Veterinary Hospital Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

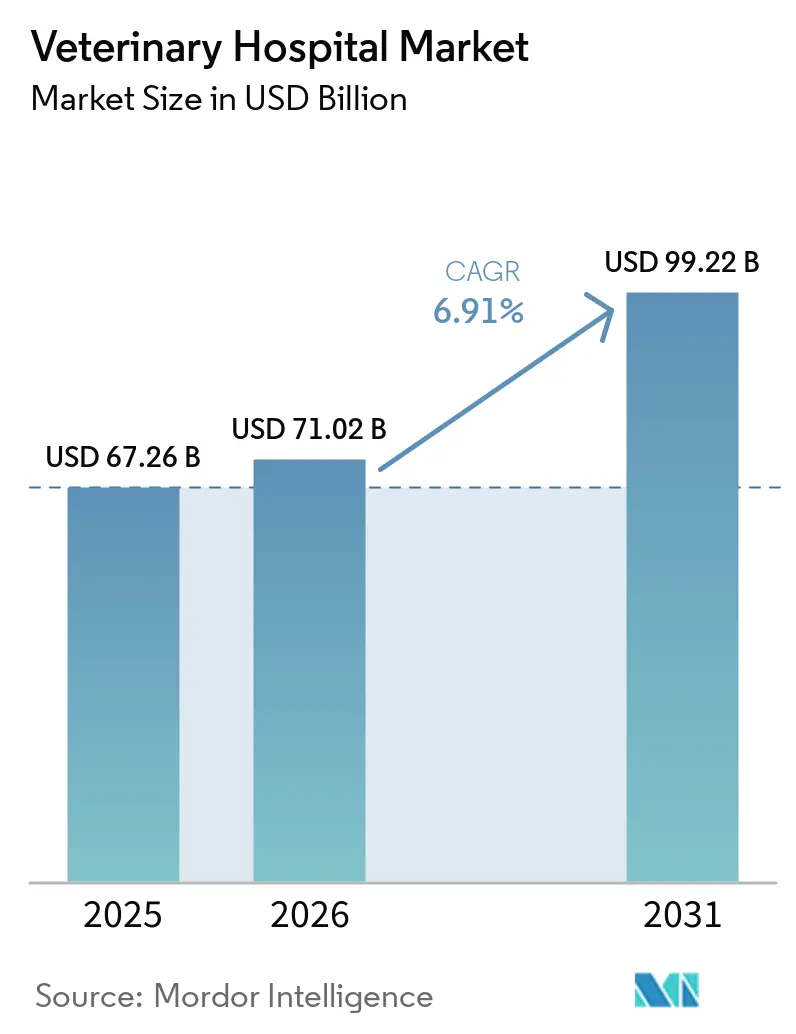

| Market Size (2026) | USD 71.02 Billion |

| Market Size (2031) | USD 99.22 Billion |

| Growth Rate (2026 - 2031) | 6.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Hospital Market Analysis by Mordor Intelligence

The Veterinary Hospital Market size is projected to be USD 67.26 billion in 2025, USD 71.02 billion in 2026, and reach USD 99.22 billion by 2031, growing at a CAGR of 6.91% from 2026 to 2031.

Momentum in the veterinary hospital market reflects expanding pet insurance coverage that improves access to advanced care, continued enterprise consolidation that enables specialty build-outs, and workflow optimization that raises average transaction value even as visit volumes fluctuate. Pricing discipline and diagnostic bundling support margins as clinics protect profitability through better utilization of imaging and labs, aided by data-guided scheduling. Corporate networks extend service breadth with 24/7 emergency hubs and oncology programs, shaping client expectations for continuity of care and predictable service standards. Regulatory scrutiny, especially in mature markets, is pushing transparent pricing and ownership disclosure, which may temper pricing power but can also boost trust and repeat usage. Workforce constraints remain a central factor shaping access and capacity, prompting investments in automation and role redesign across clinical and administrative functions.

Key Report Takeaways

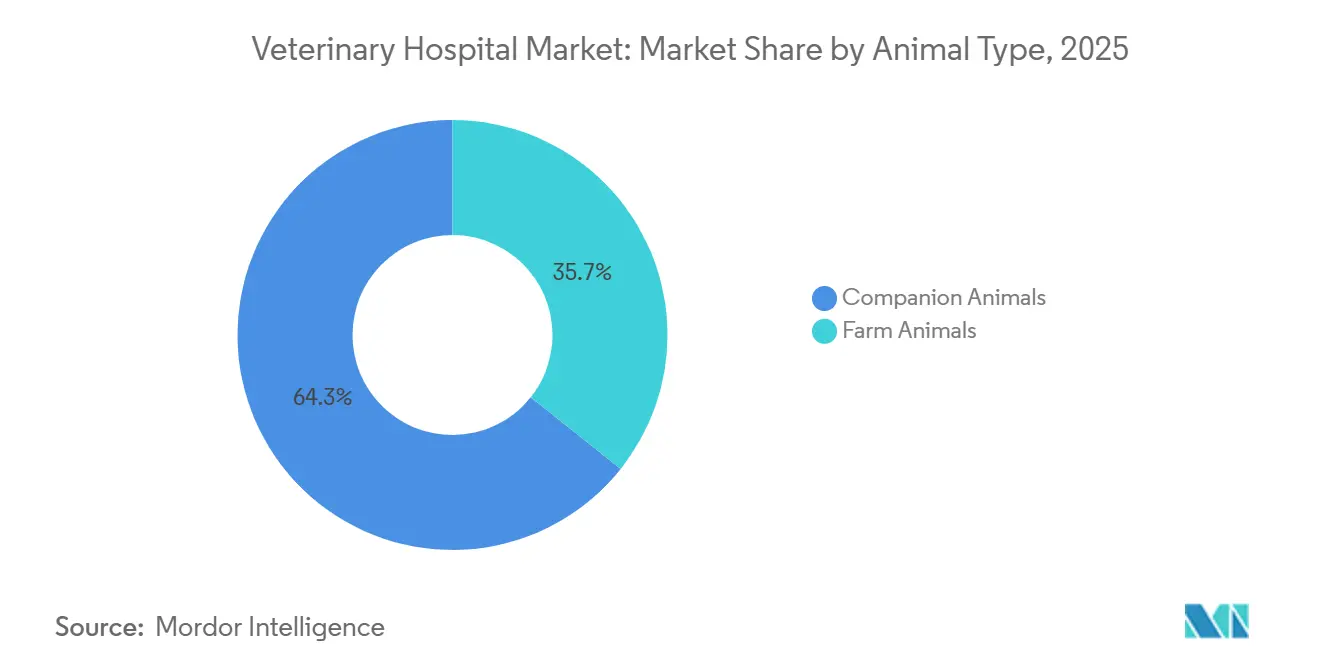

- By animal type, companion animals led with 64.32% revenue share in 2025. Companion animals are projected to expand at an 8.32% CAGR through 2031.

- By service type, medical services held 46.23% share in 2025. Surgical services are forecast to expand at an 8.58% CAGR through 2031.

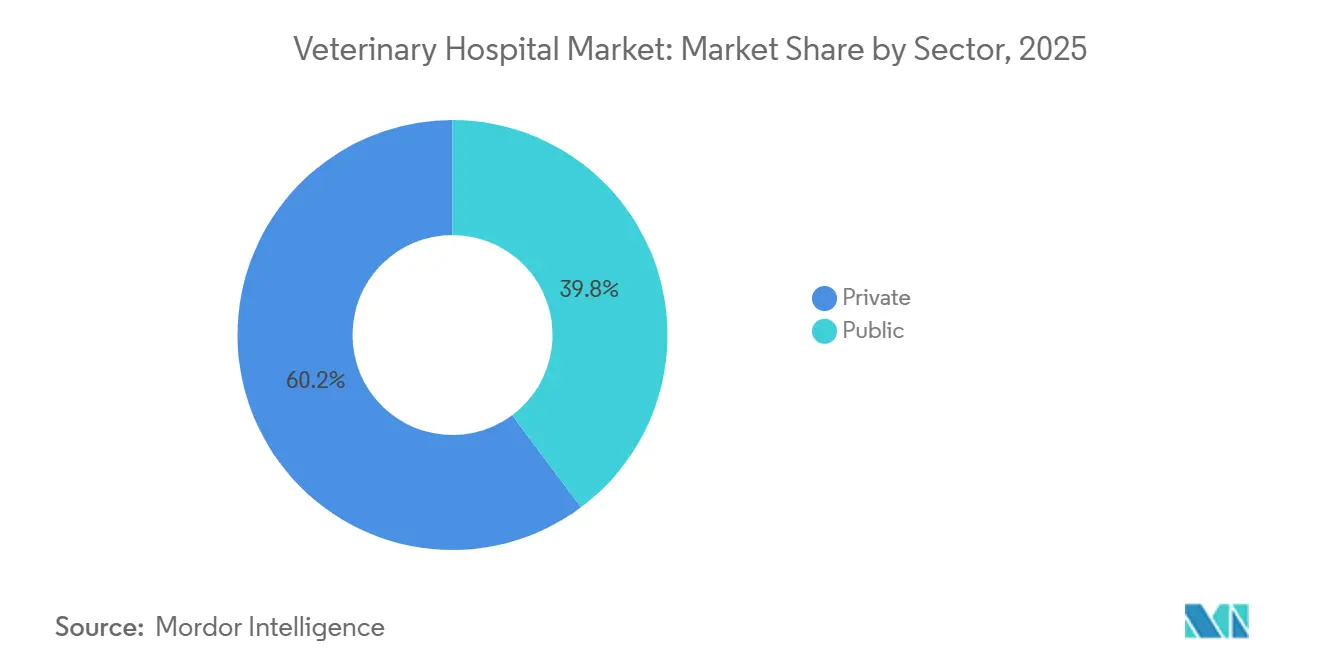

- By sector, the private segment accounted for 60.23% of 2025 revenues. The private segment is projected to grow at a 7.98% CAGR to 2031.

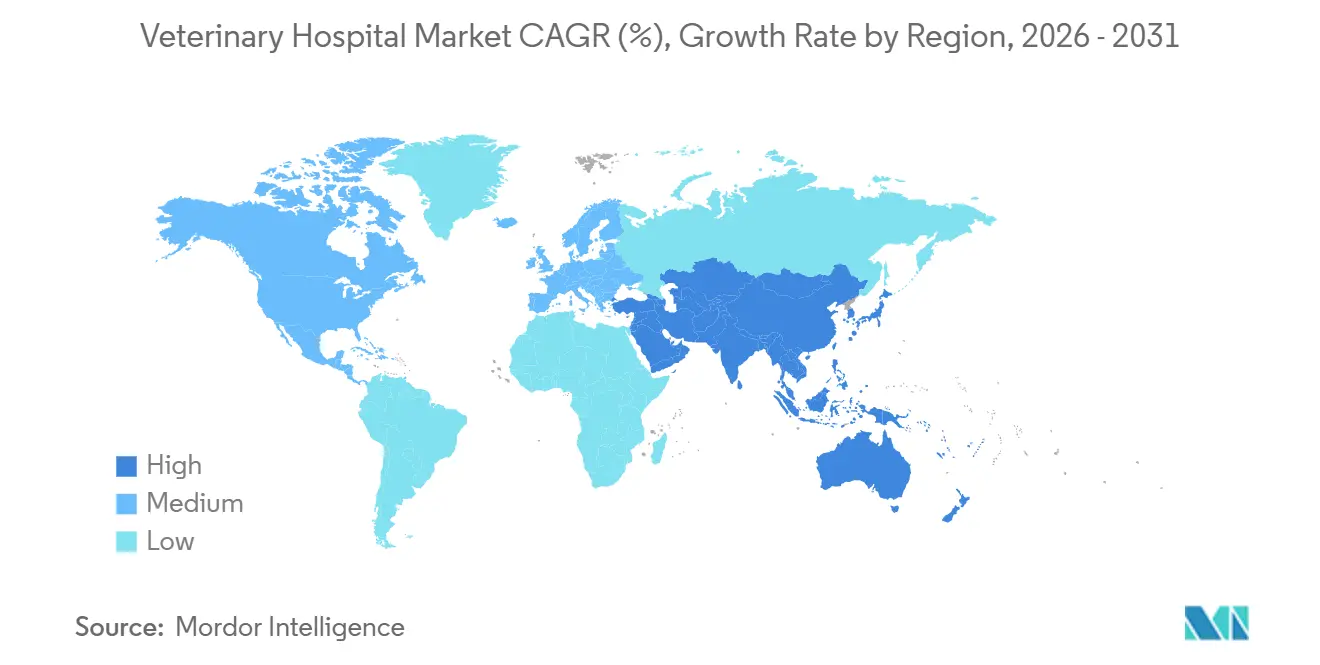

- By geography, North America held 42.32% share in 2025. Asia-Pacific is projected to record the highest CAGR at 8.93% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Veterinary Hospital Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pet Insurance Adoption Expands Access To High-Acuity Care | +1.2% | North America & EU, early APAC penetration | Medium term (2-4 years) |

| Companion Animal Ownership Intensity Sustains Visit Volumes | +1.5% | Global, strongest in urban APAC & North America | Long term (≥ 4 years) |

| Specialty And Advanced Diagnostics/Surgery Adoption Lifts Revenue Per Visit | +1.8% | North America, Western Europe, Tier-1 APAC | Medium term (2-4 years) |

| Corporate Consolidation Enables Capex, Specialty Build-Outs, And Standardized Care | +1.4% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| Enterprise Data/AI Tools Improve Scheduling, RCM, And Capacity Utilization | +0.9% | North America, Western Europe, urban APAC | Short term (≤ 2 years) |

| APAC Urbanization And Middle-Class Growth Accelerate Demand For Veterinary Care | +1.1% | China, India, Southeast Asia spill-over to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Pet Insurance Adoption Expands Access To High-Acuity Care

Written premium in North American pet health insurance rose to USD 5.2 billion in 2024, up 20.8% from 2023, with 7.03 million insured pets, reflecting accelerating adoption and an expanding financial backstop for advanced treatments[1]NAPHIA Staff, “North American Pet Health Insurance Industry Market Reaches $5.2B in Written Premium,” North American Pet Health Insurance Association, naphia.org. Penetration remains well below Nordic benchmarks, yet the direction of travel is clear as insurers, employers, and digital enrollment reduce friction and raise awareness about coverage options. Clinics serving higher shares of insured clients typically face fewer cost-driven treatment compromises, which supports a fuller diagnostic and surgical workflow. Access to coverage also reduces volatility in case acceptance for oncology and orthopedic procedures whose ticket sizes can challenge out-of-pocket affordability. As insured pet cohorts grow, hospitals can plan capacity and inventory with more confidence, aligning specialty scheduling with predictable reimbursement paths. The net effect is a wider funnel for high-acuity care that sustains the veterinary hospital market even when discretionary visit frequency softens at the margin.

Specialty And Advanced Diagnostics/Surgery Adoption Lifts Revenue Per Visit

Diagnostics outperformed in 2025 on clinics’ revenue mix, supported by pricing updates and tighter integration of in-house testing into wellness and sick-visit protocols that raise per-visit yield. Product innovation is expanding point-of-care capability, such as IDEXX’s inVue Dx Cellular Analyzer, an AI-enabled, slide-free solution launched in late 2024 that automates differential counts, and IDEXX Cancer Dx, an early detection blood test for canine lymphoma slated for rollout in March 2025[2]IDEXX Communications, “IDEXX Laboratories Announces Fourth Quarter and Full Year 2024 Results,” IDEXX Laboratories, idexx.com. These platforms compress time-to-diagnosis, enabling more general practices to complete workups without referral and to keep downstream procedures in-house. On the surgical side, cranial cruciate ligament repairs account for a dominant share of canine orthopedic cases, and advanced TPLO and TTA techniques favored by specialty hospitals command higher fees and support stronger EBITDA profiles than traditional extracapsular options. The capability to combine advanced imaging with specialty surgery centralizes more value within hospital networks that can staff and equip these services. As more clinics adopt integrated diagnostic-to-procedure workflows, revenue per active client rises and supports reinvestment in further specialty build-outs.

Corporate Consolidation Enables Capex, Specialty Build-Outs, And Standardized Care

Scaled operators continue to expand multi-location networks, which unlock capital for advanced imaging, oncology programs, and 24/7 emergency capacity that smaller clinics cannot easily finance. National Veterinary Associates’ Ethos Veterinary Health segment operates more than 140 specialty and emergency hospitals across North America, illustrating the density and scope that enterprise groups can achieve to anchor referral ecosystems. Consolidators also deploy shared IT stacks, purchasing programs, and standardized clinical pathways that drive consistency and cost control at the point of care. New integrated models are emerging, such as Chewy’s agreement to acquire Modern Animal’s membership-based clinics alongside 24/7 virtual care, creating a tighter loop between care delivery, scheduling, and commerce[3]Business Wire Editorial, “Chewy to Acquire Modern Animal Accelerating Evolution to a Fully Integrated Healthcare Ecosystem,” Business Wire, businesswire.com. Standardized pricing frameworks and enterprise analytics allow chains to shape case-mix and staffing to maximize utilization without sacrificing service quality. Scale also improves recruiting reach for scarce specialists by offering career pathways and clinical collaboration that are harder to achieve in single-site settings. These dynamics provide a durable tailwind to the veterinary hospital market as specialty and emergency capacity expand within cohesive networks.

Enterprise Data/AI Tools Improve Scheduling, RCM, And Capacity Utilization

Hospitals are using analytics to reduce no-shows, fill underutilized blocks, and lift per-visit diagnostics through protocol adherence nudges and targeted reminders. Practices supported by data-driven operations have outpaced average revenue growth, helped by tighter appointment cadence and automated follow-ups that sustain continuity of care. Digital triage and virtual rechecks extend clinician capacity while preserving in-person slots for procedures, which improves case throughput in constrained staffing environments. Revenue cycle management automation reduces leakage from estimate-to-invoice friction and improves capture of lab, imaging, and injectable services that are less exposed to online price competition. As these systems mature, clinics can better align staffing hours with peak demand and match client preferences for booking convenience, which smooths operational variability. The cumulative gains in utilization and capture rate support steady advancement of the veterinary hospital market, even when macro conditions pressure discretionary spending.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Veterinarian And Technician Shortages Constrain Capacity And Hours | -0.8% | Global, acute in North America & rural EU | Medium term (2-4 years) |

| Veterinary Services Inflation Elevates Price Sensitivity And Care Deferrals | -0.7% | North America, Western Europe | Short term (≤ 2 years) |

| UK CMA 2026 Remedies Cap Prescription Fees And Mandate Price/Ownership Transparency | -0.4% | UK, potential regulatory spill-over to EU | Short term (≤ 2 years) |

| ER/OOH Access Gaps From Staffing Shortages Reduce Delivered Emergency Volumes | -0.5% | North America, rural regions globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Veterinary Services Inflation Elevates Price Sensitivity And Care Deferrals

Clinics reported that clients became more cost-sensitive through 2025, with visit counts easing and a larger share of cases declining recommended diagnostics as budgets tightened. Practices responded by shifting emphasis toward services less vulnerable to external price competition, while also using payment options and clearer estimates to sustain acceptance. Gross payroll as a percentage of revenue rose in 2025, reflecting tighter labor markets and competitive wages that keep pressure on service fees upward. These input costs and elevated client price sensitivity limit the headroom for further fee increases without risking additional volume erosion. The near-term result is a careful balance between margin protection and case acceptance, with clinics prioritizing diagnostic utilization and procedure bundling to hold revenue per visit steady. Over the forecast horizon, efficiency gains from scheduling, automation, and in-house testing help offset inflationary headwinds, but consumer affordability remains a governor on growth in mature markets.

UK CMA 2026 Remedies Cap Prescription Fees And Mandate Price/Ownership Transparency

On March 24, 2026, the UK Competition and Markets Authority finalized remedies requiring practices to cap written prescription fees at GBP 21 for the first medicine and GBP 12.50 for each additional item, publish comprehensive price lists online and in-clinic, provide itemized bills, disclose ownership, and give estimates for treatments expected to exceed GBP 500, with compliance required by September 23, 2026. For non-USD amounts noted in UK policy, the equivalent values are GBP 21 (USD 26.7), GBP 12.50 (USD 15.9), and GBP 500 (USD 635.0). The order aims to correct information asymmetries and perceived opacity in pricing and corporate ownership, particularly at large groups, by standardizing disclosures and empowering comparison. For hospitals, these rules may constrain prescription-related fee revenue while potentially increasing client trust and price-shopping behavior over routine services. The changes could also nudge clinics to reweight revenue mixes toward procedures and diagnostics, where differentiation is clearer, and comparison shopping is less straightforward. As other mature markets monitor outcomes, similar transparency frameworks could emerge elsewhere, reinforcing a shift toward standardized disclosures across the veterinary hospital market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Animal Type: Companion Animals Lead, Farm Animal Specialty Rising

Companion animals accounted for 64.32% of the veterinary hospital market share in 2025, supported by humanization trends and the propensity to fund diagnostics and specialty procedures for family pets. The veterinary hospital market size for companion animals is projected to expand at an 8.32% CAGR between 2026 and 2031, reflecting greater insurance usage and better access to advanced treatments. Clinics lean on embedded diagnostics and structured wellness plans to capture more of the care continuum for companion animals, anchoring repeat visits and adherence to chronic-disease monitoring. Multi-location operators have created care pathways that extend from primary care to specialty and emergency, which raises lifetime client value for dogs and cats.

Farm animal services remain a smaller share but are essential to biosecurity, food-safety oversight, and zoonotic-disease control, which makes demand steadier across cycles. Public programs and mandatory vaccination efforts underpin activity in livestock hubs, and they add countercyclical stability when discretionary companion-animal visits slow. Over time, digital recordkeeping and traceability requirements can lift the complexity of farm-animal casework, which encourages integrated lab capacity within regional hospital networks.

By Service Type: Surgical Services Ascend as Diagnostics Integrate

Medical services held 46.23% of 2025 revenue, reflecting the large base of routine diagnostics, chronic-disease management, and prescription therapeutics in the veterinary hospital market. The veterinary hospital market size for surgical services is projected to expand at an 8.58% CAGR through 2031 as clinics introduce advanced orthopedic and soft-tissue techniques alongside minimally invasive approaches. Diagnostic integration is raising per-visit yield and compressing time to treatment, and point-of-care innovation is helping general practices keep more workups in-house. IDEXX’s inVue Dx Cellular Analyzer and IDEXX Cancer Dx exemplify a pipeline that pairs AI with purpose-built assays to support earlier detection and confident case management at the point of care. In orthopedics, cranial cruciate ligament cases dominate canine surgery, and TPLO or TTA approaches preferred by specialty hospitals sustain higher fees and stronger margins than extracapsular alternatives. As surgical and diagnostic pathways are bundled within standardized care plans, throughput and profitability improve for locations equipped to deliver the full chain of services.

By Sector: Private Dominance, Public Stability in Livestock Hubs

The private segment accounted for 60.23% of 2025 revenues and continues to benefit from scale advantages in procurement, IT, and staffing that improve service breadth and consistency. The veterinary hospital market size for the private segment is forecast to grow at a 7.98% CAGR through 2031, as multi-location groups add specialty and emergency capacity that captures more complex casework. National Veterinary Associates has extended the reach of its Ethos specialty and emergency platform across North America, which builds deeper referral channels and anchors 24/7 access in dense markets. Chewy’s agreement to acquire Modern Animal illustrates how membership models and virtual care can couple with brick-and-mortar clinics to raise engagement and cross-category purchasing.

As private operators unify workflows and disclosures, client experience becomes more predictable across locations, which can lift retention. The private sector also tends to adopt diagnostic innovation early and to standardize care bundles that incorporate labs and imaging, adding resilience to revenue per visit. Public-sector and quasi-public services remain critical in livestock-intensive regions, anchoring disease surveillance, vaccination campaigns, and emergency response capacity. These mandates generate steady work streams that support regional labs and field operations regardless of consumer cycles.

Geography Analysis

North America accounted for 42.32% of 2025 revenues, reflecting a deep installed base of hospitals, early adoption of specialty and emergency models, and growing insurance coverage that supports acceptance of high-acuity care. In 2024, North American pet insurance covered 7.03 million pets, up 20.9% year over year, which raised the share of clients able to pursue full diagnostic workups and advanced procedures. Clinics used protocol nudges and integrated diagnostics to lift average transaction value even as visit volumes softened, a pattern tied to automation and tighter scheduling discipline. Practices also reported rising client sensitivity to pricing, with decreases in visits and more frequent declines of recommended care when budgets were tight. In response, hospitals emphasized injectable therapies and in-clinic services to mitigate exposure to online pharmacy competition while preserving per-visit yield.

Across Europe, consolidation and insurance penetration underpin access, while the UK’s 2026 CMA remedies introduce binding requirements for price publication, ownership disclosure, itemized billing, and capped written prescription fees at USD 26.7 for the first medicine and USD 15.9 for each additional item, with written estimates required for treatment plans expected to exceed USD 635.0 by the compliance date of September, 2026. The direction of reform is clear across mature European markets, with more attention on transparent pricing and clear ownership, especially within large networks. Enterprise groups continue to invest in specialty centers with advanced imaging and ICU capacity, positioning themselves to absorb compliance costs while maintaining integrated care models. The veterinary hospital market in Europe is likely to see a measured moderation in pricing power offset by improved client confidence and stable specialty demand that sustains revenue quality.

Asia-Pacific is projected to post the fastest expansion at an 8.93% CAGR through 2031, driven by urbanization, growing disposable incomes, and rising preventive-care adoption across Tier-1 and Tier-2 cities. Hospitals in leading metros are expanding capacity in diagnostics and imaging to meet demand from a widening pet-owning base. As local operators build referral pathways and add specialty clinics, more complex procedures migrate into regional centers that can staff and equip orthopedic, oncology, and emergency suites. Digital adoption in appointment booking and payments is accelerating, which lowers friction for wellness and recheck visits and helps hospitals optimize utilization. Over the forecast horizon, these structural tailwinds position Asia-Pacific as the primary growth engine for the global veterinary hospital market.

Competitive Landscape

Global competition remains fragmented, with a long tail of independent clinics and growing multi-location groups that invest in specialty services and 24/7 emergency access. Mars Petcare’s family of providers, along with other large operators, continues to shape client expectations around standardized care and referral depth. National Veterinary Associates is strengthening executive leadership to support the growth of its Ethos specialty and emergency network, with new appointments in 2025 aligned to scale and operational excellence. Chewy’s agreement to acquire Modern Animal illustrates a hybrid approach that fuses membership-based clinics, virtual care, and retail integration to increase cross-category engagement. These strategies deepen relationships through convenience and continuity, which improves retention and the capture of diagnostic and procedure revenue streams across the veterinary hospital market.

Regulation is reshaping parts of the competitive field, particularly in the UK, where the CMA’s 2026 order mandates prescription-fee caps and broad transparency requirements by late September 2026. Larger groups are positioned to absorb compliance overhead, aided by centralized IT and communications infrastructure. Over time, clear price lists and ownership disclosure may narrow perceived brand gaps, placing more emphasis on clinical quality, access breadth, and client experience. Networks that combine general practice with specialty and emergency care are likely to sustain a durable advantage, provided they maintain clinical depth and reliable access. The outcome is a market that rewards efficient, transparent, and integrated models across the veterinary hospital market.

Veterinary Hospital Industry Leaders

Mars, Incorporated

IVC Evidensia

CVS Group plc

National Veterinary Associates (NVA)

VetCor

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Wildlife Hospital of Louisiana announced strategic expansion to strengthen educational initiatives, conservation efforts, and community outreach programs.

- May 2025: Taverham Veterinary Hospital, part of IVC Evidensia, expanded in the United Kingdom, increasing its floor space by 240 square meters to address the growing demand for referral services in the Norwich region.

Global Veterinary Hospital Market Report Scope

The veterinary hospital market refers to the global industry comprising facilities that provide medical, surgical, diagnostic, and preventive healthcare services for animals. It includes services delivered to both companion animals and livestock through public and private institutions. The market’s value reflects revenue generated from veterinary treatments, consultations, procedures, and related healthcare services.

The veterinary hospital market report is segmented by animal type into companion animals and farm animals. By service type, the market includes surgical services, medical services, and consultation services. Based on sector, the market is categorized into private and public veterinary hospitals. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Companion Animals |

| Farm Animals |

| Surgical Services |

| Medical Services |

| Consultation |

| Private |

| Public |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Animal Type | Companion Animals | |

| Farm Animals | ||

| By Service Type | Surgical Services | |

| Medical Services | ||

| Consultation | ||

| By Sector | Private | |

| Public | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and outlook for the veterinary hospital market through 2031?

The veterinary hospital market was USD 67.26 billion in 2025, is estimated at USD 71.02 billion in 2026, and is projected to reach USD 99.22 billion by 2031 at a 6.91% CAGR.

Which service categories are driving the most growth in the veterinary hospital market?

Surgical services are the fastest growing with an 8.58% CAGR through 2031, supported by orthopedic and oncology procedures, while diagnostics continue to lift per-visit revenue through tighter protocol integration.

What role do corporate groups play in the veterinary hospital market?

Enterprise operators fund specialty build-outs, emergency hubs, and standardized workflows, and they are adding integrated models that blend membership clinics and virtual care to deepen engagement and improve utilization.

Which regions show the strongest growth trajectory over the forecast period?

Asia-Pacific is projected to record the fastest expansion at an 8.93% CAGR to 2031, supported by urbanization, rising disposable incomes, and growing preventive-care adoption across Tier-1 and Tier-2 cities.

How might regulation change competitive dynamics in mature markets?

The UK's 2026 CMA order capping prescription fees, mandating price lists, itemized bills, and ownership disclosure is likely to reinforce transparency and trust, while nudging clinics to focus more on differentiated services.

Page last updated on: