Vietnam Construction Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

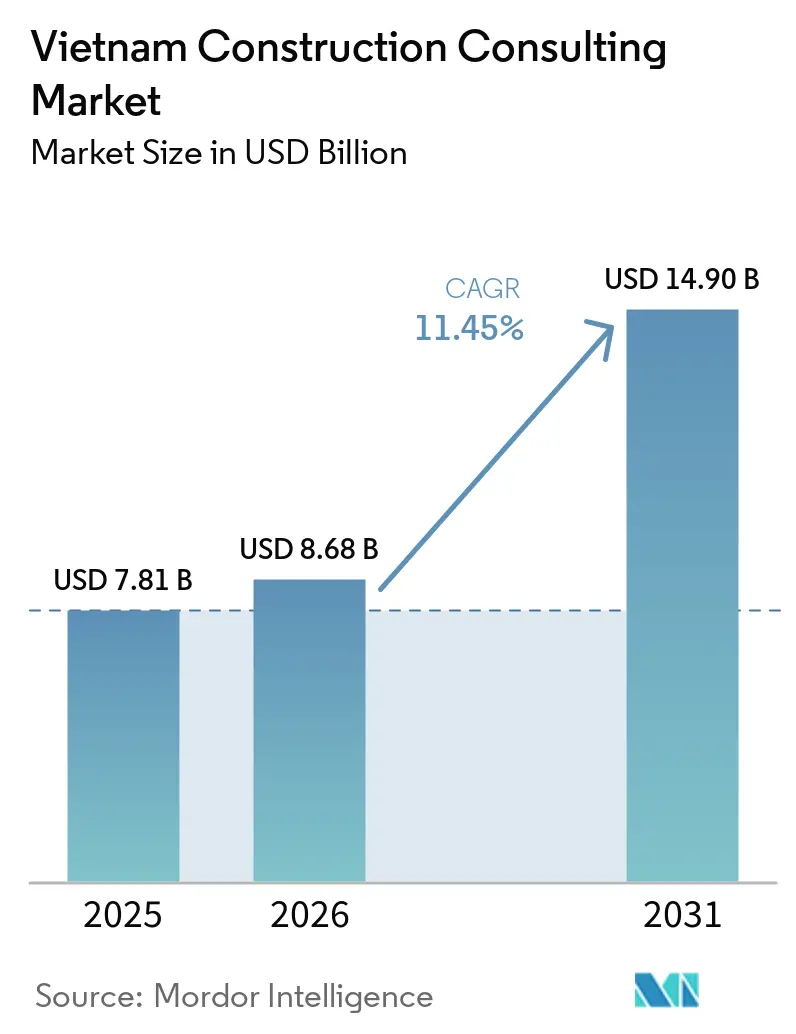

| Base Year Market Size (2025) | USD 7.81 Billion |

| Market Size (2026) | USD 8.68 Billion |

| Market Size (2031) | USD 14.90 Billion |

| Growth Rate (2026 - 2031) | 11.45% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vietnam Construction Consulting Market Analysis by Mordor Intelligence

The Vietnam construction consulting market size was valued at USD 7.81 billion in 2025 and is estimated to grow from USD 8.68 billion in 2026 to reach USD 14.9 billion by 2031, at a 11.45% CAGR during the forecast period (2026–2031). Heightened demand for front-end engineering studies on the USD 67 billion North–South High-Speed Rail and the USD 59 billion Eastern North–South Expressway is creating a long-term project pipeline that specialized Vietnamese consultants are well positioned to serve. Decision 258/QD-TTg’s nationwide BIM mandate now requires every Class II or larger project to submit a federated 3D model, accelerating the shift of the Vietnam construction consulting market toward digital and data-driven project delivery.

Updated PPP legislation is encouraging private-sector participation by allowing viability gap funding of up to 50% of project costs, thereby expanding opportunities for transaction advisory services across the transport, energy, and water infrastructure sectors. At the same time, the State Bank of Vietnam’s green-credit taxonomy is directing subsidized financing toward energy-efficient retrofits, supporting a rapidly growing niche in renovation and sustainability consulting within the Vietnam construction consulting market.

Key Report Takeaways

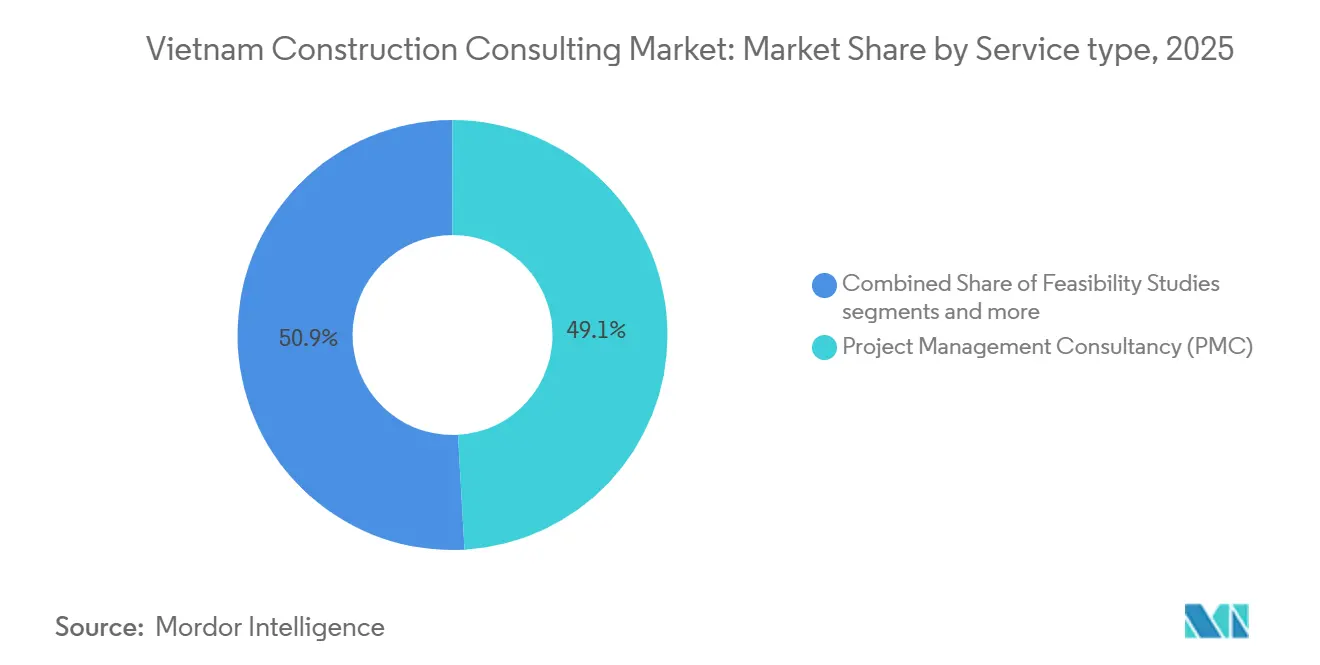

- By service type, the project management consultancy commanded 49.12% of the Vietnam construction consulting market share in 2025, while design and engineering services are projected to advance at a 14.66% CAGR through 2031.

- By sector, the residential consulting accounted for 44.33% of the Vietnam construction consulting market size in 2025, while the infrastructure consulting is projected to expand at 13.28% CAGR through 2031.

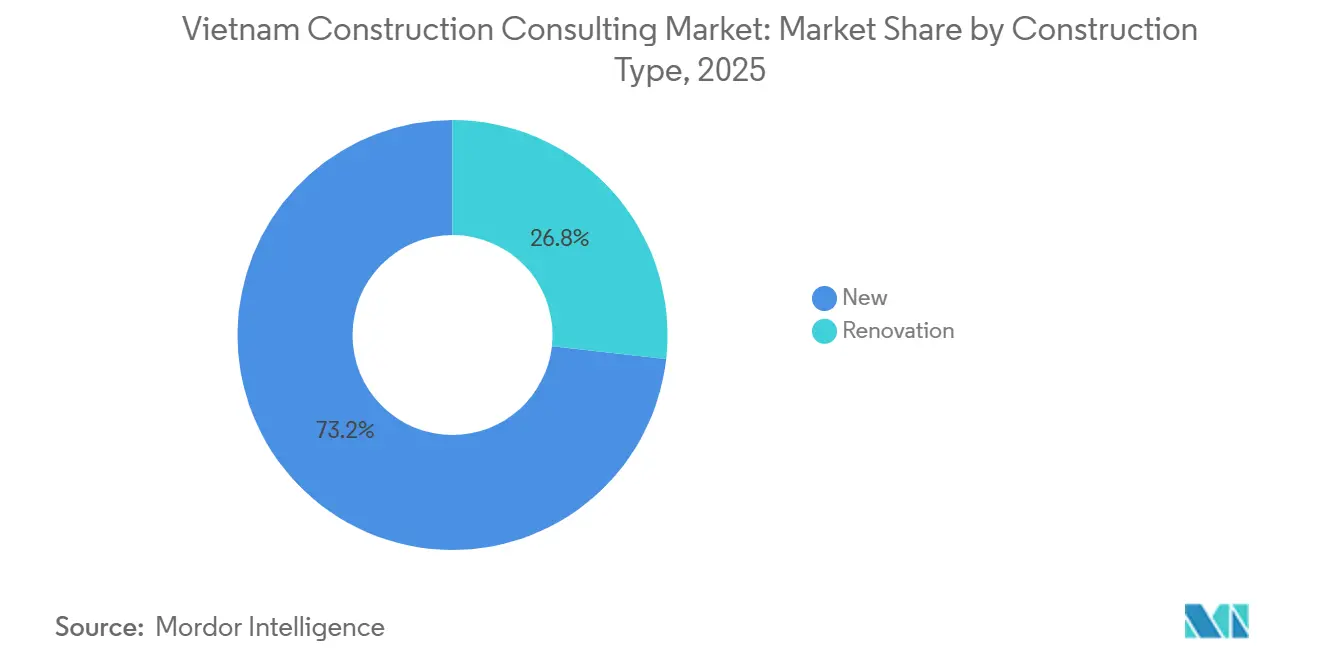

- By construction type, the new construction held 73.22% of the Vietnam construction consulting market share in 2025, while renovation consulting is projected to grow at 13.85% CAGR through 2031.

- By investment source, the public-sector projects accounted for 63.55% of the Vietnam construction consulting market size in 2025, while private-sector consulting is projected to post the fastest CAGR at 13.63% through 2031.

- By key cities, Ho Chi Minh City led with 38.10% of the Vietnam construction consulting market share in 2025, while the rest of Vietnam is projected to record the fastest CAGR at 13.85% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Vietnam Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| North-South High-Speed Rail & Eastern Expressway megaprojects fuelling multi-phase consulting demand | +3.2% | National, with early gains in Hanoi, Vinh, Nha Trang, and HCMC corridors | Long term (≥ 4 years) |

| BIM Adoption Roadmap 2023–2030 accelerating digital PMC Uptake | +2.5% | National, with faster adoption in HCMC, Hanoi, and Danang | Medium term (2–4 years) |

| Mandatory EIA Decrees & Decree 10 feasibility rules tightening pre-construction due diligence | +2.1% | National, stricter enforcement in Group I projects across all provinces | Medium term (2–4 years) |

| PPP Law 2020 revisions & Viability-Gap-Fund sweeteners raising transaction-advisory needs | +1.8% | National, concentrated in transport, energy, water/waste sectors | Medium term (2–4 years) |

| Saigon-Dong Nai "semicon & aerospace" super-clusters driving specialised infra-advisory | +1.5% | Dong Nai province and surrounding industrial corridors, with spillover to Ba Ria-Vung Tau and Binh Duong for supporting infrastructure | Long term (≥ 4 years) |

| SBV Green-Credit taxonomy incentivising green-building (EDGE/LOTUS) sustainability consulting | +1.3% | National, with early concentration in HCMC and Hanoi commercial districts; expanding to industrial parks in Dong Nai and Binh Duong | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

North-South High-Speed Rail & Eastern Expressway Megaprojects Fuelling Multi-Phase Consulting Demand

The government's December 2026 approval of the USD 67 billion North-South High-Speed Rail spanning 1,541 kilometers and the ongoing USD 59 billion Eastern North-South Expressway expansion create a sustained pipeline for feasibility studies, detailed engineering, and project-management consultancy through 2035. Resolution 106/NQ-CP mandates a Front-End Engineering Design approach for the rail project, requiring consultant selection by December 2025 and phased feasibility deliverables that integrate land-clearance schedules, rolling-stock procurement, and station-precinct master plans[1]"North-South High-Speed Railway Project." Construction.gov.vn. Accessed April 16, 2026. https://construction.gov.vn. The expressway program, which added 2,063 kilometers of BOT and PPP sections by 2025, is now expanding into mountainous provinces where geotechnical surveys, environmental-impact assessments, and transaction-advisory services command premium fees. This dual-megaproject cycle extends consultant revenue visibility beyond typical 2-to-3-year project horizons, enabling firms to invest in specialized capabilities such as high-speed-rail signaling design and expressway intelligent-transport-system integration. Smaller domestic consultants are forming joint ventures with Japanese and European firms to access FEED methodologies and secure positions on Ministry of Transport empanelment lists, while international players are establishing local subsidiaries to meet local-content requirements and capture long-term retainer contracts.

BIM Adoption Roadmap 2023-2030 Accelerating Digital PMC Uptake

Prime Minister Decision 258/QD-TTg, issued March 17, 2023, established a phased BIM mandate requiring all Class I and special-grade projects to adopt BIM from 2023, Class II and above from 2025, and universal coverage by 2030, transforming project-management consultancy from document-centric coordination to data-centric collaboration. Decree 175/2024 reinforces this by making BIM compulsory for Group B Level II+ projects, effectively covering the majority of public infrastructure, commercial high-rises, and industrial facilities. WSP Vietnam's Thu Thiem 2 Bridge, which opened in April 2022, served as the country's first BIM pilot using Finnish BIM guidelines and 3D IFC data transfer, demonstrating clash-detection savings and 100-year design-life validation that are now benchmarks for Ministry of Transport projects. However, a 2020 IOP Conference Series study identified acute shortages of BIM Managers, BIM Coordinators, and BIM Modelers, with 90 analyzed job vacancies clustering in southern Vietnam and revealing gaps in professional licensing and state-agency certification standards. Consultants are responding by partnering with technology providers such as Autodesk and Bentley Systems to deliver training programs, while international firms are transferring proprietary BIM workflows from Singapore and Australia to capture early-mover advantage on high-visibility projects such as Long Thanh Airport City, where CONINCO and Nihon Sekkei are co-developing the master-plan concept using integrated BIM and GIS platforms.

Mandatory EIA Decrees & Decree 10 Feasibility Rules Tightening Pre-Construction Due-Diligence

Law on Environmental Protection 2020, operationalized through Decree 08/2022-ND-CP and Decree 40/2019-ND-CP, classifies projects into Group I through Group IV based on environmental risk, with Group I requiring Ministry of Natural Resources and Environment approval and Group II requiring provincial Department of Natural Resources and Environment sign-off. Decree 175/2024-ND-CP, effective November 1, 2024, further mandates FEED-level feasibility studies for all Group B Level II and above construction projects, compelling developers to engage consultants earlier in the project lifecycle and allocate larger budgets to baseline surveys, social-impact assessments, and climate-resilience modeling. This regulatory tightening is particularly consequential for infrastructure and industrial projects in Dong Nai, Binh Duong, and Hai Phong, where rapid industrialization has triggered stricter scrutiny of air quality, water discharge, and biodiversity impacts. Consultants with ISO 14001 certification and in-house laboratories accredited by the Bureau of Accreditation are securing repeat engagements, as developers seek to de-risk approval timelines and avoid the project slippages that plagued 386 land-clearance-dependent projects in Hanoi during 2025. The shift from post-design EIA to integrated FEED also raises the technical bar, favoring firms that can deploy multi-disciplinary teams spanning civil, environmental, and social specialists over generalist PMC providers.

PPP Law 2020 Revisions & Viability-Gap-Fund Sweeteners Raising Transaction-Advisory Needs

Law 64/2020/QH14, effective January 1, 2021, introduced Viability Gap Funding capped at 50% of total project cost and minimum revenue guarantees for transport, energy, water, waste, health, education, and IT infrastructure, lowering private-sector hurdle rates and expanding the universe of bankable PPP projects. The law sets minimum thresholds of VND 200 billion for national projects and VND 100 billion for provincial projects, filtering out marginal proposals while concentrating transaction-advisory demand on larger, more complex structures that require financial modeling, risk allocation, and lender negotiation. The April 2026 groundbreaking of the HCM City-Moc Bai Expressway, a 51-kilometer, VND 19.6 trillion BOT project, exemplifies how VGF sweeteners enable consultants to structure hybrid financing that blends state capital, commercial debt, and equity from construction contractors VnExpress. However, the same law imposes stricter feasibility and due diligence requirements, compelling sponsors to engage transaction advisors for 12-to-18-month pre-tender periods that include traffic studies, tariff modeling, and stakeholder consultations. Consultants with prior experience on Asian Development Bank or World Bank co-financed PPPs are commanding premium fees, as they bring familiarity with multilateral procurement standards and environmental-safeguard frameworks that de-risk lender approvals and accelerate financial close.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SOE payment delays & cost overruns are squeezing consultant cash-flows | -1.6% | National, concentrated in the transport and energy sectors | Short term (≤ 2 years) |

| Lowest-bid tendering bias-reducing value-added consulting scope | -1.4% | National, more acute in provincial SOE projects | Short term (≤ 2 years) |

| Shortage of LEED/BIM-certified professionals limiting capacity | -1.2% | National, with acute gaps in southern Vietnam where BIM job vacancies cluster; only 11.8% of construction workforce holds college/intermediate qualifications | Medium term (2-4 years) |

| Fragmented provincial approvals causing project slippages | -0.9% | National, particularly severe in Hanoi (386 land-clearance-dependent projects delayed in 2025) and Mekong Delta provinces facing contractor mobilization failures | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

SOE Payment Delays & Cost Overruns Squeezing Consultant Cash-Flows

Public investment disbursement reached only VND 553,250 billion, or 60.6% of the 2025 plan, by the end of December 2025, leaving approximately VND 360,000 billion undisbursed and creating cash-flow bottlenecks for consultants awaiting milestone payments[2]"Public Investment Disbursement 2025." Ministry of Planning and Investment. Accessed April 16, 2026. https://mpi.gov.vn. CIENCO4, a major state-owned contractor, accumulated VND 941.7 billion in unfinished construction liabilities and saw over VND 156.8 billion stuck in the Ben Thanh-Suoi Tien Metro project, resulting in a 4-year bidding ban by Ha Nam province. Hoa Binh Construction, another prominent SOE, failed to pay VND 10.2 billion in Q2 2025 bond interest and carried total debt of VND 13.4 trillion, with the largest exposures to BIDV at VND 1,804 billion and VietinBank at VND 1,297 billion. These payment delays cascade to consultants, who often wait 90 to 180 days beyond contractual terms for invoice settlement, forcing them to finance working capital through expensive short-term credit and diverting management attention from project delivery to collections. The January 2026 termination requests for Can Tho-Ca Mau expressway contractors, including VNCN E&C, Thi Son, and Hai Dang, underscore how SOE financial distress triggers project suspensions that strand consultant resources and create stranded costs. In the renewable-energy sector, 23 foreign investors representing over 4,182 megawatts and 173 projects remained unpaid or partially paid since January 2025, with some awaiting settlement since August 2022, due to Circular 10/2023 cost-component-adjustment requirements. While the Prime Minister ordered debt-payment extensions and a VND 500 trillion credit package for infrastructure and digital technology in April 2025, the structural mismatch between annual budget allocations and multi-year project timelines persists, making cash-flow management a critical constraint for consultant growth and capacity investment.

Lowest-Bid Tendering Bias Reducing Value-Added Consulting Scope

Circular 79/2025/TT-BTC, effective July 2, 2025, mandates the Vietnam National E-Procurement System for all public-sector bidding, increasing transparency through digital signatures and contractor-profile extraction from national databases, but also intensifying price competition as all bids become publicly visible in real time. State-owned developers and provincial authorities frequently default to lowest-bid selection criteria, compressing consultant margins and incentivizing firms to strip out value-added services such as constructability reviews, life-cycle cost analysis, and post-construction performance monitoring. This dynamic is particularly pronounced in provincial road and irrigation projects, where procurement officers lack technical expertise to evaluate qualitative differentiation and default to price as the sole decision variable. The result is a race to the bottom that erodes consultant profitability, discourages investment in advanced capabilities such as BIM and digital twins, and increases project-delivery risk as under-resourced consultants cut corners on design verification and site supervision. International firms with diversified revenue streams can absorb occasional low-margin public tenders, but smaller domestic consultants face existential pressure, leading to industry consolidation and the exit of mid-tier players. Circular 79/2025/TT-BTC introduces standardized webform templates and performance-record disclosure, which may eventually shift evaluation criteria toward track record and technical capacity, but the transition period is creating uncertainty and margin compression across the sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: PMC Dominates, Design & Engineering Surges on BIM Mandates

Project Management Consultancy accounted for 49.12% of the 2025 Vietnam construction consulting market share, reflecting its anchor role on highway and rail megaprojects. Design & Engineering is moving faster, expanding at a 14.66% CAGR to 2031 as BIM deliverables become compulsory for Class II and larger assets. Wider adoption of 5D cost models and clash-detection routines is driving up fee rates for firms that can integrate structural, MEP, and sustainability data in a single platform. Feasibility-study work is also growing because stricter environmental reviews now begin before land acquisition.

The Vietnam construction consulting market for master planning and digital twin services is still small but growing rapidly around Long Thanh Airport City and new industrial clusters. Domestic leaders are racing to train BIM talent through university alliances, while global majors re-use workflows honed in Singapore and Australia. Mid-tier firms that rely on 2D CAD are seeing scope restricted to tender documentation, which pays lower margins. Over 2026-2031, service diversification and digital depth will dictate winners more than headcount scale.

By Sector: Infrastructure Consulting Accelerates on Semiconductor and Aerospace Clusters

Residential schemes captured 44.33% of 2025 Vietnam construction consulting market share, driven by social-housing demand in Ho Chi Minh City, Hanoi, and fast-growing satellite towns. Infrastructure work, however, is forecast to post the fastest 13.28% CAGR through 2031 as Dong Nai’s semiconductor and aerospace zones demand clean-room utilities, high-purity water, and resilient power feeds. Transportation remains the largest infrastructure sub-segment thanks to the USD 67 billion high-speed rail and the USD 59 billion expressway program.

Within commercial property, data-center projects such as the 6 MW NTT HCMC1 facility signal a shift toward mission-critical design scopes that reward consultants with Tier III+ credentials. Energy & utilities consulting is also widening as PECC2 moves from hydropower to LNG and biomass pipelines. Social infrastructure, hospitals, schools, and museums benefit from green-credit incentives that cover EDGE or LOTUS certification costs. Collectively, these trends diversify revenue away from pure residential builds and give infrastructure-ready advisers a clear growth premium.

By Construction Type: Renovation Gains Momentum from Green-Credit Taxonomy

New-build assignments dominated with 73.22% of 2025 fees; yet renovation services are set to climb at a 13.85% CAGR, the fastest among construction types. Preferential green loans worth USD 19 billion–USD 30 billion now cover façade insulation, HVAC replacement, and solar-ready rooftops, making retrofit paybacks viable within five to seven years.

The Vietnam construction consulting market size for renovation hinges on mastering LOTUS, EDGE, or LEED pathways plus new caps on clinker and mandates for non-fired brick. Heritage buildings such as the Presidential Office in Hanoi illustrate the blend of seismic upgrades and carbon-reduction tactics now in demand. Consultants offering end-to-end energy audits, materials guidance, and certification management secure repeat work from institutional landlords. Skills in life-cycle cost modeling, rather than classic site supervision, are emerging as the key differentiator.

By Investment Source: Private Sector Accelerates on PPP Law 2020 and VGF Mechanisms

Public contracts still produced 63.55% of 2025 revenue, underpinned by ministry-funded rail and road programs. Private-sector fees are forecast to expand at a 13.63% CAGR to 2031 as PPP rules inject viability-gap funding covering half of upfront cost and guarantee minimum revenue. The Vietnam construction consulting market size linked to private investors should widen further once toll-road and waste-to-energy pilots reach financial close.

Sponsors now expect advisers to deliver bank-grade traffic models, risk allocation matrices, and lender presentations within 12-18 months—services that fetch higher bill rates than routine design. Delayed public disbursements are also nudging consultants toward privately financed schemes with firmer cash-collection cycles. In turn, private owners insist on tighter timetables and BIM-rich deliverables, favoring firms that can integrate scheduling, cost, and 3D models from day one. Over the forecast window, advisory work tied to private capital will be a critical hedge against state-budget volatility.

Geography Analysis

Ho Chi Minh City generated 38.10% of 2025 consulting revenue, representing the largest provincial share in the Vietnam construction consulting market. Metro extensions, Grade A office towers in District 1, and mixed-use developments in Thu Thiem are driving steady demand for feasibility studies, design services, and sustainability consulting. Following the BIM pilot on Thu Thiem 2 Bridge, city-funded projects increasingly require federated digital models, allowing digitally capable consulting firms to command premium fees. International developers also continue to prioritize LEED or EDGE certifications, creating strong opportunities for consultants with dedicated green-building expertise.

Hanoi remains the second-largest market, supported by its role as the seat of government ministries and as the northern terminus of the high-speed rail project, where FEED contracts were awarded in late 2025. Ministry office retrofits and public building upgrades under green financing programs are also supporting demand for renovation and energy-efficiency consulting services. Danang and Hai Phong add further market depth through port dredging, logistics parks, and coastal tourism developments that require a blend of marine engineering, environmental compliance, and project advisory services. Consulting firms that can combine stakeholder management with technical delivery are increasingly favored in central and northern project tenders.

The Rest of Vietnam segment, led by Dong Nai, Binh Duong, and Mekong Delta provinces, is forecast to grow at the fastest pace with a 13.85% CAGR through 2031. Consulting demand in Dong Nai is rising rapidly due to Long Thanh Airport City and significant foreign direct investment inflows supporting new industrial zones. Specialized opportunities are emerging in clean-room utilities, high-purity water systems, and resilient power infrastructure linked to semiconductor and aerospace clusters. However, execution risks remain, particularly in provinces facing land-clearance delays that can postpone supervision contracts. Firms that deploy bilingual site teams in secondary cities and adapt quickly to national BIM standards and mandatory e-procurement systems are expected to secure repeat business.

Competitive Landscape

The Vietnam construction consulting market exhibits moderate fragmentation, with international firms such as AECOM, WSP, Arcadis, Mott MacDonald, and Arup commanding premium fees on high-visibility infrastructure and commercial projects through proprietary BIM workflows and global knowledge transfer, while domestic leaders including CONINCO, TEDI, VIWASEEN, and PECC2 leverage Ministry of Transport and Ministry of Construction empanelment, local-content compliance, and cost competitiveness to dominate public-sector megaprojects. CONINCO's January 2026 performance—achieving 223.84% of contract-value plan and 155% of revenue plan in 2025, with a 2026 target of 30% revenue increase—signals how leading domestic consultants are scaling rapidly by forming joint ventures with Japanese and Chinese firms, deploying digital-transformation partnerships with Vietnam National University, and expanding geographically through strategic cooperation with developers such as Phu My Hung. White-space opportunities are emerging in transaction advisory for PPP projects, where Law 64/2020/QH14's Viability Gap Funding and minimum revenue guarantees are expanding the universe of bankable structures but creating acute demand for financial modeling, risk allocation, and lender negotiation that few domestic consultants can deliver at international standards. Niche disruptors include technology-platform providers partnering with consultants to deliver cloud-based project controls, AI-driven cost estimation, and digital-twin visualization, as evidenced by CONINCO's digital-transformation initiative and WSP's BIM pilot on Thu Thiem 2 Bridge.

Circular 79/2025/TT-BTC, effective July 2, 2025, mandates the Vietnam National E-Procurement System for all public-sector bidding, increasing transparency through digital signatures and contractor-profile extraction from national databases, but also intensifying price competition as all bids become publicly visible in real time. This regulatory shift is accelerating industry consolidation as mid-tier consultants lacking scale and digital capabilities exit or merge, while top-tier players invest in standardized webform templates, performance-record databases, and compliance teams to navigate the new procurement regime. PECC2's portfolio expansion into Long Son LNG (1,200 to 1,500 megawatts), multiple biomass projects totaling over 100 megawatts, and nuclear-power program involvement demonstrates how specialized consultants are using technology—including BIM adoption, EPC-F models, and partnerships with international equipment suppliers such as H&M, Solarvest, and First Solar—to differentiate and capture high-margin energy and utilities consulting. TEDI's October 2025 VECAS Awards—1 First Prize for My Thuan 2 Bridge, 4 Second Prizes, and 3 Third Prizes—underscore how technical excellence and industry recognition remain critical competitive levers in a market where Ministry of Transport and Ministry of Construction empanelment lists heavily weight past performance and peer validation.

Vietnam Construction Consulting Industry Leaders

-

AECOM Vietnam

-

Arcadis Vietnam

-

WSP Vietnam

-

Mott MacDonald Vietnam

-

Arup Vietnam

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: The Vietnamese government broke ground on the HCM City-Moc Bai Expressway, a 51-kilometer, VND 19.6 trillion (approximately USD 749 million) BOT project that will connect Ho Chi Minh City to the Cambodian border, creating sustained demand for transaction-advisory, design, and project-management consultancy services through 2030.

- March 2026: CONINCO secured supervision consultancy for the Tien Cat Social Housing Project in Phu Tho province, valued at VND 452 billion, expanding its portfolio in the social-housing segment and reinforcing its position as a leading domestic consultant on government-funded residential projects.

- January 2026: CONINCO and VIAR-Nihon Sekkei formed a joint venture to develop the master-plan concept for Long Thanh Airport City, integrating BIM and GIS platforms to support the 5,000-hectare airport footprint and surrounding industrial parks, targeting USD 15 billion to USD 20 billion in FDI between 2026 and 2030.

- January 2026: CONINCO partnered with Vietnam National University to accelerate digital transformation, focusing on BIM training, proprietary workflow development, and data-analytics capabilities to compete with international firms on high-visibility infrastructure projects.

Vietnam Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design & Engineering Services |

| Master Planning & Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| Ho Chi Minh City |

| Hanoi |

| Danang |

| Hai Phong |

| Rest of Vietnam |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design & Engineering Services | ||

| Master Planning & Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Key Cities | Ho Chi Minh City | |

| Hanoi | ||

| Danang | ||

| Hai Phong | ||

| Rest of Vietnam | ||

Key Questions Answered in the Report

How large is the Vietnam construction consulting market and how fast is it growing?

The Vietnam construction consulting market reached USD 7.81 billion in 2025, expanded to USD 8.68 billion in 2026, and is forecast to reach USD 14.9 billion by 2031, advancing at an 11.45% CAGR over 2026-2031.

Which consulting service type is experiencing the fastest growth?

Design and Engineering Services is expanding at 14.66% annually through 2031, driven by Prime Minister Decision 258/QD-TTg mandating BIM for Class I and special-grade projects from 2023 and Class II+ projects from 2025.

What megaprojects are fueling consulting demand?

The USD 67 billion North-South High-Speed Rail spanning 1,541 kilometers and the USD 59 billion Eastern North-South Expressway expansion create sustained demand for feasibility studies, detailed engineering, and project-management consultancy through 2035.

How is BIM adoption reshaping the competitive landscape?

Decree 175/2024 makes BIM mandatory for Group B Level II+ projects, creating a two-tier market where firms with in-house BIM capabilities capture high-margin design contracts while those reliant on traditional CAD workflows face margin compression.

Which geographic area offers the highest growth potential?

Rest of Vietnam is expanding at 13.85% annually through 2031, driven by Long Thanh International Airport and Dong Nai industrial parks targeting USD 15 billion to USD 20 billion in FDI between 2026 and 2030 for semiconductor, aerospace, and precision-mechanics clusters.

What are the biggest challenges facing consultants?

SOE payment delays left VND 360,000 billion undisbursed by end-2025, acute shortages of BIM-certified professionals with recruitment up 171.96% year-on-year while applications declined 42.52%, and lowest-bid e-procurement intensifying price competition.

How is the PPP Law 2020 influencing the market?

Law 64/2020/QH14 caps Viability Gap Funding at 50% of project cost and introduces minimum revenue guarantees, expanding bankable PPP projects and raising transaction-advisory demand for financial modeling, risk allocation, and lender negotiation.

What role is green-building certification playing?

State Bank of Vietnam allocated VND 500 trillion to VND 780 trillion in green credit growing at 14-22% annually for LOTUS and EDGE certifications, driving sustainability consulting demand and accelerating renovation consulting at 13.85% CAGR through 2031.

Which sector is growing fastest?

Infrastructure consulting is accelerating at 13.28% annually, outpacing Residential's 44.33% share of 2025 revenue, as Dong Nai attracted USD 550 million in FDI during early 2026 for specialized industrial clusters requiring advanced infrastructure advisory.

What strategies are leading consultants deploying to gain market share?

CONINCO achieved 223.84% of contract-value plan in 2025 by forming joint ventures with Japanese and Chinese firms, partnering with Vietnam National University for digital transformation, and expanding geographically through strategic cooperation with major developers.

Page last updated on: