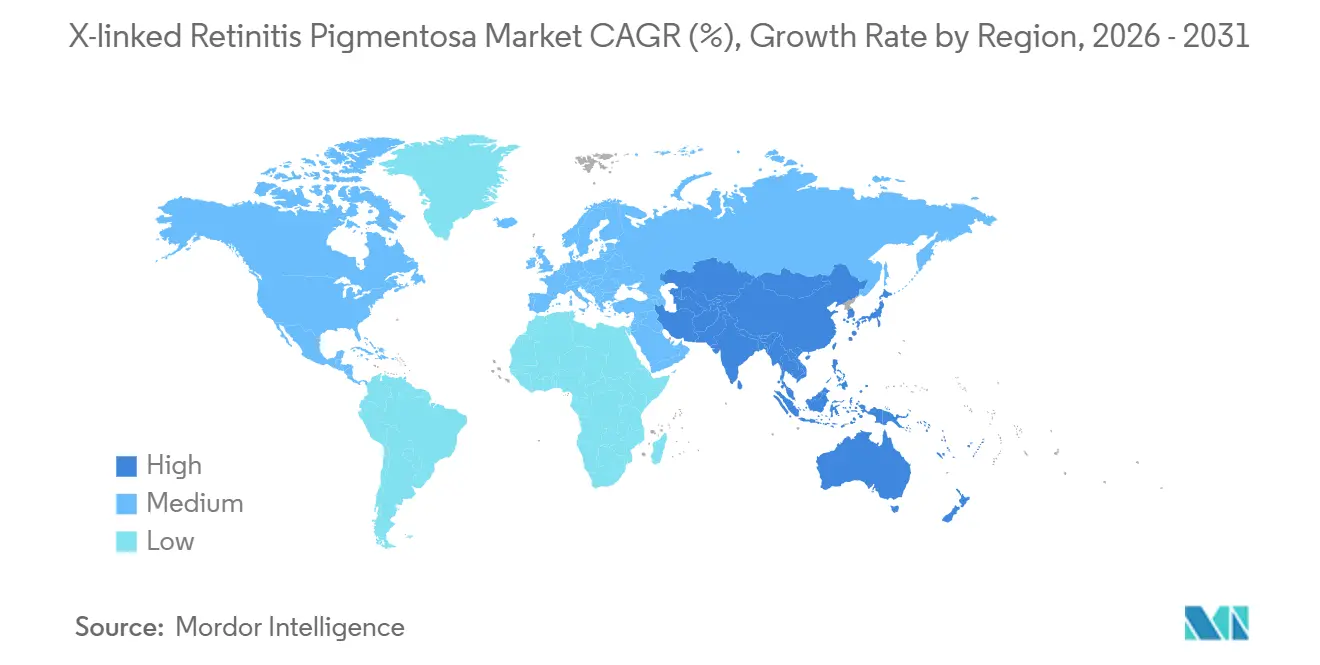

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

X-linked Retinitis Pigmentosa Market Analysis by Mordor Intelligence

The X-linked Retinitis Pigmentosa Market size is expected to grow from USD 310 million in 2025 to USD 348.94 million in 2026 and is forecast to reach USD 630.47 million by 2031 at 12.56% CAGR over 2026-2031.

Accelerating approvals under the Rare Pediatric Disease framework, a thriving secondary market for Priority Review Vouchers valued at more than USD 100 million each, and an expanding pool of venture-backed trials have introduced fresh capital into late-stage gene-replacement programs. In parallel, the Centers for Medicare & Medicaid Services (CMS) Cell and Gene Therapy Access Model has reduced reimbursement risk in five pilot states, encouraging hospitals and eye-care chains to invest in surgical infrastructure innovation. Optogenetics is emerging as the key challenger modality due to MCO-010’s rolling BLA, while capsid-engineered intravitreal vectors are expected to alleviate capacity bottlenecks caused by labor-intensive sub-retinal delivery. Against this backdrop, North America remains the largest regional node, but policy reforms in China, Japan, and South Korea are driving Asia-Pacific toward double-digit growth.

Key Report Takeaways

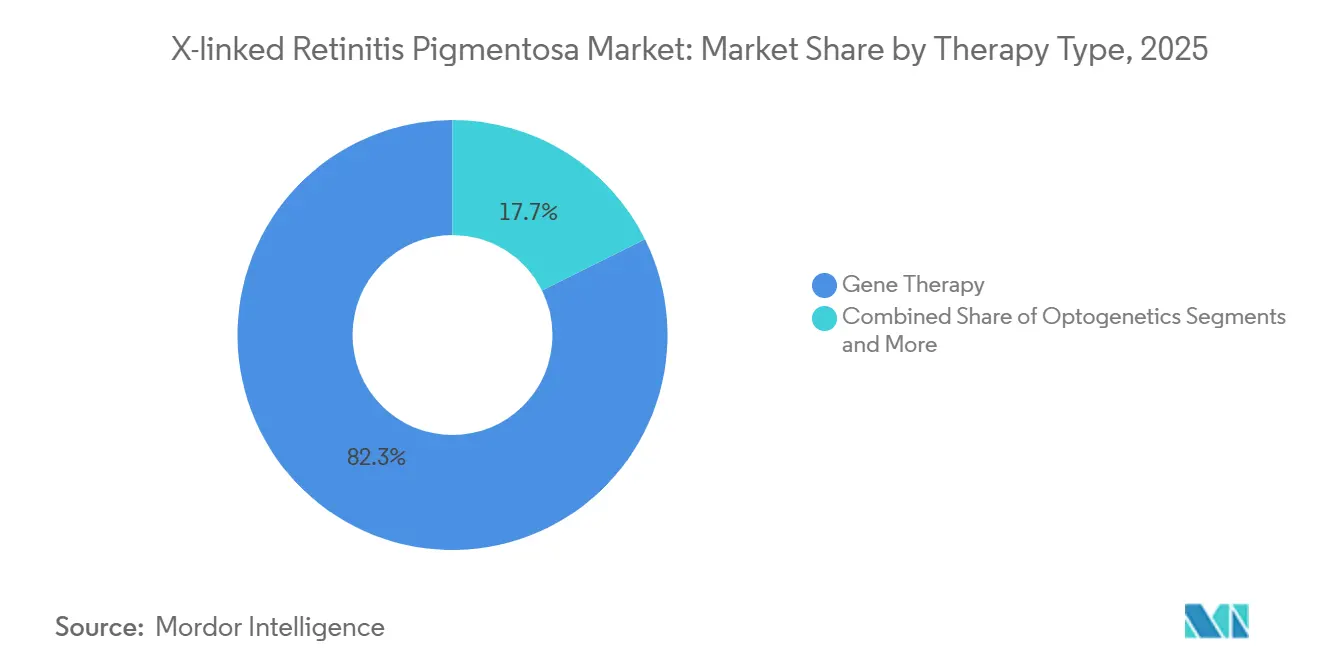

- By therapy type, gene replacement accounted for 82.34% of the X-linked retinitis pigmentosa market share in 2025, while optogenetics is forecast to expand at a 15.23% CAGR through 2031.

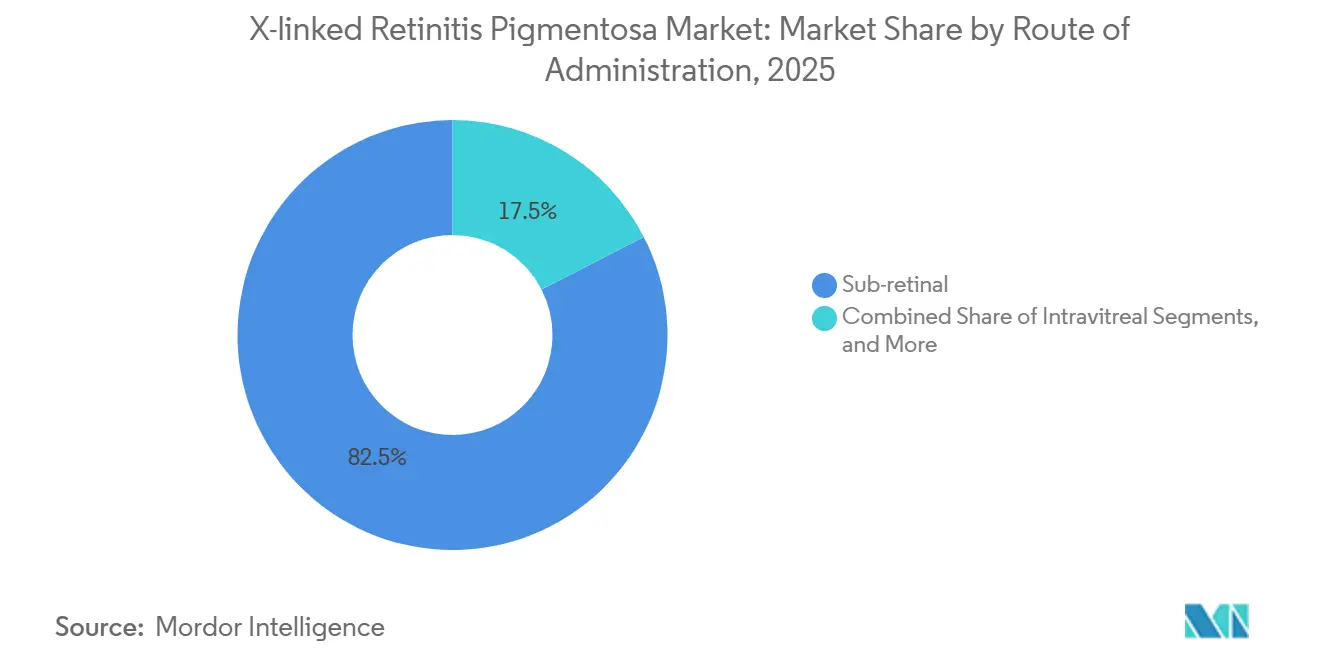

- By route of administration, sub-retinal delivery held 82.54% of the X-linked retinitis pigmentosa market size in 2025; intravitreal approaches will advance at a 15.55% CAGR to 2031.

- By stage of development, Phase I/II trials represented 54.06% of the active pipeline in 2025, whereas discovery and pre-clinical programs will grow at 14.95% CAGR through 2031.

- By end user, hospitals and eye-care chains captured 46.89% revenue share in the X-linked retinitis pigmentosa market in 2025; academic centers will be the fastest-growing channel at 14.69% CAGR to 2031.

- By geography, North America led with 41.13% share of the X-linked retinitis pigmentosa market size in 2025, while Asia-Pacific is on track for a 14.58% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global X-linked Retinitis Pigmentosa Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Breakthroughs in AAV-Mediated RPGR Gene Therapy | 2.8% | Global, led by North America & Europe | Medium term (2-4 years) |

| Payer Acceptance of One-Time Curative Pricing Models | 2.5% | North America & Europe | Short term (≤ 2 years) |

| Priority-Review Vouchers Accelerating ROI | 2.2% | Global, monetized in North America | Short term (≤ 2 years) |

| Cross-Licensing of CRISPR IP Lowering Barriers | 1.8% | Global | Long term (≥ 4 years) |

| Emergence of AI-Guided Retinal Imaging Endpoints | 1.5% | Global, early adoption in North America & APAC | Medium term (2-4 years) |

| Venture Philanthropy De-Risking Early Trials | 1.2% | Global, concentrated in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Breakthroughs in AAV-Mediated RPGR Gene Therapy

In 2024, MeiraGTx progressed botaretigene sparoparvovec to Phase III, enrolling 60 participants across 12 global sites, with interim data expected in late 2026. The vector employs a codon-optimized RPGR-ORF15 under a rhodopsin-kinase promoter, addressing approximately 70% of genetically confirmed cases.[1]MeiraGTx Holdings, “LUMEOS Trial Update,” Ir.meiragtx.com Janssen's investment of USD 1.7 billion highlighted durability expectations initially observed in non-human primates. However, high baseline anti-AAV8 antibodies, present in up to 84% of treatment-naïve children, significantly reduced the pool of eligible candidates. Sponsors are developing capsid variants through platforms like NAV to overcome neutralization at titers ten times higher than the wild-type AAV8.

Payer Acceptance of One-Time Curative Pricing Models

In 2024, CMS introduced its cell and gene therapy access model, allocating USD 2 billion for outcomes-based Medicaid contracts. These contracts reimburse therapies priced between USD 850,000 and USD 1.2 million per eye.[2]Centers for Medicare & Medicaid Services, “Cell and Gene Therapy Access Model,” Innovation.cms.gov Early adopter states require 80% of recipients to achieve a 15-letter gain on the ETDRS scale at 24 months, with rebates of up to 40% of the list price triggered if this benchmark is not met. Manufacturers can securitize future rebate obligations, reducing capital costs and enhancing payor confidence in the X-linked retinitis pigmentosa market. However, only six out of 18 surveyed US commercial insurers maintain rare-disease budgets exceeding USD 50 million, and many enforce strict lifetime caps.

Priority-Review Vouchers Accelerating ROI

Between 2024 and 2025, four XLRP programs received rare pediatric disease designation, each accompanied by a transferable voucher. These vouchers were sold on the secondary market for USD 102 million to USD 146 million, exceeding the USD 80-120 million typically required for Phase III trials in inherited retinal disorders. Nanoscope stated that monetizing a voucher could fund its optogenetic pipeline through proof-of-concept, attracting investors to high-risk, high-return trials. Voucher economics also influence trial design, encouraging companies to prioritize pediatric arms despite adult prevalence being three times higher.

Cross-Licensing of CRISPR IP Lowering Barriers

In 2025, Beam Therapeutics and CRISPR Therapeutics entered into cross-licenses, reducing royalty stacks by 5-7 percentage points and making single-base editors more economically viable in ultra-orphan settings. Simultaneously, the Broad Institute offered non-exclusive Cas9 rights for therapies priced below USD 1 million, fostering academic spin-outs. With over 1,000 documented RPGR mutations, a single adenine base editor could potentially correct 60% of pathogenic variants, simplifying regulatory processes. However, Editas Medicine's decision to pause EDIT-101 reflects how royalty burdens continue to hinder early commercialization of CRISPR ocular programs.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Sub-Retinal Surgical Capacity Bottlenecks | -1.5% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Uncertain Durability of Vector Expression | -1.2% | Global | Medium term (2-4 years) |

| Anti-AAV Neutralising Antibodies in Paediatric Pools | -1.7% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Competing Optogenetic Pipelines Crowding Trial Sites | -1.5% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sub-Retinal Surgical Capacity Bottlenecks

In 2024, the American Society of Retina Specialists reported only 3,000 active vitreoretinal surgeons in the U.S., with 40% aged over 55. While sub-retinal injections demand advanced retinotomy skills, reimbursement for the procedure (code 67036) has stagnated at USD 1,200 since 2020.[3]American Society of Retina Specialists, “2024 Vitreoretinal Workforce Analysis,” Asrs.orgConsequently, only 35 U.S. centers could administer Luxturna in its initial two commercial years, leading to six-month wait times. MeiraGTx is testing a hub-and-spoke training network, but each surgeon's capacity is limited to 2-3 cases daily until intravitreal vectors demonstrate equivalence.

Uncertain Durability of Vector Expression

Follow-ups on Luxturna indicate that 30% of treated eyes plateau between 3-5 years, with some reverting to baseline by year 7. For pediatric XLRP patients diagnosed at a median age of 8, this poses a challenge: they need durability spanning six decades, far exceeding current data. Re-dosing complications arise as 95% of recipients develop neutralizing antibodies within months, and while alternative capsids offer some relief, they only partially evade cross-reactivity. Investigations are ongoing into episomal dilution, immune clearance, and promoter methylation. However, the absence of definitive mechanistic data has led to payer apprehensions regarding long-term cost-effectiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapy Type: Gene Replacement Dominates, Optogenetics on the Rise

In 2025, gene replacement accounted for 82.34% of the x-linked retinitis pigmentosa market share, translating to approximately USD 287 million within the broader market size. Three pivotal AAV8-RPGR programs focus on preserving photoreceptors, a clinical endpoint increasingly recognized by regulators as a surrogate for functional vision. Optogenetics, while holding a smaller share in 2025, is projected to achieve the fastest growth at a 15.23% CAGR, driven by MCO-010's pursuit of FDA approval without requiring vector-serotype matching or intact outer segments.

Nanoscope’s opsin activates under ambient light, eliminating the need for bulky goggles and increasing adoption among elderly patients. Meanwhile, BlueRock’s iPSC-derived photoreceptors, which entered Phase I/II to address late-stage degeneration, face cost-of-goods challenges that could exceed USD 900,000 per dose. Pharmacologic neuroprotection remains a secondary option, limited by its transient efficacy and the need for continuous dosing.

By Stage of Development: Pipeline Immaturity Evident in Early-Phase Concentration

Phase I/II assets formed 54.06% of the X-linked retinitis pigmentosa market size pipeline in 2025, highlighting clinical immaturity despite growing enthusiasm for novel modalities. Discovery programs driven by CRISPR-based editing are advancing at a 14.95% CAGR, supported by declining royalty rates and modular guide-RNA designs that shorten lead-optimization timelines.

Phase III trials, comprising only 12% of the pipeline, exert significant influence by setting precedents for durability and safety, particularly in pediatric dosing. The first approvals are expected to trigger a follow-the-leader dynamic, with payers benchmarking budget impacts against early pricing signals. Approved therapies remain minimal, limited to off-label Luxturna use in the rare RPGR-RPE65 overlap, a cohort of fewer than 50 patients worldwide.

By Route of Administration: Intravitreal Delivery Gaining Traction

Sub-retinal injection dominated 82.54% of the X-linked retinitis pigmentosa market share in 2025, primarily due to the need for precise vector placement within the outer nuclear layer for effective photoreceptor targeting. A typical procedure lasts 90 minutes and carries a 3-5% risk of detachment.

Capsid engineering has created opportunities for intravitreal injections, which could reduce operating room time to 15 minutes and significantly increase throughput. REGENXBIO’s surface-modified AAV8 demonstrated photoreceptor transduction at titers one-tenth of those required for sub-retinal injections, encouraging sponsors to shift toward outpatient settings. If real-world efficacy aligns with surgical vectors, intravitreal delivery could challenge sub-retinal dominance before 2031.

By End User: Academic Centers Lead, Integrated Chains Expand

Hospitals and branded eye-care chains captured nearly half of the X-linked retinitis pigmentosa market in 2025, leveraging established reimbursement systems and advanced robotic suites for complex retinal cases. Academic institutions, the fastest-growing segment at a 14.69% CAGR, benefit from registries that reduce enrollment timelines by 40% and philanthropic grants that offset uncompensated care costs.

Chains such as Kaiser Permanente negotiate volume-based discounts and use their broad reach to manage payer risk pools. Community practices continue to face challenges, with only 15% equipped with surgical microscopes compatible with sub-retinal delivery, reinforcing referral patterns to tertiary centers.

Geography Analysis

In 2025, North America commanded 41.13% of the X-linked retinitis pigmentosa market size, supported by 19 active trial sites and two CMS reimbursement pilots. The U.S. Orphan Drug Act provides a waiver of USD 3.2 million in FDA fees and grants seven years of exclusivity, reducing sponsor breakeven points. Additionally, Canada’s CAD 1.4 billion rare-disease drug strategy acts as a significant payer anchor, offering conditional coverage for gene therapies that meet Health Canada’s Notice of Compliance with Conditions pathway.

Europe held a 32% share, but pricing varies threefold across member states due to distinct cost-per-QALY thresholds applied by HTA agencies. For example, Germany’s IQWiG limits willingness-to-pay at EUR 80,000 (USD 93,655.60), while England’s NHS adjusts thresholds for ultra-orphan drugs. These adjustments lead to parallel negotiations, extending launch timelines by an average of nine months. GenSight’s LUMEVOQ experience highlights this disparity: reimbursed in France and Italy within a year but still delayed in Spain as of 2026.

Asia-Pacific, currently at 18%, is the fastest-growing region with a 14.58% CAGR, driven by China’s inclusion of 85 rare-disease drugs in its National Reimbursement List and Japan’s SAKIGAKE pathway, which grants conditional approval after Phase II data. South Korea’s 2024 Rare Disease Act requires the National Health Insurance Service to reimburse 80% of therapy costs for patient populations under 20,000, effectively supporting upcoming X-linked retinitis pigmentosa launches. Latin America and the Middle East & Africa remain in early stages, hindered by limited surgical capacity and fragmented payer systems, but early regulatory developments are evident, such as ANVISA’s priority review for three ocular gene therapies in 2024.

Competitive Landscape

The clinical pipeline includes numerous developers, with none exceeding a 15% share, which categorizes the x-linked retinitis pigmentosa market as moderately fragmented. Leading players in gene therapy, such as MeiraGTx, REGENXBIO, and Spark Therapeutics, primarily compete based on vector potency and surgical simplicity. MeiraGTx has constructed a 150,000-square-foot GMP facility in Amsterdam capable of producing 200 AAV batches annually. Smaller firms, however, rely on CDMOs, which face 18-month wait times and per-batch costs reaching up to USD 4 million.

Optogenetic competitors, led by Nanoscope and GenSight, focus on patient groups excluded by anti-AAV antibodies. Ray Therapeutics raised USD 125 million in 2024 to develop an opsin that activates under ambient light, eliminating the need for external equipment and improving patient convenience. Allogeneic stem-cell developers, such as BlueRock, target late-stage diseases but must demonstrate cost-effectiveness compared to single-dose gene therapies, which already benefit from payer pilot programs.

Regulatory designations further segment the field. Programs with Regenerative Medicine Advanced Therapy status benefit from rolling submissions and extensive FDA feedback, reducing approval timelines by 18-24 months. Cross-licensing agreements, particularly between Beam and CRISPR Therapeutics, are lowering IP costs and may drive the development of hybrid pipelines that combine gene replacement with precision editing.

X-linked Retinitis Pigmentosa Industry Leaders

MeiraGTx Holdings PLC

Nanoscope Therapeutics Inc.

GenSight Biologics S.A

4D Molecular Therapeutics Inc.

Beacon Therapeutics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: MeiraGTx reacquired worldwide rights to botaretigene sparoparvovec from Johnson & Johnson, regaining full control of commercialization and manufacturing.

- January 2026: Nanoscope Therapeutics completed its rolling BLA for MCO-010 after five-year safety data in 18 patients showed no serious ocular inflammation.

- November 2025: MeiraGTx and Janssen finalized enrollment in the 60-patient Phase III LUMEOS trial; 12-month read-outs are expected in Q2 2026.

- September 2025: Beacon Therapeutics reported sustained low-luminance visual-acuity gains out to 36 months in Phase II SKYLINE trial participants treated with laru-zova.

Global X-linked Retinitis Pigmentosa Market Report Scope

As per the scope of the report, X-Linked Retinitis Pigmentosa (XLRP) is a severe, inherited retinal disease that causes progressive vision loss, typically starting with night blindness and leading to legal blindness, often by age 40. It is primarily caused by mutations in the RPGR gene on the X chromosome, affecting males (who have one X chromosome) more severely, though it can affect females as well.

The X-linked retinitis pigmentosa market is segmented by therapy type, stage of development, route of administration, and end-user. By therapy type, the market includes gene therapy, pharmacological agents, optogenetics, stem cell therapies, and others. By stage of development, the market is segmented into discovery & preclinical, phase I/II, phase III, and approved/commercial. By route of administration, the market is segmented into sub-retinal, intravitreal, oral/systemic, and others. By end-user, the market is segmented into hospitals & eye-care chains, academic & research institutes, and specialty clinics. By Geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Gene Therapy |

| Pharmacological Agents |

| Optogenetics |

| Stem Cell Therapies |

| Others |

| Discovery & Preclinical |

| Phase I/II |

| Phase III |

| Approved/Commercial |

| Sub-retinal |

| Intravitreal |

| Oral/Systemic |

| Others |

| Hospitals & Eye-care Chains |

| Academic & Research Institutes |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Therapy Type | Gene Therapy | |

| Pharmacological Agents | ||

| Optogenetics | ||

| Stem Cell Therapies | ||

| Others | ||

| By Stage of Development | Discovery & Preclinical | |

| Phase I/II | ||

| Phase III | ||

| Approved/Commercial | ||

| By Route of Administration | Sub-retinal | |

| Intravitreal | ||

| Oral/Systemic | ||

| Others | ||

| By End User | Hospitals & Eye-care Chains | |

| Academic & Research Institutes | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the X-linked Retinitis Pigmentosa market expected to grow through 2031?

The X-linked Retinitis Pigmentosa market size is set to climb from USD 348.94 million in 2026 to USD 630.47 million by 2031, reflecting a 12.56% CAGR.

Which therapy type dominates current revenues?

Gene replacement held 82.34% of X-linked Retinitis Pigmentosa market share in 2025, thanks to multiple late-stage AAV8-RPGR programs.

What is the leading delivery route, and why could that change?

Sub-retinal injection controlled 82.54% of 2025 revenue, but intravitreal vectors are on a 15.55% CAGR trajectory that could erode this lead by 2031.

Which region offers the fastest market expansion?

Asia-Pacific is projected to grow at 14.58% CAGR to 2031, driven by China's reimbursement reforms and Japan's SAKIGAKE pathway.

How concentrated is the competitive landscape?

The top five pipeline players own about half the active programs, yielding a moderate concentration score of 5 on a 1-10 scale.

Page last updated on: