Unnatural Amino Acids Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.58 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 8.70% CAGR |

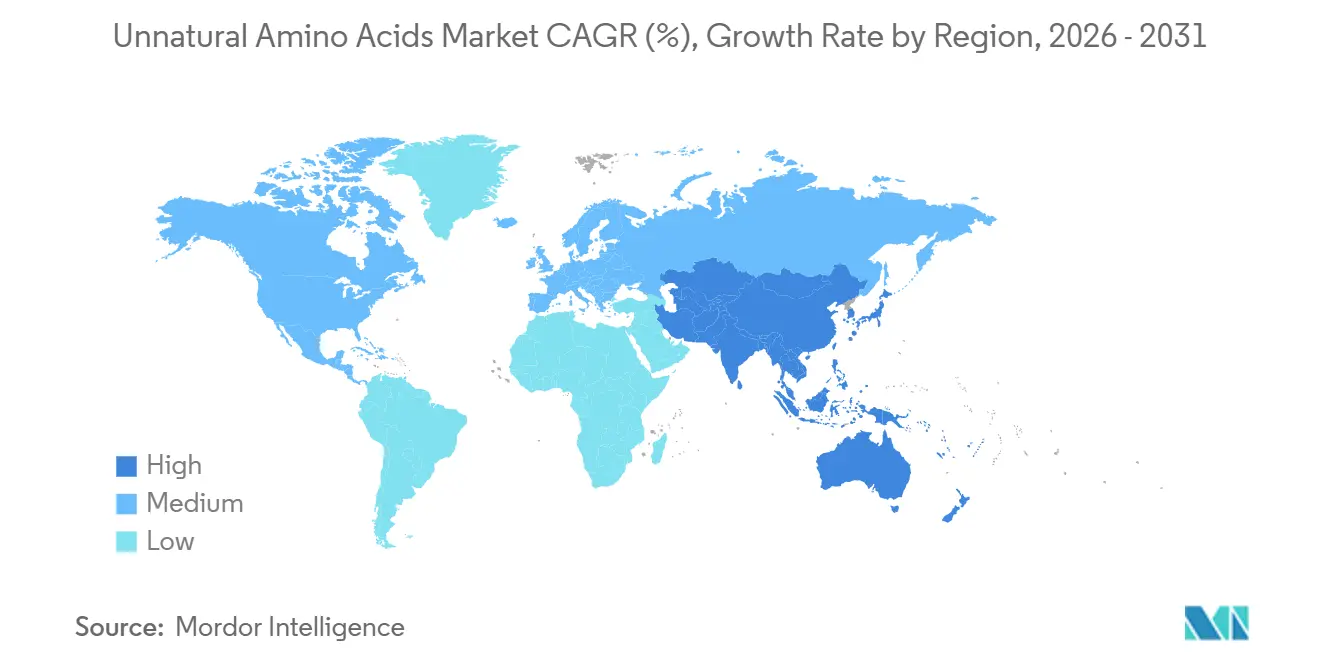

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

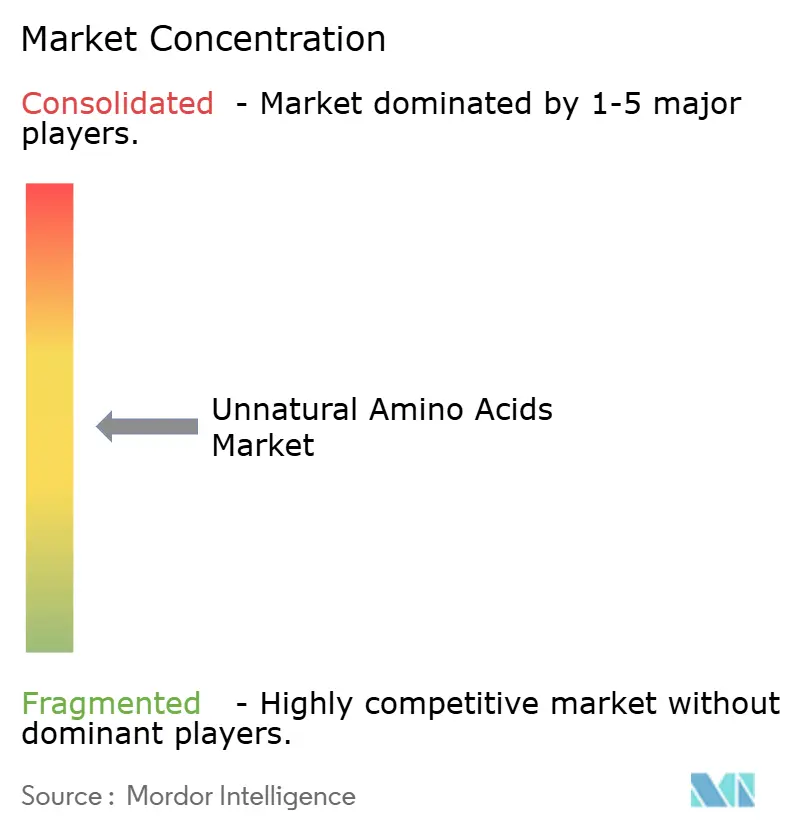

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unnatural Amino Acids Market Analysis by Mordor Intelligence

The Unnatural Amino Acids Market size is projected to expand from USD 1.45 billion in 2025 and USD 1.58 billion in 2026 to USD 2.39 billion by 2031, registering a CAGR of 8.70% between 2026 to 2031.

The unnatural amino acids market is expanding as drug developers increasingly use these molecules to improve therapeutic stability, extend half-life, and enhance target selectivity. Semaglutide remains a key commercial example, as its use of α-aminoisobutyric acid helps prevent rapid cleavage and supports its role in a leading drug franchise. Market growth is also supported by rising activity in oral GLP-1 therapies, expanding antibody-drug conjugate pipelines, and increasing commercial-scale demand. Competition centers on a small group of GMP-capable suppliers expanding peptide and building block capacity in North America and Europe as sourcing scrutiny increases. However, cost pressure for complex protected residues, efficiency limitations in advanced incorporation systems, and a narrow pool of qualified suppliers continue to restrain market expansion.

Key Report Takeaways

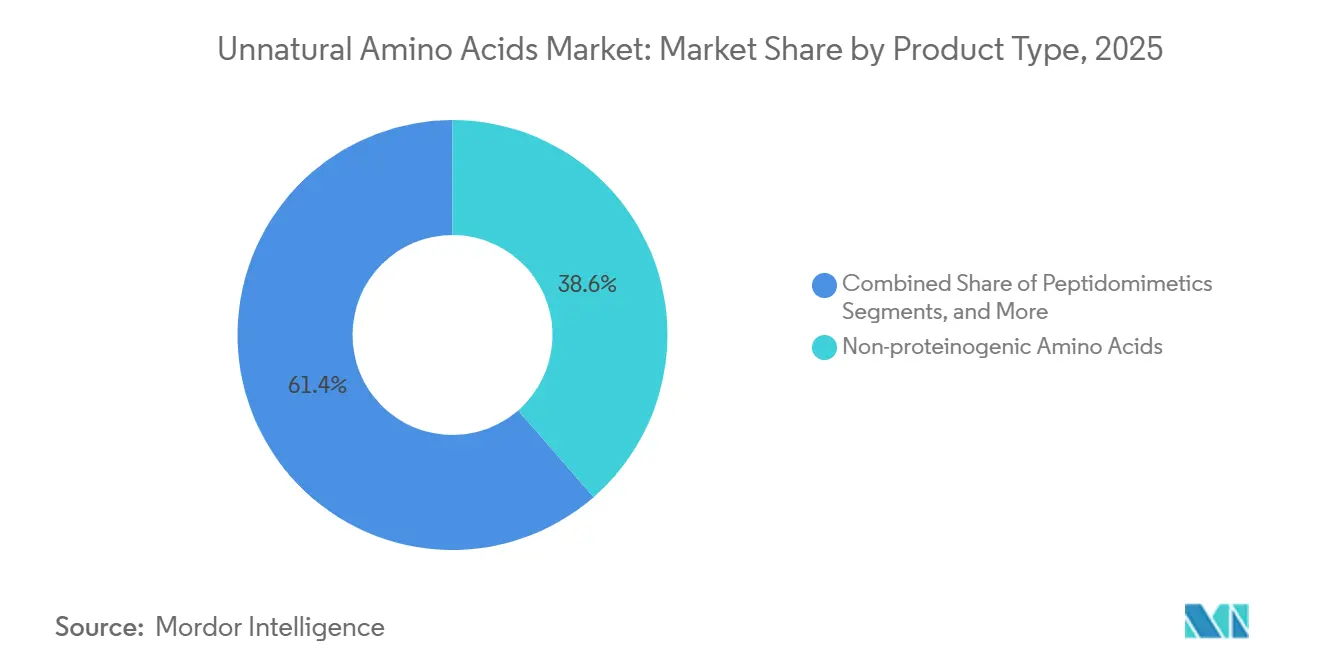

- By product type, non-proteinogenic amino acids held 38.60% of revenue in 2025, while peptidomimetics are projected to grow at an 11.45% CAGR through 2031.

- By application, pharmaceuticals accounted for 43.80% of revenue in 2025, while food and beverage is projected to expand at a 10.67% CAGR through 2031.

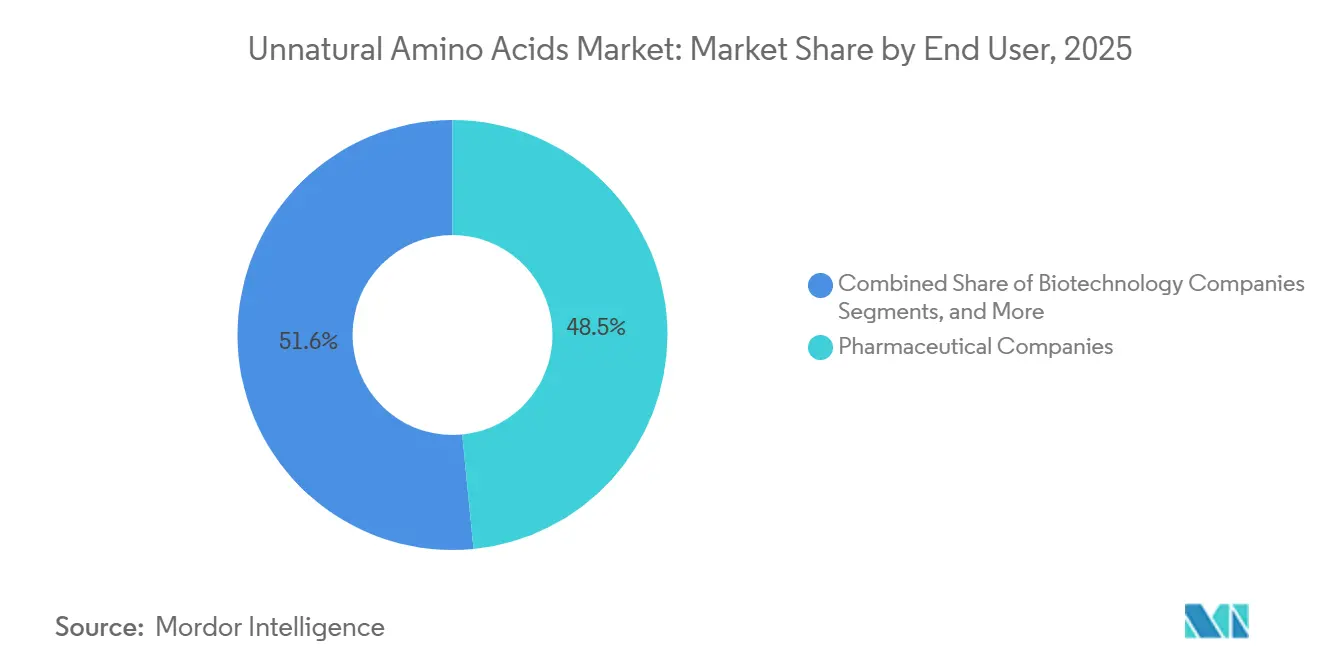

- By end user, pharmaceutical companies held 48.45% of revenue in 2025, while biotechnology companies are projected to grow at a 13.10% CAGR through 2031.

- By synthesis technology, chemical synthesis held 52.80% of revenue in 2025 and is projected to grow at a 12.40% CAGR through 2031.

- By geography, North America held 43.30% of revenue in 2025, while Asia-Pacific is projected to record the fastest CAGR of 11.56% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Unnatural Amino Acids Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in peptide therapeutics pipeline and FDA approvals | +2.3% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Expansion of genetic code expansion technologies | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising adoption in ADC and PDC development | +1.4% | Global, with North America leading and China scaling | Medium term (2-4 years) |

| Increasing pharmaceutical and biopharmaceutical R&D expenditure | +0.9% | Global | Long term (≥ 4 years) |

| Growth of CDMO outsourcing for custom UAA synthesis | +0.8% | Global, with Asia-Pacific growing fastest | Medium term (2-4 years) |

| Demand for protease-resistant and metabolically stable therapeutic peptides | +0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Peptide Therapeutics Pipeline and FDA Approvals, Including GLP-1 Receptor Agonists

The unnatural amino acids market is expected to gain strong near-term momentum from the rapid expansion of peptide therapeutics and new approval activity. Novo Nordisk is expected to receive FDA approval for Wegovy in adults with noncirrhotic MASH with moderate to advanced liver fibrosis in August 2025, expanding the commercial reach of a therapy closely linked to amino acid engineering. The company is then expected to announce U.S. approval of the first oral GLP-1 medicine for weight management in December 2025, supporting more peptide-based follow-on programs. Eli Lilly’s Foundayo, expected to be approved in 2026 as the first non-peptidic oral GLP-1 agonist, is likely to validate the oral GLP-1 category and push peptide developers to improve half-life and protease resistance. This trend supports demand for protected building blocks used in screening, optimization, and manufacturing, while a 2025 review in Amino Acids is expected to highlight the role of unnatural residues in reducing immune response.

Expansion of Genetic Code Expansion Technologies for Site-Specific Protein Modification

The commercial progress of genetic code expansion technologies is expected to support the unnatural amino acids market. A 2026 study in Nature Chemistry is expected to show that rare codon recoding enabled the simultaneous incorporation of up to five distinct non-canonical amino acids into a single protein while maintaining commercially relevant expression performance.[1]Novo Nordisk, “Wegovy Approved by FDA for the Treatment of Adults with Noncirrhotic MASH with Moderate to Advanced Liver Fibrosis,” novonordisk.mediaroom.com This development addresses a long-standing limitation that restricted many genetic code expansion tools to research settings. A 2025 report in Nature is also expected to describe RNA codon expansion through programmable pseudouridine editing, creating a cell-free route for site-specific incorporation without amber suppression.[2]Springer Nature, “Unnatural Amino Acids in Peptide Therapeutics,” springer.com These advances expand the range of proteins and conjugates that can carry precise functional handles and increase the value of suppliers offering strong analytical packages and consistent quality.

Rising Adoption in Antibody-Drug Conjugate and Peptide-Drug Conjugate Development

The unnatural amino acids market is gaining momentum from the shift toward site-specific conjugation in antibody-drug conjugates and peptide-drug conjugates. Ajinomoto’s AJICAP platform demonstrates how amino acid chemistry can enable direct, site-specific payload conjugation to native antibodies without antibody re-engineering. The platform is expected to secure a licensing agreement with Astellas Pharma in October 2025, indicating that value is shifting beyond supply toward platform access and process know-how. Ajinomoto Bio-Pharma Services and Piramal Pharma Solutions are expected to announce a strategic collaboration in April 2026 to support ADC development and manufacturing through integrated use of AJICAP. A 2025 Journal of Medicinal Chemistry study is also expected to show that unnatural amino acids engineered into peptide linkers can enable cathepsin-selective ADC behavior in HER2-positive breast cancer.[3]Nature Chemistry, “Rare Codon Recoding Enables Multi Site Incorporation of Non Canonical Amino Acids,” nature.com

Increasing Global Pharmaceutical and Biopharmaceutical R&D Expenditure

The unnatural amino acids market continues to benefit from sustained pharmaceutical and biopharmaceutical R&D spending. This trend is important because many unnatural amino acid-intensive programs focus on oncology, metabolic disease, and advanced peptide design, where technical complexity and commercial value remain high. Larger R&D budgets support more screening libraries, candidate iterations, and clinical supply activities, increasing procurement volumes for specialized residues. The outsourcing model further supports market growth as CDMOs manage more development work, purchase building blocks directly, and build repeat supply relationships with qualified manufacturers. This shift moves purchasing from one-off project demand to broader platform-level sourcing and increases the value of suppliers that offer research, clinical, and commercial grades within one network.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High cost of chemical synthesis and production scale-up challenges | -1.3% | Global, with greater pressure in developing markets | Medium term (2-4 years) |

| Stringent regulatory and GMP requirements for novel UAA drug substances | -0.9% | North America and Europe | Long term (≥ 4 years) |

| Limited commercial supplier base for specialized non standard amino acids | -0.7% | Global | Medium term (2-4 years) |

| Incorporation efficiency limits in cell based genetic code expansion systems | -0.5% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Chemical Synthesis and Challenges in Production Scale-Up

The unnatural amino acids market continues to face a significant cost barrier in producing pharmaceutical-grade protected residues. A 2025 Nature Communications study on multi-enzyme cascade synthesis indicated that non-canonical amino acids can be produced from glycerol at a cost well below conventional chemical routes, while select chemically produced building blocks were benchmarked at USD 984/kg. However, enzymatic routes still face purity, validation, and GMP translation challenges, limiting their near-term replacement of chemical synthesis.[4]Nature, “RNA Codon Expansion via Programmable Pseudouridine Editing,” nature.com Solid-phase peptide synthesis requires specialized reactor systems, chiral chemistry expertise, and recovery capabilities, making installation costly and rapid scale-up difficult. This cost structure limits supplier participation in high-purity commercial contracts and keeps prices elevated for highly modified and novel residues that have not yet reached broader manufacturing scale.

Stringent Regulatory and GMP Requirements for Novel UAA-Containing Drug Substances

The unnatural amino acids market also operates under a demanding regulatory framework when new residues enter drug substance development. Developers must provide detailed characterization of novel building blocks, including purity, impurities, stereochemistry, and stability, which extends development timelines even when the chemistry is well understood. This burden is manageable for established catalog products but increases significantly for custom structures developed in medicinal chemistry programs. Bachem’s Building K in Bubendorf is expected to require inspection at the end of 2025 before commercial batch production can begin in 2026, showing that even experienced suppliers face long qualification cycles for new GMP assets. Regulatory uncertainty around advanced platforms, such as genetic code expansion for live production systems, can delay commercialization decisions and keep early volumes below their technical potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Peptidomimetics Commanding Forward Momentum

Non-proteinogenic amino acids are expected to account for 38.60% of revenue by product type in 2025, giving them the largest base in the unnatural amino acids market. Their leadership reflects broad structural coverage, including beta amino acids, N-methylated residues, phosphorylated analogs, and ring-constrained variants used across oncology, metabolic disease, and infectious disease programs. The segment benefits from structural diversity rather than dependence on a single commercial therapy, creating a wider demand base than narrower specialty categories. D-amino acids remain strategically important because they improve resistance to protease degradation and support more durable therapeutic performance. Peptidomimetics are projected to grow at an 11.45% CAGR through 2031, making them the fastest-moving product category, supported by stronger stability, better oral potential, and improved access to protein-protein interaction targets.

By Application: Pharmaceutical Dominance Persists as Food and Beverage Accelerates

Pharmaceuticals are expected to account for 43.80% of the unnatural amino acids market size in 2025, keeping this application at the center of revenue generation. This position stems from the broad use of these materials in cyclic peptide APIs, GLP-1 analogs, ADC linker building blocks, and stapled peptide candidates that require pharma-grade supply. The segment also benefits from premium pricing because regulated programs require stricter quality standards and stronger documentation than research-grade purchases. Biotechnology is expected to follow as the second-largest application, supported by recombinant protein engineering and modified cell culture formulations. Food and beverage is forecast to expand at a 10.67% CAGR through 2031, making it the fastest-growing application in the unnatural amino acids market.

By End User: Pharmaceutical Companies Anchor Revenue, Biotech Drives Growth

Pharmaceutical companies are expected to account for 48.45% of end-user revenue in 2025, giving them the leading position in the unnatural amino acids market. Their higher spending reflects the needs of commercial and late-stage programs, including larger volumes, stricter GMP control, and stable long-term supply agreements. GLP-1 analog programs, ADC manufacturing, and peptide API scale-up continue to keep large pharmaceutical demand ahead of research reagent purchasing. Academic and research institutes remain important because they often serve as early buyers of novel residues that later move into broader commercial use. This adoption pattern often shapes the next wave of high-value demand in the unnatural amino acids industry.

Biotechnology companies are projected to grow at a 13.10% CAGR through 2031, making them the fastest-expanding end-user group in the unnatural amino acids market. Their growth is driven by UAA-intensive programs such as ADCs, antibody-oligonucleotide conjugates, and bicyclic peptides that require precise chemistry from early development.

By Synthesis Technology: Chemical Synthesis Retains Scale Advantage

Chemical synthesis is expected to account for 52.80% of revenue in 2025, keeping it the dominant manufacturing route in the unnatural amino acids market. The method remains the preferred option for commercial production because it aligns with Fmoc and Boc protection chemistry and has a mature GMP footprint across peptide manufacturing workflows. Established manufacturers continue to improve throughput and yield through advanced peptide synthesis platforms and reactor expansions. These advantages help chemical synthesis maintain leadership even as sustainability and cost pressures encourage the market to evaluate alternatives. The segment anchors the current supply base while new methods continue to develop around it.

Enzymatic synthesis is emerging as a growth route in the unnatural amino acids market, although the source draft does not provide a standalone CAGR for it. Recent research on modular multi-enzyme cascades showed the conversion of glycerol into multiple non-canonical amino acids with enantiomeric purities ranging from 68.4% to 98.5%, highlighting both technical feasibility and environmental benefits.

Geography Analysis

North America is projected to hold 43.30% of the unnatural amino acids market share in 2025, maintaining its position as the leading regional contributor. The region benefits from a strong concentration of peptide therapeutic development, advanced biotech cluster infrastructure, and high demand for research-grade and clinical-grade building blocks. The United States remains the primary demand center, supported by GLP-1 analog development, ADC activity, and peptide API manufacturing, all of which require protected non-canonical residues at meaningful scale. Approval activity is expected to further support demand, with the oral Wegovy pill anticipated to be cleared in December 2025 and Foundayo expected to be approved in 2026, strengthening confidence in oral GLP-1 development and related analog work. Canada contributes mainly through academic and research procurement, while Mexico remains a smaller but developing demand point linked to CDMO activity.

Europe remains the second-largest geography in the unnatural amino acids market, with Germany, the United Kingdom, France, Italy, and Spain forming the main regional demand base. Germany leads the region due to its strong pharmaceutical manufacturing base, specialty amino acid supply, and active chemical biology research. Regulatory rigor in Europe increases compliance costs, but it also helps qualified suppliers gain preferred status among global buyers seeking reliable peptide-grade inputs. Bachem invested CHF 332.6 million across its site network in 2025 and planned capital expenditure of more than CHF 400 million in 2026, with Building K ramping up toward commercial capacity and reinforcing Europe’s role as a major manufacturing hub.

Asia-Pacific is projected to expand at an 11.56% CAGR through 2031, making it the fastest-growing regional block in the unnatural amino acids market. Growth in the region is driven by rising ADC and peptide development, expanding CDMO capacity, and broader domestic research activity. WuXi TIDES stated in 2026 that it offered more than 2,500 UAA products and had completed more than 12,000 custom UAA synthesis projects over five years, highlighting the depth of regional commercial capability. This supply depth strengthens Asia-Pacific’s position as both a production base and a development market. South America and the Middle East and Africa remain smaller demand centers in the current period, although medium-term expansion opportunities are expected as biopharmaceutical capacity and healthcare investment improve.

Competitive Landscape

The unnatural amino acids market is moderately consolidated at the commercial-scale manufacturing level. Bachem Holding AG, PolyPeptide Group AG, CordenPharma International, and Ajinomoto Co., Inc. remain the leading large-scale competitors, supported by GMP capabilities, peptide synthesis expertise, and long-term supply relationships. Specialty suppliers such as AnaSpec, Iris Biotech, BOC Sciences, GL Biochem, and Peptides International compete through catalog breadth, custom synthesis speed, and structural specialization. This structure creates a two-tier market, where scale and compliance drive pharmaceutical supply, while flexibility supports research and early development demand.

Bachem is expected to strengthen its position through major network investments, including CHF 332.6 million (USD 411.26 million) planned for 2025 and additional 2026 capital plans linked to large-scale peptide and API capacity. CordenPharma committed EUR 900 million (USD 1,026.17 million) to transform its peptide platform in the United States and Europe, highlighting the growing strategic importance of late-stage and commercial supply. The company is also expected to expand its geographic reach and production base through the acquisition of AmbioPharm in May 2026, adding peptide API capacity in South Carolina and Shanghai. Ajinomoto’s AJICAP licensing agreement with Astellas in October 2025 further reflects the commercial value of amino acid-based conjugation platforms and supply capabilities.

White space in the unnatural amino acids market remains strongest in chemoenzymatic integration, differentiated conjugation platforms, and advanced custom synthesis support. Companies that can connect early discovery with regulated manufacturing are better positioned to secure programs before they scale into large-volume contracts. Competitive barriers remain high due to GMP qualification requirements, multi-tonne reactor infrastructure, and proven analytical control. However, the broad supplier base prevents the market from becoming highly concentrated across all customer segments, allowing leading players to dominate the commercial tier while other firms serve research, specialty, and custom demand across the value chain.

Unnatural Amino Acids Industry Leaders

Ajinomoto Co., Inc.

Merck KGaA

Thermo Fisher Scientific Inc.

Ambeed, Inc.

Bachem Holding AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ajinomoto Bio-Pharma Services and Piramal Pharma Solutions formed a strategic collaboration to expand ADC manufacturing capabilities using Ajinomoto’s AJICAP site-specific conjugation platform.

- March 2026: Croda launched its BioXPro amino acid range for bioprocessing and pharmaceutical applications, focusing on high-purity ingredient performance.

- March 2026: Ajinomoto Bio-Pharma Services partnered with NJ Bio, Inc. to extend AJICAP platform access to discovery-stage and early-development clients.

Global Unnatural Amino Acids Market Report Scope

As per the scope of the report, Unnatural amino acids, also known as non-canonical amino acids or non-proteinogenic amino acids, are building blocks that are not naturally encoded by the standard genetic code and do not typically form native proteins. They are either artificially synthesized in a laboratory or occur naturally, but are only incorporated into molecules via specialized pathways or post-translational modifications.

The unnatural amino acids market is segmented by product type, application, end user, synthesis technology, and geography. By product type, the market includes D-amino acids, non-proteinogenic amino acids, peptidomimetics, and other product types. By application, the market is segmented into pharmaceuticals, biotechnology, chemical industry, food and beverage, and other applications. By end user, the market is segmented into pharmaceutical companies, biotechnology companies, academic and research institutes, contract development and manufacturing organizations, and diagnostic and reagent manufacturers. By synthesis technology, the market is segmented into chemical synthesis, enzymatic synthesis, and other synthesis methods. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| D-Amino Acids |

| Non-proteinogenic Amino Acids |

| Peptidomimetics |

| Other Product Types |

| Pharmaceuticals |

| Biotechnology |

| Chemical Industry |

| Food and Beverage |

| Other Applications |

| Pharmaceutical Companies |

| Biotechnology Companies |

| Academic and Research Institutes |

| Contract Development and Manufacturing Organizations |

| Diagnostic and Reagent Manufacturers |

| Chemical Synthesis |

| Enzymatic Synthesis |

| Other Synthesis Methods |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | D-Amino Acids | |

| Non-proteinogenic Amino Acids | ||

| Peptidomimetics | ||

| Other Product Types | ||

| By Application | Pharmaceuticals | |

| Biotechnology | ||

| Chemical Industry | ||

| Food and Beverage | ||

| Other Applications | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Companies | ||

| Academic and Research Institutes | ||

| Contract Development and Manufacturing Organizations | ||

| Diagnostic and Reagent Manufacturers | ||

| By Synthesis Technology | Chemical Synthesis | |

| Enzymatic Synthesis | ||

| Other Synthesis Methods | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the unnatural amino acids space by 2031?

The unnatural amino acids market is forecast to reach USD 2.39 billion by 2031 from USD 1.58 billion in 2026, at a CAGR of 8.70% over 2026 to 2031.

Which application generates the most revenue today?

Pharmaceuticals remained the leading application with 43.80% of revenue in 2025 because regulated peptide, GLP-1, and conjugate programs require high quality specialized inputs.

Which end user group is expanding the fastest through 2031?

Biotechnology companies are projected to grow at a 13.10% CAGR through 2031, supported by rising ADC, AOC, and bicyclic peptide development.

Which product category shows the strongest growth outlook?

Peptidomimetics are projected to expand at an 11.45% CAGR through 2031 because they offer better stability, stronger oral potential, and better access to difficult targets.

Which region leads current demand, and which region is growing fastest?

North America led with 43.30% revenue share in 2025, while Asia-Pacific is forecast to post the fastest growth at an 11.56% CAGR through 2031.

What is the main challenge for suppliers and buyers?

The biggest challenge remains the high cost and scale up complexity of protected pharmaceutical grade residues, along with strict GMP and characterization requirements for novel structures.

Page last updated on: