VR Gambling Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

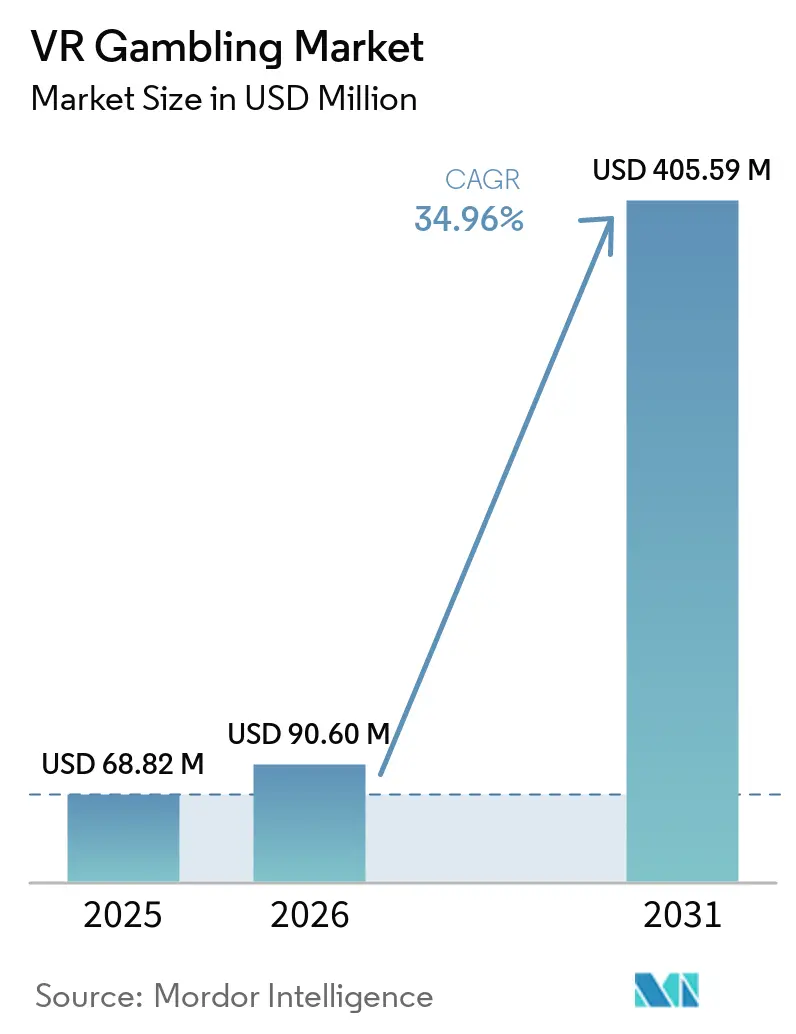

| Market Size (2026) | USD 90.60 Million |

| Market Size (2031) | USD 405.59 Million |

| Growth Rate (2026 - 2031) | 34.96% CAGR |

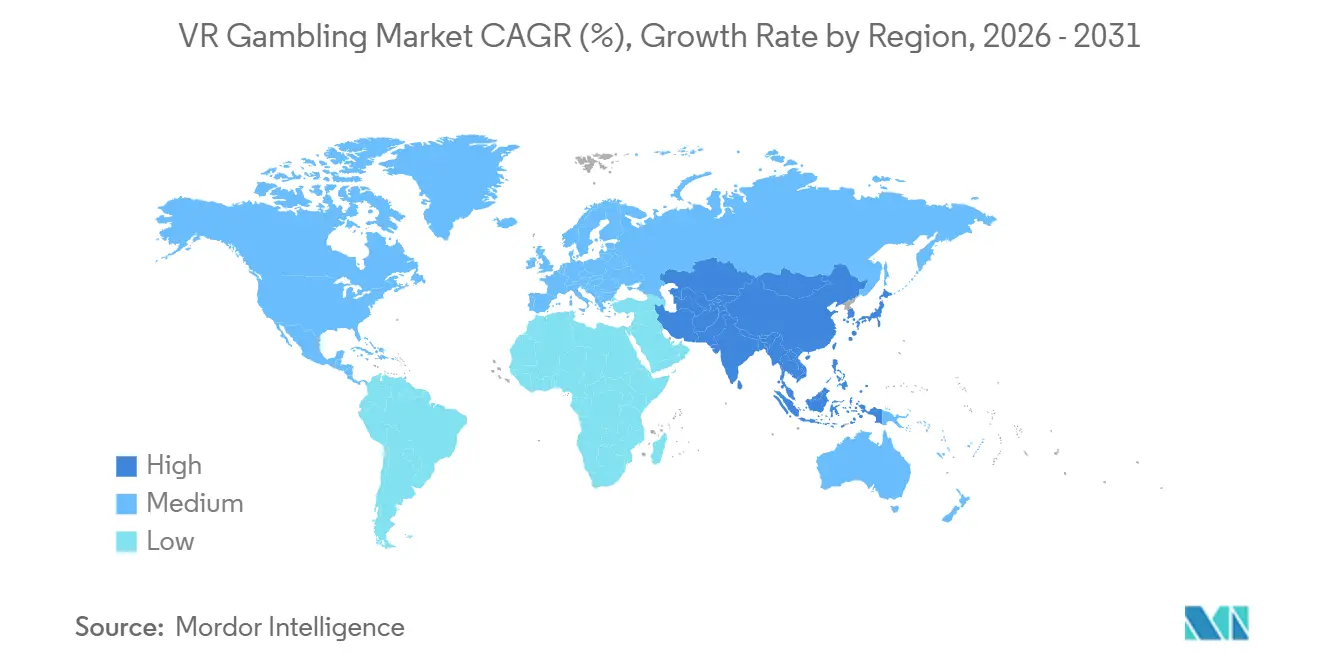

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

VR Gambling Market Analysis by Mordor Intelligence

The VR gambling market size was valued at USD 68.82 million in 2025 and estimated to grow from USD 90.60 million in 2026 to reach USD 405.59 million by 2031, at a CAGR of 34.96% during the forecast period 2026 to 2031. The VR gambling market is moving forward because online wagering audiences are already comfortable spending in digital environments, which reduces the behavioral shift needed for immersive formats to gain traction. Online casino revenue across 7 U.S. states reached USD 10.7 billion in 2025, up 27.6%, and Pennsylvania and New Jersey both saw online casino revenue surpass commercial land-based gaming revenue, indicating that high-value play is already shifting away from physical venues in key regulated states, according to the American Gaming Association[1]Source: American Gaming Association, “State of the States 2026,” American Gaming Association, americangaming.org . North America held 45.82% of the VR gambling market in 2025, supported by record U.S. commercial gaming revenue of USD 78.7 billion, up 9.2%, which gives operators a broad, licensed base from which to test immersive formats, according to the American Gaming Association. The current shape of competition also matters because most leading participants are established iGaming groups, live content suppliers, or sportsbook brands that are extending proven digital products into immersive settings rather than building a new category from scratch. The VR gambling market still faces pressure from tax changes, compliance demands, and responsible gambling rules, yet those same factors are pushing licensed operators to favor richer digital products that can justify higher spending and stronger player retention.

Key Report Takeaways

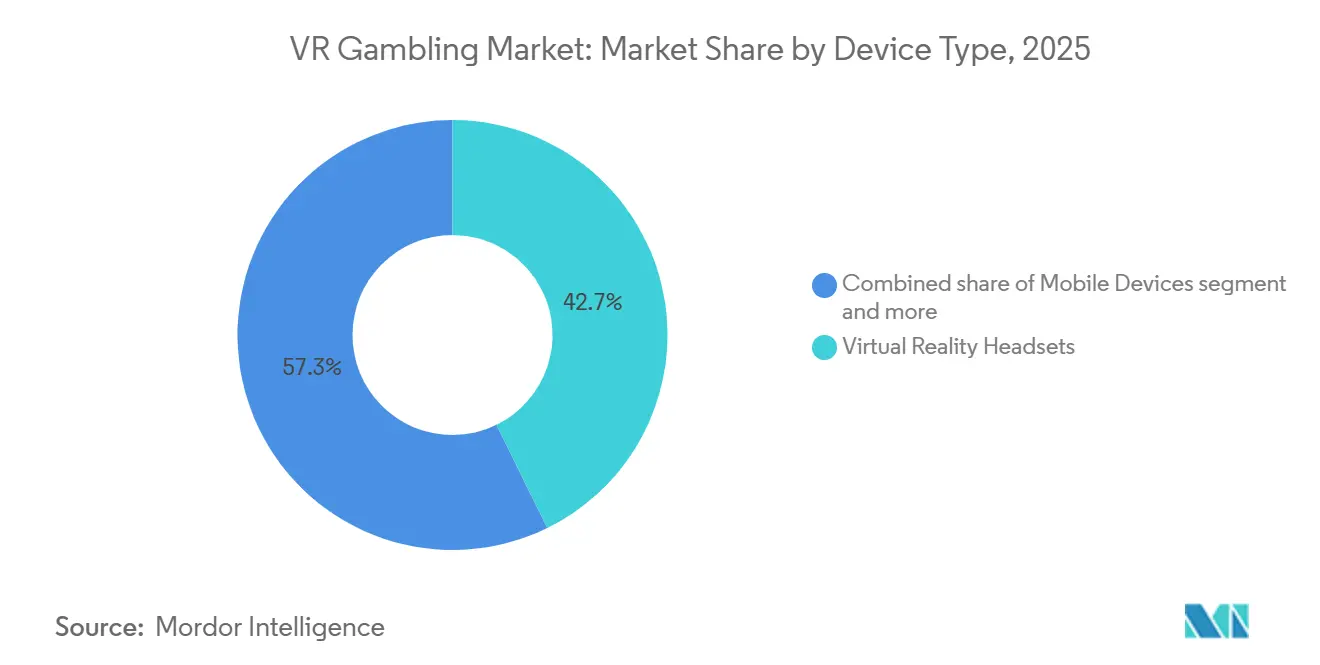

- By device type, VR headsets held 42.73% of the VR gambling market share in 2025, while mobile devices are projected to record the fastest growth at a 36.67% CAGR through 2031.

- By game type, slot machines accounted for 38.56% of the VR gambling market size in 2025, while casino games are forecast to expand at a 36.37% CAGR through 2031.

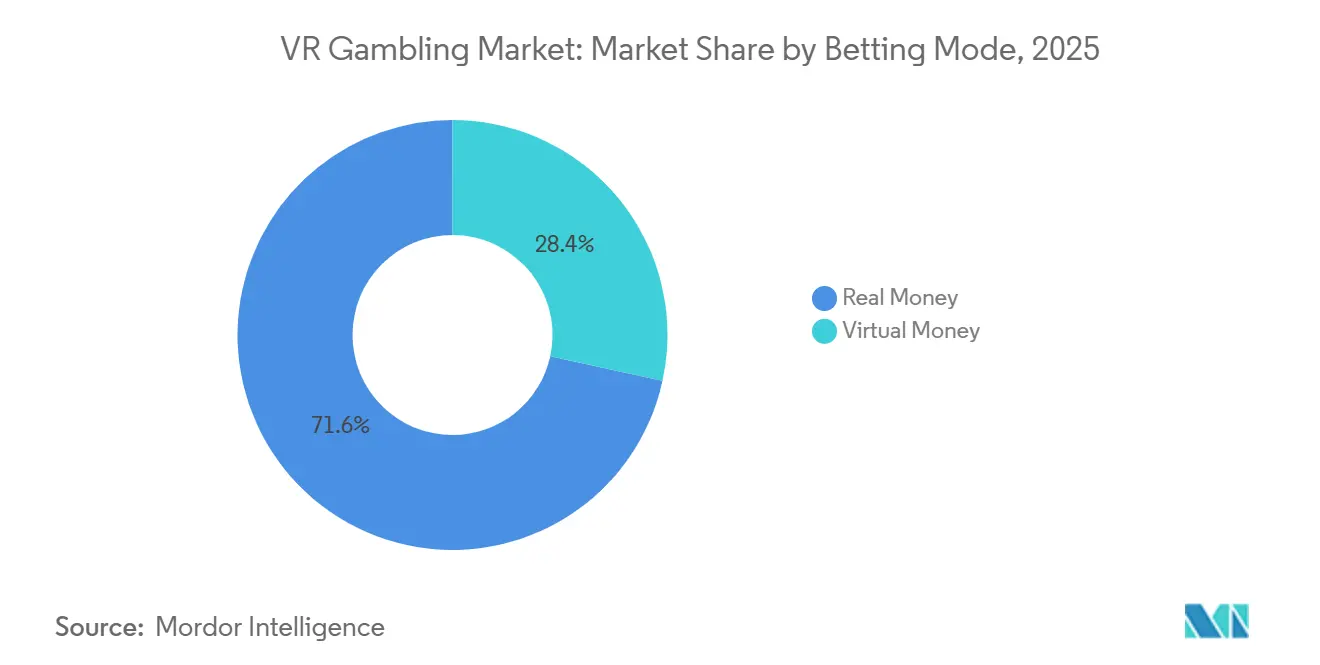

- By betting mode, real money wagering retained 71.58% share in 2025, whereas virtual money gaming is forecast to expand at a 37.86% CAGR through 2031.

- By end user, online casino operators held 27.36% of 2025 revenue, but sportsbook operators are expected to grow fastest at 38.83% through 2031.

- By geography, North America accounted for the largest share of the VR gambling market, at 45.82% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 37.24% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global VR Gambling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Immersive Casino Experiences | +5.5% | Global, North America and Europe leading | Medium term (2-4 years) |

| Expansion of VR-Capable Mobile and Standalone Headsets | +4.8% | Global, with growing APAC pull | Medium term (2-4 years) |

| Operator Push for Higher Session Time and Engagement | +3.2% | North America and Europe | Short term (≤2 years) |

| Live Dealer Integration in Virtual Casino Environments | +4.5% | Global, North America leading | Short term (≤2 years) |

| Payment Innovations Supporting Faster In-Game Wallet Funding | +2.5% | North America, global spill-over | Short term (≤2 years) |

| Regulatory Openings for Online Gambling Content | +6.5% | North America, Oceania, Rest of World | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for immersive casino experiences

The VR gambling market is being shaped by player behavior in online casinos more than by novelty in hardware. U.S. iGaming revenue across 7 states reached USD 10.7 billion in 2025, underscoring that players are already comfortable with remote wagering on regulated digital channels, according to the American Gaming Association. Moreover, Pennsylvania generated USD 3.5 billion in online casino revenue in 2025, up 28.0%, and surpassed commercial land-based casino revenue for the first time, signaling that digital play now has enough depth to support more immersive formats. New Jersey showed the same crossover, which matters because it confirms the pattern is not limited to a single state or operator mix. In that setting, the VR gambling market is not trying to create gambling demand from the ground up; it is trying to convert existing digital demand into a format that feels more social, more present, and more engaging over longer sessions.

Live dealer integration in virtual casino environments

The live dealer channel is the clearest operational bridge between mainstream iGaming and the VR gambling market. Evolution reported 99.90% system uptime in 2025 and entered 2026 with a roadmap of more than 110 new live and RNG releases, demonstrating that the live content infrastructure is already operating at scale and with the reliability operators expect before moving into more immersive formats[2]Source: Evolution AB, “Annual Report 2025,” Evolution AB, evolution.com. Evolution also introduced Ezugi as its second live dealer brand in the U.S., adding more regional production depth to a market that is already central to regulated online casino growth. BetMGM stated that it streams live dealer games from the MGM Grand casino floor in Las Vegas into multiple regulated markets, linking a known physical casino brand with remote play and providing the VR gambling market with a model that can be extended into immersive rooms and table environments. As operators continue to build live environments with higher visual quality, recognizable hosts, and branded game shows, the shift from live video to immersive participation becomes more practical and less speculative.

Regulatory openings for online gambling content

The VR gambling market depends heavily on regulated access, so each new licensing opening has a direct effect on where content can be launched and monetized. The American Gaming Association stated that Maine launched iGaming in early 2026, bringing the U.S. total to 8 licensed iGaming states, expanding the legal footprint for remote casino content and broadening the base for future immersive deployments. France activated the JONUM framework in February 2026 through ANJ, creating a 3-year experimental structure for monetizable digital objects and marking one of the clearest formal acknowledgments in Europe that digital interactive formats need a specific regulatory pathway. The UK continues to be one of the largest online gambling markets in Europe, which keeps it central to any operator that wants scale in immersive digital formats, according to the Gambling Commission. The VR gambling market benefits when regulators expand legal channels, as licensed suppliers gain more room to invest and unlicensed competitors lose some of their pricing and reach advantages.

Payment innovations supporting faster in game wallet funding

Payments are becoming increasingly relevant to the VR gambling market because immersive environments work better when deposits, wallet access, and spending limits are easy to manage within a single session. Paysafe launched Pay with Crypto in April 2026 for U.S. iGaming operators, allowing stablecoin or cryptocurrency deposits to be converted instantly to USD at the player account level. Paysafe also reported in June 2026 that 83% of U.S. bettors would use cryptocurrency for wagering when permitted, suggesting a user base open to faster, more flexible funding tools. That matters because the VR gambling market relies on session continuity, and friction at the deposit stage can undermine the appeal of a high-engagement format. When funding becomes easier but remains within licensed payment controls, operators are better positioned to connect immersive play with responsible spending tools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Consumer Adoption of Dedicated VR Hardware | -3.5% | Global | Short term (≤2 years) |

| High Content Development and Compliance Costs | -2.8% | Global | Medium term (2-4 years) |

| Limited VR-first Casino Content Libraries | -2.2% | Global | Short term (≤2 years) |

| Responsible Gambling Concerns in Immersive Environments | -1.8% | Europe and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Limited consumer adoption of dedicated VR hardware

The VR gambling market still has to work around the fact that dedicated headset ownership remains narrower than smartphone or standard PC usage. That gap affects launch economics because operators need enough active users to justify the cost of custom content, compliance work, and platform testing across multiple hardware environments. It also explains why several established brands are leaning toward cross-platform distribution rather than headset-only deployment, using existing digital player bases to reduce adoption risk. Flutter’s exposure through PokerStars Vegas Infinite clearly shows this pattern, as the company extends a known gambling brand into immersive entertainment while maintaining links to broader digital ecosystems through its larger gaming portfolio. Until immersive access becomes more routine and less hardware-dependent, the VR gambling market is likely to expand through hybrid user journeys rather than a pure headset-first model.

High content development and compliance costs

The VR gambling market also faces higher operational costs than standard digital casino formats because immersive play requires stronger visual design, more testing, and closer regulatory oversight. Operators do not just need game content; they also need payment controls, age and identity checks, responsible gambling tools, and platform processes that can stand up to regulatory scrutiny in regulated markets. The UK’s increase in Remote Gaming Duty to 40% from April 2026 raises pressure on operator margins in one of Europe’s largest online gambling jurisdictions, which can make new format investment harder to justify unless player value is clearly higher, as per the HM Treasury[3]Source: HM Treasury / HM Revenue & Customs, “The Tax Treatment of Remote Gambling, Summary of Responses and Government Response,” UK Government, assets.publishing.service.gov.uk . Responsible gambling statutes and regulations are also expanding across U.S. jurisdictions, which means immersive environments will face closer scrutiny of player protection, session design, and intervention tools. In practical terms, the VR gambling market favors larger operators and major B2B suppliers because they already have the legal, technical, and funding capacity to absorb longer development cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Mobile Devices Reduce Pure Headset Dependence

VR headsets accounted for 42.73% of the VR gambling market in 2025, indicating that early demand remains centered on users who already own immersive hardware and are willing to spend time in premium digital environments. This lead reflects the first wave of adoption, in which the user profile has been closer to existing VR enthusiasts than to the broader online gambling population. At the same time, the device picture is already broadening because the VR gambling market is unlikely to remain tied to a single hardware category for long. Mobile devices are projected to grow at a 36.67% CAGR through 2031, suggesting a more accessible path to immersive wagering than a headset-only model.

That expected shift matters because operators want to meet players where their existing gambling behavior already sits, and that behavior is still heavily mobile across digital wagering. A cross-platform approach lets brands leverage a single content investment across more touchpoints, reducing risk and helping operators reach both premium users and casual digital bettors. Flutter’s broader digital scale makes that strategy credible because it already manages large online player communities and can extend known brands into adjacent formats more efficiently than a smaller specialist can. The VR gambling market therefore looks less like a narrow hardware niche and more like a layered access model where headsets lead the experience, while mobile helps expand reach. As the installed base broadens, the winning device strategy is likely to be the one that balances immersion with convenience rather than insisting on one access route.

By Game Type: Casino Games Gain Ground Through Social Depth

Slots machine held 38.56% of the VR gambling market in 2025, consistent with slot content typically leading online gambling because it is easy to understand, quick to enter, and simple to scale across formats. That made slots the natural starting point for immersive experimentation because they do not require the same depth of social interaction or dealer presence as some other products. Even so, the growth pattern in the VR gambling market is shifting toward more interactive categories that better leverage spatial design and shared environments. Casino games are forecast to grow at a 36.37% CAGR through 2031, which reflects rising operator interest in formats that feel more communal and visually rich.

This pattern is visible in content roadmaps from major suppliers. Evolution used its Hasbro licensing deal and 2026 release pipeline to push branded live content such as MONOPOLY Live and MONOPOLY Roulette, which fit the kind of game-show-style interaction that translates well into immersive casino rooms. Table games and poker also remain relevant because they naturally support voice, presence, and repeat social play, which are all traits that can strengthen retention in immersive settings. The VR gambling market is therefore moving beyond simple one user experiences and toward products where the environment itself adds value. That is why casino games are likely to carry a larger share of premium content investment even while slots remain a major revenue base.

By Betting Mode: Real Money Formats Show Commercial Maturity

Real money wagering held 71.58% of the VR gambling market in 2025, which confirms that the category is already tied more closely to licensed gambling activity than to social entertainment alone. This matters because the commercial case for immersive formats becomes stronger once real deposits, wallet management, and repeat play are already in place. The VR gambling market is not waiting for a future legal model before monetization begins, since operators are already building on frameworks used in broader iGaming. At the same time, virtual money gaming is forecast to grow at a 37.86% CAGR through 2031, indicating that free play and entertainment-led models still play a role in user acquisition and format testing.

The balance between those 2 modes is commercially useful. Real-money products generate direct revenue and anchor the licensed end of the VR gambling market, while virtual-money environments can help operators build familiarity, collect user feedback, and expand communities before conversion. Payment innovation strengthens the real-money side of that equation by enabling easier wallet funding, which supports longer, smoother sessions without pushing users outside the regulated platform. Paysafe’s 2026 launch of Pay with Crypto and its research on bettor interest in crypto funding both support the view that new deposit methods can remove friction at a useful point in the player journey. Over time, the VR gambling market is likely to use virtual money channels as a feeder, while keeping real money formats at the center of long term revenue.

By End User: Sportsbook Operators Open the Next Growth Layer

Online casino operators accounted for 27.36% of the VR gambling market in 2025, which reflects their early start in remote wagering, live content, and player wallet management. They already operate inside the core environment that immersive casino play needs, including regulated payments, account verification, and frequent digital engagement. That makes them the first natural home for the VR gambling market, especially in North America and Europe, where licensed online casino activity is already established. Still, sportsbook operators are projected to grow at a 38.38% CAGR through 2031, which is the faster strategic story within this segment group.

Sportsbooks offer a different advantage because they sit at the intersection of live events, digital communities, and multi-product wallets. DraftKings’ Super App plan combines sportsbook, casino, predictions, and lottery under one account and wallet, making it easier to cross-sell users into richer formats over time. That kind of platform design can support future immersive lounges, live match viewing, or event-themed casino crossover without forcing users to leave the brand ecosystem. The VR gambling industry is therefore likely to see sportsbook operators play a larger role than their current share suggests because they already manage high frequency digital relationships and strong event driven traffic. The fastest growth is likely to come from groups that can connect wagering, entertainment, and wallet access inside one digital environment.

Geography Analysis

North America held 45.82% of the VR gambling market in 2025, giving the region the largest share and the clearest near-term path to licensed immersive play. U.S. online casino revenue reached USD 10.7 billion across 7 states in 2025, up 27.6%, and that scale gives operators a proven digital revenue base from which to test new formats, according to the American Gaming Association. Pennsylvania generated USD 3.5 billion, and both Pennsylvania and New Jersey saw online casino revenue exceed commercial land-based gaming revenue in 2025, demonstrating how far digital behavior has already matured in major jurisdictions. The broader gaming economy is also strong, as U.S. commercial gaming revenue reached USD 78.7 billion in 2025, supporting ongoing investment in digital expansion by large operators, according to the American Gaming Association. In parallel, sports betting tax revenue across U.S. states rose from USD 190 million in the third quarter of 2021 to USD 917 million in the second quarter of 2025, which shows that regulators and state budgets now have a growing stake in licensed remote wagering channels, according to the United States Census Bureau.

Europe remains one of the most important regions for the VR gambling market because it combines large online gambling volumes with deep regulatory oversight. EGBA reported total gross gaming revenue of EUR 21.0 billion in Italy, EUR 19.8 billion in the UK, EUR 14.4 billion in Germany, and EUR 14.0 billion in France, while the UK led online gambling revenue at EUR 11.1 billion. That makes the region attractive for immersive deployment, but it also means operators face higher legal and cost complexity than in simpler licensing environments. The UK increased Remote Gaming Duty from 21% to 40% from April 2026, which raises pressure on operator margins and forces a sharper focus on product formats that can support stronger engagement and better retention. France’s JONUM framework adds another important signal because it creates a formal trial structure for monetizable digital objects, suggesting that regulators are beginning to separate new digital mechanics from older online casino categories. For the VR gambling market, Europe offers scale and purchasing power, but progress depends on whether compliance, tax, and licensing conditions allow operators to earn enough from premium digital products.

Asia Pacific is forecast to grow at a 37.24% CAGR through 2031, giving the VR gambling market its fastest regional expansion profile. The region benefits from strong digital habits and large pools of mobile first users, even though the legal picture is mixed across countries. In Australia, Responsible Wagering Australia reported in January 2026 that 33% of online gambling activity was occurring with illegal offshore operators, and that gap points to meaningful unmet demand for better regulated digital offerings. In the Rest of the World, Flutter’s acquisition of a 56% stake in Brazil’s NSX group for BRL 3,799 million, equivalent to USD 674 million, shows that major operators are building local distribution and licensing positions in markets that could later support immersive gambling products. Taken together, these patterns suggest that the VR gambling market will expand first where digital behavior is already strong and regulated channels are still widening, even if country level progress remains uneven.

Competitive Landscape

The VR gambling market remains fragmented because no single operator or supplier controls the category, and the leading participants come from different parts of the value chain. Flutter brings scale from a broad consumer base, Evolution brings depth in live content, DraftKings brings wallet and app integration, and BetMGM brings strong casino branding tied to physical venues. Flutter reported USD 16.4 billion in fiscal 2025 revenue and 15.9 million average monthly players, which gives it a much larger digital audience than most potential immersive specialists could reach on their own. Evolution reported 99.90% uptime in 2025, and a release plan of more than 110 new live and RNG titles for 2026, which keeps it in a strong position as immersive casino formats remain close to live game show and dealer-led models. The VR gambling market is therefore being shaped less by pure play VR entrants and more by large digital gambling groups that already own player relationships, content pipelines, and regulated operating systems.

The strongest competitive moves so far show a clear pattern. Evolution used its Hasbro partnership to push branded interactive live content such as MONOPOLY Live and MONOPOLY Roulette, giving it recognizable intellectual property and a format that already fits social digital play. DraftKings unveiled its Super App plan in 2026, combining sportsbook, casino, lottery, and predictions under one account and one wallet, which is a practical foundation for immersive cross sell once the format becomes more mainstream. BetMGM’s live dealer streaming from the MGM Grand casino floor also matters because it ties remote wagering to a trusted physical casino brand and gives the VR gambling market a stronger sense of place than a standard digital interface can provide. Flutter’s current VR exposure remains concentrated rather than broad, but that is not a sign of weakness on its own because it already has the distribution power to scale faster once immersive economics improve. The commercial edge is likely to stay with companies that can combine content, compliance, and brand trust in one operating model.

The VR gambling market also shows a clear divide between strategic capacity and immediate execution. Large operators have the budgets and licensed footprints to invest, but they are moving carefully because taxes, player protection rules, and product approval processes still shape returns. The UK duty increase and ongoing expansion of responsible gambling rules show that regulators are becoming more active rather than less active as remote wagering grows. That means the most durable position in the VR gambling market is likely to belong to companies that can prove compliance, maintain strong uptime, and extend trusted brands across both digital and venue linked experiences. Over the next few years, competitive leadership will depend less on being first to launch and more on being able to scale immersive play inside fully regulated ecosystems.

VR Gambling Industry Leaders

Flutter Entertainment plc

Evolution AB

Entain plc

DraftKings Inc.

Playtech plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Evolution AB launched MONOPOLY Live in Michigan from its new Grand Rapids studio, following successful rollouts in New Jersey, Delaware, and Connecticut; the expansion extends the operator's exclusive Hasbro licensed interactive content to a fifth U.S. iGaming market, adding a significant premium live game show title to the state's online casino product mix.

- January 2026: DraftKings announced "DraftKings Sports & Casino," a unified Super App integrating Sportsbook, Predictions, Casino, and Lottery into a single account and wallet, with Phase 1 integration timed to the NCAA Tournament and further upgrades planned throughout 2026, a platform consolidation that creates the single wallet infrastructure required for seamless VR casino cross sell.

- October 2025: Evolution AB launched Ezugi as a second live dealer brand in the U.S., streaming from an Atlantic City studio in New Jersey, with Michigan studio expansion confirmed for early 2026, consolidating the company's U.S. live streaming infrastructure as the technical foundation for future VR dealer integration.

Global VR Gambling Market Report Scope

VR gambling refers to gambling experiences delivered through virtual reality technologies, enabling immersive casino and betting environments using digital simulations and interactive gameplay. The VR gambling market is segmented by device type, game type, betting mode, end user, and geography. By device type, the market includes virtual reality, augmented reality, and mixed reality headsets, as well as mobile devices. Based on game type, the market covers slot machines, table games, sports betting, casino games, poker, and other game formats. By betting mode, the market is divided into real-money and virtual-money betting. Based on end user, the market includes individual players, online casino operators, land-based casinos, sportsbook operators, game studios/platform providers, and other users. Geographically, the report covers North America, Europe, Asia-Pacific, and the Rest of the World, with market sizes and forecasts for each region. The VR gambling market size has been calculated in USD for all the above-mentioned segments.

| Virtual Reality Headsets |

| Augmented Reality Headsets |

| Mixed Reality Headsets |

| Mobile Devices |

| Slot Machines |

| Table Games |

| Sports Betting |

| Casino Games |

| Poker |

| Others |

| Real Money |

| Virtual Money |

| Individual Players |

| Online Casino Operators |

| Land-based Casinos |

| Sportsbook Operators |

| Game Studios/Platform Providers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | Oceanic Countries |

| Rest of Asia-Pacific | |

| Rest of the World | South America |

| Middle East and Africa |

| By Device Type | Virtual Reality Headsets | |

| Augmented Reality Headsets | ||

| Mixed Reality Headsets | ||

| Mobile Devices | ||

| By Game Type | Slot Machines | |

| Table Games | ||

| Sports Betting | ||

| Casino Games | ||

| Poker | ||

| Others | ||

| By Betting Mode | Real Money | |

| Virtual Money | ||

| By End User | Individual Players | |

| Online Casino Operators | ||

| Land-based Casinos | ||

| Sportsbook Operators | ||

| Game Studios/Platform Providers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | Oceanic Countries | |

| Rest of Asia-Pacific | ||

| Rest of the World | South America | |

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the forecast size of VR gambling by 2031?

The VR gambling market is projected to reach USD 405.59 million by 2031 from USD 90.60 million in 2026, growing at a 34.96% CAGR.

Which region currently leads global demand?

North America led with 45.82% in 2025, supported by mature regulated iGaming markets and strong online casino revenue in the United States.

Which device category is growing fastest?

Mobile devices are expected to grow the fastest at a 36.67% CAGR through 2031 because they reduce dependence on dedicated headsets.

Why are sportsbook operators becoming more important?

Sportsbook operators are projected to grow at a 38.38% CAGR because they already manage high traffic digital wallets, live event engagement, and broad product ecosystems.

Page last updated on: