Unmanned Aerial Systems Camera Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

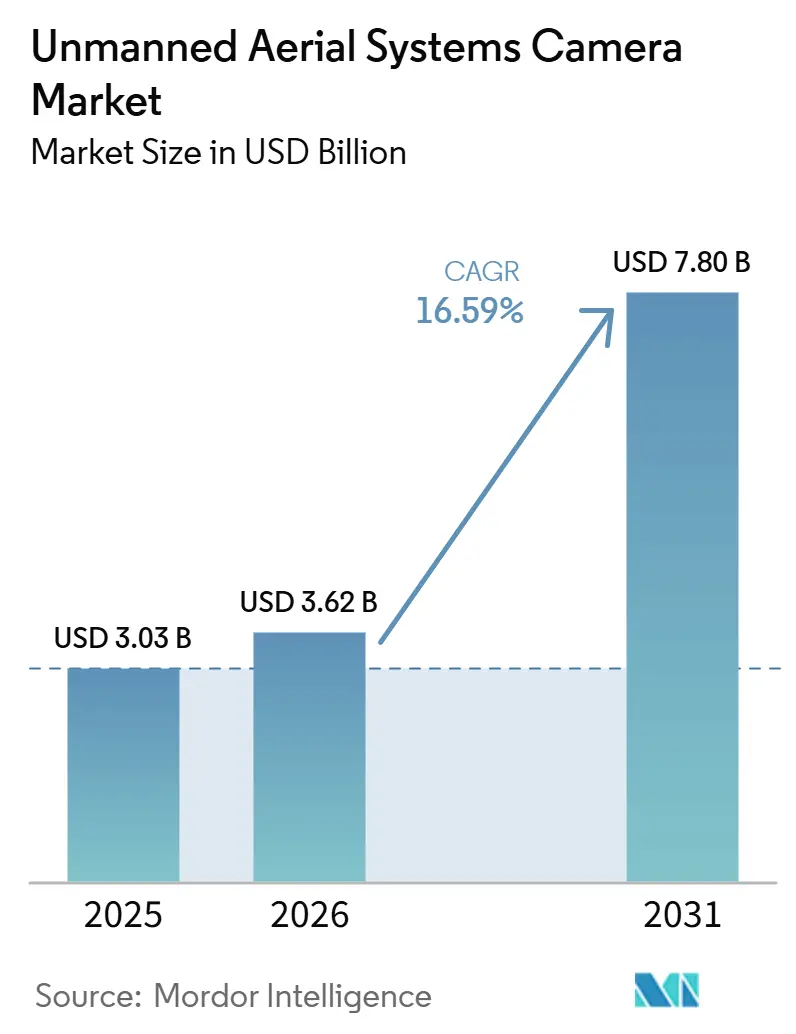

| Market Size (2026) | USD 3.62 Billion |

| Market Size (2031) | USD 7.80 Billion |

| Growth Rate (2026 - 2031) | 16.59% CAGR |

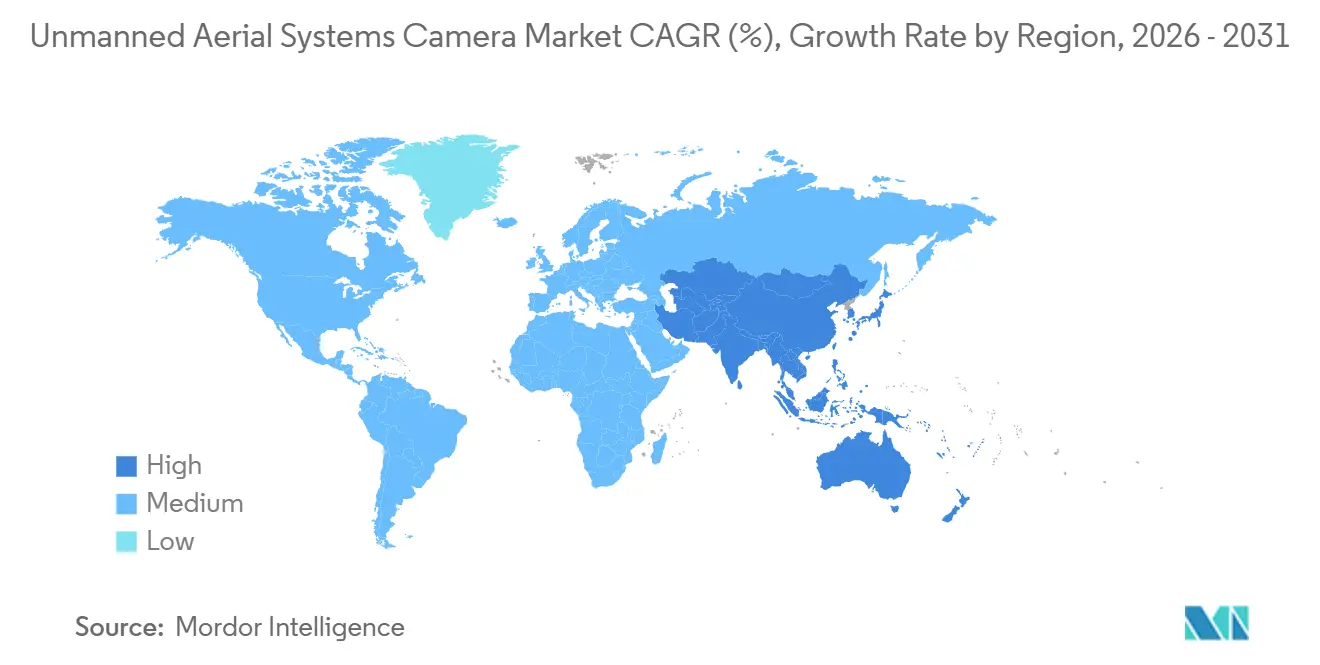

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unmanned Aerial Systems Camera Market Analysis by Mordor Intelligence

The unmanned aerial systems camera market size was valued at USD 3.03 billion in 2025 and estimated to grow from USD 3.62 billion in 2026 to reach USD 7.80 billion by 2031, at a CAGR of 16.59% during the forecast period (2026-2031). Infrared payloads, AI-assisted imaging, and compact multi-sensor designs are shaping demand across defense, industrial inspection, and public safety uses in the unmanned aerial systems camera market. The 2026 expansion reflects stronger adoption of payloads that combine visible-light, thermal, and specialized sensing functions in compact housings that meet weight and power limits for smaller aircraft. The market is also moving toward autonomous and semi-autonomous operations, in which camera systems serve as perception tools that support detection, tracking, and onboard decision support rather than serving only as capture devices. Compliance rules, domestic sourcing priorities, and export-ready product design are shifting more value toward suppliers that can package imaging performance with certification readiness in the unmanned aerial systems camera market. This leaves room for growth in public safety, government surveillance, and continuous asset inspection. At the same time, it also raises pressure on smaller vendors that lack broad product coverage or certified supply chains.

Key Report Takeaways

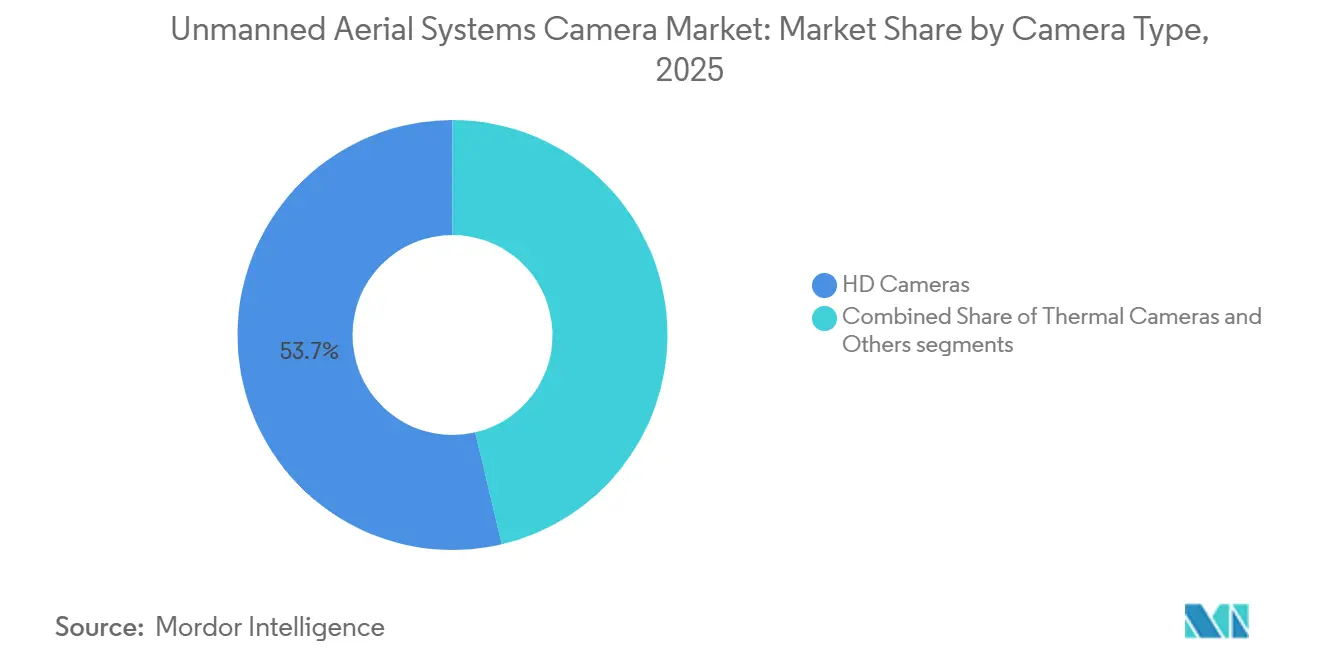

- By camera type, HD cameras accounted for 53.67% of revenue in 2025, while thermal cameras are projected to grow at an 18.65% CAGR through 2031.

- By application, photography and videography accounted for 34.40% of revenue in 2025, while thermal imaging is forecast to grow at a 19.10% CAGR through 2031.

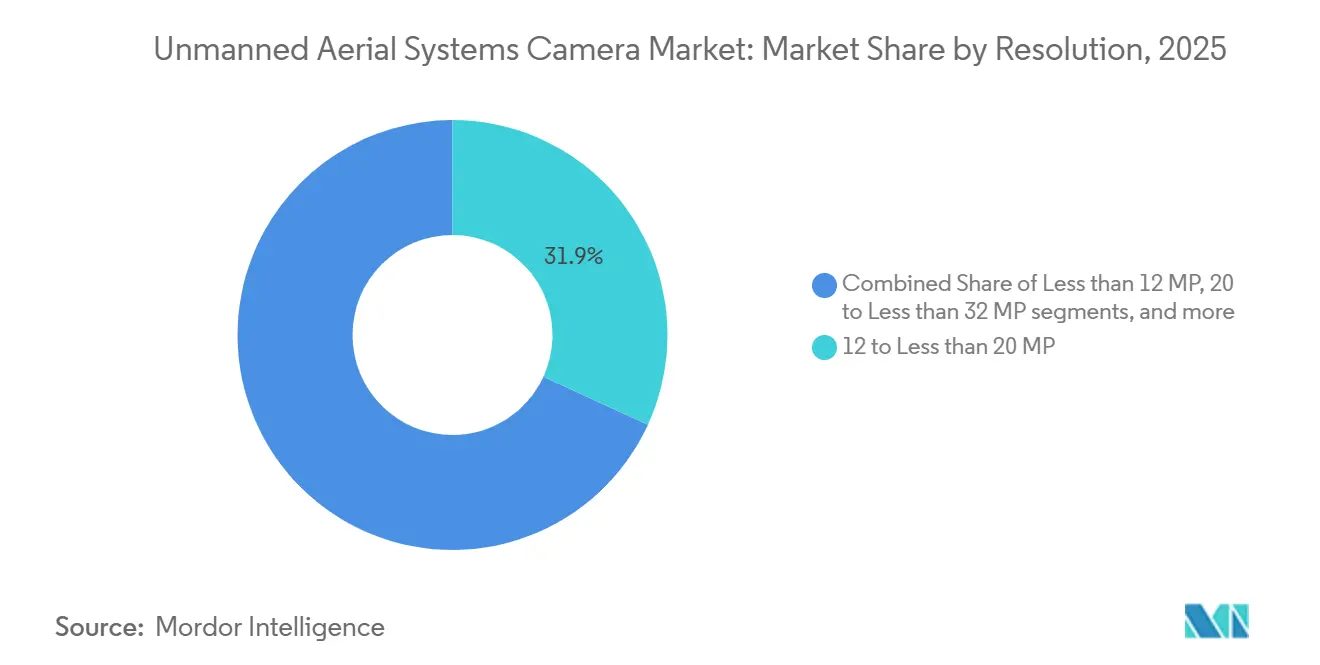

- By resolution, the 12 to 20 MP segment captured 31.85% of revenue in 2025, while the more than 32 MP segment is forecast to expand at a 19.05% CAGR through 2031.

- By end-user, commercial users represented 55.45% of revenue in 2025, while homeland security is forecast to grow at a CAGR of 17.83% through 2031.

- By geography, North America commanded 32.88% of the market share in 2025, while Asia-Pacific is projected to expand at a 17.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Unmanned Aerial Systems Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advancements in AI-enabled onboard image processing systems | +3.20% | Global, led by North America and China | Short term (≤ 2 years) |

| Emergence of SWaP-optimized thermal imaging cores for public safety UAS | +2.70% | North America and Europe, with spill-over to Middle East and Africa | Medium term (2-4 years) |

| Declining cost of high-resolution CMOS imaging sensors | +2.50% | Global | Short term (≤ 2 years) |

| Government incentives driving precision agriculture UAS applications | +2.00% | Asia-Pacific core, with secondary impact in North America | Medium term (2-4 years) |

| Accelerated adoption of FPV drones in commercial cinematography | +1.80% | North America and Europe core, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Progress in satellite-to-UAS optical communications enabling BVLOS operations | +1.50% | Europe and North America core | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advancements in AI-Enabled Onboard Image Processing Systems

AI processing inside the payload is changing what buyers expect from the unmanned aerial systems camera market. The shift reduces dependence on ground stations and supports real-time object recognition, target tracking, and scene interpretation during flight. Gremsy launched the ORUS-L payload in October 2025 with Teledyne FLIR OEM support, combining thermal and EO sensors with an NVIDIA Jetson Orin NX module that delivers 100 TOPS of AI compute in a drone-ready package. That kind of integration shifts the payload from a capture accessory to a self-contained situational-awareness system in the unmanned aerial systems camera market. IEEE research published in 2026 also showed that FPGA-based edge AI pipelines on drone swarms can deliver real-time semantic reasoning without cloud connectivity, thereby supporting the broader use of onboard analytics in field conditions.[1]IEEE ISQED, “Real-Time Edge Semantics for Drone Swarms via FPGA Perception and On-Device LLMs,” IEEE ISQED 2026 Proceedings, doi.org

Government Incentives Driving Precision Agriculture UAS Applications

Public support programs are lowering the barrier to entry for camera-equipped agricultural drones in the unmanned aerial systems camera market. India’s Kisan Drone Yojana 2025 offered subsidies of up to 90% for drones used in crop assessment, spraying, and soil analysis. It provided 100% funding for demonstrations with women-led and SC/ST farmer organizations.[2]Agro Spectrum India, “Kisan Drone Yojana 2025, Govt Offers up to 90% Subsidy, Free Training to Modernize Indian Farming,” Agro Spectrum India, agrospectrumindia.com Madhya Pradesh’s Drone Promotion and Utilization Policy 2025 added a 40% capital investment subsidy, capped at INR 30 crore (USD 3.40 million), for new manufacturing investments. They targeted INR 370 crore (USD 42.20 million) in sector investment over 5 years, along with 8,000 jobs. These programs favor demand for multispectral and near-infrared payloads because crop monitoring and disease detection require more than standard visual capture. As subsidy-backed procurement expands, the unmanned aerial systems camera market gains a steadier commercial base for mid-resolution and specialized agricultural imaging systems

Emergence of SWaP-Optimized Thermal Imaging Cores for Public Safety UAS

Thermal imaging is becoming easier to deploy on smaller airframes, which is lifting adoption in the unmanned aerial systems camera market. Teledyne FLIR OEM and Gremsy introduced the NDAA-compliant ORUS-L and Lynx payload lines in October 2025 through the Thermal by FLIR collaboration program, using the ITAR-free Boson+ LWIR module for public safety, defense, and professional inspection use. Teledyne FLIR OEM also launched the Lepton XDS in February 2026 as a compact thermal-and-visible camera module for OEM integrators working under space and power constraints. These product moves show that thermal performance is no longer limited to large defense platforms, and they are widening the addressable base of police, fire, and inspection operators. The result is a stronger path for thermal payload adoption in compact and mid-tier aircraft across the unmanned aerial systems camera market.

Progress in Satellite-to-UAS Optical Communications Enabling BVLOS Operations

Long-range missions depend on reliable links, so BVLOS connectivity remains an enabling factor for the unmanned aerial systems camera market. In April 2026, Viasat, Thales, TTP, Dimetor, and the European Space Agency completed multi-link BVLOS connectivity trials at Cranfield University under the ESA Iris RPAS program. The trial validated resilient satellite and terrestrial command links under real-world conditions, which matters for inspection and surveillance missions that require persistent image transmission and reliable aircraft control. That progress supports demand for bandwidth-aware imaging payloads that can operate efficiently beyond cellular coverage. Over time, it should broaden the serviceable mission set for the unmanned aerial systems camera market to include utility inspection, civil infrastructure review, and security patrol operations.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising costs associated with cyber-hardening and certification compliance | -0.90% | North America and Europe, with spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Stricter export controls on dual-use electro-optical and infrared (EO/IR) payloads | -1.30% | Global, with highest impact in North America and East Asia trade corridors | Medium term (2-4 years) |

| Ongoing supply chain disruptions in critical imaging sensor components | -1.00% | Global, concentrated in Chinese and Taiwanese supply chain nodes | Short term (≤ 2 years) |

| Increasing legal challenges related to aerial biometric data collection | -0.70% | North America and the European Union | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Costs Associated with Cyber-Hardening and Certification Compliance

Certification costs are becoming a real filter in the unmanned aerial systems camera market. AUVSI’s Green UAS framework, now used as a pathway toward DoD Blue UAS Cleared status, requires review of corporate cyber hygiene, product and device security, remote operations and connectivity, and supply chain risk management.[3]Association for Uncrewed Vehicle Systems International, “Green UAS Frameworks,” AUVSI, auvsi.org Those requirements increase documentation, testing, and audit work for both aircraft makers and payload suppliers in the unmanned aerial systems camera market. They also incur recurring costs when manufacturers update payload variants or switch suppliers within a certified stack. The burden is heaviest on smaller specialists because they must absorb engineering and compliance costs before they can fully meet government-linked demand.

Stricter Export Controls on Dual-Use Electro-Optical and Infrared Payloads

Export restrictions slow sales cycles and raise design pressure in the unmanned aerial systems camera market. Buyers in allied markets still want access to thermal and EO payloads, but licensing reviews and end-user checks can complicate delivery timelines when product configurations are not export-friendly. ITAR-free product status has become a competitive advantage for thermal module suppliers. Teledyne FLIR OEM’s collaboration with Gremsy on ORUS-L and Lynx used the ITAR-free Boson+ LWIR module, which helps those payloads fit broader international integration needs. The same pattern appeared in Teledyne FLIR OEM’s February 2026 launch of the Lepton XDS, which was positioned as a compact ITAR-free module for OEM adoption across space- and power-constrained platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Camera Type: Thermal Imaging Payloads Closing the Resolution Gap on HD Dominance

HD cameras accounted for 53.67% of the market in 2025, supported by their widespread use in cinematography, mapping, and construction inspection. Their lead remains strong because commercial drone fleets are already built around visible-light imaging, and many users can process this data effectively without needing advanced onboard computing. DJI’s Mini 5 Pro, launched in September 2025, showed how premium imaging features are moving into lighter, more accessible drone classes, helping extend the reach of HD camera systems. The other category, which includes multispectral, hyperspectral, and LiDAR-linked payloads, continues to serve smaller but higher-value use cases such as precision agriculture and renewable energy inspection.

Thermal cameras are projected to grow at a CAGR of 18.65% through 2031, making them the fastest-growing camera type segment. This growth is being supported by smaller, lighter, and more compliant LWIR modules that can now be used on compact commercial platforms. Teledyne FLIR’s Boson SX8, introduced in June 2026, brought higher thermal resolution into a package designed for size- and power-constrained UAS, making advanced thermal capability more accessible at production scale. The Thermal by FLIR collaboration with Gremsy also showed how sensor providers and payload integrators are working together to speed up product launches and reduce certification pressure across the value chain. In the US, NDAA compliance is increasingly shaping thermal camera design from the start, and this is also drawing attention from European suppliers seeking similar positioning.

By Application: Photography and Videography Anchors Demand as Thermal Imaging Leads Growth

Photography and videography led the application mix in 2025 with a 34.40% share. This segment continues to benefit from strong demand across commercial content creation, real estate, live production, and social media work. DJI’s Mini 5 Pro helped reinforce this trend by bringing a 1-inch sensor to the sub-250g drone class, narrowing the gap between consumer and professional imaging performance. Surveillance remains an important use case, although legal scrutiny is becoming more visible in some markets. In July 2025, the Oregon Court of Appeals ruled that enhanced aerial surveillance required separate evidentiary support when used as the basis for a warrant, underscoring the need for tighter oversight of law enforcement and commercial drone imaging programs.

Thermal imaging is expected to record the fastest application growth, with a CAGR of 19.10% through 2031. Demand is rising across infrastructure inspection, drone-as-first-responder programs, and military ISR missions that rely on similar sensor and processing capabilities. Higher-resolution thermal payloads are now entering volume production, and that is also lifting demand for stronger visible-light imaging systems in connected use cases. Sony’s ILX-LR1, showcased at Amsterdam Drone Week 2026, reflected this move toward higher-resolution payload standards in photogrammetry and precision mapping. The others category still has a role in environmental monitoring, search and rescue, and corridor inspection, where operators often need a mix of thermal and visible-light imaging in the same mission.

By Resolution: Mid-Resolution Standards Anchor the Installed Base as Ultra-High-Resolution Pulls Growth Upward

The 12 to less than 20 MP segment accounted for 31.85% of the market in 2025, making it the largest resolution bracket. This reflects the maturity of commercial drone workflows in inspection, broadcasting, and agricultural surveying, where mid-resolution imaging often meets operating needs without creating heavy data or storage demands. India’s Kisan Drone Yojana 2025 is also supporting this band by encouraging the adoption of camera-equipped agricultural drones that meet standard crop-monitoring needs. The 20 to 32 MP segment serves as a step-up option for users who want better image quality without moving fully into the cost and complexity of ultra-high-resolution systems. The less-than-12 MP category still has a place in low-cost agricultural operations and expendable UAS deployments where keeping unit cost low remains important.

The more than 32 MP segment is forecast to grow at a 19.05% CAGR through 2031, the highest among segments. Growth is being driven by rising requirements in photogrammetry, precision mapping, border monitoring, and infrastructure documentation, where higher image detail matters at operational flying height. Sony’s ILX-LR1, with its 61-megapixel full-frame design and compatibility across multiple autopilot systems, shows that ultra-high-resolution aerial imaging is moving into broader commercial use. Partnerships between sensor makers, gimbal companies, and autopilot providers are also helping this segment by making certified imaging stacks easier to deploy. Once operators invest in these integrated systems, switching costs rise, which supports continued demand in the higher-resolution tier.

By End-user: Commercial Segment Leads but Homeland Security Commands the Highest Growth Rate

Commercial end-users accounted for 55.45% of the market in 2025, reflecting broad demand across construction, agriculture, media production, and utility inspection. This remains the largest user group because it encompasses a wide range of routine, repeatable drone applications across several industries. At the same time, the commercial segment is becoming more divided. Larger enterprise operators are moving toward multi-sensor systems with AI-supported analysis and automated reporting, while smaller users remain more price-sensitive. Military demand remains distinct because procurement cycles are longer, contract values are higher, and compliance requirements limit the supplier pool.

Homeland security is projected to grow at the fastest pace, with a 17.83% CAGR through 2031. Agencies are expanding drone-as-first-responder programs, border surveillance, and infrastructure protection efforts that depend on secure ISR-grade imaging payloads. In June 2026, the Conroe Police Department launched a Skydio X10 DFR program funded through asset forfeiture, showing how local agencies can move ahead without waiting for long capital approval cycles. Autel Robotics is also gaining traction in this segment, partly because regulatory pressure has reduced the room for non-compliant platforms in government tenders. The Green UAS certification pathway has added another filter by favoring vendors that already have the documentation, compliance systems, and government contracting experience needed to qualify.

Geography Analysis

North America accounted for 32.88% of the unmanned aerial systems camera market share in 2025, which made it the leading regional contributor by revenue. The region benefits from a large defense and homeland security demand base, a mature commercial operator ecosystem, and a stronger certification culture than many other markets. Those factors support steady demand for compliant thermal, EO, and multi-sensor payloads rather than simple low-cost camera units. Public safety and inspection use cases are also more established in North America, which improves repeat purchasing and upgrade cycles in the unmanned aerial systems camera market. This keeps the region important not only for volume, but also for higher-value payload configurations.

Asia-Pacific is projected to grow at a 17.65% CAGR through 2031, making it the fastest-growing regional segment in the unmanned aerial systems camera market. The region combines large manufacturing capacity, expanding agricultural deployment, and rising interest in long-endurance surveillance and inspection applications. India’s subsidy-backed Kisan Drone Yojana 2025 and Madhya Pradesh’s investment support policy provide the region with a clear commercial basis for camera-equipped agricultural drones. Gremsy and Aerosense also completed integration of the LYNX EO/IR payload onto the Aerobo Wing VTOL in June 2026, showing that the region is moving beyond small commercial systems toward longer-endurance surveillance and inspection roles.

Europe represents the second-largest geographic cluster in the unmanned aerial systems camera market, supported by defense demand and a regulatory environment that is increasingly supportive of BVLOS operations. The ESA Iris RPAS flight trials completed in April 2026 provided evidence that resilient satellite and terrestrial command links can support real operating conditions for long-range missions. That matters for European inspection and civil infrastructure work, where compliant long-range operations can unlock demand for purpose-built imaging payloads in the unmanned aerial systems camera market. South America, the Middle East, and Africa remain smaller in current scale, but they continue to present demand for agricultural imaging, energy inspection, public safety, and border surveillance payloads.

Competitive Landscape

The unmanned aerial systems camera market exhibits a mixed competitive structure, with greater concentration at the platform layer and much broader fragmentation among payload and sensor specialists. DJI’s scale in the commercial drone ecosystem still gives it significant influence over payload expectations, product form factors, and imaging standards in the unmanned aerial systems camera market. At the same time, specialized thermal and ISR suppliers compete on compliance status, export readiness, and sensor integration rather than pure aircraft volume alone. Market power is not distributed evenly across the value chain. Companies that control thermal sensor IP, edge processing capability, or government-ready certification pathways can hold strong positions even without matching DJI's platform scale.

Teledyne FLIR OEM has strengthened its position through repeatable moves that connect sensor IP with system-level adoption in the unmanned aerial systems camera market. The Thermal by FLIR collaboration with Gremsy created the ORUS-L and Lynx payloads, which package ITAR-free thermal capability into NDAA-compliant solutions for defense, public safety, and inspection users. Teledyne FLIR OEM also launched Prism C-UAS in April 2026, extending its role from hardware supply into AI-enabled counter-drone software built around thermal camera inputs. These moves show that competitive advantage in the unmanned aerial systems camera market is increasingly tied to ecosystem depth, not only to sensor performance.

DJI remains important because it continues to raise imaging expectations in the commercial tier of the unmanned aerial systems camera market. The Mini 5 Pro in September 2025 and the Avata 360 in March 2026 both showed that advanced imaging features are moving into lighter and more immersive product classes. Gremsy’s June 2026 integration with Aerosense added another example, showing how payload makers can build position through long-endurance surveillance partnerships rather than through standalone sensor sales. Taken together, the competitive pattern in the unmanned aerial systems camera market favors companies that can link camera hardware, software intelligence, compliance, and mission integration into a single offering.

Unmanned Aerial Systems Camera Industry Leaders

Teledyne FLIR LLC

SZ DJI Technology Co., Ltd.

Sony Corporation

Canon Inc.

Panasonic Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Gremsy and Aerosense completed the strategic integration of the LYNX ultra-compact payload with the Aerobo Wing AS-VT02K VTOL fixed-wing drone. The combined platform enhances long-endurance surveillance capabilities by pairing a lightweight dual-spectrum sensor with a flight range of more than 70 km, endurance exceeding 60 minutes, and a 1.6 kg payload capacity for infrastructure inspection, environmental monitoring, coastal surveillance, and disaster-response operations.

- February 2026: Teledyne FLIR OEM unveiled the Lepton XDS, a compact dual thermal-visible camera module designed for embedded, mobile, industrial, and unmanned platform applications. The ITAR-free module integrates a 160 × 120 radiometric thermal sensor, a five-megapixel visible camera, MSX imaging, and Prism ISP processing. It supports faster OEM integration across unmanned systems, robotics, fire detection, EV battery monitoring, smart infrastructure, and industrial safety applications.

- July 2025: Auterion received a USD 50 million Pentagon contract to deliver 33,000 AI-driven drone-strike kits to Ukraine, enhancing its defense capabilities. The company's strike kits, featuring Skynode computers with integrated software, cameras, and radio modules, transform manual drones into autonomous systems capable of tracking targets within one kilometer while resisting interference.

Global Unmanned Aerial Systems Camera Market Report Scope

The unmanned aerial systems camera market refers to imaging payloads and camera systems integrated with unmanned aerial systems to capture, process, stabilize, transmit, and store aerial visual data during flight operations. These systems combine optical sensors, lenses, image processors, stabilization mechanisms, mounting interfaces, and data links to support real-time viewing, recording, inspection, mapping, monitoring, and mission intelligence functions.

The unmanned aerial systems camera market is segmented by type, application, resolution, end-user, and geography. Based on the type, the drone camera market is segmented into SD cameras and HD cameras, by application into photography & videography, thermal imaging, and surveillance. By resolution, the market is segmented into less than 12 MP, 12 to less than 20 MP, 20 to less than 32 MP, and more than 32 MP. By end user, the market is segmented into commercial, military, and homeland security. The report also covers the market sizes and forecasts for the unmanned aerial systems camera market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| HD Cameras |

| Thermal Cameras |

| Others |

| Photography and Videography |

| Thermal Imaging |

| Surveillance |

| Mapping and Surveying |

| Inspection and Maintenance |

| Other Applications |

| Less than 12 MP |

| 12 to Less than 20 MP |

| 20 to Less than 32 MP |

| More than 32 MP |

| Commercial |

| Military |

| Homeland Security |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Camera Type | HD Cameras | ||

| Thermal Cameras | |||

| Others | |||

| By Application | Photography and Videography | ||

| Thermal Imaging | |||

| Surveillance | |||

| Mapping and Surveying | |||

| Inspection and Maintenance | |||

| Other Applications | |||

| By Resolution | Less than 12 MP | ||

| 12 to Less than 20 MP | |||

| 20 to Less than 32 MP | |||

| More than 32 MP | |||

| By End-user | Commercial | ||

| Military | |||

| Homeland Security | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 size of the unmanned aerial systems camera market?

The unmanned aerial systems camera market is estimated at USD 3.62 billion in 2026 and is forecast to reach USD 7.80 billion by 2031 at a 16.59% CAGR.

Which camera type leads revenue in this space?

HD cameras led with 53.67% of revenue in 2025 because they still serve the broadest installed base across cinematography, mapping, and inspection.

Which application is growing the fastest through 2031?

Thermal imaging is the fastest-growing application, with a projected CAGR of 19.10% through 2031, driven by inspection, firefighting, and ISR-related demand.

Why is thermal imaging gaining so much attention in drone payloads?

Thermal payloads are becoming smaller, more compliant, and easier to integrate, which is widening their use in public safety, defense, and industrial inspection.

Which region is expanding the fastest for camera-equipped UAS?

Asia-Pacific is growing the fastest, with a 17.65% CAGR through 2031, supported by agricultural subsidy programs, manufacturing depth, and surveillance use cases.

What is shaping competition among leading suppliers?

Competition is increasingly defined by compliance readiness, AI-enabled imaging, thermal sensor integration, and the ability to deliver mission-ready payload systems rather than stand-alone hardware.

Page last updated on: