Vinyl Acetate Monomer Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

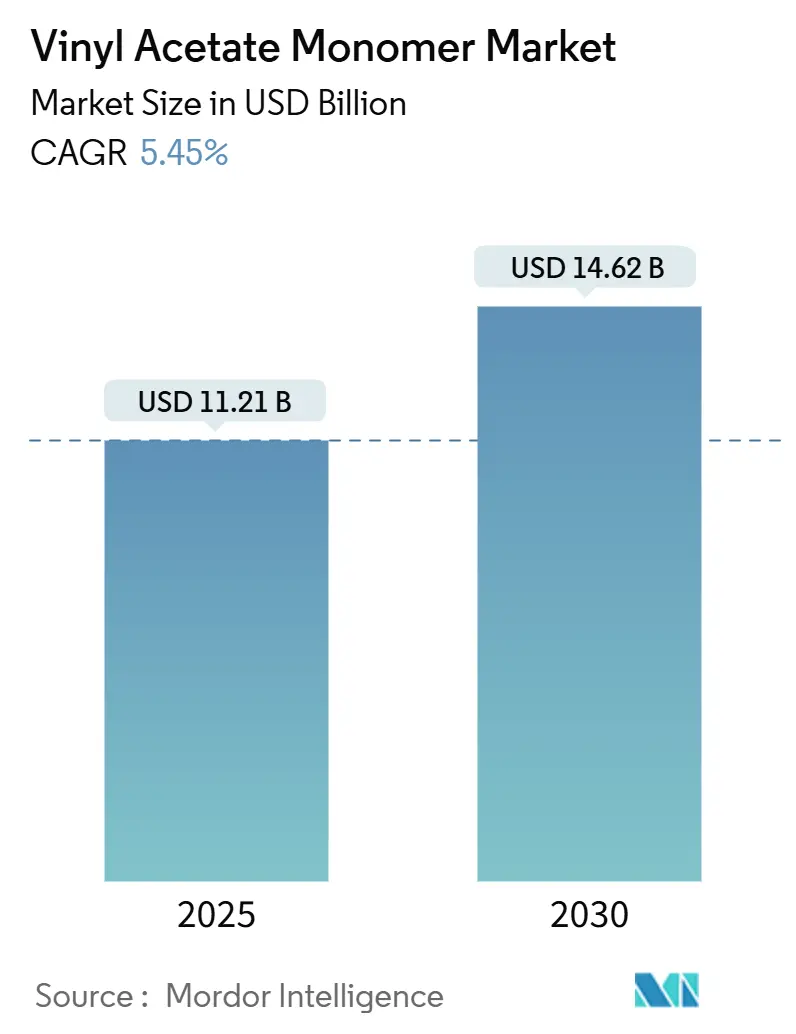

| Market Size (2025) | USD 11.21 Billion |

| Market Size (2030) | USD 14.62 Billion |

| Growth Rate (2025 - 2030) | 5.45% CAGR |

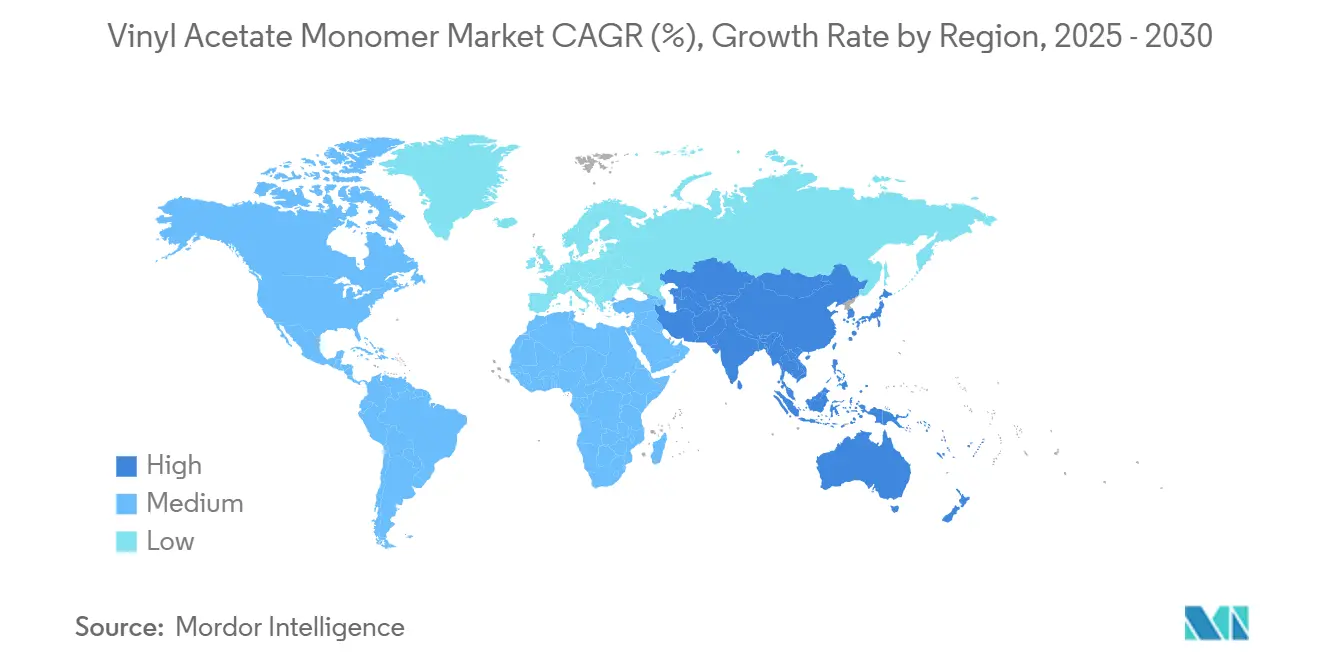

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vinyl Acetate Monomer Market Analysis by Mordor Intelligence

The Vinyl Acetate Monomer Market size is estimated at USD 11.21 billion in 2025, and is expected to reach USD 14.62 billion by 2030, at a CAGR of 5.45% during the forecast period (2025-2030). Sustained demand for polyvinyl alcohol, polyvinyl acetate, and ethylene-vinyl acetate keeps the vinyl acetate monomer market firmly anchored to packaging, construction, and solar-photovoltaic supply chains. Competitive dynamics pivot on regional feedstock economics: North American producers leverage shale-gas-derived ethylene, while new Asian capacity intensifies supply pressure. Growth in water-based adhesives, the rapid build-out of EVA encapsulant lines for solar modules, and early commercialization of bio-acetic-acid routes are set to diversify revenue streams. Near-term profitability nonetheless remains sensitive to ethylene and acetic-acid price swings, added VOC-emission compliance costs, and palladium catalyst availability. Integrated players with captive ethylene and downstream dispersion units are therefore better positioned to defend margins as merchant producers confront oversupply and rising regulatory overheads.

Key Report Takeaways

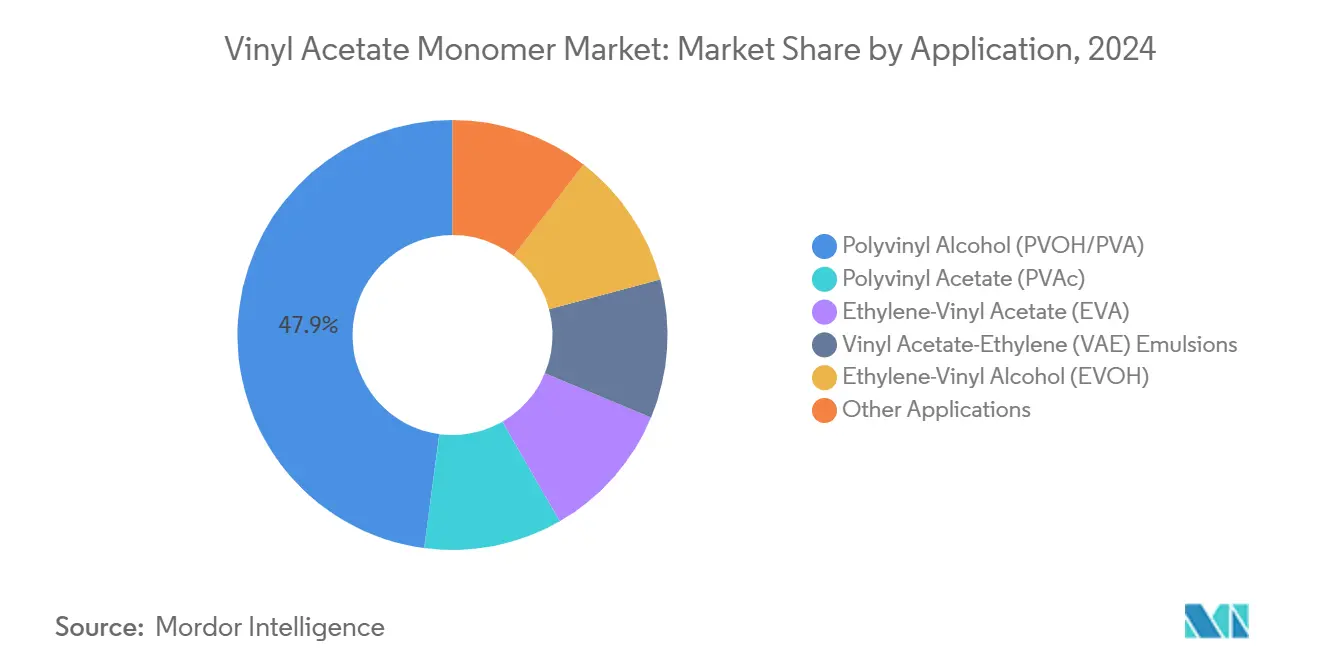

- By application, polyvinyl alcohol led with 47.89% share of vinyl acetate monomer market demand in 2024, whereas ethylene-vinyl acetate is advancing at a 5.78% CAGR through 2030.

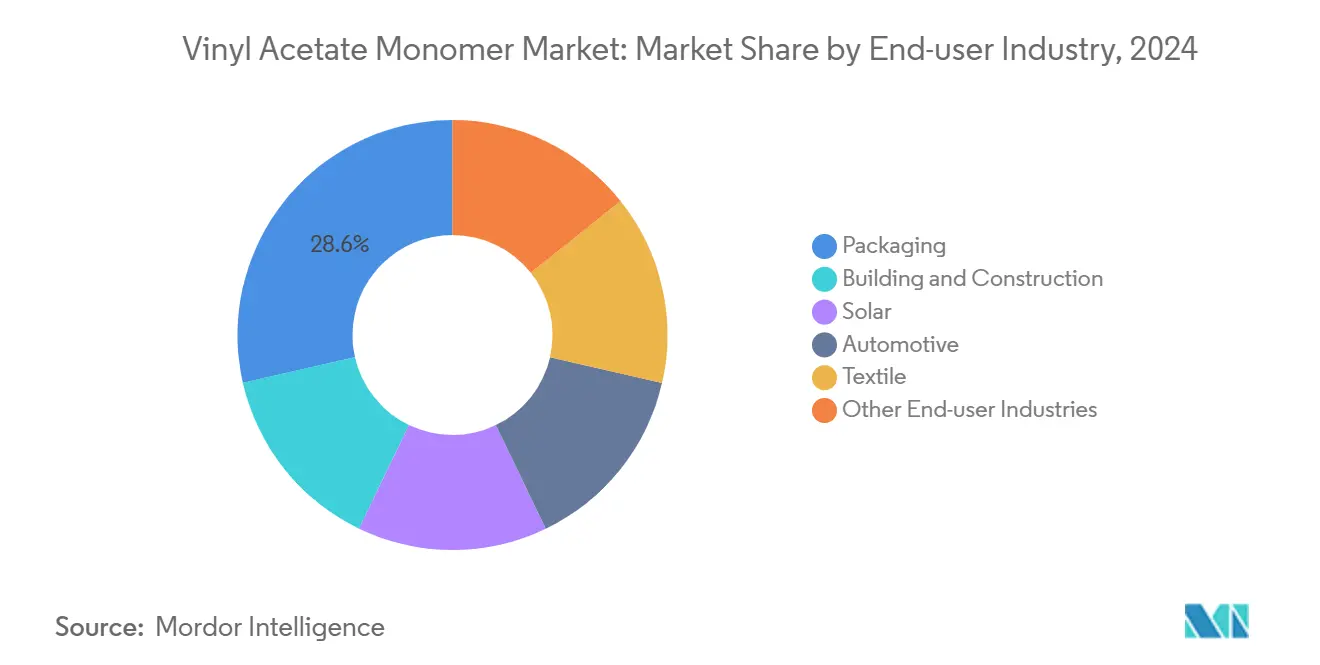

- By end-user industry, packaging accounted for 28.56% of the vinyl acetate monomer market size in 2024, while the solar sector is expanding at a 7.35% CAGR through 2030.

- By geography, Asia-Pacific commanded 48.73% of the vinyl acetate monomer market share in 2024 and is projected to post a 5.64% CAGR to 2030.

Global Vinyl Acetate Monomer Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for water-based adhesives and sealants in packaging and construction | +1.2% | North America, Europe | Medium term (2-4 years) |

| Rapid uptake of EVA encapsulant films in solar PV modules | +1.5% | Asia-Pacific core; spill-over to North America and Europe | Short term (≤2 years) |

| Growth of low-VOC architectural paints based on VAE and PVAc emulsions | +0.9% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Abundant, low-cost shale-gas ethylene improving VAM margins in North America | +0.7% | United States Gulf Coast, Appalachia | Long term (≥4 years) |

| Commercialization of bio-acetic-acid routes lowering VAM carbon footprint | +0.6% | Europe lead, early activity in Asia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Water-Based Adhesives and Sealants in Packaging and Construction

Packaging converters and construction contractors are moving away from solvent-borne systems as the U.S. EPA caps VOC content in architectural coatings at 350 g/L for primers and 450 g/L for industrial maintenance grades, with excess fees adding direct cost penalties to non-compliant formulations[1]Electronic Code of Federal Regulations, “40 CFR Part 59 Subpart D — National Volatile Organic Compound Emission Standards for Architectural Coatings,” ecfr.gov. Similar limits under EU Directive 2004/42/EC and the Nordic Swan Ecolabel, which now restricts residual vinyl acetate monomer to 700 ppm, reinforce this transition. Formulators turn to VAE and PVAc emulsions because they balance adhesion strength, fast set time, and compliance. Multinational suppliers, including Henkel, Dow, and Sika, have launched low-VOC packaging and woodworking adhesives that eliminate flammable solvents, while regional producers in India and Southeast Asia adopt similar chemistries to meet export requirements. Against this regulatory backdrop, the vinyl acetate monomer market benefits from incremental volume gains in corrugated-box sealing, furniture lamination, and building sealants. Although dispersion pricing remains linked to acetic-acid costs, lower application-site compliance expenses strengthen the overall value proposition.

Rapid Uptake of EVA Encapsulant Films in Solar PV Modules

Global EVA and POE encapsulant demand is expected to increase annually as TOPCon cell designs proliferate. Multilayer POE-EVA sheets mitigate potential-induced degradation, giving EVA demand a direct link to gigawatt-scale module manufacturing expansions in China, India, and the United States. Policy incentives such as the U.S. Inflation Reduction Act’s domestic-content tax credits and India’s production-linked incentive scheme drive non-Chinese sheet capacity. Short-cycle volatility persists; Celanese reported weaker EVA shipments in late 2024 amid module inventory overhang, prompting a temporary VAM plant standby. Nonetheless, forward module order books tied to utility-scale projects and rooftop mandates keep the long-range growth outlook intact, bolstering the vinyl acetate monomer market through higher EVA resin liftings.

Growth of Low-VOC Architectural Paints Based on VAE and PVAc Emulsions

Indoor-air-quality certifications and consumer preference for odor-free coatings favor VAE-based binders, which offer lower coalescent requirements than all-acrylic systems. A 2024 EU Joint Research Centre report identified binder production as up to 72% of cradle-to-grave climate impact for decorative paints, spotlighting the contribution of VAE latex in lowering embodied carbon[2]European Commission Joint Research Centre, “Draft Preliminary Report v2.0 for EU Ecolabel paints and varnishes,” europa.eu. Wacker Chemie responded by commercializing bio-acetic-acid-based VINNAPAS eco grades and hybrid starch-VAE systems that cut fossil raw-material use by roughly one-third. Such drop-in options allow paint makers to meet VOC and carbon-footprint targets without overhauling plant infrastructure, broadening VAM-derivative penetration in premium interior finishes across Europe and North America.

Abundant, Low-Cost Shale-Gas Ethylene Improving VAM Margins in North America

In 2024, U.S. ethane output increased. This pricing solidified a notable cost disparity against naphtha-based ethylene in Europe and Northeast Asia. Buoyed by these high margins, U.S. exporters ramped up shipments of ethylene derivatives. While new export terminals and cracker start-ups are set to tighten domestic ethane balances post-2026, Gulf Coast VAM producers currently bask in a favorable cost curve. This competitive edge not only bolsters merchant VAM exports but also facilitates conversion into VAE dispersions and EVA resins. As a result, North American vinyl acetate monomer market players find themselves shielded from price undercutting by their Asia-based counterparts.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile prices of ethylene and acetic acid feedstocks | -0.8% | Global, pronounced in Europe and India | Short term (≤2 years) |

| Tightening global VOC and carcinogen exposure regulations | -0.5% | North America and EU direct; APAC indirect | Medium term (2-4 years) |

| Palladium catalyst supply risk amid geopolitical disruptions | -0.3% | Global, higher risk for non-integrated producers | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Prices of Ethylene and Acetic Acid Feedstocks

Ethylene and acetic acid account for the bulk of VAM cash costs, making the vinyl acetate monomer market acutely sensitive to energy-price swings. U.S. ethylene contract prices rose in December 2024 after weather-driven cracker outages, while natural-gas-linked methanol costs lifted acetic-acid prices in Europe and India. Producers without backward integration or long-term supply contracts face earnings volatility and may idle capacity during cost spikes, as evidenced by Celanese’s 2024 standby decision for its Frankfurt unit. This input-price turbulence can quickly erode margins even in periods of steady downstream demand.

Tightening Global VOC and Carcinogen Exposure Regulations (OSHA, REACH)

The U.S. EPA’s January 2025 aerosol-coating amendment lowered vinyl-acetate reactivity factors and mandates detailed VOC tracking by July 2025, adding compliance overhead for resin and coating formulators. Parallel REACH revisions introduce hazard classes for persistent and mobile substances, reinforcing Carc. 2 labeling for vinyl acetate. Producers must invest in research and development, analytics, and documentation to certify residual-monomer content below ecolabel thresholds. While larger integrated firms absorb these costs, smaller standalone VAM and dispersion producers face higher per-unit regulatory expenses, constraining competitive position and potentially slowing capacity expansions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: PVOH Dominates, EVA Accelerates on Solar Tailwinds

Polyvinyl alcohol retained 47.89% of 2024 demand, underlining its established role in textile sizing, paper coatings, and water-soluble packaging. The segment anchors baseline volume for the vinyl acetate monomer market size and benefits from ongoing transition toward biodegradable films for detergent pods and agricultural mulch, particularly in China, where chemically modified PVOH grades address solubility and tensile-strength requirements. Ethylene-vinyl acetate is the fastest-growing application, expanding at a 5.78% CAGR through 2030 on the back of solar-module encapsulant demand. Polyvinyl acetate continues to gain incremental share in water-based adhesives and paints, but trails EVA in growth momentum. Vinyl acetate-ethylene emulsions leverage construction-sector spending in Southeast Asia and the Middle East, while ethylene-vinyl alcohol resins provide niche barrier properties for food packaging. The coexistence of volume leadership by PVOH and acceleration by EVA underscores the need for producers to balance mature cash-flow segments with high-growth solar opportunities within the vinyl acetate monomer industry.

Integrated capacity additions illustrate divergent strategies. Wacker Chemie doubled Nanjing dispersion output in 2023 and will start a new Calvert City VAE line in 2025, leveraging captive ethylene and bio-acetic acid to launch eco-label compliant grades. These expansions affirm confidence in long-term dispersion demand even as short-term pricing responds to feedstock swings. Producers able to supply both commodity and specialty grades through flexible reactors stand to capture incremental vinyl acetate monomer market share while cushioning against end-market cyclicality.

By End-User Industry: Packaging Leads, Solar Surges

Packaging captured 28.56% of 2024 consumption, reflecting broad use of PVAc and VAE adhesives in corrugated boxes, laminates, and labels. The shift toward recyclable substrates and lower VOC laminating adhesives sustains moderate growth, while specialty PVOH films offer dissolvable single-use solutions for detergents and agrochemicals. Constraints include tensile-strength limitations and pod leakage concerns that require ongoing formulation research and development. The solar segment, however, edges into double-digit tonnage gains, expanding at a 7.35% CAGR as module production globalizes and EVA sheet suppliers localize outside China to meet domestic-content incentives. Consequently, solar’s share of the vinyl acetate monomer market demand is expected to close the gap with packaging by 2030. Building and construction remains the next-largest outlet, where VAE dispersions and redispersible powders enable thin-bed tile adhesives and insulation systems with reduced cement usage. Automotive uptake in wire and cable insulation and PVB interlayers remains cyclical, weighed down by lower vehicle output in 2024, yet electrification trends point to future resin demand for lightweight bonding systems.

Capacity rationalization by Celanese underscores the exposure of automotive and general-construction sales to economic slowdowns. In contrast, Wacker’s push into EIFS binders that cut UV degradation demonstrates how specialty dispersions can carve defensible niches. Producers aligning product portfolios to faster-growing solar, green construction, and premium packaging applications should defend earnings and incrementally lift vinyl acetate monomer market share, mitigating the drag from matured or cyclical end-use sectors.

Geography Analysis

Asia-Pacific dominated the vinyl acetate monomer market with 48.73% of 2024 volume and will grow at a 5.64% CAGR through 2030. China's ethylene capacity, bolstered by major projects like Jiangsu Sopu's VAM line and Rongsheng Petrochemical's integrated EVA and CO₂-capture complex, is set to grow significantly by 2027. However, even with these capacity boosts, operating rates at ethylene plants dipped in 2023, hinting at margin pressures that might influence VAM pricing until the surplus is absorbed by downstream demand. Meanwhile, India's petrochemical demand, especially benefits packaging and construction dispersions. Southeast Asian nations, bolstering their infrastructure, are increasing imports of VAE dispersion, crucial for tile adhesives and waterproofing.

North America enjoys the advantage of shale gas, keeping ethylene cash costs competitive. However, with ethane exports surging and new Gulf Coast crackers set to commence by 2026, domestic balances may tighten, potentially elevating feedstock costs. For now, U.S. producers leverage their cost edge, bolstering VAM and EVA exports to Asia and Europe, thus expanding the vinyl acetate monomer market size. While Mexico and Canada rely on imports of VAM for their adhesives and resins, their limited domestic capacity ensures consistent cross-border shipments from Texas and Louisiana.

Europe grapples with a structural shortfall in ethylene and acetic acid, making its producers vulnerable to energy price fluctuations. Wacker Chemie reported significant savings in raw materials in 2023 compared to 2022, yet costs remain elevated above pre-pandemic figures. Europe's competitive edge is tied to ventures like INEOS Project One, slated for 2026, and the swift adoption of bio-acetic-acid methods to align with the Carbon Border Adjustment Mechanism. CropEnergies' investment in a renewable ethyl-acetate plant underscores the region's shift towards low-carbon feedstocks. While the Middle East and Africa consume modest volumes, they harbor untapped potential, especially as integrated refineries in Saudi Arabia and the UAE ramp up EVA capacity for broader export opportunities. In South America, Brazil and Argentina drive demand, particularly in construction dispersions, though currency fluctuations pose challenges for immediate investments.

Competitive Landscape

The vinyl acetate monomer market is moderately consolidated. Forward strategies coalesce around three themes. First, vertical integration into ethylene and acetic acid shields against volatility and supports margin resilience. Second, specialty dispersion and encapsulant-grade EVA capacity aligns supply with solar and eco-label-driven demand pockets, carving premium niches within an otherwise commoditized portfolio. Third, early adoption of renewable acetic-acid routes and ISCC-certified mass-balance bookkeeping positions producers to monetize carbon-differentiated products as Europe’s CBAM and corporate Scope 3 targets take effect. Suppliers balancing cost leadership with sustainability credentials can capture incremental vinyl acetate monomer market share while safeguarding profitability through the cycle.

Vinyl Acetate Monomer Industry Leaders

Celanese Corporation

LyondellBasell Industries Holdings B.V.

Dow

Wacker Chemie AG

China Petrochemical Corporation (Sinopec)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Kuraray Co., Ltd. secured ISCC PLUS certification for five vinyl-acetate-related products, establishing a certified Japanese supply chain beginning with VAM produced at its Okayama plant.

- March 2025: Celanese Corporation announced price increases for vinyl acetate monomer, vinyl-based emulsions, and redispersible powders across the Western Hemisphere, effective March 17, 2025.

Global Vinyl Acetate Monomer Market Report Scope

Vinyl acetate, also known as vinyl acetate monomer (VAM), is mainly used to make other chemicals for industrial and consumer products. Polymers made from VAM, such as vinyl chloride-vinyl acetate copolymer, polyvinyl acetate (PVA), and polyvinyl alcohol (PVOH), are used in many applications across different industries. The vinyl acetate monomer (VAM) market is segmented by application, end-user industry, and geography. By application, the market is segmented into polyvinyl acetate (PVAc), polyvinyl alcohol (PVOH/PVA), ethylene-vinyl acetate (EVA), vinyl acetate-ethylene (VAE) emulsions, ethylene-vinyl alcohol (EVOH), and other applications. By end-user industry, the market is segmented into packaging, building and construction, solar, automotive, textile, and other end-user industries. The report also covers the market size and forecasts for the vinyl acetate monomer (VAM) market in 16 countries across the major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Polyvinyl Acetate (PVAc) |

| Polyvinyl Alcohol (PVOH/PVA) |

| Ethylene-Vinyl Acetate (EVA) |

| Vinyl Acetate-Ethylene (VAE) Emulsions |

| Ethylene-Vinyl Alcohol (EVOH) |

| Other Applications |

| Packaging |

| Building and Construction |

| Solar |

| Automotive |

| Textile |

| Other End-user Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Application | Polyvinyl Acetate (PVAc) | |

| Polyvinyl Alcohol (PVOH/PVA) | ||

| Ethylene-Vinyl Acetate (EVA) | ||

| Vinyl Acetate-Ethylene (VAE) Emulsions | ||

| Ethylene-Vinyl Alcohol (EVOH) | ||

| Other Applications | ||

| By End-user Industry | Packaging | |

| Building and Construction | ||

| Solar | ||

| Automotive | ||

| Textile | ||

| Other End-user Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected global value of the vinyl acetate monomer market in 2030?

The market is forecast to reach USD 14.62 billion by 2030, rising at a 5.45% CAGR from USD 11.21 billion in 2025.

Which application currently dominates demand for vinyl acetate monomer?

Polyvinyl alcohol accounts for 47.89% of 2024 consumption, underscoring its entrenched position in textiles, packaging films, and construction additives.

Why is EVA consumption growing faster than other applications?

Solar-photovoltaic module makers are adopting EVA encapsulant films at a pace that supports a 5.78% CAGR through 2030, driven by TOPCon cell architectures and renewable-energy incentives.

How does shale gas influence North American VAM competitiveness?

Abundant, low-cost ethane keeps U.S. ethylene production costs below those in naphtha-based regions, supporting attractive margins for VAM and derivative exports.

What sustainability trends affect future VAM production?

Commercialization of bio-acetic acid, stricter VOC limits, and ISCC PLUS certification are pushing producers to adopt low-carbon feedstocks and mass-balance accounting.

Page last updated on: