Virtual Reality (VR) Corporate Training Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 16.64 Billion |

| Market Size (2031) | USD 41.10 Billion |

| Growth Rate (2026 - 2031) | 19.82% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Virtual Reality (VR) Corporate Training Market Analysis by Mordor Intelligence

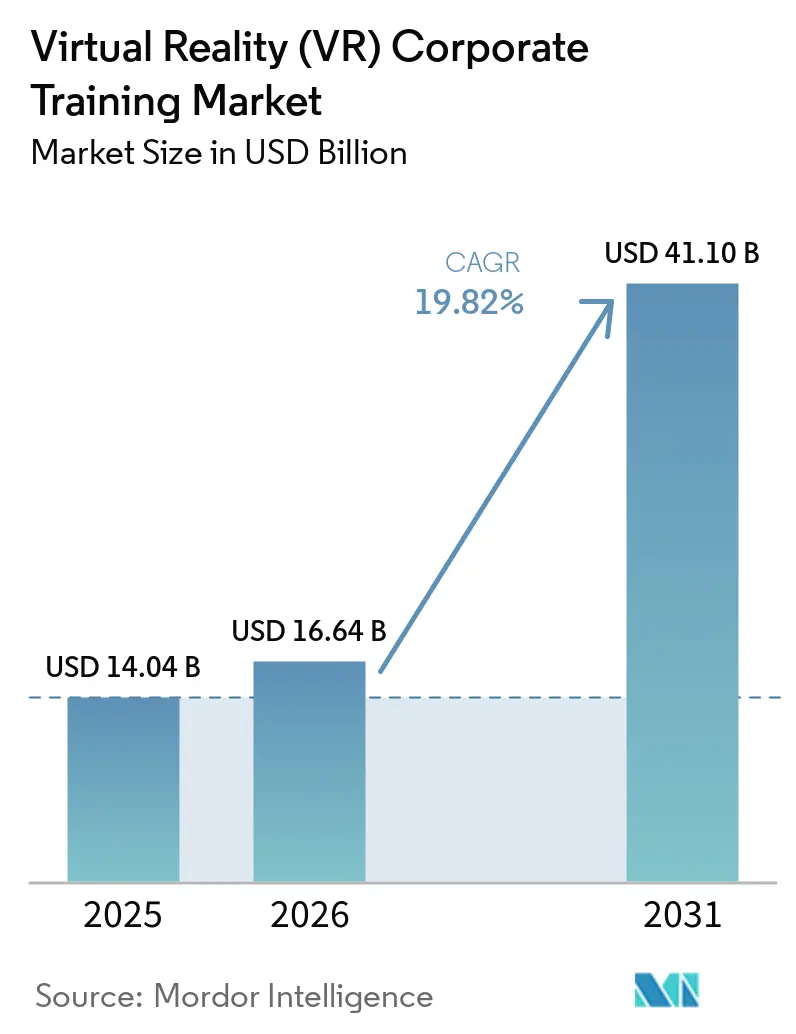

The virtual reality (VR) corporate training market size was valued at USD 14.04 billion in 2025 and estimated to grow from USD 16.64 billion in 2026 to reach USD 41.10 billion by 2031, at a CAGR of 19.82% during the forecast period (2026-2031). Workforce development teams now treat immersive training as a production-ready layer, as measurable training outcomes are documented in operating environments, not just in pilots. A 2025 study in Scientific Reports found that industrial workers trained through VR improved safety awareness by 30%, safety knowledge by 25%, and risk awareness by 30% compared with conventional methods. That advantage is shortening procurement cycles in industrial, healthcare, and defense settings where employers want auditable performance records and faster time to competency. The virtual reality (VR) corporate training market is also benefiting from cloud delivery, scalable content management, and AI-assisted scenario creation that help enterprises move from isolated deployments to repeatable programs. Regulatory caution around biometric data and long IT validation cycles still slows some rollouts, yet workforce shortages, distributed operations, and the need for safer training environments continue to support demand.

Key Report Takeaways

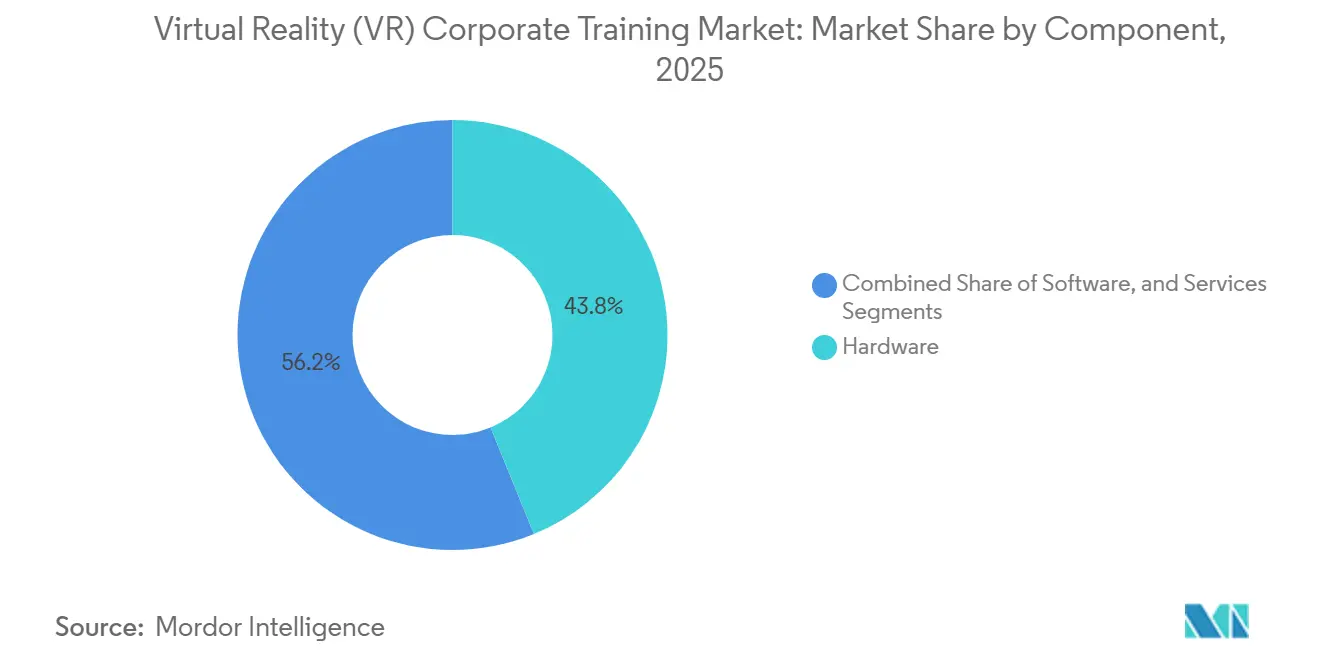

- By component, hardware led with 43.81% of virtual reality (VR) corporate training market share in 2025, while software is forecast to expand at a 22.42% CAGR through 2031.

- By deployment mode, cloud-based delivery held 58.62% of virtual reality corporate training market share in 2025, while hybrid deployment is projected to record the highest CAGR at 21.36% through 2031.

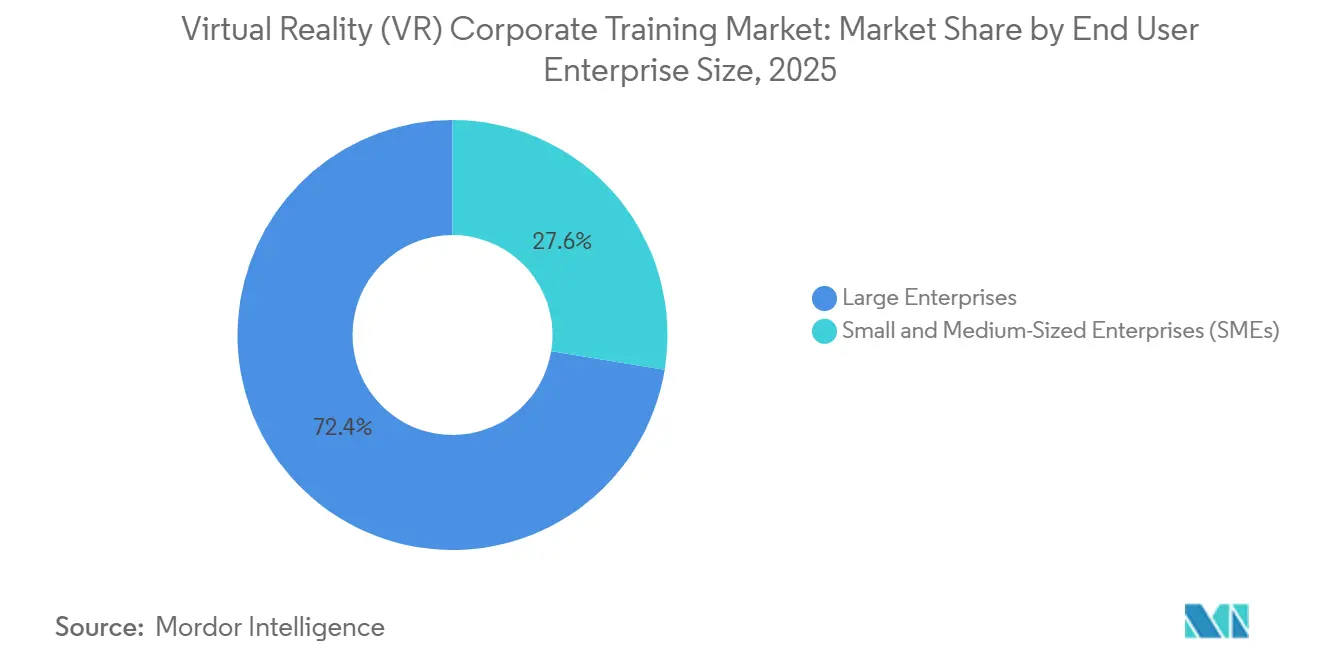

- By end-user enterprise size, large enterprises accounted for 72.41% of the market share in 2025, while SMEs are expected to grow at a 23.12% CAGR through 2031 in the VR corporate training market.

- By training type, safety and compliance training captured 28.91% of the market in 2025, while soft skills and leadership training are projected to advance at a 24.61% CAGR through 2031.

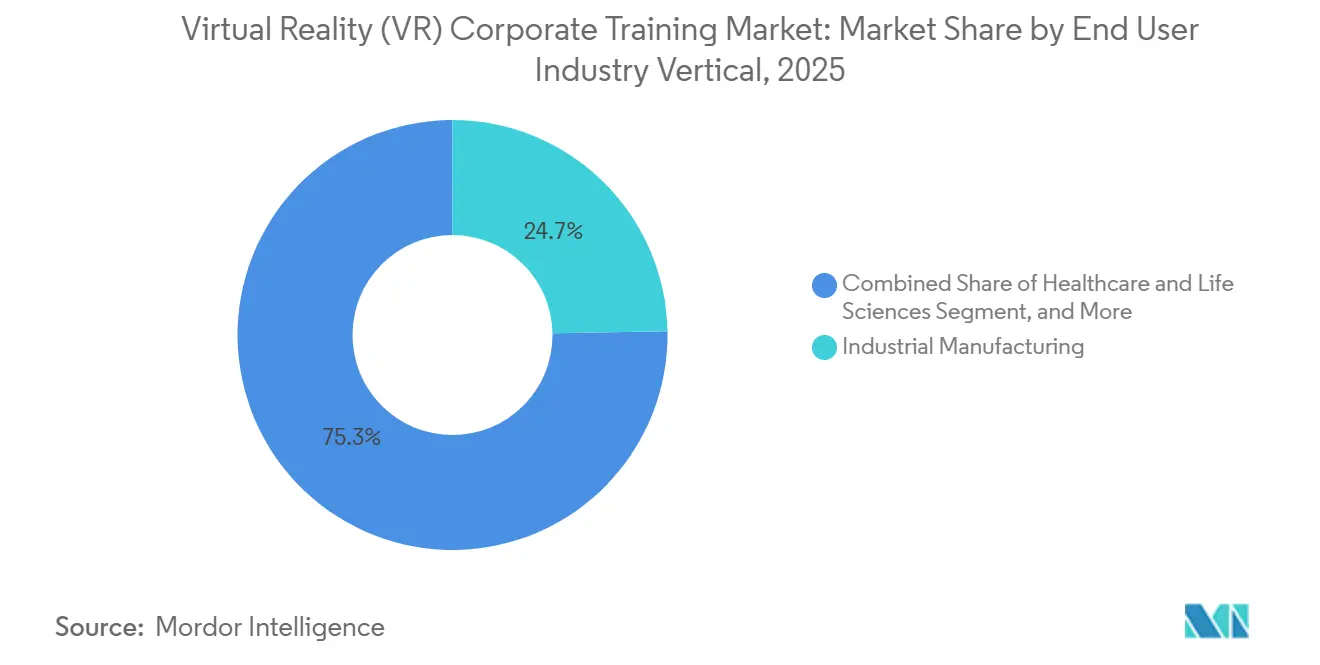

- By end-user industry vertical, industrial manufacturing held a 24.72% share of the virtual reality (VR) corporate training market in 2025, while healthcare and life sciences are forecast to grow at a 25.21% CAGR through 2031.

- By geography, North America held 36.51% share in 2025, while Asia-Pacific is projected to expand at a 23.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Virtual Reality (VR) Corporate Training Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proven Reduction in Training Time and Error Rates | +3.5% | Global | Short term (≤ 2 years) |

| Rising Need for Safe Simulation in High-Risk Workflows | +2.8% | Global, core in North America and Europe | Medium term (2-4 years) |

| Standardization of Training Across Distributed Workforces | +2.4% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Falling Deployment Friction From Standalone Headsets and Cloud Delivery | +2.2% | Global, core in APAC and SME-dense markets | Short term (≤ 2 years) |

| AI-Generated Scenario Authoring Compressing Custom Content Backlogs | +1.9% | North America and Europe, APAC emerging | Medium term (2-4 years) |

| Audit-Ready Skills Telemetry Supporting Regulated Competency Assurance | +1.5% | North America and Europe (regulated industries) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proven Reduction In Training Time And Error Rates

In the virtual reality (VR) corporate training market, adoption rises fastest when employers can tie immersive learning to a faster time-to-competency. A 2025 review covering 37 peer‑reviewed studies found that VR‑based safety training produced stronger immediate knowledge acquisition and hazard identification than traditional classroom formats. The same review showed that traditional training groups lost declarative knowledge much faster over comparable periods, underscoring VR’s value beyond the session. A separate 2025 study found that industrial workers improved safety awareness by 30%, safety knowledge by 25%, and risk awareness by 30% after VR training. Reports also showed that average training duration fell from 120 minutes in classroom settings to 30 minutes with VR in enterprise use cases. This mix of shorter training time and stronger retention supports recurring investment when organizations need repeat certification across large workforces.[1]Al-Hamad, Abdallah, Mohammad Wedyan, and Attila Gilányi. "Virtual Reality Safety Training and Auditing in Warehouse Environments, AHP and Critical Thinking Approach." Cognition, Technology and Work. June 2, 2025. springer.com

Rising Need For Safe Simulation In High-Risk Workflows

The virtual reality corporate training market has a clear use case in high‑risk workflows, as live practice exposes workers to injury, equipment damage, and downtime. VR lets workers repeat hazardous tasks in a controlled environment without risking people or assets. A 2025 study found that 86.67% of warehouse‑environment experts rated VR safety training as effective and realistic. The same study found that 75% of respondents considered VR safety training cost‑effective. Another 2025 study also showed measurable gains in safety awareness and risk awareness among industrial workers trained with VR. As logistics, manufacturing, and construction employers seek safer rehearsal methods, immersive simulation is moving closer to the core of the virtual reality corporate training market.[2]Demmerle, Sebastian. "VR Training Für Unternehmen." NMY. June 30, 2025. nmy.de

Standardization Of Training Across Distributed Workforces

The VR corporate training market is also benefiting from the need to deliver the same training standard across large, distributed workforces. Traditional methods often vary by location, instructor quality, and shift timing, which weakens content consistency and assessment rigor. VR reduces that variation because every learner moves through the same scenario, the same prompts, and the same scoring logic. One company used VR safety simulations for more than 20,000 flight attendants annually and reported savings of EUR 14 million (USD 15.26 million) compared with real‑environment training programs. Further reports show that enterprise buyers increasingly expect integration with learning systems such as Workday, Cornerstone, and Docebo, which reflects how tightly immersive learning is now tied to workforce systems in the virtual reality (VR) corporate training market.

Falling Deployment Friction From Standalone Headsets And Cloud Delivery

The VR corporate training market is seeing fewer deployment barriers as standalone headsets and cloud delivery eliminate the need for PC‑tethered setups. Organizations can now launch training fleets with less cabling, reduced site preparation, and simpler device logistics. Cloud platforms also allow teams to update content across distributed headset fleets without manual reimaging at every location. One provider reported that its builder tool reduced the time required for custom VR module development by 93% through AI‑powered assembly. It also noted that many standard procedural training modules now fall within the USD 5,000 to USD 15,000 range rather than in the six‑figure custom-build range. Lower setup friction is widening the addressable market for virtual reality corporate training, especially among buyers who previously delayed adoption due to cost and IT effort.[3]Connelly, Leslie. "Immersive Virtual Reality Training Can Enhance Construction Site Safety." ASCE Civil Engineering Source. November 25, 2025. asce.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Custom Content, Integration, and Fleet Rollout | -2.5% | Global | Medium term (2-4 years) |

| Motion Sickness, Headset Fatigue, and Hygiene Constraints in Repeated Use | -1.8% | Global | Long term (≥ 4 years) |

| Biometric and AI-Governance Scrutiny Over Eye-Gaze, Voice, and Behavioral Data | -1.3% | North America and Europe (GDPR, EU AI Act) | Medium term (2-4 years) |

| Procurement Delays From Cybersecurity and Identity-Stack Validation Requirements | -0.9% | North America and Europe (strict IT governance) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Of Custom Content, Integration, And Fleet Rollout

The virtual reality (VR) corporate training market still faces hesitation when buyers evaluate the full first-year cost of custom content, systems integration, and device fleets. VRC reported that professional interactive modules historically required USD 50,000 to USD 200,000 per completed hour of content, with ongoing maintenance needed to keep scenarios aligned with changing procedures. The same source said programs for 100 to 200 users in year 1 can range from USD 150,000 to USD 300,000, once hardware, licensing, and IT integration are included. This burden is hardest for organizations with small specialist crews or infrequent training because the payback period is longer. AutoVRse and other no-code approaches are reducing development time and easing pressure on custom build costs, but highly specific workflows still require design, validation, and internal process mapping. For that reason, some buyers in the virtual reality (VR) corporate training market still phase rollouts site by site instead of expanding immediately across the full enterprise.

Motion Sickness, Headset Fatigue, And Hygiene Constraints In Repeated Use

The VR corporate training market also remains constrained by motion sickness, headset fatigue, and hygiene issues in repeated-use programs. A 2026 arXiv study found that VR-induced cybersickness raised salivary cortisol levels for up to 90 minutes after exposure and reduced working memory performance. That matters in aviation, surgery, and heavy equipment settings because the training session itself can affect near-term readiness. VRC reported that 20% to 40% of users experience meaningful discomfort during artificial locomotion scenarios, while 5% to 15% find continuous movement intolerable. Shared-headset programs also require cleaning, face cushion changes, and interpupillary distance resets, which add to turnover time between learners. These frictions do not stop adoption, but they push providers in the virtual reality corporate training market to favor shorter sessions, better scenario design, and more disciplined device operations.[4]Zielasko, Daniel, Ben Rehling, Bernadette von Dawans, and Gregor Domes. "Do Not Immerse and Drive? Prolonged Effects of Cybersickness on Physiological Stress Markers and Cognitive Performance." arXiv. February 2, 2026. arxiv.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Scale Meets Software Speed

Hardware captured 43.81% of the virtual reality (VR) corporate training market share in 2025, which reflected the cost of enterprise fleet buildouts across multi-site organizations. Standalone headsets led most new deployments because they reduced setup complexity and lowered the ownership burden for buyers. Tethered systems kept a premium role in surgical, aviation, and defense training where higher visual fidelity still mattered. Controllers, trackers, and haptic tools gained relevance in maintenance and equipment simulation because they added interaction, which improved procedural realism. The virtual reality (VR) corporate training market, remained hardware-heavy at the point of first rollout, even when buyers planned to shift value capture toward software over time.

Software is projected to expand at a 22.42% CAGR from 2026 to 2031, making it the fastest-growing component in the virtual reality (VR) corporate training market. The shift is moving from bespoke engine development toward no-code authoring platforms that let internal learning teams build modules faster. Cloud content management, behavioral analytics, and LMS integration are becoming baseline software requirements rather than optional add-ons. A 2026 study in Virtual Reality found that AI-LLM-integrated VR training outperformed standard VR on knowledge acquisition, 1-week retention, and trainee self-efficacy. Services remain important within the VR corporate training industry because many enterprises still need outside support for custom scenario design, rollout planning, and managed operations.

By Deployment Mode: Cloud Leads, Hybrid Gains

Cloud-based delivery captured 58.62% of the virtual reality (VR) corporate training market in 2025, underscoring a strong preference for scalable content management. Cloud delivery helps organizations push updated modules to global headset fleets without reimaging devices at each site. That advantage matters most in compliance programs where outdated content can create audit problems. On-premises deployments still matter in defense, finance, and other tightly controlled environments that require stronger data residency or isolated systems. The virtual reality corporate training market has therefore favored cloud, where scale and update speed matter, while preserving on-premises options for higher-control use cases.

Hybrid deployment is forecast to grow at a 21.36% CAGR through 2031 in the virtual reality (VR) corporate training market. This model combines cloud-scale distribution with local identity controls and local handling of sensitive performance data. That balance is gaining relevance as employers review how eye-gaze, voice, and behavioral data fit within GDPR and newer AI-governance rules. Hybrid architectures are especially relevant for large enterprises that want centralized content management without giving up tighter internal security workflows. Deployment choices in the virtual reality (VR) corporate training market are therefore being shaped more by privacy governance and enterprise IT policy than by device type or bandwidth.

By End User Enterprise Size: Large Enterprises Anchor, SMEs Accelerate

Large enterprises accounted for 72.41% of spending in 2025, which kept the virtual reality (VR) corporate training market anchored in organizations with broader rollout budgets. These buyers could absorb headset fleet costs, integration work, and internal change management across many sites. They also had the staff needed to manage learning content pipelines, identity systems, and support processes after deployment. In practice, large enterprises use VR to standardize repetitive training where quality variation across sites creates operational risk. Their scale gave the virtual reality (VR) corporate training market an early base of recurring demand and reference deployments.

SMEs are projected to expand at a 23.12% CAGR through 2031, making them the fastest-growing buyer group in the virtual reality (VR) corporate training market. Lower headset prices, per-user SaaS pricing, and pre-built scenario libraries have reduced three early barriers: device cost, custom content spending, and IT complexity. This shift matters because smaller firms often need the same safety and process-consistency benefits as large enterprises but cannot support the long payback periods required. As software tools simplify content creation, more of the virtual reality (VR) corporate training industry can move from bespoke projects toward repeatable subscription models. That change supports broader adoption across mid-market operations, especially where training demand is steady and geographically dispersed.

By Training Type: Safety Dominates, Soft Skills Drive Growth

Safety and compliance training accounted for 28.91% of spending in 2025, making it the largest use case in the virtual reality (VR) corporate training market. The category remains strong because many high-risk procedures cannot be performed repeatedly in live environments without incurring costs or risks. VR makes those scenarios repeatable while keeping the training setting controlled and auditable. Technical operations, maintenance, equipment simulation, and onboarding also held meaningful shares because procedural tasks fit well with immersive rehearsal. Early adoption of customer interaction training remained small, though better avatar conversations are expanding that use case.

Soft skills and leadership training are projected to grow at a 24.61% CAGR through 2031 in the virtual reality (VR) corporate training market. Mursion reports that 4 10-minute simulation sessions produced measurable behavior change in leadership communication, and that 90% of leaders demonstrated competency in change-management conversations after training. The growth driver is stronger conversational realism because AI-enabled avatars can sustain more natural dialogue than earlier rule-based systems. Bodyswaps also shows that NHS Primary Care scaled this type of training to sessions with more than 40 learners, signaling that the delivery model is moving beyond small pilots. As a result, the virtual reality (VR) corporate training market is broadening from procedural use cases into managerial communication, empathy, and feedback training.

By End User Industry Vertical: Manufacturing Leads, Healthcare Surges

Industrial manufacturing accounted for 24.72% of the virtual reality (VR) corporate training market in 2025, reflecting strong demand for safe, repeatable process training. Manufacturers need consistent assembly steps, maintenance practices, and safety routines across multiple plants. A 2025 Scientific Reports study found that VR-trained industrial workers improved safety awareness by 30%, safety knowledge by 25%, and risk awareness by 30% compared with conventional methods. That evidence supports manufacturing demand because the benefit connects directly to plant safety and process consistency. The virtual reality (VR) corporate training market also draws industrial demand from construction, utilities, and logistics, where operational errors carry direct costs and safety consequences.

Healthcare and life sciences are forecast to grow at a 25.21% CAGR through 2031, making it the fastest-growing vertical in the virtual reality (VR) corporate training market. Osso VR states that learners trained on its platform required 67% fewer instructor prompts and achieved procedural competence scores up to 300% higher than those in traditional methods. Oxford Medical Simulation said in March 2026 that it had secured GBP 5 million (USD 6.35 million) to expand into U.S. health systems and advance AI-driven scenario development. Osso VR also expanded its nurse training proposition in 2025, which shows that the vertical is moving from specialist procedures toward broader frontline onboarding. This leaves the virtual reality (VR) corporate training market well-positioned in healthcare, where educator shortages and competency documentation needs are reinforcing adoption.

Geography Analysis

North America held 36.51% of the virtual reality (VR) corporate training market share in 2025, maintaining its leading position. The United States drove most of that demand through earlier enterprise adoption across manufacturing, retail, healthcare, and financial services. The region also benefits from a dense vendor base, including providers focused on safety, healthcare simulation, soft skills, and enterprise deployment. This concentration helps buyers compare vendors, pilot faster, and expand from one use case into broader learning programs. In the virtual reality (VR) corporate training market, North America therefore remained the clearest reference point for scaled enterprise deployment.

Europe remained the second-largest region in the virtual reality (VR) corporate training market, led by Germany, the United Kingdom, and France. NMY reported that Lufthansa Aviation Training used VR safety simulations for more than 20,000 flight attendants annually and achieved EUR 14 million (USD 15.26 million) in savings relative to traditional formats. Uptale announced a strategic alliance with VRdirect in April 2025 to serve more than 350 enterprise customers across Europe, North America, and Asia, which strengthened regional platform reach. Europe also faces tighter scrutiny of biometric and inferred data under GDPR and related AI governance rules, which can slow procurement but also reward privacy-focused platform design.

Asia-Pacific is projected to expand at a 23.81% CAGR through 2031, making it the fastest-growing region in the virtual reality corporate training market. Industrial workforce scale, expanding domestic headset ecosystems, and public workforce upskilling programs are supporting adoption across the region. India, China, Japan, South Korea, Singapore, and Australia align well with VR training because they combine large labor pools with sector-specific skills gaps. The Middle East is also increasing investment in construction, energy, government, and defense programs, while South America is building momentum from manufacturing digitization and workforce modernization. Africa remains earlier in adoption, but mining, energy, and government use cases provide a strong base for the VR corporate training market in countries such as South Africa, Egypt, and Nigeria.

Competitive Landscape

The virtual reality (VR) corporate training market remained moderately fragmented, with specialist providers spread across safety training, soft skills, healthcare simulation, authoring, and device management. No single vendor held a dominant cross-segment share, so competition centered on fit by use case rather than on broad platform control. The field can be grouped into vertical specialists, horizontal platform providers, and implementation partners that connect immersive learning with LMS and HR systems. This structure keeps switching options open for buyers, but it also raises the value of integration quality and analytics depth. In the virtual reality (VR) corporate training market, the battleground is moving away from headset novelty and toward measurable performance data and faster content creation.

Vendors that once competed mainly on content quality are now under pressure to show cleaner workflow integration and clearer competency tracking. AI-supported scenario generation is becoming increasingly central as enterprises seek to turn SOPs, clinical pathways, and service scripts into deployable modules faster. Oxford Medical Simulation’s March 2026 financing was directed toward U.S. expansion and AI-driven scenario development, which shows where value creation is moving in healthcare training. In the virtual reality corporate training market, software layers that connect authoring, analytics, and deployment are increasingly the key differentiator.

Partnerships and product extensions are also shaping the next phase of competition. Uptale and VRdirect joined forces in April 2025 to expand their enterprise reach across Europe, North America, and Asia. Osso VR partnered with EBSCO in November 2025 to add Dynamic Health content to its nurse training platform, which tied immersive scenarios more closely to clinical reference content. Facilitate and VR Expert also announced a partnership in November 2025 to combine no-code software with hardware supply across Europe and North America. These moves show that the VR corporate training market is consolidating around integrated content, distribution, and domain-specific expertise rather than around hardware alone.

Virtual Reality (VR) Corporate Training Industry Leaders

-

Strivr Labs, Inc.

-

VRdirect GmbH

-

PixoVR, Corp.

-

Transfr Inc.

-

Virti Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Oxford Medical Simulation raised GBP 5M from Salica Investments to expand in U.S. health systems and advance AI-driven scenario development.

- January 2026: Meta ended commercial Quest SKUs, repositioned Horizon Managed Services as free, with support until 2030, creating fleet-strategy uncertainty.

- November 2025: Osso VR partnered with EBSCO to add Dynamic Health content to its nurse training platform; Facilitate teamed with VR Expert for hardware-software integration in energy, manufacturing, and education.

- October 2025: Osso VR launched early access to Osso Nurse Training, combining VR scenarios with Osso Loop for onboarding, dashboards, and competency tracking.

Global Virtual Reality (VR) Corporate Training Market Report Scope

The virtual reality corporate training market refers to the use of immersive simulation technologies to deliver standardized, scalable, and engaging workforce education. By enabling risk‑free practice, faster time to competency, and stronger knowledge retention, VR training reduces costs and logistical barriers while ensuring consistency across distributed teams. This market is expanding as enterprises integrate VR into core learning systems to enhance safety, efficiency, and workforce readiness.

The Virtual Reality (VR) Corporate Training Market Report is segmented by Component (Hardware [Standalone Head-Mounted Displays, Tethered Head-Mounted Displays, Controllers, Trackers, and Peripherals, and Haptics and Accessories], Software [Content Authoring and Scenario Design, Content Management and Delivery Platforms, Analytics and Assessment Software, and LMS and HRIS Integration Software], and Services [Custom Content Development, Implementation and Systems Integration, Managed Device and Program Operations, and Support and Maintenance]), Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Training Type (Safety and Compliance Training, Technical and Operational Training, Soft Skills and Leadership Training, Sales and Customer Interaction Training, Onboarding and Employee Orientation, and Equipment Simulation and Maintenance Training), Industry Vertical (Industrial Manufacturing, Healthcare and Life Sciences, Retail and Ecommerce, Energy and Utilities, Transportation and Logistics, BFSI, Construction and Engineering, and Government, Defense, and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware | Standalone Head-Mounted Displays |

| Tethered Head-Mounted Displays | |

| Controllers, Trackers, and Peripherals | |

| Haptics and Accessories | |

| Software | Content Authoring and Scenario Design |

| Content Management and Delivery Platforms | |

| Analytics and Assessment Software | |

| LMS and HRIS Integration Software | |

| Services | Custom Content Development |

| Implementation and Systems Integration | |

| Managed Device and Program Operations | |

| Support and Maintenance |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| Safety and Compliance Training |

| Technical and Operational Training |

| Soft Skills and Leadership Training |

| Sales and Customer Interaction Training |

| Onboarding and Employee Orientation |

| Equipment Simulation and Maintenance Training |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Retail and Ecommerce |

| Energy and Utilities |

| Transportation and Logistics |

| BFSI |

| Construction and Engineering |

| Government, Defense, and Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Component | Hardware | Standalone Head-Mounted Displays |

| Tethered Head-Mounted Displays | ||

| Controllers, Trackers, and Peripherals | ||

| Haptics and Accessories | ||

| Software | Content Authoring and Scenario Design | |

| Content Management and Delivery Platforms | ||

| Analytics and Assessment Software | ||

| LMS and HRIS Integration Software | ||

| Services | Custom Content Development | |

| Implementation and Systems Integration | ||

| Managed Device and Program Operations | ||

| Support and Maintenance | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By End User Enterprise Size | Large Enterprises | |

| Small and Medium-Sized Enterprises | ||

| By Training Type | Safety and Compliance Training | |

| Technical and Operational Training | ||

| Soft Skills and Leadership Training | ||

| Sales and Customer Interaction Training | ||

| Onboarding and Employee Orientation | ||

| Equipment Simulation and Maintenance Training | ||

| By End User Industry Vertical | Industrial Manufacturing | |

| Healthcare and Life Sciences | ||

| Retail and Ecommerce | ||

| Energy and Utilities | ||

| Transportation and Logistics | ||

| BFSI | ||

| Construction and Engineering | ||

| Government, Defense, and Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected size of the virtual reality corporate training space by 2031?

The virtual reality (VR) corporate training market is projected to reach USD 41.10 billion by 2031, up from USD 16.64 billion in 2026, at a 19.82% CAGR.

Which training category currently leads spending?

Safety and compliance training held the largest share at 28.91% in 2025 because high-risk tasks benefit from repeatable practice in controlled virtual environments.

Which buyer group is expanding the fastest?

SMEs are projected to grow at a 23.12% CAGR through 2031 as lower headset prices, SaaS pricing, and pre-built content reduce adoption barriers.

Why is software growing faster than hardware in this field?

Software is forecast to grow at a 22.42% CAGR because enterprises increasingly value no-code authoring, analytics, LMS integration, and AI-supported scenario creation.

Which region offers the strongest current demand and which one is growing fastest?

North America held the largest share at 36.51% in 2025, while Asia-Pacific is expected to grow the fastest at a 23.81% CAGR through 2031.

Which end-user vertical shows the strongest growth outlook?

Healthcare and life sciences is forecast to grow at a 25.21% CAGR through 2031, supported by workforce shortages, procedural training needs, and stronger competency tracking.

Page last updated on: