U.S. Pet Grooming Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

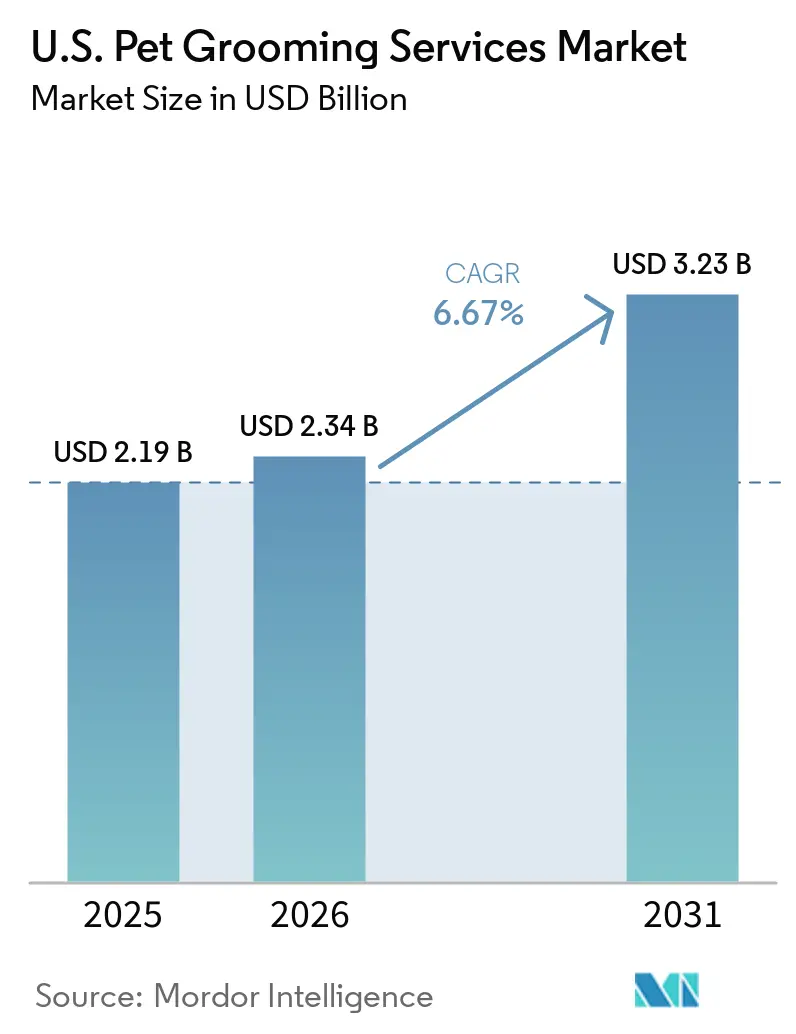

| Base Year Market Size (2025) | USD 2.19 Billion |

| Market Size (2026) | USD 2.34 Billion |

| Market Size (2031) | USD 3.23 Billion |

| Growth Rate (2026 - 2031) | 6.67% CAGR |

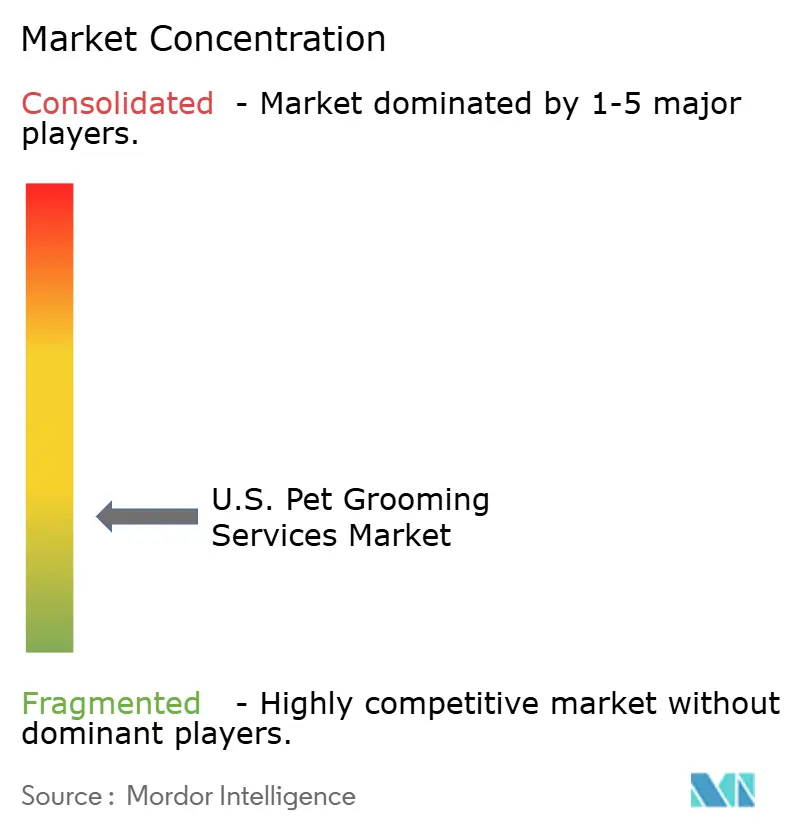

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Pet Grooming Services Market Analysis by Mordor Intelligence

The U.S. Pet Grooming Services Market size is expected to increase from USD 2.19 billion in 2025 to USD 2.34 billion in 2026 and reach USD 3.23 billion by 2031, growing at a CAGR of 6.67% over 2026-2031.

The category is benefiting from a broader wellness trend, as grooming is increasingly viewed as a critical health and skin-coat care service rather than merely cosmetic. Cat ownership is driving future demand, with 49 million United States households owning a cat in 2024, rising to 53 million in 2025, despite the service network remaining largely dog-focused. The United States pet grooming services market is undergoing significant changes, driven by premium treatment packages, mobile service adoption, and rapid franchise expansions. These developments are improving accessibility in metro and suburban areas. This shift is increasing the value of frequent, higher-ticket visits while creating opportunities for operators skilled in handling cats, anxious pets, and specialized coat-care needs.

Key Report Takeaways

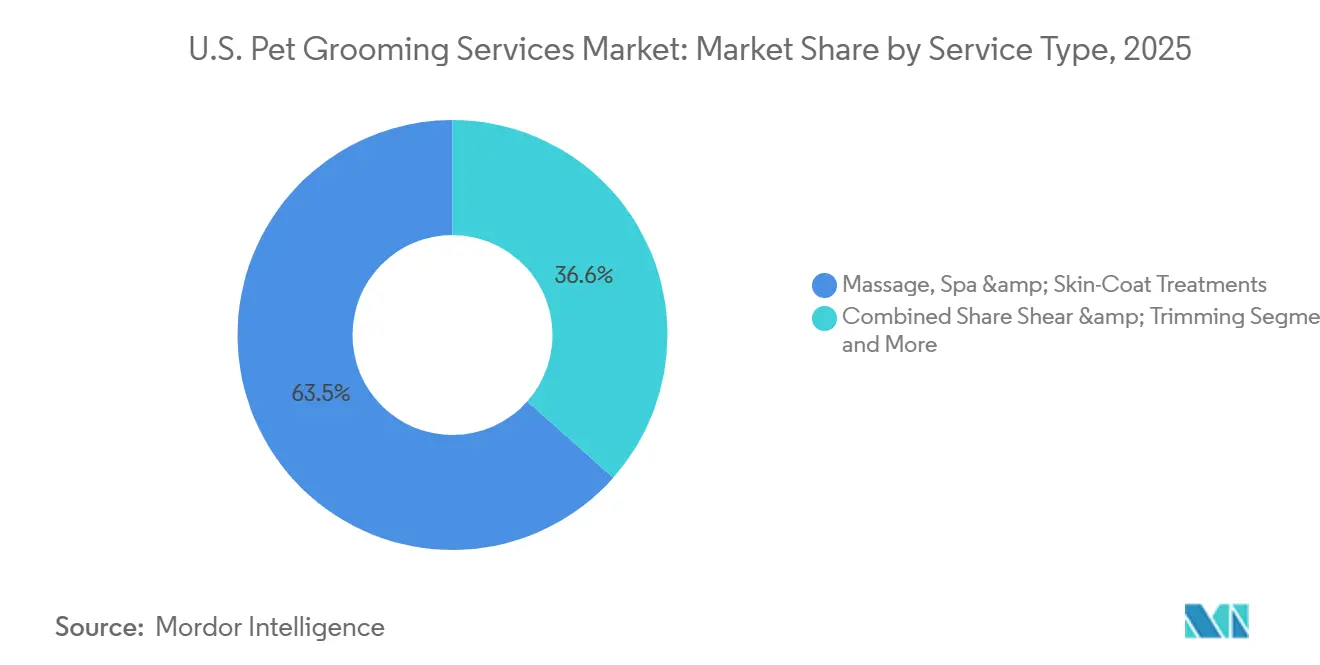

- By service type, massage, spa & skin-coat treatments held 63.45% of the U.S. pet grooming services market share in 2025, while shear & trimming is projected to expand at an 8.25% CAGR through 2031.

- By pet type, dogs accounted for 44.45% of the segment in 2025, while cats recorded the highest projected CAGR at 7.56% through 2031.

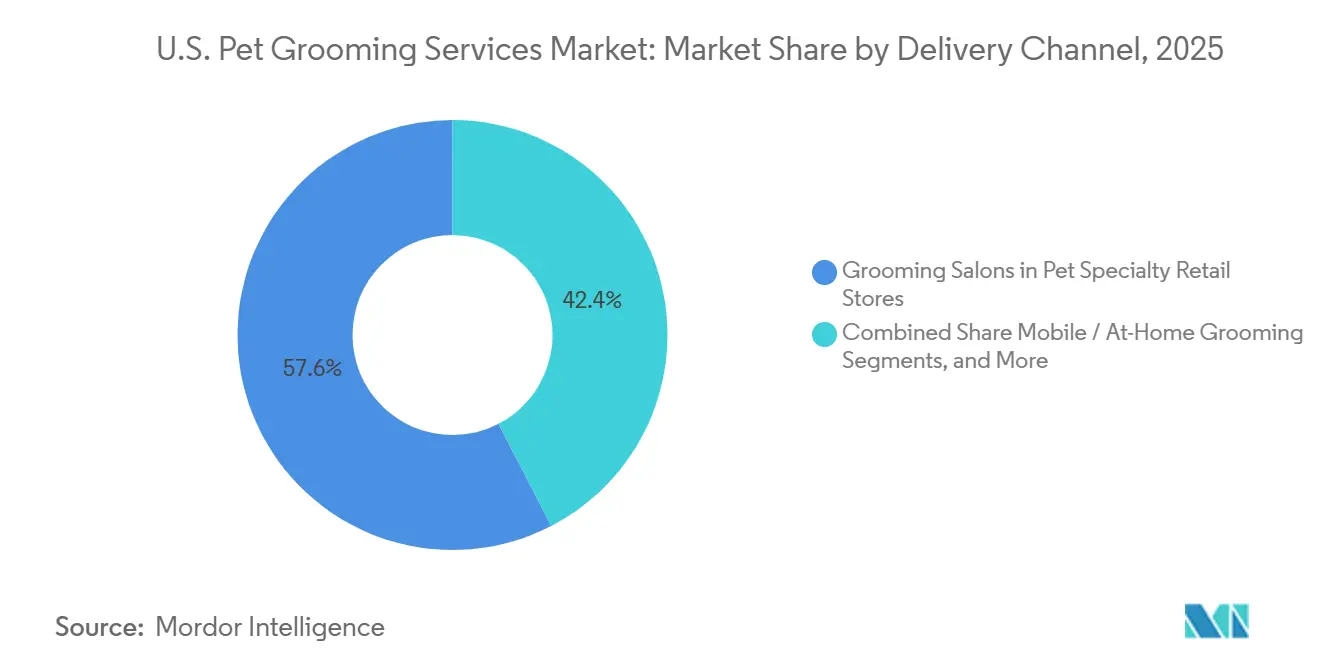

- By delivery channel, grooming salons in pet specialty retail stores captured 57.60% of the segment in 2025, while mobile / at-home grooming is forecasted to grow at an 8.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Pet Grooming Services Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising dog-owning household base | +1.5% | National, early gains concentrated in Sun Belt states including Texas, Florida, and Arizona | Short term (≤ 2 years) |

| Pet humanization sustains premium grooming spend | +1.4% | National, highest intensity in Northeast and West Coast urban markets | Medium term (2-4 years) |

| Mobile and at-home convenience expands addressable demand | +1.2% | National, concentrated in high-density metros including New York, Los Angeles, and Chicago | Short term (≤ 2 years) |

| Multi-location salon and franchise expansion improves access | +1.0% | Southeast and Southwest, with expanding Midwest penetration | Medium term (2-4 years) |

| High-maintenance coat mix lifts recurring visit frequency | +0.8% | National, with higher concentration in suburban single-family home markets | Medium term (2-4 years) |

| Grooming as preventive skin-coat wellness touchpoint | +0.6% | National, with early penetration in premium metropolitan markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Dog-Owning Household Base

The United States pet grooming services market benefits from an expanding base of dog-owning households. By 2025, dog ownership reached 71 million households, increasing from 51% in 2024 to 53% in 2025. This growth drives recurring demand, as most dogs require grooming every 4 to 8 weeks.[1]American Pet Products Association, “U.S. Pet Industry Reaches USD 158 Billion in 2025, Poised for Continued Growth in 2026,” American Pet Products Association, americanpetproducts.org Younger owners are adopting high-maintenance breeds like doodles and Portuguese Water Dogs, which need frequent grooming, boosting revenue potential, and emphasizing the value of household growth.

Pet Humanization Sustains Premium Grooming Spend

The pet grooming market in the United States is supported by the growing trend of pet humanization, with grooming now seen as part of pet wellness. In 2025, grooming sessions in high-income urban areas exceeded USD 1,000, reflecting demand for premium skin and coat treatments. Mid-tier premium packages have become central to salon revenue, offering operators pricing flexibility and sustaining spending despite increasingly layered service menus.

Mobile And At-Home Convenience Expands Addressable Demand

Mobile and at-home grooming services are expanding the reach of the United States pet grooming market. These services cater to time-constrained dual-income households, owners of anxious dogs, and older individuals with large breeds. In 2025, Lucky Dog Mobile Groomers reported 300% year-over-year growth, operating over 90 vans across 30+ markets and serving an estimated 25 million dog owners. The convenience premium in mobile grooming drives higher service fees and increased visit frequency.

High-Maintenance Coat Mix Lifts Recurring Visit Frequency

Shifts in breed preferences are enhancing demand in the United States pet grooming market. Breeds with curly or continuously growing coats require more frequent grooming than short-haired breeds, driving revenue even during slower household growth. In 2025, South Texas College launched a 14-week Professional Dog Grooming program, highlighting the need for specialized skills. Groomers now see more repeat appointments every 4 to 6 weeks, enabling pricing models based on coat condition and styling complexity.[2]American Pet Products Association, “U.S. Pet Industry Reaches USD 158 Billion in 2025, Poised for Continued Growth in 2026,” American Pet Products Association, americanpetproducts.org

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Groomer shortage constrains appointment capacity | -1.3% | National, most acute in suburban and rural markets | Short term (≤ 2 years) |

| Budget pressure shifts demand toward basic packages | -0.9% | National, concentrated in middle-income households | Short term (≤ 2 years) |

| No national licensing creates quality variance and trust risk | -0.6% | National, particularly disruptive in non-metropolitan areas | Long term (≥ 4 years) |

| Rising safety and operating protocols increase cost to serve | -0.5% | National, with highest impact in states with active local ordinances | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Groomer Shortage Constrains Appointment Capacity

The United States pet grooming services market faces a significant challenge due to a shortage of trained professionals. Clients in many regions experience wait times of 3 to 6 weeks, while groomers deal with physical strain and career burnout. Employment for animal care and related services is projected to grow by 11% from 2024 to 2034, with a median annual wage of USD 33,470 as of May 2024.[3]Petco Health and Wellness Company, “Petco Reports Fourth Quarter and Full Year 2025 Results,” PR Newswire, prnewswire.com Despite demand, operators struggle with limited appointment capacity. Initiatives like registered apprenticeships supported by Groom Curriculum and the World Pet Association aim to address the gap, but resolution will take time.

No National Licensing Creates Quality Variance And Trust Risk

The absence of a national licensing standard creates inconsistent service quality in the United States pet grooming services market. Consumers face varying training levels among providers, making it difficult to assess service quality, especially for new users. Poor experiences reduce repeat visits, discourage trying new providers, and limit premium pricing for operators without strong trust signals. Programs like the American Kennel Club's S.A.F.E. Grooming Program, adopted by Woofie’s in July 2025 through a nationwide franchise collaboration, aim to standardize safety education and certification. However, until such standards are widely adopted, quality disparities will continue to impact first-time conversions in some markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Skin-Coat Treatments Lead As Shear & Trimming Accelerates

In 2025, Massage, Spa & Skin-Coat Treatments accounted for 63.45% of the United States pet grooming services market, leading the segment. This reflects the growing demand for multi-step treatment packages that combine coat conditioning, topical care, and stress relief. Bathing & Brushing and Nail Care remain popular as entry services or add-ons, while Ear, Eye & Teeth Hygiene is increasingly viewed as preventive care rather than basic maintenance.

Shear & Trimming is projected to grow at an 8.25% CAGR from 2026 to 2031, making it the fastest-growing service in the United States pet grooming market. This growth is driven by the popularity of coat-intensive breeds and increased spending on regular styling. The service aligns well with mobile formats, as trimming and breed-specific styling are central to full-groom packages. Specialty add-ons in the Others category highlight the overlap between grooming and wellness, with training programs adapting to advanced styling demands.

By Pet Type: Cat Grooming Emerges As The Underdeveloped High-Growth Segment

In 2025, dogs held 44.45% of the United States pet grooming services market, supported by 71 million dog-owning households. Routine visits every 4 to 8 weeks across various breeds drive this segment. The category continues to grow in value as owners of high-maintenance mixed breeds seek regular grooming. Salons with breed-specific expertise and flexible pricing capture more value than those offering flat-rate services.

Cats are expected to grow at a 7.56% CAGR from 2026 to 2031, making them the fastest-growing segment in the United States pet grooming market. Cat ownership rose by 23% from 2023 to 2024, reaching 53 million households in 2025. Despite this growth, cat grooming remains underdeveloped due to dog-centric operations. Long-haired breeds like Maine Coons and Persians require specialized grooming techniques. Groomers offering feline-specific services and quieter environments face less competition in this segment.

By Delivery Channel: Retail Salons Dominate As Mobile Gains Speed

In 2025, Grooming Salons in Pet Specialty Retail Stores held a 57.60% share of the United States pet grooming services market. Their dominance stems from built-in store traffic, loyalty programs, and centralized staffing. Petco reported strong grooming performance in FY2025, with over 40% of appointments booked online. Retail formats benefit from routine customer visits, ensuring grooming remains a convenient option.

Mobile / At-Home Grooming is projected to grow at an 8.35% CAGR through 2031, making it the fastest-growing delivery model in the United States pet grooming market. It appeals to owners seeking personalized service, reduced travel, and a calmer experience for pets. The 2024 merger of Barkbus and Groombuggy highlights the growing scale of mobile grooming. Standalone boutiques compete through personalized services and strong local ties, while grooming bundled with boarding or daycare converts pet stays into grooming opportunities.

Geography Analysis

Regional variations in the United States pet grooming services market are shaped by household density, income patterns, and expanding service networks. The Northeast is a premium-heavy region, supported by dense urban and suburban areas that favor boutique salons, mobile vans, and high-value treatment packages. Apartment living further drives demand for external grooming services. Woof Gang Bakery & Grooming has expanded its presence across states like New York, New Jersey, and Massachusetts, reflecting steady demand for boutique formats.

The South and Southeast are experiencing rapid network expansions in the United States pet grooming services market. In March 2025, Scenthound announced 11 new locations in the Southwest, including 3 in Phoenix, 5 in Salt Lake City, and its first franchise partners in Albuquerque. The company has identified Arizona, California, Nevada, Texas, and Kentucky as key growth areas. These regions, characterized by household formation, suburban growth, and increased pet care spending, align well with franchise models that combine route-based and store-based operations.

The Midwest, though historically less penetrated by franchises compared to coastal regions, is now attracting more attention. In June 2025, Scenthound signed a five-unit agreement in Wisconsin and highlighted Ohio, Illinois, Indianapolis, and Oklahoma as growth areas, signaling a shift toward less saturated markets. Woof Gang Bakery & Grooming has also expanded into Wisconsin and North Dakota, indicating growing demand beyond major metros. While fixed-location salons in smaller cities and rural areas face staffing and density challenges, mobile formats effectively address dispersed demand, creating opportunities for operators balancing efficiency, quality, and local trust.

Competitive Landscape

The United States pet grooming services market remains highly fragmented, with no single operator dominating across service type, delivery format, or price tier. Key players like Petco and PetSmart anchor the market by leveraging their retail networks to drive recurring traffic, enable cross-selling, and enhance customer visibility. Petco reported strong grooming performance through FY2025, with online booking penetration surpassing 40%, highlighting the role of digital systems in improving convenience and booking conversions.

Franchise groups are rapidly expanding into underserved areas while standardizing operations, shaping the second competitive tier. Scenthound plans to operate over 400 locations across 32 states, demonstrating its swift scaling beyond regional roots. Woof Gang Bakery & Grooming, with more than 450 locations operational or in development, continues its aggressive state expansion through 2025. Geographic clustering, where operators open multiple sites in close proximity, has emerged as a key strategy to boost brand visibility and operational efficiency.

Newer concepts are testing innovative approaches to compete in the United States pet grooming services market. Sparkle Grooming Co. awarded over 500 licenses by April 2026, reflecting investor interest in wellness-focused boutique formats with structured expansion plans. Mobile grooming operators are gaining traction by catering to anxious pets, busy owners, and underserved areas. The 2024 merger of The Barkbus and Groombuggy highlights the shift toward larger, more coordinated platforms in the mobile grooming segment.

U.S. Pet Grooming Services Industry Leaders

Petco Health and Wellness Company, Inc.

PetSmart LLC

Woof Gang Bakery & Grooming

Aussie Pet Mobile

Groomit for Pets LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sparkle Grooming Co. surpassed 500 licenses awarded to regional developers across 27 states within 24 months of franchising, with major agreements in Tennessee, South Florida, and Houston, establishing wellness-focused boutique grooming franchises as a growing investment category.

- December 2025: Woof Gang Bakery & Grooming expanded to 33 states and Canada by opening its first franchised stores in Boston, Massachusetts, and Fargo, North Dakota, targeting 450+ locations by 2027 after opening over 70 stores in 2025.

- October 2025: Scenthound finalized plans for over 400 franchised and corporate-owned locations across 32 states, supported by a growth equity investment from VMG Partners to drive geographic expansion and enhance technology infrastructure.

- September 2025: Woof Gang Bakery & Grooming entered Oregon, its 30th state, with over 450 locations open or in development nationwide, following earlier expansions in Washington, Wisconsin, Maryland, and Massachusetts.

U.S. Pet Grooming Services Market Report Scope

As per the scope of the report, pet grooming services refer to the professional hygienic care, cleaning, and maintenance of domestic animals like dogs and cats. These services, including bathing, brushing, nail trimming, and haircuts, are designed to enhance the pet's aesthetic appearance while proactively monitoring their skin, coat, and overall physical health.

The U.S. pet grooming services market is segmented by service type, pet type, and delivery channel. By service type, the market includes bathing & brushing, shearing & trimming, nail care, ear, eye, & teeth hygiene, massage, spa, & skin-coat treatments, and other services. By pet type, the market is segmented into dogs and cats. By delivery channel, the market is categorized into grooming salons in specialty pet retail stores, standalone grooming boutiques & salons, mobile/at-home grooming services, and grooming bundled with boarding & daycare facilities. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Bathing & Brushing |

| Shear & Trimming |

| Nail Care |

| Ear, Eye & Teeth Hygiene |

| Massage, Spa & Skin-Coat Treatments |

| Others |

| Dogs |

| Cats |

| Grooming Salons in Pet Specialty Retail Stores |

| Standalone Grooming Boutiques & Salons |

| Mobile / At-Home Grooming |

| Grooming Bundled with Boarding / Daycare Facilities |

| By Service Type | Bathing & Brushing |

| Shear & Trimming | |

| Nail Care | |

| Ear, Eye & Teeth Hygiene | |

| Massage, Spa & Skin-Coat Treatments | |

| Others | |

| By Pet Type | Dogs |

| Cats | |

| By Delivery Channel | Grooming Salons in Pet Specialty Retail Stores |

| Standalone Grooming Boutiques & Salons | |

| Mobile / At-Home Grooming | |

| Grooming Bundled with Boarding / Daycare Facilities |

Key Questions Answered in the Report

What is the current size of U.S. pet grooming services in 2026?

The U.S. pet grooming services market size is USD 2.24 billion in 2026 and is projected to reach USD 3.23 billion by 2031 at a 6.67% CAGR.

What is driving growth in pet grooming demand across the United States?

Growth is being supported by 71 million dog-owning households in 2025, higher pet wellness spending, stronger mobile service adoption, and expanding franchise access.

Which service category leads spending in pet grooming?

Massage, Spa & Skin-Coat Treatments led with 63.45% share in 2025, showing that premium multi-step treatment packages now account for a large part of customer spending.

Which pet type is growing fastest in grooming services?

Cats are the fastest-growing pet type, with a projected 7.56% CAGR from 2026 to 2031, even though much of the current salon infrastructure still focuses on dogs.

Which delivery channel is expanding the quickest?

Mobile / At-Home Grooming is the fastest-growing channel, with an 8.35% CAGR through 2031, driven by convenience needs and demand from anxious or hard-to-transport pets.

How competitive is the U.S. grooming landscape?

The field is highly fragmented, with Petco and PetSmart serving as major anchors while Scenthound, Woof Gang, Sparkle, mobile operators, and independent salons continue to expand.

Page last updated on: