Urinary Drainage Bags Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 2.79 Billion |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

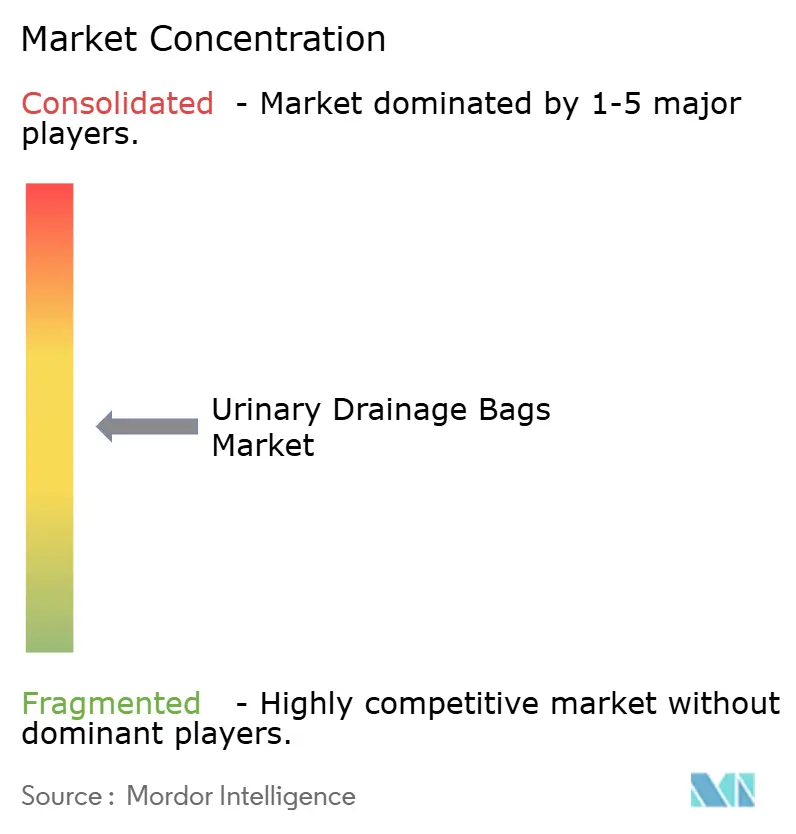

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Urinary Drainage Bags Market Analysis by Mordor Intelligence

The Urinary Drainage Bags Market size is expected to increase from USD 2.12 billion in 2025 to USD 2.22 billion in 2026 and reach USD 2.79 billion by 2031, growing at a CAGR of 4.69% over 2026-2031.

The urinary drainage bags market is supported by a growing elderly population, rising surgical procedure volumes, and a stronger clinical focus on preventing catheter-associated urinary tract infections. Demand is shifting across care settings as hospital-led catheter management increasingly extends into home care, influencing product selection and repeat purchases. Premium suppliers are strengthening their positions with anti-reflux designs, latex-free and silicone-based formats, and bundled continence care models, while lower-cost suppliers remain active in price-sensitive tenders. However, substitution from intermittent catheterization and continued pricing pressure in institutional procurement are keeping market growth measured.

Key Report Takeaways

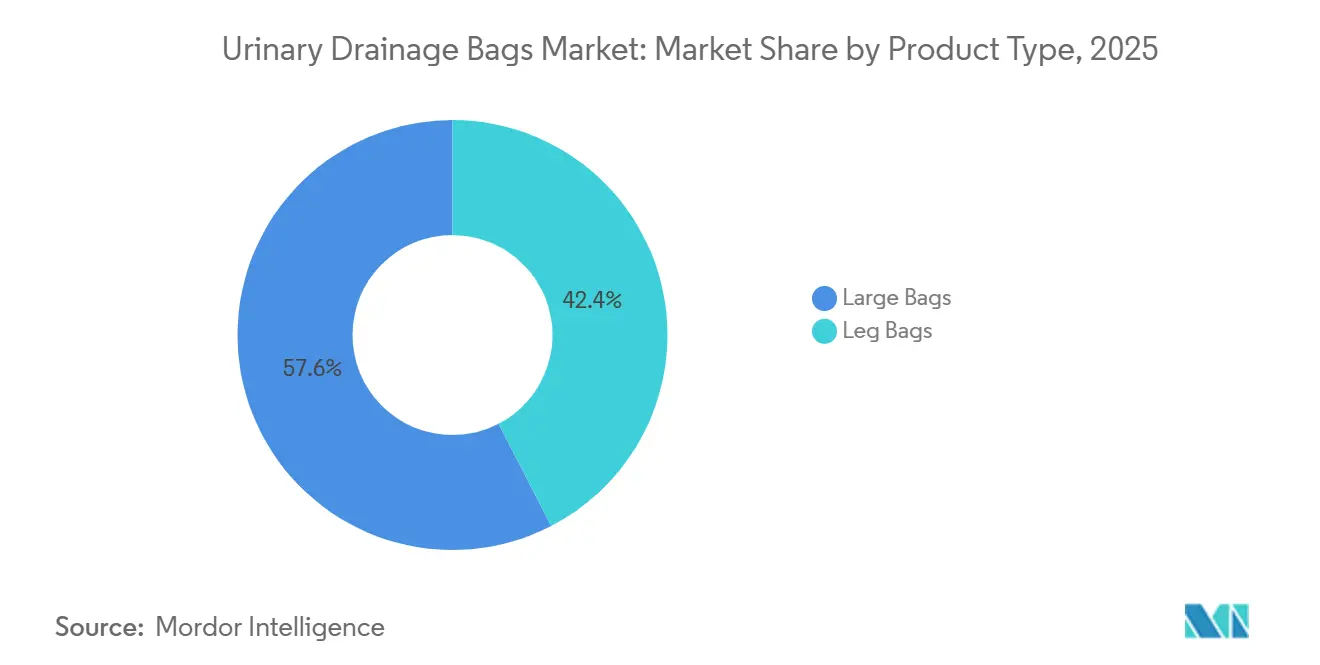

- By product type, leg bags held 57.60% of revenue in 2025 and are projected to grow at a 5.30% CAGR through 2031.

- By usage type, disposable bags represented 59.55% of revenue in 2025, while disposable urinary drainage bags are projected to grow at a 4.90% CAGR through 2031.

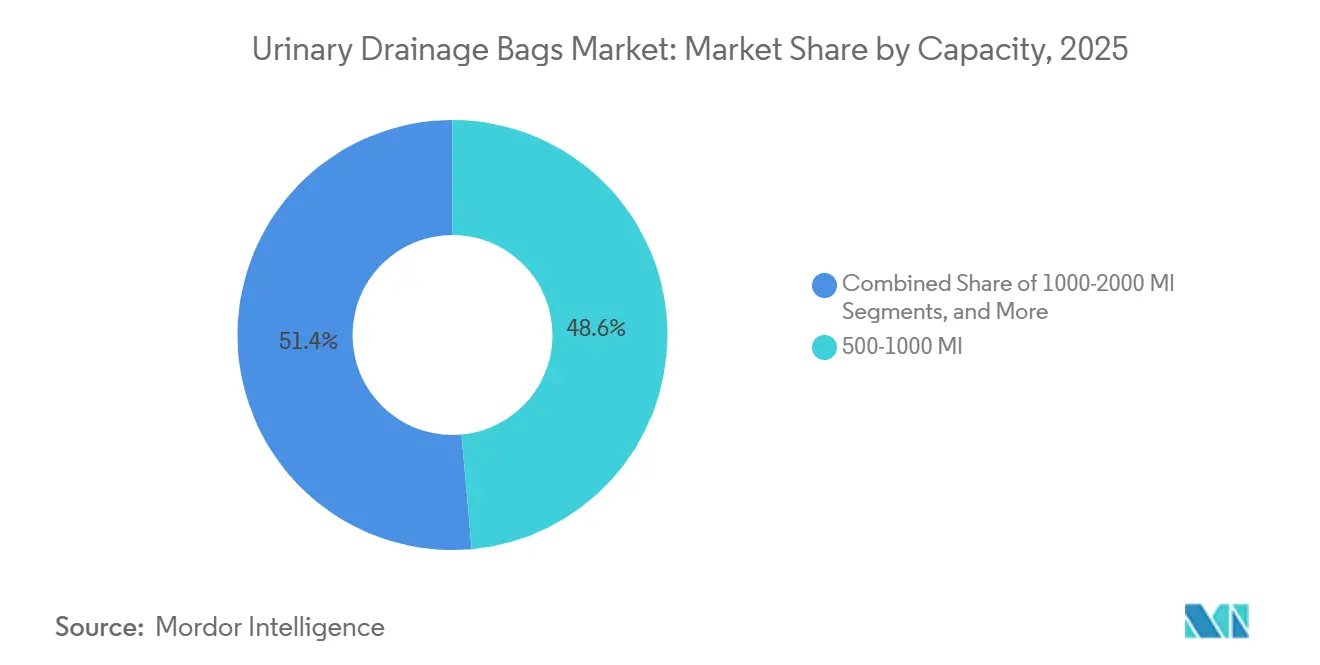

- By capacity, the 500-1000 Ml segment accounted for 48.58% of revenue in 2025, while the 0-500 Ml segment is projected to expand at a 5.60% CAGR through 2031.

- By end user, hospitals accounted for 47.89% of revenue in 2025, while home healthcare is projected to advance at a 5.15% CAGR through 2031.

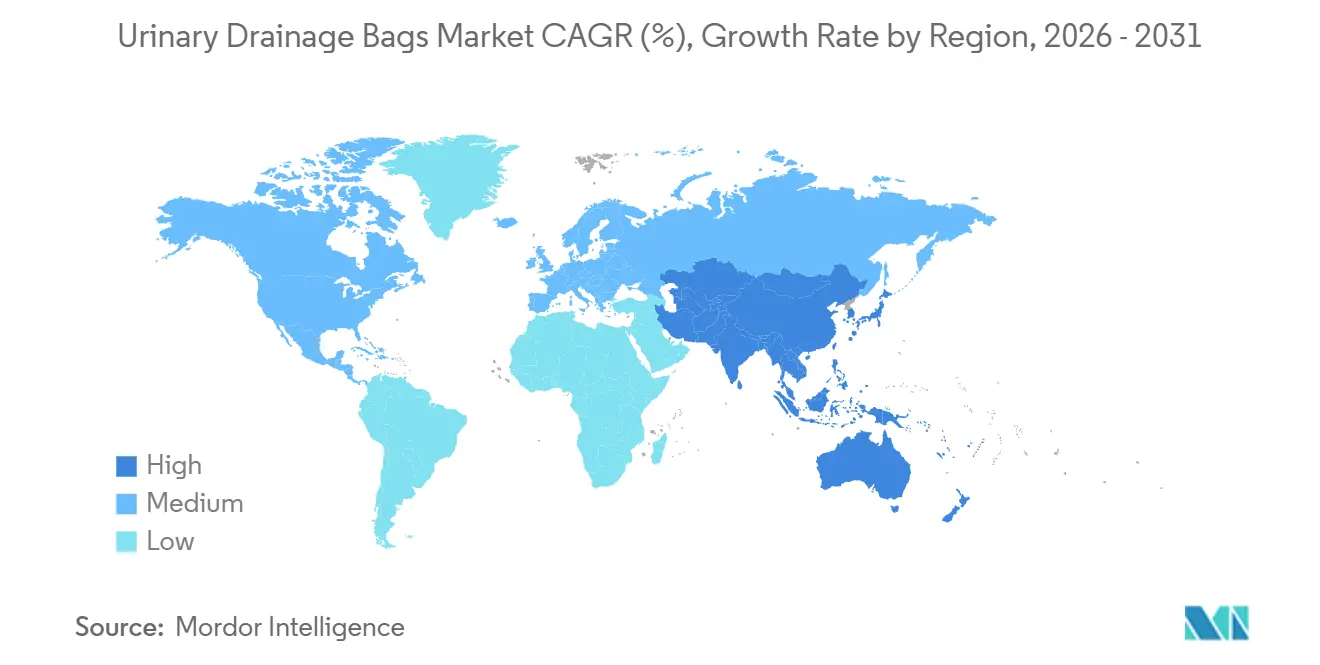

- By geography, North America held 39.95% of revenue in 2025, while Asia-Pacific is projected to grow at a 5.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Urinary Drainage Bags Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising burden of urinary incontinence and retention | +1.5% | Global, with highest concentration in North America and Europe | Long term (≥ 4 years) |

| Growth in postoperative urinary management needs | +0.9% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Expanding home-based continence care pathways | +0.8% | North America, Europe, APAC emerging markets | Medium term (2-4 years) |

| Infection-control upgrades, latex-free and anti-reflux | +0.6% | North America and EU, with spillover to core APAC markets | Short term (≤ 2 years) |

| Reimbursement pressure favoring standardized low-cost solutions | +0.5% | North America, Western Europe | Medium term (2-4 years) |

| Under-recognized demand from long-stay mobility-limited patients | +0.3% | Global, concentrated in APAC and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden Of Urinary Incontinence and Retention

Urinary incontinence and urinary retention remain key demand drivers for the urinary drainage bags market. The World Health Organization identifies incontinence as a core geriatric syndrome that often occurs alongside frailty, limited mobility, and cognitive decline, keeping it central to care planning for older adults. In Europe, the condition affects 25% to 45% of women and up to 40% of the broader population. Its economic burden was estimated at EUR 69.2 billion (USD 79.08 billion) in 2023 and is projected to reach EUR 86.7 billion (USD 99.08 billion) by 2030. Demand is rising faster among people aged 80 years and older, the fastest-growing group in several mature healthcare systems, while improved screening and care pathways continue to expand the treated patient base.[1]“Review, Incontinence Prevalence, Socioeconomic, and Environmental Costs of Urinary Incontinence in the European Union,” European Urology, sciencedirect.com

Growth In Postoperative Urinary Management Needs

Postoperative urinary retention continues to support the urinary drainage bags market, as catheterization remains a common practice after many procedures. A 2025 study in the Journal of the American Academy of Orthopaedic Surgeons reports that postoperative urinary retention can affect up to 43% of orthopedic surgery patients, keeping drainage bag use closely linked to perioperative care.[2]“Trends in Perioperative Urinary Catheter Utilization by Surgical Procedure Type in the United States, 2010 to 2017, Evidence From the Nationwide Inpatient Sample,” World Journal of Surgery, doi.org In the United States, published research states that nearly 30 million indwelling urethral catheters are placed each year across medical and surgical settings, with most placements tied to hospital-based care. As elective procedures recover and expand, the market continues to benefit from steady demand for catheter-associated drainage products, with clinical protocols shifting preference toward anti-reflux and infection-resistant systems for sensitive postsurgical periods.

Expanding Home-Based Continence Care Pathways

The shift of continence and catheter management into home settings is reshaping growth in the urinary drainage bags market. Home-based care requires products with easier handling, lower-profile wear, improved odor control, and simpler drainage steps. Product selection in this setting depends on comfort and repeat use, not only institutional purchasing rules. BD’s planned November 2025 launch of the PureWick Portable Collection System indicates that major manufacturers are developing products for active mobility and non-hospital use, supporting demand for discreet, ergonomic, and patient-friendly collection systems.

Infection-Control Upgrades, Latex-Free and Anti-Reflux

Infection prevention is reshaping product specification standards across the urinary drainage bags market. The 2025 APIC CAUTI Implementation Guide states that urinary tract infections account for more than 30% of infections in acute care hospitals, with nearly half associated with indwelling urinary catheters. This burden is driving provider preference for closed drainage systems with anti-reflux valves, sampling ports, and improved outlet designs over simple open-system formats. The 2025 position paper from the International Society for Infectious Diseases also reinforces strict aseptic maintenance and regular review of catheter necessity, supporting premium positioning for infection-resistant products as hospitals treat these features as a practical standard.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Infection risk, leakage anxiety, and user non-compliance | -0.8% | Global | Long term (≥ 4 years) |

| Hospital budget compression and tender-driven pricing | -0.7% | North America and EU | Medium term (2-4 years) |

| Disposal, odor, and biomedical waste handling burden | -0.4% | Global, concentrated in APAC and MEA | Medium term (2-4 years) |

| Substitution risk from intermittent catheterization and alternative modalities | -0.6% | North America, Western Europe, high-income APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Infection Risk, Leakage Anxiety, and User Non-Compliance

The urinary drainage bags market faces constraints from infection concerns, leakage anxiety, odor issues, and the social burden of visible catheter use, which can reduce acceptance and lead to early discontinuation. The World Health Organization’s ICOPE guidance recommends absorbent products as the first containment option when catheterization is not clinically required, limiting broader use in community and long-term care settings.[3]World Health Organization, “WHO ICOPE Training Programme, Module 16, Urinary Incontinence,” World Health Organization, who.int In home settings, poor handling practices, such as incorrect bag positioning, irregular emptying, or improper reconnection, can reduce the perceived benefits of higher-quality systems. This restraint is more evident in lower-resource settings, where limited patient education and follow-up support continue to affect adoption and pricing in the urinary drainage bags market.

Hospital Budget Compression and Tender-Driven Pricing

Budget pressure continues to limit value capture in the urinary drainage bags market. Group purchasing organizations and public tenders continue to reduce unit prices, especially for standardized bag formats that suppliers struggle to differentiate in contract-based procurement. Hospitals require better infection-control products, but finance teams face pressure to control consumable spending, creating a balance between clinical quality and cost discipline. This environment favors suppliers that can justify premium pricing with stronger clinical and economic evidence, while mid-tier suppliers face more commodity-like competition and weaker pricing power across institutional channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Leg Bags Drive Ambulatory Catheter Management

Leg bags are expected to account for 57.60% of revenue in 2025, giving them the leading position in the urinary drainage bags market. Their share reflects a steady shift toward ambulatory-compatible formats that better support daily mobility and home care use. Patients and caregivers value their compact design, adjustable fixation, and discreet wear, which make leg bags easier to use outside hospital settings. This format also supports a wider pricing ladder than large bedside bags, as it includes basic home-use products as well as premium silicone and anti-reflux variants. This broader product mix creates a stronger value opportunity for the urinary drainage bags market than standardized inpatient bags.

By Usage Type: Disposables Gain Share on Infection-Control Imperative

Disposable urinary drainage bags are projected to register a 4.90% CAGR from 2026 to 2031, making them the faster-growing usage format in the urinary drainage bags market. Disposable bags are expected to represent 59.55% of revenue in 2025, while reusable alternatives remain relevant mainly in home care settings where cost control matters and users can manage manual cleaning more consistently. Infection-control expectations, rather than simple affordability, shape the difference between the two formats. APIC guidance states that the drainage system should remain a sterile closed circuit, and any disconnection is considered a break in prevention practice, supporting wider disposable use in acute care. As a result, hospital procurement is steadily shifting toward single-use systems in the urinary drainage bags market.

By Capacity: Mid-Range Volumes Anchor Hospitals, Compact Formats Accelerate

The 500-1,000 mL segment is expected to hold 48.58% of revenue in 2025, remaining the volume center of the urinary drainage bags market. This range fits standard hospital collection needs because it balances safe fill levels with fewer bag changes during typical nursing shifts. It supports moderate urine output and everyday ward use without adding excess weight for patients. At the same time, the 0-500 mL segment is projected to grow at a 5.60% CAGR through 2031, making it the fastest-growing capacity tier in the urinary drainage bags market.

By End User: Hospitals Anchor Volume, Home Care Captures Value Growth

Hospitals are expected to account for 47.89% of end-user revenue in 2025, maintaining their position as the largest care setting in the urinary drainage bags market. Their leading position reflects the fact that catheterization often begins in acute care after surgery, trauma, or neurological events. Hospitals also remain the primary demand center for standardized high-volume procurement, especially for bedside and overnight drainage applications. Despite this scale, the faster growth path now lies outside hospitals. Home healthcare is projected to register a 5.15% CAGR from 2026 to 2031, making it the most dynamic end-user channel in the urinary drainage bags market.

Geography Analysis

North America accounted for 39.95% of revenue in 2025, making it the largest regional segment in the urinary drainage bags market. The United States remains the primary demand center, supported by high catheter use across hospital, surgical, and home-based care settings. Nearly 30 million indwelling urethral catheters are placed each year in the country across medical and surgical settings, creating a large recurring base for drainage products. Canada adds stable demand through an aging population and broad healthcare coverage, while Mexico benefits from expanding private hospital capacity and rising continence care awareness.

Europe remains a large and structurally important region in the urinary drainage bags market, with Germany, the United Kingdom, and France supporting the largest regional demand pools. The prevalence burden remains substantial, with a broad base of continence-related needs that continues to increase with age. Germany remains especially important, as an aging population and strong specialist access support the continued use of advanced catheter and drainage solutions. In parts of Western Europe, preference is shifting toward silicone-based formats for longer dwell times, while Italy, Spain, and the rest of Europe remain more price sensitive.

Asia-Pacific is projected to grow at a CAGR of 5.34% from 2026 to 2031, making it the fastest-growing geography in the urinary drainage bags market. The region’s rapidly expanding elderly population and growing focus on integrated care for older adults continue to support demand. China is expanding hospital and urological care capacity, Japan has a mature home care base, and India and South Korea are adding demand through healthcare expansion and demographic change. South America is benefiting from infrastructure investment, led by Brazil and Argentina, while the Middle East and Africa remain earlier-stage markets driven mainly by hospital expansion in the Gulf and gradual home care adoption in South Africa.

Competitive Landscape

The urinary drainage bags market is moderately concentrated at the premium end, though it is not fully consolidated. Coloplast A/S, Becton, Dickinson and Company, ConvaTec Group Plc, Hollister Incorporated, and B. Braun SE maintain strong positions through broad continence care portfolios, long-standing clinical relationships, and bundled catheter-plus-bag supply models. These companies compete on product reliability, infection-prevention features, and service support rather than unit price alone. Regional and Asian manufacturers remain competitive in tender-based and cost-sensitive channels, keeping the market balanced between scale advantages and active price competition.

Leading companies are expanding competition beyond standard drainage bags. BD is expected to expand its PureWick platform in November 2025 with the PureWick Portable Collection System, targeting active users and wheelchair mobility in addition to institutional care settings. In April 2026, BD is also expected to publish new clinical evidence from 13 U.S. clinical sites showing improved nighttime sleep and comfort among women using the BD PureWick Urine Collection System, strengthening the commercial case for non-invasive urine management in home settings. Coloplast is expected to complete the acquisition of Uromedica in February 2026, while Boston Scientific announced an agreement in January 2026 to acquire Valencia Technologies, reflecting continued interest in adjacent continence technologies.

ConvaTec has signaled a stronger competitive push, with company disclosures indicating more than USD 1 billion in long-term R&D investment, including capacity expansion and continued focus on continence care development. These initiatives show that broader portfolio development across continence and urology care is shaping the urinary drainage bags market, along with line extensions. The shift from PVC-dependent formats toward silicone and latex-free materials is raising the bar for manufacturing capability and clinical positioning. Sensor-enabled drainage monitoring also presents an opportunity, but no supplier has achieved scaled clinical adoption in this area.

Urinary Drainage Bags Industry Leaders

B. Braun SE

Coloplast A/S

ConvaTec Group Plc

Hollister Incorporated

Cardinal Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: HR HealthCare acquired SteriGear LLC, including Fig Leaf urinary drainage devices and the covers and drapes portfolio, expanding its urology solutions across acute, post-acute, and home-based care settings.

- April 2026: Becton, Dickinson and Company published U.S. clinical evidence from 13 sites showing improved sleep and comfort among women using the BD PureWick Urine Collection System for nighttime urinary incontinence.

- February 2026: Coloplast completed the acquisition of Uromedica Inc., adding implantable balloon therapies for male and female stress urinary incontinence, with products used in over 16,000 patients worldwide.

- October 2025: ConvaTec announced plans to invest over USD 1 billion in R&D in the United States and the United Kingdom over the next decade, including USD 600 million for U.S. activities.

Global Urinary Drainage Bags Market Report Scope

As per the scope of the report, a urinary drainage bag is a sterile, flexible medical device connected to a catheter to collect urine from the bladder. Used for urinary incontinence, retention, or post-surgery recovery, the bag sits below the bladder level to allow continuous gravity drainage.

The urinary drainage bags market is segmented by product type, usage type, capacity, and end user. By product type, the market includes large bags and leg bags. By usage type, the market is segmented into reusable urinary drainage bags and disposable urinary drainage bags. By capacity, the market is categorized into 0-500 mL, 500-1,000 mL, and 1,000-2,000 mL. By end user, the market is segmented into hospitals, clinics, home healthcare, ambulatory surgical centers, and others.

| Large Bags |

| Leg Bags |

| Reusable Urinary Drainage Bags |

| Disposable Urinary Drainage Bags |

| 0-500 Ml |

| 500-1000 Ml |

| 1000-2000 Ml |

| Hospitals |

| Clinics |

| Home Healthcare |

| Ambulatory Surgical Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Large Bags | |

| Leg Bags | ||

| By Usage Type | Reusable Urinary Drainage Bags | |

| Disposable Urinary Drainage Bags | ||

| By Capacity | 0-500 Ml | |

| 500-1000 Ml | ||

| 1000-2000 Ml | ||

| By End User | Hospitals | |

| Clinics | ||

| Home Healthcare | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current and forecast value of the urinary drainage bags space?

The urinary drainage bags market size stands at USD 2.22 billion in 2026 and is projected to reach USD 2.79 billion by 2031, growing at a 4.69% CAGR.

Which product type leads urinary drainage bag demand?

Leg bags led the category with 57.60% of revenue in 2025 because they fit ambulatory use and home care needs more effectively than larger institutional formats.

Which usage format is growing faster, disposable or reusable urinary drainage bags?

Disposable urinary drainage bags are growing faster, with a projected 4.90% CAGR from 2026 to 2031, as infection-control standards favor closed single-use systems.

Which capacity range is most important today?

The 500-1000 Ml segment held 48.58% of revenue in 2025 because it aligns well with common hospital collection needs and standard nursing shift patterns.

Which end-user setting offers the strongest growth opportunity?

Home healthcare is the fastest-growing end-user segment, with a projected 5.15% CAGR through 2031, as more urological care moves outside hospitals.

Which region leads and which region is growing fastest?

North America led with 39.95% of revenue in 2025, while Asia-Pacific is expected to grow fastest at a 5.34% CAGR through 2031.

Page last updated on: