Water Flosser Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.7 Billion |

| Growth Rate (2026 - 2031) | 6.80% CAGR |

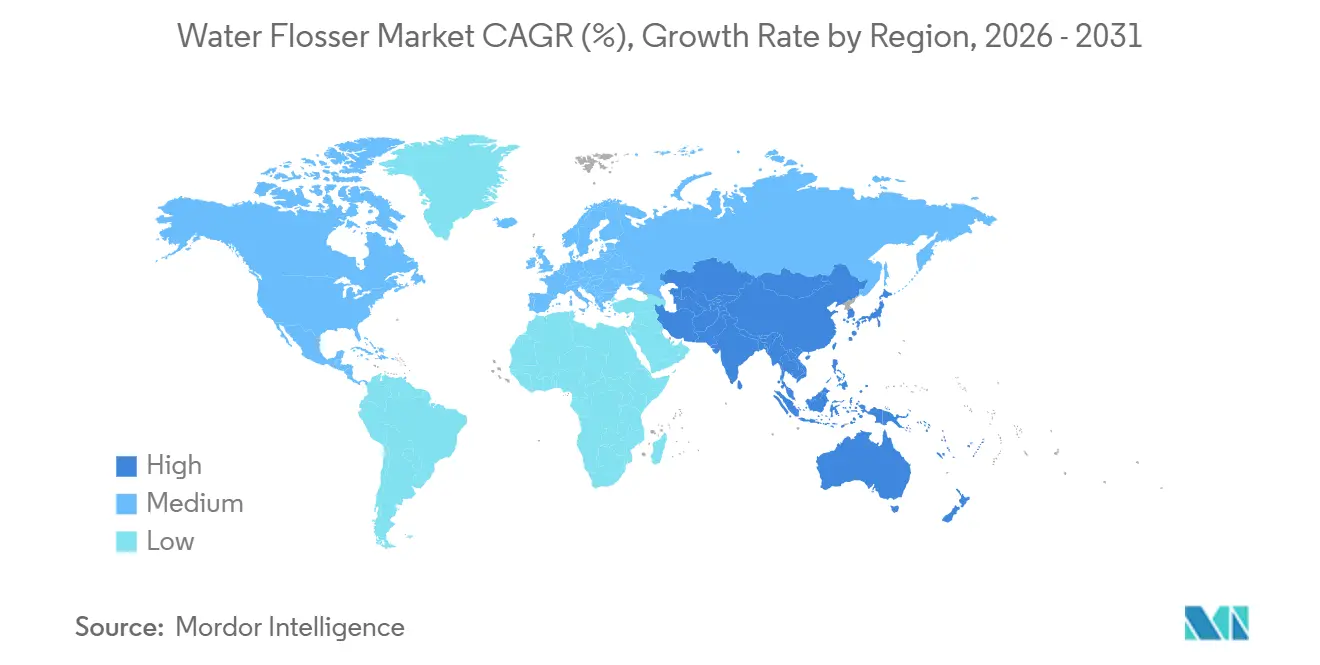

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

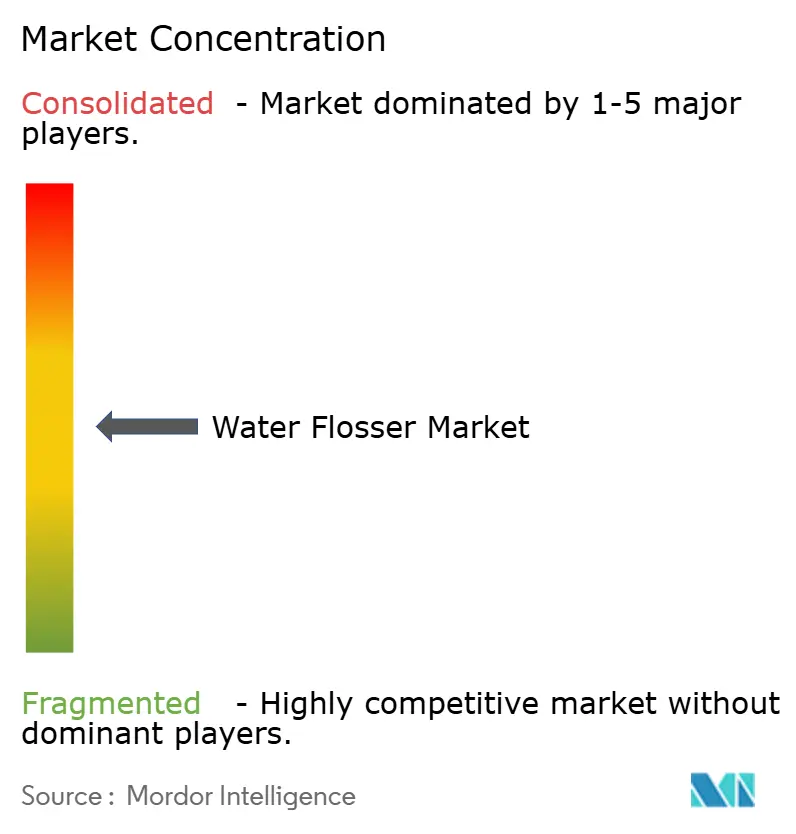

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water Flosser Market Analysis by Mordor Intelligence

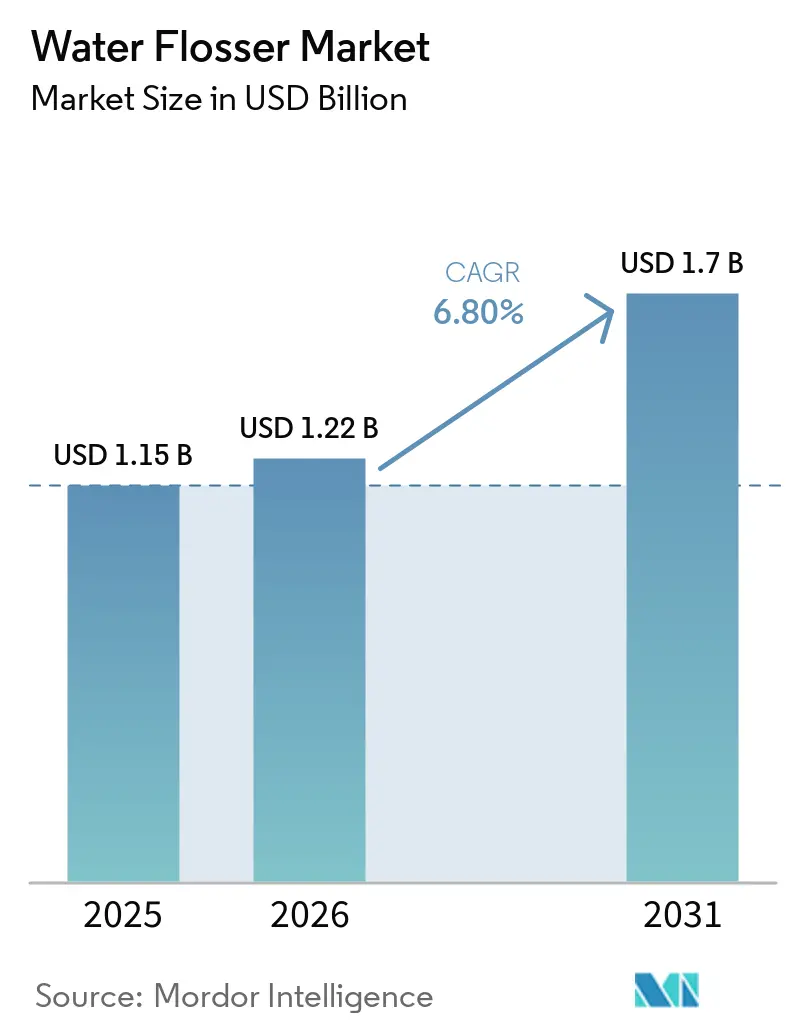

The Water Flosser Market size is expected to grow from USD 1.15 billion in 2025 to USD 1.22 billion in 2026 and is forecast to reach USD 1.7 billion by 2031 at 6.80% CAGR over 2026-2031.

The water flosser market is experiencing growth driven by increasing oral health challenges, aging populations, and a growing number of users with dental implants, braces, and other restorative needs. Global data from 2025 highlighted a significant periodontal disease burden, reinforcing the demand for preventive dental devices that integrate into daily routines rather than relying solely on clinic visits. The projected rise in severe periodontitis cases by 2035 further strengthens the role of oral irrigators as essential tools for everyday dental care. Advancements in product design, such as cordless formats, standardized charging, and improved online visibility, have enhanced accessibility for first-time users. Additionally, policy support in key markets like China and growing clinical recognition of interdental cleaning methods continue to position the water flosser market for steady growth throughout the forecast period.

Key Report Takeaways

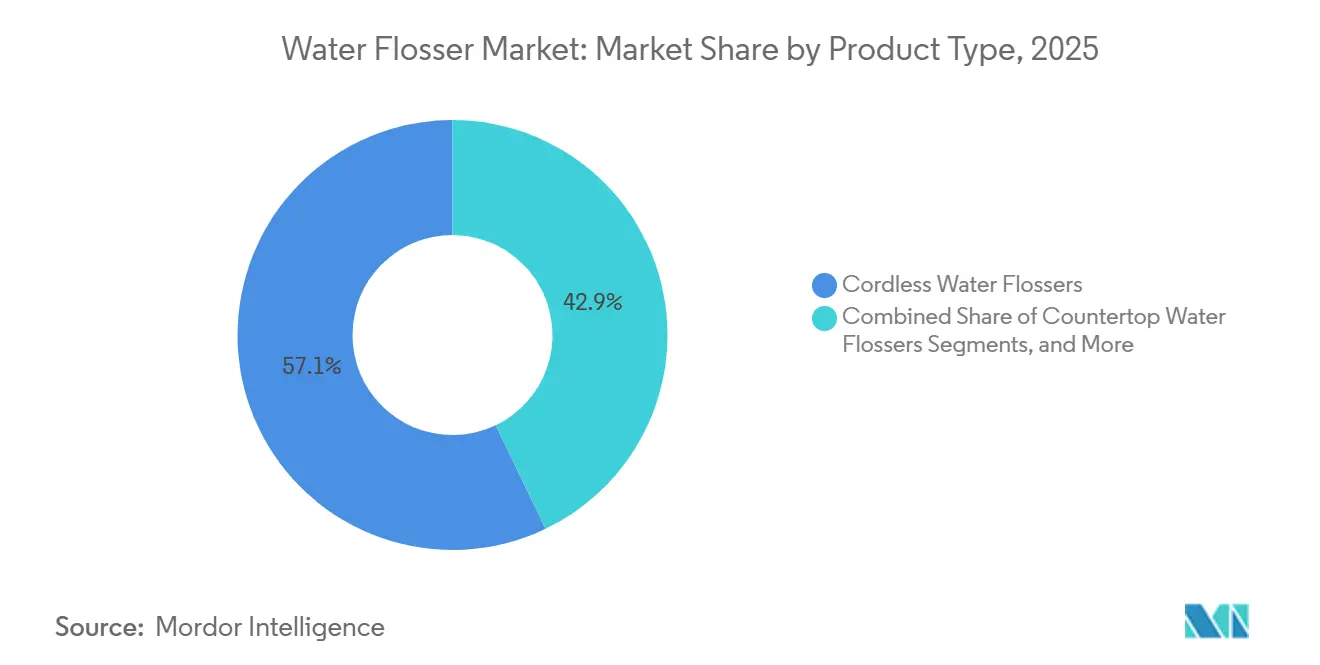

- By product type, cordless water flossers held 57.12% of the water flosser market share in 2025.

- By care setting, home care accounted for 71.7% of the water flosser market size in 2025 and is projected to grow at a 6.99% CAGR from 2026 to 2031.

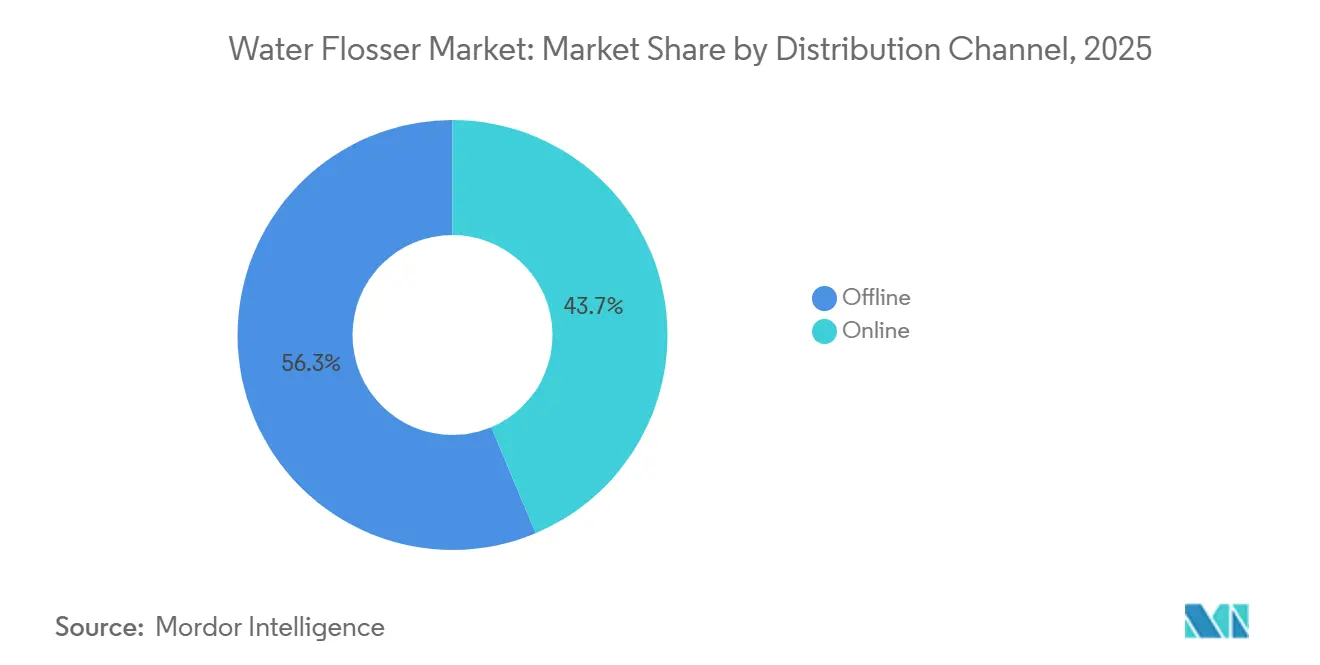

- By distribution channel, online channels captured 43.67% share in 2025 and are forecasted to expand at an 8.34% CAGR through 2031.

- By technology, battery-operated devices remained the volume leader in 2025, while electric rechargeable devices are projected to record the highest CAGR at 7.25% through 2031.

- By geography, North America held 38.47% share in 2025, while Asia-Pacific is expected to grow at the fastest pace with a 7.90% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Water Flosser Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising periodontal disease burden and prevention awareness | +1.5% | Global, with stronger relevance in China, the UK, South Asia, and Tropical Latin America | Long term (≥ 4 years) |

| Orthodontics, implants, and restorative demand supporting adjunct tool adoption | +1.0% | North America and Europe, with spillover into Asia-Pacific orthodontic centers | Medium term (2-4 years) |

| Cordless convenience and travel-friendly formats lowering adoption friction | +1.2% | North America, Asia-Pacific, and Western Europe | Short term (≤ 2 years) |

| E-commerce and DTC education improving product discovery and repeat purchase | +1.1% | Global, with stronger relevance in China, Southeast Asia, and Middle East e-commerce corridors | Medium term (2-4 years) |

| Replacement-TIP replenishment models supporting recurring revenue and upgrade cycles | +0.5% | North America, Europe, and Australia | Medium term (2-4 years) |

| Pediatric and family-oriented product expansion widening the user base | +0.7% | Asia-Pacific, North America, and the GCC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Periodontal Disease Fuels Demand for Preventive Devices

The water flosser market is increasingly driven by the growing global prevalence of periodontal disease in both developed and developing regions. Research from 2025 highlighted the widespread nature of periodontal disease, with projections indicating a continued rise in severe periodontitis cases by 2035.[1]Keke Zhang, Yingyi Ma, Jinfang Shi, and Yudong Geng, “Epidemiological Trends and Incidence Prediction of Periodontal Disease Based on the Global Burden of Disease Study 2021,” Frontiers in Dental Medicine, frontiersin.org This trend positions water flossers as essential health tools rather than convenience products. Additionally, links between periodontal disease and conditions like cardiovascular disease and diabetes strengthen clinical recommendations for improved home oral care routines, further supporting market growth.

Growing Orthodontic and Implant Treatments Broaden Market Reach

The rising number of orthodontic treatments, implant placements, and restorative dental procedures is expanding the water flosser market. Patients with fixed appliances or implants often face challenges with traditional string floss, making oral irrigators a preferred choice. Studies have shown that oral irrigators significantly improve plaque removal and reduce bleeding around implants compared to dental floss.[2]Meiling Hu, Ruibin Zhang, Ren Wang, Yan Wang, and Jincai Guo, “Global, Regional, and National Burden of Periodontal Diseases From 1990 to 2021 and Predictions to 2040, An Analysis of the Global Burden of Disease Study 2021,” Frontiers in Oral Health, pubmed.ncbi.nlm.nih.gov Manufacturers like Panasonic are addressing this demand with tailored cordless models for orthodontic, travel, and sensitive-gum needs, launched in 2025.

Cordless Innovations and Travel-Friendly Formats Drive Product Evolution

Cordless innovations are a key growth driver in the water flosser market. Portable designs cater to travel, shower, and compact living needs, overcoming barriers associated with countertop models. Features like USB-C charging and extended battery life enhance convenience, particularly for first-time buyers. Leading brands such as Waterpik are introducing affordable cordless devices with clinical positioning and user-friendly designs, while premium models with advanced features are driving upgrades across price segments.

Online Sales and Direct-to-Consumer Channels Transform Retail Dynamics

The water flosser market is undergoing a shift as online platforms dominate product discovery, sales, and repeat purchases. Digital channels enable brands to educate consumers, showcase product benefits, and offer bundled refills, which physical stores often cannot match. By 2025, online sales accounted for 43.67% of the market and are projected to grow at 8.34% annually through 2031. Brands like AquaSonic are leveraging their online success to establish offline trust through retail partnerships, creating a competitive advantage in omnichannel execution.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price premium versus string floss and interdental picks limiting first-time adoption | -0.7% | Emerging markets, including Middle East and Africa, South America, and lower-tier cities in Asia-Pacific | Medium term (2-4 years) |

| Low awareness and onboarding friction in emerging markets | -0.5% | Middle East and Africa, South America, and rural Asia-Pacific | Medium term (2-4 years) |

| Value-brand switching and tariff volatility pressuring premium-tier economics | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Counterfeit and compatibility issues in replacement tips eroding brand trust | -0.3% | Asia-Pacific, especially China and Southeast Asia, and parts of Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Premium Creates a Persistent Adoption Ceiling in High-Potential Markets

The water flosser market faces a significant challenge due to the price gap between powered devices and traditional floss products. In emerging markets, this gap often positions water flossers as non-essential, even with growing awareness and clear oral health needs. The issue is more pronounced in less-developed retail environments, where consumers prefer physical trials or professional guidance before purchasing. This slows the transition to routine use and limits household penetration. Until manufacturers reduce entry price points or public health campaigns promote daily use, adoption in these regions will likely remain below potential.

Tariff Pressure and Value-Brand Migration Disrupt Incumbent Economics

The water flosser market is under pressure from trade policy changes and consumer shifts toward value brands, particularly in premium segments. Inflation has driven some consumers away from Waterpik-branded products to lower-cost alternatives, highlighting increased price sensitivity. Additionally, supply chain adjustments tied to import exposure have added cost pressures for established brands. These factors limit reinvestment in innovation and marketing while creating opportunities for leaner competitors and private-label brands. As a result, the market has become more price-sensitive and competitive, especially in the mid-tier segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cordless formats remain the core growth engine

Cordless water flossers accounted for 57.12% of the market in 2025, highlighting the growing demand for portable devices. Consumers increasingly prefer products that fit into travel, shower routines, and compact spaces. The market has responded with innovations like compact reservoirs, easy refilling, and extended battery life, addressing concerns about frequent power loss. Cordless models now dominate as the primary entry point for new users, aligning with daily habits and supporting premium upgrades.

Countertop models remain relevant for households with multiple users and those prioritizing larger reservoirs for extended cleaning sessions. Faucet-attached and shower-attached formats cater to niche markets with limited counter space. The market is shifting towards feature segmentation, with cordless devices leading due to their practicality and alignment with consumer preferences.

By Care Setting: Home care remains dominant while clinical channels shape premium conversion

Home care held a 71.7% share in 2025, driven by devices tailored for individual use and supported by retail, e-commerce, and clinician recommendations. The segment is projected to grow at 6.99% through 2031, indicating continued expansion potential. Home care remains the cornerstone of the market, emphasizing repeat use over occasional clinical exposure.

Dental clinics, while a smaller segment, play a strategic role in converting patients through professional recommendations, especially for braces, implants, and gum-sensitive users. Hospitals and orthodontic centers enhance credibility by addressing advanced oral hygiene needs. The synergy between home care and clinical guidance strengthens the market by combining scale with premium adoption.

By Distribution Channel: Online sales lead discovery and repeat purchase

Online channels captured 43.67% of sales in 2025 and are expected to grow at an 8.34% CAGR from 2026 to 2031. Digital platforms excel in educating consumers through product comparisons, videos, and reviews, while also driving recurring revenue through accessory sales. The online channel has become central to category expansion, offering speed and flexibility in brand visibility.

Offline retail remains important for consumers who prefer hands-on evaluation, particularly in developing markets. Physical stores also help newer brands establish credibility. The market increasingly favors integrated channel models that combine content, direct sales, and repeat purchases, with online platforms leading growth.

By Technology: Rechargeable devices set the pace for future upgrades

Battery-operated devices dominated in 2025 as an accessible entry point, but the market is shifting towards rechargeable formats. Rechargeable devices, projected to grow at a 7.25% CAGR from 2026 to 2031, offer advanced features like smarter pressure control and longer battery life, aligning with sustainability trends and premium pricing strategies.

USB-C standardization and improved battery designs enhance convenience and reliability, making rechargeable devices the focus of future growth. While manual pump-action devices serve budget-conscious users, the value pool is increasingly concentrated in rechargeable platforms, which drive differentiation and premium adoption in the market.

Geography Analysis

In 2025, North America accounted for 38.47% of the water flosser market, maintaining its position as the leading revenue generator. The United States drives this dominance due to established dental professional recommendation networks and the ADA's endorsement of oral irrigators, which build trust among users. Canada and Mexico offer growth potential, particularly in improving distribution and language-specific education. The region is transitioning from early adoption to a premium replacement cycle, with users upgrading to advanced rechargeable models.

Asia-Pacific is projected to grow at a 7.90% CAGR through 2031, the fastest among all regions. China leads this growth, supported by favorable policies, an expanding urban middle class, and digital commerce. Rising awareness of preventive oral care further fuels market expansion, with growth driven by new user additions rather than premium upgrades.

Europe's growth is influenced by regulatory-driven product redesigns, such as replaceable batteries and recyclable materials, which enhance premium positioning despite higher costs. The Middle East and Africa, though smaller in size, benefit from younger populations, rising disposable incomes, and improved online retail access in Gulf markets. In South America, Brazil and Argentina are driving adoption beyond affluent households, supported by the region's need for better preventive oral care. Globally, the market reflects a divide between revenue concentration in mature economies and faster unit growth in developing regions.

Competitive Landscape

The water flosser market is moderately concentrated at the branded level but remains fragmented when private-label and OEM suppliers are included across various price tiers. Waterpik, Koninklijke Philips N.V., and Panasonic dominate the premium segment through strong brand recognition, diverse product portfolios, and clinical trust. Waterpik holds a leading position in the U.S. market due to professional endorsements, while Panasonic expands its offerings to cater to portable, sensitive-gum, and travel needs. This creates a premium layer led by established brands, even as the broader market remains dispersed.

Competition is intensifying as lower-cost competitors leverage digital marketing, faster product refresh cycles, and flexible sourcing models. The mid-tier segment has become particularly dynamic, with consumers comparing price, battery life, portability, and accessories within narrow decision windows. Tariff fluctuations and inflationary pressures have increased the vulnerability of premium brands to value-driven consumer shifts, leading to a mix of premium brand dominance and pricing fragmentation in the market.

Strategic initiatives by key players reflect the market's evolution. Waterpik’s launch of the Cordless 1100 in June 2025 targeted budget-conscious first-time users, while the PROMAX, introduced in March 2026, focused on high-end countertop innovations with advanced features. Panasonic’s release of three cordless models in May 2025 highlighted its strategy to address diverse user needs. AquaSonic’s entry into Target stores in February 2026 demonstrated the transition of digitally-native brands into physical retail. These developments underscore the market's focus on price accessibility, feature innovation, and channel expansion.

Water Flosser Industry Leaders

Koninklijke Philips N.V.

Aquapick Co., Ltd.

Panasonic Holdings Corporation

The Procter & Gamble Company (Oral-B)

Church & Dwight Co., Inc. (Water Pik, Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Waterpik (Church & Dwight) launched the PROMAX Water Flosser with SMARTADVANCE mode, which adjusts water intensity over two weeks and is clinically proven to reverse gum bleeding in six weeks. Priced at USD 149.99, it is Waterpik's most feature-rich countertop model, targeting premium, medically-anchored positioning.

- February 2026: AquaSonic expanded its retail footprint by entering hundreds of Target stores nationwide, offering its Precision series, including an electric flosser, at approximately USD 40.

- June 2025: Waterpik introduced the Cordless 1100, its most affordable cordless water flosser with ADA Seal of Acceptance, featuring PRECISIONPULSE technology and a compact design for small sinks and showers, aimed at first-time buyers.

- May 2025: Panasonic Australia launched three cordless water flossers: the EW-DJ66 with ultrasonic microbubble technology, the EW-DJ27 for sensitive gums, and the travel-friendly EW-DJ11, targeting clinical, sensitive, and portable sub-segments.

Global Water Flosser Market Report Scope

As per the scope of the report, a water flosser (often called a dental water jet or oral irrigator) is a handheld electronic device that shoots a targeted, pulsing stream of pressurized water. It is designed to flush out food particles and dislodge plaque from between your teeth and along your gumline.

The water flosser market is segmented by product type, care setting, distribution channel, technology, and geography. By product type, the market includes cordless water flossers, countertop water flossers, faucet-attached water flossers, and shower-attached water flossers. By care setting, the market is segmented into home care, dental clinics, hospitals, and orthodontic care centers. By distribution channel, the market is categorized into online and offline. By technology, the market is segmented into battery-operated, electric (rechargeable), and manual pump action. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Cordless Water Flossers |

| Countertop Water Flossers |

| Faucet-Attached Water Flossers |

| Shower-Attached Water Flossers |

| Home Care |

| Dental Clinics |

| Hospitals |

| Orthodontic Care Centers |

| Online |

| Offline |

| Battery Operated |

| Electric (Rechargeable) |

| Manual Pump Action |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Cordless Water Flossers | |

| Countertop Water Flossers | ||

| Faucet-Attached Water Flossers | ||

| Shower-Attached Water Flossers | ||

| By Care Setting | Home Care | |

| Dental Clinics | ||

| Hospitals | ||

| Orthodontic Care Centers | ||

| By Distribution Channel | Online | |

| Offline | ||

| By Technology | Battery Operated | |

| Electric (Rechargeable) | ||

| Manual Pump Action | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the water flosser market?

The water flosser market size is USD 1.22 million in 2026 and is projected to reach USD 1.70 million by 2031, growing at a 6.80% CAGR over the forecast period.

Which product type leads sales in water flossers?

Cordless water flossers lead the category with 57.12% share in 2025, supported by easier portability, travel use, and stronger fit with daily home routines.

Which sales channel is growing the fastest for water flossers?

Online channels are the fastest-growing route to market, with an 8.34% CAGR from 2026 to 2031, while already accounting for 43.67% of sales in 2025.

Why are oral irrigators gaining more clinical relevance?

Clinical studies cited in the draft show better outcomes in orthodontic and implant-related use cases, while periodontal disease remains a large and rising global burden.

Which region has the strongest growth outlook?

Asia-Pacific has the fastest regional growth outlook at a 7.90% CAGR through 2031, while North America remains the largest regional market with 38.47% share in 2025.

What is limiting faster adoption in some countries?

The main barriers are higher device prices versus string floss, onboarding friction for first-time users, and greater price sensitivity in emerging markets.

Page last updated on: