Water and Wastewater Treatment Equipment Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

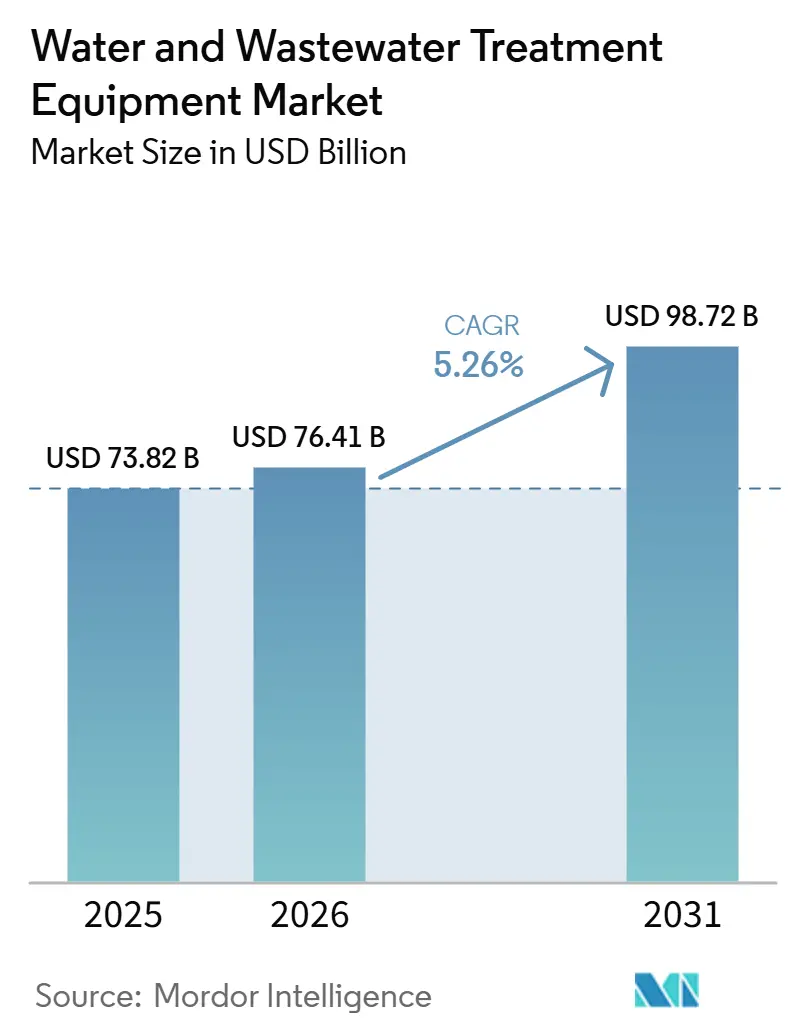

| Market Size (2026) | USD 76.41 Billion |

| Market Size (2031) | USD 98.72 Billion |

| Growth Rate (2026 - 2031) | 5.26% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water and Wastewater Treatment Equipment Market Analysis by Mordor Intelligence

The water and wastewater treatment equipment market is projected to grow from USD 73.82 billion in 2025 and USD 76.41 billion in 2026 to USD 98.72 billion by 2031, and is expected to register a CAGR of 5.26% between 2026 and 2031. Growth is driven by industrial water stress, stricter discharge regulations, and a shift toward water reuse and closed-loop water management. Municipal infrastructure spending supports baseline demand, while industrial investment is shifting the product mix toward higher-value systems such as membranes, advanced filtration, and digital monitoring platforms. Demand is distributed across Asia-Pacific, North America, and Europe, reducing dependence on a single spending cycle or regulatory regime. Competitive strategy is moving toward integrated offerings that combine equipment, monitoring, operations, and performance commitments, rather than stand-alone hardware sales. Market opportunity is strongest where utilities and industrial users require both regulatory compliance and reduced freshwater withdrawal, particularly in wastewater reuse, advanced treatment retrofits, and modular deployments.

Key Report Takeaways

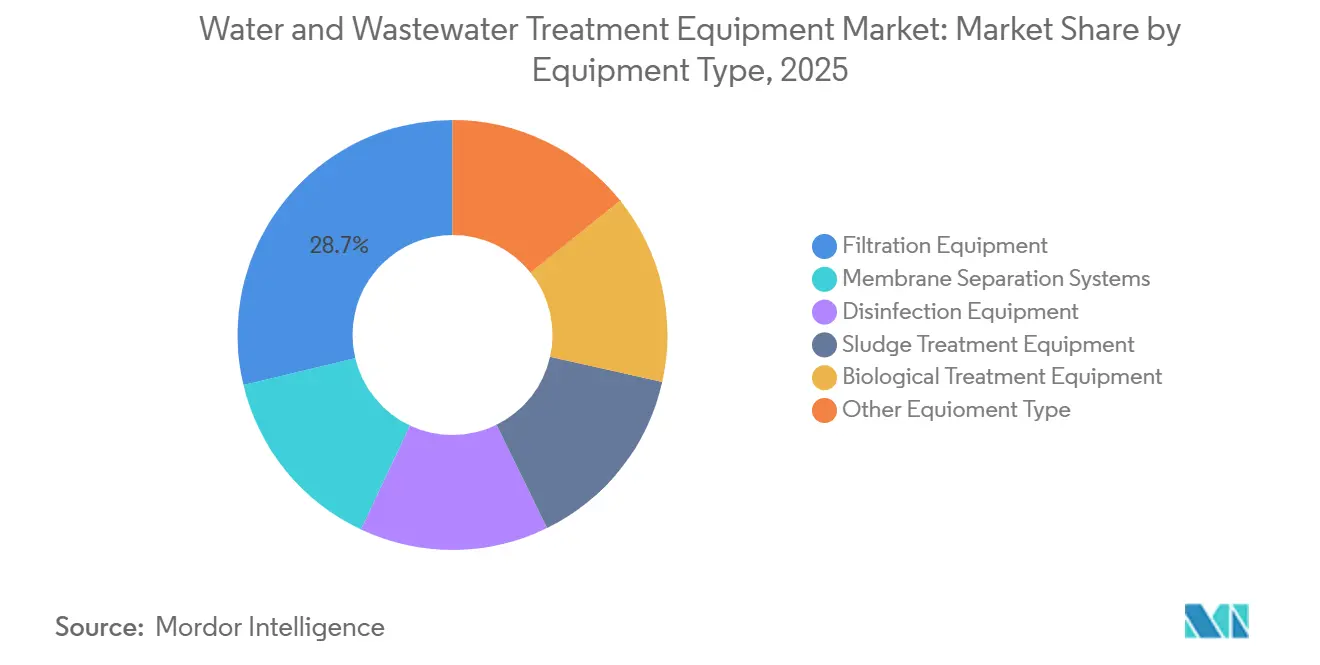

- By equipment type, filtration equipment held 28.74% of revenue in 2025, while membrane separation systems are expected to record the fastest projected growth at a 6.52% CAGR through 2031.

- By application, wastewater treatment accounted for 43.62% of revenue in 2025, while water reuse and recycling are forecast to grow at a 6.42% CAGR through 2031.

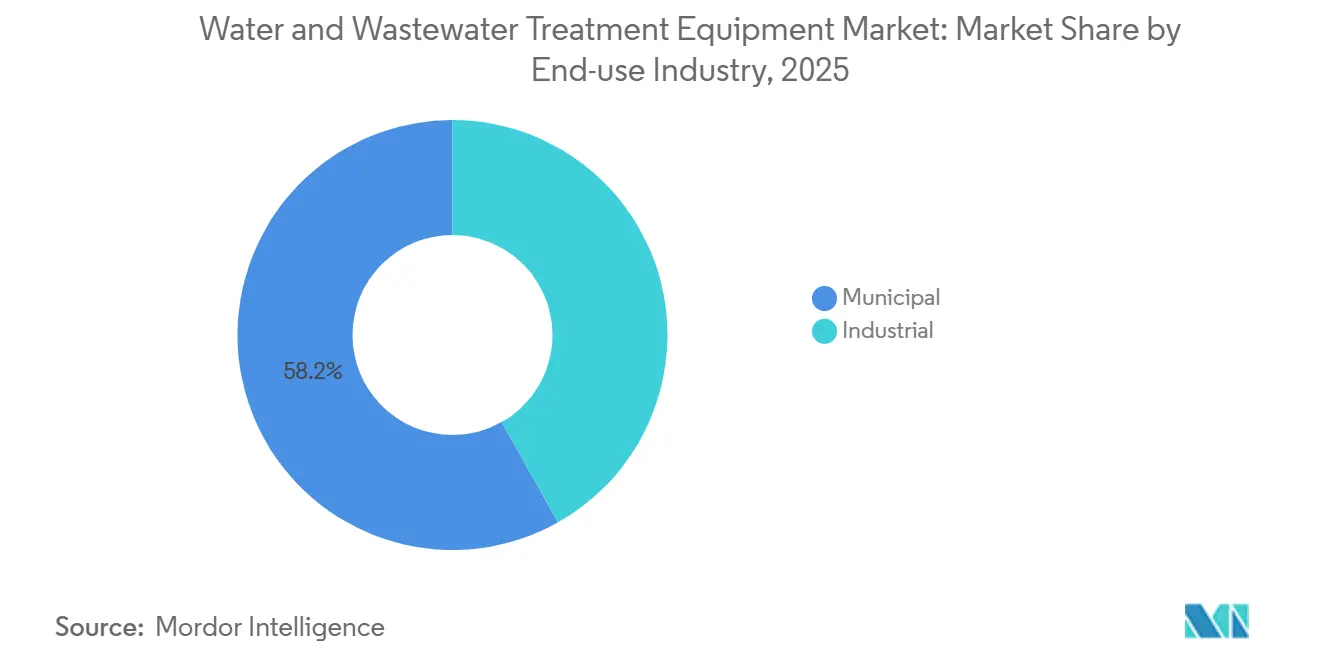

- By end-use industry, municipal accounted for 58.17% of revenue in 2025, while industrial is expected to expand at a 5.83% CAGR through 2031.

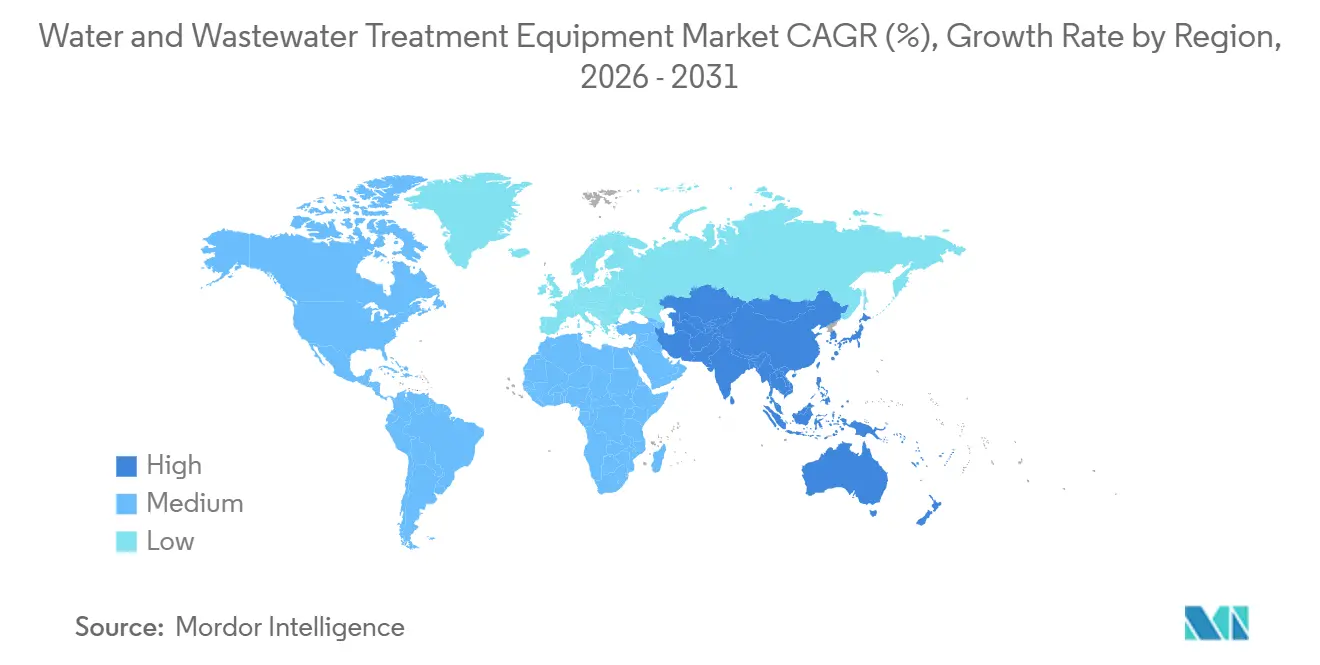

- By geography, Asia-Pacific held 40.32% of 2025 revenue and is also expected to post the highest projected regional CAGR of 5.82% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Water and Wastewater Treatment Equipment Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Industrial Water Reuse Mandate | +1.3% | Global, with concentrated demand in South Asia, Southeast Asia, and North America | Medium term (2-4 years) |

| Expansion of Modular Decentralized Treatment Systems | +0.9% | Asia-Pacific, Sub-Saharan Africa, Latin America | Short term (≤ 2 years) |

| Tighter Zero-Liquid-Discharge Compliance | +1.1% | South Asia, East Asia, Europe | Medium term (2-4 years) |

| Growth in PFAS, Microplastics, and Emerging Contaminants | +0.8% | North America, the European Union, and Australia | Long term (≥ 4 years) |

| Stringent Environmental Regulations | +0.9% | Global, with the strongest relevance in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Industrial Water Reuse Mandate

Industrial water reuse has shifted from a voluntary target to a formal operating requirement in several major economies, giving the water and wastewater treatment equipment market a more stable demand base. In April 2026, the U.S. Environmental Protection Agency launched Water Reuse Action Plan 2.0, explicitly linking reuse to semiconductor manufacturing, data centers, and energy production, which places advanced treatment equipment within national industrial priorities[1]U.S. Environmental Protection Agency, “EPA Launches Water Reuse Action Plan 2.0 to Advance Agency’s Core Mission and Strengthen US Industry, AI, and Energy Dominance,” U.S. Environmental Protection Agency, epa.gov. In the water and wastewater treatment equipment market, this is significant because reuse projects typically require more treatment stages than discharge-only systems, including filtration, membrane separation, and disinfection. Industrial buyers are treating water reuse as a supply-security measure, not only an environmental response, as water access now affects uptime in production-intensive facilities. This shift supports equipment demand even when broader capital spending turns selective, since water reuse can protect output and ensure compliance. It also increases the value of suppliers that can package equipment with controls, remote monitoring, and performance guarantees in a single offering.

Expansion of Modular Decentralized Treatment Systems

Modular systems are shortening project lead times and widening the addressable base for the water and wastewater treatment equipment market. In 2025, Grundfos completed the acquisition of Newterra, indicating that major suppliers view packaged and decentralized systems as an important part of future growth in treatment solutions. Modular systems reduce site engineering complexity and can be deployed across remote communities, industrial parks, and smaller treatment points. They also allow customers to phase capital spending over time, which is useful in markets where centralized infrastructure projects progress slowly. As modular adoption increases, equipment standardization becomes more feasible, supporting faster replication across locations. Basic modular assemblies may become more price competitive, while differentiated suppliers maintain stronger pricing through controls, service, and application-specific design.

Tighter Zero-Liquid-Discharge Compliance

Zero-liquid-discharge enforcement is expanding from a niche requirement into a broader industrial compliance issue, increasing the technology intensity of the water and wastewater treatment equipment market. A 2025 study in the Journal of Cleaner Production examined China's water-scarce regions and found that zero-liquid-discharge planning can create a tradeoff between pollution control and carbon emissions, which increases the appeal of membrane-led system design. In April 2026, DuPont expanded its FILMTEC Fortilife portfolio with elements designed for advanced zero-liquid-discharge, minimal liquid discharge, and resource recovery applications. In the water and wastewater treatment equipment market, stronger zero-liquid-discharge enforcement favors membranes, concentration systems, polishing stages, and integrated process design over simple end-of-pipe treatment. It also strengthens the case for suppliers that can reduce thermal load, lower brine volume, and cut energy use across the full treatment train. As economics improve, more mid-sized industrial operators are likely to move from delayed compliance to active procurement.

Growth in Per- and Polyfluoroalkyl Substances (PFAS), Microplastics, and Emerging Contaminants

Per- and polyfluoroalkyl substances (PFAS) and microplastics are adding a long-cycle layer of replacement and retrofit demand to the water and wastewater treatment equipment market. In 2026, the U.S. Environmental Protection Agency advanced its PFAS drinking water strategy, maintaining enforceable limits while allowing a longer compliance path, which delays some projects but does not eliminate the need for treatment upgrades. ISO issued ISO 5667-27:2025 on sampling for microplastics in water, strengthening the measurement base that future treatment and monitoring rules will rely on. PFAS and microplastics often require multi-barrier treatment rather than a single process step, meaning retrofit spending per site can increase considerably. This supports demand for activated carbon, nanofiltration, oxidation, and monitoring equipment in both municipal and industrial settings. Testing, treatment, and replacement cycles are likely to build over several years, extending the growth path of the water and wastewater treatment equipment market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment and Operational Costs | -1.5% | Global, with the strongest effect in emerging markets and smaller industrial facilities | Long term (≥ 4 years) |

| Complex Operation and Maintenance Requirements | -0.7% | Asia-Pacific emerging economies, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Membrane Fouling and Brine Disposal Challenges | -0.5% | Asia-Pacific, Middle East, and Africa, inland industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment and Operational Costs

High capital and operating costs remain a key restraint on the water and wastewater treatment equipment market, particularly for advanced systems. A 2025 article in Nature Reviews Clean Technology described zero and minimal liquid discharge systems as capital-intensive and highlighted the burden created by energy use, concentration steps, and downstream brine handling. This cost pressure divides buyers into two groups: large utilities and industrial users that can proceed with investments, and smaller operators that delay upgrades. The challenge is more pronounced in emerging economies, where project timing often depends on public finance capacity and lender support. Even when compliance pressure exists, upfront expenditure on membranes, pumps, polishing units, and thermal stages can defer procurement decisions by several years. This leaves suppliers under pressure to demonstrate lower lifecycle costs, phased deployment options, and improved operating efficiency before customers commit.

Membrane Fouling and Brine Disposal Challenges

Membrane fouling and brine disposal continue to limit the pace at which the water and wastewater treatment equipment market can scale in advanced treatment applications. A 2024 pilot study in the Journal of Membrane Science identified non-uniform fouling patterns in an integrated membrane system treating steel industry brine, indicating higher pretreatment requirements and more complex operating protocols. A 2025 review in Environmental Science: Water Research & Technology noted that pretreatment requirements and membrane replacement costs continue to slow the scale-up of advanced brine management technologies[2]Royal Society of Chemistry, “Emerging Investigator Series, A State-of-the-Art Review on Large-Scale Desalination Technologies and Their Brine Management,” Environmental Science: Water Research & Technology, pubs.rsc.org. Inland facilities face an additional challenge, as common disposal routes are not always practical or permitted, pushing projects toward energy-intensive crystallization or other costly alternatives. Suppliers that can combine concentration, brine handling, and resource recovery within a single system are likely to gain an advantage over vendors offering only individual treatment steps. Until such integration becomes more accessible and cost-effective, some customers will continue to postpone full advanced-treatment investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Membranes Outpace Conventional Filtration in Growth

Filtration equipment held 28.74% of 2025 revenue, while membrane separation systems are forecast to grow at 6.52% CAGR through 2031. Filtration maintains its lead in the water and wastewater treatment equipment market due to its use across municipal intake treatment, industrial pretreatment, and final polishing stages. Its broad installed base supports recurring replacement demand in mature regions, while greenfield projects in Asia sustain volume growth. Membrane separation systems are growing faster as they are central to reuse, desalination, pathogen control, and advanced contaminant removal. Their stronger growth also reflects their role in helping customers meet tighter performance requirements within smaller plant footprints.

DuPont launched upgraded FilmTec NF270 nanofiltration elements for drinking water applications in March 2026, with the release focused on biofouling resistance, permeability, and lower energy consumption. This product direction aligns with the water and wastewater treatment equipment market, where buyers weigh operating costs as closely as treatment performance. Disinfection equipment continues to benefit from pathogen control requirements, and UV systems remain relevant as utilities manage treatment quality and by-product concerns. Sludge treatment and biological treatment equipment are also seeing upgrade activity as plants respond to tighter handling and removal requirements. SUEZ won a sludge dewatering contract in Hong Kong in January 2026, demonstrating that dense urban projects continue to support specialized equipment demand in large treatment facilities.

By Application: Wastewater Treatment Leads Revenue While Water Reuse Gains Momentum

Wastewater treatment accounted for 43.62% of revenue in 2025, giving it the largest share of the water and wastewater treatment equipment market by application. Wastewater treatment maintains this lead because discharge compliance applies across both municipal and industrial systems, and most existing networks still require upgrades. The segment also benefits from a large installed base, which supports equipment replacement and new capacity additions. Water reuse and recycling is the fastest-growing application at a 6.42% CAGR, reflecting how treatment demand is shifting from disposal toward recovery and recirculation. In the water and wastewater treatment equipment market, this shift is driving demand for tertiary polishing, membrane separation, advanced disinfection, and monitoring tools.

SUEZ signed a 15-year contract with Nama Water Services in Oman in June 2026, covering water and wastewater services for 2.3 million people and including digital optimization and leak-detection tools. This example illustrates how wastewater treatment projects increasingly combine physical assets with digital performance management, raising system value beyond equipment alone. Desalination remains a strategic application in water-scarce regions, as high-capacity seawater reverse osmosis projects continue to advance where supply security is a priority. SUEZ also highlighted its Jordan desalination concession in 2026, including a plant with a capacity of 851,000 m³ per day and a long-term supply role in the country. Together, wastewater treatment, reuse, potable production, and desalination give the water and wastewater treatment equipment market a balanced demand profile rather than dependence on a single application.

By End-Use Industry: Municipal Scale Anchors Revenue, Industrial Growth Drives Incremental Value

Municipal held 58.17% of 2025 revenue, making it the largest contributor to water and wastewater treatment equipment market share by end use. Municipal demand remains dominant because drinking water and wastewater treatment are essential public services with long planning cycles and broad coverage needs. The segment also tends to favor suppliers with local service support, proven installations, and the ability to meet public procurement standards. Industrial is the fastest-growing end-use segment at a 5.83% CAGR through 2031, reflecting rising spending on reuse, zero-liquid discharge (ZLD), and site-level treatment performance. The water and wastewater treatment equipment market is therefore gradually shifting toward a mix with greater industrial technology content and higher average system value.

Pentair reported USD 391 million in Q1 2026 revenue for its Water Solutions segment, supported by remaining performance obligations tied to multiyear contracts. This pattern is consistent with the municipal side of the water and wastewater treatment equipment market, where contract visibility can remain strong over long delivery periods. At the same time, industrial customers are beginning to evaluate treatment systems not only on compliance outcomes but also on energy use and resource recovery. NX Filtration reported orders from Thermax in 2025 for nanofiltration and ultrafiltration projects in India, illustrating how regional engineering partners are scaling to serve industrial demand. This trend supports suppliers that can offer process expertise, modularity, and faster delivery in addition to equipment performance.

Geography Analysis

Asia-Pacific accounted for 40.32% of 2025 revenue and is projected to record the fastest regional CAGR of 5.82% through 2031, giving it the largest share by geography in the water and wastewater treatment equipment market. The region combines municipal infrastructure expansion with industrial compliance enforcement, supporting both volume growth and increasing technology intensity. India remains a major demand center, where large household water programs drive municipal capital expenditure while compliance requirements continue to tighten across water-intensive industries. The Central Pollution Control Board reinforced this direction in 2025 through zero-liquid-discharge enforcement actions affecting hundreds of textile units, signaling stricter compliance in industrial clusters. Mature markets such as Japan, South Korea, and Singapore show spending concentrated on membrane upgrades, advanced disinfection, and digital control systems rather than basic capacity expansion.

North America is the second-largest regional market for water and wastewater treatment equipment, driven by aging infrastructure renewal, per- and polyfluoroalkyl substances (PFAS) treatment demand, and water stress linked to data-center expansion. The U.S. Environmental Protection Agency outlined nearly USD 1 billion in PFAS-related support in 2026, translating policy into procurement of adsorption, ion exchange, and membrane technologies. The U.S. Senate introduced the Advancing Water Reuse Act in 2025, which adds a fiscal mechanism that could improve the economics of reuse projects for equipment manufacturers. Grundfos expanded dosing skid production in Fresno in 2025, reflecting suppliers localizing output to reduce lead times and serve North American projects more directly. Canada and Mexico are smaller in absolute equipment demand but continue to generate opportunities in mining water management and industrial effluent treatment.

Europe is characterized by high replacement intensity and detailed regulation, which keeps the water and wastewater treatment equipment market active even where basic treatment coverage is already mature. Directive (EU) 2024/3019 requires member states to implement broader urban wastewater treatment obligations, including expanded collection and treatment requirements that will support plant upgrades. Directive (EU) 2026/805 introduces tighter water quality standards, which will affect industrial discharge conditions across manufacturing regions. In the Middle East and Africa, long-tenor performance contracts in Oman and Jordan illustrate how suppliers are bundling equipment, operations, and digital oversight under single commercial structures. South America and Sub-Saharan Africa remain longer-cycle opportunities, where coverage gaps and industrial water demand are building future project pipelines, though financing conditions continue to shape project timing.

Competitive Landscape

The water and wastewater treatment equipment market is moderately fragmented at the upper tier, with Veolia, SUEZ, Xylem, DuPont Water Solutions, and Ecolab among the prominent players, while a wide range of regional specialists remains active in local projects and narrower product categories. Competition is shifting from stand-alone product sales toward integrated offerings that combine treatment assets, digital tools, operations, and performance-based contracts. This shift favors companies with broad portfolios, service networks, and the financial capacity to support long project cycles, while still leaving room for specialists that can address specific operational problems more effectively than full-line suppliers. The most defensible positions in this market are forming where technology depth and service continuity converge.

Recent deal activity reflects how larger companies are expanding their capabilities through acquisitions and portfolio moves. Veolia completed its Clean Earth acquisition in 2026, strengthening its hazardous waste and PFAS treatment position in the United States and deepening its industrial treatment reach. Ecolab announced the acquisition of Ovivo's electronics ultra-pure water business in August 2025, aligning it with rising treatment demand from semiconductor and data center applications. In September 2025, DuPont announced plans to expand FilmTec manufacturing into China through a reverse osmosis acquisition, supporting supply access in a major zero liquid discharge and industrial treatment market. Xylem acquired a majority stake in Idrica in 2024, reflecting continued interest in utility intelligence and software-led water management.

Technology differentiation is becoming a key competitive lever for companies that do not operate at the same contract scale as the largest players. DuPont's high-pressure and advanced nanofiltration product launches demonstrate how membrane performance, fouling resistance, and reduced energy consumption can create differentiation in this market. Grundfos is also moving beyond hardware by integrating its treatment portfolio with digital tools and packaged systems, which can support recurring revenue and stronger customer retention. The broad middle of the market remains fragmented, particularly where local engineering support, project customization, and price competitiveness matter more than global scale.

Water and Wastewater Treatment Equipment Industry Leaders

Veolia

Xylem

Pentair

Ecolab Inc.

DuPont

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SUEZ signed a EUR 2 billion (~USD 2.16 billion) 15-year performance-based contract with Nama Water Services, Oman, to operate and maintain water and wastewater services for approximately 2.3 million people across Muscat and the North and South Sharqiyah Governorates. The contract includes the Aquadvanced network optimization system and smart leak-detection tools to reduce water losses from 34% to 11%.

- April 2026: The U.S. Environmental Protection Agency (EPA) launched Water Reuse Action Plan (WRAP) 2.0, targeting industrial reuse for semiconductor manufacturing, data centers, and energy production. The plan establishes a federal policy framework for equipment procurement across advanced filtration, UV disinfection, and membrane systems in North America.

Global Water and Wastewater Treatment Equipment Market Report Scope

Water and wastewater treatment equipment includes physical, biological, and chemical systems used to remove contaminants, ensuring water is safe for industrial, municipal, and residential reuse. Systems such as Effluent Treatment Plants (ETP) and Sewage Treatment Plants (STP) address global water scarcity.

The Water and wastewater treatment equipment market is segmented by equipment type, application, end-use industry, and geography. By equipment type, the market is segmented into filtration equipment, membrane separation systems, disinfection equipment, sludge treatment equipment, biological treatment equipment, and other equipment types. By application, the market is segmented into water treatment, wastewater treatment, water reuse and recycling, and desalination. By end-use industry, the market is segmented into municipal and industrial. The report also covers market size and forecasts for water and wastewater treatment equipment across 16 countries in major regions. The market sizes and forecasts are provided in terms of value (USD).

| Filtration Equipment |

| Membrane Separation Systems |

| Disinfection Equipment |

| Sludge Treatment Equipment |

| Biological Treatment Equipment |

| Other Equipment Type |

| Water Treatment |

| Wastewater Treatment |

| Water Reuse and Recycling |

| Desalination |

| Municipal |

| Industrial |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Equipment Type | Filtration Equipment | |

| Membrane Separation Systems | ||

| Disinfection Equipment | ||

| Sludge Treatment Equipment | ||

| Biological Treatment Equipment | ||

| Other Equipment Type | ||

| By Application | Water Treatment | |

| Wastewater Treatment | ||

| Water Reuse and Recycling | ||

| Desalination | ||

| By End-use Industry | Municipal | |

| Industrial | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Water And Wastewater Treatment Equipment Market?

The water and wastewater treatment equipment market is projected to grow from USD 73.82 billion in 2025 and USD 76.41 billion in 2026 to USD 98.72 billion by 2031, and is expected to register a CAGR of 5.26% between 2026 and 2031.

Which equipment category is growing the fastest?

Membrane separation systems are the fastest-growing equipment category, with a projected 6.52% CAGR through 2031, driven by reuse, ZLD, and advanced contaminant-removal needs.

Which application area generates the most revenue?

Wastewater treatment held the largest application share at 43.62% in 2025 because both municipal and industrial systems continue to require broad compliance upgrades.

Why is water reuse becoming more important for suppliers and end users?

Reuse is becoming increasingly important because industrial operators are treating it as both a compliance tool and a water security measure, thereby supporting spending on advanced filtration, membranes, and disinfection.

Page last updated on: