Vagus Nerve Stimulation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

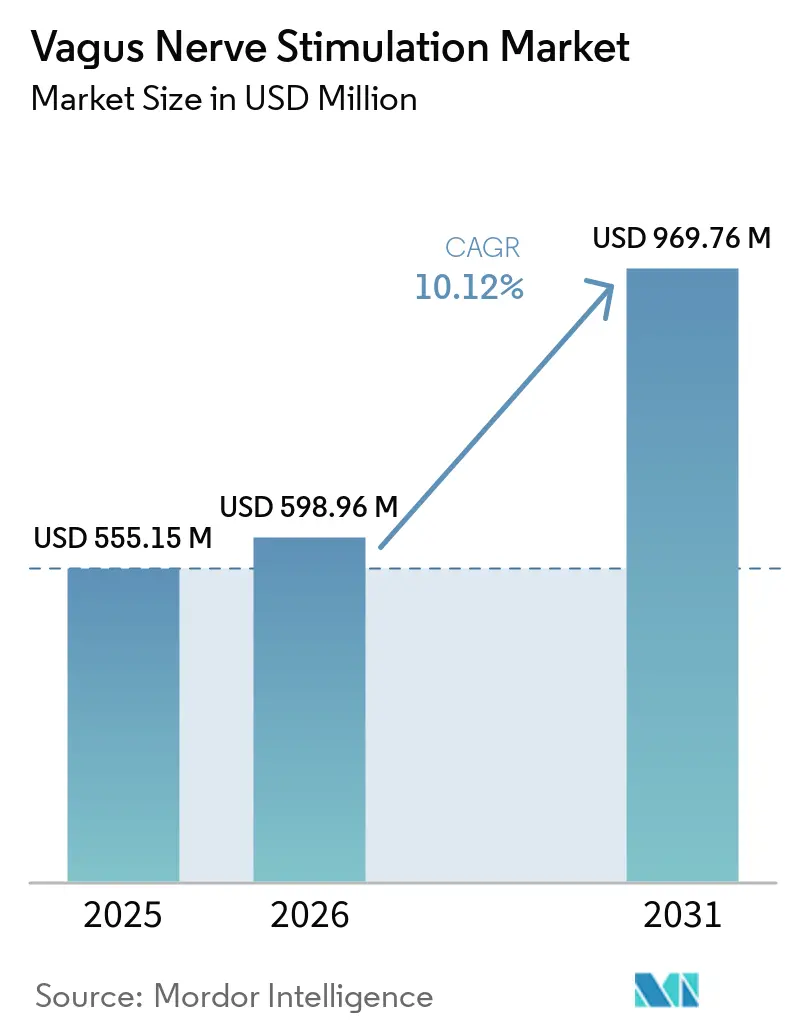

| Market Size (2026) | USD 598.96 Million |

| Market Size (2031) | USD 969.76 Million |

| Growth Rate (2026 - 2031) | 10.12% CAGR |

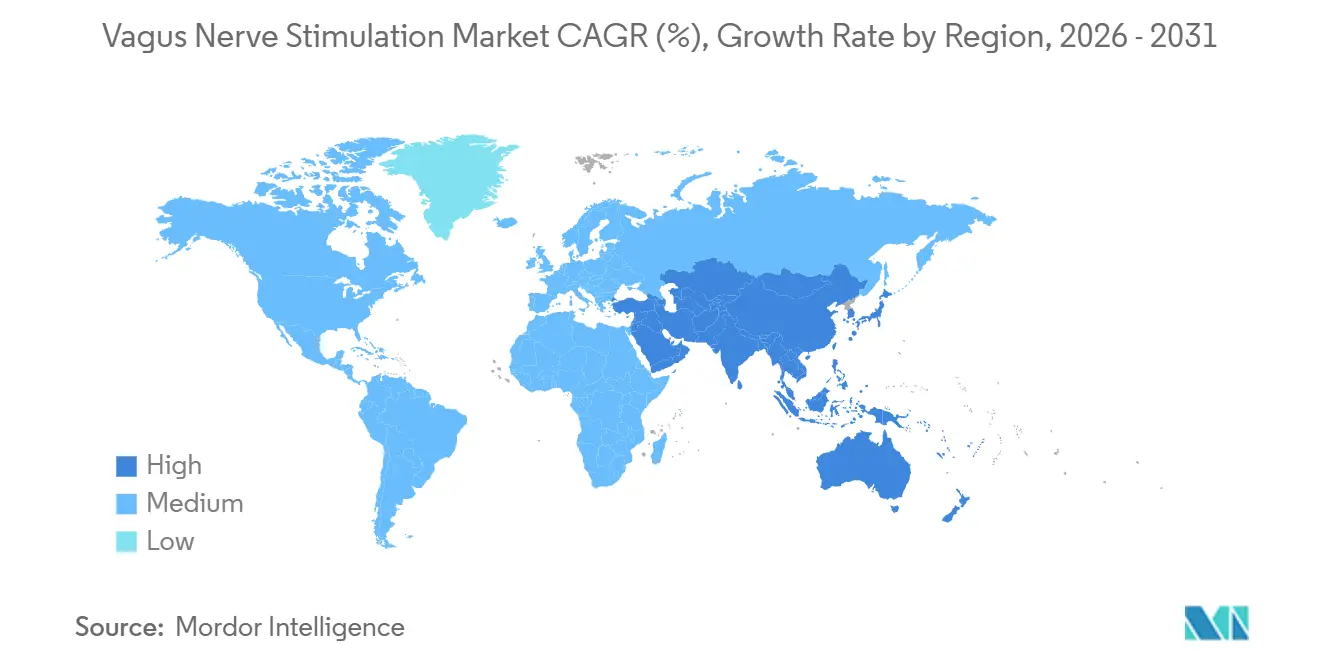

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Vagus Nerve Stimulation Market Analysis by Mordor Intelligence

The Vagus Nerve Stimulation Market size is expected to increase from USD 555.15 million in 2025 to USD 598.96 million in 2026 and reach USD 969.76 million by 2031, growing at a CAGR of 10.12% over 2026-2031.

Therapy adoption builds on a consistent pattern of long-term symptom reduction, payer interest in device-enabled cost offsets, and a tighter link between clinical evidence and coverage decisions. In 2026, payer deliberations for treatment-resistant depression continue to emphasize multi-year durability and quality-of-life outcomes as core criteria for access, with the RECOVER program’s 24-month results informing a national coverage reconsideration in the United States. External non-invasive devices gain momentum in settings where surgical risk avoidance, home use, and rapid-start protocols matter to clinicians and health systems, aided by contracting channels that reach veterans and outpatient neurology networks. Cross-indication progress in rheumatoid arthritis and stroke rehabilitation broadens the clinical footprint of bioelectronic medicine, reinforcing the value proposition for diversified clinical portfolios and multi-specialty care teams.

Key Report Takeaways

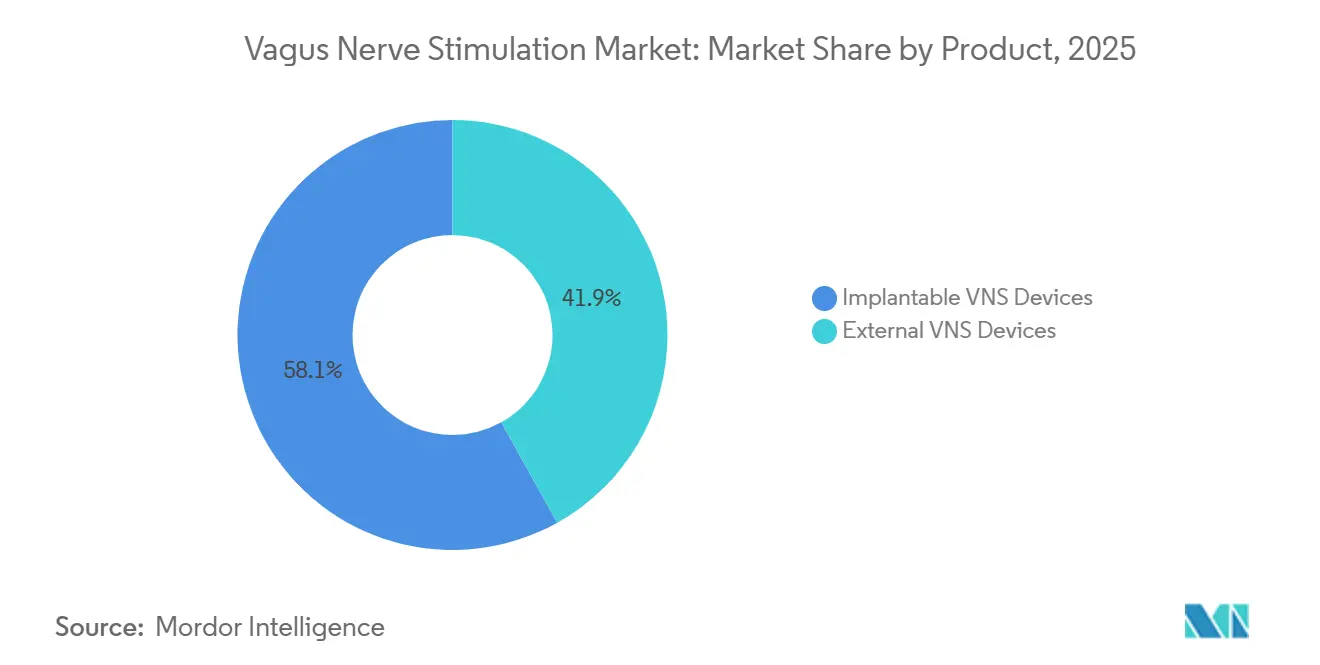

- By product, implantable VNS devices led with 58.10% revenue share in 2025, while external VNS devices are forecast to expand at a 10.64% CAGR to 2031.

- By application, epilepsy accounted for a 56.67% share in 2025, while depression is projected to grow at a 9.75% CAGR through 2031.

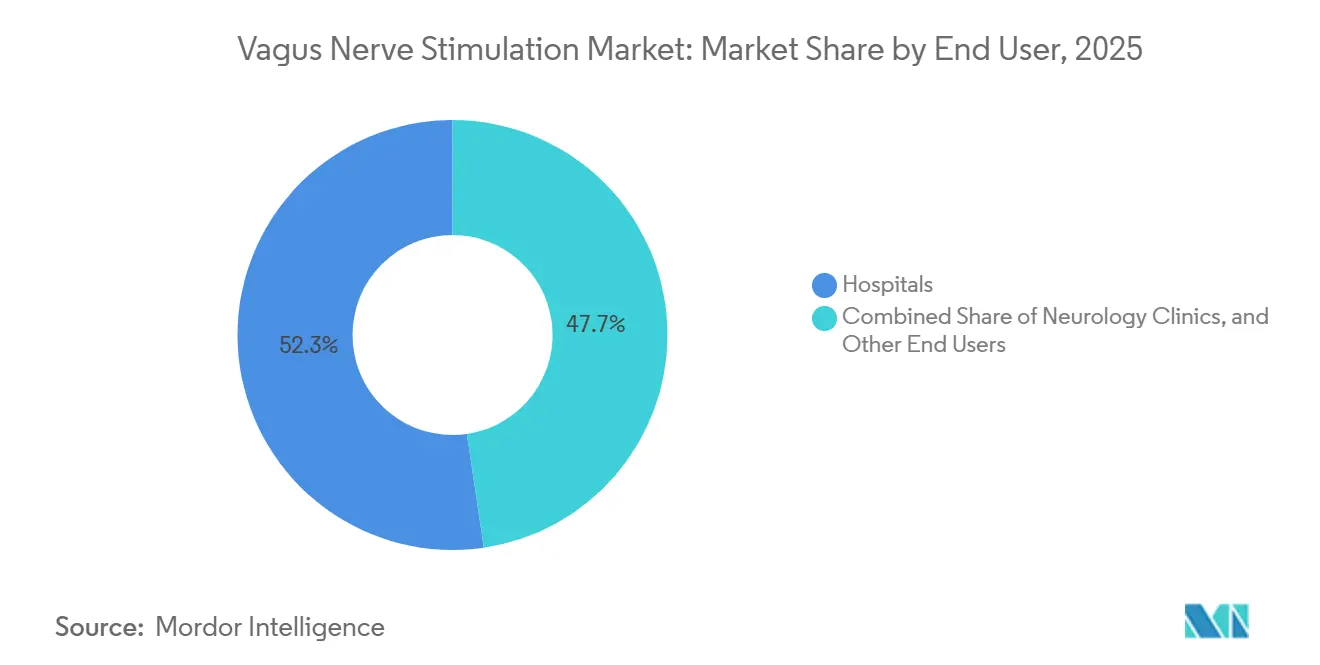

- By end user, hospitals held a 52.33% share in 2025, while neurology clinics are projected to grow at a 10.61% CAGR to 2031.

- By geography, North America captured a 58.22% share in 2025, while Asia-Pacific is forecast to grow at an 11.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vagus Nerve Stimulation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence of Drug-Resistant Neurological Disorders | + 2.8% | Global, with early gains in North America, Western Europe | Short term (≤ 2 years) |

| Shift Toward Neuromodulation Over Chronic Drug Therapy | + 2.1% | North America, Western Europe, spill-over to APAC | Medium term (2-4 years) |

| Growing Clinical Evidence and Label Expansion | + 1.9% | Global, led by regulatory clearances in US, EU | Medium term (2-4 years) |

| Advancement in Device Miniaturization and Closed-Loop Systems | + 1.7% | APAC core, North America, select EU markets | Long term (≥ 4 years) |

| Expansion of Non-Invasive VNS Applications | + 1.1% | North America, UK, Belgium; nascent in APAC | Medium term (2-4 years) |

| Home-Use and Remote Therapy Compatibility | + 0.6% | North America, Northern Europe; limited in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Drug-Resistant Neurological Disorders

Across major care settings, the share of epilepsy patients classified as drug resistant remains high, with professional society communications describing a 20% to one-third range when two appropriate antiseizure medications fail to deliver sustained control.[1]Nome, Cecilie. "Drug-resistant epilepsy: Dr. Patrick Kwan." *Epigraph* 27, no. 4 (November 24, 2025). Clinical guidance continues to evolve toward earlier consideration of device-enabled neuromodulation when predicted probabilities of medication response are low, a shift that aligns with expanded programming options and longer-term benefit profiles in real-world cohorts. In treatment-resistant depression, evidence summaries describe sizable nonresponse to first-line pharmacotherapy and diminishing returns with successive switches, which raises the salience of device pathways that can deliver durable symptom relief in later lines of care. The most recent U.S. coverage reconsideration process for depression is now anchored in 24-month outcomes, including a 51.6% response rate and strong durability among earlier responders, which together inform how payers balance access and evidence requirements in the next cycle.[2]LivaNova PLC. "LivaNova Initiates Process with U.S. Centers for Medicare and Medicaid Services for Reconsideration of National Coverage for VNS Therapy for Treatment-Resistant Depression." June 4, 2025. As these dynamics converge, therapy awareness in neurology and psychiatry underscores broader applicability for both implantable and non-invasive systems in the vagus nerve stimulation market.

Shift Toward Neuromodulation Over Chronic Drug Therapy

Clinicians continue to weigh systemic side effects, adherence challenges, and quality-of-life trade-offs of multi-drug regimens against device-based neuromodulation that can be programmed and titrated over time. Longitudinal data show progressive efficacy with implantable systems in focal seizure types, reinforcing their positioning in later lines when respective surgery is contraindicated or declined. In depression, multi-year observational findings show clinically meaningful response and remission rates in cohorts that had exhausted numerous prior options, which supports a pathway to sustained benefit beyond typical pharmacologic ceilings. Head-to-head parity with non-invasive brain stimulation is not the standard of care, yet benchmark response rates for transcranial magnetic stimulation often cluster in the 50–60% range in standard programs, with durability dependent on maintenance strategies in many sites. Within the U.S., the coverage-with-evidence-development framework that constrained access to depression indications since 2019 is now under formal reconsideration, which could accelerate adoption if the final decision recognizes real-world durability in addition to symptom scales. Over the long run, health-economic analyses presented by manufacturers emphasize breakeven in a two-year window due to reductions in hospitalizations and emergency utilization, a narrative that continues to resonate with stakeholders watching the vagus nerve stimulation market.

Growing Clinical Evidence and Label Expansion

Regulatory progress has extended the reach of bioelectronic medicine into autoimmune disease, with U.S. approval in July 2025 for a neuroimmune modulation system to treat moderate-to-severe rheumatoid arthritis after inadequate response to biologics.[3]"Premarket Approval (PMA) - P240039: SetPoint System." U.S. Food and Drug Administration. July 30, 2025. Company-reported clinical metrics for this platform include meaningful improvements in tender and swollen joint counts over 12 months, a large share of patients discontinuing biologics at one year, and low rates of related serious adverse events. In neurorehabilitation, paired vagus nerve stimulation integrated with therapy continues to hold regulatory clearance for chronic ischemic stroke, while trial registries document the design choices and endpoints that structured pivotal evidence. Non-invasive cervical systems demonstrate traction in headaches and migraine, with commercial updates citing adolescent clearance, deeper penetration into veterans’ care, and expanding payer dialogues in Europe. Belgium’s 2025 reimbursement decision for a transcutaneous system is a clear policy milestone in the region and serves as a reference point for discussions across neighbouring markets. Together, these advances strengthen the evidence base that informs coverage and clinical pathways in the vagus nerve stimulation market.

Advancement in Device Miniaturization and Closed-Loop Systems

Closed-loop systems and miniaturized architectures are reshaping expectations around implantation time, battery maintenance, and compatibility with imaging workflows. A dime-sized vagus nerve stimulator that uses external wireless power and closed-loop algorithms has shown sustained functional improvements in randomized chronic stroke research, including double-digit gains on upper-extremity motor scales after home-based sessions. Trial reporting highlights the feasibility of self-paced regimens and the capacity to extend benefit beyond clinic-based intensive phases, which aligns with patient preferences for hybrid care models. University-led updates have emphasized device size, wireless powering, and cross-modality imaging compatibility, underscoring potential reductions in surgical burden and follow-on generator replacements over the life of therapy. On the non-invasive side, pooled analyses of transcutaneous auricular protocols suggest that intermittent stimulation can cut the likelihood of neck pain and dizziness compared with continuous modes, improving tolerability in outpatient settings. These engineering and protocol innovations add practical value to clinicians seeking to expand access without compromising safety and consistency in the vagus nerve stimulation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost of Implantable VNS System | - 1.6% | Global, acute in low-to-middle-income countries (India, Brazil, South Africa) | Short term (≤ 2 years) |

| Surgical Risk and Patient Reluctance | - 0.9% | Emerging markets in Asia, Africa, Latin America; pediatric and geriatric | Medium term (2-4 years) |

| Limited Reimbursement for Non-Invasive VNS | - 0.7% | US (commercial payers), Europe excluding UK/Belgium, all of APAC except Japan | Short term (≤ 2 years) |

| Competition From Alternative Neuromodulation Therapies | - 1.0% | North America, Western Europe (TMS, DBS, RNS penetration high) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Implantable VNS System

Total acquisition and perioperative costs remain a near-term barrier, as implantable systems require specialist procedures, specialized surgical facilities, and ongoing follow-up programming. Further emphasizing the financial burden, a study based on a United States healthcare claims database found that the mean healthcare costs were approximately USD 123,500 per person in the 2 years prior to VNS implantation. U.S. reimbursement for end-of-service procedures has moved through proposed updates that would increase payment levels in 2026, although the direction and timing of final rulings will determine how much relief hospitals and clinics experience on cash flows. Access pathways for depression are still constrained in the United States because the current national coverage determination limits payment to coverage-with-evidence-development studies with extended follow-up. Commercial plans often require multiple medication failures and psychotherapy trials before approving implantable options, which elongates time-to-therapy for patients who remain symptomatic. Several payers classify implantable vagus nerve stimulation for depression as investigational or unproven in their 2026 policy manuals, reflecting an evidence posture that has not fully converged with multi-year observational findings. New autoimmune indications may alter the cost-benefit narrative, because the 2025 U.S. approval of neuroimmune modulation for rheumatoid arthritis arrived alongside a growth capital raise intended to support commercial rollout and real-world data generation. Manufacturers also present payer-facing analyses that place breakeven for implantable systems in a roughly two-year window due to fewer hospitalizations and emergency visits, which remains a key message in the vagus nerve stimulation market.

Surgical Risk and Patient Reluctance

While implantation is less invasive than cranial electrode placement, it still involves cervical dissection and placement of an electrode cuff around the vagus nerve, so infection risk, temporary hoarseness, and wound concerns shape patient choices. Parents and caregivers can be cautious about visible hardware and follow-up procedures for children, and older adults weigh anesthesia exposure and comorbidities when considering timing. Non-invasive cervical devices eliminate the need for surgical exposure, which is one reason they have gained ground in veterans’ care and outpatient headache clinics, supported by tangible revenue growth in 2025 and multi-year supply agreements with federal networks. Clinicians also track safety profiles in noninvasive auricular approaches, where intermittent stimulation has been associated with fewer unpleasant sensations than continuous modes, a factor that can improve adherence. Meanwhile, the next wave of implantable platforms is designed to shorten procedure time and eliminate the need for battery exchanges, which may reduce aversion to surgery as awareness spreads. Education and shared decision-making practices that present consistent information on risks, benefits, and programming expectations remain essential for expanding confident adoption in the vagus nerve stimulation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: External Devices Narrow Gap Through VA Contracts and Adolescent Approvals

Implantable devices held 58.10% of the vagus nerve stimulation market share in 2025, while external systems are projected to lead with a 10.64% CAGR to 2031. Expanded access for non-invasive systems after adolescent clearance in the United States, combined with outpatient usability, underpins volume gains in clinics and home settings. Department of Veterans Affairs purchasing increased meaningfully in 2024 and continued to grow in 2025, reinforcing procurement-led scale in which device training and standardized protocols can be rolled out across many centers. European policy follow-through in Belgium adds another access point, which in turn supports distribution and medical education economics outside the United Kingdom. As reimbursement channels diversify and clinical teams expand their experience sets, non-invasive options are gaining ground in the vagus nerve stimulation market for patients who do not want surgery or who benefit from rapid starts in outpatient care.

Implantable platforms continue to offer structural advantages in severe or refractory presentations, where continuous and algorithm-optimized stimulation can be programmed to long-term targets. Manufacturer reporting highlights steady neuromodulation revenue growth across 2025, with regional contributions from the United States and Europe supporting ongoing portfolio investment. Next-generation closed-loop concepts and miniaturized, battery-free implants tested in randomized trials point to shorter procedures and fewer generator exchanges over time, which could reduce barriers that have historically favored nonsurgical options. With product strategies that match patient preferences, the vagus nerve stimulation industry leans into a hybrid model, pairing robust implantable performance for highly refractory cases with non-invasive convenience where flexibility and speed matter most. As these approaches mature, diversified product lines can expand participation in the vagus nerve stimulation market across hospitals, neurology clinics, and veterans’ health systems.

By Application: Depression Segment Faces TMS and Ketamine Competition Despite Long-Term VNS Durability

Epilepsy accounted for 56.67% of the vagus nerve stimulation market in 2025 and is projected to expand steadily as real-world data reinforce multi-year reductions in seizure frequency. Longitudinal updates indicate high median reductions in select focal seizure types at multi-year follow-up, supporting durable positioning for patients who have failed other interventions. In parallel, U.S. reimbursement updates in 2026 continue to shape provider economics for device maintenance and programming, which influences how quickly eligible epilepsy patients transition to neuromodulation after medication failure. As health systems refine referral patterns, the vagus nerve stimulation market is demonstrating more consistent pathways for patients with drug-resistant conditions who do not qualify for the respective procedures.

Depression holds a meaningful share in 2025 yet grows at a 9.75% rate through 2031 in a competitive environment shaped by transcranial magnetic stimulation and newer pharmacologic options. TMS response rates often fall in the 50–60% range in standard regimens, and many programs rely on maintenance sessions to sustain benefit over time. The 24-month RECOVER data report a 51.6% response and high durability among 12-month responders, which supports a claims-based narrative centred on long-lasting benefit in late-line depression. In the United States, the national coverage reconsideration process could unlock broader access if the agency concludes that contemporary outcomes meet practical care thresholds for severe cases. Commercial policy language from major plans still lists implantable VNS for depression as unproven in 2026, which magnifies the importance of peer-reviewed publications and consistent endpoint reporting for changes in coverage stances. Within this context, the vagus nerve stimulation industry continues to prioritize pragmatic evidence and payer engagement to improve access pathways over the forecast period.

By End User: Neurology Clinics Gain Share Through Ambulatory Programming and Telemedicine

Hospitals commanded 52.33% share of the vagus nerve stimulation market size in 2025, reflecting their role in device implantation and perioperative care, while neurology clinics are projected to grow at a 10.61% pace as outpatient programming and follow-ups scale. The mix of in-person and virtual programming is now more common, which helps reduce travel burdens and supports coverage across larger geographic footprints in rural and suburban settings. Hospitals retain advantages in surgical infrastructure and multi-specialty consults, while clinics are well placed to manage titration, troubleshooting, and ongoing education once patients enter the maintenance phase. As platform capabilities expand, the vagus nerve stimulation market is likely to see a more balanced distribution of visits between hospital systems and independent neurology groups.

Specialized centers and research networks also shape patient flow by enrolling eligible candidates into trials and by publishing outcomes that guide practice. Depression coverage reconsideration programs in the United States have attracted participation from many academic sites, which has accelerated familiarity with consent, endpoints, and expectations for long-term follow-up. Stroke rehabilitation programs exhibit similar network effects, with multicenter trials defining how pairing protocols and therapy intensity translate into functional gains in the real world. University-led publications on closed-loop miniaturized systems demonstrate the feasibility of at-home sessions that build on supervised therapy, a direction that may increase the proportion of follow-ups handled in ambulatory settings. As more clinics adopt shared tools and care pathways, the vagus nerve stimulation industry benefits from streamlined operations that support both surgical and nonsurgical patient journeys.

Geography Analysis

North America captured 58.22% of vagus nerve stimulation market share in 2025, and Asia-Pacific is poised to record an 11.93% CAGR through 2031. In the United States, the national coverage reconsideration process for depression has placed multi-year outcomes at the center of policy debate, which could affect access and utilization patterns across both implantable and non-invasive systems. 2024 financial disclosures showed steady gains in U.S. neuromodulation revenue, indicating stable demand through provider channels that rely on consistent programming and follow-up. Federal purchasing has become a meaningful driver for non-invasive devices, with 2024 veterans’ system sales cited as a key growth component and 2025 revenues reaching near USD 32 million on a company-reported basis.[4]electroCore, Inc. "electroCore Provides Preliminary Full-Year 2025 Business Update; Expects ~26% Revenue Growth to ~$31.8–$32.0 Million." January 20, 2026. These signals are consistent with a maturing channel strategy in the vagus nerve stimulation market that blends hospital systems, academic networks, and national payers.

Europe retained a significant portion of 2025 demand and displayed policy movement for non-invasive coverage in Belgium, which can catalyze broader discussions across neighbouring payers. The 2025 reimbursement decision for a cervical non-invasive system provides a concrete example of how headache and migraine indications can open a toehold for other evidence-based uses in neuromodulation. Ongoing portfolio updates from manufacturers and academic partners complement these policy developments, and they position Europe to integrate device evidence into neurology and rheumatology pathways over the forecast window.

Asia-Pacific’s long-run growth trajectory ties to clinic readiness, patient access programs, and the diffusion of newer device designs. Countries such as China and Japan have streamlined medical device approval pathways in recent years, accelerating the entry of innovative implantable and non-invasive VNS systems. In China, reforms by the National Medical Products Administration (NMPA) have reduced device review timelines, while Japan’s Pharmaceuticals and Medical Devices Agency (PMDA) continue to prioritize innovative neurological therapies under fast-track programs. These regulatory improvements are encouraging multinational manufacturers to expand their footprint across the region. Reimbursement developments are also strengthening market penetration. In Japan, VNS therapy for epilepsy has been covered under the national health insurance system for several years, significantly improving patient accessibility. Similarly, Australia includes VNS therapy for drug-resistant epilepsy under the Medicare Benefits Schedule and private insurance coverage frameworks. In China, inclusion of more neurological treatments under the National Reimbursement Drug List (NRDL) and provincial reimbursement programs is gradually improving affordability for advanced device-based therapies. Recent randomized research on closed-loop miniaturized implants has showcased at-home functional gains in chronic stroke cohorts, which may inform therapy adoption in rehabilitation hubs across developed APAC markets over time. As more trials launch across neurology and autoimmune conditions, providers in major cities can leverage international findings to build multidisciplinary programs that align with local payer requirements. This foundation supports a durable gradient for adoption in the vagus nerve stimulation market over the forecast horizon.

Competitive Landscape

The vagus nerve stimulation market exhibits moderate-to-high consolidation, with established manufacturers and focused innovators shaping product roadmaps and evidence generation. LivaNova maintains a large installed base and a broad evidence platform in epilepsy and depression, supported by steady 2024 neuromodulation revenue and continuing publications that anchor payer narratives. The company initiated a national coverage reconsideration for depression in June 2025, citing 24-month RECOVER outcomes that inform the policy case for sustained benefit in late-line patients. electroCore’s channel strategy emphasizes veterans’ care and outpatient headache pathways, with documented revenue momentum in 2025 as noninvasive protocols become standard in select centers.

Innovators with focused indications broaden the technical envelope and clinical reach. MicroTransponder, which pairs vagus nerve stimulation with therapy in post-stroke programs, maintains an approved platform and published trial designs that clarify eligibility, endpoints, and workflow for rehabilitation sites. Research on miniaturized, battery-free, closed-loop implants has reported meaningful functional improvements in randomized trials of patients with chronic stroke, highlighting patient-centered features such as home-based sessions and shorter procedures that can reduce maintenance burdens over time. SetPoint Medical extended the neuromodulation portfolio into autoimmune disease with a 2025 U.S. approval in rheumatoid arthritis and followed with a significant financing to support U.S. rollout and pipeline development. These strategies expand the clinical dialog around neuromodulation and create adjacencies that reinforce the value of platform-based development in the vagus nerve stimulation market.

Recent strategic moves reflect a blend of regulatory action, capital allocation, and payer-facing execution. LivaNova’s pursuit of national coverage reconsideration for depression targets the most material access barrier in the U.S. and ties corporate strategy to peer-reviewed outputs and pragmatic outcomes. electroCore’s multi-year relationships with veterans’ health systems provide recurring demand in noninvasive headache care, underpinned by targeted education and device readiness at point of care. Belgium’s 2025 decision to reimburse a noninvasive system for headache indications in turn sets a European reference case that others can examine as evidence evolves and payer priorities shift. Across these moves, participants in the vagus nerve stimulation market are aligning technical roadmaps with coverage and clinical adoption levers to sustain growth through 2031.

Vagus Nerve Stimulation Industry Leaders

-

electroCore, Inc.

-

LivaNova PLC

-

MicroTransponder Inc.

-

Parasym

-

tVNS Health GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: SetPoint Medical closed a USD 140 million Series B financing round, the largest single raise for a VNS platform company in 2024–2025, to support US commercialization of its rheumatoid arthritis neuroimmune modulation system and advance investigational trials in multiple sclerosis and Crohn's disease. The financing included participation from Bluebird Ventures and Western Technology Investment, signaling institutional confidence in platform expansion into billion-dollar autoimmune submarkets beyond the company's RESET-RA pivotal data.

- July 2025: SetPoint Medical received FDA approval for its implantable neuroimmune modulation system (SetPoint System) to treat moderate-to-severe rheumatoid arthritis in adults with inadequate response to one or more biologics, marking the first VNS indication outside neurology and psychiatry.

- June 2025: LivaNova PLC initiated formal reconsideration proceedings with the US Centers for Medicare & Medicaid Services for national coverage of VNS Therapy in unipolar treatment-resistant depression, submitting five peer-reviewed publications from the RECOVER study that document 51.6% median response rate at 24 months and 81.3% durability of benefit among 12-month responders. The submission challenges CMS's 2019 coverage-with-evidence-development policy, arguing the trial data satisfy clinically relevant outcome measures including symptoms, function, and quality of life, and noting VNS is the only treatment demonstrating therapeutic effects in patients who previously failed electroconvulsive therapy.

- May 2025: The University of Texas at Dallas published Phase 1/Phase 2 spinal cord injury VNS trial results in Nature, reporting unprecedented recovery rates in 19 participants with chronic incomplete cervical SCI, where therapy alone provided no benefit. The findings, using X Nerve’s miniaturized, dime-sized, closed-loop device compatible with MRI/CT/ultrasound, position investigators to initiate a Phase 3 pivotal trial enrolling 70 participants across multiple US institutions—the final hurdle for potential FDA approval of VNS for upper-limb impairment due to SCI.

Global Vagus Nerve Stimulation Market Report Scope

Vagus nerve stimulation (VNS) devices are implantable or external medical devices that deliver controlled electrical impulses to the vagus nerve to modulate brain and organ activity. The devices are primarily used to treat drug-resistant epilepsy, treatment-resistant depression, and certain inflammatory or cardiovascular conditions. VNS works by influencing neural pathways involved in mood, seizure control, and autonomic regulation. The Vagus Nerve Stimulation Market is segmented by Product (Implantable VNS Devices and External VNS Devices), Application (Epilepsy, Depression, and Other Applications), End User (Hospitals, Neurology Clinics, and Other End Users), and Geography (North America, Europe, Asia-Pacific, the Middle East and Africa, and South America). The Market Size and Forecasts are provided in Terms of Value (USD) for all the above segments.

| Implantable VNS Devices |

| External VNS Devices |

| Epilepsy |

| Depression |

| Other Applications |

| Hospitals |

| Neurology Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Implantable VNS Devices | |

| External VNS Devices | ||

| By Application | Epilepsy | |

| Depression | ||

| Other Applications | ||

| By End User | Hospitals | |

| Neurology Clinics | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the global vagus nerve stimulation market size in 2025 and by 2031?

The market size is USD 555.15 million in 2025 and is projected to reach USD 969.76 million by 2031, reflecting a 10.12% CAGR during 2026-2031.

How much absolute dollar growth is expected between 2025 and 2031?

The vagus nerve stimulation market is set to add USD 414.61 million over 2025-2031 based on the forecast values.

How large was North America in 2025 by revenue?

North America represented 58.22% of the total in 2025, equal to USD 323.2 million.

Which product category is projected to grow the fastest to 2031?

External VNS devices are projected to grow at a 10.64% CAGR through 2031.

Which end user type is projected to grow the fastest to 2031?

Neurology clinics are projected to grow at a 10.61% CAGR through 2031.

Which region is projected to grow the fastest to 2031?

Asia-Pacific is projected to expand at an 11.93% CAGR through 2031.

Page last updated on: