Vibe Coding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

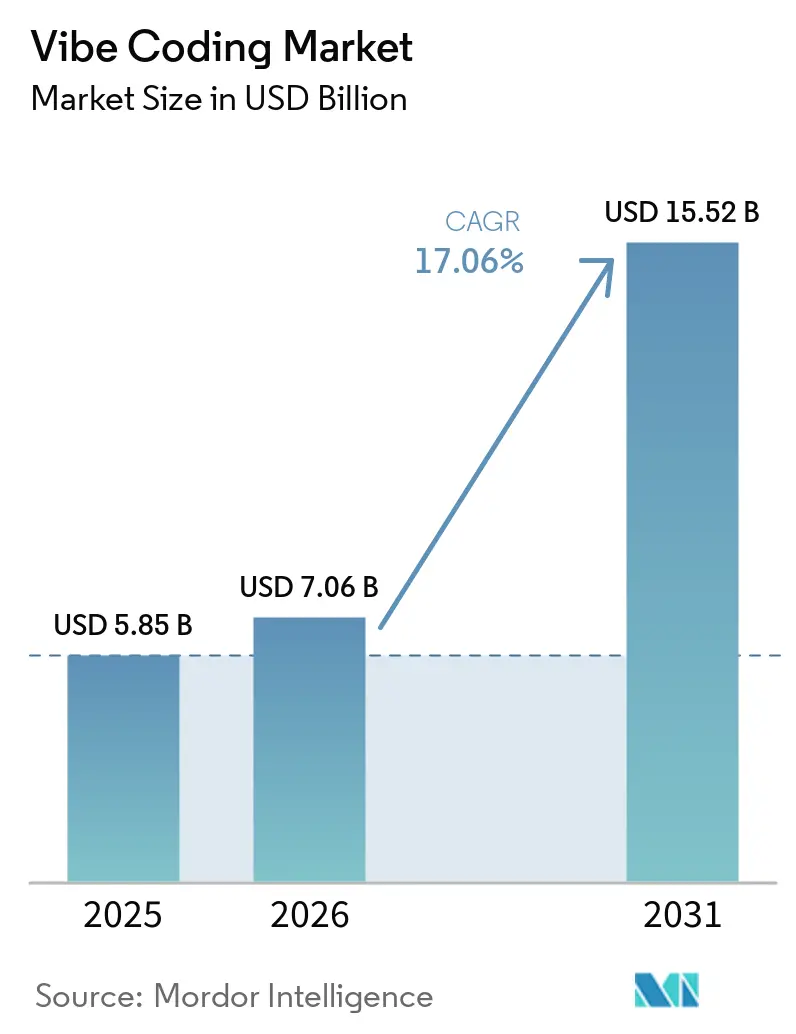

| Market Size (2026) | USD 7.06 Billion |

| Market Size (2031) | USD 15.52 Billion |

| Growth Rate (2026 - 2031) | 17.06% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vibe Coding Market Analysis by Mordor Intelligence

The vibe coding market size is projected to expand from USD 5.85 billion in 2025 and USD 7.06 billion in 2026 to USD 15.52 billion by 2031, registering a 17.06% CAGR between 2026 and 2031. Haptic adoption is accelerating as 6G testbeds prove sub-10-millisecond round-trip latency, automotive programs move to software-defined cockpits, and accessibility mandates embed tactile cues across consumer devices. Edge-AI co-processors now synchronize vibration patterns with sensor fusion in under 1 millisecond, closing the performance gap with high-frame-rate graphics. Platform vendors bundle reference designs with cloud authoring tools, signaling a strategic shift from component sales to vibe coding platform ecosystems. Meanwhile, proprietary haptic protocols and diverse actuator physics continue to fragment the supply base, elevating the role of middleware that translates design intent into device-specific waveforms.

Key Report Takeaways

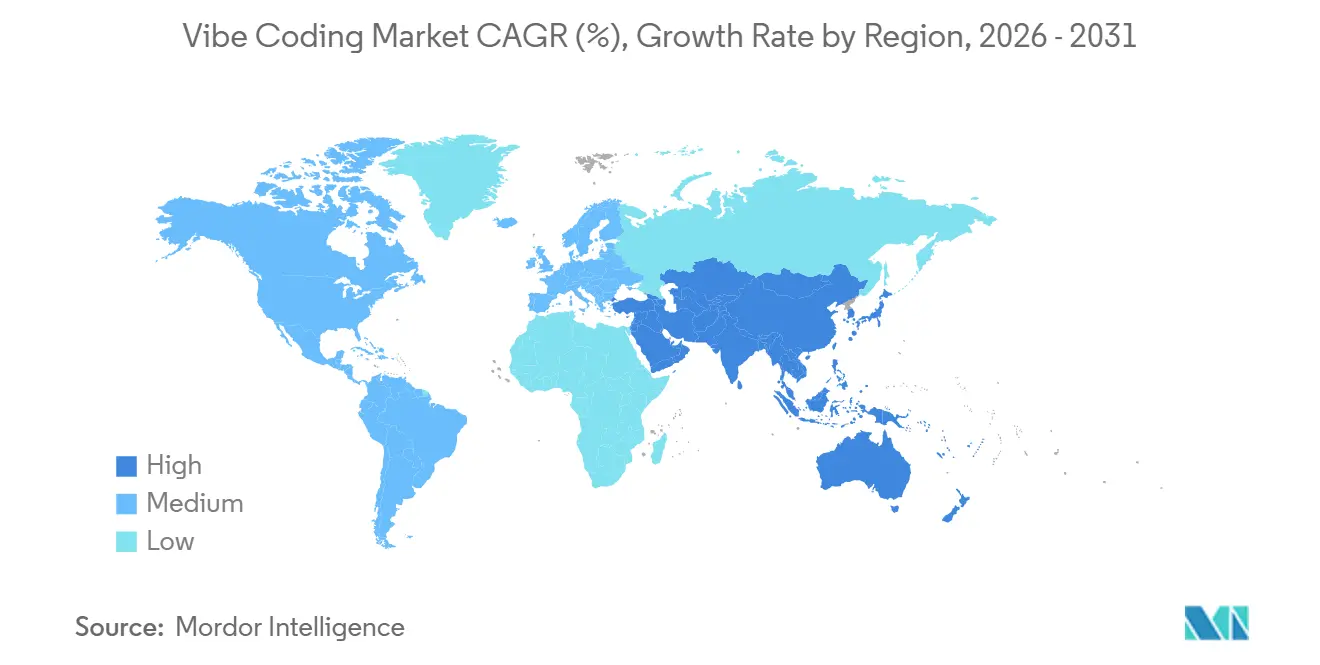

- By geography, Asia-Pacific led with 31.82% of the vibe coding market share in 2025, while the Middle East is forecast to grow at a 17.92% CAGR through 2031.

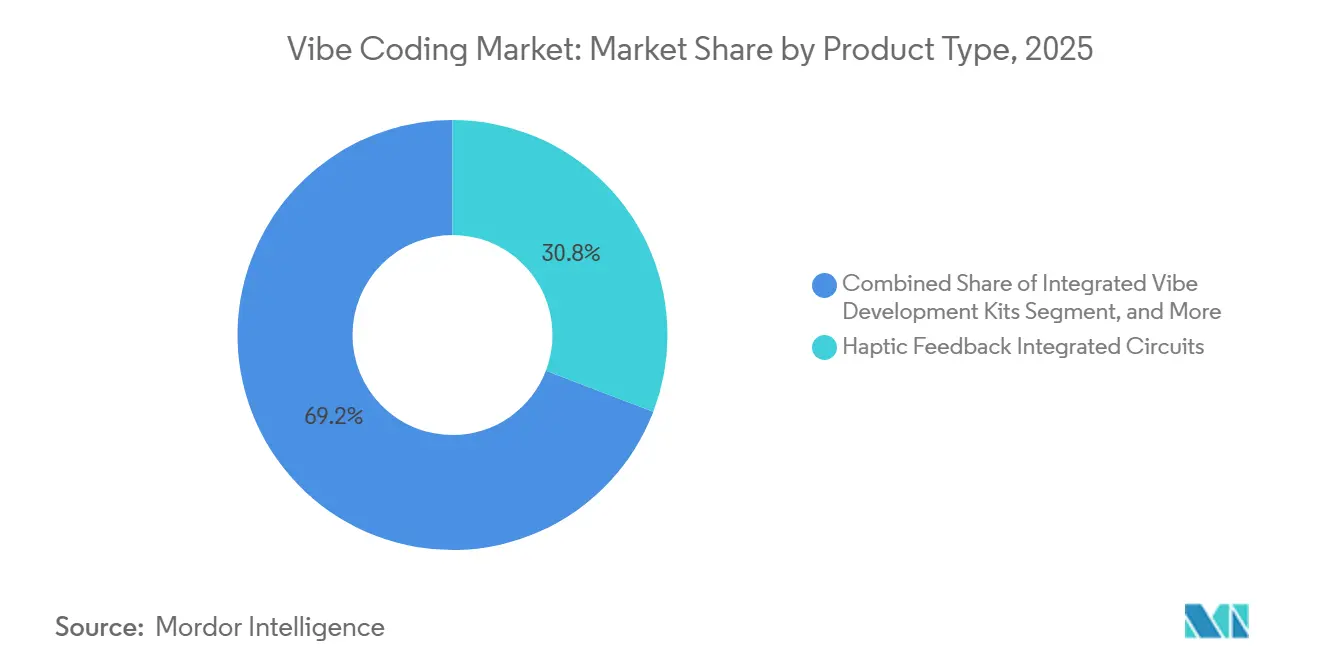

- By product type, haptic feedback integrated circuits accounted for 30.82% of 2025 revenue, whereas integrated vibe development kits are poised to grow at an 18.3% CAGR through 2031.

- By programming paradigm, object-oriented coding accounted for 33.72% of 2025 revenue, but reactive models are projected to grow at a 17.73% CAGR over the same horizon.

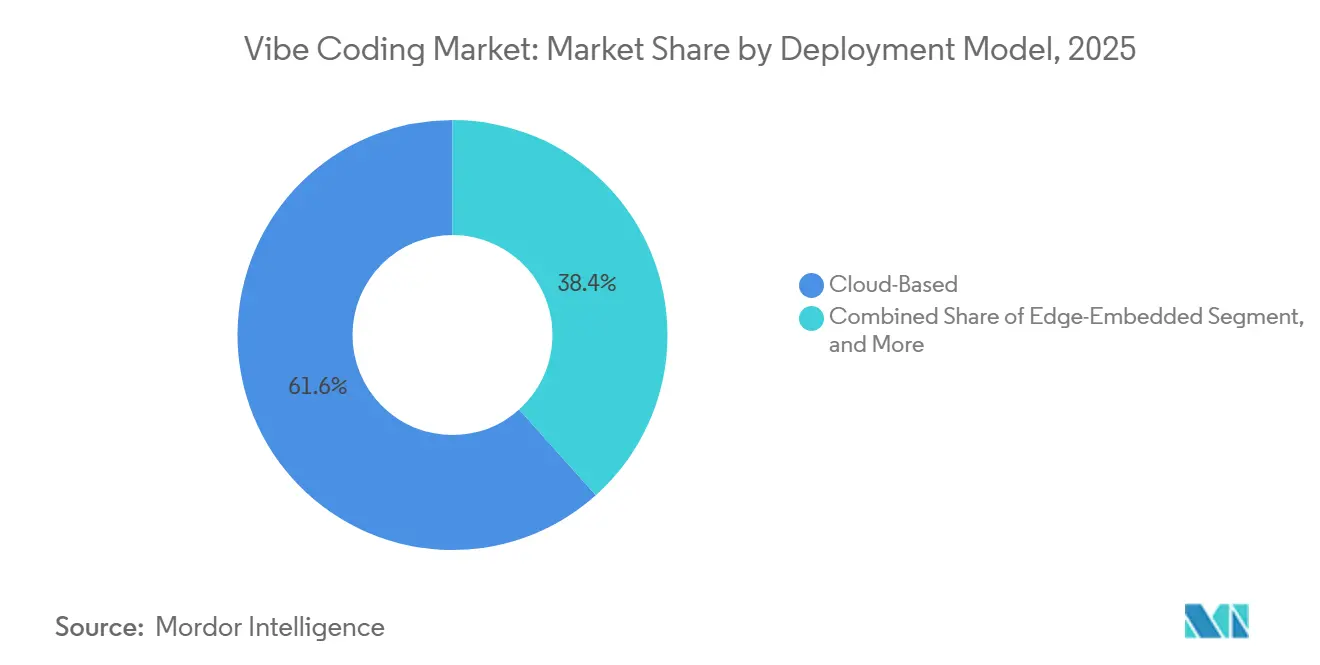

- By deployment model, cloud-based workflows accounted for 61.62% of revenue share in 2025, yet edge-embedded architectures are expected to grow at a 19.15% CAGR through 2031.

- By end user, consumer electronics accounted for 28.93% of revenue in 2025, whereas gaming and AR/VR applications are set to expand at a 18.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vibe Coding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Adoption of Tactile Internet in 6G Testbeds | +3.80% | China, South Korea, Germany | Medium term (2-4 years) |

| Expanding Use of Advanced Haptics in AR and VR Headsets | +4.20% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Automotive Shift to Software-Defined Cockpits | +3.50% | Europe, North America, China | Medium term (2-4 years) |

| Regulatory Push for Accessibility Features in Consumer Devices | +2.10% | North America, Europe | Short term (≤ 2 years) |

| Open-Source Frameworks Lowering Entry Barriers for Developers | +2.90% | Global | Medium term (2-4 years) |

| Edge-AI Optimisation Enabling Ultra-Low-Latency Vibe Coding | +3.30% | Asia-Pacific, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Adoption of Tactile Internet in 6G Testbeds

National consortia in China, South Korea, and Germany are embedding haptic channels into early 6G prototypes, aiming to achieve end-to-end latencies below 1 millisecond to enable remote surgery and industrial teleoperation. IEEE 1918.1.1-2024 codifies tactile codecs that reduce kinesthetic data by up to 90%, enabling coexistence with ultra-high-definition video over constrained wireless links. Germany’s Center for Tactile Internet with Human-in-the-Loop secured long-term funding that supports passivity algorithms resilient to network jitter. South Korea’s Electronics and Telecommunications Research Institute validated force-feedback transfer at 10 kHz over 28 GHz millimeter-wave channels in December 2025, confirming commercial feasibility. These proofs of concept are translating laboratory advances into pilot deployments that will inform volume rollouts after 2027.[1]Deutsches Zentrum für Luft- und Raumfahrt, “Centre for Tactile Internet Phase II Funding,” DLR.de

Expanding Use of Advanced Haptics in AR and VR Headsets

Meta Quest 3 integrates dual linear resonant actuators that synchronize vibrations to virtual interactions, moving precision tactile cues into the mid-price headset tier. Sony PlayStation VR2 extends immersion with adaptive triggers that modulate resistance for firearm recoil and bow tension. Apple Vision Pro embeds a head-mounted Taptic Engine that converts spatial audio cues into localized vibration, supporting users with hearing impairments. Razer’s Dynamic Haptics, launched in March 2026, converts game soundtracks into real-time vibration patterns, eliminating the need for manual authoring. Collectively, these platform moves transform haptics from a premium add-on to an expected baseline, compelling smaller vendors to license turnkey vibe coding stacks.[2]Meta Platforms, “Meta Quest 3 Product Specifications,” Meta.com

Automotive Shift to Software-Defined Cockpits

BMW Panoramic iDrive replaces most physical buttons with a curved OLED display, overlaid with a piezoelectric haptic layer that delivers localized clicks, allowing drivers to confirm inputs without taking their eyes off the road. Mercedes-Benz MBUX Hyperscreen employs 12 independent actuators across a 56-inch glass surface to differentiate climate, navigation, and media controls. Boréas Technologies supplies AEC-Q100 Grade 2 drivers for NIO’s ET9 sedan, enabling reliable solid-state haptic buttons. Cirrus Logic’s CS40L5x family entered mass production in December 2025 and integrates sensor-less velocity control to adapt feedback to cabin noise. These developments confirm that software-defined cockpits are a reality in production and are reshaping automotive bills of materials.[3]BMW Group, “BMW Panoramic iDrive Technical Documentation,” BMW.com

Regulatory Push for Accessibility Features in Consumer Devices

WCAG 3.0 Working Draft introduces tiered conformance that requires tactile cues for critical actions such as form submission. The European Accessibility Act, which took effect in June 2025, mandates vibration support even in budget smartphones. The United States Department of Justice clarified in January 2025 that Title III of the ADA covers digital interfaces on consumer electronics, increasing litigation risk for non-compliant brands. Japan’s draft mobile alert rule adds haptic confirmation for emergency broadcasts. Mandatory compliance is accelerating penetration in markets where voluntary adoption lagged.[4]World Wide Web Consortium, “WCAG 3.0 Working Draft,” W3.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmentation of Proprietary Haptic Protocols | -2.70% | Global | Medium term (2-4 years) |

| Limited Standardisation Across Hardware Layer | -2.30% | Global, Asia-Pacific | Medium term (2-4 years) |

| High Upfront Costs of Precision Actuators | -1.90% | South America, Africa | Short term (≤ 2 years) |

| Risk of Sensory Overload and User Fatigue | -1.40% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmentation of Proprietary Haptic Protocols

Most handset and operating-system vendors still deploy incompatible APIs, including Core Haptics on iOS, Immersion TouchSense SDK on Android, and Windows Haptic Interface, requiring separate codebases that inflate engineering budgets. Automotive Tier-1 suppliers such as Bosch and Continental specify unique actuator interfaces, blocking dual sourcing and driving component premiums. The lack of a universal codec forces manual re-tuning when shifting between linear resonant and piezo actuators, consuming up to 40% of design budgets. This protocol balkanization discourages small developers and concentrates innovation within large incumbents.

Limited Standardisation Across Hardware Layer

Actuator heterogeneity in response time, force output, and energy consumption constrains consistent haptic performance across devices. TDK Corporation Mini PowerHap achieves sub-1 ms response at ~0.6 mJ per click, while legacy eccentric rotating mass motors can require up to 20 ms and ~100 mW, creating large latency and efficiency gaps. Middleware providers must implement device-specific compensation algorithms, resulting in perceptual inconsistencies when users transition between devices. Alps Alpine Co., Ltd. offers 14 Haptic Reactor variants spanning 4.9-15 G without standardized performance baselines. Although ISO/IEC 23090-31 improves codec-level interoperability, it does not define actuator classes or minimum thresholds. In the absence of industry-wide benchmarks or regulatory standards, performance fragmentation is expected to persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Integrated Kits Outpace Standalone Components

Haptic Feedback Integrated Circuits accounted for 30.82% of 2025 revenue, establishing the core hardware layer of the vibe coding market across smartphones and automotive systems. These ICs integrate digital playback engines, boost converters, and closed-loop control into a single die, reducing board footprint and standby power consumption. The integration improves system efficiency while simplifying design complexity for OEMs operating under tight space and energy constraints. This positions ICs as the primary value-capture point, particularly in high-volume applications where performance consistency and cost optimization directly influence product competitiveness and scalability.

Integrated Vibe Development Kits are expanding at an 18.30% CAGR through 2031, driven by demand for turnkey prototyping solutions that combine actuators, drivers, and reference firmware. These kits accelerate design cycles by enabling rapid tactile prototyping, allowing industrial design teams to validate user experiences within weeks rather than months. They also reduce entry barriers by exposing I2C interfaces and force-tuning parameters via intuitive GUIs, minimizing the need for deep firmware expertise. This broadens the customer base and creates a pull-through effect, where early-stage prototyping adoption directly translates into downstream IC demand and ecosystem lock-in.

By Programming Paradigm: Reactive Models Gain Traction

Object-Oriented Vibe Coding led 2025 revenue at 33.72%, reflecting its structural advantage in cross-platform development environments such as Android and Unity. By encapsulating haptic effects, calibration tables, and playback logic into reusable classes, teams achieve modularity, cleaner version control, and faster iteration cycles. This approach reduces integration friction across applications, particularly in ecosystems where tactile feedback consistency is critical. Its dominance is therefore rooted in maintainability and portability, aligning with enterprise-scale development workflows and multi-platform deployment requirements.

Reactive Vibe Coding, growing at 17.73% CAGR through 2031, introduces an event-driven paradigm where haptic responses are triggered by real-time sensor inputs rather than continuous polling. This reduces CPU overhead while enabling sub-100 microsecond response times, critical for latency-sensitive applications. Emerging hybrid models combine object-oriented containers with reactive bindings, allowing stored tactile assets to be dynamically deployed based on live force or proximity data. This convergence improves both system responsiveness and code maintainability, positioning reactive architectures to gradually displace procedural frameworks, particularly in wearables, gaming controllers, and other interaction-intensive devices.

By Deployment Model: Edge Inference Closes Latency Gaps

Cloud-based solutions accounted for 61.62% of 2025 revenue, driven by OEMs' preference for centralized waveform management and OTA distribution. Vendors stream licensed haptic libraries and update profiles without firmware refresh cycles, reducing deployment friction and enabling continuous optimization. Integration with platforms such as Android supports large-scale A/B testing, where telemetry links tactile patterns to user engagement metrics. This creates a measurable feedback loop for UX tuning. However, 20-50 ms network latency introduces synchronization drift across touch, audio, and visual layers in high-speed use cases such as gaming, limiting performance reliability under real-time constraints.

Edge-embedded models, expanding at 19.15% CAGR through 2031, address these latency and privacy constraints by shifting inference closer to the device. Modern edge drivers incorporate neural processing capabilities to interpret grip force, motion, and contextual signals locally, eliminating the need for cloud round-trips. This improves determinism and protects sensitive user data. On-premise deployments remain relevant in surgical simulation and hazardous-environment teleoperation, where strict latency bounds and data sovereignty are non-negotiable, though high capex limits adoption. The market is therefore converging toward hybrid architectures that balance cloud scalability with edge responsiveness and resilience.

By End User Industry: Gaming Outpaces Consumer Electronics

Consumer Electronics accounted for 28.93% of 2025 spending, driven by the standardized adoption of X-axis LRAs in smartphones and tablets. Platforms such as Android have normalized richer notification feedback, making haptics a baseline UX layer rather than a differentiator. Scale economics, mature supply chains, and consistent integration frameworks sustain this segment’s lead. However, growth is plateauing as feature parity across OEMs increases, limiting incremental monetization. The segment remains volume-driven, with value tied to efficiency gains in actuator performance, power consumption, and firmware optimization rather than new use-case expansion.

Gaming and AR/VR are projected to grow at 18.92% CAGR through 2031, supported by demand for multidimensional haptics in immersive environments. Systems such as the PlayStation 5 DualSense controller demonstrate how advanced feedback enhances realism through recoil simulation and environmental texture mapping. Parallel expansion is visible in healthcare simulators, automotive seating systems, and industrial robotics, where force feedback improves training precision, safety signaling, and remote operation control. These applications diversify demand beyond mobile, shifting the market toward high-value, performance-critical deployments where latency, fidelity, and contextual responsiveness directly impact user outcomes.

Geography Analysis

Asia-Pacific generated 31.82% of 2025 revenue and is projected to grow at 17.06% CAGR through 2031, supported by integrated supply chains across China, Japan, and South Korea. Regional manufacturers shipped over 1.5 billion vibration motors by 2025, creating cost advantages and reducing lead times for handset OEMs. Local fabs commercialized miniature piezo strips delivering up to 5 g peak acceleration within thin device architectures, strengthening export competitiveness. Electric-vehicle OEMs are embedding software-defined cockpits with piezo haptic bars, reinforcing domestic driver IC ecosystems and vertically integrated innovation capacity.

North America and Europe together accounted for approximately 40% of 2025 revenue, driven by premium automotive demand and a strong console gaming ecosystem. Automotive Tier 1 suppliers integrated closed-loop haptic drivers into steering systems and infotainment stacks to comply with safety and driver-distraction regulations. Meanwhile, IP licensors based in the United States renewed global royalty agreements, sustaining predictable cash flows. Fabless semiconductor entrants gained traction in laptops and solid-state button modules, leveraging design innovation to capture incremental share in higher-margin applications across computing and interface technologies.

The Middle East is projected to expand at 17.92% CAGR through 2031, led by investments in Saudi Arabia and United Arab Emirates targeting smart-city infrastructure and service robotics. Public funding models often subsidize up to 85% of project costs, contingent on local workforce development. In contrast, South America, Africa, and smaller Asian markets remain price-sensitive, favoring sub-USD 1.00 LRAs until piezo costs decline further. However, global cost curves are trending downward, enabling broader adoption of high-definition haptics and expanding the long-term addressable market.

Competitive Landscape

The vibe coding market exhibits moderate fragmentation, with value distributed across IP licensors, component manufacturers, and fabless semiconductor entrants. A limited number of licensors monetize extensive patent portfolios, capturing recurring royalty streams despite hardware-centric deployment. For instance, Immersion Corporation reported USD 1.56 billion in fiscal 2025 revenue, including USD 74.1 million from haptic royalties. This highlights the disproportionate value of software and algorithmic IP in shaping tactile experiences, even as hardware remains the primary integration layer across consumer and automotive systems.

Component vendors are increasingly moving up the stack, integrating actuators with firmware and AI-driven signal processing. Companies such as AAC Technologies have surpassed 1 billion cumulative shipments of X-axis motors by April 2026 and are collaborating with OEMs to co-develop advanced vibration ecosystems. These solutions bundle hardware with audio-to-haptic conversion algorithms, enabling differentiated user experiences. Simultaneously, fabless players are targeting efficiency gains, offering piezo drivers with up to 10x lower power consumption and 4x smaller PCB footprints, securing design wins in premium automotive and solid-state interface modules.

White-space opportunities center on standardized haptic libraries and development ecosystems that reduce integration complexity. Open-source frameworks are enabling actuator control via commodity audio amplifiers, while proprietary SDKs provide multiuser force-feedback APIs for VR and simulation use cases. Competitive differentiation is increasingly defined by closed-loop control algorithms that ensure output consistency, integrated force sensing for contextual responsiveness, and on-device AI that personalizes feedback intensity. These capabilities are likely to drive consolidation, as vendors with full-stack integration across hardware, software, and AI establish sustainable competitive advantages.

Vibe Coding Industry Leaders

Immersion Corporation

Synaptics Incorporated

TDK Corporation

Alps Alpine Co., Ltd.

Cirrus Logic Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Boréas Technologies integrated an AEC-Q100 Grade 2 piezo module into the NIO ET9 touch bar, delivering context-sensitive feedback with force sensing.

- December 2025: Cirrus Logic introduced automotive-grade CS40L5x haptic drivers with sensor-less velocity control and active vibration compensation, with mass production slated for late 2025.

- December 2025: Cirrus Logic introduced automotive-grade CS40L5x haptic drivers with sensor-less velocity control and active vibration compensation, with mass production slated for late 2025.

- January 2026: Teslasuit unveiled the XR5 full-body interface combining haptics, motion capture, and biometrics, priced at USD 7,500 for early orders and supporting Unity 6.0 and Unreal Engine 5.1.

Global Vibe Coding Market Report Scope

The Vibe Coding Market refers to the ecosystem of technologies, tools, and platforms that enable the creation, optimization, and deployment of programmable haptic feedback across digital systems. It encompasses both software layers, such as coding frameworks, signal encoding libraries, and development environments, and hardware-enabling components, including drivers, actuators, and integrated circuits that translate code into tactile experiences.

The Vibe Coding Market Report is Segmented by Product Type (Vibe Pattern Encoders, Resonance Signal Transducers, Haptic Feedback Integrated Circuits, and Integrated Vibe Development Kits), Programming Paradigm (Procedural, Object-Oriented, Functional, Reactive, and Hybrid), Deployment Model (On-Premise, Cloud-Based, and Edge-Embedded), End User Industry (Consumer Electronics, Automotive, Industrial Automation, Healthcare, Gaming and AR/VR, and Other End User Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Vibe Pattern Encoders |

| Resonance Signal Transducers |

| Haptic Feedback Integrated Circuits |

| Integrated Vibe Development Kits |

| Procedural Vibe Coding |

| Object-Oriented Vibe Coding |

| Functional Vibe Coding |

| Reactive Vibe Coding |

| Hybrid Paradigms |

| On-Premise |

| Cloud-Based |

| Edge-Embedded |

| Consumer Electronics |

| Automotive |

| Industrial Automation |

| Healthcare |

| Gaming and AR/VR |

| Other End User Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Vibe Pattern Encoders | |

| Resonance Signal Transducers | ||

| Haptic Feedback Integrated Circuits | ||

| Integrated Vibe Development Kits | ||

| By Programming Paradigm | Procedural Vibe Coding | |

| Object-Oriented Vibe Coding | ||

| Functional Vibe Coding | ||

| Reactive Vibe Coding | ||

| Hybrid Paradigms | ||

| By Deployment Model | On-Premise | |

| Cloud-Based | ||

| Edge-Embedded | ||

| By End User Industry | Consumer Electronics | |

| Automotive | ||

| Industrial Automation | ||

| Healthcare | ||

| Gaming and AR/VR | ||

| Other End User Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the vibe coding market by 2031?

The vibe coding market is expected to reach USD 15.52 billion by 2031.

How fast is the vibe coding market growing between 2026 and 2031?

It is forecast to register a 17.06% CAGR during the 2026-2031 period.

Which product type currently holds the largest share?

Haptic Feedback Integrated Circuits led with 30.82% of 2025 revenue.

Which end-user segment is expanding the quickest?

Gaming and AR/VR is projected to grow at an 18.92% CAGR through 2031.

Why are edge-embedded deployments gaining traction?

Integrated force-sensing drivers eliminate cloud round-trips, reducing latency and enhancing on-device privacy.

Which region is forecast to grow the fastest after 2026?

The Middle East is set to grow at a 17.92% CAGR through 2031, propelled by smart-city investments.

Page last updated on: