Video Intercom Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 51.79 Billion |

| Market Size (2030) | USD 86.33 Billion |

| Growth Rate (2025 - 2030) | 0.00% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Video Intercom Devices Market Analysis by Mordor Intelligence

The Video Intercom Devices Market size is estimated at USD 51.79 billion in 2025, and is expected to reach USD 86.33 billion by 2030, at a CAGR of 10.76% during the forecast period (2025-2030). A growing preference for IP-enabled door stations that integrate video, audio, analytics, and mobile apps is replacing analog buzzers and accelerating adoption across both new-build and retrofit projects. Convergence with smart-home ecosystems, tighter building-code mandates, and increased visibility of crime are prompting property owners to favor networked systems that enable real-time monitoring, cloud backups, and remote access. Technology suppliers respond with scalable platforms that bundle software subscriptions and AI functions, thereby shifting revenue models toward recurring fees. Meanwhile, cybersecurity certifications, data sovereignty compliance, and 2-wire retrofit kits are emerging as differentiators that lower the total cost of ownership and widen the addressable demand.

Key Report Takeaways

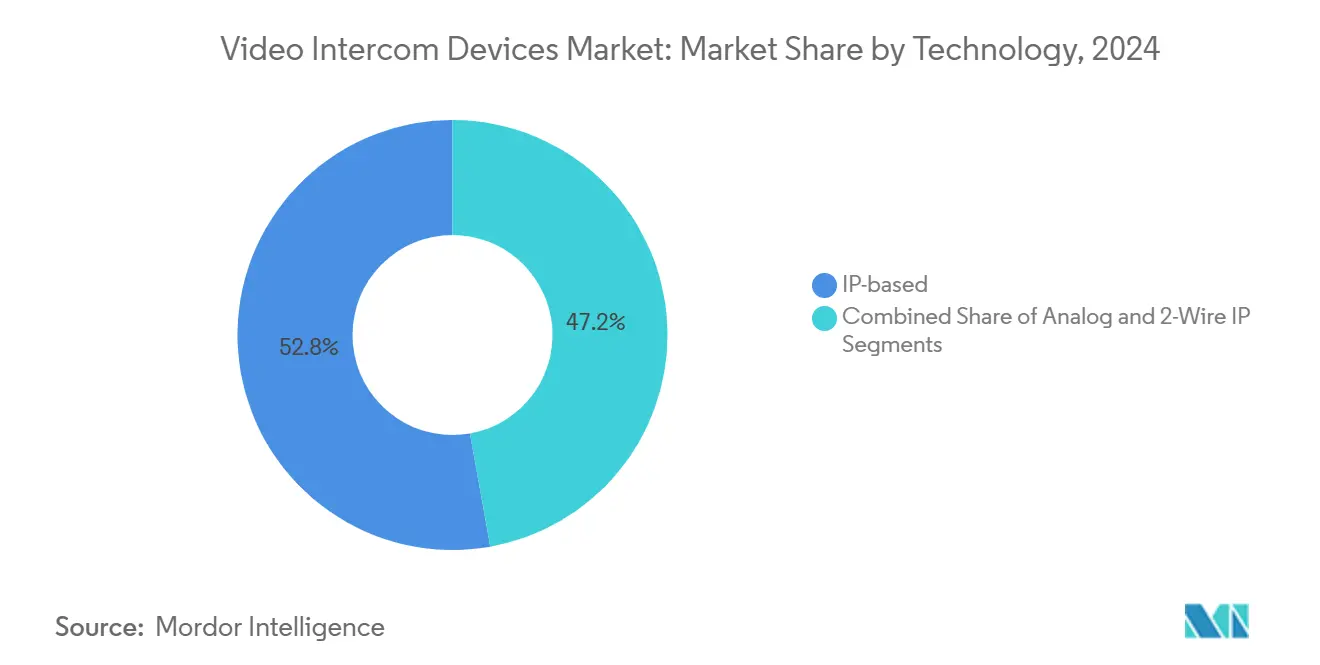

- By technology, IP-based systems led with 52.80% of the video intercom devices market share in 2024; 2-Wire IP solutions are projected to expand at a 14.65% CAGR through 2030.

- By product type, indoor monitors accounted for a 34.70% share of the video intercom devices market size in 2024, and all-in-one kits are projected to advance at a 13.90% CAGR through 2030.

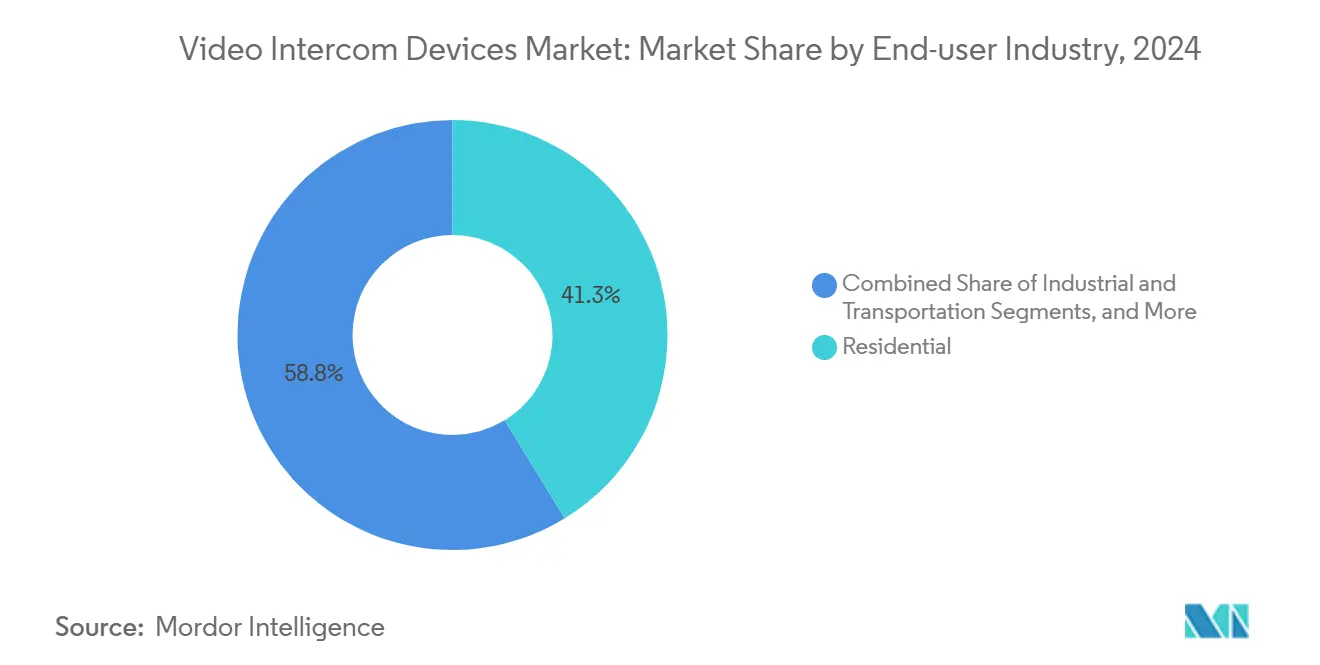

- By end-user, residential applications accounted for 41.25% of the video intercom devices market share in 2024; the healthcare and education segments are forecasted to grow at a 12.70% CAGR through 2030.

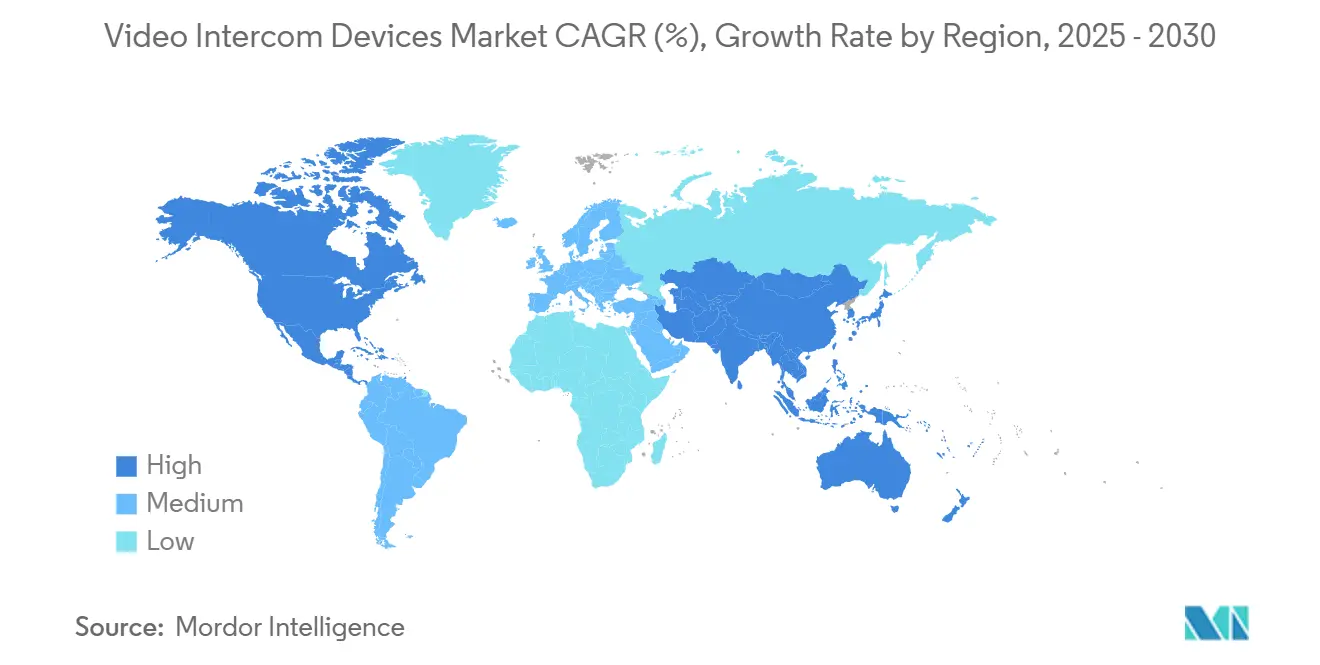

- By geography, North America captured 36.55% revenue share in 2024, while Asia-Pacific is forecast to register a 14.34% CAGR to 2030.

Global Video Intercom Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from Analog to IP-based Systems | +2.8% | North America, Europe | Medium term (2-4 years) |

| Smart-Home and IoT Penetration | +2.1% | North America, Europe, expanding to APAC | Long term (≥4 years) |

| Rapid Urban Crime-rate Escalation | +1.9% | Global urban centers | Short term (≤2 years) |

| Integration with Access-Control Ecosystems | +1.6% | Commercial facilities, global | Medium term (2-4 years) |

| AI-enabled Facial Recognition Mandates | +1.4% | APAC core, spill-over to MEA | Long term (≥4 years) |

| 2-Wire IP Retrofits Slashing Upgrade CAPEX | +1.2% | Legacy buildings worldwide | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Shift from Analog to IP-based Systems

IP migration transforms legacy intercoms into IP-addressable endpoints that deliver HD video, two-way audio, and remote management without proprietary cabling. Hikvision’s IEC 62443-4-1 certification in February 2025 underscores the vendor's commitment to embedding cybersecurity by design, thereby easing enterprise risk assessments.[1]Hikvision, “Hikvision Achieves IEC 62443-4-1 Certification,” hikvision.com Combined with PoE power and browser-based configuration, IP platforms reduce maintenance visits and enable portfolio-wide firmware updates, improving uptime and lowering lifecycle costs. Integration with CCTV, alarms, and building-management software gives facility teams a single security pane of glass. The resulting operational efficiencies and data insights are prompting institutional buyers to standardize on IP across new and retrofit projects.

Smart-Home and IoT Penetration

Smart-home spending is projected to exceed USD 317 billion by 2026, creating a mass-market base for video intercom hubs that link cameras, lights, and voice assistants.[2]SDM Magazine, Mike Rose, “Calculating the Hidden Costs of Video Security,” sdmmag.comResidents now expect parcel management, guest pre-authorization, and smartphone unlock from a single app, repositioning intercoms as lifestyle enablers rather than mere doorbells. The shift allows vendors to upsell cloud recording, AI event summaries, and subscription add-ons. Amazon Ring’s June 2025 launch of AI-generated motion alerts underscores how consumer devices are adopting large language models to distill security footage into concise notifications. As households upgrade routers and fiber connectivity, latency concerns decline, opening room for higher-resolution video streams and richer analytics.

Rapid Urban Crime-rate Escalation

Insurance underwriters, particularly in multifamily housing, now tie premium discounts to electronic access controls that provide evidentiary video and granular audit trails. Deployments equipped with real-time analytics have shown a 70% reduction in incidents after installation, according to large-scale rollouts documented by LVT in 2025.[3]LVT, Kailey Boucher, “Top Six Challenges and Solutions for Scaling Enterprise Surveillance,” lvt.com Public demand for safer common areas raises the stakes for tenant retention, prompting landlords to prioritize visible, camera-equipped entry panels. Municipal safe-city grants and police partnerships further subsidize deployments in high-risk districts, accelerating short-term procurement cycles.

Integration with Access-Control Ecosystems

Enterprise buyers are increasingly requiring intercoms that integrate natively with identity-management suites and VMS dashboards. Aiphone’s 2024 integration with Genetec Security Center demonstrated how one SDK alignment can unlock visitor management, time-and-attendance, and emergency lockdown capabilities from a single screen.[4]Aiphone, “Aiphone Integrates with Genetec Security Center,” aiphone.comThis ecosystem approach eliminates data silos, speeds incident response, and allows badge provisioning workflows to extend automatically to intercom call stations. The result is a compelling ROI narrative that links occupant experience, compliance reporting, and space-utilization analytics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-hacking and Privacy Breaches | -1.8% | EU, North America | Short term (≤2 years) |

| High Up-front Hardware and Install Costs | -1.5% | Global, emerging markets sensitive | Medium term (2-4 years) |

| Unreliable Last-Metre Connectivity in MDUs | -0.9% | Dense urban areas | Short term (≤2 years) |

| Rising Compliance Cost for Video-Data Sovereignty | -0.7% | EU core, privacy-regulated markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Cyber-hacking and Privacy Breaches

Average global breach costs reached USD 4.88 million in 2024, with US incidents averaging USD 9.36 million, prompting property owners to scrutinize the hardening of IoT devices. Exposure of default passwords and weak encryption in commodity doorbells has spurred demand for end-to-end TLS, secure boot, and signed firmware updates. ADT’s 2024 disclosure of 30,800 compromised customer records highlights the reputational fallout, prompting integrators to adopt zero-trust architectures and implement continuous penetration testing. Vendors that publish third-party audit reports and support on-premise storage options gain a procurement edge in highly regulated verticals.

High Up-front Hardware and Install Costs

Comprehensive commercial deployments cost USD 2,500-USD 3,000 per door, and a 16-camera bundle can add USD 8,000-USD 30,000, often exceeding annual security allocations for small portfolios. Beyond hardware, ongoing VMS licenses, cloud retention, and maintenance contracts can significantly increase the total cost of ownership over the system's life. Retrofit projects often require network switches, PoE injectors, and fiber backhaul, which can inflate capital budgets. Vendors counter by promoting 2-wire kits and device-as-a-service leases that spread payments over multi-year terms, yet sticker shock still delays some tenders, especially in price-sensitive emerging markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: IP Consolidation Deepens Platform Value

IP-based solutions accounted for 52.80% of the video intercom devices market share in 2024, underscoring buyer emphasis on high-definition video, mobile unlock, and cloud management. The IP leadership is reinforced by enterprise demand for open APIs that feed building-management dashboards and AI engines. Meanwhile, 2-wire IP retrofits are expected to post a 14.65% CAGR, enabling legacy buildings to adopt IP capabilities without requiring new cabling, thereby increasing video intercom device market penetration among cost-conscious landlords. Analog deployments persist only where connectivity is limited or budgets are highly constrained, and their share continues to erode as IP hardware prices approach parity.

Momentum around software-defined functionality is redefining the value chain of the video intercom devices industry. Verkada’s 2025 road map points to natural-language interfaces and vision-model analytics that push intercoms beyond access control into asset tracking and anomaly detection. Predictive maintenance features notify operators of lens obstructions or failing power supplies, reducing truck rolls and raising system uptime. As AI workloads shift to edge chipsets, bandwidth demand plateaus, enabling multi-door complexes to add cameras without expanding backbone capacity.

By Product Type: All-in-One Kits Democratize Adoption

Indoor monitors remained the top product, accounting for a 34.70% share of the video intercom devices market size in 2024, serving as the user-experience anchor that drives satisfaction scores. However, packaged all-in-one kits are forecast to post a 13.90% CAGR through 2030 by bundling door stations, monitors, and access-control relays in a single SKU. The simplified procurement eliminates the need for separate BOM approvals and accelerates installation schedules from days to hours. For small condo associations and single-family builders, kit pricing unlocks features such as cloud calls and mobile unlock, which were previously reserved for premium multi-tenant solutions.

Accessory sales and software licenses increase the average revenue per unit over time. ButterflyMX’s partnership with iApartments demonstrates how integrating video intercoms with property-management software can automate lease renewals, self-guided tours, and delivery lockers, thereby extending the product's relevance beyond security. Over-the-air firmware upgrades add new AI analytics or mobile widgets, preserving hardware usefulness for a decade or more and underlining why recurring revenue now drives investor interest.

By End-user Industry: Healthcare Outpaces Overall Growth

Residential deployments accounted for 41.25% of the video intercom devices market size in 2024, as smart-home adoption makes video entry a baseline amenity. In contrast, the healthcare and education segments are expected to grow at a 12.70% CAGR, driven by contactless visitor policies, HIPAA privacy requirements, and active-shooter preparedness drills. Hospitals require staff-badge authentication, patient-room video check-ins, and lockdown triggers that integrate with nurse-call and PA systems, moving intercoms into mission-critical workflows.

Commercial offices, government facilities, and transportation hubs also invest in hardened units with vandal-resistant casings and encrypted storage for evidentiary compliance. Industrial operators favor edge analytics that detect PPE compliance at gatehouses, turning intercoms into safety enforcers. This diversification enables suppliers to tailor SKUs with sector-specific firmware, allowing for premium pricing in regulated niches and broadening the addressable revenue streams of the video intercom devices market.

Geography Analysis

North America held a 36.55% revenue share in 2024, supported by building codes that encourage electronic access controls, high disposable incomes, and familiarity with the cloud SaaS ecosystem. The US deployments frequently bundle intercoms with smart lock and parcel locker integrations, turning lobbies into unattended concierges. Canada’s multifamily boom and Mexico’s urban-revitalization projects further expand regional demand.

The Asia-Pacific region is expected to record the fastest growth, with a 14.34% CAGR through 2030, as smart-city initiatives incorporate video intercoms into mixed-use towers and government complexes. China’s mass housing projects specify networked door stations as standard fit-outs, while Japan and South Korea pioneer AI facial recognition mandates at residential blocks. India’s tier-1 cities, grappling with densely populated high-rise clusters, adopt 2-wire retrofits that enhance IP performance without requiring rewiring, thereby broadening the consumer base.

Europe shows steady uptake driven by GDPR clarity that eases data-handling concerns for property managers. Germany, the United Kingdom, and France retrofit energy-efficient facades with combined security and building-automation nodes. Eastern Europe benefits from EU structural funds earmarked for infrastructure modernization, while upcoming AI legislation in Brazil and similar Latin American markets suggests future convergence toward EU-style compliance regimes.

Competitive Landscape

The market remains moderately fragmented, with hardware giants, specialist access-control vendors, and cloud-native disruptors vying for share. Hikvision and Samsung utilize scale to anchor pricing at the entry level, while achieving cybersecurity certifications such as IEC 62443-4-1, which reassure enterprise buyers.

Aiphone integrates with Genetec VMS to embed intercom feeds directly into established control rooms, thereby reducing the need for rip-and-replace barriers on corporate campuses. ButterflyMX, backed by FTV Capital in January 2025, concentrates on mobile-first user experiences and property-management APIs, targeting multifamily portfolios seeking operational efficiency.

Strategic alliances dominate recent activity. Door-hardware manufacturers partner with cloud platforms to co-market credential management and smart-lock bundles. Vendors expand SDK libraries, enabling third parties to add occupancy analytics or HVAC triggers. Price competition persists at the low end, but differentiation is increasingly shifting to software roadmaps, cybersecurity posture, and compliance toolkits. As service revenues outpace hardware margins, suppliers prioritize customer success teams and AI-powered health monitoring to minimize churn.

Video Intercom Devices Industry Leaders

Hangzhou Hikvision Digital Technology Co., Ltd.

Samsung Electronics Co., Ltd.

Comelit Group SpA

Siedle and Söhne OHG

Legrand SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Amazon Ring launched AI-generated security alerts for premium subscribers in the United States and Canada, signaling mainstream adoption of LLM summaries in home security.

- February 2025: Hikvision has attained IEC 62443-4-1 cybersecurity certification, extending secure development practices across its intercom portfolio.

- January 2025: ButterflyMX secured growth equity investment from FTV Capital to accelerate product development and expand smart-access solutions.

- September 2024: iApartments has completed full integration with ButterflyMX 8-inch and 12-inch panels to streamline multifamily access control and property management workflows.

Global Video Intercom Devices Market Report Scope

Video intercom devices use video methods and are stand-alone intercom systems used to manage calls made at the entrance to a building with access control. The diversity of video intercom devices and equipment applications has added security and comfort in commercial, residential, and industrial applications. The study tracks the revenue generated by vendors through device offerings among end users.

The Video Intercom Devices Market Report is segmented by technology (analog, ip-based, 2-wire ip), product type (door stations, indoor monitors, all-in-one video intercom kits, accessories, and software licenses), end-user industry (residential, commercial, government and public infrastructure, industrial and transportation, healthcare and education), and geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The market forecasts are provided in terms of value (USD).

| Analog |

| IP-based |

| 2-Wire IP |

| Door Stations |

| Indoor Monitors |

| All-in-One Video Intercom Kits |

| Accessories and Software Licenses |

| Residential |

| Commercial |

| Government and Public Infrastructure |

| Industrial and Transportation |

| Healthcare and Education |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| Rest of Asia Pacific | |

| Middle East | GCC |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Rest of Africa |

| By Technology | Analog | |

| IP-based | ||

| 2-Wire IP | ||

| By Product Type | Door Stations | |

| Indoor Monitors | ||

| All-in-One Video Intercom Kits | ||

| Accessories and Software Licenses | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Government and Public Infrastructure | ||

| Industrial and Transportation | ||

| Healthcare and Education | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia Pacific | ||

| Middle East | GCC | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected revenue for the video intercom devices market by 2030?

It is forecast to reach USD 86.33 billion, growing at a 10.76% CAGR between 2025 and 2030.

Which technology segment leads current adoption?

IP-based systems hold 52.80% share, driven by demand for HD video, analytics and remote management.

Why are 2-wire IP retrofits gaining traction?

They deliver IP functionality over existing cabling, reducing upgrade costs and enabling a 14.65% CAGR through 2030.

Which end-user vertical is expanding the fastest?

Healthcare and education facilities are expected to grow at 12.70% CAGR due to stringent compliance and contactless access needs.

How significant is North America’s role in market revenue?

North America accounts for 36.55% of global revenue, underpinned by smart-home penetration and supportive building codes.

What is the primary restraint inhibiting faster deployment?

Cyber-hacking concerns, with breach costs averaging USD 4.88 million globally, compel buyers to demand robust security certifications.

Page last updated on: