Vial Adaptors For Drug Reconstitution Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 1.78 Billion |

| Growth Rate (2026 - 2031) | 6.29% CAGR |

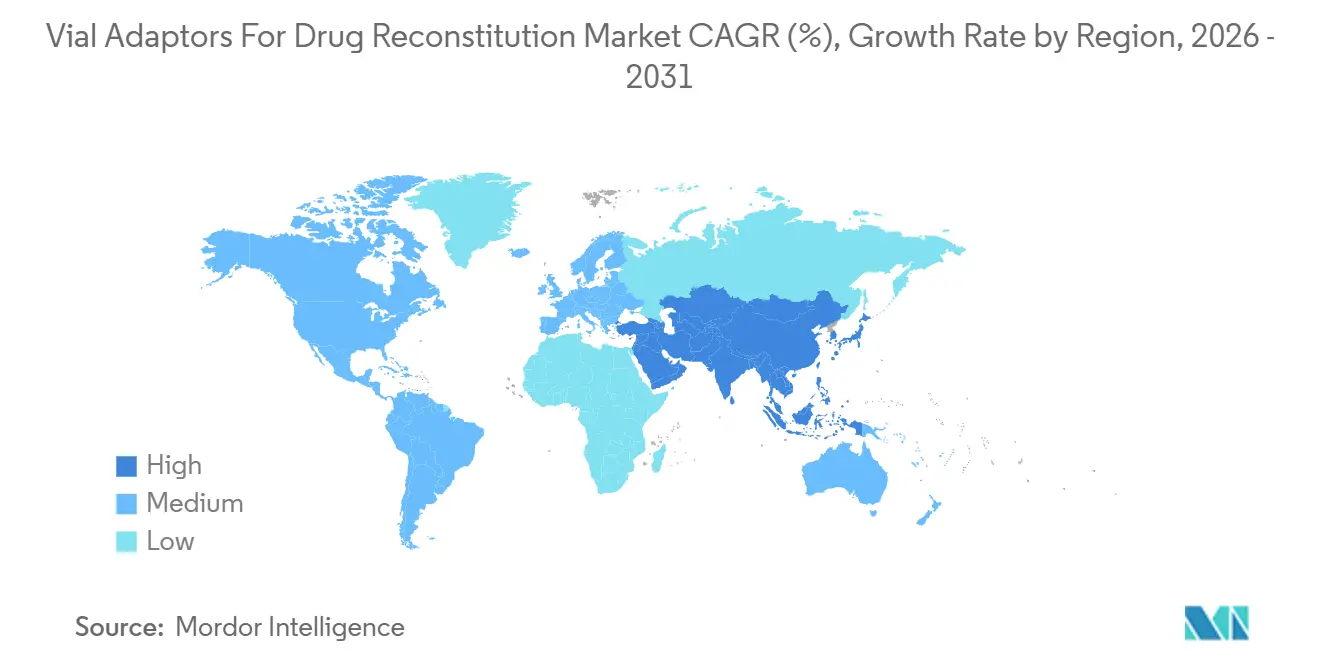

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

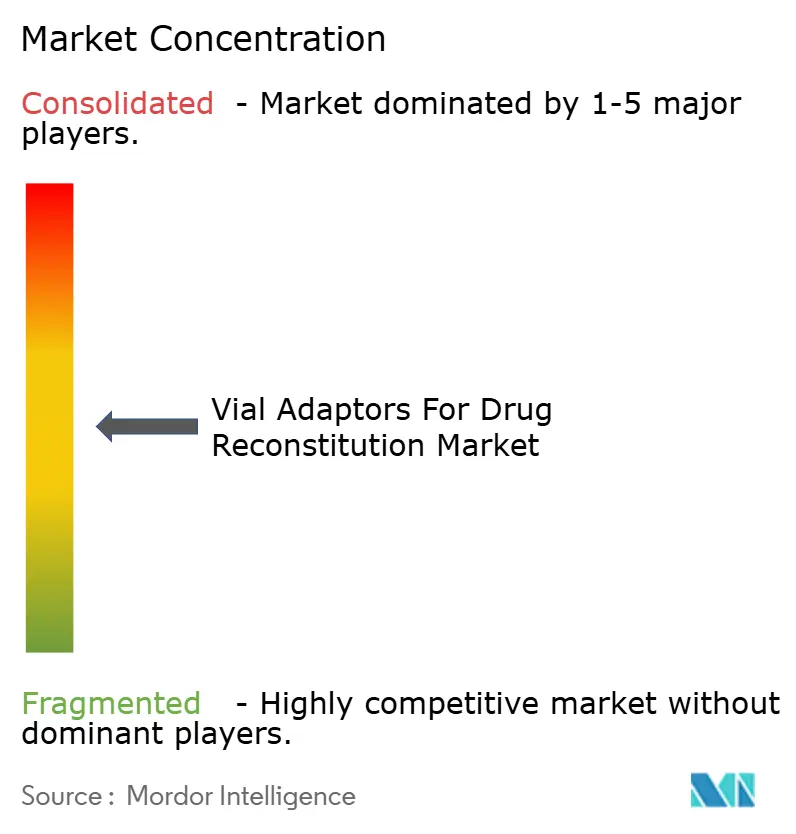

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vial Adaptors For Drug Reconstitution Market Analysis by Mordor Intelligence

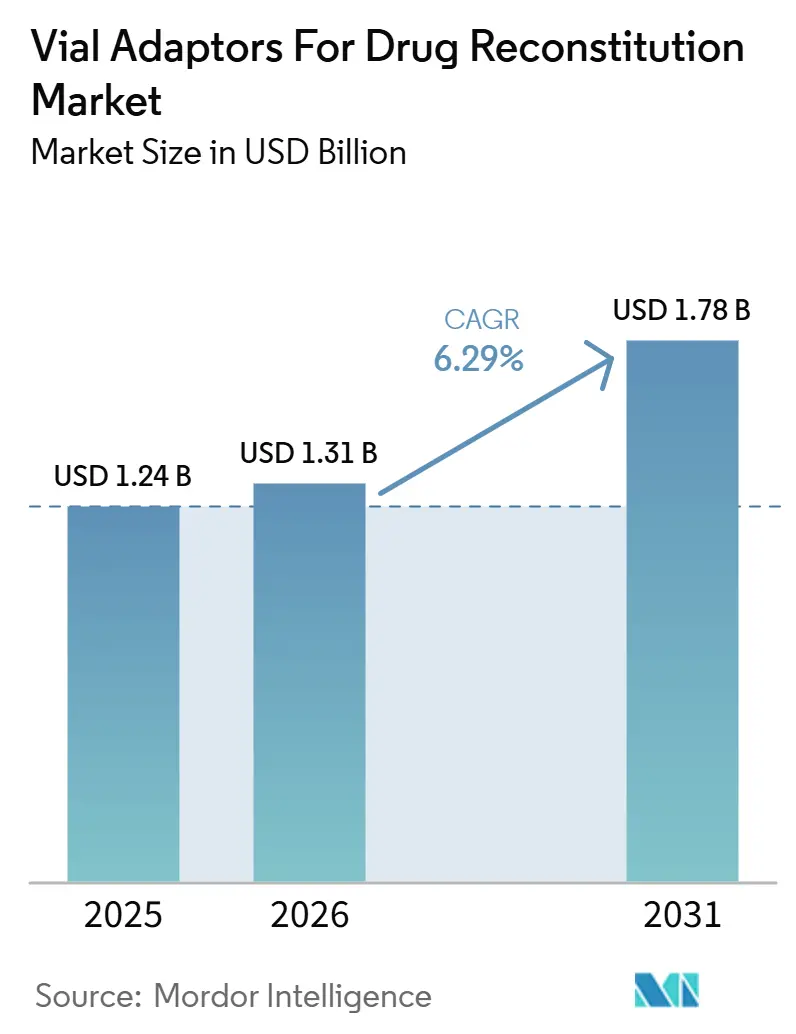

The Vial Adaptors For Drug Reconstitution Market size is expected to grow from USD 1.24 billion in 2025 to USD 1.31 billion in 2026 and is forecast to reach USD 1.78 billion by 2031 at 6.29% CAGR over 2026-2031.

Growth is being sustained by the larger mix of biologics and lyophilized injectables that still need controlled vial-based preparation before administration. The FDA had approved 71 biosimilars by the end of 2024, and each one still requires controlled handling at the point of reconstitution. Hospital pharmacies are also moving toward tighter sterile compounding practices, which keeps demand centered on validated closed-system and needle-free workflows. Connector redesign requirements under ISO 80369-7 are raising validation work for suppliers, but they are also strengthening the position of manufacturers with established regulatory and engineering capabilities. A second layer of expansion is coming from home infusion, outpatient preparation, and cell and gene therapy handling, where standard hospital-oriented devices do not fully address ease of use, compatibility, and workflow needs.

Key Report Takeaways

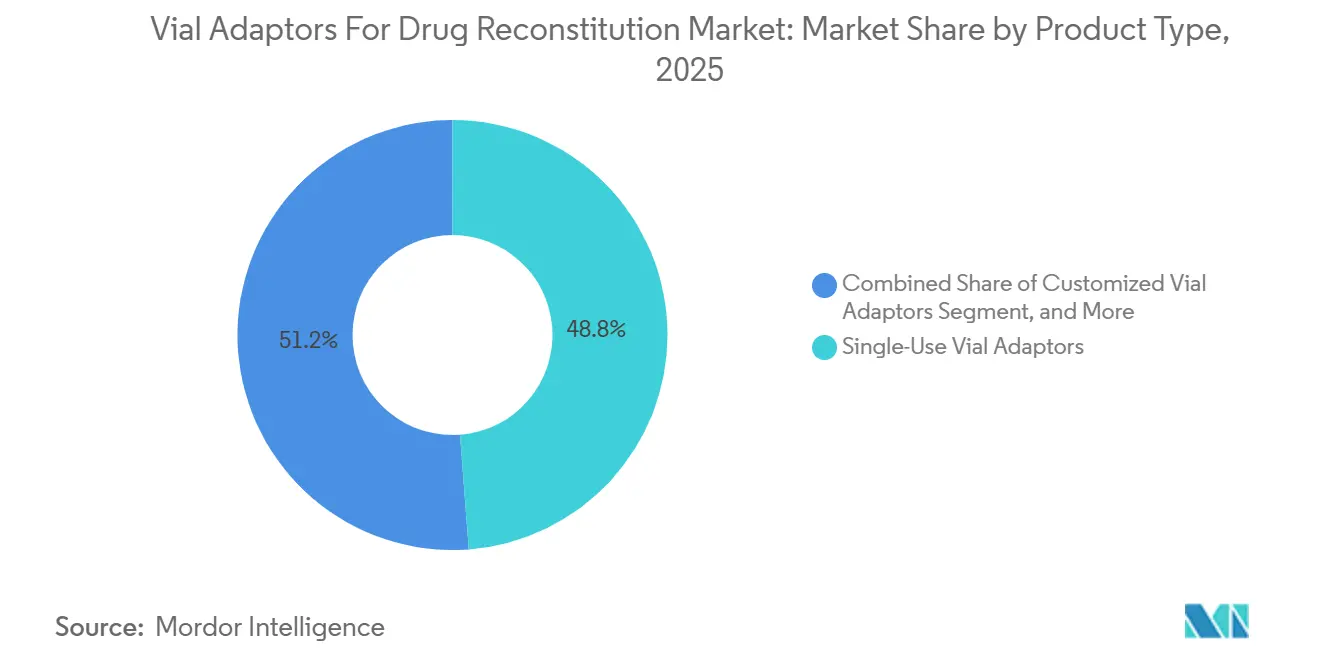

- By product type, single-use vial adaptors led with 48.83% revenue share in 2025, while customized vial adaptors are forecast to expand at a 7.05% CAGR through 2031.

- By material, polycarbonate accounted for 42.38% of revenue in 2025, while polyethylene recorded the highest projected CAGR at 8.66% through 2031.

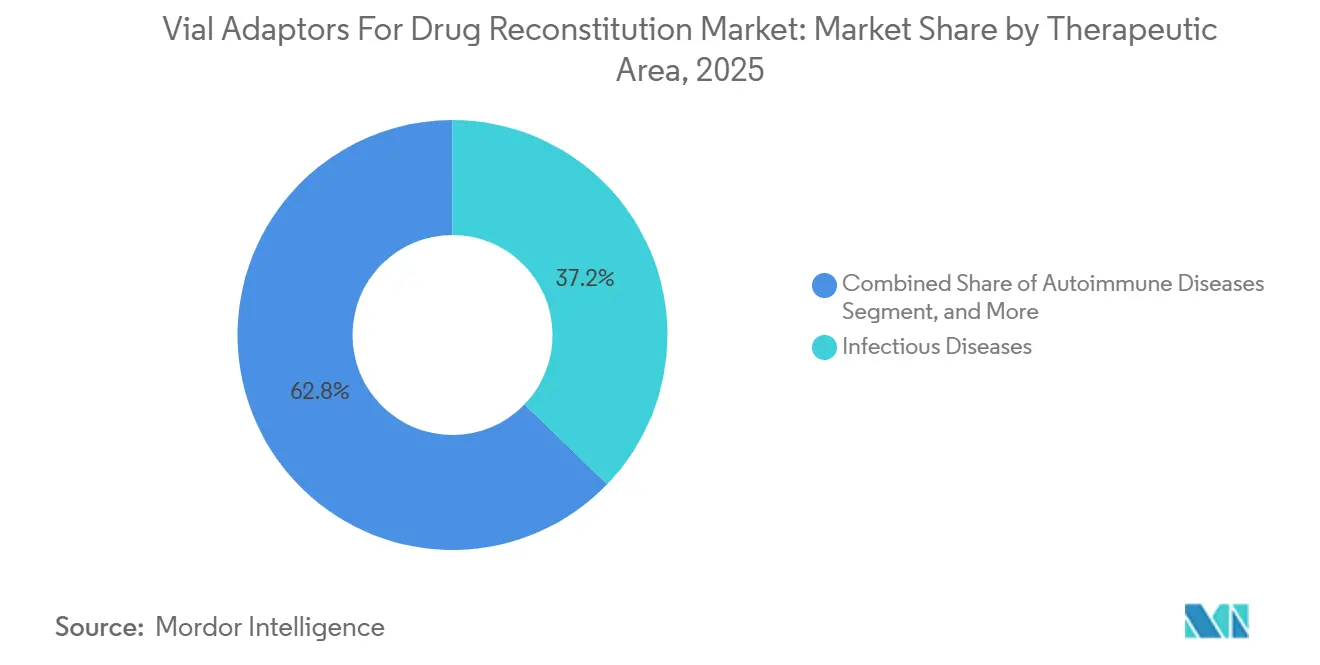

- By therapeutic area, infectious diseases held 37.16% of revenue in 2025 and also posted the fastest projected CAGR at 6.69% through 2031.

- By delivery mode, injection represented 61.16% of revenue in 2025, while infusion is advancing at a 9.19% CAGR through 2031.

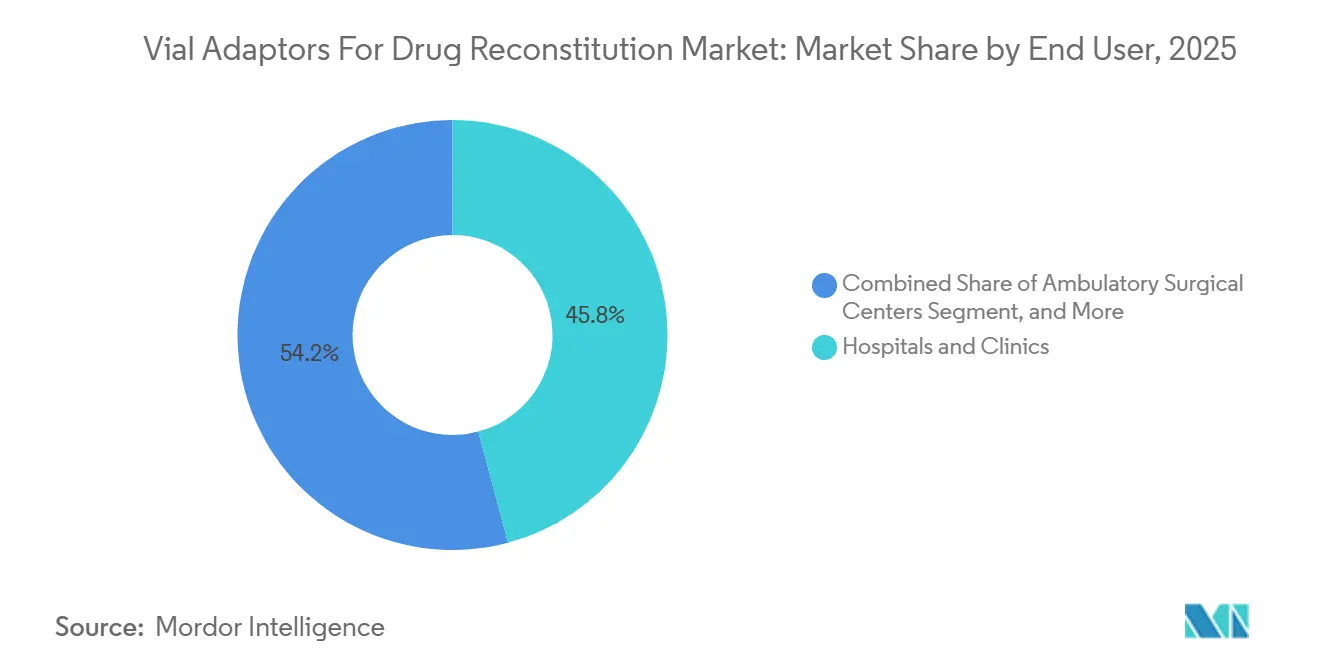

- By end user, hospitals and clinics captured 45.84% of revenue in 2025, while home care is projected to grow at an 8.07% CAGR through 2031.

- By geography, North America held 39.63% of revenue in 2025, while Asia-Pacific is projected to expand at a 7.69% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vial Adaptors For Drug Reconstitution Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Closed-System Reconstitution In High-Risk Injectable Settings | +1.8% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Biosimilar And Lyophilized Drug Pipeline Expansion | +1.5% | Global, with strong Asia-Pacific pull | Medium term (2-4 years) |

| Standardization Of Needleless Transfer Protocols In Hospital Pharmacies | +0.9% | North America and Europe, with spillover to Asia-Pacific | Short term (≤ 2 years) |

| Growth In Home Infusion And Outpatient Infusion Preparation | +1.2% | North America and Europe, with early gains in Asia-Pacific | Medium term (2-4 years) |

| Stronger Focus On Contamination Reduction In Sterile Compounding | +0.8% | Global, concentrated in USP and ISO regulated markets | Short term (≤ 2 years) |

| Shelf-Life Preservation And Dose Preparation Efficiency Gains | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Occupational Safety Standards in High-Risk Drug Handling

The vial adaptors for drug reconstitution market is being supported by stricter handling standards in oncology, immunotherapy, and other high-risk preparation settings. Hospital teams are under stronger pressure to reduce exposure risk during compounding, transfer, and administration of hazardous medicines. That is pushing buyers toward validated closed-system formats instead of open needle-and-syringe steps that create greater operational variability. The 2025 APIC position paper reinforced safe injection, infusion, and medication vial practices across care settings, which keeps safer handling methods visible in infection control and pharmacy policy decisions.[1]Association for Professionals in Infection Control and Epidemiology, “APIC Releases Update to Position Paper on Safe Injection, Infusion, Medication Vial, and Point-of-Care Testing Practices in Health Care,” APIC, apic.org In the vial adaptors for drug reconstitution market, this shift matters beyond oncology because hospitals often extend successful hazardous-drug workflows into broader sterile compounding routines once staff training and procurement standards are already in place. That wider carryover is helping closed-system adoption move from a narrow compliance tool to a routine workflow choice in several hospital departments.

Biosimilar and Lyophilized Drug Pipeline Amplifying Device Volume

The vial adaptors for drug reconstitution market is also being lifted by the growing number of therapies that still depend on vial reconstitution before use. Biosimilars remain a direct demand anchor because each approved product still needs a controlled handling process in hospitals, clinics, or infusion settings. The FDA biosimilar list had reached 71 approvals by the end of 2024, which supports a larger installed base of reconstitution activity across care sites. A 2025 peer-reviewed analysis in Pharmaceutical Research also showed continued investment by major manufacturers in lyophilization capacity, which supports sustained demand for devices used in sterile reconstitution workflows.[2]Mujumdar et al., “Critical Needs and Opportunities for Advanced Manufacturing of Lyophilized Injectables,” Pharmaceutical Research, springer.com In the vial adaptors for drug reconstitution market, this means volume growth is being tied not only to more drugs, but also to a therapy mix that continues to favor formats with greater stability needs before administration. That keeps device demand structural rather than episodic because preparation events rise with both biosimilar adoption and lyophilized drug use.

Growth in Home Infusion and Outpatient Infusion Preparation

The vial adaptors for drug reconstitution market is gaining a separate growth channel as infusion activity shifts out of inpatient hospital environments. Home and alternate-site care require preparation tools that are easy to handle, consistent to connect, and suitable for smaller batch activity. CMS reimbursement support for home infusion therapy has created a practical base for this care setting to expand in the United States.[3]Centers for Medicare and Medicaid Services, “Home Infusion Therapy/Home IVIG Services,” CMS, cms.gov The National Home Infusion Association reported in 2026 that therapy mix and payer patterns continue to evolve across infusion settings, which supports a broader care network for reconstitution activity outside acute care hospitals. In the vial adaptors for drug reconstitution market, the shift favors simple single-use and needle-free formats because the workflow often relies on nurses or alternate-site staff rather than centralized hospital pharmacy teams. It also improves the case for ergonomic and training-light designs that can perform reliably in less controlled care environments.

Contamination-Reduction Metrics in Sterile Compounding Pharmacies

The vial adaptors for drug reconstitution market is also benefiting from the way contamination control is now measured more closely in sterile compounding operations. USP General Chapter <797> tightened expectations around sterile preparation categories, environmental control, and staff competency, which makes contamination prevention a continuous operating issue rather than a periodic review item. That change increases the appeal of devices that help protect sterility during repeated preparation tasks and reduce variability across pharmacy teams. APIC also updated its safe injection and medication vial guidance in 2025, which reinforces consistent vial handling and infection prevention standards across healthcare settings. In the vial adaptors for drug reconstitution market, the value of these devices is no longer limited to exposure reduction because they also support measurable quality goals for pharmacy departments. This makes validated adaptors more attractive in both high-volume biologic preparation and routine sterile compounding workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alternative Reconstitution And Transfer Solutions | -1.1% | Global | Short term (≤ 2 years) |

| Price Sensitivity In Public Hospital Procurement | -0.7% | Asia-Pacific core, Middle East and Africa, and South America | Medium term (2-4 years) |

| Compatibility Limits Across Vial Neck Sizes And Drug Formats | -0.8% | Global | Medium term (2-4 years) |

| Validation Burden For New Device-Drug Handling Workflows | -0.6% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compatibility Limits Across Vial Neck Sizes and Drug Formats

Compatibility remains a core restraint in the vial adaptors for drug reconstitution market because one device format does not easily fit every vial geometry, stopper material, and drug characteristic. Suppliers still have to account for multiple neck diameters, different stopper behaviors, and formulation differences that can change transfer performance. This challenge becomes more serious when drug sponsors use custom primary packaging or specialized biologic formats with limited legacy compatibility data. A 2025 Journal of Pharmaceutical Sciences publication noted that there is still no defined regulatory guidance for compatibility testing expectations for closed system transfer devices used with non-hazardous drugs, leaving sponsors and care sites to complete their own risk assessments. In the vial adaptors for drug reconstitution market, that uncertainty lengthens validation cycles and raises switching costs when hospitals or manufacturers consider new adaptor configurations. It also helps incumbents because approved and familiar formats face fewer questions than new designs entering broader clinical use.

Price Sensitivity in Public Hospital Procurement

Price pressure continues to limit the vial adaptors for drug reconstitution market in public healthcare systems, where tenders still focus heavily on unit cost. Single-use adaptors create a recurring consumable expense, which can push budget-constrained hospitals back toward lower-cost manual workflows. This is especially relevant in systems that do not yet score contamination prevention, exposure reduction, or workflow efficiency as formal purchasing criteria. The result is a split environment where premium validated systems gain traction in tightly regulated hospitals, while public-sector buyers in cost-sensitive regions move more slowly. In the vial adaptors for drug reconstitution market, this is not only a pricing issue because it also reflects uneven measurement of downstream safety and quality outcomes. Until procurement models place a stronger weight on these wider benefits, adoption will stay slower in hospitals that face tight operating budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Single-Use Dominance Tempered by Customization Demand

Single-use vial adaptors held 48.83% of the vial adaptors for drug reconstitution market size in 2025, which shows how strongly hospitals still favor disposable formats for sterile preparation. Their position is tied to everyday pharmacy practice because disposable use reduces concerns around cross-contamination, reuse risk, and workflow variation. The vial adaptors for drug reconstitution market continues to reward this format in hospitals that treat sterility assurance as a baseline requirement rather than a discretionary feature. USP <797> has reinforced that environment by tightening expectations around sterile compounding control and handling discipline. Single-use products also fit better with alternate-site settings where device simplicity matters as much as sterility protection. They are therefore likely to remain the volume anchor of the vial adaptors for drug reconstitution market even as other formats grow faster.

Multi-use vial adaptors still retain a place in high-throughput settings where defined compatibility data and controlled operating routines can support repeated activations. B. Braun states that its OnGuard 2 closed system transfer device supports validated use windows of up to 7 days and 10 activations, which helps explain why some pharmacies still evaluate multi-use economics carefully. Customized vial adaptors are the fastest-growing product type at a 7.05% CAGR through 2031, and that pace shows where the vial adaptors for drug reconstitution market is opening new value pools. West highlighted cell and gene therapy evaluations for its vial adapter and vented vial adapter devices in early 2026, which points to active development for specialized applications. As a result, customized products are moving away from a commodity device role and toward a partner-led specification business shaped by therapy design, fill-finish choices, and sponsor validation needs. In segment terms, this is where the vial adaptors for drug reconstitution industry show the clearest move toward solution selling instead of standard catalog competition.

By Material: Polycarbonate's Optical Advantage and the Emerging Polyethylene Challenge

Polycarbonate accounted for 42.38% of revenue in 2025, making it the leading material platform in the vial adaptors for drug reconstitution market. Its position reflects the practical value of visibility during preparation, since pharmacists and nurses need to inspect fluid transfer and solution appearance during handling. The material also remains familiar to manufacturers because it offers durability and a known performance profile across a wide range of drug workflows. The vial adaptors for drug reconstitution market still benefits from that familiarity because buyers often prefer materials with a longer record in regulated sterile applications. Stevanato Group’s EZLINK vial adapter shows how suppliers combine rigid polymer design with safety features that help limit stopper coring and improve handling consistency. That balance between visibility, safety, and established processing keeps polycarbonate firmly positioned in current demand.

Polyethylene is the fastest-growing material at an 8.66% CAGR through 2031, which signals changing priorities in the vial adaptors for drug reconstitution market as biologic sensitivity gains importance. Buyers are placing greater weight on material behavior with protein-based drugs, especially where extractables, leachables, and surface interaction concerns influence device selection. This gives polyethylene a stronger role in newer therapy workflows where chemical inertness matters more than visual familiarity alone. Silicone also remains relevant within seals and valve components because repeated connection performance still depends on stable elastomeric behavior. The vial adaptors for drug reconstitution market is therefore not moving toward a single winning material, but toward more deliberate material matching by therapy type and handling protocol. That is another area where the vial adaptors for drug reconstitution industry are becoming more specification-driven as drug complexity increases.

By Therapeutic Area: Infectious Diseases Volume Masks Oncology's Strategic Value

Infectious diseases represented 37.16% of revenue in 2025, making them the largest therapy segment in the vial adaptors for drug reconstitution market. The leading position comes from daily hospital volume because antibiotics, antivirals, and antifungals are reconstituted at a scale that few other therapy classes match. These workflows are often repetitive and standardized, which supports high recurring adaptor use across inpatient and outpatient care. B. Braun’s April 2025 FDA approval and December 2025 launch of Piperacillin and Tazobactam in the DUPLEX Drug Delivery System showed how anti-infective therapy suppliers are continuing to embed closed-system preparation into ready-to-use formats. Even when those formats can compete with standalone adaptor demand, they still validate the same clinical logic behind safer and more efficient reconstitution. For that reason, infectious disease volume still sets the operating rhythm of the vial adaptors for drug reconstitution market in many hospital pharmacies.

Infectious diseases also post the fastest growth within therapeutic areas at a 6.69% CAGR through 2031, which means their lead is being reinforced rather than diluted. Outpatient antibiotic infusion and home-based anti-infective reimbursement are widening the settings where these products are prepared. Oncology remains strategically important because it is the area where buyers most clearly justify premium adaptor pricing through exposure control and dose accuracy. A June 2026 analysis in the European Journal of Hospital Pharmacy showed how monoclonal antibody reconstitution practices affect both efficiency and patient safety in chemotherapy units. Autoimmune and metabolic therapies are smaller in current revenue, but they are expanding as more biologic treatment regimens rely on vial-based handling. Within the vial adaptors for drug reconstitution market, this creates a mix where infectious diseases drive breadth while oncology and advanced biologics influence value capture and product differentiation.

By Delivery Mode: Injection's Scale vs. Infusion's Structural Acceleration

Injection remained the dominant delivery mode with 61.16% of the vial adaptors for drug reconstitution market share in 2025, which reflects how widely bolus and intramuscular administration still shape global injectable care. This mode covers the broadest set of hospital use cases, from emergency medicine to routine sterile pharmacy preparation. Because so many injectable drugs still reach care sites in vial formats, injection continues to anchor demand across both standard and specialized workflows. The vial adaptors for drug reconstitution market, therefore, retain a strong base in products designed around injection-oriented preparation and connection steps. West’s May 2026 ISO 80369-7 update for vial adapter transfer devices also shows how injection-mode components are still evolving to meet connector compliance requirements. That kind of redesign work supports the segment’s long-term relevance even though its growth rate is lower than that of infusion.

Infusion is the fastest-growing delivery mode at a 9.19% CAGR through 2031, which makes it the clearest structural acceleration point in the vial adaptors for drug reconstitution market. Growth is tied to specialty drug use, hospital-at-home models, and wider reliance on ambulatory infusion centers. West’s Vial2Bag Advanced needle-free admixture devices directly address vial-to-IV-bag workflows, which show how manufacturers are targeting infusion-specific preparation needs rather than adapting older hospital formats without change. As infusion activity spreads into community and home settings, buyers will need devices that balance sterility control with straightforward bedside or alternate-site handling. That will keep infusion at the center of product redesign, training simplification, and broader device differentiation. In this segment, the vial adaptors for drug reconstitution industry are being reshaped by the way care delivery is moving closer to the patient.

By End User: Hospital Core Efficiency vs. Home Care Growth Opportunity

Hospitals and clinics represented 45.84% of revenue in 2025, giving them the leading end-user position in the vial adaptors for drug reconstitution market. Their dominance is rooted in hazardous drug preparation, high-volume compounding, and formal pharmacy oversight. Large hospital systems also tend to standardize around a smaller set of approved device platforms, which strengthens incumbent supplier positions once workflows are embedded. The vial adaptors for drug reconstitution market still depend on these institutions for scale because they concentrate the largest number of validated preparation events. Ambulatory surgical centers are also gaining relevance as same-day procedure volumes rise and pre-operative injectable preparation increases. Pharmaceutical and biotechnology companies form a separate end-user group because they use these devices in stability testing, clinical supply, and process validation activities.

Home care is the fastest-growing end-user segment at an 8.07% CAGR through 2031, showing how the vial adaptors for drug reconstitution market is expanding beyond institutional pharmacy walls. CMS home infusion payment support creates a basic reimbursement framework that helps sustain this shift in the United States. NHIA’s 2026 trends report also highlights continuing evolution in therapy categories and care settings across the infusion landscape. Devices used in home care need to be reliable with limited setup complexity, minimal sharps risk, and clear connection logic. Retail pharmacies remain a smaller segment, but they matter more as sterile compounding activity grows in outsourced and semi-institutional channels. This is another area where the vial adaptors for drug reconstitution market is opening room for differentiated design rather than only scale manufacturing.

Geography Analysis

North America accounted for 39.63% of global revenue in 2025, giving the region the largest position in the vial adaptors for drug reconstitution market. Its lead is supported by strong sterile compounding oversight, a dense network of oncology and infusion care sites, and more established home infusion adoption. USP <797> and related compounding expectations continue to shape pharmacy handling practices, which supports consistent use of validated reconstitution tools. APIC’s 2025 update on safe injection and medication vial practices also reinforced the infection prevention case for better-controlled handling methods across healthcare settings. The United States remains the anchor of the vial adaptors for drug reconstitution market in this region, while Canada and Mexico add smaller but rising demand as biologics use broadens.

Europe remains a significant region in the vial adaptors for drug reconstitution market because large hospital systems continue to emphasize controlled compounding and worker safety in injectable preparation. Germany, France, the United Kingdom, Italy, and Spain form the main demand base through their hospital pharmacy infrastructure and recurring tender cycles. The region also remains important for premium device adoption because buyers often expect strong validation files and reliable compatibility performance. This keeps Europe relevant both for current sales and for the early adoption of higher-specification adaptor systems.

Asia-Pacific is the fastest-growing regional segment, and its 7.69% CAGR marks the strongest geographic expansion path in the vial adaptors for drug reconstitution market through 2031. Demand is rising as hospitals in China, India, South Korea, Japan, and Australia modernize pharmacy workflows and increase biologic handling capacity. The region also benefits from expanding domestic injectable manufacturing and broader public health procurement activity, which widens the base for reconstitution events. The Middle East and Africa and South America remain smaller today, but they are gradually adding demand as biosimilar use, hospital modernization, and safer handling expectations improve across public care systems.

Competitive Landscape

The vial adaptors for drug reconstitution market operates through a moderately concentrated structure with 2 broad competitive tiers. The first tier includes large integrated players such as Becton, Dickinson and Company, West Pharmaceutical Services Inc., B. Braun SE, and Baxter International Inc., which benefit from existing hospital relationships and wider drug preparation portfolios. Their scale matters because hospitals often prefer suppliers with regulatory depth, training support, and a broader installed product base. The second tier includes specialist companies such as Simplivia Healthcare Ltd., EQUASHIELD LLC, and Corvida Medical Inc., which compete through narrower but more differentiated value claims. In the vial adaptors for drug reconstitution market, this mix creates steady pressure between platform stability on one side and niche performance positioning on the other.

Competition is also being shaped by compliance readiness and product development partnerships. West implemented an ISO 80369-7-compliant design update for its vial adapter transfer devices in May 2026, which shows how connector standard changes can become a meaningful differentiator for suppliers that can execute redesigns smoothly. BD announced a strategic collaboration with Suttons Creek in April 2026 to help pharmaceutical and biotech clients manage combination product development and testing, which reflects a move toward deeper device-drug integration support. B. Braun renamed its OEM division as B. Braun Pharma & MedTech Partner in March 2026, signaling a stronger co-development approach for customized delivery and reconstitution solutions. These moves show that the vial adaptors for drug reconstitution market is no longer driven only by individual device units, but also by broader service, validation, and partnership capabilities.

White-space opportunities in the vial adaptors for drug reconstitution market are most visible in cell and gene therapy applications, home-care-friendly ergonomics, and cost-conscious solutions for public sector procurement. West’s January 2026 publication on sterile vial adapter transfer devices for cell and gene therapy use showed that suppliers are actively tailoring platforms for advanced therapy workflows. Simplivia’s March 2026 EAHP presence also highlighted continued effort to strengthen visibility around full vial-to-vein closed-system workflows in hospital pharmacy practice. As a result, the vial adaptors for drug reconstitution market is likely to reward companies that can combine compatibility breadth, regulatory credibility, and easier use across nontraditional care environments. Suppliers that rely only on older hospital-centric formats may find it harder to keep pace as demand shifts toward more specialized and decentralized handling settings.

Vial Adaptors For Drug Reconstitution Industry Leaders

Becton, Dickinson and Company

B. Braun SE

EQUASHIELD LLC

Nipro Corporation

Vygon SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: West Pharmaceutical Services, Inc. implemented an ISO 80369-7-compliant design update to its Vial Adapter transfer devices for US and EU SKUs, effective May 13, 2026, replacing the withdrawn ISO 594-1/2 standards with revised Luer-lock thread geometry. The update maintains 510(k) clearance and CE mark status and underscores compliance-driven product lifecycle management at a key market inflection point.

- April 2026: Becton, Dickinson and Company announced a strategic collaboration with Suttons Creek (a BlueRidge Life Sciences company) to streamline combination product development for pharmaceutical and biotech clients, integrating BD's ZebraSci device testing services with Suttons Creek's systems integration capabilities. The partnership targets device-drug compatibility validation timelines for complex biologics requiring reconstitution-ready configurations.

- March 2026: Simplivia Healthcare Ltd. showcased the Chemfort CSTD at the 30th EAHP Congress in Barcelona, including live demonstrations of the full vial-to-vein closed-system workflow. The Chemfort Vial Adaptor's ToxiGuard activated-carbon barrier technology, which physically locks in hazardous drug molecules during reconstitution, received expanded attention from European hospital pharmacy delegates.

- March 2026: B. Braun SE renamed its OEM Division to B. Braun Pharma & MedTech Partner, signalling a strategic shift toward co-development partnerships for customized drug delivery and reconstitution solutions covering hospital, outpatient, and home-care settings, with 2026 priorities including expanded clinical trial supply and kitting capabilities.

Global Vial Adaptors For Drug Reconstitution Market Report Scope

The vial adaptors for drug reconstitution market refers to the global market for medical devices designed to facilitate the safe, efficient, and sterile transfer of diluents into drug vials and the withdrawal of reconstituted medications for administration. Vial adaptors are attached to medication vials to provide a secure, needle-free, or low-needle-access connection between the vial and syringes or transfer devices, minimizing the risk of contamination, drug spillage, needlestick injuries, and medication preparation errors.

The vial adaptors for drug reconstitution market is segmented based on product type, material, therapeutic area, delivery mode, end user, and geography. By product type, the market is categorized into single-use vial adaptors, multi-use vial adaptors, and customized vial adaptors. Based on material, the market includes polycarbonate, silicone, polyethylene, and other materials, with material selection depending on factors such as durability, chemical compatibility, sterility, and performance. By therapeutic area, the market is segmented into infectious diseases, autoimmune diseases, metabolic conditions, oncology, and other therapeutic areas. Based on delivery mode, the market is divided into injection and infusion. By end user, the market comprises hospitals and clinics, ambulatory surgical centers, retail pharmacies, home care settings, pharmaceutical and biotechnology companies, and other end users. Geographically, the market is analyzed across North America (United States, Canada, and Mexico), Europe (Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and the Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, and the Rest of the Middle East & Africa), and South America (Brazil, Argentina, and the Rest of South America).

| Single-Use Vial Adaptors |

| Multi-Use Vial Adaptors |

| Customized Vial Adaptors |

| Polycarbonate |

| Silicone |

| Polyethylene |

| Other Materials |

| Infectious Diseases |

| Autoimmune Diseases |

| Metabolic Conditions |

| Oncology |

| Other Therapeutic Areas |

| Injection |

| Infusion |

| Hospitals and Clinics |

| Ambulatory Surgical Centers |

| Retail Pharmacies |

| Home Care Settings |

| Pharmaceutical and Biotechnology Companies |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Single-Use Vial Adaptors | |

| Multi-Use Vial Adaptors | ||

| Customized Vial Adaptors | ||

| By Material | Polycarbonate | |

| Silicone | ||

| Polyethylene | ||

| Other Materials | ||

| By Therapeutic Area | Infectious Diseases | |

| Autoimmune Diseases | ||

| Metabolic Conditions | ||

| Oncology | ||

| Other Therapeutic Areas | ||

| By Delivery Mode | Injection | |

| Infusion | ||

| By End User | Hospitals and Clinics | |

| Ambulatory Surgical Centers | ||

| Retail Pharmacies | ||

| Home Care Settings | ||

| Pharmaceutical and Biotechnology Companies | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the vial adaptors for drug reconstitution market?

The vial adaptors for drug reconstitution market was valued at USD 1.24 billion in 2025 and reached USD 1.31 billion in 2026, with a forecast of USD 1.78 billion by 2031.

What is driving growth through 2031?

Growth is being supported by more biosimilars, broader lyophilized injectable use, tighter sterile compounding standards, and rising home and outpatient infusion activity.

Which product type leads demand today?

Single-use vial adaptors led demand with 48.83% revenue share in 2025 because hospitals continue to prioritize disposable sterile workflows.

Which segment is expanding the fastest?

Infusion is the fastest-growing delivery mode at a 9.19% CAGR through 2031, while polyethylene is the fastest-growing material at 8.66% and home care is the fastest-growing end user at 8.07%.

Which region leads global revenue?

North America held 39.63% of revenue in 2025 due to stronger sterile compounding oversight, established infusion networks, and broader adoption of validated handling systems.

Why are customized vial adaptors gaining traction?

Customized products are projected to grow at a 7.05% CAGR because cell and gene therapy, non-standard vial formats, and sponsor-specific compatibility needs are creating demand beyond standard hospital configurations.

Page last updated on: