Vasopressin For Vasoplegic Shock Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

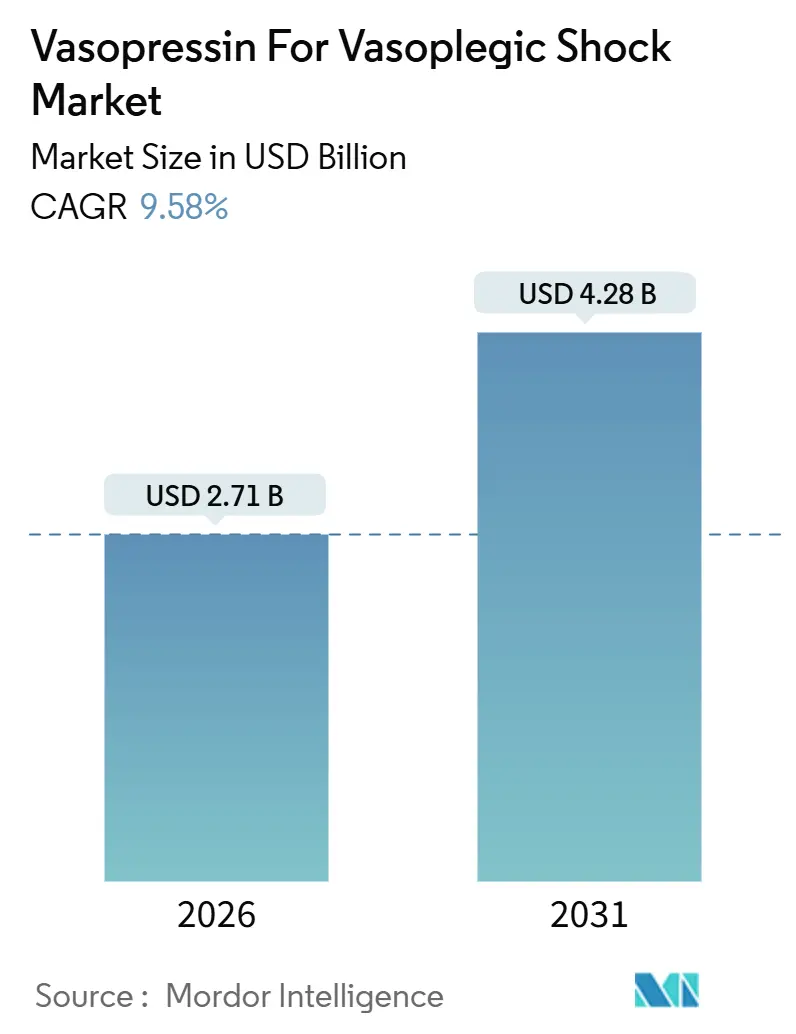

| Market Size (2026) | USD 2.71 Billion |

| Market Size (2031) | USD 4.28 Billion |

| Growth Rate (2026 - 2031) | 9.58% CAGR |

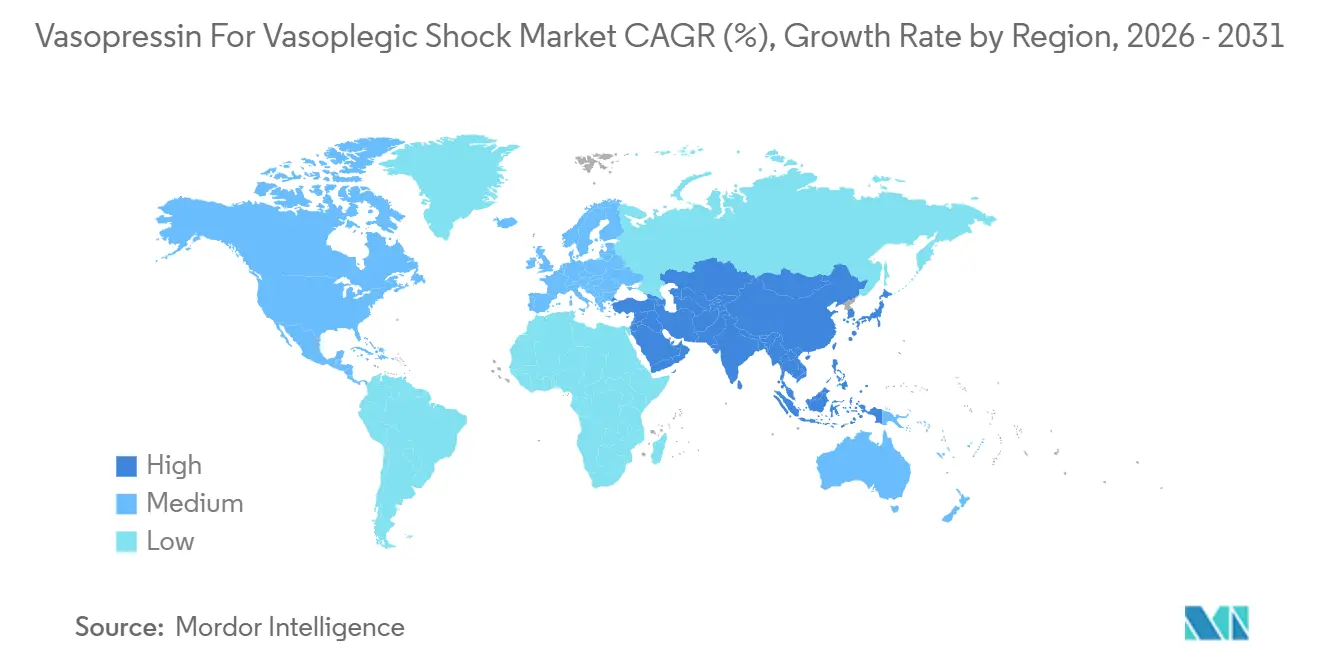

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vasopressin For Vasoplegic Shock Market Analysis by Mordor Intelligence

The Vasopressin For Vasoplegic Shock Market size is estimated at USD 2.71 billion in 2026, and is expected to reach USD 4.28 billion by 2031, at a CAGR of 9.58% during the forecast period (2026-2031).

Robust, protocol-driven resuscitation pathways, expansion of minimally invasive cardiac surgery, and alignment of Medicare reimbursement collectively accelerate adoption. Injectable solutions continue to dominate, yet lyophilized powder, favored for room-temperature stability, is gaining ground. Closed-loop smart pumps automate titration, boosting continuous-infusion use, while ambulatory surgical centers (ASCs) emerge as the fastest-growing care setting. The North American lead persists thanks to domestic peptide capacity and payer coverage, but Asia-Pacific is expanding even faster on the back of Chinese and Indian generic output. Competitive intensity centers on supply-chain resilience rather than molecular innovation, with API shortages and the rise of angiotensin II representing headline risks.

Key Report Takeaways

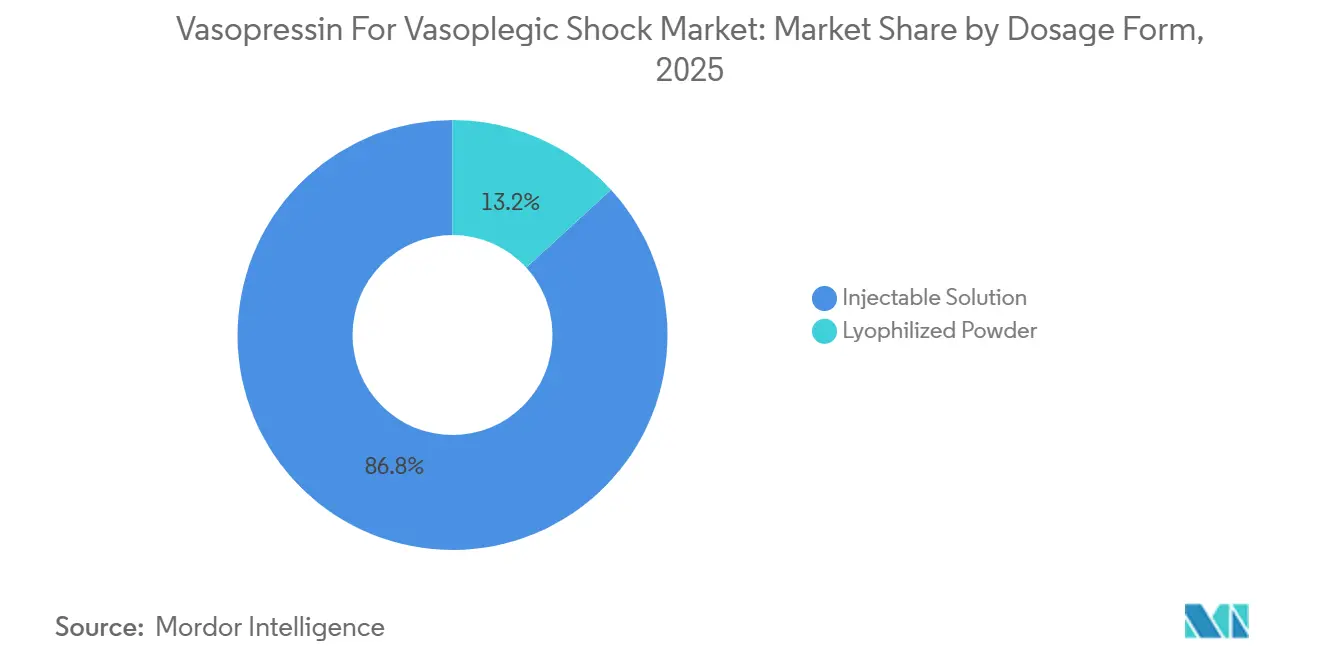

- By dosage form, injectable solutions held 86.81% of the vasopressin market share for vasoplegic shock in 2025, whereas lyophilized powder is set to expand at a 10.30% CAGR through 2031.

- By route of administration, continuous infusion accounted for 65.57% of the vasopressin market for vasoplegic shock in 2025 and is projected to grow at a 11.31% CAGR to 2031.

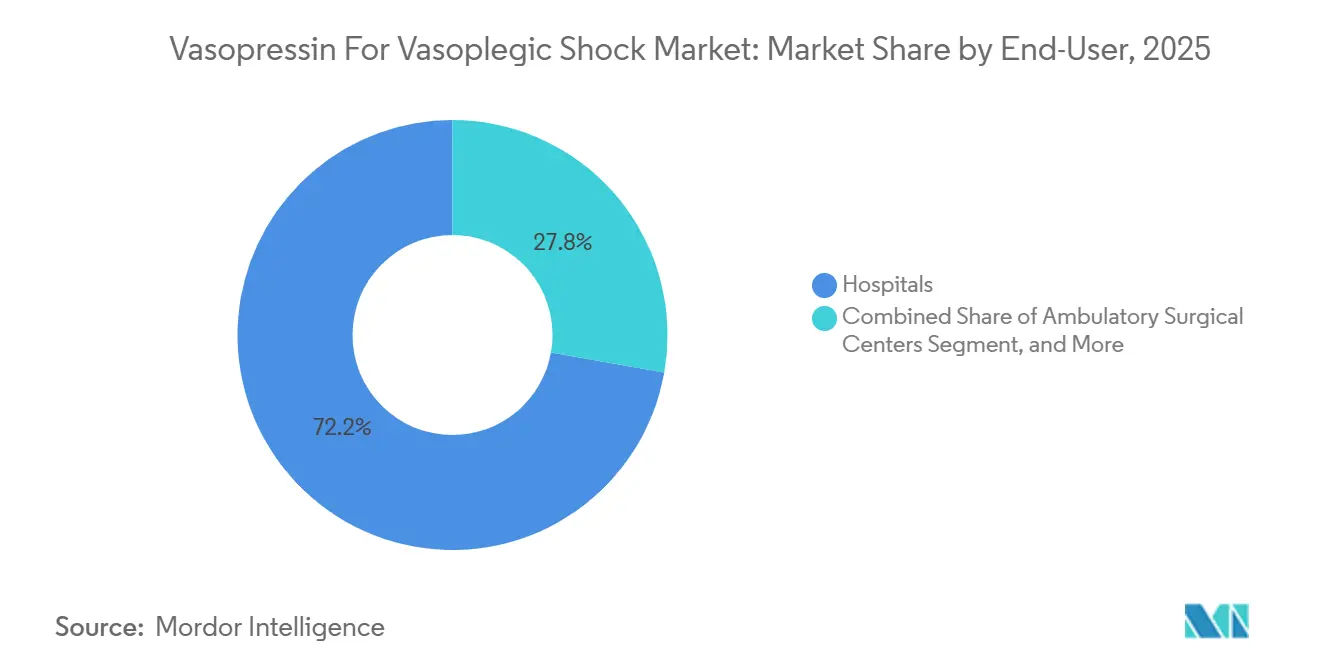

- By end user, hospitals captured 72.22% of revenue in 2025, while ASCs are forecast to record a 12.09% CAGR through 2031.

- By geography, North America led with 46.83% revenue in 2025, while Asia-Pacific is poised to grow at a 14.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vasopressin For Vasoplegic Shock Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Short-supply of norepinephrine-resistant therapeutics | +1.8% | North America, EU | Short term (≤ 2 years) |

| Protocol-driven peri-operative management | +1.5% | North America, EU, expanding to APAC hubs | Medium term (2-4 years) |

| Rising cardiac-surgery volumes | +1.6% | China, India, Japan, North America, Western EU | Long term (≥ 4 years) |

| Formulary tilt toward cost-effective generics | +1.3% | Global, strongest in U.S., India, China | Medium term (2-4 years) |

| Shelf-stable lyophilized presentations | +1.4% | Rural North America, APAC tier-2 cities | Medium term (2-4 years) |

| Closed-loop smart-pump algorithms | +1.2% | Early adopters in North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Short-Supply of Norepinephrine-Resistant Vasoplegic Shock Therapeutics

Vasopressin fills a critical gap when catecholamines fail. The 2025 ESICM guidelines recommend it as the preferred adjunct, citing lower arrhythmia risk at high norepinephrine doses.[1]European Society of Intensive Care Medicine, “ESICM Guidelines on Shock Management 2025,” ESICM.ORG Roughly 25% of cardiopulmonary-bypass cases develop refractory vasoplegia, and the 2024 European Best Practice in Cardiopulmonary Bypass (EBCP) guidelines embed vasopressin into pre-printed order sets, boosting hospital utilization by 30-40% in the first year of adoption. This shift from episodic rescue use to protocol-mandated therapy stabilizes demand and shields the vasopressin for vasoplegic shock market from competitive erosion.

Growing Adoption of Protocol-Driven Peri-Operative Hemodynamic Management

Standardized bundles now guide vasopressor escalation. The 2024 ANDROMEDA-SHOCK-2 protocol adds vasopressin if the capillary refill time exceeds 4.5 s despite adequate norepinephrine.[2]Critical Care Medicine, “ANDROMEDA-SHOCK-2 Protocol,” CCMJOURNAL.COM French SFAR guidelines echo this directive and have led hospitals to sign multi-year bulk contracts. Automation lets nurses initiate therapy once electronic records flag criteria, extending vasopressin use into step-down and post-anesthesia units.

Rising Cardiac-Surgery Volumes in Rapidly Ageing Populations

Valve replacement and CABG procedures are on the rise. Japan’s health ministry says patients aged≥75 accounted for 42% of cardiac surgeries in 2024, up from 35% in 2020. China tallied a 19% year-on-year jump in CABG in 2024, mostly in tier-1 centers adopting Western protocols. Because guidelines now recommend earlier vasopressin initiation, each incremental surgery translates into higher drug consumption, compounding demand growth.

Improved Shelf-Stable Lyophilized Presentations Enabling Wider ICU Penetration

Lyophilized powder doubles shelf life to 36 months at room temperature, letting small hospitals avoid refrigerated write-offs. USP Chapter 1207 favors such products due to simpler beyond-use compliance. Robotic dispensers store ambient vials more efficiently, while rural budgets benefit from lower wastage. These factors underpin the dosage form’s above-market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recurring peptide-API shortages | -0.9% | North America, EU, global spillover | Short term (≤ 2 years) |

| Interest in non-catechol alternatives | -0.7% | North America, EU, early APAC adoption | Medium term (2-4 years) |

| Restrictive septic-shock guidelines | -0.8% | North America, EU | Medium term (2-4 years) |

| Pending USP bulk-peptide revisions | -0.6% | North America, EU manufacturers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Recurring API Shortages Linked to Limited Peptide Synthesis Capacity

With fewer than 50 global plants capable of producing commercial-scale peptide APIs, single-site outages ripple across the globe. ASHP listed vasopressin in shortage in March 2025 after a Fresenius Kabi plant disruption, forcing 30% hospital allocation cuts.[3]American Society of Health-System Pharmacists, “Current Drug Shortages: Vasopressin,” ASHP.ORG FDA data show peptide shortages last 18 months on average, compared with small-molecule gaps, which last 9 months on average. Such bottlenecks curtail volume growth and push hospitals back toward higher-dose catecholamines.

Growing Interest in Non-Catechol Alternatives Such as Angiotensin II

Angiotensin II (Giapreza) activates AT1 receptors, bypassing vasopressin pathways. A 2024 Italian Delphi consensus recommends it when vasopressin-norepinephrine fails within 6 hours. Real-world ATHOS-3 data show a 69% MAP success rate in patients with triple-refractory disease. Although therapy costs USD 1,200, compared with USD 40-60 for vasopressin, value-based contracts are narrowing the gap. Capturing even 10% of refractory cases could dent premium demand segments by 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Dosage Form: Lyophilized Powder Gains on Logistics Advantage

Injectable solutions dominated the vasopressin market share for vasoplegic shock in 2025, with 86.81%. Lyophilized powder, however, is forecast to grow at a 10.30% CAGR, benefiting facilities lacking cold-chain infrastructure. The USP Chapter 797 overhaul tightened beyond-use limits for compounded liquids, accelerating conversion to FDA-approved powder vials. Community hospitals in rural North America and tier-2 APAC cities now favor lyophilized stock to curb wastage and labor-intensive refrigeration. Large tertiary centers still opt for liquids because pharmacy automation already integrates chilled storage. This divergence means that dosage-form preference will increasingly correlate with facility scale rather than with clinical indication.

The price premium of 15-20% per vial for lyophilized powder is offset by fewer expiries. Adoption is further propelled by robotic dispensers that retrieve room-temperature vials faster than refrigerated ones. Meanwhile, the vasopressin for vasoplegic shock market for injectable solutions continues to expand in absolute terms, but at a slower pace, as guideline neutrality toward dosage form leaves cost of ownership as the deciding factor.

By Route of Administration: Continuous Infusion Dominates, Bolstered by Smart Pumps

Continuous IV infusion held a 65.57% share of the vasopressin for vasoplegic shock market in 2025 and is projected to grow at a 11.31% CAGR to 2031, driven by closed-loop algorithms that auto-titrate dosage based on real-time arterial pressure. Smart pumps minimize human error and smooth hemodynamics, aligning with ESICM recommendations for a 0.03-0.04 unit/minute baseline. Intermittent bolus remains common only in emergency departments managing variceal bleeds. Hospitals adopting the ANDROMEDA-SHOCK-2 protocol report 25-30% fewer vasopressor-related adverse events, underscoring the superiority of infusion.

As smart-pump penetration rises above 70% in U.S. ICUs, continuous infusion’s share could exceed 75% by 2030. Bolus dosing will persist in niche indications where pump setup time is prohibitive. No regulatory body mandates specific routes, leaving institutional protocols to drive continued growth in infusion.

By End-User: Ambulatory Surgical Centers Emerge as Growth Frontier

Hospitals accounted for 72.22% of revenue in 2025, buttressed by complex cardiac and septic shock care. ASCs, however, are expanding at 12.09% CAGR. Medicare’s 2024 addition of transcatheter aortic valve replacement to the ASC list forces these centers to stock vasopressors for same-day discharge patients. Low case volumes mean ASCs favor single-agent solutions with broad indication coverage, positioning vasopressin favorably against narrower catecholamines. Academic medical centers, though smaller, pioneer investigational protocols such as SEPSIS-BRAIN, which are later adopted community-wide.

The vasopressin market for vasoplegic shock tied to ASCs could double by 2031 as outpatient valve interventions proliferate. Hospitals will retain a dominant share thanks to emergent septic-shock volumes, yet the site-of-care migration signals a structural change in distribution channels rather than diminished overall demand.

Geography Analysis

North America led with 46.83% of revenue in 2025, underpinned by Medicare coverage and FDA-mitigation rules that prioritize domestic peptide synthesis. The Society of Thoracic Surgeons embedded vasopressin into 2024 cardiac-surgery order sets, spurring predictable bulk purchases across 1,100-plus U.S. hospitals. Canada’s provincial formularies negotiated 18-22% price cuts in 2025 and expanded crash-cart stocking. Mexico’s IMSS guidelines newly recommend vasopressin for distributive shock, unlocking fresh demand in public hospitals.

Asia-Pacific is the fastest-growing region, slated for a 14.93% CAGR through 2031. China recorded a 19% year-on-year surge in CABG procedures in 2024, and CDSCO cleared three generic vasopressors in India, triggering price competition. Japan’s strict reimbursement confines use to cardiac-surgery vasoplegia, yet an aging cohort sustains baseline volumes. South Korea added vasopressin to its 2024 essential-drug list, driving 35% uptake within six months.

The 2024 EBCP guidelines unified vasoplegia protocols across member states, stimulating cross-border generic launches via EMA’s centralized pathway. Germany, the UK, and France dominate regional demand thanks to sizable cardiac-surgery caseloads. Middle East & Africa and South America remain smaller, constrained by limited surgical infrastructure, though Saudi Arabia and the UAE are upgrading tertiary care capacity under national health transformation agendas.

Competitive Landscape

The top five firms, Fresenius Kabi, Baxter, Pfizer, Hikma, and Par Pharmaceutical, held an estimated significant share in 2025, giving the vasopressin for vasoplegic shock market a moderate concentration. Competition revolves around supply-chain resilience; molecule differentiation is moot because the peptide is off-patent. GPO contracts lock in multi-year volumes, making inspection track records decisive. Vertically integrated players such as Amphastar and Eagle hedge against API shortages by synthesizing in-house. The ASHP’s March 2025 shortage alert highlighted single-site risks, prompting GPOs to diversify sources even at higher unit prices.

White-space lies in three niches: bundled ASC kits pairing vasopressin vials with infusion sets, closed-loop pump integration with pre-validated drug libraries, and lyophilized SKUs tailored for rural facilities and APAC tier-2 cities. Pending USP bulk-peptide revisions will escalate compliance costs, likely consolidating upstream synthesis among better-capitalized actors. Patent activity now focuses on combination bags and auto-injectors rather than new analogs, signaling that future advantage will stem from manufacturing agility rather than R&D breakthroughs.

Vasopressin For Vasoplegic Shock Industry Leaders

Amneal Pharmaceuticals

Sun Pharmaceutical

Amneal Pharmaceuticals

Pfizer Inc.

Gland Pharma

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Gland Pharma obtained FDA clearance for ready-to-use Vasopressin Injection in 5% dextrose, covering 40 Units/100 mL vials and granting tentative approval for 20 Units/100 mL vials.

- December 2024: Endo received FDA approval to commercialize Vasostrict at its new aseptic site in Indore, India, adding 20,000 ft² of sterile capacity

Global Vasopressin For Vasoplegic Shock Market Report Scope

The Vasopressin for Vasoplegic Shock Market encompasses the global commercial market for vasopressin preparations specifically indicated, used off-label, or studied for the management of vasoplegic/vasodilatory shock.

The Vasopressin for Vasoplegic Shock Market Report is Segmented by Dosage Form (Injectable Solution, Lyophilized Powder), Route of Administration (Intravenous Bolus, Continuous IV Infusion), End-user (Hospitals, Ambulatory Surgical Centers, Academic Medical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Injectable Solution |

| Lyophilized Powder |

| Intravenous Bolus |

| Continuous IV Infusion |

| Hospitals |

| Ambulatory Surgical Centers |

| Academic Medical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Dosage Form | Injectable Solution | |

| Lyophilized Powder | ||

| By Route of Administration | Intravenous Bolus | |

| Continuous IV Infusion | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centers | ||

| Academic Medical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is forecast for vasopressin sales through 2031?

The vasopressin for vasoplegic shock market is projected to expand at a 9.58% CAGR from 2026 to 2031.

Which dosage form is growing fastest?

Lyophilized powder is forecast to grow at a 10.30% CAGR, outpacing injectable solutions due to room-temperature stability.

Why are ASCs becoming important buyers?

Medicare now reimburses outpatient TAVR, requiring ASCs to stock vasopressin for same-day cardiac procedures, driving a 12.09% CAGR in that channel.

How do API shortages affect drug availability?

Limited global peptide synthesis capacity leads to prolonged shortages, forcing hospitals to ration vasopressin and seek multiple suppliers.

Which region shows the fastest growth?

Asia-Pacific is projected to register a 14.93% CAGR, propelled by rising cardiac surgeries in China and India and expanded generic manufacturing.

Page last updated on: