Vietnam Global Capability Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

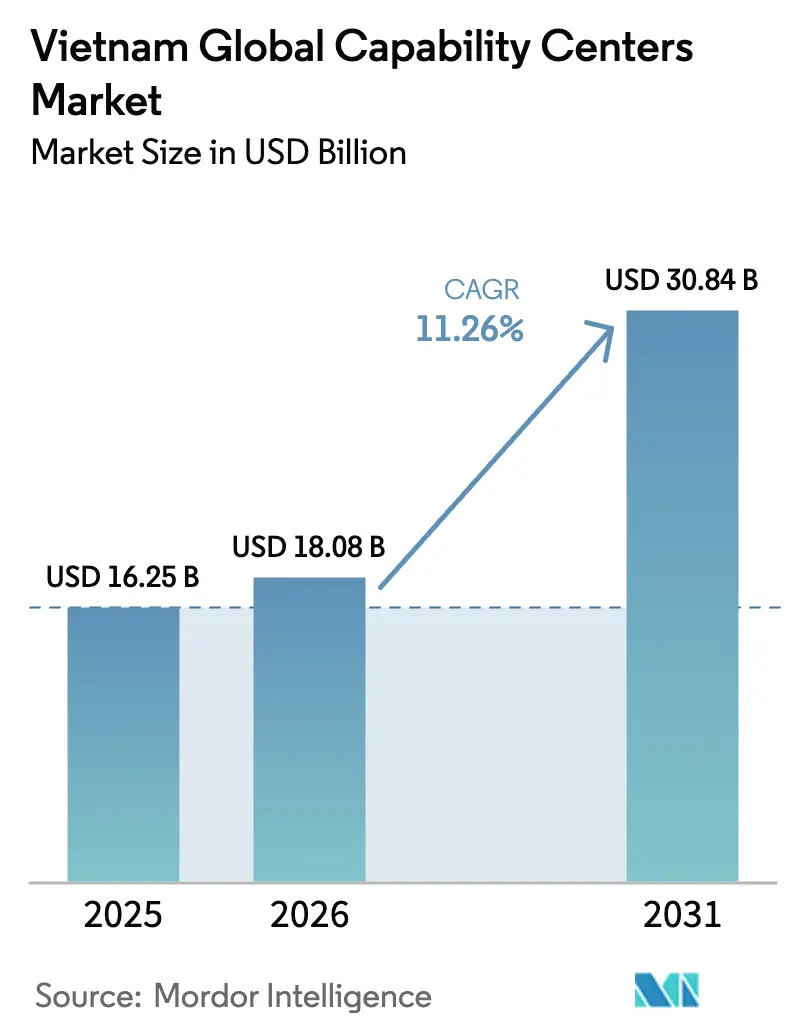

| Base Year Market Size (2025) | USD 16.25 Billion |

| Market Size (2026) | USD 18.08 Billion |

| Market Size (2031) | USD 30.84 Billion |

| Growth Rate (2026 - 2031) | 11.26% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Global Capability Centers Market Analysis by Mordor Intelligence

The Vietnam Global Capability Centers market size is expected to grow from USD 16.25 billion in 2025 to USD 18.08 billion in 2026 and is forecast to reach USD 30.84 billion by 2031 at 11.26% CAGR over 2026-2031. Cost arbitrage of 30-40%, dependable English-speaking talent, and expanding renewable power commitments anchor the current growth momentum. Multinational corporations continue to relocate complex digital, engineering, and business process mandates to Vietnam, attracted by preferential income tax rates, land lease incentives, and import duty exemptions under Decree 10/2024 and Decree 182/2024. The continuous rollout of nationwide 5G, three new submarine cables, and government-funded digital-skills programs further broadens the functional spectrum deliverable from Vietnamese hubs. Meanwhile, rising wage inflation in Ho Chi Minh City and Hanoi, as well as skill shortages in artificial intelligence and cybersecurity, temper the upside yet have not derailed the overall expansion trajectory of the Vietnam Global Capability Centers market.

Key Report Takeaways

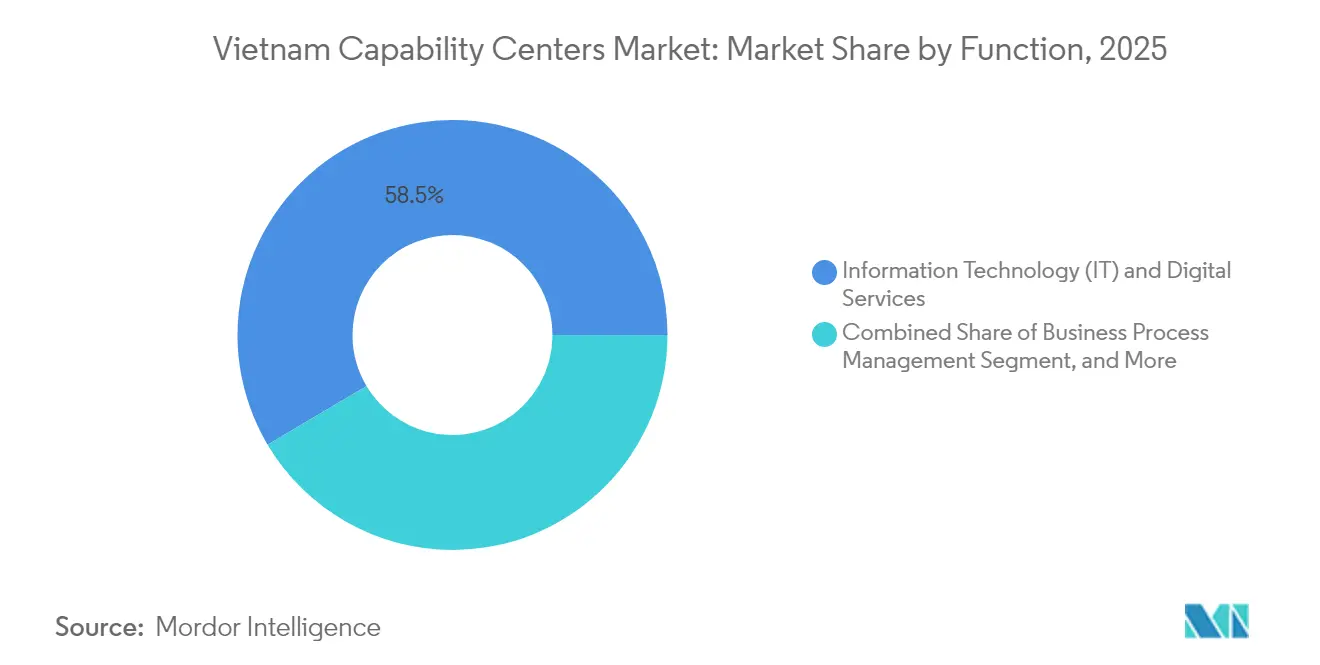

- By function, information technology and digital services captured 58.52% of the Vietnam Global Capability Centers market share in 2025; engineering and R&D are projected to progress at a 12.08% CAGR through 2031.

- By engagement model, the captive format held a 56.10% revenue share in 2025, while hybrid build-operate-transfer arrangements are projected to grow at a 11.69% CAGR through 2031.

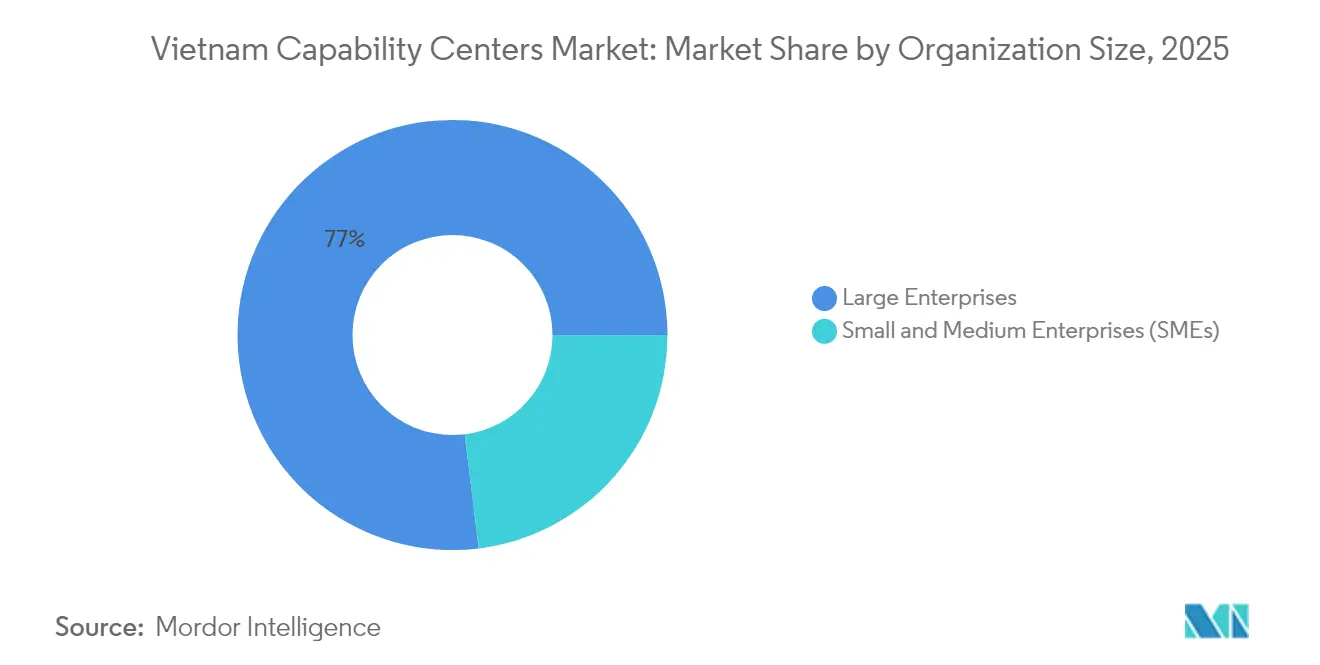

- By organization size, large enterprises accounted for 76.95% of the Vietnam Global Capability Centers market size in 2025, while small and medium enterprises are expected to expand at a 13.05% CAGR through 2031.

- By industry vertical, the manufacturing, automotive, and industrial sectors led with a 38.20% revenue share in 2025; telecom and IT are expected to grow at a 11.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Global Capability Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost arbitrage versus Western markets | +2.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Large pool of STEM graduates with strong English proficiency | +2.2% | Global, most useful for English-speaking markets | Long term (≥ 4 years) |

| Government incentives for high-tech investment | +1.9% | National, concentrated in Ho Chi Minh City and Hanoi | Short term (≤ 2 years) |

| Upgraded telecom infrastructure and high-speed internet | +1.5% | National, spillovers to ASEAN | Medium term (2-4 years) |

| Reverse brain drain of Vietnamese diaspora tech talent | +1.3% | National, early gains in Silicon Valley-linked sectors | Long term (≥ 4 years) |

| ESG-driven shift toward Vietnam’s renewable power mix | +1.1% | Global, relevant for European and North American MNCs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost Arbitrage Versus Western Markets

Large enterprises and an increasing cohort of mid-sized firms choose the Vietnam Global Capability Centers market primarily for the substantial labor and real-estate differentials available relative to Silicon Valley, London, or Frankfurt. Software engineers in Ho Chi Minh City earned an average of USD 18,000-25,000 in 2024, representing a 60-70% savings compared to peer positions in the United States or Western Europe. Grade A commercial space ranged between USD 35 and USD 42 per square meter monthly during the same period, well below Singapore’s USD 80-120 per square meter band.[1]Vietnam Real Estate Association, “Commercial Property Market Analysis Q3 2024,” vnrea.org Combined with a 10% corporate income tax rate for high-tech projects, as outlined in Decree 10/2024, the aggregate delivered service advantage remains meaningful despite emerging salary pressures. Consequently, the Vietnam Global Capability Centers market continues to secure new bookings from financial services, healthcare, and engineering clients targeting sustainable opex savings without quality trade-offs.

Large Pool of STEM Graduates With Strong English Proficiency

Roughly 500,000 STEM graduates enter Vietnam’s labor market each year, and 85% of them demonstrate intermediate-to-advanced English skills based on 2024 Ministry of Education assessments.[2]Vietnam Ministry of Education and Training, “STEM Education Enhancement Strategy 2024-2030,” moet.gov.vn This young, scalable, and multilingual talent base enables companies to roll out complex mandates, from full-stack development to data engineering pipelines, at a rapid pace. The National Strategy for Digital Transformation allocates USD 1.2 billion for STEM and language programs through 2030, aiming to increase the country’s total technology workforce to 1 million over the next five years. Universities have signed dual-degree agreements with U.S. and EU schools, tightening curriculum alignment in artificial intelligence, cybersecurity, and semiconductor design. Such initiatives reinforce the Vietnam Global Capability Centers market as an attractive alternative to saturated Indian and Philippine talent hubs.

Government Incentives For High-Tech Investment

The Investment Support Fund under Decree 182/2024 can co-finance up to USD 50 million for projects larger than USD 100 million in registered capital, prioritizing semiconductor, renewable-energy, and AI ventures. Land-lease concessions across 18 high-tech zones compress long-term occupancy costs, while import-duty waivers on capital equipment accelerate greenfield build-outs. Collectively, these measures improve the net-present-value of large-scale setups by 15-20 percentage points, bolstering the Vietnam Global Capability Centers industry pipeline with marquee names in automotive electronics and cloud infrastructure. Ho Chi Minh City’s Saigon Hi-Tech Park and Hanoi’s Hoa Lac Hi-Tech Park remain the primary beneficiaries, while secondary clusters in Da Nang and Bac Giang are beginning to attract follow-on electronics suppliers, thereby tightening regional supply-chain linkages.

Upgraded Telecom Infrastructure And High-Speed Internet

Nationwide 5G deployment reached 85% population coverage by late 2024 through a USD 1.5 billion capex push led by Viettel.[3]Vietnam Telecommunications Authority, “5G Infrastructure Development Progress Report,” mic.gov.vn Three additional submarine cables increased international bandwidth by 400%, reducing latency to San Francisco and Frankfurt to levels comparable to those in Singapore. Urban fixed-broadband speeds averaged 108 Mbps, enabling secure cloud-native development environments, high-resolution collaboration, and real-time data replication. These connectivity gains reduce operational risk, expand service portfolios into latency-sensitive edge-computing and DevOps work, and enhance the competitive positioning of the Vietnam Global Capability Centers market among digitally sophisticated clients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising wage inflation in Tier 1 cities | -1.8% | Ho Chi Minh City and Hanoi | Short term (≤ 2 years) |

| Skill gaps in advanced digital engineering | -1.5% | National, acute in AI and cybersecurity | Medium term (2-4 years) |

| Limited Grade A office space in emerging cities | -0.9% | Da Nang, Can Tho, Hai Phong | Medium term (2-4 years) |

| Geopolitical trade-approval delays for certain sectors | -0.7% | Global, mainly semiconductor and telecom | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Wage Inflation In Tier 1 Cities

A salary acceleration of 15-20% per year for experienced developers in Ho Chi Minh City and Hanoi erodes part of the cost differential versus Kuala Lumpur and Bangkok. Senior engineers are expected to reach a base pay of around USD 40,000 by 2024, and ongoing supply-demand imbalances in AI, DevOps, and cybersecurity indicate further upward movement. Commercial rents in District 1 have reached USD 42 per square meter monthly, representing a 25% annual increase that squeezes margin assumptions for large captives. To mitigate these cost headwinds, multinationals are piloting satellite hubs in lower-cost northern and central provinces, while strengthening retention through career progression programs.

Skill Gaps In Advanced Digital Engineering

Specialists in AI, machine learning, and cybersecurity are in short supply, accounting for less than 8% of the IT labor pool, according to 2024 VINASA data.[4]Vietnam Software and IT Services Association, “Technology Workforce Skills Assessment 2024,” vinasa.org.vn Global Capability Centers serving regulated verticals, such as finance and healthcare, often need to import seasoned leads from Singapore or Tokyo, thereby extending their ramp-up timelines. Limited hands-on exposure to cloud-native microservices and container orchestration further constrains high-value work placement. Although the National Digital Transformation Program allocates USD 2.8 billion for upskilling, the medium-term availability gap could limit the premium-segment revenue potential within the Vietnam Global Capability Centers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function / Capability: IT Services Lead Digital Transformation Wave

Information technology and digital services accounted for 58.52% of the Vietnam Global Capability Centers market in 2025, driven by robust demand for application modernization, cloud migration, and customer-experience platforms. The segment is expected to expand at a 12.08% CAGR, adding more than USD 6.7 billion to the Vietnam Global Capability Centers market size by 2031. Engineering and R&D work, covering electric-vehicle component design, semiconductor backend validation, and smart-factory solutions, has become the fastest-moving niche. Bosch Global Software Technologies and Fujitsu Vietnam both doubled headcount for embedded-software teams, underscoring rising sophistication. Business process management keeps a stable clip because global banks and insurers route anti-money-laundering checks, claims adjudication, and KYC documentation to Vietnam for cost efficiencies. Knowledge-process outsourcing is emerging but already commands premium rates in pharmaceutical competitive intelligence and technology patent analytics roles.

The functional pattern shows Vietnam transiting from transactional coding centers toward innovation-linked hubs. Decree-backed tax relief and project grants have prompted captives to integrate AI design, cloud-security architecture, and IoT systems into their legacy support operations. Consequently, the Vietnam Global Capability Centers market is moving up the value curve and improving price realization, giving firms headroom to absorb moderate wage inflation while still offering attractive economics relative to more mature outsourcing destinations.

By Engagement Model: Hybrid Models Gain Traction

Captive centers delivered 56.10% of 2025 revenue, aligning with multinationals’ preference for IP control, stringent security, and direct cultural integration. Yet, build-operate-transfer hybrids are set to outpace the market at an 11.69% CAGR, fueled by mid-cap firms that lack the initial critical mass to operate fully in-house. Under the hybrid, a Vietnamese vendor like FPT Software co-hires staff, establishes infrastructure, and hands over ownership once contractual milestones are achieved, thereby limiting upfront capital risk. These structures are now embedded into Procurement and Legal playbooks, shortening decision cycles and funneling more logos into the Vietnam Global Capability Centers market.

Local providers have invested in robust governance templates, SOC 2-aligned controls, and living knowledge-transfer repositories to smooth the final handoff stage. The upshot is a widening funnel of 50-200-seat centers that migrate into captives within three years, enlarging the installed base and deepening Vietnam’s strategic relevance inside global technology portfolios.

By Organization Size: SME Segment Emerges As Growth Driver

Large enterprises still contributed 76.95% of 2025 turnover, a product of multi-continent supply chains and transformational budgets. Yet small and medium enterprises are forecast to register 13.05% CAGR, reflecting cloud-delivered, pay-as-you-grow engagement structures that lower entry thresholds. For instance, an EU-based e-commerce scale-up activated a 35-engineer DevOps pod in Ho Chi Minh City using an outcome-based contract priced on deployment velocity rather than headcount, marking a shift toward elastic consumption models inside the Vietnam Global Capability Centers industry.

Government-subsidized digital maturity assessments, zero-interest technology loans, and a nationwide mentoring network further encourage local SMEs to collaborate with Global Capability Center operators, creating reference use cases that resonate internationally. Each successful SME engagement amplifies Vietnam’s brand as a destination for accessible tech services, expanding the total addressable opportunity for mid-tier vendors while balancing exposure away from highly negotiated mega deals.

By Industry Vertical: Manufacturing Leads, Telecom Accelerates

Manufacturing, automotive, and industrial clients contributed 38.20% of 2025 revenue, reflecting Vietnam’s prominence in the global electronics and high-precision assembly sectors. Co-location synergies enable engineers to iterate firmware alongside factory floors, thereby shortening the design-to-production loop. Banking, financial services, and insurance operations rely on Vietnam for payment-gateway coding, risk analytics models, and regulatory compliance documentation, helped by competitive labor costs and growing domain expertise. Healthcare and life sciences Global Capability Centers have established clinical-data management pods to support trial monitoring for Asia-Pacific markets, gradually lifting the premium end of the Vietnam Global Capability Centers market.

Telecom and IT is the breakout vertical, projected to grow at a 11.98% CAGR through 2031, thanks to 5G rollouts and the rapid expansion of cloud usage across ASEAN. Vietnamese centers now deliver network-optimization algorithms, software-defined-network orchestration, and edge-computing container stacks for regional carriers. The proximity to new submarine cables and rising local cyber-talent pool strengthen Vietnam’s value proposition for latency-sensitive telco workloads and augur well for sustained double-digit growth.

Geography Analysis

Ho Chi Minh City and Hanoi jointly captured a significant share of the Vietnam Global Capability Centers market in 2025, leveraging integrated infrastructure, international air links, and proximity to universities. Saigon Hi-Tech Park hosts more than 200 tech firms, including Intel’s largest semiconductor assembly center outside the United States. Hanoi’s Hoa Lac Hi-Tech Park benefits from policy proximity and a talent supply fed by Vietnam National University. The dual-city concentration offers network effects and mature vendor ecosystems, but it also contributes to wage inflation.

Secondary cities, Da Nang, Hai Phong, and Can Tho, offer 20-30% cost advantages and growing 5G coverage. Da Nang IT Park has attracted dedicated engineering pods for electric-vehicle software, while Hai Phong supports printed-circuit-board design aligned with its manufacturing base. Government infrastructure outlays of USD 3.2 billion through 2030 will enhance roads, logistics hubs, and fiber backbones in these localities, effectively expanding the catchment area of the Vietnam Global Capability Centers market.

Vietnam’s membership in the CPTPP, RCEP, and the 2024 ASEAN Digital Economy Framework Agreement streamlines cross-border data flows and harmonizes service-delivery standards, allowing Vietnamese centers to manage multi-jurisdictional workloads seamlessly. The strategic position along the Greater Mekong logistics corridor and deepened rail links to southern China further enlarge the addressable industry verticals, such as supply-chain analytics and automotive design. These geographic factors, combined with cost and talent dynamics, position Vietnam well to capture incremental market share from India, the Philippines, and emerging Eastern European hubs over the next half-decade.

Competitive Landscape

The Vietnam Global Capability Centers market remains moderately fragmented. Domestic leaders, such as FPT Software, TMA Solutions, and NashTech Global, leverage deep client networks, favorable wage structures, and multilingual capabilities. International entrants, such as Bosch Global Software Technologies, Fujitsu Vietnam, and NEC Vietnam, specialize in high-margin embedded software and engineering services, benefiting from their parent company's ecosystems. Competitive levers have shifted toward vertical-specific intellectual property. FPT’s automotive-grade AUTOSAR stack, Bosch’s E-bike motor firmware, and TMA’s hospital information system platform illustrate this niche differentiation.

Mergers and acquisitions have escalated, exemplified by TMA Solutions’ USD 25 million acquisition of two AI boutiques to bolster its advanced analytics capabilities. Strategic alliances are equally important; FPT Software inked a multi-year USD 50 million contract with a major European automotive OEM to operate an electric-vehicle software center in Da Nang. Patent filings by Vietnamese firms increased by 35% in 2024, underscoring a shift toward proprietary tooling. The integration of ESG objectives is now evident, as players pursue renewable energy sourcing and LEED-certified campuses to satisfy client audits, thereby reinforcing Vietnam’s market appeal to sustainability-focused corporations.

Talent retention and employee experience strategies are becoming increasingly decisive. Vendors provide micro-credential training, international rotations, and equity-linked incentives to curb attrition, which averaged 12-15% in 2024. Given the still-fragmented vendor landscape and deepening client preference for multi-vendor diversification, there is room for both scale players and specialist boutiques, preserving a healthy level of competitive tension across the Vietnam Global Capability Centers market.

Vietnam Global Capability Centers Industry Leaders

FPT Software Co. Ltd.

CMC Corporation

TMA Solutions

NashTech Global Ltd.

KMS Technology Vietnam Co. Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Vietnam’s Ministry of Planning and Investment has cleared a USD 2.3 billion package to expand the national semiconductor ecosystem, earmarking funds for backend assembly, testing plants, and training programs aimed at adding 50,000 engineers by 2028.

- August 2025: FPT Software signed a strategic deal with a leading European automaker to build a USD 120 million electric-vehicle software hub in Hanoi, a facility that will employ 2,000 engineers working on autonomous-driving and battery-management code.

- July 2025: Samsung Electronics committed USD 220 million to expand display technology, semiconductor design, and semiconductor design work at its Hanoi R&D complex, cementing Vietnam’s role in the global electronics supply chain.

- June 2025: The government introduced the National AI Strategy Implementation Fund with an initial USD 500 million, offering grants and co-investment to firms opening AI research centers and machine-learning GCC units.

Vietnam Global Capability Centers Market Report Scope

The scope of the global capability center study for the market segmentation by the Function/Capability for (i) Information Technology (IT) and Digital Services segment is limited to Software Development, Cloud and Infrastructure Management, Cybersecurity, Data Analytics and AI/ML; (ii) Engineering / ER&D segment is limited to Product Design and Testing, Embedded Systems, Digital Twin / Simulation; (iii) Business Process Management (BPM) segment is limited to Finance and Accounting, HR, Payroll and Talent Management, Procurement, Customer Service; and (iv)Knowledge Process Outsourcing (KPO) segment is limited to Market Research and Insights, Risk and Compliance, Legal and Regulatory Support, Strategy and Consulting Support. Similarly, for segmentation by the Engagement Model, scope for (i) Hybrid Build-Operate-Transfer (BOT) is limited to Joint Venture / Strategic Partnership and Virtual Captive Model. The rest of the segment scope is as specified for the listed segment.

| Information Technology (IT) and Digital Services |

| Engineering / ER&D |

| Business Process Management (BPM) |

| Knowledge Process Outsourcing (KPO) |

| Captive (Self-Build) / In-house |

| Build-Operate-Transfer (BOT) |

| Hybrid Build-Operate-Transfer (BOT) |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT |

| Healthcare and Life Sciences |

| Manufacturing, Automotive and Industrial |

| Retail and Consumer Goods |

| Other Industry Verticals |

| By Function / Capability | Information Technology (IT) and Digital Services |

| Engineering / ER&D | |

| Business Process Management (BPM) | |

| Knowledge Process Outsourcing (KPO) | |

| By Engagement Model | Captive (Self-Build) / In-house |

| Build-Operate-Transfer (BOT) | |

| Hybrid Build-Operate-Transfer (BOT) | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises (SMEs) | |

| By Industry Vertical | Banking, Financial Services, and Insurance (BFSI) |

| Telecom and IT | |

| Healthcare and Life Sciences | |

| Manufacturing, Automotive and Industrial | |

| Retail and Consumer Goods | |

| Other Industry Verticals |

Key Questions Answered in the Report

What is the current value of the Vietnam Global Capability Centers market?

The market generated USD 18.08 billion in 2026 and is set to reach USD 30.84 billion by 2031.

How fast is the Vietnam Global Capability Center segment for telecom and IT expected to expand?

Telecom and IT workloads are forecast to post a 11.98% CAGR through 2031, the fastest among all verticals.

Which engagement model is growing quickest in Vietnam?

Hybrid build-operate-transfer structures are projected to grow at a 11.69% CAGR, outpacing pure captive or outsourced formats.

Why do multinational firms favor Vietnam over other Southeast Asian destinations?

They achieve 30-40% cost savings, access to half a million STEM graduates annually, and receive supportive tax incentives under Decree 10/2024 and Decree 182/2024.

Which Vietnamese cities are emerging as secondary hubs for the Global Capability Center?

Da Nang, Hai Phong, and Can Tho offer 20-30% cost advantages while benefiting from new 5G and infrastructure upgrades.

Page last updated on: