Ursodeoxycholic Acid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 660.40 Million |

| Market Size (2031) | USD 986.90 Million |

| Growth Rate (2026 - 2031) | 7.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ursodeoxycholic Acid Market Analysis by Mordor Intelligence

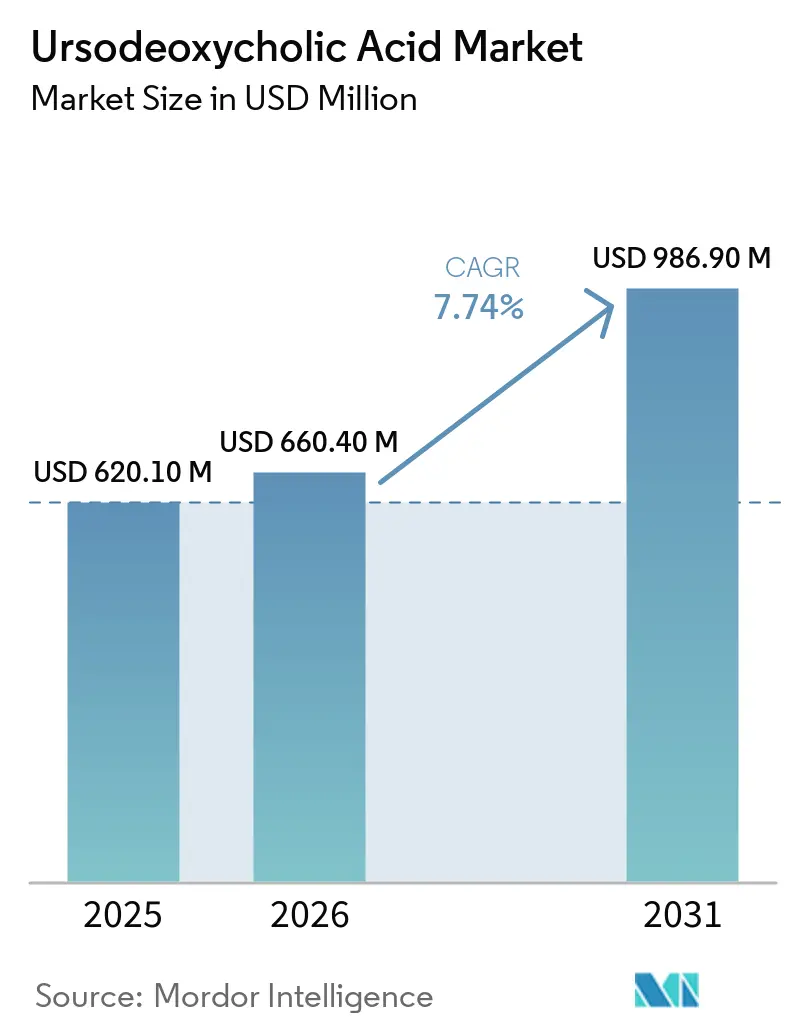

The Ursodeoxycholic Acid Market size was valued at USD 620.10 million in 2025 and is estimated to grow from USD 660.40 million in 2026 to reach USD 986.90 million by 2031, at a CAGR of 7.74% during the forecast period (2026-2031).

UDCA remains the first-line therapy for primary biliary cholangitis under AASLD and EASL recommendations, which secures baseline demand through 2031. The accelerated approvals of seladelpar and elafibranor did not displace UDCA because their labels emphasize use in combination for inadequate responders, which strengthens UDCA’s role in routine care pathways. The November 2025 withdrawal of obeticholic acid in the United States further consolidated UDCA’s position by removing a substitute agent from second-line use. Capacity additions and vertical integration on the API side, including chicken-bile sourcing and scale-up in India, stabilize supply and help offset pricing pressure from generics[1]ICE Pharma, “ICE Pharma Inaugurates New F Block at Raichem (India), Boosting UDCA Production from Chicken Bile,” ICE Pharma, icepharma.com. Demand upside continues to build in gallstone prevention post-bariatric surgery and in selected cholestatic conditions where guideline-backed use or strong clinical rationale supports prescribing through the forecast window.

Key Report Takeaways

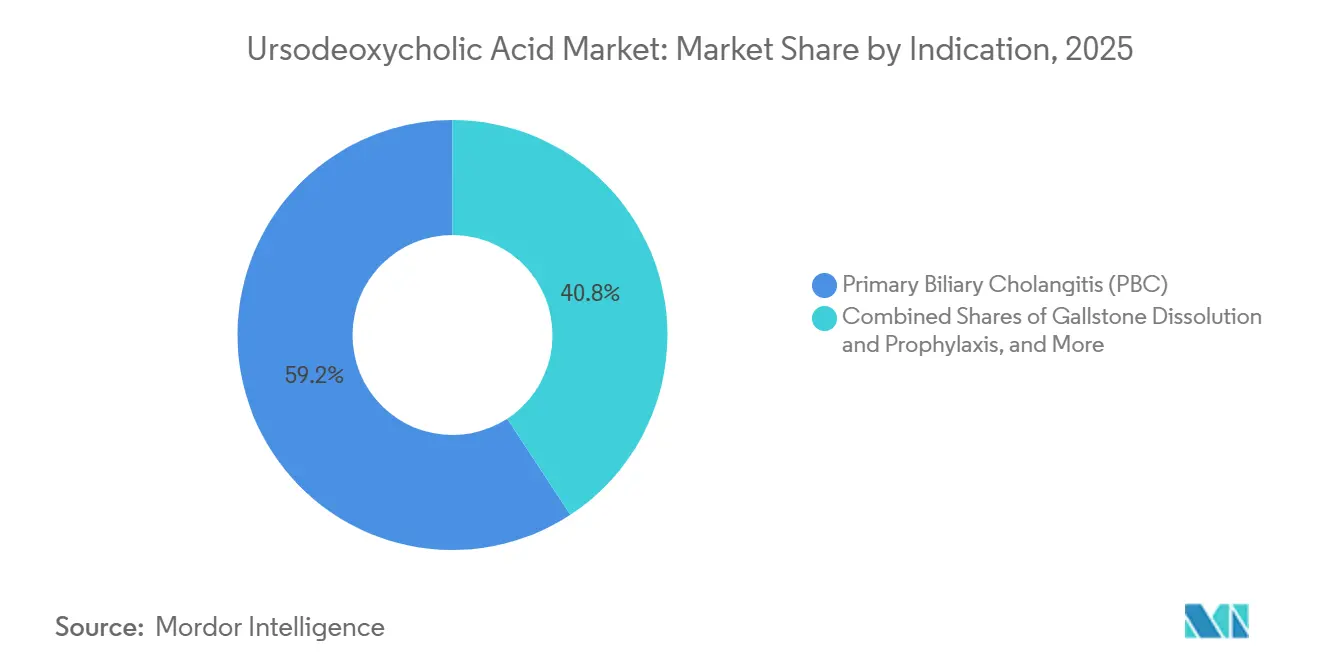

- By indication, primary biliary cholangitis led with 59.23% of the ursodeoxycholic acid market share in 2025, while gallstone dissolution and prophylaxis is projected to expand at a 9.54% CAGR through 2031.

- By dosage form, tablets accounted for 54.32% of the ursodeoxycholic acid market in 2025, while oral suspensions are forecast to grow at 9.75% CAGR through 2031.

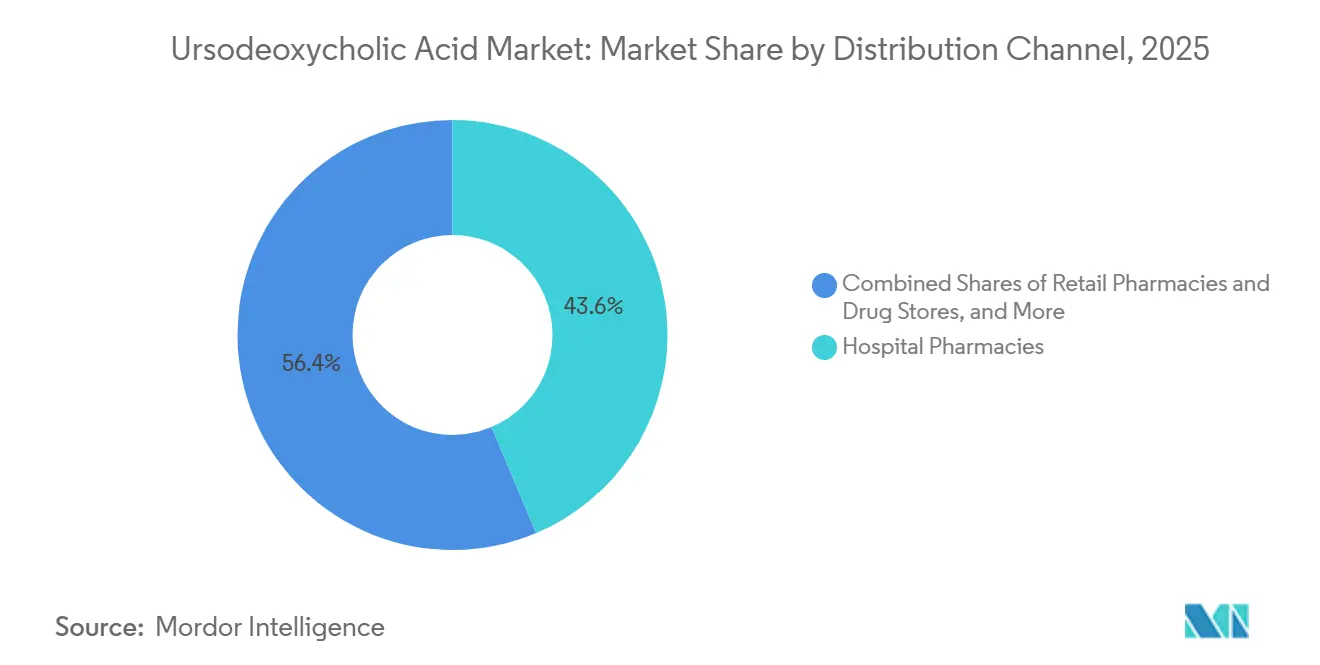

- By distribution channel, hospital pharmacies captured 43.64% of the ursodeoxycholic acid market in 2025, while online pharmacies are projected to grow at a 10.23% CAGR through 2031.

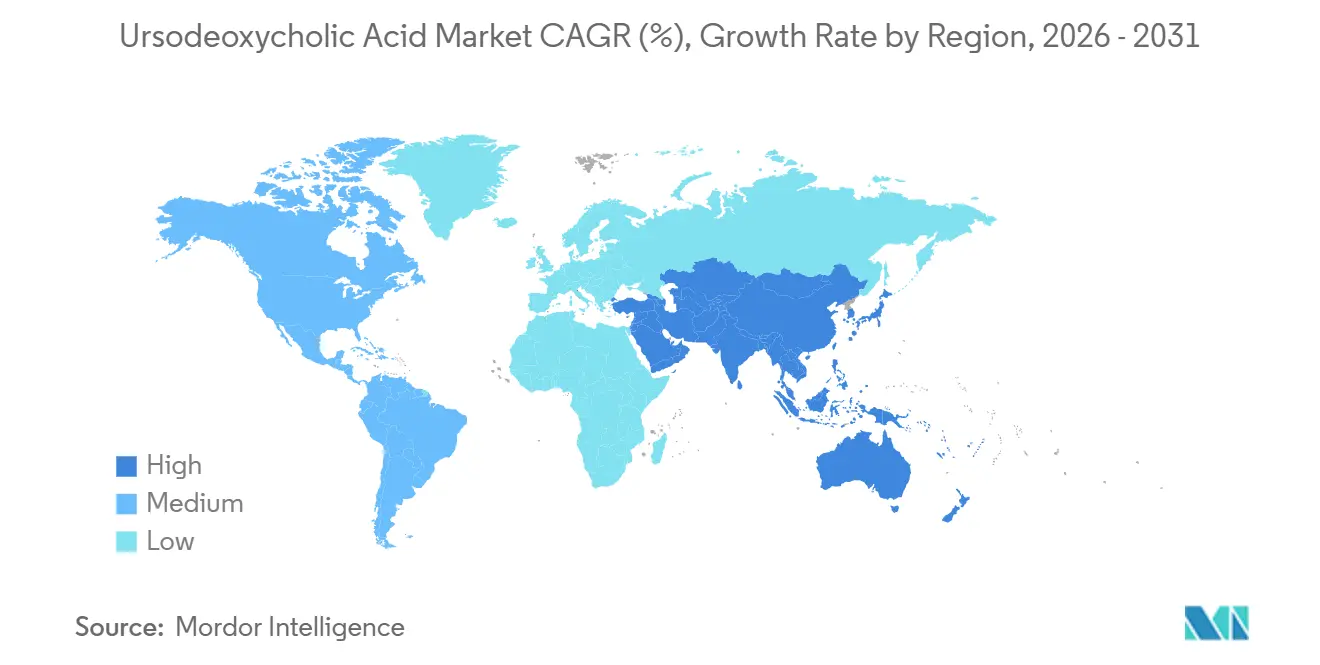

- By geography, North America held 41.32% of the ursodeoxycholic acid market in 2025, while Asia-Pacific is set to grow at a 10.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ursodeoxycholic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| First-line therapy status in PBC under AASLD/EASL | +2.1% | Global, particularly North America and Europe | Long term (≥ 4 years) |

| Rising diagnosed prevalence of PBC and cholestatic liver diseases | +1.8% | Global, with concentration in developed markets | Medium term (2-4 years) |

| Increasing gallstone disease and non-surgical management cohorts | +1.5% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Expansion of generics and API capacity improving affordability | +1.3% | Global, spill-over to emerging markets | Short term (≤ 2 years) |

| Vertically integrated bile-acid supply chains stabilizing UDCA output | +0.9% | Global, with API hubs in India and China | Medium term (2-4 years) |

| Pipeline of second-line PBC agents preserves UDCA as backbone | +0.7% | North America, Europe, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

First-line Therapy Status in PBC Under AASLD/EASL

UDCA remains the recommended first-line therapy for PBC at 13–15 mg/kg/day, which locks in consistent treatment volumes and provides a durable base for the ursodeoxycholic acid market across major regions. Longstanding clinical evidence shows that UDCA improves liver biochemistry and transplant-free survival when initiated early in the disease course, which sustains physician confidence and adherence to guidelines. The 2024 approvals of seladelpar and elafibranor did not alter the standard of care because both are used alongside UDCA for inadequate responders rather than as replacements, reinforcing UDCA’s backbone role[2]U.S. Food and Drug Administration, “2024 New Drug Therapy Approvals Annual Report,” FDA, fda.gov. The 2025 U.S. withdrawal of obeticholic acid further strengthened UDCA positioning since a second-line competitor exited the market, which redirected escalation pathways toward PPAR agonists added to UDCA. As a result, the ursodeoxycholic acid market is anchored by guideline-backed use and reinforced by add-on strategies for partial responders. This combination of guidelines and label positioning helps stabilize core demand for UDCA through the forecast period.

Rising Diagnosed Prevalence of PBC and Cholestatic Liver Diseases

Better awareness and serologic testing have increased diagnosed PBC prevalence, which steadily expands the patient pool eligible for UDCA. Clinicians rely on established guideline frameworks that endorse UDCA as lifelong therapy in PBC, which supports a sustained prescription base as more cases are detected at earlier stages[3]NHS, “Primary Biliary Cholangitis (Primary Biliary Cirrhosis) - Treatment,” NHS, nhs.uk. A considerable share of patients do not fully respond biochemically to UDCA alone, which concentrates add-on use for that cohort while preserving UDCA in the regimen. Additional cholestatic conditions also contribute to volumes in specialist practice, particularly where clinical guidance supports UDCA use to improve cholestatic parameters.

The direction of travel favors earlier diagnosis and sustained therapy durations, which underpins growth in the ursodeoxycholic acid market as treated prevalence rises. These patterns are most visible in health systems with screening infrastructure and specialist access in place.

Increasing Gallstone Disease and Non-surgical Management Cohorts

The number of patients living with gallstones has grown in several countries, and many are asymptomatic, which opens space for prevention and medical management in selected cohorts. Bariatric surgery programs have expanded, and rapid postoperative weight loss increases the risk of gallstone formation in the first year, which creates a clear rationale for UDCA prophylaxis. Evidence indicates that prophylactic UDCA significantly reduces gallstone formation and symptomatic disease after bariatric procedures, which is a strong tailwind for this high-growth use case. Medical dissolution remains a targeted option for small cholesterol stones in functional gallbladders, although real-world practice emphasizes careful patient selection for best outcomes.[4]Merck Manual Professional Edition, “Cholelithiasis - Hepatology,” Merck Manuals, merck.com

Together, these cohorts expand the addressable base beyond PBC, which benefits the ursodeoxycholic acid market as surgical contraindications or patient preferences favor medical pathways. In markets where bariatric volumes are rising, this driver contributes to growth above the global average

Expansion of Generics and API Capacity Improving Affordability

Increased generic availability reduces unit prices and improves access, especially in price-sensitive regions, which lifts total volumes dispensed. On the supply side, capacity additions and vertically integrated API operations have reduced upstream constraints while diversifying feedstocks, most notably through scaled chicken-bile processing in India. These manufacturing improvements underpin stable output and enhance resilience if one source region faces disruptions, which supports the ursodeoxycholic acid market during demand spikes. Labeling and dosage-form breadth documented in official repositories also reflects mature generic participation across multiple strengths and presentations. In emerging markets, better affordability tends to correlate with improved adherence and completion of prescribed courses, which further supports volume growth. This dynamic is already visible in regions expanding insurance coverage or public procurement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Generic pricing pressure compressing branded margins | -1.4% | Global | Short term (≤ 2 years) |

| Limited efficacy/non-response in subsets | -1.1% | Global | Medium term (2-4 years) |

| Feedstock exposure to cholic-acid/bovine bile supply risks | -0.6% | Global, concentrated in API manufacturing regions | Medium term (2-4 years) |

| New PBC agents competing for non-responder share | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Generic Pricing Pressure Compressing Branded Margins

Broader generic participation shifts price competition from brand value to supply chain efficiency, which compresses margins for finished-dose manufacturers. In this environment, the locus of profitability often moves upstream to API producers with cost advantages and secure feedstock, while finished-dose players differentiate through distribution execution. Mature labeling across presentations and strengths evidences the depth of generic availability, which makes sustained price premiums difficult to defend in pharmacy channels. For the ursodeoxycholic acid market, this pressure can flatten average selling prices even as total prescriptions rise. The net effect is top-line growth that relies more on volumes than on price realization in many geographies. In regions with public reimbursement and tendering, this restraint is more pronounced as procurement favors lowest bids.

Limited Efficacy/Non-response in Subsets

A meaningful fraction of PBC patients do not achieve adequate biochemical response to UDCA monotherapy after one year, which caps the ceiling for UDCA-only regimens and requires add-on therapy. Evidence reviews in 2025 reconfirm that in PBC, the non-responder group remains clinically important, which sustains the role of second-line agents for escalation. In PSC, UDCA improves cholestatic markers but does not change disease progression endpoints, which constrains adoption and steers practice toward surveillance and procedural management. This clinical ceiling narrows monotherapy use but still preserves UDCA as a base layer where add-on labels require combination. For the ursodeoxycholic acid market, the restraint is balanced by the fact that non-responders often continue UDCA while adding a second agent. That pattern supports volume stability despite efficacy limits in specific subgroups.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: PBC Dominates, but Gallstone Prophylaxis Accelerates Fastest

PBC captured 59.23% of the ursodeoxycholic acid market share in 2025, reflecting entrenched first-line use and guideline continuity that stabilizes long-term therapy. Combination regimens in partial responders extend UDCA duration and keep the base in place while add-on agents target more ambitious biochemical endpoints, which supports the ursodeoxycholic acid market in core hepatology practices. Gallstone dissolution and prophylaxis are projected to grow at 9.54% CAGR between 2026 and 2031, which is higher than the overall trajectory and signals a more dynamic secondary use case. The ursodeoxycholic acid market benefits as bariatric programs scale and as clinicians standardize prevention protocols for high-risk postoperative periods, where UDCA has shown meaningful reductions in gallstone formation. Cholestatic liver diseases outside PBC contribute steady volumes where laboratory improvements are clinically valued, and safety is well characterized in long-term use. In PSC, adoption is limited by a lack of impact on progression endpoints in recent overviews, which restricts UDCA mainly to selected biochemical management strategies.

The ursodeoxycholic acid market size for gallstone prevention is aligned with bariatric program growth because the risk of postoperative stone formation is highest in the first postoperative year, and clinical guidance supports prophylactic use in defined cohorts. For small, cholesterol-rich stones in functioning gallbladders, medical management remains a targeted option in patients where surgery is delayed or contraindicated, and this use preserves continuity across surgical pathways.

In PBC, stable long-term prescribing anchors base volumes that extend across primary and specialty care, which is central to the consistency of the ursodeoxycholic acid market. Across indications, add-on labels for second-line PBC therapies sustain UDCA’s role rather than displacing it, which lowers substitution risk and supports long-range planning for supply chains. These patterns keep PBC as the largest contributor, while gallstone prevention and selected cholestatic uses provide higher incremental growth. The balance yields a portfolio effect that underpins resilient revenue for the ursodeoxycholic acid market through 2031.

By Dosage Form: Tablets Lead, Oral Suspensions Gain Pediatric and Geriatric Traction

Tablets accounted for 54.32% of the ursodeoxycholic acid market in 2025, supported by weight-based dosing ranges that align well with 250 mg and 500 mg strengths and by broad generic availability documented in official labeling sources. The ursodeoxycholic acid industry has standardized around tablet presentations in long-term PBC care, which supports procurement, stocking, and patient adherence in both hospital and retail settings. Capsules hold a smaller, stable slice of the market based on patient preference, while offering no therapeutic differences that could change the competitive balance in dosage-form choice. Labeling depth and consistent dosage guidance across forms support clinician confidence, which helps maintain the leading share for tablets in chronic-use indications. In addition, tablets continue to form the default choice in formularies that evaluate cost and logistics alongside clinical appropriateness.

Oral suspensions are forecast to grow at 9.75% CAGR through 2031, which reflects demographic and practical factors in pediatric and geriatric care. In pediatrics, cystic fibrosis-related hepatobiliary disorders and other cholestatic presentations benefit from weight-based dosing and palatable liquid forms that simplify administration. In older patients with dysphagia or complex regimens, suspensions ease adherence and enable flexible titration to target dose ranges. The ursodeoxycholic acid industry has responded with formulation improvements that support stability and administration convenience, which further drives uptake where liquids fit better into home-care routines. Given tablets’ entrenched base and wide generic competition, the primary source of dosage-form share changes comes from rising use of oral suspensions in defined subpopulations. This keeps the ursodeoxycholic acid market diversified across forms, while highlighting the expanding role of liquids in special populations.

By Distribution Channel: Hospital Pharmacies Dominant, Online Pharmacies Surge

Hospital pharmacies captured 43.64% of the ursodeoxycholic acid market in 2025, which reflects acute use during inpatient care for cholestatic episodes and initiation of long-term therapy for newly diagnosed PBC. Hospitals also see initiation or adjustment of UDCA therapy alongside interventional procedures in complex cholestatic disease, which strengthens this channel’s role in care transitions. Retail pharmacies maintain a steady share for chronic refills and counseling that supports adherence in early-stage PBC and in select gallstone management cases. The channel mix is stable in mature markets that rely on established dispensing networks and integrated health system workflows. The ursodeoxycholic acid market relies on predictable replenishment patterns in both hospital and retail settings to maintain on-shelf availability.

Online pharmacies are projected to grow at 10.23% CAGR through 2031, which reflects the integration of telemedicine, e-prescribing, and home delivery for chronic hepatology care. Digital platforms enable rapid initiation and refills for PBC patients and for those receiving UDCA after bariatric procedures, which compresses the time from diagnosis to first fill. In regions with sparse specialist access, online models bridge geographic gaps and sustain continuity of care through automated reminders and pharmacist chat services. The ursodeoxycholic acid market size related to online dispensing expands as insurers reimburse digital pharmacy services and as patients adopt home delivery for chronic medications. While local regulations may require counseling for first-time prescriptions, most markets now recognize the legitimacy of digital fulfillment backed by licensed pharmacists. This trend lifts the convenience factor and supports long-term adherence for UDCA regimens that extend over many years.

Geography Analysis

North America held 41.32% of the ursodeoxycholic acid market share in 2025, led by the United States, where guideline-backed first-line use in PBC is firmly established, and coverage policies support long-term therapy. The U.S. withdrawal of obeticholic acid in 2025 removed a second-line option and reinforced the pairing of UDCA with PPAR agonists for inadequate responders, which kept UDCA volumes intact at escalation. Canada and Mexico contribute additional volumes through public and private coverage frameworks that tend to favor cost-effective generics, which stabilizes uptake where hepatology centers coordinate care. Specialist networks and transplant programs also support the use of UDCA in defined protocols, while bariatric surgery programs add demand through preventive use in high-risk cohorts. The overall picture in North America is one of maturity in share but resilient volume based on long-term therapy behaviors.

Europe accounts for the second-largest regional base, driven by adherence to EASL-aligned guidance and robust reimbursement across major markets. National health systems in Germany, the United Kingdom, France, Italy, and Spain have established pathways for UDCA access and for escalation to second-line therapies where criteria are met. Physician familiarity with long-term safety and dosing consistency supports stable demand, while demographic aging increases the share of patients under chronic care. Tendering structures and public procurement in the European Union tilt toward low-cost generics, which benefits the ursodeoxycholic acid market in terms of volume but caps pricing power. Variations in bariatric surgery uptake across Europe also influence the pace of growth in gallstone prophylaxis. Overall, Europe shows steady expansion driven by clinical continuity and payer support.

Asia-Pacific is set to grow at 10.45% CAGR through 2031, which positions the region as the fastest-growing engine for the ursodeoxycholic acid market. Rising hepatitis B prevalence in some countries, a growing burden of metabolic liver disease, and fast-expanding bariatric surgery programs drive incremental demand. Local API expansions in India and strong manufacturing ecosystems in China increase supply security and support affordability, which broadens access to UDCA. Japan and Australia provide steady demand based on established care pathways, while China and India produce the largest incremental gains due to scale and improving reimbursement coverage. In Southeast Asia, policy initiatives to improve viral hepatitis screening and metabolic disease management are likely to lift diagnosed prevalence and treatment initiation. The ursodeoxycholic acid market size in Asia-Pacific is therefore set to expand in line with clinical infrastructure and payer policies through the forecast horizon.

Competitive Landscape

The ursodeoxycholic acid market features fragmented structure with many generic manufacturers and a concentrated group of API producers with vertical integration and regulatory credentials. On the API side, capacity expansions and diversified animal-bile sourcing reduce reliance on any single feedstock and add resilience for global supply. Producers with GMP certifications and DMF filings maintain a competitive advantage in tenders and long-term supply contracts. Finished-dose manufacturers compete on procurement, cost control, and distribution reach rather than on product differentiation, which tightens the spread between suppliers in mature channels. This structure points to moderate fragmentation with pockets of advantage where integration, scale, and regulatory strength converge. The ursodeoxycholic acid market, therefore, rewards upstream control and quality systems as much as downstream channel execution.

Innovator activity in second-line PBC agents shapes escalation pathways and indirectly supports UDCA volumes. Seladelpar and elafibranor won accelerated approvals with response rates that significantly exceeded placebo, and both position UDCA as the base in combination regimens for inadequate responders. This pairing reinforces the role of UDCA as the backbone in specialty hepatology even as prescribers escalate to newer agents. The 2025 withdrawal of obeticholic acid removed a prior alternative and shifted non-responder care toward PPAR agonists plus UDCA. For the ursodeoxycholic acid market, these shifts reduce substitution risk and preserve baseline volumes while compressing branded margins in finished-dose generics.

Channels and technology also influence competition as hospital, retail, and online pharmacies demand reliable supply and integration. Digital pharmacy models and e-prescribing create incentives for manufacturers to enable direct-to-platform agreements for faster fulfillment in chronic therapy. Label reliability and dosing clarity across presentations support adherence, which is vital in lifelong regimens. API suppliers with diversified feedstocks and validated processes continue to secure multi-year agreements in regulated markets. The net result is a competitive landscape that favors cost leadership upstream and distribution agility downstream, both of which are central to sustained share in the ursodeoxycholic acid market.

Ursodeoxycholic Acid Industry Leaders

Teva Pharmaceutical Industries Ltd.

Dr. Falk Pharma GmbH

Daewoong Pharmaceutical (INDIA) Pvt. Ltd.

Grindeks

Apotex Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Ice Pharma, one of the players in ursodeoxycholic acid (UDCA) APIs announced a strategic expansion beyond its core active pharmaceutical ingredient business to enter higher-value markets, including finished dosage forms, nutraceuticals, and specialty excipients. By leveraging its vertically integrated bile acid platform, the company aims to develop new bile acid applications and create additional growth opportunities across pharmaceutical and health-focused sectors.

- July 2025: ICE Pharma inaugurated a new production block at Raichem India dedicated to chicken-bile UDCA, adding 120 metric tons of raw UDCA capacity per year and enhancing global supply resilience.

Global Ursodeoxycholic Acid Market Report Scope

The scope of the ursodeoxycholic acid market report comprises the global production, distribution, and sale of ursodeoxycholic acid finished formulations used primarily to treat chronic liver diseases such as primary biliary cholangitis (PBC) and cholesterol gallstones.

The ursodeoxycholic acid market is segmented by indication, dosage form, distribution channel, and geography. Indication covers primary biliary cholangitis, gallstone dissolution and prophylaxis, cholestatic liver diseases (non-PBC), primary sclerosing cholangitis, and others, such as intrahepatic cholestasis of pregnancy and cystic fibrosis-associated hepatobiliary disorders. The dosage form includes tablets, capsules, and oral suspension. The distribution channel includes hospital pharmacies, retail pharmacies & drug stores, and online pharmacies. Geography spans North America, Europe, Asia-Pacific, the Middle East and Africa, and South America with standard country-level breakouts. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. All forecasts are provided in terms of value in USD.

| Primary Biliary Cholangitis (PBC) |

| Gallstone Dissolution and Prophylaxis |

| Cholestatic Liver Diseases (non-PBC) |

| Primary Sclerosing Cholangitis (PSC) |

| Other Indications |

| Tablets |

| Capsules |

| Oral Suspension |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Indication | Primary Biliary Cholangitis (PBC) | |

| Gallstone Dissolution and Prophylaxis | ||

| Cholestatic Liver Diseases (non-PBC) | ||

| Primary Sclerosing Cholangitis (PSC) | ||

| Other Indications | ||

| By Dosage Form | Tablets | |

| Capsules | ||

| Oral Suspension | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| Online Pharmacies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the ursodeoxycholic acid market?

The ursodeoxycholic acid market size was USD 620.1 million in 2025 and is set to reach USD 986.9 million by 2031 at an 8.37% CAGR over 2026-2031.

Which indication contributes the most to ursodeoxycholic acid demand in 2026?

PBC remains the largest indication, anchored by first-line guideline use and stable long-term therapy, which keeps the core of the ursodeoxycholic acid market intact.

Where are the fastest growth opportunities by channel and form?

Online pharmacies and oral suspensions show the fastest growth rates through 2031, supported by telemedicine adoption and dosing flexibility in pediatric and geriatric care.

Which region will contribute the most incremental growth by 2031?

Asia-Pacific is projected to grow at 10.45% CAGR through 2031, supported by expanding bariatric surgery programs, improving reimbursement, and rising treated prevalence.

What supply-side actions are most relevant to ensuring availability?

Vertical integration, multi-feedstock strategies like chicken-bile sourcing, and new capacity in India and China support consistent API supply and lower the risk of bottlenecks.

Page last updated on: