Market Overview

| Study Period | 2020 - 2030 |

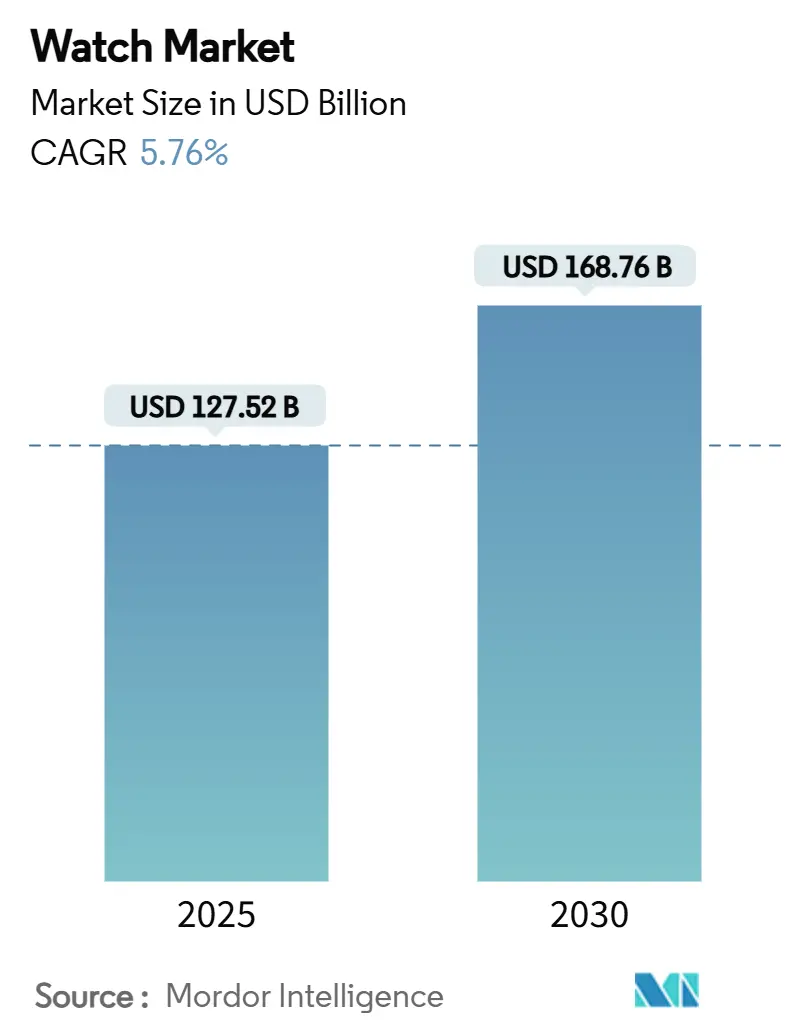

| Market Size (2025) | USD 127.52 Billion |

| Market Size (2030) | USD 168.76 Billion |

| Growth Rate (2025 - 2030) | 5.76% CAGR |

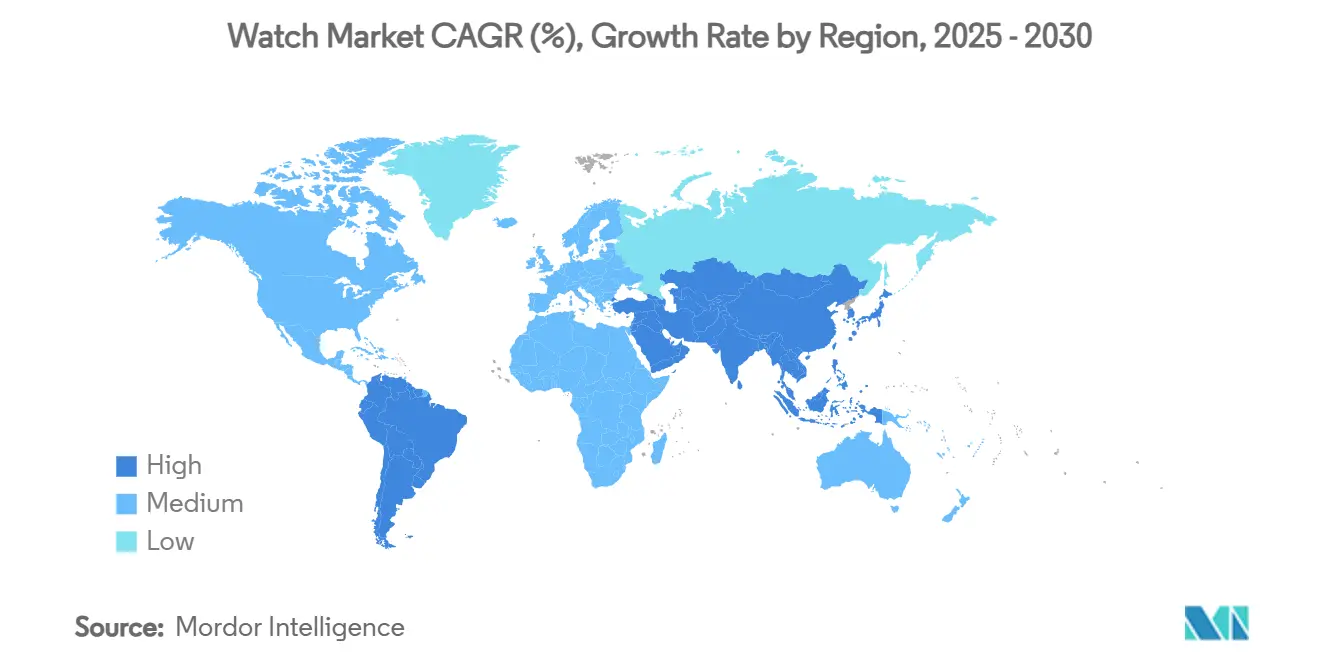

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

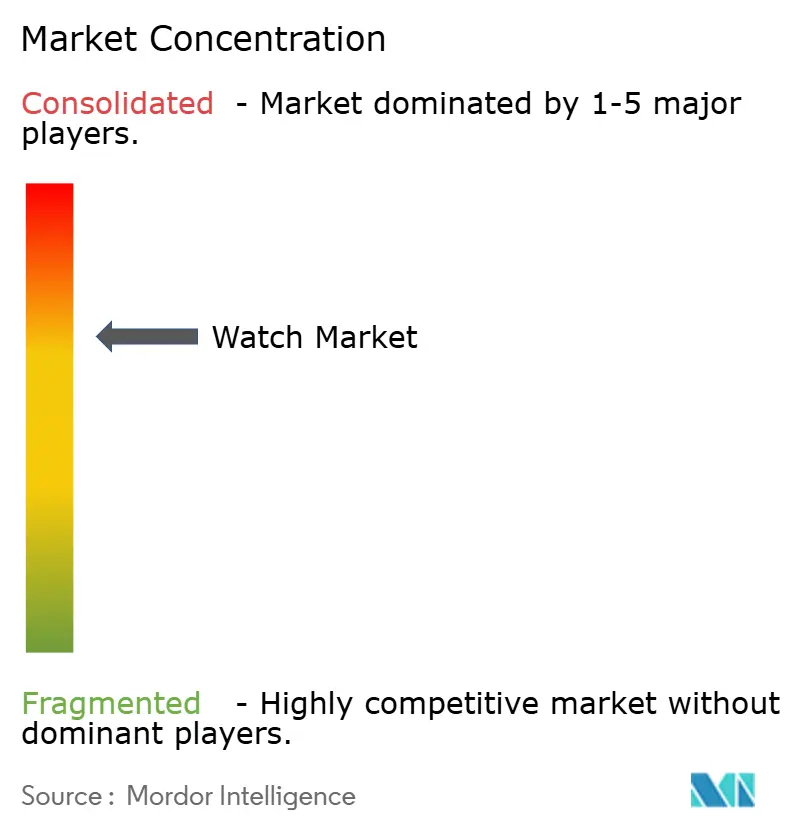

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Watch Market Analysis by Mordor Intelligence

The global watch market is estimated to be worth USD 127.52 billion in 2025 and is expected to grow to USD 168.76 billion by 2030, registering a CAGR of 5.76% during the forecast period. Several factors, including the continued demand for traditional craftsmanship, the increasing popularity of smart features in watches, and a growing preference for gender-neutral designs, drive this growth. Luxury brands are combining their expertise in traditional watchmaking with discreet digital technology to maintain their brand image while meeting the needs of tech-savvy consumers. The Asia-Pacific region is leading the growth due to the rising disposable income of the middle class, while South America, though starting from a smaller base, is showing signs of faster development. Specialty stores continue to attract customers by offering personalized services, while e-commerce platforms are gaining popularity due to improved authentication processes and better after-sales support. The global watch market has a moderate consolidation, which leaves room for emerging brands to compete. Major players like Swatch Group, Richemont, and LVMH dominate the market with their diverse product portfolios, which range from affordable fashion watches to high-end luxury timepieces.

Key Report Takeaways

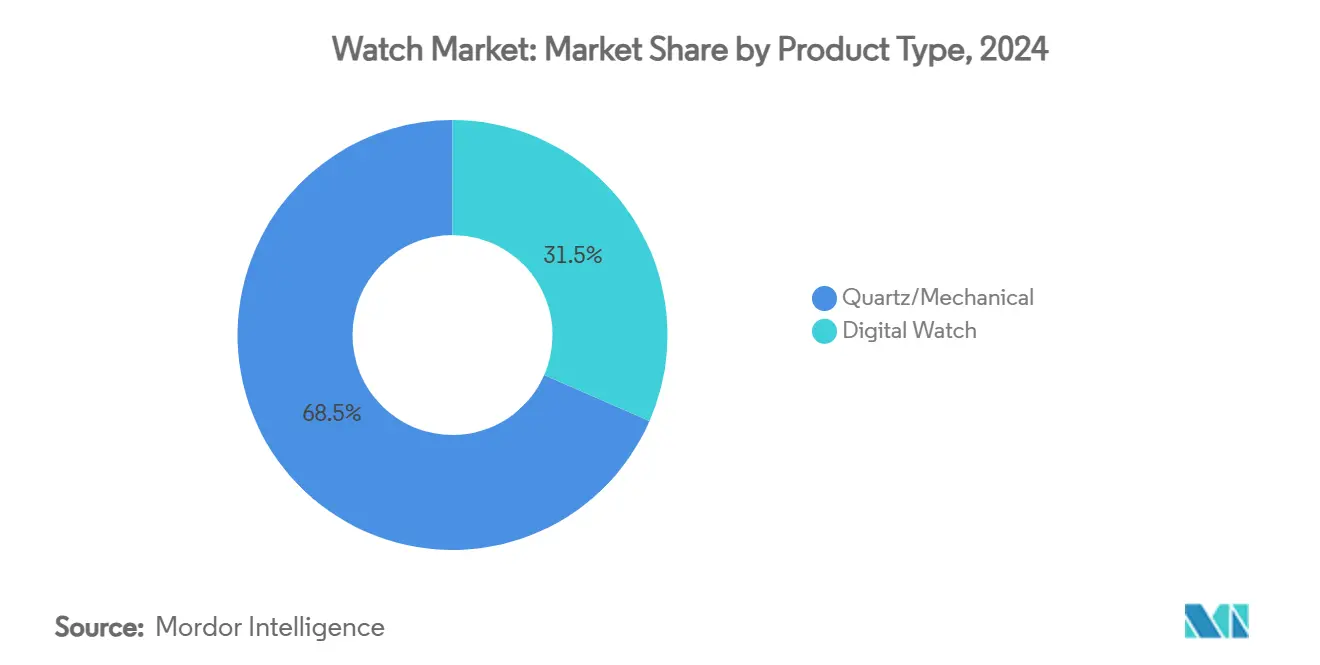

- By product type, quartz and mechanical lines held 68.46% of the watch market share in 2024; digital watches are on track for the fastest 2025-2030 CAGR at 5.86%.

- By category, the premium tier accounted for 37.63% of 2024 sales and is set to expand at a 6.23% CAGR to 2030, outpacing the mass segment.

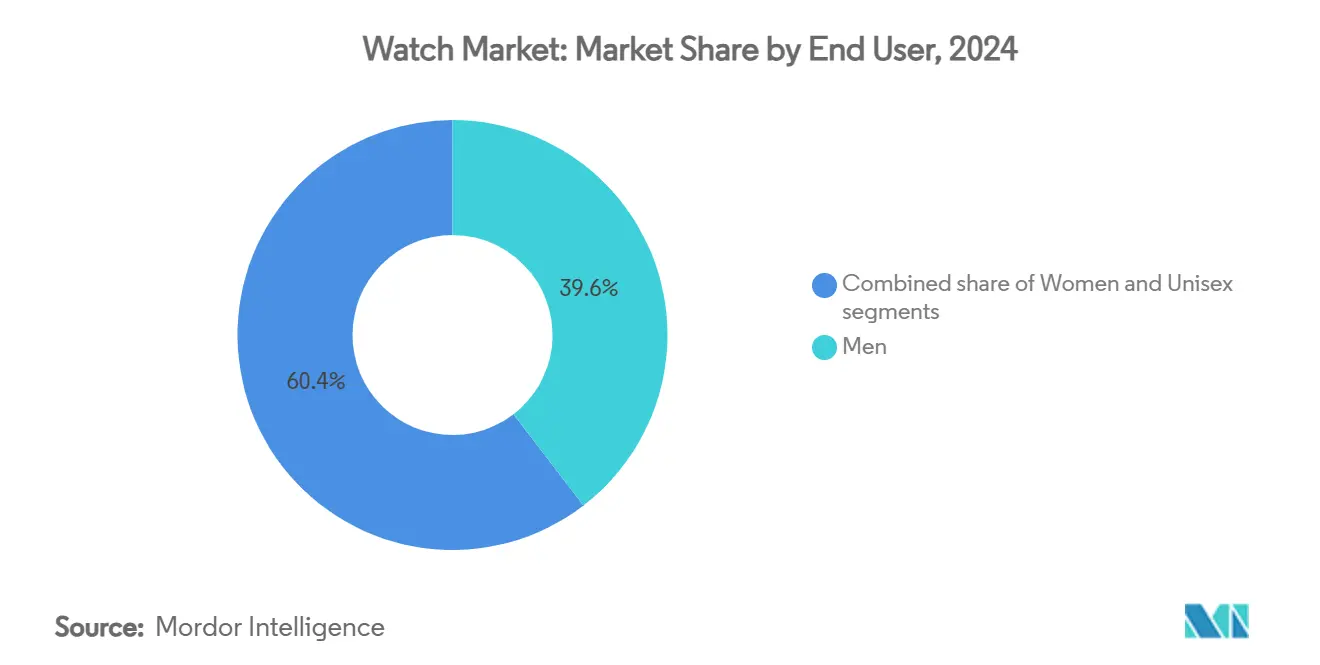

- By end user, men’s models remained the largest slice at 39.57% in 2024, while unisex pieces are projected to grow at a 6.88% CAGR through 2030.

- By distribution channel, specialty stores retained 54.34% of 2024 revenue, yet online retail is forecast to rise at a 7.23% CAGR over the outlook period.

- By geography, Asia-Pacific led with 39.54% of sales in 2024, whereas South America is expected to register the quickest regional CAGR of 7.65% through 2030.

Global Watch Market Trends and Insights

Drivers Impact Table

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for smartwatches with health features | +1.2% | Global, with Asia-Pacific and North America leading adoption | Medium term (2-4 years) |

| Technological advancements and innovation | +0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Increasing demand for luxury watches | +0.8% | North America, Europe, Asia-Pacific high-income segments | Medium term (2-4 years) |

| Brand heritage and craftsmanship | +0.7% | Europe, North America, select Asia-Pacific markets | Long term (≥ 4 years) |

| Growing demand for sports watches from fitness conscious consumers | +0.6% | Global, with stronger penetration in developed markets | Short term (≤ 2 years) |

| Growing social media influence and celebrity endorsements | +0.4% | Global, particularly strong in emerging markets | Short term (≤ 2 years) |

Source: Mordor Intelligence

Understand The Key Trends Shaping This Market

Download PDF

Rising demand for smartwatches with health features

Interest in preventive health has grown significantly, leading to a surge in smartwatch demand. According to the World Health Organization, cardiovascular diseases (CVDs) are the top cause of death worldwide, responsible for about 17.9 million deaths annually [1]Source: World Health Organization, "Cardiovascular diseases,"who.int. Smartwatches like the Apple Watch Series 9 and Samsung Galaxy Watch 6 now come with advanced health features, including ECG monitoring, alerts for irregular heartbeats, and continuous tracking of heart rate, sleep patterns, and blood oxygen levels. These features help users keep a closer eye on their health and identify potential issues, such as atrial fibrillation, early on. As technology improves, with smaller sensors and longer-lasting batteries, smartwatch brands are rolling out regular health-focused updates, encouraging users to upgrade their devices more frequently. Traditional watchmakers are also adapting by introducing hybrid models that combine classic watch designs with modern health-tracking technology, offering a mix of style and functionality.

Increasing demand for luxury watches

The perception of luxury watches as investment assets has become increasingly popular, particularly among younger, financially aware buyers. Brands like Rolex and Patek Philippe have amplified this trend by limiting production and discontinuing iconic models like the Nautilus 5711, creating exclusivity and driving up resale values. This growing demand is also supported by rising disposable incomes, especially in regions with fast-growing economies. According to the International Monetary Fund, as of April 2025, the global GDP per capita in purchasing power parity terms is USD 206.88 thousand per capita [2]Source: International Monetary Fund, "GDP, current prices,Purchasing power parity; billions of international dollars,"imf.org. Additionally, the top three countries with the highest number of individuals having a net worth between USD 1 million and USD 5 million are the United States, China, and France [3]Source: World Population Review, "High Net Worth Individuals by Country 2025," worldpopulationreview.com. Luxury watchmakers are responding to this trend by focusing on limited production and showcasing artisanal craftsmanship. For instance, Richard Mille’s RM 65‑01 “King James,” introduced in June 2025 in collaboration with LeBron James, was limited to just 150 pieces worldwide.

Growing social media influence and celebrity endorsements

The rise of social media and celebrity culture has profoundly influenced how consumers perceive watches, transforming them into powerful symbols of status and personal identity. Platforms like Instagram, TikTok, and YouTube have made luxury watches more visible than ever, with influencers and celebrities such as Roger Federer (Rolex) and Timothée Chalamet (Cartier) driving brand desirability, particularly among younger audiences. These high-profile endorsements lead to immediate surges in demand, especially when tied to limited-edition releases. For instance, footballer Kylian Mbappé’s presence as a Hublot ambassador at Watches and Wonders Geneva 2024 created significant buzz for the brand. User-generated content, such as unboxing videos and personal reviews, further amplifies the aspirational appeal of these timepieces. Social media also allows brands to showcase their heritage and craftsmanship through behind-the-scenes content, offering a glimpse into the artistry and precision behind their creations.

Technological advancements and innovation

Innovative advancements are transforming both luxury and mass-market watch segments, enhancing performance, durability, and consumer confidence. In luxury watches, brands like Omega and Breguet are incorporating silicon-based escapements, which reduce friction and resist magnetism, resulting in improved accuracy and longer service intervals. This allows brands to offer extended warranties, reassuring customers about the reliability of their timepieces. The use of advanced materials such as high-entropy alloys and carbon composites is gaining traction. These materials create lightweight yet highly durable watch cases, appealing to consumers seeking robust sports and adventure watches. For instance, the TAG Heuer Carrera Plasma Diamant d’Avant-Garde, launched in 2023, features lab-grown diamonds and a carbon composite case, blending cutting-edge aesthetics with enhanced durability. On the digital side, blockchain technology is revolutionizing the industry. Brands like Breitling and Vacheron Constantin are introducing blockchain-backed digital certificates, which verify the authenticity of watches and simplify the resale process.

Restraints Impact Analysis

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Availability of counterfeit products | -0.8% | Global, with higher impact in emerging markets | Long term (≥ 4 years) |

| Surge in demand for smart variables | -0.6% | Developed markets, particularly North America and Europe | Medium term (2-4 years) |

| High production cost associated with luxury watches | -0.5% | Global, concentrated in premium segment | Short term (≤ 2 years) |

| Fluctuating raw material prices | -0.4% | Global, affecting all segments | Short term (≤ 2 years) |

Source: Mordor Intelligence

Availability of counterfeit products

The availability of counterfeit watches continues to undermine brand reputation and erode consumer trust in the global watch industry. According to the OECD, counterfeit watches accounted for 23% of the total value of seized counterfeit goods globally as of 2025 [4]Source: Organization for Economic Co-operation and Development, "Mapping Global Trade in Fakes 2025," oecd.org. Despite significant enforcement efforts, such as large-scale seizures by customs authorities in regions like the U.S., EU, and Asia, counterfeit sellers quickly reappear on digital marketplaces and social media platforms under new identities. For instance, in 2025, U.S. Customs and Border Protection seized over two dozen counterfeit Rolex watches and designer sunglasses in Pittsburgh. This issue is particularly harmful to entry-level luxury brands, where first-time buyers may unknowingly purchase counterfeit products, leading to mistrust and potential long-term disengagement with the brand. To combat this growing problem, leading brands like Rolex and Audemars Piguet are adopting advanced digital verification measures. These include serial-number tracking, scannable QR codes, and NFC-enabled certificates of authenticity, which aim to provide consumers with greater confidence in their purchases and protect brand equity.

High production cost associated with luxury watches

Rising material and labor costs are creating significant challenges for profitability in the high-end watchmaking industry. The increasing prices of essential materials like gold, platinum, and surgical-grade steel, driven by factors such as geopolitical instability, inflation, and limited mining output, have substantially raised production costs. Precious-metal watches, which account for nearly 40% of Swiss watch export value, are particularly vulnerable to these price fluctuations. Large conglomerates like Richemont and LVMH can manage these pressures more effectively through strategies like bulk purchasing and hedging. However, smaller independent watchmakers often face tough decisions, balancing the need to maintain quality with the necessity of protecting profit margins. The artisanal nature of luxury watchmaking adds to the cost burden, as training and retaining skilled horologists require significant investment and competitive wages. To address these challenges, some brands are focusing on improving operational efficiency and exploring the use of alternative or recycled materials.

Segment Analysis

By Product Type: Digital Innovation Accelerates Traditional Dominance

Quartz and mechanical watches made up 68.46% of the revenue in 2024, showcasing the enduring appeal of traditional craftsmanship and the reliability of these timepieces. Consumers continue to value the tactile experience and long-term durability that these watches offer, making them a cornerstone of the watch market. This dominance provides a stable base for the industry, even as newer technologies emerge. Meanwhile, hybrid models that combine classic features like sapphire crystals and mechanical hands with subtle digital displays are gaining traction. These designs prove that traditional and modern elements can coexist, appealing to a broader range of consumers without diminishing the value of either segment.

Digital watches, though currently holding a smaller share of the market, are projected to grow at a 5.86% CAGR through 2030, driven by increasing demand from tech-savvy and health-conscious buyers. These watches have evolved beyond simple timekeeping to offer advanced features such as fitness tracking, heart-rate monitoring, and contactless payment options. This expanded functionality has made them indispensable for many consumers, particularly those focused on wellness and convenience. Over-the-air updates ensure these devices remain relevant over time, enhancing their value proposition. Traditional watchmakers are also adapting by collaborating with semiconductor companies to integrate reliable smart components, allowing them to capture a share of this growing segment while maintaining their reputation for precision and quality.

By Category: Premium Resilience versus Mass-Market Volume

The mass-tier segment accounted for 62.37% in 2024, driven by its affordability and frequent updates to align with fashion trends. However, the premium segment is experiencing faster revenue growth, with a projected CAGR of 6.23%, and is contributing significantly to the overall value growth of the watch market during the forecast period. Premium watches justify their higher price points through limited production runs, unique complications, and the use of high-quality materials, which appeal to consumers seeking exclusivity and craftsmanship.

The market is witnessing a clear divide in consumer preferences, with aspirational buyers either upgrading to high-end, investment-worthy watches or opting for affordable and feature-rich smartwatches. To address this, premium brands are enhancing customer experiences through concierge-driven online platforms, exclusive boutique collections, and personalized after-sales services to build customer loyalty. On the other hand, mass-market brands are focusing on cost-effective designs, collaborations with fashion labels, and frequent seasonal launches to maintain their appeal. This dual-speed dynamic fosters intense competition and drives continuous innovation across the watch market.

By End User: Gender-Neutral Design Gains Momentum

Men’s watches accounted for 39.57% of the revenue in 2024, driven by their classic designs, professional aesthetics, and traditional case sizes. These watches often feature restrained color schemes and are tailored to suit formal and business settings. However, the unisex segment is gaining significant traction, with a projected growth rate of 6.88% CAGR, as societal preferences shift toward inclusivity and versatility. Watches with slimmer profiles, interchangeable straps, and minimalist designs are appealing to a broader audience, including those who value functionality and style without gender-specific labels. To cater to this demand, brands are increasingly launching collections with neutral designs and avoiding gendered marketing strategies to attract a wider customer base.

In the luxury segment, women’s demand is also growing, but many female buyers are now opting for unisex designs that prioritize mechanical sophistication over traditional embellishments like gemstones. This shift reflects a preference for watches that combine technical excellence with understated elegance. Additionally, the rising popularity of influencer content showcasing couples sharing the same watch has helped normalize the trend of cross-gender wear. This has further boosted the appeal of neutral aesthetics, encouraging brands to rethink their approach to segmentation.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Experience-Led Stores Meet Expanding E-Commerce

Specialty watch retailers accounted for 54.34% of the market's revenue in 2024, supported by their expertise in horology, in-house repair services, and exclusive partnerships with leading brands. These retailers offer a personalized shopping experience, including tailored fittings, detailed product education, and ceremonial handovers that create a sense of occasion for buyers. This hands-on approach continues to attract customers who value the tactile and immersive experience that physical stores provide. However, the rise of e-commerce is undeniable, with online sales expected to grow at a 7.23% CAGR through 2030. This growth is fueled by the increasing popularity of certified pre-owned platforms, live-streamed product launches, and secure payment systems that enhance customer confidence.

The shift toward online shopping, which gained momentum during the pandemic, has proven to be a lasting trend. Many watch brands now offer virtual consultations, 360-degree product views, and home delivery services for try-ons, making the online shopping experience more convenient and engaging. Additionally, advancements in verification technologies, such as blockchain-based certificates, have addressed concerns about authenticity, further boosting consumer trust in online purchases. Physical stores are adapting to this new landscape by transforming into appointment-only showrooms and service centers, focusing on creating a complementary omnichannel strategy that blends the best of both physical and digital retail experiences.

Geography Analysis

Asia-Pacific accounted for 39.54% of global watch sales in 2024, making it the largest regional market. The region's growth is driven by increasing disposable income among middle-class households and a strong cultural emphasis on luxury and status symbols. Key markets like China, Japan, and India dominate sales, while Southeast Asian countries are rapidly catching up due to expanding retail networks and tax-free shopping opportunities for tourists. The widespread use of smartphones supports omnichannel strategies, as consumers often research products online before making in-store purchases.

South America, led by Brazil and Argentina, is expected to grow at a 7.65% CAGR through 2030, making it the fastest-growing region in the watch market. This growth is fueled by rising urbanization, improving access to credit, and a growing demand for lifestyle upgrades. While challenges such as fluctuating import duties and currency instability persist, the region's favorable demographics and increasing consumer spending power provide a strong foundation for long-term growth. Both global luxury brands and local mid-tier players are capitalizing on these opportunities to expand their presence in the region.

North America and Europe remain mature but highly profitable markets for watches. In the United States, a strong community of watch collectors and a well-established pre-owned market drive consistent sales, even during economic slowdowns. Europe benefits from its proximity to Swiss watchmakers and its rich heritage in luxury craftsmanship, which ensures steady demand. While growth in these regions is slower compared to emerging markets, they continue to generate significant revenue. Meanwhile, the Middle East and Africa, though smaller contributors today, show promising potential. High-value transactions in Gulf Cooperation Council countries and increasing online penetration across Africa are expected to boost sales in the coming years.

Competitive Landscape

The global watch market shows moderate consolidation, leaving space for emerging challenger brands to grow. Dominant players like Swatch Group, Richemont, and LVMH maintain their leadership through diverse portfolios that cater to a wide range of consumers, from entry-level fashion watches to high-end luxury timepieces. Their control over in-house component manufacturing and ownership of multi-brand retail chains gives them a competitive edge. These companies also benefit from economies of scale, ensuring access to premium materials and securing prime retail locations, which further solidifies their market position.

Independent luxury watchmakers continue to thrive by focusing on authenticity, craftsmanship, and limited production runs, appealing to collectors and enthusiasts who value exclusivity. However, these smaller brands face challenges in gaining visibility as larger conglomerates dominate mainstream distribution channels. To counter this, many independents are leveraging digital platforms and storytelling to connect directly with their audience. The rise of online marketplaces and influencer-driven storefronts has provided these brands with alternative avenues to reach consumers, proving that compelling narratives can still compete with the resources of industry giants.

Technology companies are intensifying competition by incorporating advanced features like sensors, proprietary operating systems, and cloud connectivity into smartwatches. In response, traditional watchmakers are introducing hybrid models that combine mechanical craftsmanship with digital functionality or forming partnerships to integrate software capabilities. Sustainability initiatives, such as circular-economy trade-ins and localized production, are becoming key differentiators. These efforts not only address consumer demand for eco-friendly practices but also offer newer entrants opportunities to carve out a niche in the evolving watch market.

Watch Industry Leaders

-

The Swatch Group

-

Fossil Group Inc.

-

LVMH (Louis Vuitton Moët Hennessy)

-

Compagnie Financière Richemont S.A

-

Rolex SA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- June 2025: LeBron James's RM 65-01 "King James" watch is a special collaboration with Richard Mille. The watch combines cutting-edge technology with bold aesthetics, making it a standout accessory for collectors and fans alike.

- April 2025: Patek Philippe unveiled 15 references at Watches and Wonders 2025, including its first World Time with a synchronized date indication and a revived Golden Ellipse bracelet.

- October 2024: The Watches of Switzerland Group (WOS) acquired online watch publication Hodinkee with the goal of supporting Hodinkee’s continued operation as a leader in the watch community.

- September 2024: New World Solutions entered the Global Watch Market with the acquisition of a majority Stake in dialMKT.

Global Watch Market Report Scope

A watch is a portable timepiece intended to be carried or worn by a person.

The watch market is segmented by product type into quartz watches and digital watches. The digital watch is further segmented into smart and others. The market is segmented by price range into low-range, mid-range, and luxury. By end user, the market is segmented into women, men, and unisex. The market is segmented by distribution channels into offline and online retail stores. The market is segmented by geography into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

| By Product Type | Quartz/Mechanical | ||

| Digital Watch | Smart Watches | ||

| Other Digital Types | |||

| By Category | Mass | ||

| Premium | |||

| By End User | Men | ||

| Women | |||

| Unisex | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Specialty Stores | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

By Product Type

| Quartz/Mechanical | |

| Digital Watch | Smart Watches |

| Other Digital Types |

By Category

| Mass |

| Premium |

By End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the global watch market?

The watch market is valued at USD 127.52 billion in 2025 and is forecast to grow to USD 168.76 billion by 2030.

Which region leads watch sales today?

Asia-Pacific accounts for 39.54% of global revenue, making it the largest regional contributor.

How fast are premium watches growing compared with mass-market models?

Premium lines are projected to expand at a 6.23% CAGR through 2030, ahead of the wider market’s 5.76% pace.

Why is counterfeiting a serious issue for watch brands?

High-quality replicas erode consumer trust, divert revenue, and force legitimate brands to spend heavily on authentication and enforcement programs.

What factors are driving digital watch adoption?

Always-on health monitoring, software updates, and mobile payment integration are key drivers behind the 5.86% CAGR expected for digital watches.

Page last updated on: July 2, 2025