Walk Behind Lawn Mowers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 10.95 Billion |

| Market Size (2031) | USD 14.26 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Walk Behind Lawn Mowers Market Analysis by Mordor Intelligence

The walk-behind lawn mowers market size is estimated to grow from USD 10.41 billion in 2025 and USD 10.95 billion in 2026 to reach USD 14.26 billion by 2031, at a CAGR of 5.42% during the forecast period (2026-2031). The walk-behind lawn mower market is being driven by faster adoption of battery-powered equipment, as buyers place greater weight on low noise, low maintenance, and easier operation in both home and institutional settings. Regulation has also become a stronger purchase trigger, especially after California’s Assembly Bill 1346 took effect in 2024 and changed the sales outlook for new gasoline-powered small off-road engines in one of the world’s most visible outdoor power markets[1]Source: California Air Resources Board, “Assembly Bill 1346, Small Off-Road Engine Regulations,” 2024, arb.ca.gov. The category is also benefiting from smaller residential lot sizes, rising interest in cordless tool ecosystems, and a homeowner base that now treats compatibility across outdoor tools as part of the purchase decision. Competition in the market is shifting from pure product comparisons toward runtime, platform depth, dealer support, and product launches tied to battery expansion across several outdoor power categories. Even so, the walk-behind lawn mowers market still faces pressure from narrow seasonal demand windows and battery runtime concerns in heavier commercial use, which will keep product mix and replacement timing central to growth through 2031.

Key Report Takeaways

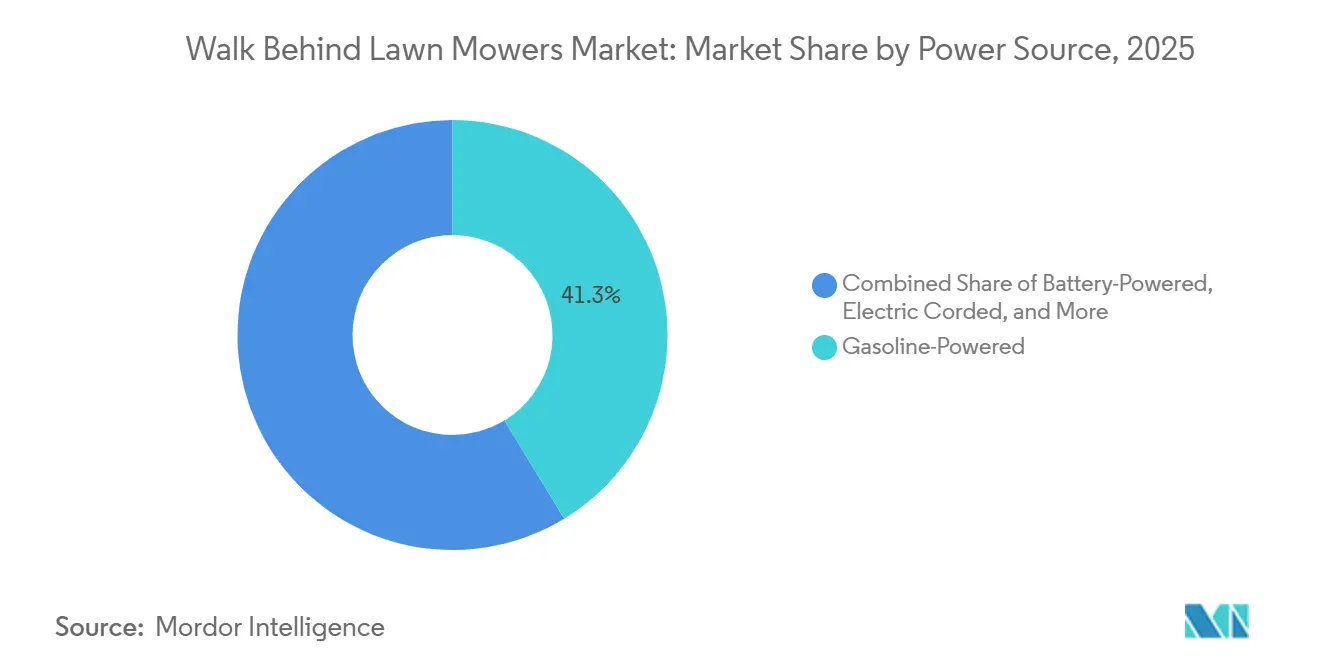

- Gasoline-powered models accounted for 41.3% of the walk-behind lawn mowers market size in 2025, while battery-powered models are projected to experience the fastest growth, with a CAGR of 11.1% through 2031.

- By product type, push mowers led with 45.2% of the walk-behind lawn mowers market share in 2025, while self-propelled models recorded the highest projected CAGR at 6.8% through 2031.

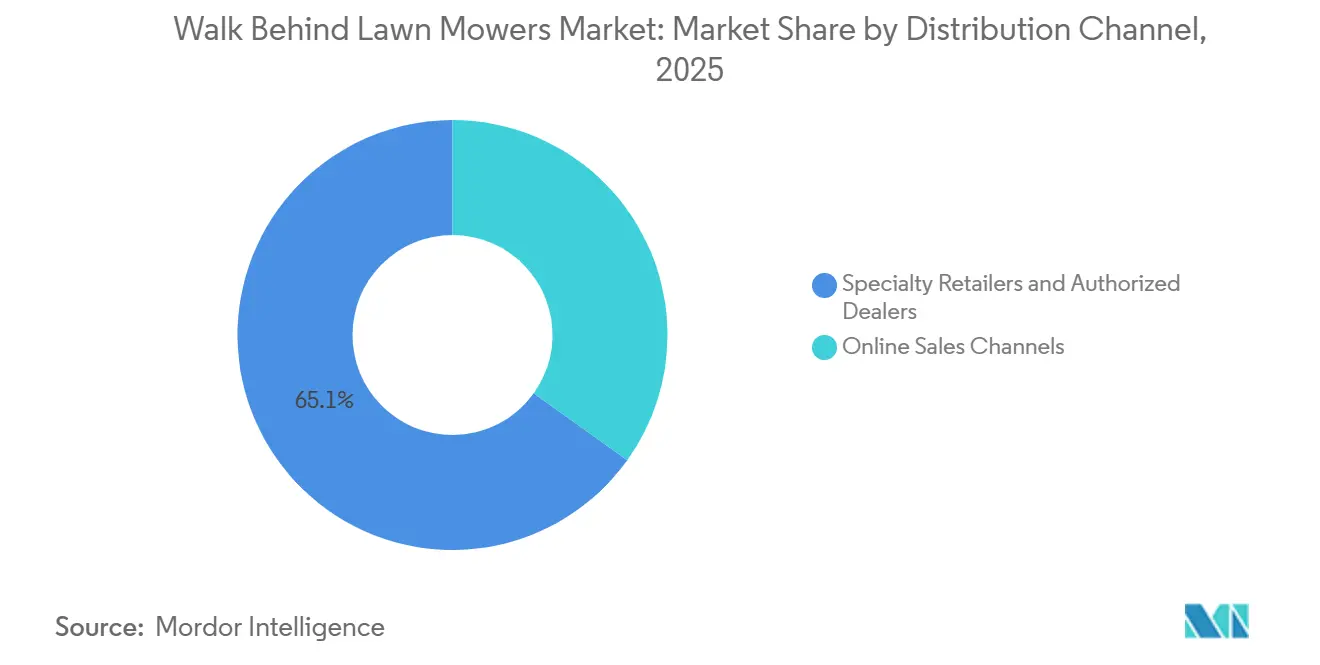

- By distribution channel, specialty retailers and authorized dealers accounted for 65.1% of the market in 2025, while online sales channels are projected to grow at a 8.9% CAGR through 2031.

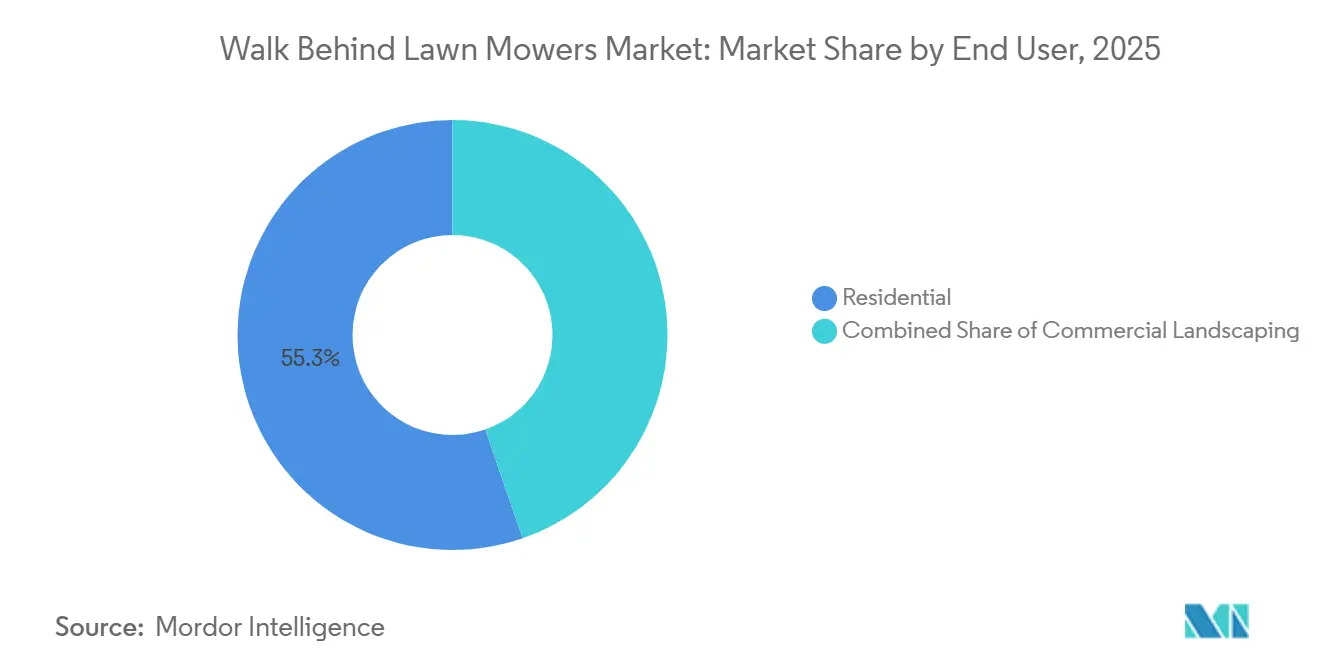

- By end user, residential buyers accounted for 55.3% of the market size in 2025, while commercial landscaping is anticipated to grow at the fastest CAGR of 6.7% through 2031.

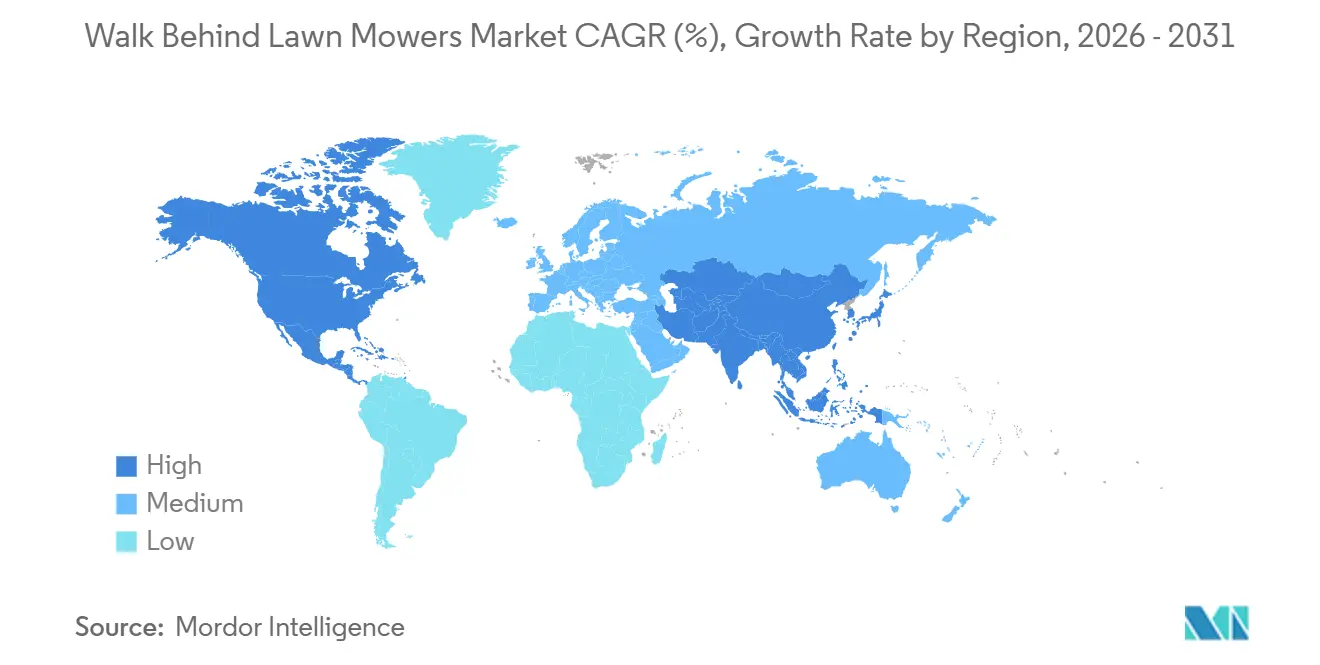

- By geography, North America accounted for 44.5% of the share in 2025, while Asia-Pacific is projected to experience the fastest growth, with a 7.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Walk Behind Lawn Mowers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for low-noise and low-maintenance lawn care equipment | +1.20% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Battery ecosystem lock-in across outdoor power tool brands | +1.00% | North America and Asia-Pacific core, with spillover to Europe | Medium term (2-4 years) |

| Municipal and commercial electrification in noise-sensitive zones | +0.80% | Europe and North America, with early gains in Asia-Pacific metros | Medium term (2-4 years) |

| Growth of compact-lot housing and smaller lawn ownership | +0.70% | North America, Europe, and Asia-Pacific urban corridors | Long term (≥ 4 years) |

| Dealer bundling and retail shelf expansion for cordless platforms | +0.60% | North America and Europe | Short term (≤ 2 years) |

| Faster replacement cycles for premium battery models | +0.60% | Global, with early penetration in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Low-Noise and Low-Maintenance Lawn Care Equipment

The walk-behind lawn mowers market is seeing a clear demand shift toward products that reduce neighborhood noise and routine upkeep. What was once treated as a comfort feature is now influencing buying decisions at the point of sale, especially in suburban and urban residential areas. The European Commission updated lawn mower noise measurement rules through Delegated Regulation (EU) 2024/1208, and the revised framework took effect on May 22, 2025, which raised the compliance burden for gasoline-based equipment entering the European Union[2]Source: European Commission, “Delegated Regulation (EU) 2024/1208 Amending Directive 2000/14/EC,” Official Journal of the European Union, europa.eu. That change matters because it makes guaranteed sound power labeling more visible and pushes manufacturers to justify the continued use of louder power formats. Battery walk-behind mowers also reduce day-to-day maintenance because they avoid fuel handling, engine servicing, and several recurring upkeep tasks that many household buyers dislike. This benefit is especially important for first-time buyers who want simpler operation and faster setup. The result is a stronger pull toward cordless formats in markets where noise sensitivity and convenience now carry as much weight as cutting performance.

Battery Ecosystem Lock-In Across Outdoor Power Tool Brands

Battery platform ownership is becoming one of the strongest hidden forces inside the walk-behind lawn mowers market. Once a household or contractor buys into a battery family through a blower, trimmer, or chainsaw, the next mower purchase becomes easier because the charger and battery investment are already in place. Makita Corporation, a Japan-headquartered manufacturer of professional power tools and outdoor equipment with a global presence, continued to expand its cordless ecosystem in 2025. The company's 40V XGT platform supported over 170 compatible tools, illustrating how integrated battery platforms have become an important competitive differentiator across the outdoor power equipment industry[3]Source: Makita Corporation, “40V Max XGT Outdoor Power Equipment Portfolio,” Makita, makitatools.com. This changes the competition because buyers are no longer comparing only deck width, runtime, and price. They are also comparing how well a mower fits the tools already stored in the garage or trailer. Stanley Black & Decker, Inc., along with brands under Techtronic Industries, benefits from this platform effect in ways that gasoline-focused suppliers struggle to match. Battery ecosystem lock-in is turning brand familiarity into repeat purchasing behavior that may last across several replacement cycles. That makes early adoption of the battery platform one of the most defensible ways to retain long-term share.

Municipal and Commercial Electrification in Noise-Sensitive Zones

Institutional buyers are becoming a more important source of demand in the walk-behind lawn mowers market, particularly where public noise limits influence landscaping contracts. Parks departments, schools, campuses, and commercial property managers are steadily shifting attention toward cordless equipment because it helps them align with quieter operating standards. The updated European Union noise framework has strengthened that shift by making compliance and certification more visible across member states. This matters because public tenders often reward equipment that reduces community disruption and fits broader environmental procurement goals. Commercial landscaping is one of the fastest-growing end-user categories, and a significant part of that growth is tied to replacing older gasoline fleets in controlled operating environments. The electrification at the municipal and contractor level also helps validate battery performance for smaller private buyers who watch public fleets adopt new formats first. Over time, these institutional purchases are likely to reinforce product availability, service readiness, and confidence in battery-powered work routines.

Growth of Compact-Lot Housing and Smaller Lawn Ownership

The walk-behind lawn mowers market continues to benefit from the spread of smaller residential properties that do not need riding equipment. Walk-behind units are a practical fit for lawns up to 0.5 acres, which lines up well with compact suburban plots and denser residential development. This is one reason entry and mid-tier mowers remain a large and stable part of category demand. Smaller lawns also make cordless mowing more workable because buyers are less likely to view runtime as a barrier when the cutting job is shorter. This housing pattern broadens the installed base that will eventually enter the replacement cycle, even without a major behavior shift from homeowners. The trend also supports push and self-propelled models because both formats are well matched to the size, maneuverability, and storage needs of compact properties. As more new households settle into these lot profiles, replacement demand should remain structurally supportive over the forecast period.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seasonal demand concentration and weather-linked purchase deferrals | -0.80% | North America and Europe | Short term (≤ 2 years) |

| Battery replacement cost and runtime anxiety in high-duty use cases | -0.90% | Global, most acute in North America and Asia-Pacific commercial markets | Medium term (2-4 years) |

| Fragmented aftermarket service coverage in rural and semi-urban markets | -0.50% | Asia-Pacific, South America, Africa, and rural North America | Long term (≥ 4 years) |

| Emissions and noise compliance pressure on gasoline models | -0.70% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Seasonal Demand Concentration and Weather-Linked Purchase Deferrals

The walk-behind lawn mowers market still depends heavily on a narrow selling season in North America and Europe. Much of the annual demand is concentrated in the spring and early summer window, making revenue timing sensitive to weather patterns beyond the manufacturer's control. A delayed spring, extended rainfall, or a prolonged drought can shift purchases by weeks and disrupt dealer sell-through. This pressure is more noticeable in premium battery products because buyers tend to take longer to make higher-ticket decisions than for lower-cost legacy equipment. Retailers have responded with longer spring promotions, online order pickup, and earlier-season discounts, but those tactics have not fully altered the seasonal structure of demand. That means inventory planning and pricing remain exposed to timing volatility even when category fundamentals stay healthy. The result is not a collapse in demand, but rather uneven quarterly performance that can compress margins for both manufacturers and retailers.

Battery Replacement Cost and Runtime Anxiety in High-Duty Use Cases

Battery economics remain a real restraint for the market in commercial and high-duty use cases. Lithium-ion packs can account for a large share of the cost of a premium mower, and replacement after intensive use can create an expense that buyers closely track. This issue becomes sharper for landscaping crews that cover multiple one-acre properties in a single shift and need repeated battery swaps to complete routes efficiently. Honda Motor Co., Ltd. stated that its HRN-BV mower delivers around 30 minutes of runtime on an 8Ah pack for a quarter-acre cut, which fits many residential needs but remains less suited to uninterrupted commercial operation[4]Source: Honda Power Sports and Products, “Honda HRN-BV Lawn Mower, Features and Benefits,” Honda Newsroom, hondanews.com. Because of that gap, some contractors still view gasoline-powered units as the safer choice for long routes where charging access and downtime matter. Runtime anxiety does not stop battery adoption, but it does slow conversion in the heaviest-duty work settings. Until battery life, charging speed, and pack economics improve further, commercial adoption will continue to lag residential adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Source: Battery Electrification Reshapes Platform Competition

Gasoline-powered models accounted for 41.3% of the walk-behind lawn mowers market size in 2025. This segment maintained the largest share due to its established presence in residential and commercial applications that require extended runtime, higher cutting power, and reliable performance across larger properties. Battery-powered equipment accounted for a significant share of the market, driven by growing consumer preference for lower-noise, lower-maintenance lawn care solutions. Electric corded products catered to a smaller niche, particularly among households with compact lawns and convenient access to power outlets. Manual reel mowers retained a limited but stable market presence, appealing to consumers seeking simple, cost-effective, and environmentally friendly mowing options.

Battery-powered models are anticipated to expand at the fastest pace, advancing at a 11.1% CAGR through 2031. California’s 2024 zero-emission small engine rule changed the direction of demand in a major outdoor power market and strengthened the long-term case for battery investment. Honda Motor Co., Ltd. also accelerated the shift by introducing new battery-powered walk-behind lineups and deepening its focus on cordless products in 2025. As this transition continues, gasoline will retain a role in heavier-duty work, while corded and manual formats will stay concentrated in smaller use cases.

By Product Type: Push Configurations Lead Scale While Self-Propelled Drives Growth

Push mowers held 45.2% of the walk-behind lawn mowers market share in 2025, which made them the largest product type by value. Their lead came from price accessibility, easy storage, and a strong fit with sub-half-acre residential lots. Hover mowers followed as a meaningful secondary choice, particularly for homeowners maintaining uneven terrain, sloped gardens, and irregularly shaped lawns where enhanced maneuverability is valued. Self-propelled units formed the next major layer of demand, while other product types remained smaller and more specialized.

Self-propelled models are anticipated to record the fastest growth, with the market segment estimated to grow at a 6.8% CAGR through 2031. Demand is being helped by aging homeowner demographics, reduced operator effort, and stronger commercial interest in productivity gains on dense routes. The Toro Company supported that direction with the TurfMaster HDX 30-inch with casters, introduced in March 2025 for professional landscaping crews that need maneuverability and stable cutting performance. Push mowers should remain the volume anchor, while hover and other specialized formats will continue to grow from a smaller base.

By Distribution Channel: Dealer Strength Holds While Online Sales Gain Momentum

Specialty retailers and authorized dealers accounted for 65.1% of revenue in 2025, giving them the leading place in the walk-behind lawn mowers market. Their position remained strong because buyers still rely on in-person product explanation, battery education, setup guidance, and post-sale support when choosing higher-value equipment. Commercial purchasers also place weight on service depth and parts access, which favors established dealer networks. Online channels remained smaller, but they continued to close the gap as battery mowers became easier to ship and simpler to prepare for use.

Online sales channels are anticipated to expand at the fastest rate, advancing at a 8.9% CAGR through 2031 in the market. The channel benefits from pricing transparency, broader product selection, and faster fulfillment for buyers who already understand battery platforms. It also aligns with the habits of younger homeowners, who are more comfortable making larger outdoor equipment purchases online. Even so, dealers should remain important because premium cordless products still need stronger service and warranty support than most commodity tools. This means digital growth will be strong, but channel leadership will remain tied to support infrastructure.

By End User: Residential Demand Anchors Volume While Commercial Landscaping Adds Speed

Residential buyers accounted for 55.3% of global demand in 2025, making homes the core volume base of the walk-behind lawn mowers market. This lead reflects the large installed base of privately maintained lawns across North America and Europe and the steady replacement cycle tied to seasonal yard care. Household demand is also being reinforced by buyers who already use battery-powered outdoor tools and are more open to buying cordless mowers. Government and golf course demand remained smaller and more specialized by comparison.

Commercial landscaping is anticipated to grow the fastest, with a 6.7% CAGR through 2031. This acceleration is tied to municipal contracts, commercial property maintenance, and procurement rules that increasingly value lower-noise and lower-emission equipment. Public spaces such as parks, schools, and transportation corridors are also becoming more relevant to the category as contractors refresh older fleets. Golf courses and sports turf operators add another premium use case because they need precision trimming around edges and perimeters. Residential demand will stay broader, but commercial landscaping will add the next growth layer.

Geography Analysis

North America accounted for 44.5% of global revenue in 2025, making it the largest region in the walk-behind lawn mowers market. The region is supported by a large base of single-family homes and a well-established do-it-yourself lawn care culture. California’s 2024 rule on new gasoline-powered small off-road engines changed purchase behavior in a highly visible state and increased the urgency around battery conversion. The United States remains the dominant national contributor because residential ownership patterns create predictable annual replacement demand. Canada is stronger in urban cordless adoption, while Mexico continues to face more price sensitivity and infrastructure constraints in lower-density areas.

Asia-Pacific is the fastest-growing region in the market, with a projected CAGR of 7.1% through 2031. Urbanization remains the primary driver, as expanding residential communities and the preservation of green spaces create new demand across both private and commercial settings. According to the World Bank, about 36% of South Asia’s population lived in urban areas in 2025, highlighting the scale of the landscape being formed across the region. South America, the Middle East, and Africa remain smaller contributors, with growth limited by fragmented retail structures, service gaps, and slower battery adoption outside commercial and hospitality landscaping.

Europe is benefiting from faster gasoline displacement as revised outdoor equipment noise rules increase the compliance burden on louder mower formats. Germany, the United Kingdom, France, and Italy form the core of regional demand because they combine residential lawn maintenance with stronger landscaping service ecosystems. Italy also stands out as a manufacturing base for brands such as STIGA S.p.A. and Emak S.p.A., which helps support product availability across Southern Europe. Nordic countries show stronger adoption of premium cordless models, while Central and Eastern Europe remain earlier in the shift from gasoline to battery products.

Competitive Landscape

The walk-behind lawn mower market is moderately concentrated, with Deere & Company, Husqvarna Group, The Toro Company, Stanley Black & Decker, Inc., and Honda Motor Co., Ltd. accounting for a significant share of global revenue in 2025. Deere & Company held the top position in the market, followed by Husqvarna Group, with no single player holding a dominant market share. Competition is centered on battery ecosystems, runtime, dealer support, and the pace of cordless product launches rather than on price alone. Husqvarna Group strengthened its cordless and autonomous positioning with the launch of 13 boundary wire-free robotic mower models in March 2025, which the company described as its largest launch to date.

Honda Motor Co., Ltd. and The Toro Company are also using product launches to protect relevance as the market shifts toward electrified formats. Honda Motor Co., Ltd. introduced the HRN-BV battery-powered walk-behind mower in October 2025 and expanded its battery zero-turn lineup, signaling a broader commitment to cordless product development. The Toro Company added the redesigned GrandStand Multi Force Evo and Proline AMI in 2025, linking its portfolio more directly to labor efficiency and autonomous commercial operation. These moves show that leading companies are not treating electrification as a side category. They are using it as a core portfolio direction that will shape brand relevance over the next replacement cycle.

The lower end of the market is seeing stronger pressure from battery-native challengers such as Greenworks Tools and Positec Tool Corporation’s WORX brand. Their presence is making entry-level cordless products more competitive and is forcing larger incumbents to defend margins through performance, ecosystem depth, and service access rather than through broad discounting. Dealer-backed support remains a strong advantage for larger brands because battery service, parts access, and product setup still matter in premium categories. That helps explain why market power is meaningful but not absolute, since smaller challengers can gain traction while still struggling to match the support systems of established brands. Overall, competition remains active, but the category still favors companies that can combine product launches, platform compatibility, and post-sale infrastructure at scale.

Walk Behind Lawn Mowers Industry Leaders

Husqvarna Group

The Toro Company

Honda Motor Co., Ltd.

Deere & Company

Stanley Black & Decker, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Honda Motor Co., Ltd. launched the HRN-BV battery-powered walk-behind mower at Equip Exposition 2025. The model is designed, tested, and assembled in the United States, featuring a brushless 1.5 kW motor, patented floating battery contacts, and an 8Ah lithium-ion pack providing 30 minutes of runtime per charge.

- October 2025: The Toro Company debuted the redesigned GrandStand Multi Force Evo and the autonomous Proline AMI at Equip Exposition 2025, targeting commercial landscape contractors. It combines a powerful 34.5 HP Kawasaki EVO engine with a cutting deck to deliver high-performance mowing and superior cut quality in commercial applications.

- March 2025: The Toro Company rolled out the TurfMaster HDX 30-inch with casters, a commercial walk-behind mower designed for landscaping crews that require high maneuverability on tight terrain, incorporating operator feedback from active professional users.

Global Walk Behind Lawn Mowers Market Report Scope

Walk-behind lawn mowers are pedestrian-operated grass-cutting machines that require the user to walk behind the equipment and guide it during operation. They are designed for maintaining lawns, gardens, parks, sports fields, and other turf areas by cutting grass to a uniform height. The Walk-Behind Lawn Mowers Market is segmented by Power Source (Gasoline-Powered, Electric Corded, Battery-Powered, and Manual Reel), by Product Type (Push, Self-Propelled, Hover, and Other Types), by Distribution Channel (Online Sales Channels and Specialty Retailers & Authorized Dealers), by End User (Residential, Commercial Landscaping, Government & Public Spaces, and Golf Courses & Sports Turf), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value.

| Gasoline-Powered |

| Electric Corded |

| Battery-Powered |

| Manual Reel |

| Push |

| Self-Propelled |

| Hover |

| Other Types |

| Online Sales Channels |

| Specialty Retailers and Authorized Dealers |

| Residential |

| Commercial Landscaping |

| Government and Public Spaces |

| Golf Courses and Sports Turf |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Power Source | Gasoline-Powered | |

| Electric Corded | ||

| Battery-Powered | ||

| Manual Reel | ||

| By Product Type | Push | |

| Self-Propelled | ||

| Hover | ||

| Other Types | ||

| By Distribution Channel | Online Sales Channels | |

| Specialty Retailers and Authorized Dealers | ||

| By End User | Residential | |

| Commercial Landscaping | ||

| Government and Public Spaces | ||

| Golf Courses and Sports Turf | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the walk-behind lawn mowers market?

The walk-behind lawn mowers were valued at USD 10.41 billion in 2025, increasing to USD 10.95 billion in 2026, and is projected to reach USD 14.26 billion by 2031.

What is driving battery-powered mower adoption?

Low noise, lower maintenance, tighter emissions rules, and battery ecosystem compatibility across outdoor tools are the main forces supporting battery adoption.

Which product type led the revenue in 2025?

Push mowers led the category with 45.2% of revenue in 2025 because they remain affordable and fit the most common residential lot sizes.

Which sales channel is growing the fastest?

Online sales channels are projected to grow at the fastest rate, with an 8.9% CAGR through 2031, due to pricing transparency and broader product selection.

Page last updated on: