Vietnam Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

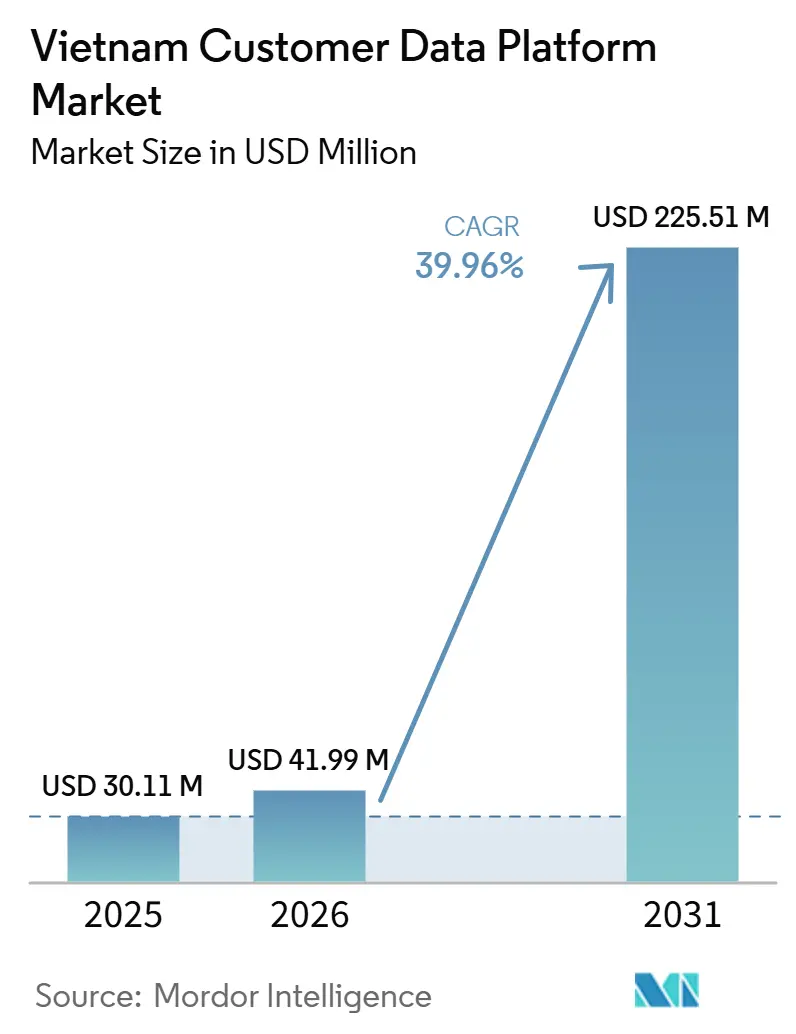

| Base Year Market Size (2025) | USD 30.11 Million |

| Market Size (2026) | USD 41.99 Million |

| Market Size (2031) | USD 225.51 Million |

| Growth Rate (2026 - 2031) | 39.96% CAGR |

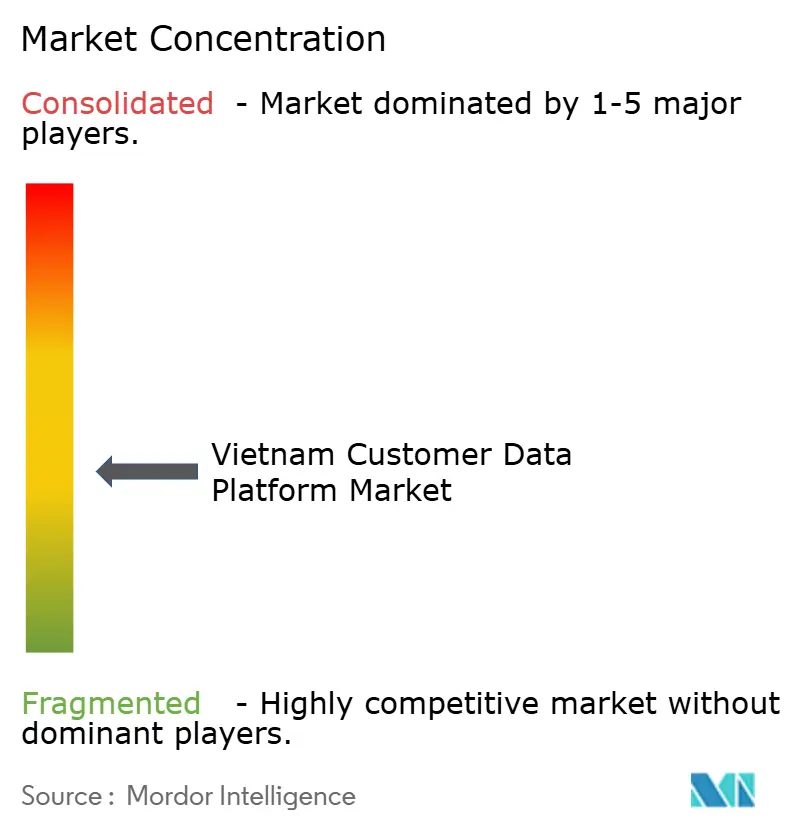

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Customer Data Platform Market Analysis by Mordor Intelligence

The Vietnam customer data platform market size was valued at USD 30.11 million in 2025 and is estimated to grow from USD 41.99 million in 2026 to reach USD 225.51 million by 2031, at a CAGR of 39.96% during the forecast period 2026-2031. Growth is being shaped by the rapid expansion of digital commerce, because Vietnam’s e-commerce sector reached USD 31 billion in 2025 and the largest marketplaces recorded sharp sales growth, which has made customer data fragmentation harder for brands to manage across marketplaces, direct channels, loyalty tools, and offline systems. The new personal data protection framework that took effect in 2026 is also changing buying behavior, because many enterprises now need auditable consent records and clearer control over how customer information is collected, stored, and activated. Demand is also moving beyond basic data storage toward real-time identity resolution, campaign activation, and AI-driven personalization, especially in banking, retail, and healthcare settings where customer journeys now span many digital and physical touchpoints. Competition is splitting between global enterprise vendors and local providers, with local suppliers gaining traction through lower implementation burden, native integration with Vietnam’s digital ecosystem, and closer alignment with domestic compliance needs. The Vietnam customer data platform market also faces a structural execution gap, because integration effort and shortages in data engineering and martech talent can slow activation even after a platform is purchased.

Key Report Takeaways

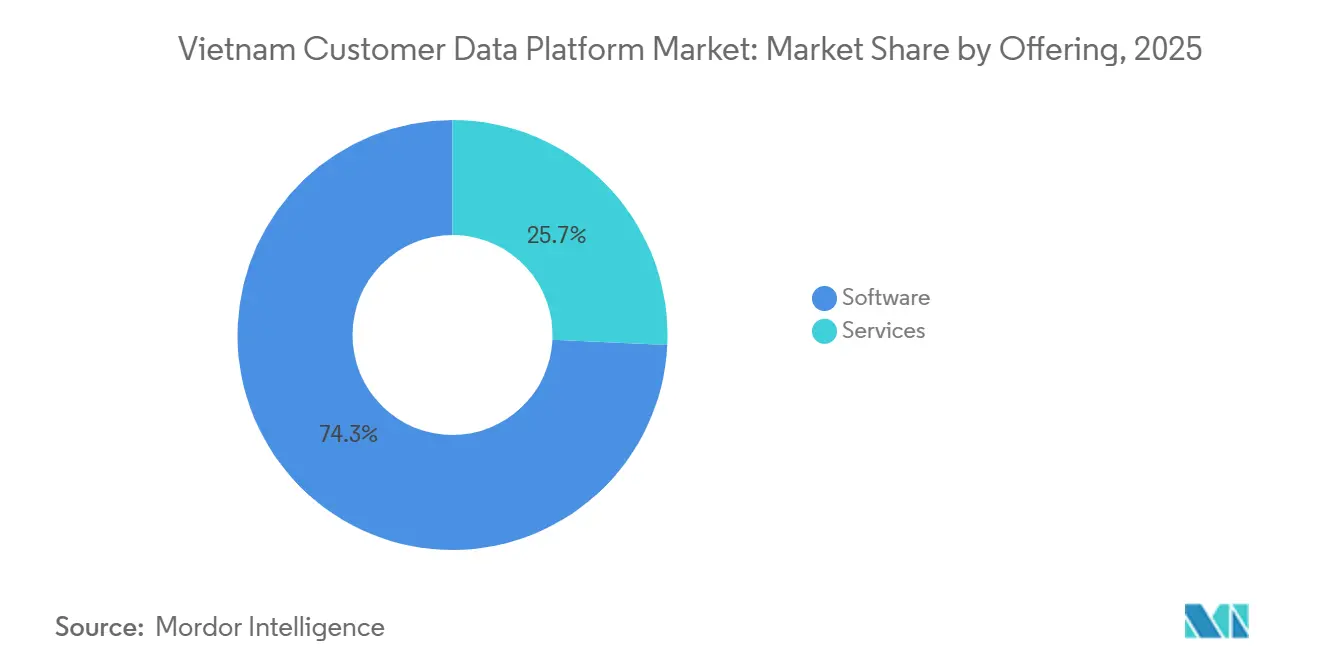

- By offering, software held 74.26% of the Vietnam customer data platform market share in 2025, while services are projected to expand at a 40.16% CAGR through 2031.

- By deployment mode, cloud accounted for 68.12% of the Vietnam customer data platform market size in 2025, while hybrid is expected to record the highest CAGR at 41.73% through 2031.

- By organization size, large enterprises held 67.82% share in 2025, while SMEs are projected to grow at a 41.24% CAGR through 2031.

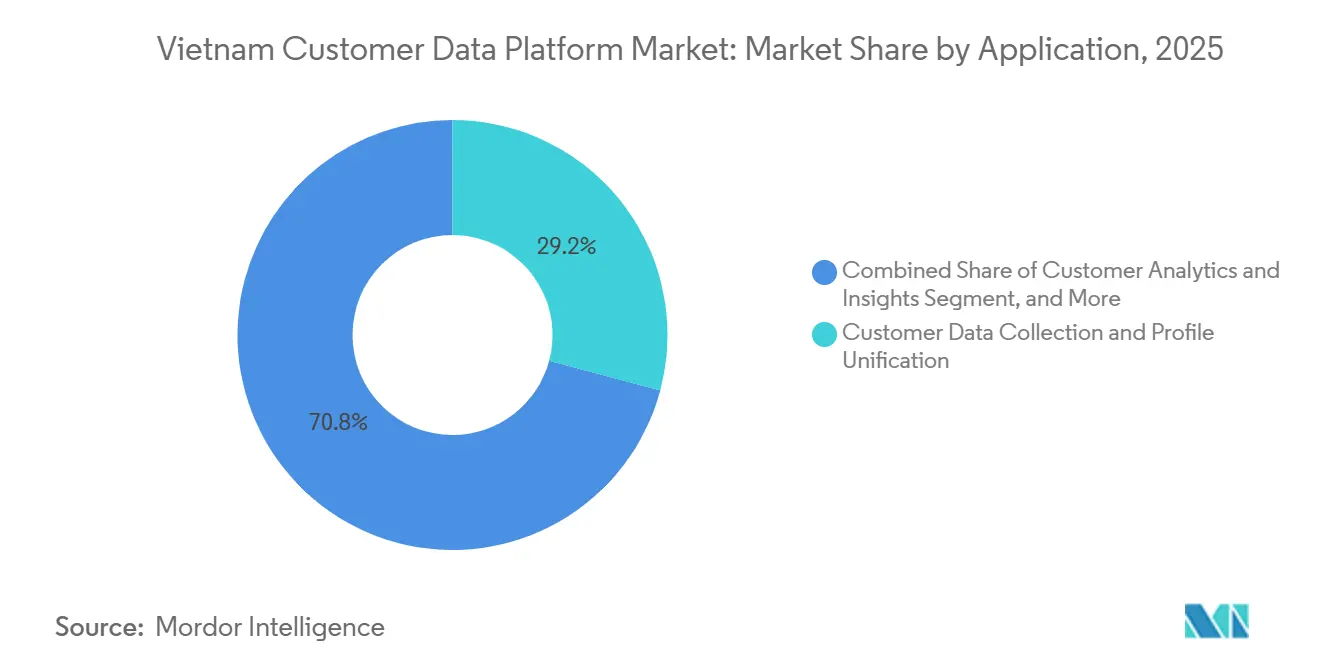

- By application, customer data collection and profile unification accounted for 29.16% share in 2025, while audience segmentation and personalization are projected to advance at a 42.32% CAGR through 2031.

- By end-user industry, retail and e-commerce held 33.37% share in 2025, while healthcare and life sciences are expected to expand at a 42.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising E-Commerce and Marketplace Data Fragmentation | +9.2% | National, strongest in Ho Chi Minh City and Hanoi e-commerce corridors | Short term (≤ 2 years) |

| Accelerating First-Party Data Strategies | +8.1% | National, led by digital-first retail and BFSI clusters in Ho Chi Minh City | Short term (≤ 2 years), Medium term (2-4 years) |

| Omnichannel Identity Resolution In Retail and BFSI | +7.5% | National, with early intensity in Ho Chi Minh City, Hanoi, and Da Nang | Medium term (2-4 years) |

| AI-Enabled Personalization and Next-Best-Action Use Cases | +6.8% | National, with BFSI and large retail chains leading deployment | Medium term (2-4 years) |

| SME Adoption Through Modular Cloud CDPs | +4.3% | National, strongest in southern Vietnam’s SME commercial centers | Medium term (2-4 years), Long term (≥ 4 years) |

| Consent Management Under the New Privacy Regime | +3.2% | National, especially in sectors processing large volumes of sensitive personal data | Short term (≤ 2 years), Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce and Marketplace Customer Data Fragmentation

Vietnam’s e-commerce ecosystem includes major marketplaces, brand websites, social commerce channels, loyalty apps, and offline stores. This complexity makes it difficult for enterprises to maintain unified customer records without a dedicated data layer. The market continues to expand rapidly, increasing pressure on businesses to connect more customer touchpoints while minimizing data gaps. Much of the customer activity occurs on large external platforms rather than within merchants’ own systems. When businesses combine this data with store operations, messaging apps, and payment flows, brands often end up with fragmented records instead of a single, actionable customer profile. This fragmentation is driving demand for customer data platforms that can unify behavioral, transactional, and consent records in real time, rather than store them across separate systems. As digital commerce continues to grow, the Vietnam customer data platform (CDP) market is benefiting from a structural need for identity stitching and unified data management rather than a short-term software cycle.

Accelerating First-Party Data Strategies Across Digital Channels

Vietnam’s updated data privacy regime has made first-party data strategy more urgent, because consent capture and traceability now matter as much as campaign performance. The Personal Data Protection Law took effect on January 1, 2026, and its implementing decree requires clearer governance around processing, documentation, and accountability for personal data activities. That change is pushing enterprises to treat customer data platforms not only as marketing infrastructure, but also as systems that support evidence, auditability, and process control. Zalo has become especially important in this shift, because messaging remains central to customer engagement in Vietnam, and native integration with local channels is now a practical requirement for first-party data activation. Local vendors are gaining from this transition because they can connect domestic platforms and compliance workflows with less customization than many imported stacks. This is one reason the Vietnam customer data platform market is moving quickly from experimental deployments toward broader operational use in 2026.

Omnichannel Identity Resolution Needs in Retail and BFSI

Retailers and banks in Vietnam now serve customers through branches, apps, websites, QR payment journeys, service centers, and messaging platforms, but those touchpoints often do not share one stable identifier. MSB’s July 2025 rollout with mParticle, FPT, and AKA Digital showed how identity resolution can turn into usable business value, because the bank activated 14 use cases, enriched more than 700 customer attributes, and reduced reporting workload by up to 90% within 88 days.[1]FPT Information System, “MSB Leads the Way With FPT – AKA – mParticle in Transforming Data Into Superior Customer Experiences,” FPT IS, fpt-is.com In banking, the problem is not only personalization. It also affects reporting, service consistency, offer targeting, and the ability to connect a customer’s digital and assisted interactions into one record. In retail, the same issue appears when loyalty programs, in-store transactions, online purchases, and marketplace interactions are stored in separate environments. Because these issues are operational and regulatory at the same time, identity resolution remains a core growth driver for the Vietnam customer data platform market. The strength of this driver also helps explain why large enterprises still account for most current spending, since complex orchestration usually needs bigger internal teams and partner support.

AI-Enabled Personalization and Next-Best-Action Use Cases

Banks and retailers in Vietnam are moving from static segmentation toward AI-assisted recommendations, onboarding flows, and customer treatment rules, which raises the value of real-time data activation. VIB deployed Salesforce Data 360, Agentforce Financial Services, Agentforce Marketing, and MuleSoft in June 2026 across operations serving 7 million customers in 33 provinces and more than 200 branches, with plans that include AI-driven segmentation and product recommendations. FPT Corporation and Salesforce also launched an ASEAN Data and AI Innovation Center in Hanoi in April 2026, which adds local implementation capacity and talent development for data-led banking use cases. These moves matter because AI performance depends on usable, connected, and permissioned customer data rather than isolated campaign lists. The customer analytics and insights application segment is therefore becoming an important proving ground for enterprises that want measurable gains before scaling wider activation programs. As more firms in the Vietnam customer data platform market link unification with AI use cases, platform selection is likely to depend more on activation depth than on storage alone.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Limited In-House Data Engineering and Martech Talent | -4.8% | National, most severe in secondary cities and among non-technology enterprises | Long term (≥ 4 years) |

| High Integration Effort With Legacy and Local Digital Systems | -3.9% | National, concentrated in banking, insurance, and traditional retail sectors | Medium term (2-4 years), Long term (≥ 4 years) |

| Budget Sensitivity Among Mid-Market Buyers | -3.1% | National, highest in SME-heavy provinces outside Ho Chi Minh City and Hanoi | Medium term (2-4 years) |

| Consent Reconciliation Across Distributed Data Sources | -2.2% | National, most acute for multi-entity businesses with fragmented infrastructure | Short term (≤ 2 years), Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited In-House Data Engineering and Martech Talent

Talent limitations remain one of the clearest restraints on execution in the Vietnam customer data platform market, especially for companies that can buy software but cannot activate it well. Vietnam National University Hanoi reported in its 2025 Annual AI Report that 45% of AI providers saw the lack of high-quality human resources as their main barrier, which shows how capacity constraints extend beyond one product category. VINASA also projected a major IT professional shortfall by the end of 2026, reinforcing the view that technical labor supply is not keeping pace with digital demand.[2]Vietnam Software and IT Services Association, “Vietnam Tech Talent Shortage 2026,” NKK, nkk.com.vn customer data platform projects are especially exposed because they depend on data pipeline work, integration mapping, governance rules, and activation logic rather than on simple license installation. This gap tends to delay value realization after procurement, which can raise churn risk when customers do not move beyond initial deployment. It also helps local and modular suppliers, because an easier setup and lighter engineering demands are often more attractive than broader feature depth.

High Integration Effort With Legacy and Local Digital Systems

Integration difficulty remains a major brake on adoption, because many Vietnamese banks, insurers, and traditional retailers still operate older systems that were not designed for real-time data exchange. FPT Information System described BIDV’s migration from a legacy card core platform to Way4 as a foundational step in digital transformation, illustrating how deeply legacy architecture still shapes enterprise technology decisions. In practice, customer data platform rollout often requires custom interfaces, schema harmonization, and process redesign across local software, core systems, and cloud tools. That work can stretch deployment schedules and raise the total cost of ownership, especially when sensitive data must remain under stricter control. The compliance environment adds to the burden, because vendors must align architecture choices with residency, governance, and consent requirements under the new legal regime. As a result, implementation depth and partner capability often matter as much as product features when buyers evaluate the Vietnam customer data platform market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Anchors Revenue While Services Gain Weight

Software held 74.26% of the Vietnam customer data platform market share in 2025, which confirms that platform licensing still sits at the center of most buying decisions. This pattern reflects a market that is still building core infrastructure, because many adopters are first focused on data collection, profile unification, and basic activation rather than full optimization. In the Vietnam customer data platform industry, software remains the main commercial entry point because a platform is required before enterprises can organize consent, identities, and omnichannel workflows in one place. Many buyers also prefer to secure a stable core system before widening spend into service-heavy work such as custom models, deeper orchestration, and advanced analytics. This explains why software captured most revenue even as implementation complexity continued to rise.

Services is projected to grow at a 40.16% CAGR from 2026 to 2031, which points to a market moving from procurement toward execution. MSB’s 88-day activation cycle showed that real deployment often depends on ecosystem partners that can integrate data sources, configure use cases, and support activation across operational tools. Service demand is also widening because enterprises increasingly want managed analytics, implementation support, consent configuration, and change management rather than only software access. Compliance-related support is becoming more visible in this mix, since privacy documentation and control design now influence vendor selection and rollout sequencing.[3]Government of Vietnam, “The Latest Law on Personal Data Protection and the Guiding Documents,” LuatVietnam, english.luatvietnam.vn Over time, this should make the Vietnam customer data platform market less dependent on licensing alone and more tied to execution services that turn purchased capability into live business outcomes.

By Deployment Mode: Cloud Leads While Hybrid Gains Strategic Ground

Cloud deployment accounted for 68.12% of the Vietnam customer data platform market size in 2025, which shows that scale, speed, and lower infrastructure burden remain strong buying priorities. This lead is closely tied to digital commerce and retail, where businesses often need flexible rollout, simpler upgrades, and easier activation across distributed sales channels. Cloud deployment also fits the needs of organizations with lean internal technology teams, because it reduces the burden of managing core infrastructure in-house. For many adopters, this makes the cloud the most practical path to unify customer data from marketplaces, web properties, mobile touchpoints, and messaging channels. The current lead of cloud, therefore, reflects operating reality rather than only technology preference.

Hybrid deployment is projected to grow at a 41.73% CAGR from 2026 to 2031, which shows how sector-specific compliance needs are reshaping architecture decisions. Financial institutions and other sensitive sectors increasingly need a structure that can keep critical data under tighter control while still using cloud layers for activation and analytics. The Personal Data Protection Law and its implementing decree have made governance and accountability more central to architecture planning, which supports a stronger case for hybrid designs. On-premises remains the smallest deployment mode, but it still matters in government-adjacent and state-linked settings where infrastructure control stays a hard requirement. In the Vietnam customer data platform industry, this means the long-term story is not a simple shift from on-premises to cloud, but a more selective move toward hybrid environments that balance speed with governance.

By Organization Size: Large Enterprises Lead Spend While SMEs Build Momentum

Large enterprises held 67.82% of the Vietnam customer data platform market share in 2025, reflecting their stronger budgets, deeper integration capacity, and better access to implementation partners. This group includes the banks and large enterprises that have already moved into significant deployments, such as MSB and VIB, where use cases extend across customer service, product targeting, and data-led engagement. Large organizations are better placed to deal with fragmented legacy systems, stricter governance demands, and longer rollout cycles. They also have more incentive to invest because value rises quickly when customer activity is spread across many business lines and channels. This combination keeps large enterprises at the center of present-day revenue in the Vietnam customer data platform market.

SMEs are projected to grow at a 41.24% CAGR from 2026 to 2031, supported by modular and lower-code offerings that reduce technical burden. CNV Loyalty reported more than 3,000 SME clients across food and beverage, retail, education, and healthcare in Vietnam by 2025, which shows that smaller businesses are already finding practical use cases for customer data unification.[4]CNV Loyalty, “Lý Do Nào Thuyết Phục Hơn 3.000 Doanh Nghiệp Chọn CDP,” CNV Loyalty Platform, cnv.vn Those clients also reported lower marketing costs and stronger repeat purchase behavior after adoption, which helps explain why SME interest is rising. Native connectivity with local channels such as Zalo lowers entry barriers further, because small firms can activate data without building large custom stacks. National digital transformation support for SME technology adoption adds another layer of momentum, which should widen the buyer base of the Vietnam customer data platform market over the forecast period.

By Application: Profile Unification Remains Foundational While Personalization Expands Fastest

Customer data collection and profile unification accounted for 29.16% share in 2025, making it the largest application because it supports every downstream CDP use case. Without one usable profile, companies cannot run high-quality segmentation, journey orchestration, or consent management across multiple touchpoints. This is why profile unification remains the first operational step for many buyers in the Vietnam customer data platform market, especially those dealing with fragmented commerce and service channels. The size of this segment also reflects a market that is still normalizing core data infrastructure before moving deeper into full activation. Even when companies plan advanced use cases, they usually start by repairing fragmented customer identity and record quality.

Audience segmentation and personalization are projected to grow at a 42.32% CAGR from 2026 to 2031, showing that buyers are moving from data assembly toward data use. VIB’s 2026 deployment highlighted this direction, because the roadmap includes AI-assisted segmentation and recommendation workflows built on a broader customer data foundation. Marketing campaign and customer journey orchestration are also gaining momentum because enterprises increasingly want action layers across email, push, web, and messaging rather than static customer records. Consent and preference management is becoming more material as well, since traceable permission handling has moved from a helpful feature to a compliance requirement. Customer analytics and insights is therefore becoming an important evaluation point, because buyers want proof that profile unification can improve retention, conversion, or lifetime value before they scale broader deployment.

By End-User Industry: Retail Leads Demand While Healthcare Accelerates

Retail and e-commerce held 33.37% share in 2025, giving the segment the largest position among end-user industries in the Vietnam customer data platform market. The lead comes from constant pressure to unify customer behavior across marketplaces, direct channels, mobile experiences, store systems, and loyalty tools. The Ministry of Industry and Trade’s e-commerce figures support that position, because rapid online commerce growth naturally expands the number of systems and interactions that merchants must connect. BFSI remains another major demand center because banks need better identity resolution, more consistent service journeys, and stronger governance around sensitive customer data. Together, these sectors account for much of the present revenue base because they combine high transaction intensity with clear business and compliance value.

Healthcare and life sciences are projected to grow at a 42.86% CAGR from 2026 to 2031, making it the fastest-moving vertical. This momentum is being driven by public-sector digitalization rather than only by commercial marketing demand, because Vietnam’s Ministry of Health has pushed electronic medical records and broader digital infrastructure across the care system. The ministry reported nearly 40 million citizen health records on the VNeID platform by April 2026 and continued to advance national data architecture for healthcare, which creates infrastructure conditions that fit CDP-style unification needs. FPT and Utop’s CRM and CDP deployment for the Saigon Eye Hospital System provides an early commercial example of how that demand is entering live healthcare settings. IT and telecom, media and entertainment, and industrial manufacturing remain smaller segments, but they provide steady incremental demand as retention analytics and customer engagement programs become more important.

Geography Analysis

Vietnam is the only geographic unit in the Vietnam customer data platform market, so national shifts in e-commerce, digital engagement, and privacy law shape the entire addressable opportunity. The Ministry of Industry and Trade stated that e-commerce reached USD 31 billion in 2025, and the 2026 action plan targets USD 37 billion, which keeps the operating environment favorable for customer data unification tools. The same source noted that e-commerce represented nearly 10% of total national retail sales in 2025, which shows how central digital channels already are to customer acquisition and retention. Online shopping penetration also remains broad, which means CDP demand is not confined to a narrow consumer niche but tied to a large national digital customer base. Because the Vietnam customer data platform market sits inside a single-country framework, changes in regulation and digital behavior can scale quickly across the market rather than diffusing across many jurisdictions.

Within the country, Ho Chi Minh City remains the strongest commercial node for deployment because it concentrates major retail groups, digital commerce firms, fintech activity, and foreign-invested businesses. Hanoi plays a different role, with stronger demand from state-linked enterprises, large banks, and technology ecosystems that are increasingly connected to data and AI deployment. The April 2026 launch of the ASEAN Salesforce Center of Excellence for Data and AI Innovation in Hanoi reinforces the city’s role as a delivery and talent hub for customer data applications. Da Nang is emerging as a secondary node as more service and manufacturing businesses adopt digital engagement tools and require better customer data management. This internal spread matters because the Vietnam customer data platform market is not growing from one uniform demand pattern, but from different city-level mixes of retail, finance, public-sector, and SME activity.

The legal framework now applies across all provinces and cities, which means procurement criteria are being reshaped at the national level rather than only in top-tier urban centers. Law No. 91/2025/QH15 and its implementing decree have made consent traceability, data handling discipline, and accountability more central to platform selection. Healthcare digitalization is extending this demand beyond the two largest cities, because hospitals and health facilities across the country are being drawn into electronic record and data infrastructure programs. That creates room for vendors that can implement outside tier-1 city ecosystems and support organizations across Vietnam’s wider provincial footprint. Geography therefore supports growth in the Vietnam customer data platform market not through cross-border expansion, but through deeper spread across domestic verticals and city clusters.

Competitive Landscape

The Vietnam customer data platform market remains moderately fragmented, with no single vendor dominating both enterprise and mid-market demand. Global enterprise platforms such as Salesforce, Adobe, SAP, Oracle, and Microsoft compete most directly for large accounts that need wider orchestration, ecosystem support, and multi-function integration. Regional specialists such as Antsomi, Insider, Tealium, and Bloomreach sit between global scale and local flexibility, while Vietnam-native providers such as PangoCDP, Mobio, and CNV Loyalty compete through price, local channel integration, and implementation simplicity. This structure keeps competition active because buyers are not selecting from one narrow feature ladder. They are often choosing between different operating models, different deployment assumptions, and different levels of local fit.

Strategic moves in 2025 and 2026 show that vendors are competing through ecosystem depth rather than product claims alone. Salesforce strengthened its position through VIB’s June 2026 deployment of Data 360, Agentforce, and MuleSoft, which embedded the platform in a large retail banking environment serving 7 million customers. Salesforce also deepened local enablement through its April 2026 center in Hanoi with FPT, which ties product adoption to implementation and talent capacity. Antsomi took a different route by extending its footprint through a March 2026 partnership with Hakuhodo DY ONE for Japan, which signals a regional growth strategy built on Southeast Asian CDP experience. These actions show that competitive position in the Vietnam customer data platform market depends on delivery capability, partner reach, and use-case credibility as much as on platform breadth.

White-space remains visible in healthcare deployment, government-linked data unification, and SME-oriented managed offerings where internal technical capacity is limited. Local vendors appear well placed in these spaces because they can align more closely with Zalo-based engagement models, local support expectations, and domestic compliance workflows. CNV Loyalty’s scale among smaller businesses suggests that the lower end of the market can be meaningful when setup is simple and value is tied to repeat purchase and marketing efficiency. Public procurement also matters, as shown by Vietnam Airlines’ January 2026 call for bids for a CDP system covering August 2026 to July 2031, which points to visible enterprise demand beyond banking and retail. The result is a market where global vendors keep the large-account edge, but local and regional suppliers can still win by removing friction around implementation, channel fit, and compliance execution.

Vietnam Customer Data Platform Industry Leaders

Adobe Inc.

Acquia, Inc.

Antsomi

Bloomreach, Inc.

HubSpot, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: VIB deployed Salesforce Data 360, Agentforce Financial Services, Agentforce Marketing, and MuleSoft across its retail banking operations serving 7 million customers across 200+ branches in 33 provinces, with Deloitte as implementation partner. The platform is designed to consolidate customer profiles across relationship management, lending, deposit, and contact center operations, with planned AI-driven workflows for segmentation and product recommendations.

- April 2026: FPT Corporation and Salesforce launched the first ASEAN Salesforce Center of Excellence for Data and AI Innovation in Hanoi, located at FPT Tower. The center, which provides a controlled environment for financial institutions to deploy data-driven applications, leverages FPT's base of over 1,000 Salesforce-certified developers and more than 800 professional certifications, with training programs on Agentforce and Data 360 designed to develop in-country AI-ready talent.

- January 2026: Vietnam Airlines issued a call for bids for the implementation of a Customer Data Platform system covering the period August 2026 to July 2031, with proposals submitted to the Digital Marketing Department by February 2026. The 5-year CDP implementation mandate from the national carrier represents one of the largest publicly disclosed CDP procurement commitments in Vietnam's aviation sector.

- June 2025: MSB Bank activated its CDP deployment with mParticle, FPT, and AKA Digital within 88 days of project initiation, enabling 14 customer use cases, enriching over 700 customer attributes, and reducing reporting workload by up to 90% by integrating real-time data from the bank's website, mobile app, and core EDP system with engagement tools including Insider, Appsflyer, Cortex AI, Indicative, and Qualtrics.

Vietnam Customer Data Platform Market Report Scope

The Vietnam customer data platform market includes platforms and services that consolidate customer data from multiple sources into unified, centralized profiles. These platforms support identity resolution, real-time integration, segmentation, personalization, and analytics, enabling enterprises in Vietnam to deliver consistent omnichannel customer experiences. Rapid e-commerce growth, a mobile-first consumer base, and the increasing adoption of AI-powered personalization drive the market. Evolving data privacy regulations and the growing demand for scalable martech solutions across the retail, banking, and telecom sectors also influence market dynamics.

The Vietnam Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid) Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administrationm and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size outlook for the Vietnam customer data platform market?

The Vietnam customer data platform market was valued at USD 30.11 million in 2025, stands at USD 41.99 million in 2026, and is forecast to reach USD 225.51 million by 2031 at a 39.96% CAGR.

What is driving customer data platform adoption in Vietnam?

The main drivers are fast e-commerce growth, fragmented customer data across channels, tighter privacy compliance needs, stronger first-party data strategies, and rising interest in AI-led personalization.

Which deployment model leads CDP adoption in Vietnam?

Cloud led with 68.12% share in 2025 because it offers faster deployment and lower infrastructure burden, while hybrid is projected to grow fastest at 41.73% CAGR as regulated sectors balance scale with governance.

Which end-user sector creates the most revenue in Vietnam?

Retail and e-commerce led with 33.37% share in 2025, because brands in this segment need to unify data from marketplaces, direct sites, apps, loyalty tools, and offline channels.

Why is healthcare becoming important for CDP vendors in Vietnam?

Healthcare and life sciences is projected to grow at a 42.86% CAGR through 2031, supported by electronic medical record rollout, broader health data infrastructure, and early commercial deployments in hospital systems.

Are local vendors competitive against global CDP providers in Vietnam?

Yes. Global vendors remain strong in large-enterprise accounts, but local vendors are gaining through lower setup burden, closer compliance fit, and stronger integration with local platforms such as Zalo.

Page last updated on: