Urometer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

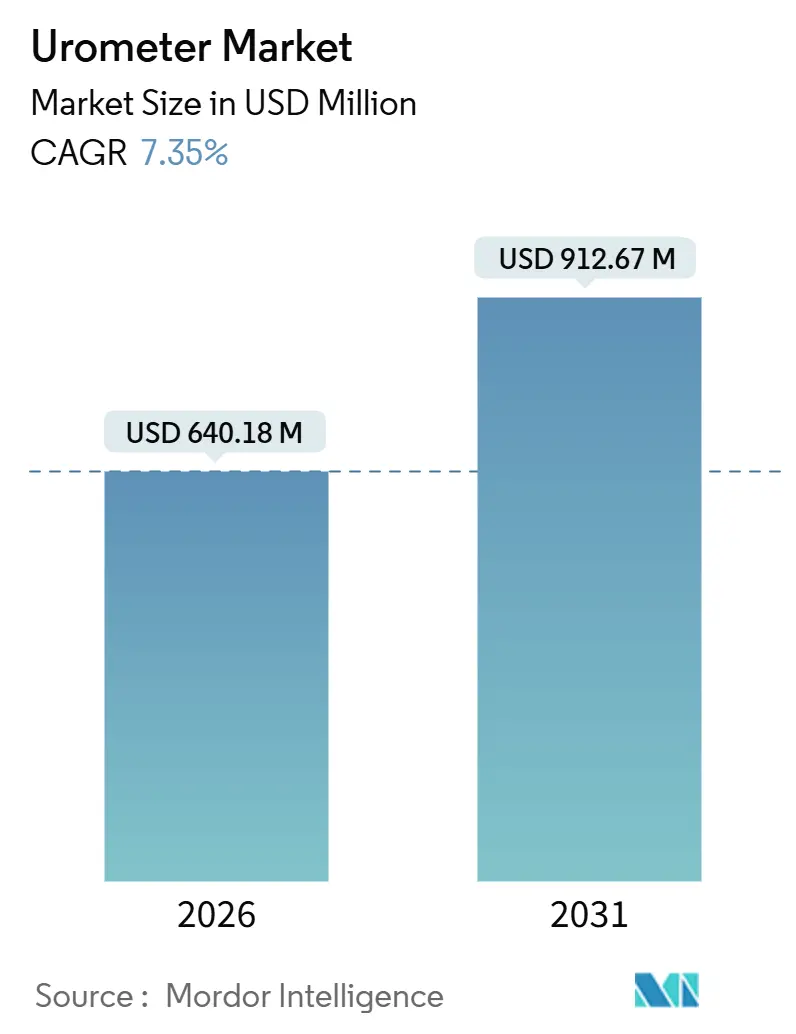

| Market Size (2026) | USD 640.18 Million |

| Market Size (2031) | USD 912.67 Million |

| Growth Rate (2026 - 2031) | 7.35% CAGR |

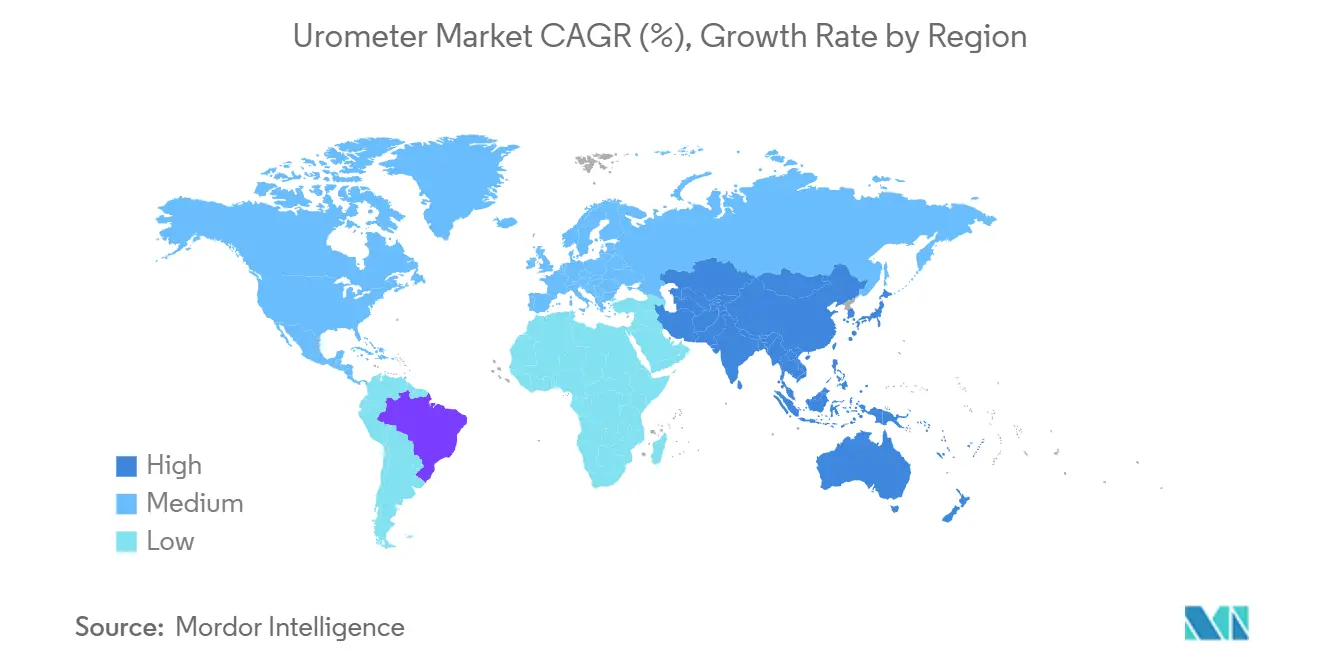

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urometer Market Analysis by Mordor Intelligence

The Urometer Market size is estimated at USD 640.18 million in 2026, and is expected to reach USD 912.67 million by 2031, at a CAGR of 7.35% during the forecast period (2026-2031).

The market is driven by increasing surgical volumes, a rising prevalence of perioperative acute kidney injuries, and the widespread adoption of goal-directed fluid therapy, prompting hospitals and home-care providers to invest heavily in real-time urine-output monitoring solutions. North America dominates revenue generation, supported by robust reimbursement frameworks, while the Asia-Pacific region is experiencing the fastest growth, driven by the expansion of critical-care infrastructure in China and India. Premium-priced connected devices with predictive analytics are gaining traction; however, cost-sensitive buyers in low-resource regions continue to prefer basic gravity-drainage models. Additionally, environmental regulations in Europe and evolving cybersecurity standards in the United States are influencing product design cycles and operational costs.

Key Report Takeaways

- By end-user, hospitals held 53.87% of 2025 revenue; home healthcare is the fastest climber at a 10.23% CAGR to 2031

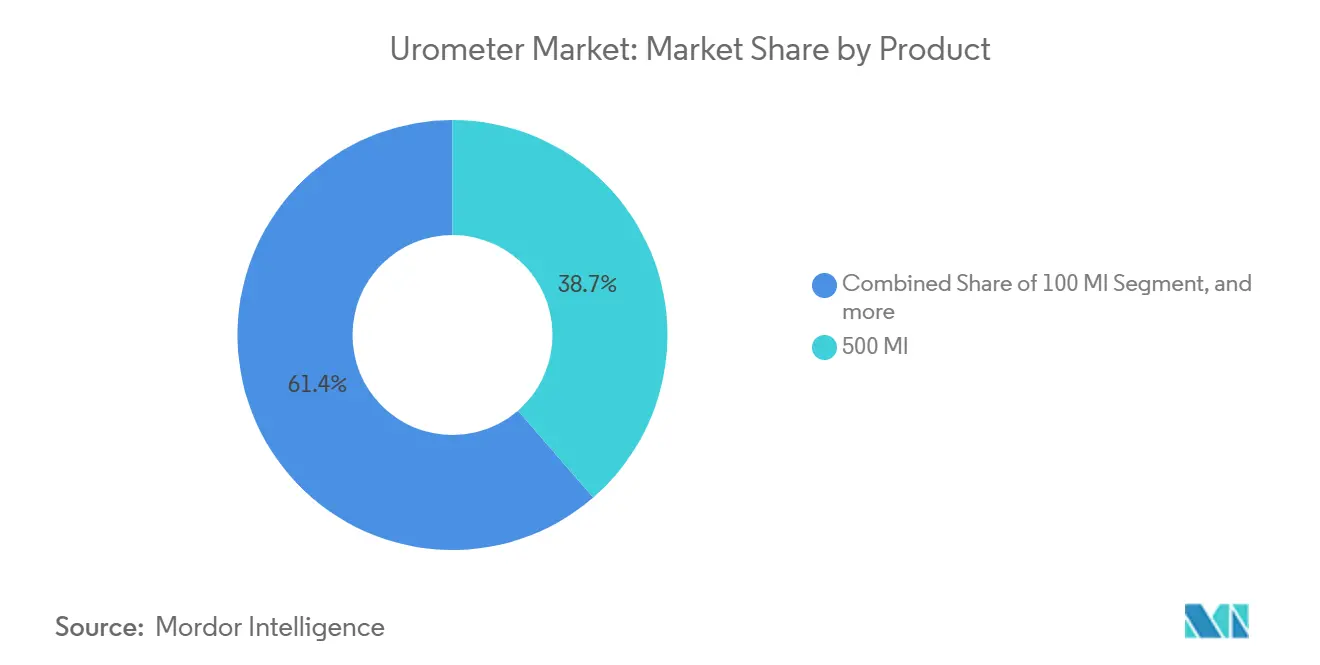

- By product capacity, 500 mL systems led with a 38.65% revenue share in 2025; devices above 500 mL are forecast to expand at a 9.65% CAGR through 2031

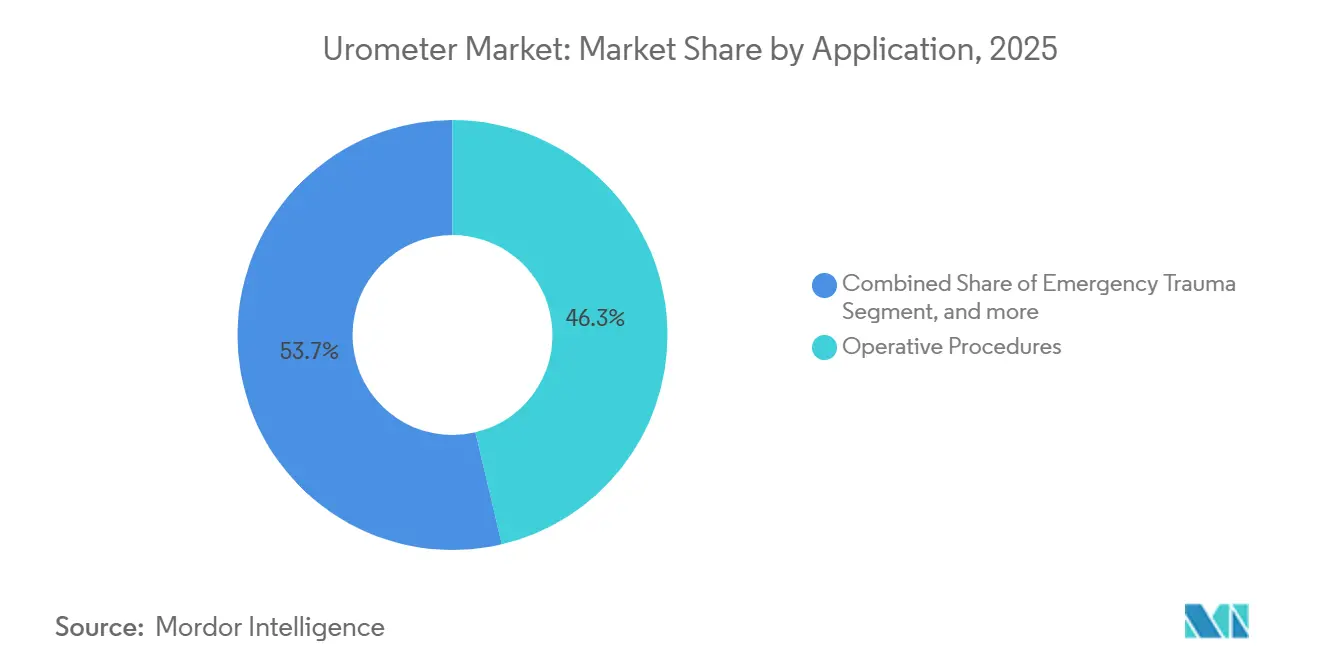

- By application, operative procedures captured 46.32% of the urometer market share in 2025; palliative care is set to grow at 9.77% CAGR through 2031

- By geography, North America contributed 42.87% of 2025 sales; Asia-Pacific is projected to register an 8.43% CAGR during the outlook period

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Urometer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Urinary Tract and Kidney Disorders | +1.2% | Global, with higher intensity in North America and Europe due to aging demographics | Long term (≥ 4 years) |

| Increasing Surgical and Critical Care Admissions | +1.8% | Global, concentrated in North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Technological Advancements in Urine Output Monitoring Devices | +1.5% | North America and Europe lead adoption; Asia-Pacific following with 2-3 year lag | Medium term (2-4 years) |

| Expanding Healthcare Infrastructure and Expenditure | +1.3% | Asia-Pacific core, spillover to Middle East & Africa; sustained growth in North America | Long term (≥ 4 years) |

| Growing Preference for Home-Based Patient Monitoring | +1.0% | North America and Europe dominate; emerging in urban Asia-Pacific markets | Short term (≤ 2 years) |

| Integration of Digital Health and Connectivity Solutions | +0.9% | North America and Europe early adopters; gradual penetration in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Urinary Tract and Kidney Disorders

Chronic kidney disease affects 788 million people worldwide, and urinary tract infections number in the billions each year. These conditions increase the need for early detection of fluid imbalances, making real-time urine-output tracking a front-line tool in both general wards and critical-care units. Clinicians now intervene when urine output dips below 0.5 mL/kg/h—often 12–24 hours before serum creatinine rises—embedding urometers into sepsis and post-operative protocols. U.S. and E.U. regulators continue to classify urometers as Class II devices, requiring 510(k) or MDR conformity, which assures reliability but lengthens product cycles.

Increasing Surgical and Critical Care Admissions

U.S. hospitals perform 48 million inpatient and 58.3 million outpatient surgeries yearly, while intensive-care admissions exceed 5.7 million. Enhanced Recovery After Surgery guidelines now stipulate hourly urine-output targets, extending device use to minimally invasive cases. Cardiac units, where AKI incidence can reach 50%, rely on continuous urine data to titrate diuretics and vasopressors, reducing dialysis needs by up to 20%[1]American Heart Association, “Cardiac Surgery and AKI,” heart.org. China mirrors this trend with more than 50 million surgeries each year and rapid ICU-bed construction, embedding digital urometers from day-one in new facilities.

Technological Advancements in Urine-Output Monitoring Devices

IEEE standard 11073-10422, published in 2024, enables plug-and-play connectivity with electronic health records[2]IEEE Standards Association, “11073-10422 Urine Analyzers,” ieee.org. Becton Dickinson’s PureWick Portable Collection System, launched November 2025, lets patients ambulate while the device transmits data wirelessly, shaving half a day off average length of stay in ERAS pathways. Potrero Medical’s Accuryn platform pairs urine flow with intra-abdominal pressure, predicting AKI six to eight hours sooner than serum markers. Vendors able to layer predictive analytics onto hardware are achieving 25–30% price premiums.

Expanding Healthcare Infrastructure and Expenditure

United States health spending hit USD 4.9 trillion in 2024 and is tracking toward USD 7.2 trillion by 2031. Asia-Pacific outpaces in relative terms: China and India are adding critical-care beds at record speed, and new builds are pre-wired for digital monitoring, cutting retrofit costs by as much as 40%. These greenfield installations favor fully integrated urometer stations over stand-alone gravity units, lifting average selling prices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Costs and Budget Constraints in Low-Resource Settings | -0.8% | Sub-Saharan Africa, South Asia, and rural Latin America; limited impact in OECD markets | Long term (≥ 4 years) |

| Stringent Regulatory and Reimbursement Barriers | -0.6% | Global, with highest friction in Europe (MDR compliance) and emerging Asia-Pacific markets | Medium term (2-4 years) |

| Data Security and Interoperability Challenges | -0.4% | North America and Europe where HIPAA and GDPR enforcement is strictest | Short term (≤ 2 years) |

| Environmental Concerns Over Plastic Medical Waste | -0.3% | Europe leading with Extended Producer Responsibility mandates; emerging in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Costs and Budget Constraints in Low-Resource Settings

Basic gravity-drainage units cost USD 15–50, while connected models run USD 200–400, exceeding budgets in regions where annual per-capita health spend can be under USD 150. Total cost of ownership climbs further once training and IT support are added. Leasing and pay-per-use pilots exist but lack broad reimbursement, confining uptake to urban tertiary centers.

Stringent Regulatory and Reimbursement Barriers

Europe’s Medical Device Regulation, fully active since May 2024, lengthens certification by up to 18 months[3]European Commission, “Medical Device Regulation Guidance,” ec.europa.eu. In the United States, connected devices with embedded software algorithms require extensive validation under Software-as-a-Medical-Device rules, driving submission costs above USD 500,000. Outpatient and home-care settings still lack dedicated CPT codes, pushing providers to absorb device outlays.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: High-Volume Formats Gain in Extended Care

The 500 mL category generated 38.65% of 2025 revenue, anchored in general surgery and orthopedic wards where monitoring spans 12–24 hours. Above-500 mL models are expanding at a 9.65% CAGR, reflecting growth in trauma and sepsis care that favors fewer bag changes and reduced nurse workload. Smaller 400–450 mL units serve pediatric centers, while 100–200 mL designs focus on neonatal ICUs. The urometer market size for the above-500 mL segment is projected to climb to USD 360 million by 2031, outpacing every other capacity tier. IEEE-compliant digital sensors and antimicrobial coatings are now bundled into premium 500 mL devices, pushing average selling prices up by 15–20%.

Battery power and Bluetooth connectivity are moving from novelty to baseline. Becton Dickinson’s PureWick system allows early ambulation and has cut average length of stay by nearly one day in Enhanced Recovery After Surgery programs. Potrero’s Accuryn adds intra-abdominal pressure sensing, turning the bag into a decision-support node rather than a passive collector.

By Application: Palliative Care Emerges as Growth Frontier

Operative procedures retain 46.32% of 2025 revenue, underpinned by 48 million inpatient surgeries in the United States and equivalent momentum in Europe and China. Palliative care, however, shows the quickest runway at a 9.77% CAGR as global end-of-life populations seek home-based symptom control. The urometer market share for palliative applications is forecast to double by 2031 as remote monitoring technologies mature. Emergency-trauma and outpatient urology remain important but secondary contributors.

Design shifts mirror this usage mix. Home-care models must withstand lay handling, run on consumer Wi-Fi or LTE, and ship with intuitive disposable chambers. Observe Medical’s Sippi platform delivers on these needs and gained CE clearance in 2024. Hospitals continue to deploy advanced systems for operative and trauma use, yet shorter monitoring windows in minimally invasive surgery are trimming per-case consumption even as case volumes rise.

By End-User: Home Healthcare Disrupts Hospital Dominance

Hospitals commanded 53.87% of 2025 sales, but a robust 10.23% CAGR positions home-care agencies to erode that lead. The urometer market size attached to home settings is on course to surpass USD 200 million by 2031. Clinics and skilled-nursing facilities claim the rest of demand, with adoption rates tied closely to reimbursement clarity.

Connected platforms drive home-care traction. CMS remote-monitoring codes support recurring revenue streams, enabling vendors to bundle hardware and charge subscription fees for analytics. RenalSense’s Clarity RMS, targeted for acquisition by Nuwellis, exemplifies the move toward software-as-a-service deployments. Hospitals are responding by integrating bedside devices into enterprise analytics stacks, preserving their central role yet ceding some volume to decentralized care.

Geography Analysis

North America generated 42.87% of 2025 revenue, anchored by USD 4.9 trillion in health spending and robust ICD-10 billing that bundles urometers into DRG payments. FDA pathways remain predictable, but new cybersecurity rules add six-to-nine-month extensions for connected-device reviews. Teleflex’s decision to divest its acute-care line for USD 2.03 billion illustrates how reimbursement scrutiny is driving portfolio realignment toward higher-margin niches.

Asia-Pacific is the growth engine at an 8.43% CAGR. China executes more than 50 million surgeries a year and is adding over a million new hospital beds between 2024 and 2026. India, while lower on per-capita spend, is expanding critical-care infrastructure under universal-coverage mandates. Greenfield construction often includes digital urometer stations from inception, sparing retrofit expenses and boosting average order values.

Europe holds a mid-twenties share, yet MDR compliance and environmental rules elevate costs. Extended Producer Responsibility adds logistics burdens, and economic pressures in southern states lengthen replacement cycles. Germany, France, and the United Kingdom dominate regional demand, while the Middle East, Africa, and South America remain single-digit contributors due to budget limitations, except in Gulf Cooperation Council hubs where spending parallels North American norms.

Competitive Landscape

The urometer market is moderately fragmented. B. Braun, Becton Dickinson, and Teleflex leverage broad catalogs and global sales teams to capture mid-teens percentages each. Digital-native challengers—Observe Medical, Potrero Medical, RenalSense—differentiate through IoT connectivity and predictive analytics, securing hospital pilots and early home-care contracts. Teleflex’s USD 2.03 billion divestiture deal underlines conglomerates’ shift toward higher-margin verticals, opening room for mid-tier acquirers to gain scale.

Technology is the new fault line. Potrero’s Accuryn integrates pressure data for AKI prediction; RenalSense’s Clarity RMS sells analytics on a subscription basis; and Observe Medical positions Sippi for caregiver-friendly home use. IEEE interoperability standards lower entry barriers, but FDA cybersecurity demands and EU sustainability rules raise ongoing compliance costs. Vendors able to harmonize connectivity, data security, and circular-economy packaging are best placed to expand share.

Urometer Industry Leaders

Becton, Dickinson & Co. (BD)

Teleflex Inc

Medline Industries LP

ConvaTec Group pl

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Teleflex agreed to sell its Acute Care and Interventional Urology units to Intersurgical and a Montagu-Kohlberg consortium for USD 2.03 billion

- November 2025: Becton Dickinson introduced the PureWick Portable Collection System, a battery-powered mobile urometer

- November 2025: Boston Scientific completed its USD 3.7 billion takeover of Axonics, broadening its continence-care offerings

- August 2025: Nuwellis signed a letter of intent to acquire RenalSense’s Clarity RMS analytics platform.

Global Urometer Market Report Scope

As per the scope of the report, a urometer is a medical device used to accurately measure and monitor urine output. It is commonly employed in hospitals to assess kidney function and fluid balance. The device typically consists of a graduated container or a specialized measuring system.

The The Urometer Market is Segmented by Product (100 Ml, 200 Ml, 400 Ml, 450 Ml, 500 Ml, and Above 500 Ml), Application (Operative Procedures, Emergency Trauma, Palliative Care, and Others), End-User (Hospitals, Clinics, Home Healthcare, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| 100 Ml |

| 200 Ml |

| 400 Ml |

| 450 Ml |

| 500 Ml |

| Above 500 Ml |

| Operative Procedures |

| Emergency Trauma |

| Palliative Care |

| Others |

| Hospitals |

| Clinics |

| Home Healthcare |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product | 100 Ml | |

| 200 Ml | ||

| 400 Ml | ||

| 450 Ml | ||

| 500 Ml | ||

| Above 500 Ml | ||

| By Application | Operative Procedures | |

| Emergency Trauma | ||

| Palliative Care | ||

| Others | ||

| By End-User | Hospitals | |

| Clinics | ||

| Home Healthcare | ||

| Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the current value of the urometer market?

The urometer market size is USD 640.18 million in 2026 with a forecast to reach USD 912.67 million by 2031.

Which region grows fastest for urometer demand?

Asia-Pacific leads growth at an 8.43% CAGR, propelled by expanding surgical volumes and ICU capacity.

How are connected urometers changing hospital workflows?

Bluetooth-enabled and cloud-linked systems cut manual charting errors, enable early AKI alerts, and can shave up to one day from surgical recovery times.

Why is home healthcare important for urometer vendors?

CMS remote-monitoring codes support monthly reimbursements, encouraging device use after hospital discharge and driving a 10.23% CAGR in home settings.

What are the main regulatory hurdles for new urometers?

Compliance with FDA cybersecurity mandates, European MDR rules, and data-privacy laws lengthens approval timelines and raises development costs.

Page last updated on: