Oil and Gas Valves Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

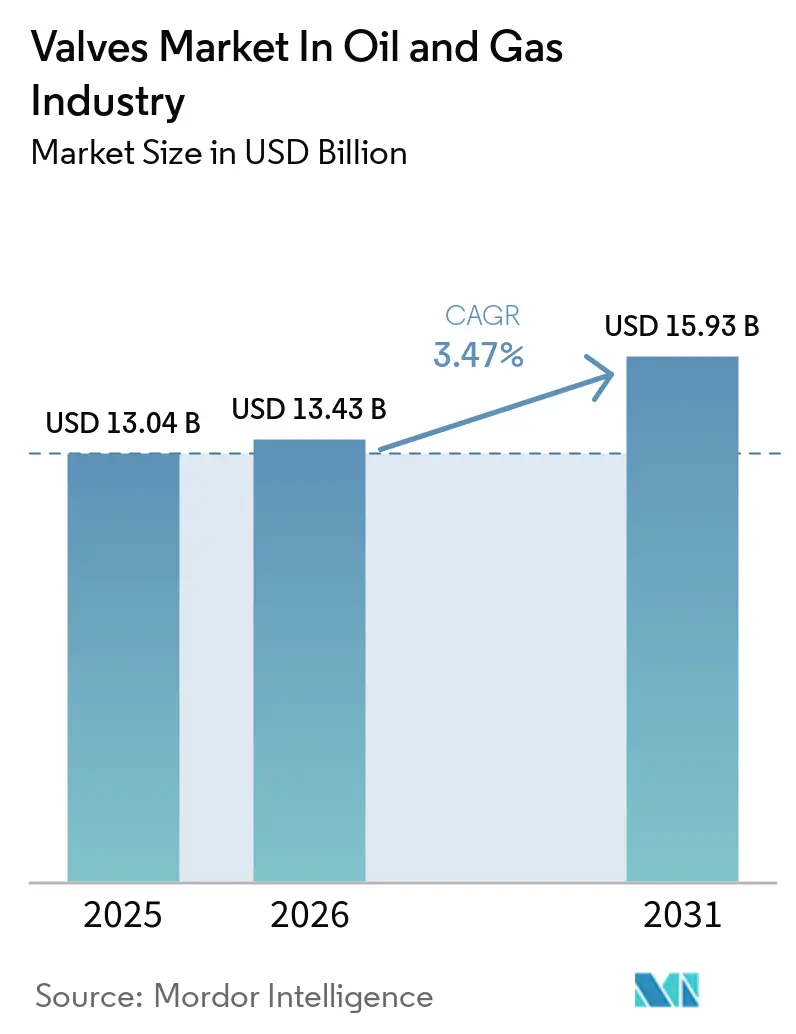

| Market Size (2026) | USD 13.43 Billion |

| Market Size (2031) | USD 15.93 Billion |

| Growth Rate (2026 - 2031) | 3.47% CAGR |

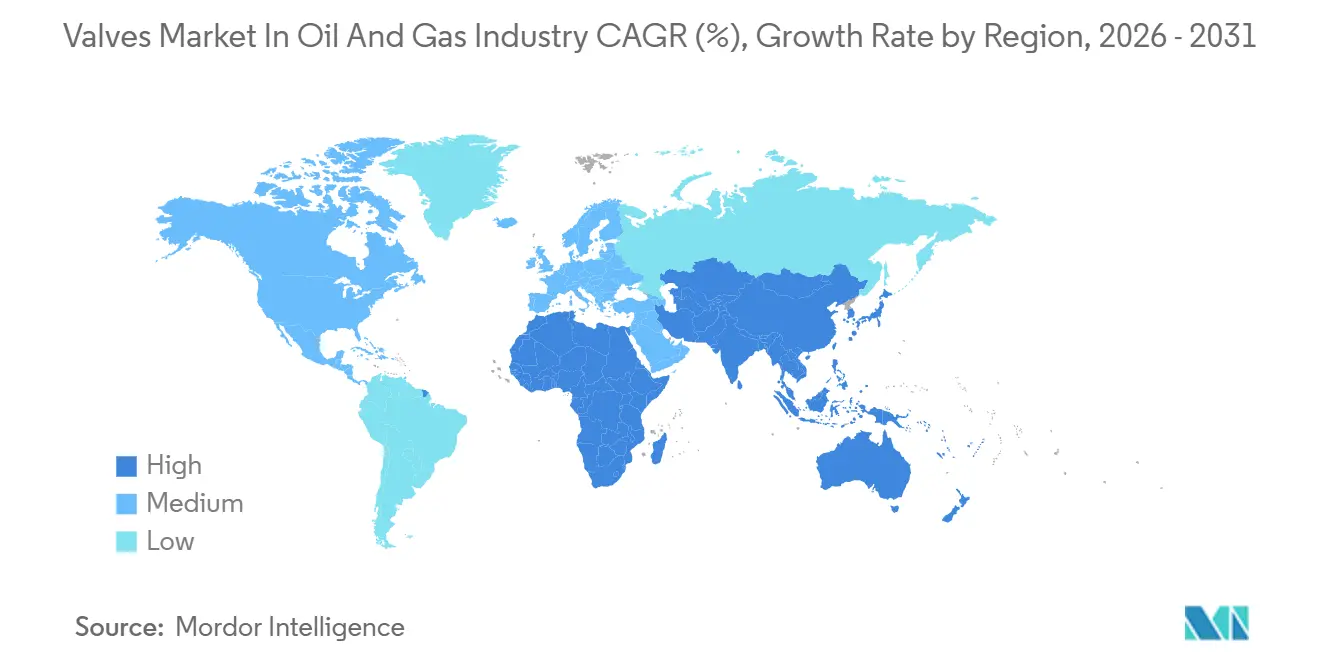

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oil and Gas Valves Market Analysis by Mordor Intelligence

The Oil and Gas Valves Market size is expected to grow from USD 13.04 billion in 2025 to USD 13.43 billion in 2026 and is forecast to reach USD 15.93 billion by 2031, advancing at a 3.47% CAGR. This steady expansion reflects capital flowing back into long-cycle upstream projects, a surge of new liquefied-natural-gas facilities, and the fast spread of smart-valve retrofits. Operators are investing in hydrogen-ready metallurgy to future-proof assets, yet remain disciplined in project selection amid oscillating Brent prices. Digital-twin rollouts and strict methane-leak regulations are driving demand for low-emission control valves, while heightened cybersecurity risks are spurring orders for secure electric actuators. Asia-Pacific and the Middle East dominate new installations, whereas North America drives upgrades that stretch asset life.

Key Report Takeaways

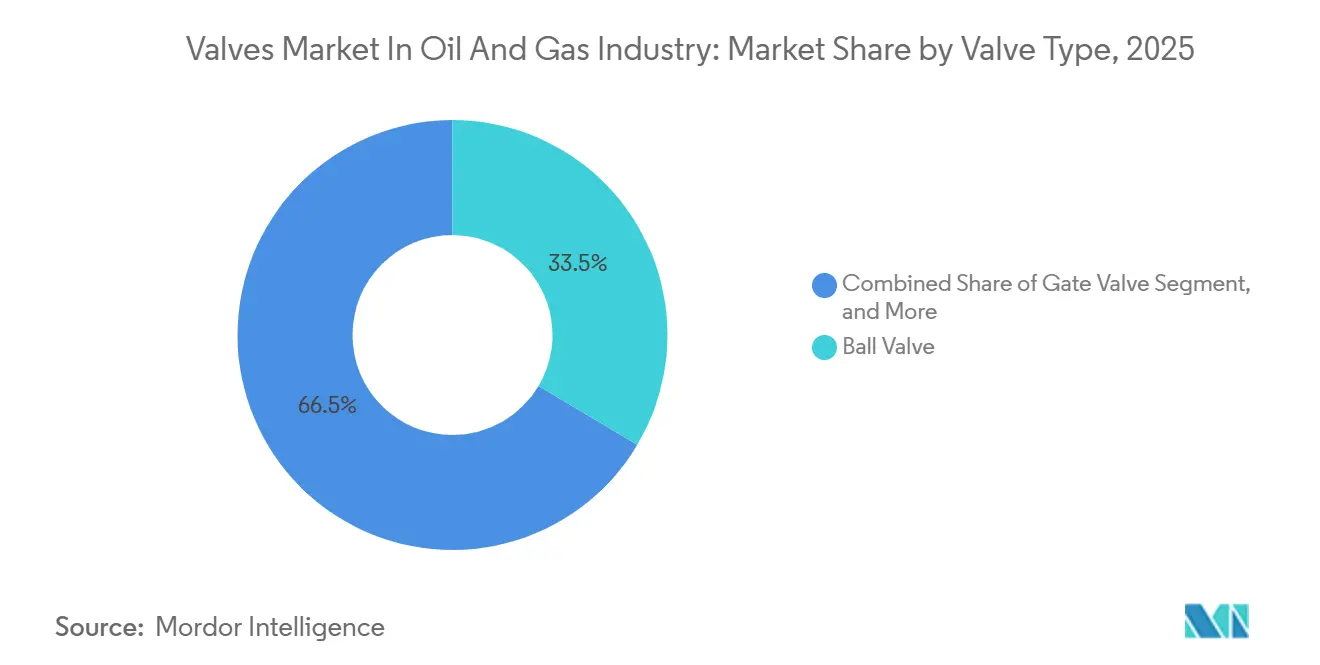

- By valve type, control valves are forecast to expand at a 5.12% CAGR through 2031; ball valves held 33.53% of the oil and gas industry's valve market share in 2025.

- By material, cast steel accounted for 27.31% of the oil and gas industry's valve market in 2025, while alloy and duplex steels are poised to grow at a 4.72% CAGR to 2031.

- By application, midstream captured 38.09% revenue share in 2025; LNG facilities are set to rise at a 4.32% CAGR through 2031.

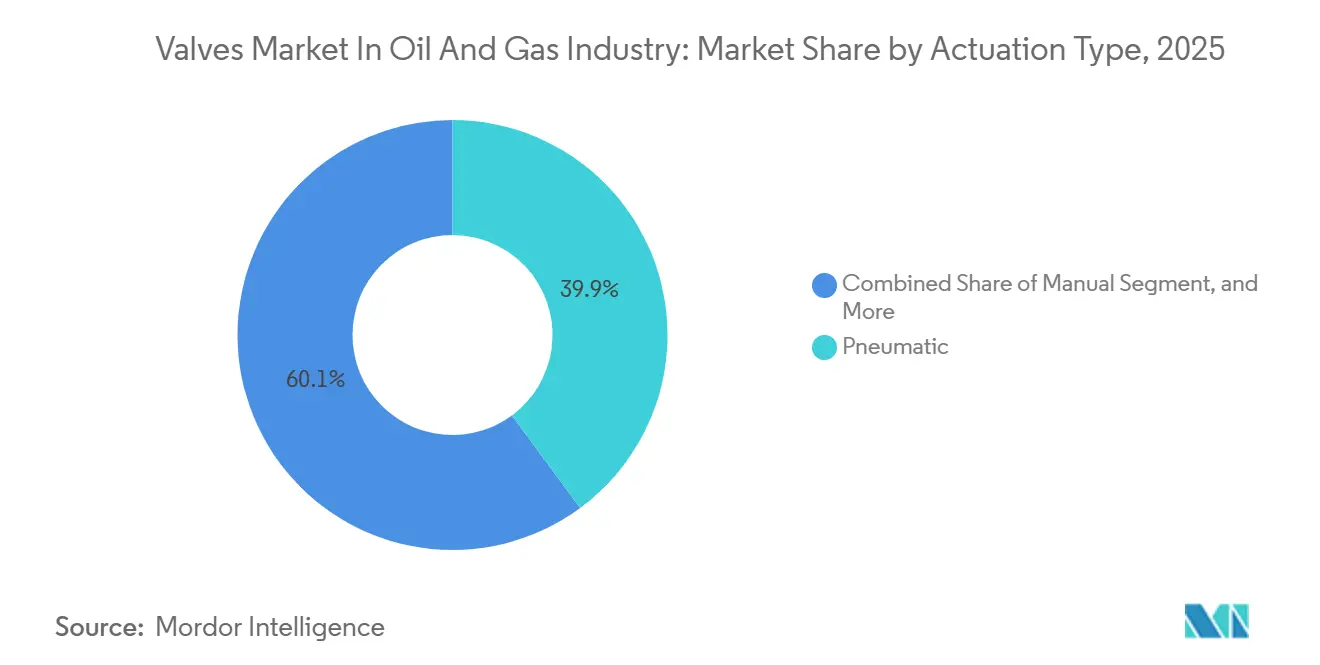

- By actuation, pneumatic units dominated with a 39.87% share in 2025, and electric actuation is projected to register a 4.21% CAGR to 2031.

- By size, the 6-to-12-inch class held 32.94% share in 2025, whereas valves above 24 inches are projected to grow at a 4.01% CAGR to 2031.

- By region, Asia-Pacific led with a 41.09% share in 2025; the Middle East is anticipated to post the fastest regional CAGR at 4.76% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Oil and Gas Valves Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Upstream and Midstream Pipeline Projects | +0.9% | Asia-Pacific, Middle East, North America | Medium term (2-4 years) |

| Surge in LNG Terminal Constructions | +0.8% | Middle East, Asia-Pacific, North America | Medium term (2-4 years) |

| Accelerating Adoption of Digital and Smart Valves | +0.6% | North America, Europe, Global | Long term (≥ 4 years) |

| Stringent Global Safety and Emission Regulations | +0.5% | Europe, North America, Global | Long term (≥ 4 years) |

| Hydrogen-Ready Valve Designs for Energy Transition | +0.4% | Europe, North America, Asia-Pacific hubs | Long term (≥ 4 years) |

| Aging Offshore Assets Requiring Valve Retrofits | +0.3% | North Sea, Gulf of Mexico, West Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Upstream And Midstream Pipeline Projects

Upstream spending rebounded to USD 570 billion in 2025 despite a 4% year-over-year dip, and analysts see an upswing to USD 738 billion by 2030.[1]International Energy Agency, “Oil and Gas Investment,” iea.org Deepwater programs in Brazil and unconventional gas in Saudi Arabia are locking in multi-year contracts for high-pressure gate and ball valves rated for sour service.[2]Baker Hughes Company, “Energy Transition and LNG Solutions,” bakerhughes.comMidstream growth is similar, as Enbridge approved a USD 1.4 billion gas line in 2024 while ADNOC funded a USD 2.4 billion seawater-injection network that requires corrosion-resistant check valves. China’s national grid is adding 48-inch trunk lines, boosting demand for valves above 24 inches. Compliance with API 6D and ISO 15848 is now standard procurement language.

Surge In LNG Terminal Constructions

Roughly 300 billion m³ per year of new liquefaction capacity is scheduled for completion by 2030, led by 80 billion m³ sanctioned in the United States during 2025. QatarEnergy’s USD 30 billion North Field expansion raises capacity to 126 million tpa and needs thousands of cryogenic ball and triple-offset butterfly valves engineered for −196 °C duty. Import terminals across India, Vietnam, and the Philippines prefer suppliers with local inventory and API 6FA fire-testing certification from Baker Hughes. Alloy and duplex steels, growing at a 4.72% CAGR, counter thermal-cycling damage inherent in LNG service. Local after-sales clauses in EPC contracts raise barriers for distant vendors.

Accelerating Adoption Of Digital And Smart Valves

Industrial IoT rollouts convert valves into data sources for predictive maintenance. Emerson embedded edge processors in its 2024 ASCO electric dump valve, streaming actuator health to cloud dashboards. Schlumberger’s Sensia venture cut valve downtime 18% at Middle Eastern gas plants through machine-learning diagnostics. Rotork’s Bluetooth-enabled IQ3 actuator is popular on unmanned platforms. Electric actuation, projected to grow at a 4.21% CAGR, integrates smoothly with distributed control systems for finer positioning than pneumatic systems. Cyber threats follow connectivity, prompting operators to harden networks after CISA advisories in 2024.

Stringent Global Safety And Emission Regulations

API updated its 607 fire test in 2024, lengthening burn duration for soft-seated ball valves. The European Union Methane Regulation now obliges operators to quantify valve-stem leakage, propelling retrofits with ISO 15848-qualified packing. The United States extended leak-detection rules to gathering pipelines in 2024, enlarging the market for smart-valve platforms. China floated draft methane guidelines in 2025, while India mandated API 6D for all new pipelines in 2024. Higher penalties for non-compliance shift budgets toward premium low-emission designs that lower life-cycle costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude Oil Price Volatility Dampening CAPEX | -0.8% | North America shale, offshore regions | Short term (≤ 2 years) |

| Intensifying Shift Toward Renewable Energy | -0.6% | Europe, North America, Global | Long term (≥ 4 years) |

| Alloy and Stainless-Steel Cost Spikes from Trade Tariffs | -0.4% | North America, Europe | Medium term (2-4 years) |

| Rising Cybersecurity Risks in Connected Valve Networks | -0.3% | Digitally advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Crude Oil Price Volatility Dampening CAPEX

Brent fluctuated between USD 70 and USD 90 per barrel in 2024-2025, stalling final investment decisions and trimming valve orders for marginal projects.[3]International Energy Agency, “Oil and Gas Investment,” iea.org Upstream spending slipped 4% year over year to USD 570 billion in 2025, as shale operators favored free cash flow over growth. Permian producers deferred tie-ins, softening demand for wellhead valves, while North Sea and Gulf of Mexico assets leaned toward decommissioning rather than costly subsea replacements. Downturns shrink order books faster than recoveries expand them because operators hesitate to carry spare inventory. Suppliers thus face cyclic revenue swings that complicate production planning.

Intensifying Shift Toward Renewable Energy

Renewable-energy investment hit USD 1.9 trillion in 2024, nearly triple the USD 700 billion flowing to oil and gas supply. BP, Shell, and TotalEnergies pledged to cut hydrocarbon production before 2030, reducing greenfield valve demand. Europe’s Fit for 55 package accelerates coal retirements and lowers natural-gas reliance, trimming future orders for transmission-pipeline isolation valves. Valve OEMs are diversifying into hydrogen and carbon-capture services, but standards and volumes remain nascent, limiting near-term revenue replacement. High-pressure hydrocarbon expertise transfers only partially to low-pressure renewable flows, pressing firms to redesign portfolios and pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Valve Type: Control Valves Gain Ground In Automated Facilities

Control valves, aided by digital twins, are expected to advance at a 5.12% CAGR, outpacing the overall Oil and Gas Valves Market. Ball valves retained a 33.53% share in 2025 for on-off isolation, while gate valves dominate in high-pressure drilling and subsea trees. Plug and butterfly valves carve out niches in abrasive slurries and large-diameter low-pressure lines. The oil and gas industry's control valve market is projected to expand as predictive analytics sharpen throughput optimization.

Predictive maintenance keeps control-valve uptime high, compelling operators to specify ISO 15848 fugitive-emission ratings alongside API 607 fire testing. Electric actuation improves throttling accuracy, reinforcing the growth of control valves. Competitive entry barriers rise with each new standard, safeguarding incumbents that boast global test facilities and digital-service suites.

By Material: Alloy And Duplex Steels Rise In Corrosive Environments

Cast steel held a 27.31% share in 2025, but alloy and duplex steels are forecast to grow 4.72% annually as sour-gas and hydrogen blends require enhanced corrosion resistance. Duplex grades now line Qatar’s expanded North Field process trains, while nickel alloys equip Emerson’s HV-7000 hydrogen regulator. The oil and gas industry's alloy steel valve market share is set to increase as NACE MR0175 compliance becomes routine.

Forged steel remains vital for 10,000 psi wellheads, whereas composite bodies are used for low-pressure, highly corrosive amine units. Positive material identification and mill test reports are mandatory, adding administrative cost that favors established suppliers with integrated metallurgy labs.

By Application: LNG Facilities Outpace Midstream Growth

Midstream assets accounted for 38.09% of revenue in 2025, yet LNG facilities are on track for a 4.32% CAGR through 2031. The Oil and Gas Valves Market benefits from the United States projects approved in 2025 and QatarEnergy’s investment surge. LNG duty cycles demand cryogenic integrity, boosting control-valve content per train.

Upstream demand rides deepwater and unconventional plays, though muted North American shale drilling constrains volume. Downstream refinery retrofits keep globe-valve sales steady for high-temperature services. Emerging hydrogen pipelines are too small today to displace core LNG spending, but they represent an option for valve OEMs.

By Actuation Type: Electric Gains In Remote Operations

Pneumatic systems held a 39.87% share in 2025, but electric actuators are forecast at a 4.21% CAGR as unmanned facilities favor plug-and-play digital integration. The Oil and Gas Valves Market is growing, driven by electric actuation, Bluetooth diagnostics, and over-the-air updates that slash helicopter trips to offshore platforms.

Fail-safe behavior still gives pneumatics an edge in hazardous zones where compressed air is plentiful. Manual gearboxes linger in low-criticality lines but are being replaced by small electric drives as ergonomic rules tighten. Hydraulic and electro-hydraulic units keep their niche in high-torque subsea trees.

By Size: Large-Diameter Valves Serve Trunk Pipelines And LNG

The 6-to-12-inch class accounted for 32.94% of the market in 2025, yet valves above 24 inches are due for a 4.01% CAGR, riding China’s 48-inch trunk lines and the United States export pipes. Large-bore butterfly and ball valves handle LNG feed-gas headers where throughput matters more than footprint.

Smaller-than-6-inch valves dominate instrumentation loops but face price pressure from high-volume Asian foundries. The Oil and Gas Valves Market gains diversification as 12-to-24-inch units populate compressor stations, bridging the size gap while meeting API 6D and ISO 15848 mandates.

Geography Analysis

Asia-Pacific generated 41.09% of 2025 revenue, anchored by China’s pipeline-grid integration and India’s city-gas buildout. National Pipeline Network Company deploys 48-inch mains, raising the need for duplex-steel butterfly valves, while India’s regulator demands API 6D compliance, shutting out low-spec imports.[4]Petroleum and Natural Gas Regulatory Board, “Pipeline Standards and Regulations,” pngrb.gov.in Japan and South Korea pursue hydrogen pilots, creating niche orders for nickel-alloy trim. Southeast Asian LNG import terminals are adding regas capacity but advancing slowly due to financing hurdles.

The Middle East is projected to have a 4.76% CAGR to 2031. QatarEnergy’s North Field expansion specifies thousands of cryogenic valves engineered for minus 196 °C, and Saudi Arabia’s Jafurah tight-gas development calls for hydrogen-sulfide-resistant duplex-steel trim. ADNOC’s seawater-injection network demands corrosion-proof check valves for high-salinity fluids. Regional national-oil-company funding shields projects from crude swings, sustaining predictable order flows.

North America focuses on LNG export trains along the Gulf Coast and takeaway pipelines leaving the Permian Basin. The United States sanctioned 80 billion m³ per year of liquefaction capacity in 2025, triggering demand for large-diameter isolation valves. Meanwhile, the decommissioning of aging Gulf of Mexico platforms sustains retrofit activity for subsea isolation valves. Europe’s market contracts amid declining hydrocarbon volumes, yet pivots to hydrogen blends and carbon-capture projects that require high-pressure CO₂ valves. South America depends on Brazil’s pre-salt fields and Argentina’s Vaca Muerta infrastructure, while Africa’s growth hinges on Nigerian gas monetization and Mozambique LNG, tempered by political risk.

Competitive Landscape

Tier-one suppliers Emerson Electric, Flowserve, and Baker Hughes integrate valves, actuators, and digital services, securing framework contracts with super-majors. Baker Hughes closed the USD 13.6 billion acquisition of Chart Industries in July 2025, accelerating its LNG and hydrogen product suite. Flowserve added severe-service capacity by buying MOGAS for USD 290 million in August 2024, sharpening its edge in refinery coking units. Rotork’s USD 775 million Mastergear acquisition in October 2024 brings high-torque electric gearboxes that target large-diameter pipeline valves.

Smaller challengers differentiate through modular trim and specialty metallurgy. Neway Valve’s 2024 interchangeable-seat platform reduces spare parts inventory for operators. Parker Hannifin expanded 1,500-bar hydrogen valves, tapping nascent refueling demand. Digital capability distinguishes leaders; built-in sensors and encrypted protocols ease predictive maintenance yet raise cybersecurity stakes, pressing vendors to certify against CISA guidance. Compliance with API 6D, 6A, ISO 15848, and NACE MR0175 is now baseline, with fire-test and hydrogen-embrittlement standards adding hurdles for new entrants.

A growing share of research budgets targets hydrogen infrastructure and carbon-capture pipelines. OEMs that can validate hydrogen-service materials in accordance with ISO/TR 15916 stand to win early projects. However, low initial volumes limit profit contribution, compelling firms to defend core hydrocarbon segments while incubating transition products.

Oil and Gas Valves Industry Leaders

Emerson Electric Co.

Flowserve Corporation

Schlumberger N.V.

Rotork plc

Baker Hughes Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Emerson Electric completed the first shipment of HV-7000 hydrogen regulators for a Gulf Coast pilot pipeline.

- July 2025: Baker Hughes finalized the USD 13.6 billion acquisition of Chart Industries, integrating cryogenic and hydrogen technologies.

- January 2025: Baker Hughes secured a major valve and actuator order for Saudi Aramco’s Jafurah gas field.

- October 2025: Rotork closed the USD 775 million Mastergear purchase, enhancing electric-actuator torque capacity.

Global Oil and Gas Valves Market Report Scope

The Oil and Gas Valves Market Report is Segmented by Valve Type (Ball Valve, Gate Valve, Globe Valve, Butterfly Valve, Check Valve, Plug Valve, Control Valve), Material (Cast Steel, Forged Steel, Stainless Steel, Alloy and Duplex Steels, Non-Metallic and Composite), Application (Upstream, Midstream, Downstream, LNG Facilities), Actuation Type (Manual, Pneumatic, Electric, Hydraulic and Electro-Hydraulic), Size (Less than 6 inch, 6 to 12 inch, 12 to 24 inch, More than 24 inch), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Ball Valve |

| Gate Valve |

| Globe Valve |

| Butterfly Valve |

| Check Valve |

| Plug Valve |

| Control Valve |

| Cast Steel |

| Forged Steel |

| Stainless Steel |

| Alloy and Duplex Steels |

| Non-Metallic, Composite |

| Upstream (Drilling, Wellhead, Artificial Lift) |

| Midstream (Pipelines, Terminals, Storage) |

| Downstream (Refining, Petrochemical) |

| Liquefied Natural Gas (LNG) Facilities |

| Manual |

| Pneumatic |

| Electric |

| Hydraulic, Electro-Hydraulic |

| Less than 6 inch |

| 6 to 12 inch |

| 12 to 24 inch |

| More than 24 inch |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Kenya | |

| Rest of Africa |

| By Valve Type | Ball Valve | |

| Gate Valve | ||

| Globe Valve | ||

| Butterfly Valve | ||

| Check Valve | ||

| Plug Valve | ||

| Control Valve | ||

| By Material | Cast Steel | |

| Forged Steel | ||

| Stainless Steel | ||

| Alloy and Duplex Steels | ||

| Non-Metallic, Composite | ||

| By Application | Upstream (Drilling, Wellhead, Artificial Lift) | |

| Midstream (Pipelines, Terminals, Storage) | ||

| Downstream (Refining, Petrochemical) | ||

| Liquefied Natural Gas (LNG) Facilities | ||

| By Actuation Type | Manual | |

| Pneumatic | ||

| Electric | ||

| Hydraulic, Electro-Hydraulic | ||

| By Size | Less than 6 inch | |

| 6 to 12 inch | ||

| 12 to 24 inch | ||

| More than 24 inch | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the valves market in the oil and gas industry?

The market was valued at USD 13.43 billion in 2026 and is projected to reach USD 15.93 billion by 2031.

Which valve type is growing fastest in oil and gas facilities?

Control valves are forecast to register the highest 5.12% CAGR to 2031 as digital automation expands.

Why are alloy and duplex steels gaining share in valve materials?

Sour-gas developments and hydrogen-blend pilots require corrosion-resistant metallurgy, lifting alloy, and duplex demand at a 4.72% CAGR.

Which region will see the quickest growth in demand for oil and gas valves?

The Middle East is projected to lead with a 4.76% CAGR through 2031, led by Qatar and Saudi Arabia.

How are digital technologies changing valve maintenance strategies?

Embedded sensors and edge analytics enable predictive maintenance, reducing unplanned downtime and enabling remote operations.

What impact does renewable-energy investment have on oil and gas valve demand?

Rising renewables divert capital from new hydrocarbon projects, tempering long-term valve orders and motivating suppliers to diversify.

Page last updated on: