United States Turning Machine and Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

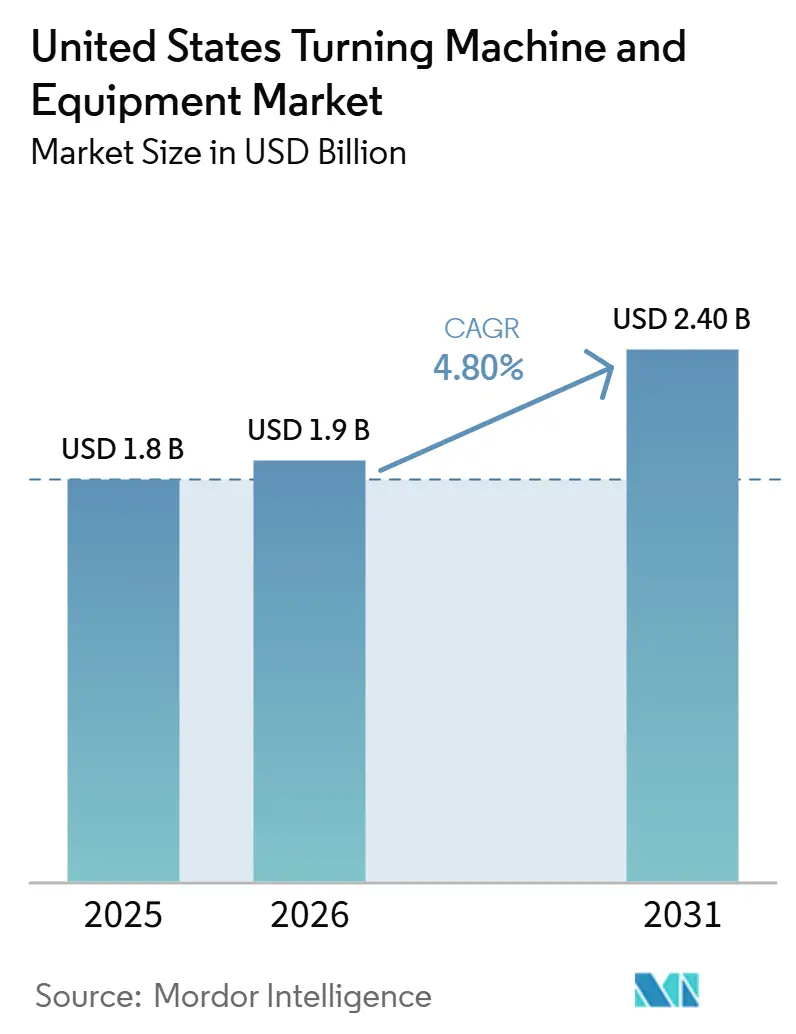

| Base Year Market Size (2025) | USD 1.8 Billion |

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.40 Billion |

| Growth Rate (2026 - 2031) | 4.80% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Turning Machine and Equipment Market Analysis by Mordor Intelligence

The United States Turning Machine and Equipment Market size was valued at USD 1.8 billion in 2025 and is estimated to grow from USD 1.9 billion in 2026 to reach USD 2.40 billion by 2031, at an CAGR of 4.80% during the forecast period (2026-2031).

Federal industrial policy continues to support the United States turning machine and equipment market, as manufacturing programs tied to infrastructure, semiconductors, and energy have expanded the base of facilities that need precision-machining capacity. Demand in the United States turning machine and equipment market is also supported by automotive, aerospace, medical device, electronics, and energy production, all of which depend on repeatable tolerance control that conventional machining cannot deliver with the same consistency. The competitive field remains fragmented, which supports technology diffusion and service competition, while also keeping pressure on suppliers to shorten development cycles and bundle automation with the machine sale. Capital costs, tariff exposure, and labor constraints still limit buying speed for some shops. Yet, the broader mix of domestic manufacturing projects keeps the United States turning machine and equipment market on a steady expansion path.

Key Report Takeaways

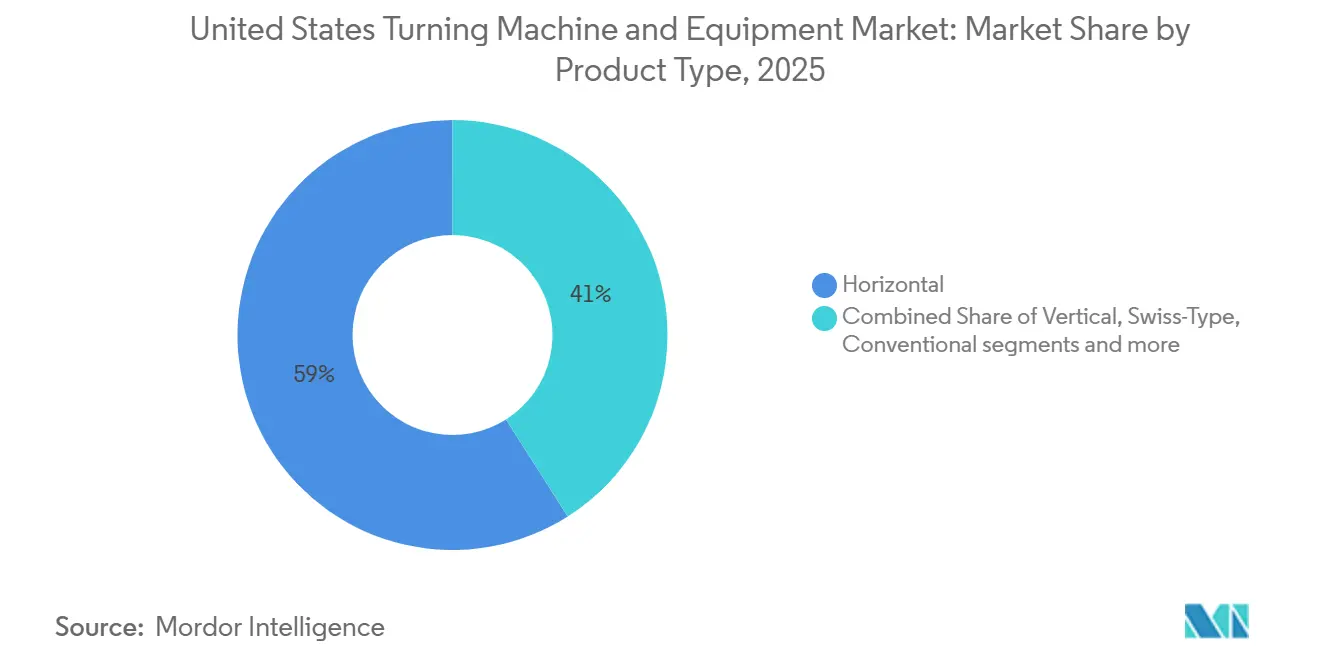

- By product type, the horizontal segment held 59% of the United States turning machine and equipment market share in 2025, while the multi-tasking segment is forecast to expand at an 6.1% CAGR through 2031.

- By automation type, fully automatic CNC accounted for 84% of the United States turning machine and equipment market size in 2025 and is advancing at a 5.9% CAGR through 2031.

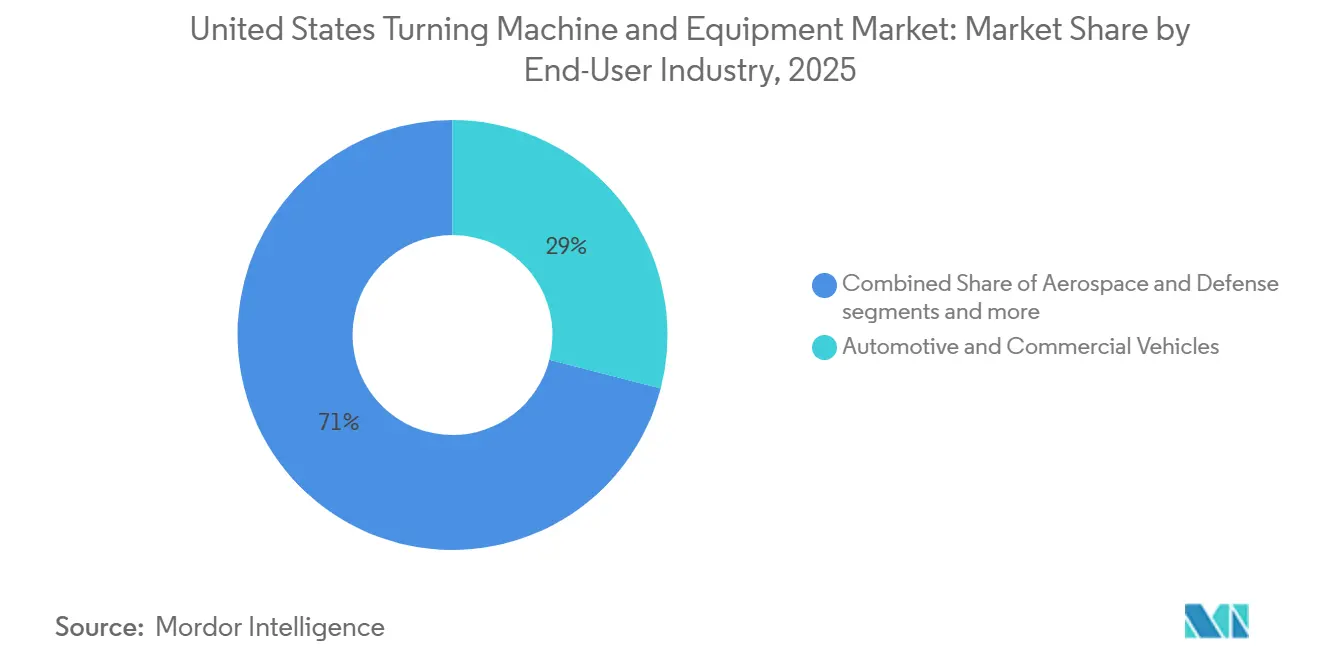

- By end-user industry, automotive and commercial vehicles accounted for 29% of the United States turning machine and equipment market size in 2025, while aerospace and defense are projected to grow at an 6.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Turning Machine and Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reshoring and Domestic Manufacturing Investments Increasing Demand for Machine Tools | +1.2% | National, with strong concentration in the Midwest, Southeast, and Texas | Short term (≤ 2 years) |

| Expansion of Aerospace and Defense Manufacturing Requiring High-Precision Machining | +0.9% | Pacific Coast, New England, and Southeastern aerospace corridors | Medium term (2-4 years) |

| Expansion of Domestic Advanced Manufacturing Capacity | +0.7% | National, especially Arizona, Texas, Ohio, and New York | Medium term (2-4 years) |

| Growing Adoption of Automation and Lights-Out Manufacturing | +0.5% | National, with early concentration in the Midwest and high-mix shop clusters | Short term (≤ 2 years) |

| Growing Adoption of Swiss-Type and Precision Turning Technologies | +0.4% | Northeast, Midwest, and Southeast medical device and electronics clusters | Medium term (2-4 years) |

| Rising Demand for High-Precision and Tight-Tolerance Machining | +0.3% | National, including defense-adjacent manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reshoring and Domestic Manufacturing Investments Increasing Demand for Machine Tools

Federal policy remains the main driver of equipment demand in the United States, shaping the machine and equipment market. The Department of Labor stated in 2024 that manufacturing legislation since 2021 has supported nearly USD 2 trillion in investments, which is expanding both production sites and workforce needs.[1]U.S. Department of Labor, “Benefits of Collaboration Between the Public Workforce System, the Manufacturing Extension Partnership (MEP) Program and the Manufacturing USA Network of Institutes,” Employment and Training Administration, dol.gov These commitments are creating new facilities and upgrades across automotive, semiconductor, and industrial production, and each facility requires precision-machining capability, either in-house or through specialized machining suppliers. The National Association of Manufacturers (NAM) in the United States found that more than 54.3% of manufacturers considered industrial machinery their most critical input, suggesting active procurement rather than delayed purchasing. Tax treatment for equipment purchases has also improved buying conditions for smaller shops, and NAM cited a 2026 example of a machine shop that purchased more than USD 1.1 million of equipment after expensing rules were restored.[2]National Association of Manufacturers, “NAM Q1 2026 Manufacturers' Outlook Survey,” National Association of Manufacturers, nam.org Federal procurement rules tied to domestic production are also reinforcing equipment demand where public funding and strategic manufacturing programs are involved.

Expansion of Aerospace and Defense Manufacturing Requiring High-Precision Machining

Aerospace and defense activity is adding a durable layer of demand to the United States turning machine and equipment market. The Department of Defense requested USD 961.6 billion for FY2026, including USD 5.7 billion for the submarine industrial base and USD 2.6 billion in IBAS and Defense Production Act Title III funding for casting, forging, and machining capacity.[3]U.S. Department of Defense Office of the Comptroller, “FY2026 Budget Request Overview Book,” U.S. Department of Defense, comptroller.defense.gov Those allocations support the purchase of machines at prime contractors, Tier 1 suppliers, and specialist shops that work with titanium, nickel alloys, and high-strength steel. The production chain for these parts depends on tight repeatability, fewer setups, and reliable programming, which favors CNC turning centers and multi-tasking platforms over simpler equipment. Next-generation defense aircraft programs are expected to create long-term demand for high-precision machining capacity. Qualification requirements such as AS9100 and ITAR further narrow the supplier pool, which increases the value of domestic shops that already meet defense and aerospace standards.

Expansion of Domestic Advanced Manufacturing Capacity

Semiconductor and battery investments are widening the application base for the United States turning machine and equipment market. The Department of Commerce reported in 2026 that CHIPS for America had catalyzed more than USD 555 billion in announced United States semiconductor investments, which supports broad demand for precision components used in fluid handling, transport, housings, and process tools. The Economic Development Administration also directed USD 504 million to 12 regional technology and innovation hubs in 2024, helping to form dense clusters of advanced manufacturing activity. New fabrication and battery facilities require large volumes of fixtures, custom housings, and equipment parts during installation and ramp-up, and much of that work fits the dimensional range of modern turning centers. That means facility construction creates additional demand for tooling, fixtures, and machining capacity, in addition to the headline spend on the plant itself. As more of this production footprint comes onstream, the United States turning machine and equipment market benefits from both initial tooling demand and recurring replacement and maintenance work.

Growing Adoption of Automation and Lights-Out Manufacturing

Automation is becoming a standard manufacturing approach across many parts of the United States turning machine and equipment market. The National Institute of Standards and Technology documented in 2025 that manufacturers combining robots with CNC turning equipment increased production by 16 or more hours per day without corresponding increases in staffing. The National Institute of Standards and Technology also cited an Ohio manufacturer that reduced downtime by 70% and improved efficiency by 40%, then purchased a second automated cell within 8 months because the return profile was strong. At the same time, average weekly hours in machinery manufacturing rose from 39.5 in January 2024 to 42.0 in January 2026, indicating that capacity pressure remains high even as some firms remain cautious about capex. The Bureau of Labor Statistics also projected 13% employment growth for industrial machinery mechanics from 2024 to 2034, which shows that automated machining cells still depend on skilled support roles rather than replacing them outright. This combination of labor scarcity, longer utilization windows, and faster payback is making automated turning cells a practical response for both large plants and mid-sized job shops.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Investment Requirements for Advanced Turning Machine and Equipment | -0.8% | National, with stronger pressure on small and mid-sized job shops in the Midwest and Southeast | Short term (≤ 2 years) |

| Persistent Shortage of Skilled CNC Operators and Programmers | -0.6% | National, especially the industrial Midwest, Southeast, and defense-adjacent communities | Medium term (2-4 years) |

| Cyclical Nature of Manufacturing Capital Expenditure | -0.4% | National, with higher sensitivity in automotive-linked Midwest regions | Long term (≥ 4 years) |

| Intense Competitive Pressure from Global Machine Tool Suppliers | -0.3% | National, especially in entry-level and mid-tier horizontal turning machine and equipment | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment Requirements for Advanced Turning Machine and Equipment

Machine prices remain a significant barrier in the United States turning machine and equipment market, particularly for smaller manufacturers. Entry-level CNC turning centers begin near USD 80,000, multi-tasking systems can exceed USD 500,000, and large vertical turning lathes for aerospace or energy work can surpass USD 1 million per installation, which stretches balance sheets and slows approvals. The NAM Q1 2026 survey found that only 41.0% of manufacturers expected to increase capital spending in the next 12 months, while 16.2% expected lower spending. Tariffs on steel, aluminum derivatives, and machine components also raise acquisition cost, and NAM warned in 2025 that Section 232 actions could slow plant and equipment investment. Defense-related compliance requirements can increase qualification time for machine suppliers serving aerospace and defense manufacturers.

Persistent Shortage of Skilled CNC Operators and Programmers

Labor availability continues to limit how quickly the United States turning machine and equipment market can convert demand into installed and productive capacity. The Bureau of Labor Statistics reported 299,500 machinists employed in 2024 and projected 34,200 annual openings through 2034, with most openings tied to retirements and occupational transfers rather than net workforce expansion. The Department of Labor also identified CNC machinists as a high-risk shortage occupation in 2024 and linked the gap to weak career perceptions and limited training pathways. In 2026, the Department of Labor highlighted a projected shortage of more than 3,000 skilled workers in defense and advanced manufacturing in Maine alone, including CNC roles. The NAM Q1 2026 survey also found that 44.68% of manufacturers cited workforce attraction and retention as a main challenge, and firms expected 4.13% of jobs to remain unfilled. The constraint is most severe in programming and process planning, where modern multi-tasking equipment needs a deeper skill base than standard machine operation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Horizontal Platforms Anchor Volume, Multi-Tasking Systems Command Growth Premium

Horizontal segment accounted for 59% of demand in 2025. It led the installed base across the United States turning machine and equipment market because it is widely used in automotive and industrial applications. The multi-tasking segment is projected to grow at a 6.1% CAGR through 2031, which makes it the fastest-rising product category in the United States turning machine and equipment market. This product mix reflects a clear split between volume-oriented production on standard horizontal platforms and higher-value demand for machines that combine turning, milling, and drilling in one setup. Swiss-type machines are also gaining ground in medical devices and electronics because long, slender parts and very tight tolerances are harder to control on standard horizontal lathes. The vertical segment continues to serve large-diameter workpieces in heavy machinery, power generation, and energy applications, where workpiece orientation reduces setup complexity. The conventional segment remains in use for repair work and training, but its role in new equipment procurement continues to narrow as CNC capability becomes the default requirement.

The product category mix shows how advanced features are becoming increasingly available across mid-range turning machine and equipment platforms. Suppliers are now designing even standard horizontal and vertical CNC models with greater automation compatibility, live tooling, and broader axis functionality, which is reducing the gap between mainstream and premium systems. That shift is important because many buyers now want one machine that can support current production as well as later robotic loading or unattended operation. Mazak highlighted this direction in 2025 when it introduced the QRX-50MSY multi-spindle turning center for high-volume production and placed strong emphasis on automatic operation and lower operator intervention. Mazak also presented Ez-series turning centers with bar feeder and Ez LOADER connectivity in Kentucky during DISCOVER 2025, which shows that automation-ready design is spreading into more accessible product tiers. As that feature set becomes common, share movement within the United States turning machine and equipment market is likely to favor suppliers that can combine flexibility, service support, and a practical operating cost profile.

By Automation Type: CNC Dominance Deepens Across Shop Sizes

Fully automatic CNC held 84% of 2025 demand, giving it the largest position in the United States turning machine and equipment market share, and it is also projected to expand at a 5.9% CAGR through 2031. The same segment, therefore, drives both current scale and future growth, indicating that automation penetration is still deepening rather than leveling off. Semi-automatic turning machines and equipment remain relevant for some shops that are still moving away from manual production, especially when batch sizes are small and investment budgets are tight. Manual turning machines and equipment are now concentrated in prototype work, vocational programs, and legacy repair environments where a low-cost machine still serves a purpose. Even in those settings, procurement direction continues to favor CNC because programming, repeatability, and labor efficiency matter more than upfront purchase price alone.

The economics of unattended production explain why the United States turning machine and equipment market keeps shifting toward fully automatic systems. NIST documented cases in 2025 in which robotic tending enabled CNC turning cells to extend machine utilization without adding headcount on the same scale. One Ohio manufacturer reduced downtime by 70% and improved efficiency by 40%, then moved quickly to install a second automated cell after an 8-month payback period. Weekly hours in machinery manufacturing also rose to 42.0 by January 2026, up from 39.5 in January 2024, indicating that plants are still pushing available capacity to the limit. That operating pressure is pushing mid-tier shops toward CNC adoption for the same reason larger manufacturers moved earlier: the need to run longer, hold tolerances more reliably, and reduce dependence on scarce labor. As a result, the United States turning machine and equipment market is seeing automation become the standard production format rather than a premium upgrade.

By End-User Industry: Automotive Anchors Demand, Aerospace Leads Growth

Automotive and commercial vehicles accounted for 29% of the market share. They remained the largest end-use base in the United States turning machine and equipment market, as high-volume powertrain, transmission, and chassis parts still require extensive precision turning. Aerospace and defense is projected to grow at a 6.3% CAGR through 2031, making it the fastest-growing end-user vertical in the United States turning machine and equipment market. Medical devices and surgical instruments constitute another precision-sensitive segment in which Swiss-type turning machines and equipment are widely used, and supplier quality systems are critical. Oil, gas, and energy demand remains linked to drilling activity, LNG infrastructure, and refinery maintenance, which creates irregular but high-value orders for valve bodies, flanges, and pressure-related components. Electrical, electronic, and semiconductor equipment is also becoming a stronger structural opportunity as facility construction drives demand for wafer-handling parts, precision housings, and fluid-delivery components.

Qualification standards shape competition within these end-user groups more strongly than in many other equipment categories. Aerospace and defense suppliers need AS9100 discipline and often operate under ITAR-related requirements, which limits the pool of machine shops that can win and retain this work. The FY2026 defense budget supports this segment with USD 2.6 billion in IBAS and Defense Production Act Title III funding, which includes machining-related capacity across the defense industrial base. The 2026 announcement of the F-47 fighter program also adds to the long-cycle demand outlook for qualified aerospace machining suppliers. In medical devices and electronics, the advantage shifts toward precision control, smaller part geometry, and documentation discipline rather than simple machine throughput. Demand trends increasingly favor shops and suppliers that combine advanced process capability, compliance readiness, and strong service support.

Geography Analysis

The Midwest remains the largest installed base for the United States turning machine and equipment market because Michigan, Ohio, Indiana, and Illinois continue to host dense machining and vehicle supply chains. Ohio alone had 59,550 production workers in machinery manufacturing in 2025, underscoring the region’s depth of industrial labor and its central role in precision component output. This concentration supports steady demand for horizontal turning machine and equipment used in shafts, bushings, housings, and similar high-volume parts. Illinois is also adding supplier-side capacity because DMG MORI is investing USD 40.5 million in 2026 in a new 90,000 sq ft advanced manufacturing and research facility in the Chicago area. That project adds local engineering and service capability to the United States turning machine and equipment market, and gives Midwest buyers closer access to product development support. The NAM Q1 2026 survey also found that 75.3% of manufacturers reported a positive business outlook, which supports the view that capital spending sentiment has improved across core factory states.

The Southern corridor is also taking on a larger role in the United States turning machine and equipment market, as Alabama, Tennessee, South Carolina, and Texas continue to attract automotive, energy, and defense-linked production. Alabama and Tennessee benefit from major vehicle assembly campuses that have expanded local sourcing and increased the need for repeatable machining capacity on production parts. Texas has a broader mix that includes energy hardware, valve components, pressure systems, and aerospace structures, which supports both horizontal and vertical turning demand. Defense spending also supports Southern demand because the F-47 program and other aerospace work help sustain long production cycles for precision-machined components.

Although the Pacific Coast and Northeast account for a smaller share of volume, they remain strategically important due to strong aerospace, defense, and medical device clusters. Washington supports advanced turning demand through commercial aviation suppliers that machine titanium and high-temperature alloys. New England benefits from dense networks of defense subcontractors and medical device manufacturers that rely heavily on Swiss-type and high-precision CNC turning platforms. Western coverage is also improving because Mazak opened a new Phoenix Technical Center in January 2026, giving buyers in aerospace, electronics, and precision machining faster access to application support, demonstrations, training, and service.

Competitive Landscape

The United States turning machine and equipment market remains fragmented, with domestic and international suppliers competing across horizontal, vertical, swiss-type, and multi-tasking platforms. No single supplier controls the field, keeping the United States turning machine and equipment market open to a broad mix of machine builders, distributors, and specialized product lines. Competition is shaped by machine capability, control quality, automation readiness, price accessibility, financing, and the density of local service support. Domestic suppliers often compete on lead times, pricing, and aftermarket responsiveness, while Japanese, German, Swiss, and South Korean builders keep strong positions in higher-precision applications. This structure benefits end users by expanding the choice set, but it also puts pressure on suppliers to demonstrate application performance rather than rely solely on brand position.

A clear change in the United States turning machine and equipment market is the shift from selling standalone machines to selling operating solutions. DMG MORI is strengthening this approach in 2026 through its USD 40.5 million Illinois investment, which adds North American research and manufacturing capacity and supports buyers that need local development support and closer alignment with domestic sourcing expectations. Mazak is following a similar path through domestic production, technical center expansion, and service infrastructure that helps customers shorten ramp-up time and reduce downtime. Mazak produced its 40,000th machine at its Kentucky iSmart Factory in 2025 and, in January 2026, opened its Phoenix Technical Center, which expanded western coverage for application engineering, programming support, and service response. These moves show that competitive strength in the United States turning machine and equipment market now depends as much on local execution as on machine specifications.

The specialized swiss-type category adds another layer of competition within the United States turning machine and equipment market. Suppliers such as Citizen, Star Micronics, Tsugami, and Tornos serve end uses where part geometry, tolerance discipline, and compact component design matter more than raw work envelope size. Star Micronics received JPY 25 billion (USD 160.1 million) in strategic funding in May 2026 to support reform in its machine tools and special products businesses, which could influence cost structure and product focus in this niche. Citizen Machinery also reported more than GBP 4.5 million (USD 6.1 million) in lathe orders at MACH 2026, indicating that demand for swiss-type systems remains firm in precision manufacturing applications. Across the wider field, suppliers that can pair reliable machine performance with automation integration, training, and local service are likely to defend pricing better than those that compete solely on hardware.

United States Turning Machine and Equipment Industry Leaders

Haas Automation Inc.

Mazak Corporation

DMG MORI

Okuma Corporation

DN Solutions

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Star Micronics Co. Ltd received JPY 25 billion (USD 160.1 million), in strategic funding from Taiyo Pacific Partners L.P. to support fundamental reform across its machine tools and special products businesses. The company's investor documentation notes an intention to concentrate on key markets where cost competitiveness is strongest. This strategic pivot could materially alter product focus and pricing strategy in the United States Swiss-type turning segment.

- February 2026: DMG MORI Federal Services committed USD 40.5 million to establish a new 90,000 sq ft advanced manufacturing and R&D facility in Chicago, Illinois, creating 74 full-time jobs. The facility serves as the center of North American R&D. It drives strategic initiatives tied to the company's global MX machining transformation, with implications for product localization and procurement eligibility in defense-related contracts.

- January 2026: Mazak opened its new Phoenix Technical Center in Arizona, bringing its North American Technical Center network to 6 facilities and 8 Technology Centers. The Phoenix location provides applications engineering, CNC programming training, machine demonstrations, and service support, extending Mazak's coverage across the Western United States aerospace, electronics, and precision machining customer base.

United States Turning Machine and Equipment Market Report Scope

The United States Turning Machine and Equipment Market is Segmented by Product Type (Horizontal, Vertical, Swiss-Type, Multi-Tasking, and Conventional), by Automation Type (Manual, Semi-Automatic, and Fully Automatic CNC), and by End-User Industry (Automotive & Commercial Vehicles, Aerospace & Defense, Medical Devices & Surgical Instruments, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal |

| Vertical |

| Swiss-Type |

| Multi-Tasking |

| Conventional |

| Manual |

| Semi-Automatic |

| Fully Automatic CNC |

| Automotive & Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices & Surgical Instruments |

| Oil, Gas, & Energy |

| Electrical, Electronics & Semiconductor Equipment |

| General Industrial Machinery |

| Others (Consumer Goods, Defense Ordnance) |

| By Product Type | Horizontal |

| Vertical | |

| Swiss-Type | |

| Multi-Tasking | |

| Conventional | |

| By Automation Type | Manual |

| Semi-Automatic | |

| Fully Automatic CNC | |

| By End-User Industry | Automotive & Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices & Surgical Instruments | |

| Oil, Gas, & Energy | |

| Electrical, Electronics & Semiconductor Equipment | |

| General Industrial Machinery | |

| Others (Consumer Goods, Defense Ordnance) |

Key Questions Answered in the Report

What is the market size of the United States turning machine and equipment market in 2026, and how is it expected to grow by 2031?

The United States turning machine and equipment market is forecast to grow from USD 1.9 billion in 2026 to USD 2.4 billion by 2031 at a 4.8% CAGR, supported by automation upgrades, EV-related machining demand, and replacement of older machine tools.

Which product category leads current demand?

Horizontal segment led with 59% of 2025 demand because it remains deeply embedded in automotive and other high-volume machining applications.

Which product category is growing the fastest?

Multi-tasking segment is projected to grow at a 6.1% CAGR through 2031 as manufacturers seek to combine multiple machining steps in a single setup.

Why is fully automatic CNC machine and equipment taking share from other automation types?

Fully automatic CNC held 84% of 2025 demand and is growing at 5.9% because it improves repeatability, supports unattended production, and reduces exposure to labor shortages.

Which end-user segment offers the strongest growth outlook?

Aerospace and defense have the fastest forecast growth at 6.3% CAGR through 2031, supported by defense funding, qualification-driven supply chains, and long production cycles.

What is the biggest challenge for machine buyers and suppliers?

High machine cost and the shortage of skilled CNC operators and programmers remain the biggest constraints, even though overall factory investment conditions have improved.

Page last updated on: