Video Microscopes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

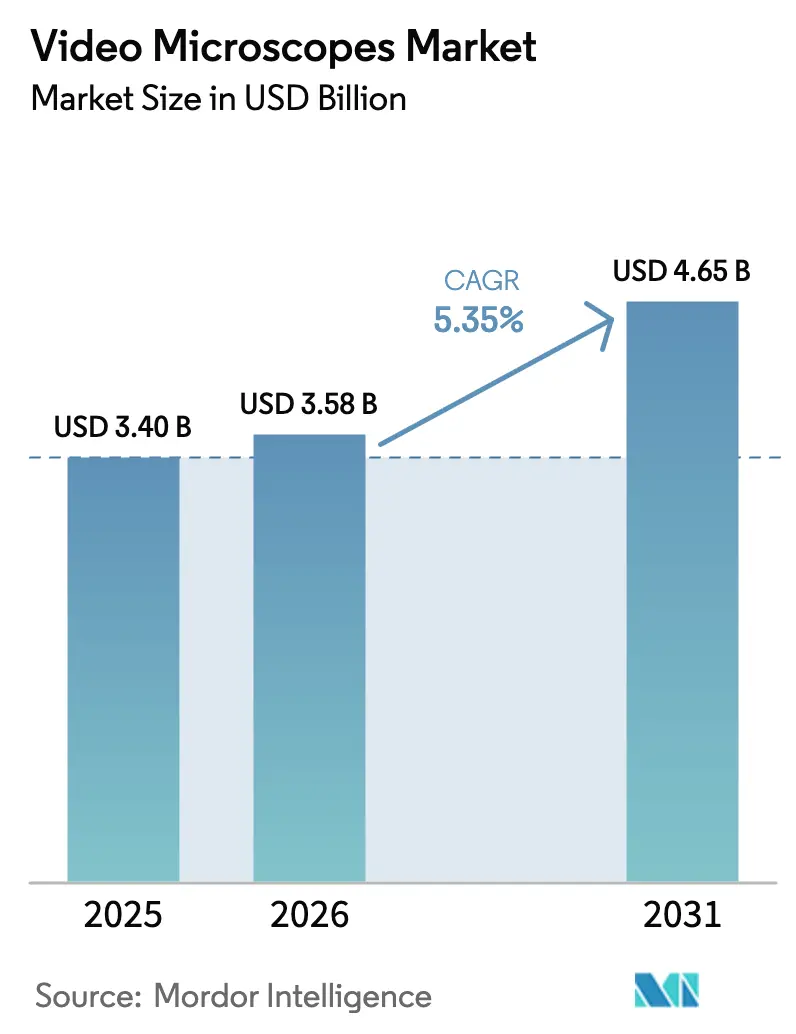

| Market Size (2026) | USD 3.58 Billion |

| Market Size (2031) | USD 4.65 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

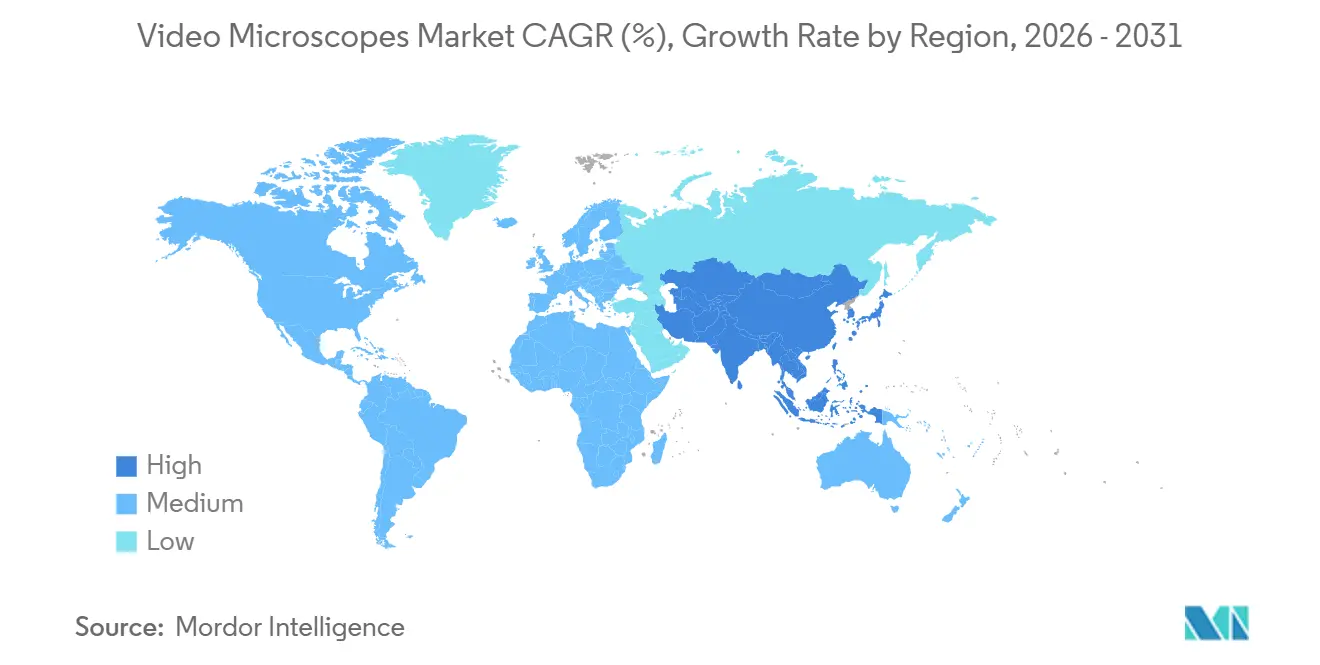

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Microscopes Market Analysis by Mordor Intelligence

The Video Microscopes Market size was valued at USD 3.40 billion in 2025 and is estimated to grow from USD 3.58 billion in 2026 to reach USD 4.65 billion by 2031, at a CAGR of 5.35% during the forecast period (2026-2031).

Growth is fueled by rapid sensor innovation, advances in computational imaging, and stricter cybersecurity rules that favor integrated hardware-software platforms[1]U.S. Food and Drug Administration, “Cybersecurity in Medical Devices: Quality System Considerations,” fda.gov. High-resolution back-illuminated sCMOS cameras are gaining favor for quantum efficiency, yet procurement teams are balancing those gains against pixel-crosstalk-driven resolution losses documented at green wavelengths near the Nyquist limit[2]Ortkrass H. et al., “High Sensitivity Cameras Can Lower Spatial Resolution,” nature.com. Meanwhile, neural phase microscopy and smart lattice light-sheet techniques have redefined throughput, enabling sub-micron detail at video-rate speeds and reshaping expectations across clinical, industrial, and academic workflows. Regulatory momentum is equally transformative: Section 524B of the FD&C Act now obliges connected microscopes to ship with software bills of materials and coordinated vulnerability disclosure processes, accelerating vendor consolidation as only firms with robust quality systems can comply on schedule. On the demand side, semiconductor fabs moving toward sub-3 nm nodes, the rise of AI-enabled wafer inspection, and hospitals adopting 4K exoscopes for minimally invasive surgery collectively sustain steady equipment refresh cycles[3]Reuters, “Samsung Announces AI Megafactory Partnership with NVIDIA,” reuters.com .

Key Report Takeaways

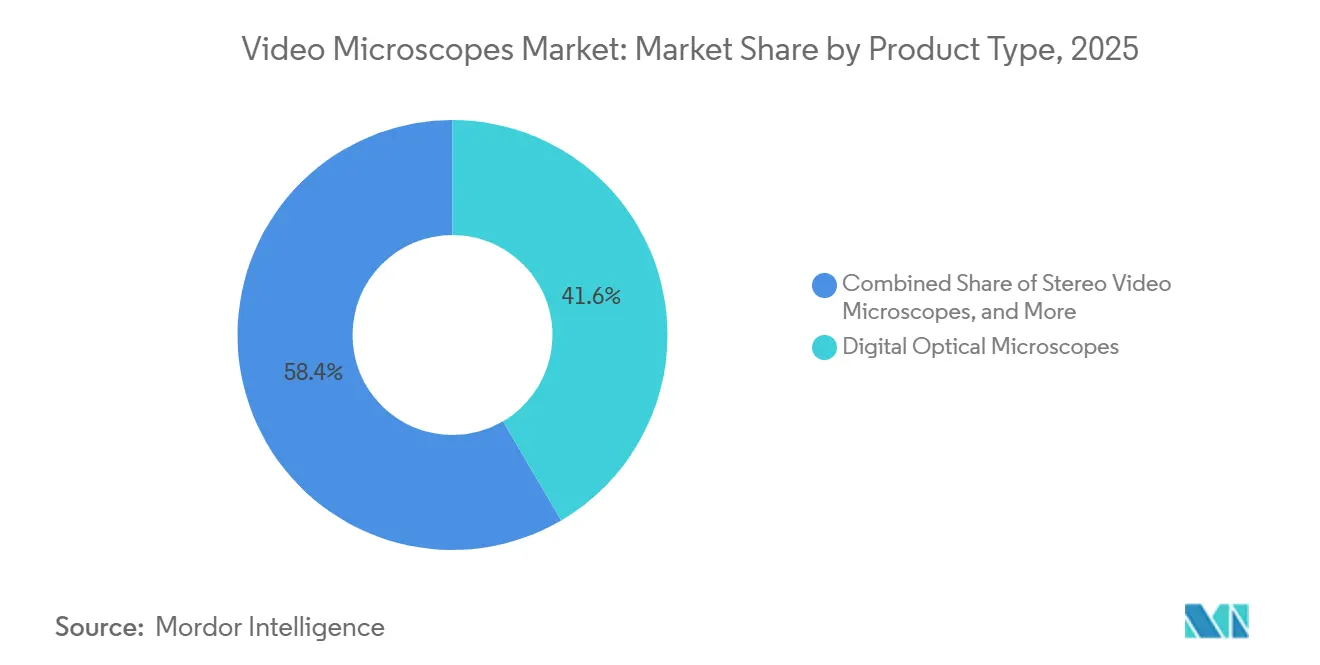

- By product type, Digital Optical Microscopes led with 41.55% revenue share in 2025; Portable/Hand-held systems are advancing at a 10.25% CAGR through 2031.

- By technology, 2D Imaging Systems held 61.23% of the video microscopes market share in 2025, while 3D Imaging Systems are projected to expand at a 7.15% CAGR to 2031.

- By application, Clinical Diagnostics & Pathology accounted for 36.15% of the video microscopes market size in 2025, and Surgical & Minimally-Invasive Procedures are forecast to grow at a 9.51% CAGR through 2031.

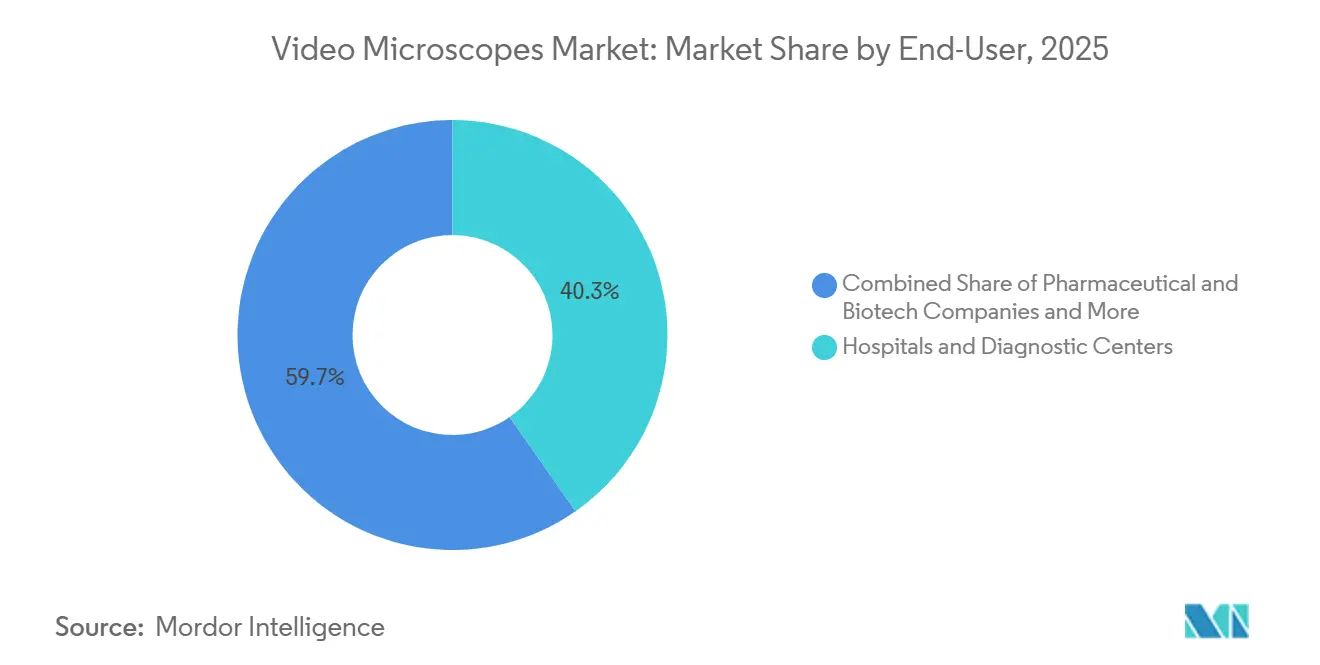

- By end-user, Hospitals & Diagnostic Centers captured 40.35% share in 2025; Electronics/Semiconductor Manufacturers are rising at a 9.11% CAGR to 2031.

- By geography, North America commanded a 35.25% share in 2025, while Asia-Pacific is the fastest-growing region, with an 8.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Video Microscopes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensor-Resolution Leaps & AI-enabled analytics | +1.8% | Global, led by APAC and North America | Medium term (2-4 years) |

| Rising Life-Science R&D Funding | +1.2% | North America & Europe with spillover to APAC hubs | Long term (≥ 4 years) |

| Industrial Quality-Control & Semiconductor Inspection | +1.5% | APAC core (China, South Korea, Taiwan) plus North America | Medium term (2-4 years) |

| Adoption in Minimally Invasive & Robotic Surgery | +0.9% | North America & Europe, pilot programs in APAC hospitals | Short term (≤ 2 years) |

| AR/VR-Assisted Remote Collaboration & Training | +0.6% | Global academic centers and corporate training facilities | Medium term (2-4 years) |

| Portable Microscopes for field Diagnostics | +0.7% | APAC, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sensor-Resolution Leaps & AI-Enabled Analytics

Computational imaging now decouples resolution from objective NA, with neural phase microscopy reaching 840 nm detail at 74 Hz, while smart lattice light-sheet platforms record 112 frames per second. Yet buyers must reconcile these gains with sensor trade-offs: a 28% drop in modulation transfer function has been documented at high spatial frequencies for back-illuminated sCMOS devices. Laboratories, therefore, demand validated pipelines, large-scale storage, and LIS connectivity alongside the hardware.

Rising Life-Science R&D Funding

Public research grants and biopharma pipelines continue to expand allocations for live-cell and fluorescence imaging. EU NextGeneration EU funds financed Italy’s Veneto digital pathology network, which now digitizes up to 3 million slides annually and anchors multicenter AI studies. Japan’s revised Next Generation Medical Infrastructure Act likewise eases data-sharing barriers, encouraging long-cycle investments in advanced microscopes.

Industrial Quality-Control & Semiconductor Inspection

Sub-3 nm nodes magnify defect-detection challenges. Samsung’s USD 310 billion AI Megafactory project with NVIDIA typifies APAC’s capex surge, directly boosting demand for wafer-scale 4K and multispectral inspection rigs. Keyence’s VHX-X1 with a 300 mm stage and ZEISS’s large-field Axioscan iterations epitomize systems optimized for inline scrutiny.

Adoption in Minimally Invasive & Robotic Surgery

Apple Vision Pro deployments in 41 surgical cases yielded a low NASA Task Load Index of 22.3, confirming headset-based visualization as a practical successor to classic towers. Leap-motion-enabled gesture control and 4K exoscopes further improve ergonomics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost & Total Cost of Ownership | -1.3% | Global; acute in smaller hospitals and emerging labs | Short term (≤ 2 years) |

| Shortage of Skilled Operators & Image-Analysis Expertise | -0.8% | Global; most severe in APAC and Sub-Saharan Africa | Long term (≥ 4 years) |

| Regulatory Hurdles for Medical-Grade Systems | -0.5% | North America & Europe, tightening in APAC | Medium term (2-4 years) |

| Cybersecurity & Data-Sovereignty Risks | -0.4% | Europe (GDPR) and China lead stricter regimes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost & TCO

A seven-year model across eight European labs put discounted investment at EUR 5.09 million, with scanners priced around EUR 277,000 and maintenance at EUR 65,000 per year. Storage expenses vary widely: 11.1% of labs add more than 50 TB annually, resulting in negative early cash flow and a 1.3-point decline in short-term growth.

Shortage of Skilled Operators & Image-Analysis Expertise

A 127-lab survey revealed focus errors, slow loading, and microorganism recognition as common pain points; only 29.2% even tracked scan-failure rates. Training lags persist, especially in rural regions with limited broadband, trimming CAGR by 0.8 points over the long term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: 4K Systems Anchor Premium Tier

Digital Optical Microscopes held the dominant 41.55% share in 2025, supported by versatile brightfield and fluorescence modalities. Portable units, however, are set for the fastest 10.25% CAGR as low-resource clinics and space-constrained fabs adopt palm-sized devices. Keyence’s VHX-7000 claims 0.1-6000× magnification with 20× deeper focus, while ZEISS’s Smartzoom 100 delivers 4K at 60 fps for collaborative reviews. NASA’s bench-quality, portable platform proves that sub-micron performance can fit in a carry-on case, a shift likely to redistribute video microscope market share toward mobility-focused vendors by 2031.

Second-tier options include stereo video microscopes for electronics rework and entomology, as well as ultra-HD exoscopes used in surgical theaters where multiple observers need pixel-sharp detail across wide screens. Open-source projects such as Octopi 2.0 show how do-it-yourself ecosystems can undercut premium incumbents without sacrificing AI-supported analytics.

By Technology: 3D Gains on Cytology and Spatial Biology

2D Imaging Systems accounted for 61.23% of 2025 revenue, driven by high-throughput pathology and industrial QC tasks. Yet 3D Imaging Systems are projected to grow at 7.15% CAGR as Z-stacking and volumetric tools enter cytology and spatial biology pipelines. ZEISS’s Axioscan 7 and Lightfield 4D capture up to 80 volumes per second, driving adoption among labs mapping cell-state gradients in tumors. Meanwhile, Keyence’s VK-X3000 offers 0.01 nm vertical resolution for semiconductor surface profiling, blurring boundaries between optical microscopy and metrology.

By Application: Surgical Procedures Outpace Diagnostics Growth

Clinical Diagnostics & Pathology led with 36.15% of 2025 revenue, but Surgical & Minimally-Invasive Procedures are tracked to rise at a 9.51% CAGR. Surgeons cite lower neck strain and cognitive load when 4K exoscopes or VR headsets stand in for stacked monitors. Industrial Inspection & NDT also accelerates as AI-driven visual inspection models screen entire wafers in real time, compressing test cycles and reducing scrap.

By End-User: Semiconductor Fabs Outpace Hospitals

Hospitals & Diagnostic Centers owned a 40.35% share in 2025, yet Electronics/Semiconductor Manufacturers are pacing at a 9.11% CAGR. Samsung’s mega-foundry program alone is expected to pull dozens of wafer-scale microscopes per line, pushing the video microscopes market size for industrial buyers toward parity with healthcare by decade’s end. Academic institutes follow, backed by grant-funded consortia building annotated slide repositories for AI validation.

Geography Analysis

North America retained a 35.25% share in 2025, driven by dense clusters of academic medical centers and semiconductor fabs. FDA 510(k) clearances for Roche, Lumicell, Lumea, PathPresenter, and Proscia in 2024-2025 validate whole-slide workflows and underpin reimbursement eligibility. However, rolling cybersecurity mandates raise compliance costs, nudging some smaller labs toward leasing models.

Europe’s outlook depends on public investment: Veneto’s network digitizes 3 million slides per year under NextGenerationEU, but a seven-year NPV of only EUR 0.21 million underscores slim financial margins absent workflow efficiencies. The European Society of Pathology now recommends DICOM output and at least 80-slide validation sets, making interoperability a purchase prerequisite.

Asia-Pacific is poised for the fastest growth rate at 8.02%. Samsung’s USD 310 billion AI Megafactory project is accelerating equipment demand in South Korea, while Chinese and Taiwanese foundries are driving secondary uptake. India’s laboratory digitalization lags due to broadband gaps and limited accreditation, yet portable platforms like Octopi 2.0 show promise in bridging rural diagnostics. Japan’s legal revisions support data sharing for AI research, although strict privacy amendments temper cross-border collaborations.

Competitive Landscape

Industry concentration is moderate as optics stalwarts absorb niche innovators to own complete computational pipelines. Bruker’s 2024 acquisition spree, which included Phasefocus, Spectral Instruments Imaging, and NanoString assets, added USD 168 million in revenue and broadened its live-cell and fluorescence stack. Tescan’s pending tie-up with Shimadzu and its 2025 purchase of FemtoInnovations mark a foray into femtosecond-laser imaging. ZEISS integrated single-photon avalanche diode arrays through its 2025 Pi Imaging acquisition, positioning it for photon-counting super-resolution.

Competitive vectors now center on delivered AI models, LIS connectors, and cybersecurity documentation rather than pure optics. Twenty-six CE-marked AI algorithms exist for digital pathology, yet fewer than half have peer-reviewed external validation, a gap incumbents with in-house clinical networks aim to close. Portable disruptors like the ISS-qualified NASA unit and Octopi 2.0 continue to challenge price points, though after-sales support and calibration standards remain barriers in low- and middle-income regions.

Video Microscopes Industry Leaders

Carl Zeiss AG

Hamamatsu Photonics

Olympus Corporation

Nikon Corporation

OPTO GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Researchers unveiled a single-snapshot microscope capable of capturing giga-pixel images of non-flat objects, promising faster medical and QC workflows.

- February 2025: SOMETECH introduced the VOMS-202D dental 3D video microscope and an RF electrosurgical hand-piece for endodontics

Global Video Microscopes Market Report Scope

As per the report's scope, video microscopes are advanced optical instruments that integrate a digital camera with a microscope to capture, display, and record magnified images in real time. They allow users to view specimens on external monitors, enabling easier observation, documentation, and sharing compared to traditional eyepiece viewing. Widely used in research, medical diagnostics, and industrial quality control, video microscopes enhance precision and collaboration by combining microscopy with digital imaging technology.

The video microscopes market segmentation includes product type, technology, application, end-user, and geography. By product type, the market is segmented into digital optical microscopes, stereo video microscopes, 4K/ultra-HD video microscopes, and portable/hand-held video microscopes. By technology, the market is segmented into 2D Imaging Systems and 3D Imaging Systems. By application, the market is segmented into clinical diagnostics & pathology, surgical & minimally invasive procedures, research & academia, industrial inspection & NDT, and forensics & law enforcement. By end user, the market is segmented into hospitals & diagnostic centers, pharmaceutical & biotech companies, academic & research institutes, electronics & semiconductor manufacturers, and others (education, CROs, contract QC). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Digital Optical Microscopes |

| Stereo Video Microscopes |

| 4K/Ultra-HD Video Microscopes |

| Portable/Hand-held Video Microscopes |

| 2D Imaging Systems |

| 3D Imaging Systems |

| Clinical Diagnostics & Pathology |

| Surgical & Minimally-Invasive Procedures |

| Research & Academia |

| Industrial Inspection & NDT |

| Forensics & Law-Enforcement |

| Hospitals & Diagnostic Centers |

| Pharmaceutical & Biotech Companies |

| Academic & Research Institutes |

| Electronics / Semiconductor Manufacturers |

| Others (Education, CROs, Contract QC) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Digital Optical Microscopes | |

| Stereo Video Microscopes | ||

| 4K/Ultra-HD Video Microscopes | ||

| Portable/Hand-held Video Microscopes | ||

| By Technology | 2D Imaging Systems | |

| 3D Imaging Systems | ||

| By Application | Clinical Diagnostics & Pathology | |

| Surgical & Minimally-Invasive Procedures | ||

| Research & Academia | ||

| Industrial Inspection & NDT | ||

| Forensics & Law-Enforcement | ||

| By End-User | Hospitals & Diagnostic Centers | |

| Pharmaceutical & Biotech Companies | ||

| Academic & Research Institutes | ||

| Electronics / Semiconductor Manufacturers | ||

| Others (Education, CROs, Contract QC) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the video microscopes market?

The video microscopes market size is USD 3.58 billion in 2026 and is forecast to reach USD 4.65 billion by 2031.

Which product category is growing fastest?

Portable and hand-held video microscopes lead with a 10.25% CAGR through 2031, driven by point-of-care and field diagnostics.

How is Asia-Pacific expected to perform?

Asia-Pacific is the fastest-growing geography with an 8.02% CAGR, propelled by semiconductor fab expansion and rising healthcare investment.

What regulatory change most affects new devices?

Section 524B of the FD&C Act requires connected microscopes to include a software bill of materials and vulnerability-disclosure plans, reshaping vendor qualification.

Which end-user segment shows the highest growth?

Electronics and semiconductor manufacturers are set to expand at a 9.11% CAGR as sub-3 nm process nodes demand wafer-scale inspection.

Page last updated on: