Waterborne Epoxy Resin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

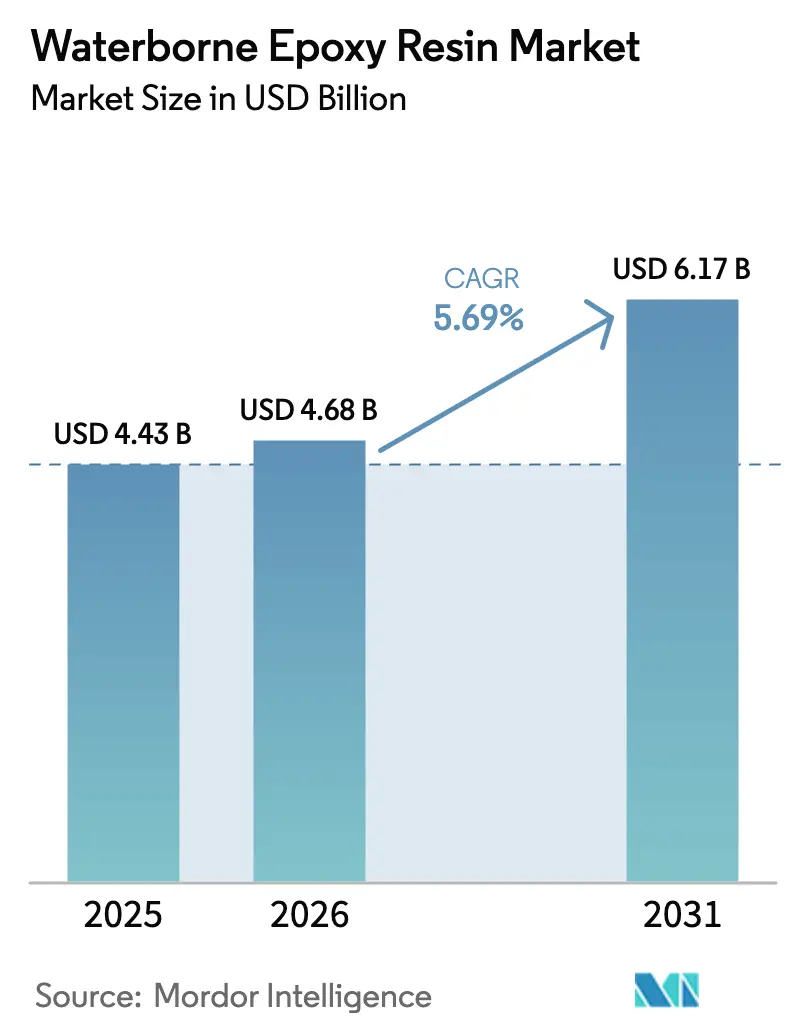

| Market Size (2026) | USD 4.68 Billion |

| Market Size (2031) | USD 6.17 Billion |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

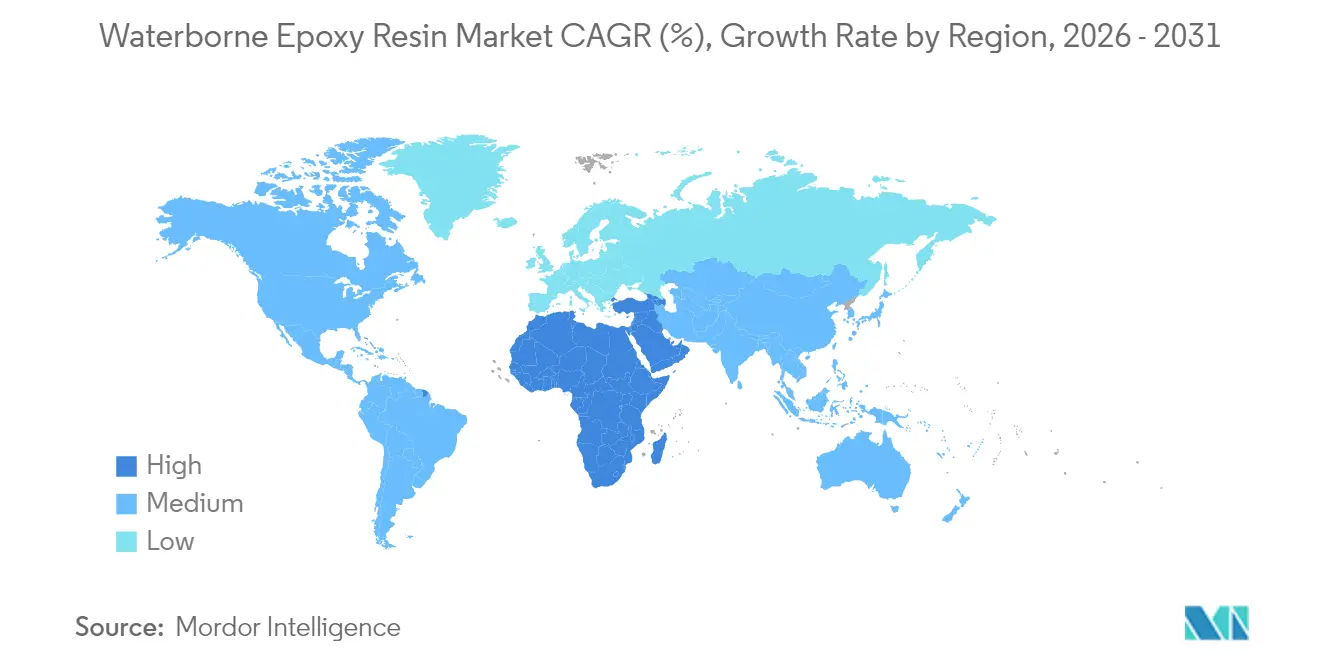

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Waterborne Epoxy Resin Market Analysis by Mordor Intelligence

Waterborne Epoxy Resin Market size in 2026 is estimated at USD 4.68 billion, growing from 2025 value of USD 4.43 billion with 2031 projections showing USD 6.17 billion, growing at 5.69% CAGR over 2026-2031. This performance highlights the sector’s shift toward low-emission chemistries in response to tightening volatile organic compound regulations, increasing renewable energy investment, and advancements in bio-based feedstocks. Increasing adoption of water-dilutable binders in automotive refinish, infrastructure coatings, and electronic encapsulation reinforces demand, while capacity additions in the Asia Pacific and North America sustain supply resilience. Product innovation centered on bio-circular raw materials, nano-reinforced films, and rapid-cure additives sustains competitive differentiation; however, raw-material cost fluctuations and technical gaps in heavy-duty anticorrosion systems temper growth momentum. Companies are mitigating these risks by expanding their renewable power sourcing, backward integrating critical intermediates, and forming downstream application alliances, positioning the waterborne epoxy resin market for broad-based, regulation-led expansion.

Key Report Takeaways

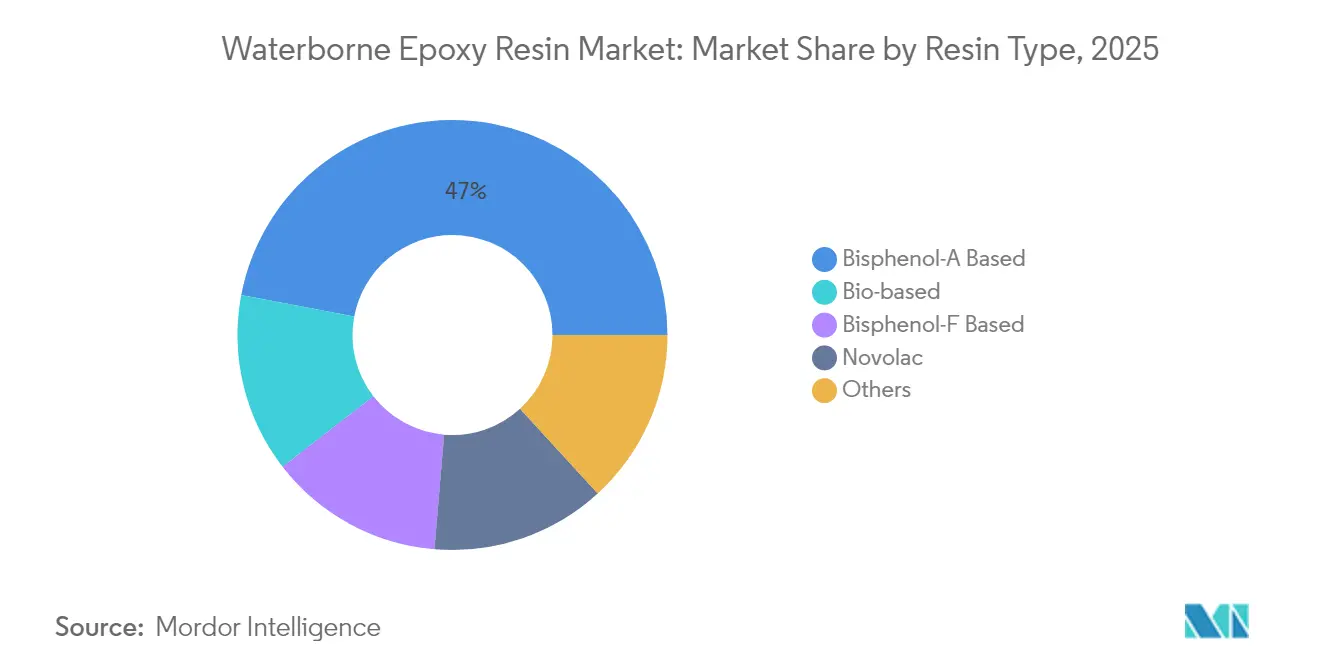

- By resin type, bisphenol-A grades retained 47.02% of the waterborne epoxy resin market share in 2025, while bio-based grades are projected to expand at a 6.73% CAGR through 2031.

- By curing-agent chemistry, amine systems led with 38.01% revenue share in 2025; phenolic systems are expected to record the fastest 5.98% CAGR to 2031.

- By application, paints and coatings contributed 44.20% share of the waterborne epoxy resin market size in 2025; adhesives and sealants are anticipated to grow at a 6.14% CAGR during 2026-2031.

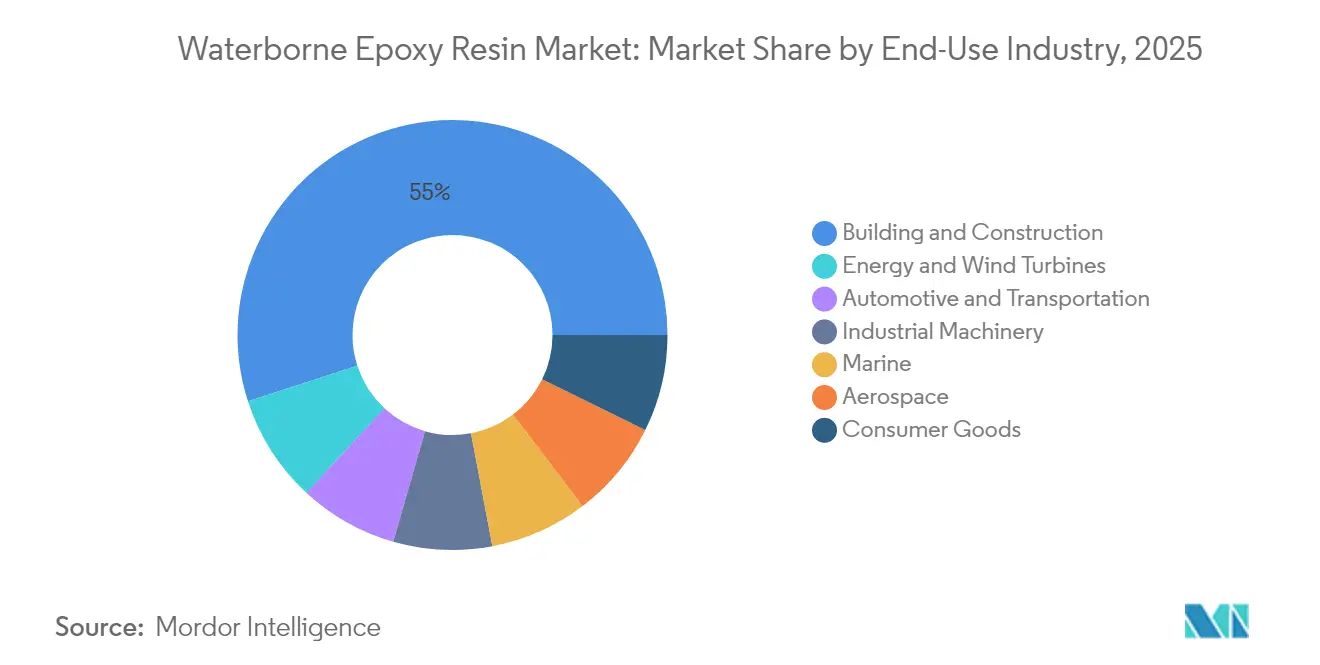

- By end-use industry, building and construction accounted for 54.98% of demand in 2025; energy and wind turbines are forecast to expand at a 6.67% CAGR to 2031.

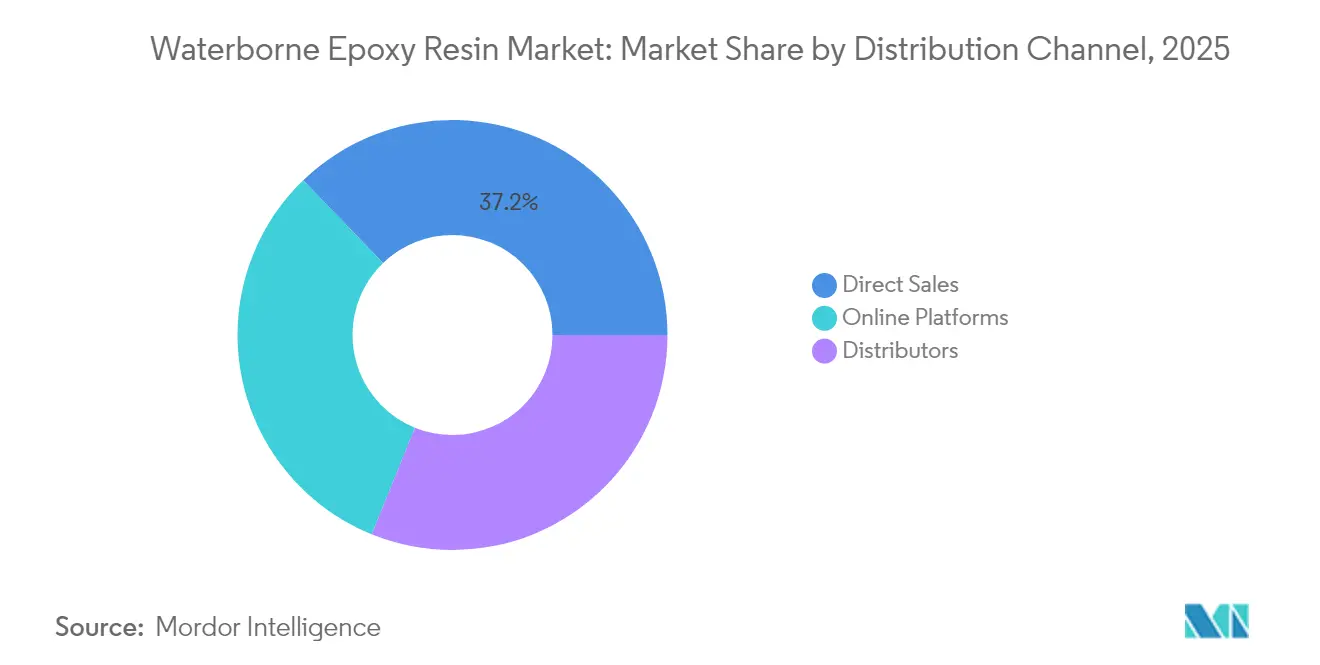

- By distribution channel, direct sales retained 37.22% of the waterborne epoxy resin market share in 2025, while online platforms are projected to expand at a 6.31% CAGR through 2031.

- By geography, Asia Pacific commanded 47.05% share of the waterborne epoxy resin market in 2025; the Middle East and Africa region is projected to post the quickest 6.43% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Waterborne Epoxy Resin Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| VOC-based emission limits favour waterborne systems | +1.20% | Global, with early adoption in North America and EU | Medium term (2-4 years) |

| Construction boom raising demand for low-odor interior coatings | +1.80% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Electronics encapsulation shift to halogen-free chemistries | +0.90% | Global, concentrated in APAC manufacturing hubs | Short term (≤ 2 years) |

| Offshore wind blade repair kits adopting waterborne epoxy | +0.70% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| EU circular-economy incentives for bio-based waterborne epoxy | +0.60% | Europe, with regulatory spillover to other regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

VOC-Based Emission Limits Favour Waterborne Systems

Regulators are imposing stricter VOC ceilings, prompting formulators to develop water-dilutable chemistries that satisfy compliance while maintaining film integrity. The US EPA’s revised aerosol-coating rule extended the transition deadline to January 2027, giving manufacturers time to optimise waterborne packages[1]U.S. Environmental Protection Agency, “National Volatile Organic Compound Emission Standards for Aerosol Coatings,” epa.gov . Similar momentum is evident in California’s South Coast Air Quality Management District, where Rule 1151 mandates waterborne automotive refinish systems by 2033[2]South Coast Air Quality Management District, “Rule 1151 Automotive Refinish Coatings,” aqmd.gov . European regulators follow parallel paths by lowering allowable solvent thresholds in industrial maintenance paints, stimulating demand for zero-solvent epoxy dispersions. Producers are increasingly leveraging renewable electricity and high-solid feedstocks to reduce their total carbon footprints and meet corporate net-zero pledges, creating a virtuous cycle that accelerates uptake across the waterborne epoxy resin market.

Construction Boom Raising Demand for Low-Odor Interior Coatings

Rapid urbanization, coupled with worker safety mandates, fuels interest in low-smell, low-toxic coatings for commercial buildings, hospitals, and residential towers. National infrastructure plans across India, Indonesia, and GCC states prioritise green building certifications that reward low-emission materials. Contractors select waterborne epoxy primers and self-leveling flooring compounds because they reduce ventilation requirements and accelerate job-site turnaround. Building-material suppliers now bundle epoxies with antimicrobial additives to meet post-pandemic hygiene criteria and secure specifications in healthcare projects, thereby deepening the penetration of the waterborne epoxy resin market.

Electronics Encapsulation Shift to Halogen-Free Chemistries

Semiconductor and consumer-electronics producers are eliminating brominated and chlorinated compounds to meet RoHS directives. Waterborne epoxy-powder coatings, such as CAPLINQ’s GCP 1805, already carry UL 94 V-0 ratings and demonstrate thermal cycling endurance suitable for automotive modules. Portable-device makers value the negligible VOC profile, which reduces the risk of cleanroom contamination and enables thinner, optically clear layers over LEDs and sensors. These benefits drive fast-track qualification of waterborne systems in Asia-based outsource semiconductor assembly and test facilities, galvanising demand throughout the waterborne epoxy resin market.

EU Circular-Economy Incentives for Bio-Based Waterborne Epoxy

The European Commission’s Green Deal offers tax breaks and public procurement preferences for bio-renewable polymers, creating a demand pull for soy-, lignin-, or sugar-based epoxy monomers. Arkema’s mass-balance certified grades, which deliver up to 100% carbon footprint reduction, illustrate commercial traction at arkema.com. Similar programmes spread to Canada and Japan, ensuring long-term support for sustainable chemistry platforms across the waterborne epoxy resin market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance gap vs. solvent-borne in heavy-duty anti-corrosion | -1.40% | Global, particularly in marine and industrial applications | Medium term (2-4 years) |

| Price volatility | -0.80% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| Nano-silica solvent-free PU top-coats cannibalising epoxy share | -0.70% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Performance Gap vs. Solvent-Borne in Heavy-Duty Anti-Corrosion

Waterborne epoxies still lag behind solvent-borne rivals in the barrier properties required by ships and offshore platforms. Moisture presence during film formation can create micro-porosity that lowers impedance values. Comparative studies show that solvent-borne coatings maintain resistance above 10^9 Ω after extended salt-spray exposure, whereas waterborne equivalents plateau at a value nearer 10^8 Ω, necessitating thicker builds or more frequent maintenance. International Marine’s low-VOC product lines have helped mitigate part of this gap, yet applicators remain cautious about life-cycle costs, constraining uptake in the waterborne epoxy resin market.

Price Volatility and Nano-Silica Solvent-Free PU Top-Coats

Bisphenol-A and epichlorohydrin prices fluctuate with crude-oil shifts and downstream supply outages, pressuring formulators’ margins. At the same time, nano-silica-filled solvent-free polyurethanes are positioning themselves as direct substitutes by offering similar abrasion resistance without water sensitivity. UV-curable epoxy-modified silicone hybrids now deliver 95% light transmission and 5H hardness, narrowing the performance gap while retaining near-zero VOC[3]MDPI, “UV-Cured Epoxy-Modified Silicone Coatings With High Transparency,” mdpi.com . Budget-constrained buyers may favour these alternatives, limiting near-term penetration of premium waterborne technologies in certain regions of the waterborne epoxy resin market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Bio-Based Innovation Drives Sustainability Transition

Bisphenol-A resins dominated the 2025 waterborne epoxy resin market with a 47.02% share. Their established supply chains, predictable cure behaviour, and wide formulation latitude underpin leadership. Yet market sentiment is shifting. Bio-based chemistries built from lignin, tall-oil fatty acids, and sugar derivatives are growing at a 6.73% CAGR as regulators incentivise circular raw materials and brand owners seek low-carbon footprints. The European Green Deal channels funding toward demonstration plants that scale bio-epoxy dispersion output for coatings and electronics, driving diversification within the waterborne epoxy resin industry.

Bisphenol-F variants offer lower viscosity and improved electrical insulation, making them suitable for high-layer-count printed circuit boards. Novolac epoxies fulfil heat-resistance mandates in aerospace composites. Researchers have developed bisphenol-free diepoxide monomers with a thermal conductivity of 0.4 W/m · K, easing heat management challenges in electric vehicle battery packs. This breadth of options secures innovation momentum across the waterborne epoxy resin market, even as fossil-based incumbents guard volume share.

By Curing-Agent Chemistry: Amine Systems Dominate Despite Phenolic Growth

Amine-based hardeners held 38.01% of the 2025 demand in the waterborne epoxy resin market. They cure at ambient temperature, offer broad substrate adhesion, and tolerate variable humidity, making them the default for flooring, primers, and electronic encapsulation. Producers have decreased residual free amine content to enhance worker safety and reduce odour. Phenolic adducts, although comprising a smaller share, will log a 5.98% CAGR through 2031, thanks to their high chemical and thermal resistance, which is valued in tank linings and high-speed rail infrastructure.

Anhydride chemistries remain niche, targeting high-temperature composites. Hybrid bio-amine hardeners, utilizing amino acids such as tryptophan, have demonstrated comparable tensile performance while reducing carbon footprints, aligning with customer decarbonization roadmaps. Evonik’s VESTAMIN IPD eCO employs biomass-balanced ammonia to slash cradle-to-gate emissions. These advances broaden the toolkit available to formulators across the waterborne epoxy resin market.

By Application: Paints and Coatings Lead While Adhesives Accelerate

Paints and coatings accounted for 44.20% of the 2025 volume, reflecting the large-scale deployment in architectural interiors, concrete floors, and the use of corrosion-resistant primers. Contractors prefer low-smell water-dilutable binders that can reopen spaces within 24 hours, lowering labour overheads. Regulatory VOC caps below 250 g/L in California expedite migration from solvent-borne grades, reinforcing the dominance of this application category within the waterborne epoxy resin market.

Adhesives and sealants are expected to record a 6.14% CAGR as vehicle lightweighting, battery pack bonding, and flexible circuit lamination adopt high-strength, flame-retardant waterborne systems. Electronics encapsulation leverages the near-zero ionic contamination and optical clarity of aqueous dispersions, which are essential for reliability in advanced driver-assistance systems. Composites, inks, and 3D-printing resins form smaller but growing niches that reward custom functionality such as dielectric strength or rapid thermal cycling endurance.

By End-Use Industry: Construction Dominance Meets Energy Sector Dynamism

Building and construction represented 54.98% of 2025 consumption and remains the cornerstone of the waterborne epoxy resin market. Mega-projects, such as smart-city corridors, mass-transit hubs, and logistics parks, specify low-VOC coatings and self-leveling floors that reduce indoor air quality risks and support green building certification. Civil engineering codes in Europe now credit waterborne epoxy systems toward embodied carbon targets, providing regulatory impetus.

Energy—especially offshore wind—displays the highest 6.67% CAGR. Blade fabricators and service contractors specify waterborne repair pastes that cure at ambient temperature, allowing short weather windows for maintenance. The automotive and transportation segment benefits from electric-vehicle battery encapsulation, where water-processed dielectric layers enhance thermal dissipation and fire safety. Marine and aerospace remain specialized outlets, demanding high-barrier film builds that are still under active research in the waterborne epoxy resin industry.

By Distribution Channel: Direct Sales Prevail While Online Platforms Surge

Direct selling accounted for 37.22% of 2025 revenue, as complex formulation support and on-site troubleshooting remain critical for the successful application of waterborne epoxies. Resin suppliers operate pilot lines and mobile lab services to fine-tune cure profiles, substrate preparation, and spray parameters, ensuring high-quality outcomes in the waterborne epoxy resin market.

Online platforms are expected to post a 6.31% CAGR, reflecting digital procurement trends. Buyers can access real-time inventory, searchable technical data sheets, and virtual application support, which reduces cycle times for small-batch orders. Hybrid models that combine e-commerce with local distributor warehousing are emerging, particularly in Southeast Asia and Latin America, thereby widening reach without sacrificing technical service breadth.

Geography Analysis

The Asia Pacific region held 47.05% of the global 2025 sales value, anchored by robust manufacturing bases in China, India, and Southeast Asia. China remains the largest producer and consumer, despite preliminary dumping margins being imposed on exports to the United States. Local infrastructure upgrades, semiconductor fab expansion, and electric-vehicle output sustain domestic offtake. India’s Smart Cities Mission and national expressway plan unlock multi-year flooring and waterproofing demand, propelling the regional waterborne epoxy resin market. Multinational suppliers continue to localise capacity; Evonik will bring a specialty amine plant online in Nanjing by 2026 to serve regional formulators.

North America is a significant consumer of coatings. Progressive VOC legislation and decarbonisation programmes encourage rapid conversion to water-dilutable coatings. California’s Rule 1151 revisions prescribe waterborne refinishing by 2033, setting a nationwide compliance benchmark. Wind-farm repowering and US-Mexico-Canada trade stability support long-term demand visibility. BASF’s shift to 100% renewable electricity in key North American sites demonstrates supplier commitment to sustainable operations.

Europe occupies a technology leadership role. The region shapes global standards through Green Deal regulations and carbon-border-adjustment mechanisms that favour low-footprint chemistries. Mass-balance-certified resins, waste-derived bio-feedstocks, and closed-loop collection of construction debris gain traction. Offshore wind capacity additions in the North Sea require erosion-resistant, fast-cure repair epoxies, lifting regional demand.

The Middle-East and Africa, though smaller, will expand at a 6.43% CAGR. National diversification agendas in Saudi Arabia and the United Arab Emirates prioritise downstream chemical production and high-performance building materials, stimulating offtake. Government investment in desalination plants and petrochemical complexes necessitates corrosion-resistant waterborne coatings, bolstering the regional waterborne epoxy resin market.

Competitive Landscape

The waterborne epoxy resin market is moderately fragmented. Global chemical majors leverage scale economies, integrated raw material positions, and application laboratory networks to defend their market share. Small and mid-sized innovators carve niches through bio-based chemistries and user-specific performance packages. Competitive intensity is rising as sustainability goals elevate switching incentives for downstream users. Strategic alliances are proliferating. Resin suppliers collaborate with wind-turbine OEMs to co-develop erosion-resistant blade repair kits, while electronics conglomerates sign joint-development agreements for halogen-free encapsulation powders. Producers also invest in renewable energy procurement and life-cycle analysis tools to differentiate their carbon footprints. Market participants that align product innovation with verifiable sustainability metrics are best positioned to capture share in the evolving waterborne epoxy resin market.

Waterborne Epoxy Resin Industry Leaders

Allnex Netherlands B.V.

Arkema

BASF SE

Dow

Huntsman International LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tnemec has launched Series 288 and Series 289 Enviro-Pox, advanced waterborne epoxies designed for high-performance flooring and wall coatings. This development is poised to strengthen innovation and competition within the waterborne epoxy resin market.

- March 2025: Westlake launched its EpoVIVE portfolio at ECS 2025, highlighting innovations in waterborne epoxy resins. These advancements focus on reducing carbon footprints through bio-circular materials and feature AQUAREOUS epoxy systems designed for low VOC coatings.

Global Waterborne Epoxy Resin Market Report Scope

Waterborne epoxy resin, an eco-friendly polymer coating, primarily uses water as its solvent, significantly curbing emissions of volatile organic compounds (VOCs) compared to traditional organic solvents. The waterborne epoxy resin market is segmented by resin type, curing-agent chemistry, application, end-use industry, distribution channel, and geography. By resin type, the market is segmented into Bisphenol-A-based, Bisphenol-F-based, Novolac, bio-based resins, and other variants. By curing-agent chemistry, the market is segmented into amine-based, anhydride, phenolic, and others. By application, the market is segmented into paints and coatings, adhesives and sealants, composites, inks, electrical and electronics encapsulation, and others. By end-use industry, the market is segmented into building and construction, automotive and transportation, industrial machinery, aerospace, marine, consumer goods, and energy and wind turbines. By distribution channel, the market is segmented into direct sales, distributors, and online platforms. The report also covers the market size and forecasts for the waterborne epoxy resin market in 23 countries across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

| Bisphenol-A Based |

| Bisphenol-F Based |

| Novolac |

| Bio-based |

| Others |

| Amine-Based |

| Anhydride |

| Phenolic |

| Others |

| Paints and Coatings |

| Adhesives and Sealants |

| Composites |

| Inks |

| Electrical and Electronics Encapsulation |

| Others |

| Building and Construction |

| Automotive and Transportation |

| Industrial Machinery |

| Aerospace |

| Marine |

| Consumer Goods |

| Energy and Wind Turbines |

| Direct Sales |

| Distributors |

| Online Platforms |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Resin Type | Bisphenol-A Based | |

| Bisphenol-F Based | ||

| Novolac | ||

| Bio-based | ||

| Others | ||

| By Curing-Agent Chemistry | Amine-Based | |

| Anhydride | ||

| Phenolic | ||

| Others | ||

| By Application | Paints and Coatings | |

| Adhesives and Sealants | ||

| Composites | ||

| Inks | ||

| Electrical and Electronics Encapsulation | ||

| Others | ||

| By End-Use Industry | Building and Construction | |

| Automotive and Transportation | ||

| Industrial Machinery | ||

| Aerospace | ||

| Marine | ||

| Consumer Goods | ||

| Energy and Wind Turbines | ||

| By Distribution Channel | Direct Sales | |

| Distributors | ||

| Online Platforms | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the waterborne epoxy resin market?

The waterborne epoxy resin market size stood at USD 4.68 billion in 2026 and is projected to grow to USD 6.17 billion by 2031.

Which region leads consumption of waterborne epoxy resins?

Asia Pacific commands 47.05% of global demand, supported by strong construction and manufacturing activity across China, India, and Southeast Asia.

Which application segment is growing fastest?

Adhesives and sealants will advance at a 6.14% CAGR through 2031, driven by electric-vehicle bonding and electronics miniaturisation trends.

Why are VOC regulations important for this market?

Stricter VOC limits in North America and Europe compel formulators to shift from solvent-borne to water-dilutable systems, driving structural demand for waterborne epoxies.

How does bio-based chemistry influence future growth?

EU circular-economy incentives and brand owner sustainability targets foster rapid adoption of bio-based epoxy monomers, enabling lower-carbon products and opening new premium niches.

What challenges restrict full replacement of solvent-borne epoxies?

Waterborne systems still face performance gaps in extreme anticorrosion environments and are exposed to raw-material price volatility, prompting some users to retain solvent-borne or polyurethane alternatives.

Page last updated on: