United States Quantum Computing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

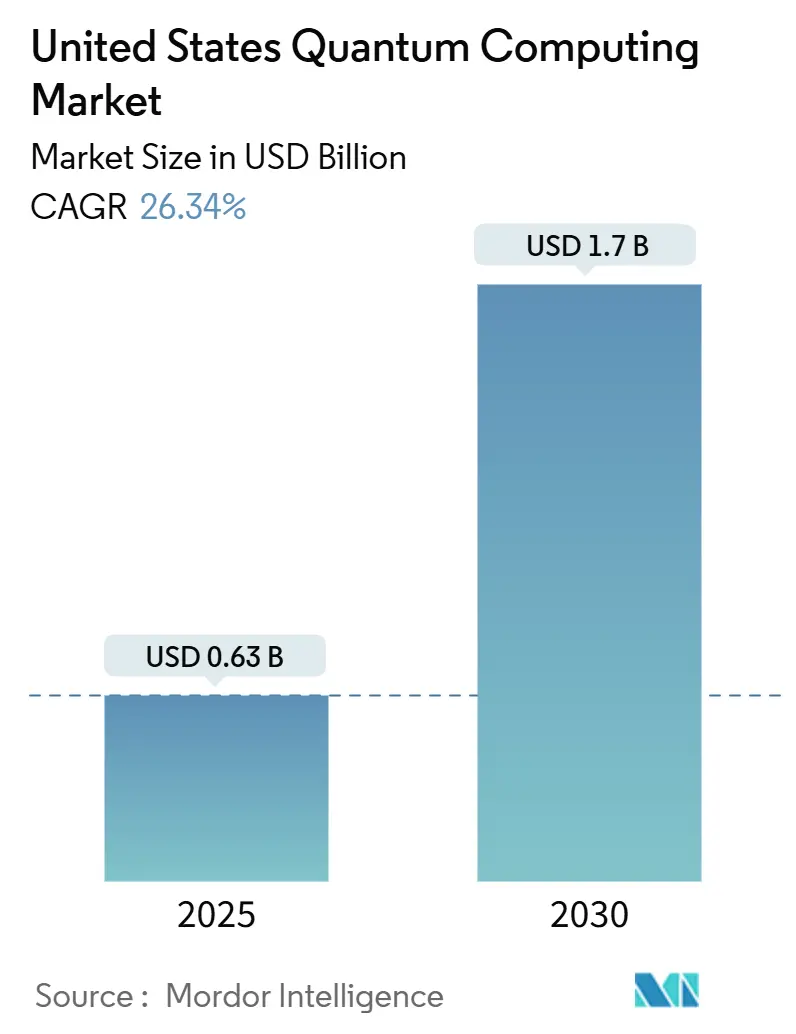

| Market Size (2025) | USD 0.63 Billion |

| Market Size (2030) | USD 1.7 Billion |

| Growth Rate (2025 - 2030) | 26.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Quantum Computing Market Analysis by Mordor Intelligence

The United States quantum computing market size stands at USD 0.63 million in 2025 and is projected to expand at a 26.34% CAGR to touch USD 1.7 billion by 2030, underscoring the sector’s rapid commercialization trajectory. Federal appropriations under the CHIPS and Science Act, NIST’s 2024 release of quantum-resistant encryption standards, and corporate urgency to future-proof cryptographic infrastructure are converging to accelerate adoption. Superconducting platforms maintain a commanding lead thanks to continual qubit-count scaling, yet topological architectures are gaining momentum as error-correction breakthroughs shrink the performance gap. Cloud-based quantum-as-a-service offerings drive accessibility, while hybrid classical-quantum workflows shorten time-to-value for enterprises experimenting with optimization, simulation, and security use cases. Persistent supply-chain bottlenecks around cryogenics and isotopes, coupled with a mid-career talent shortage, temper growth but do not derail the long-run outlook.

Key Report Takeaways

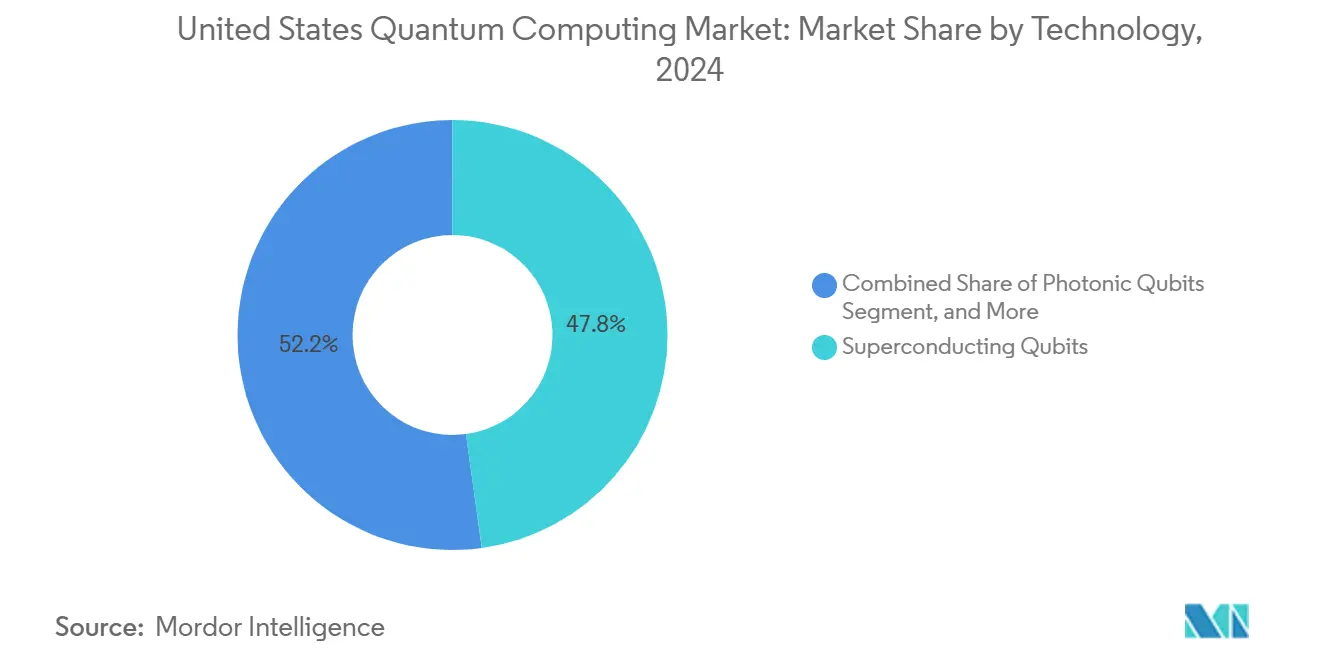

- By technology, superconducting qubits led with a 47.83% United States quantum computing market share in 2024, whereas topological qubits are forecast to advance at a 27.22% CAGR through 2030.

- By deployment model, cloud-delivered quantum-as-a-service captured 59.73% of the United States quantum computing market size in 2024; hybrid classical-quantum solutions are poised to grow at a 27.56% CAGR to 2030.

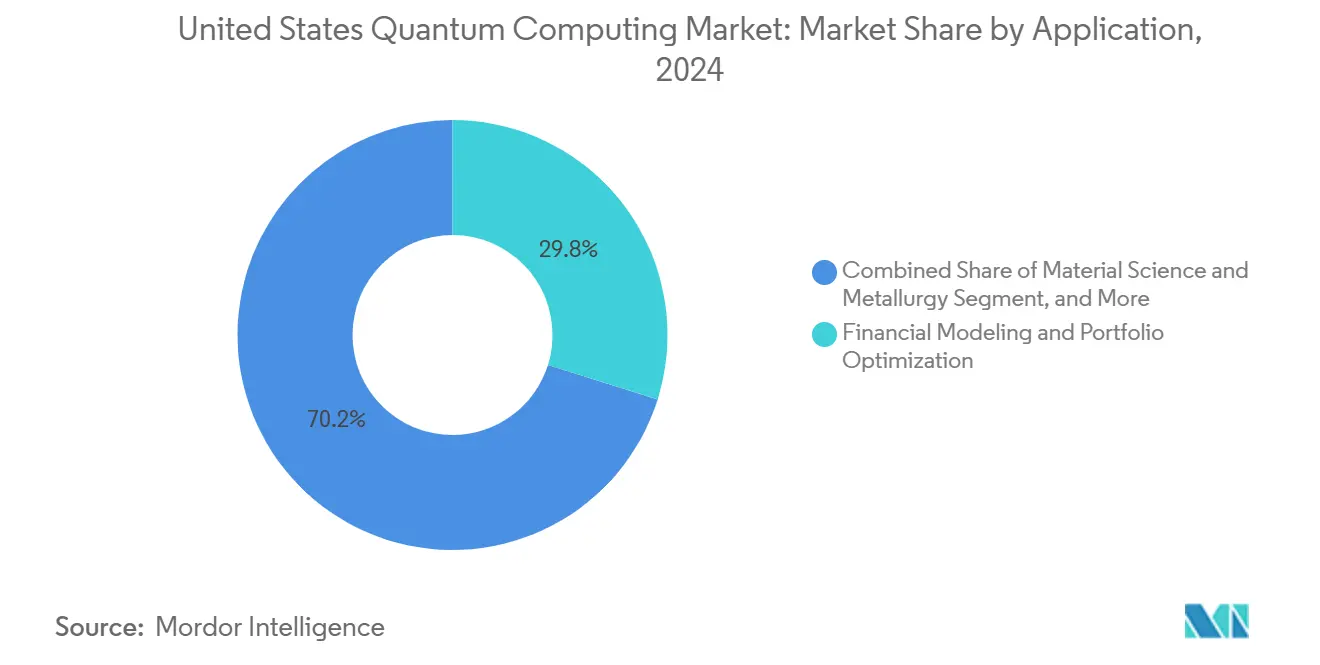

- By application, financial modeling and portfolio optimization accounted for 29.84% of the United States quantum computing market size in 2024, while drug discovery and molecular simulation are projected to expand at a 26.99% CAGR over the same horizon.

- By end-user industry, BFSI generated 28.73% of 2024 revenue in the United States quantum computing market, and healthcare and life sciences are on track for the fastest 27.07% CAGR through 2030.

United States Quantum Computing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated federal R&D funding through CHIPS and Science Act follow-on appropriations | +4.2% | National, concentrated in quantum hubs | Medium term (2-4 years) |

| Rise of quantum-ready cloud developer ecosystems (AWS Braket, Azure Quantum, IBM Q) | +3.8% | National, with West Coast leadership | Short term (≤ 2 years) |

| Strategic on-shoring of cryogenic and photonic supply chains for defense applications | +2.9% | Northeast and West regions | Long term (≥ 4 years) |

| Corporate demand for post-quantum cryptography migration assessments | +3.1% | National, BFSI sector concentration | Medium term (2-4 years) |

| Venture capital shift toward deep-tech hardware after AI valuation plateau | +2.7% | West Coast venture hubs | Short term (≤ 2 years) |

| State-level incentives (NY, CO, IL) to anchor quantum corridors and talent pipelines | +1.9% | Targeted state regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Federal R&D Funding Through CHIPS and Science Act Follow-on Appropriations

Federal outlays for quantum information science surged to USD 1.2 billion in 2024, a 40% jump from 2023, catalyzing commercialization pipelines across superconducting, trapped-ion, and photonic modalities.[1]White House, “FACT SHEET: Biden-Harris Administration Announces New Actions to Advance Quantum Computing,” whitehouse.gov Five new national quantum centers, each endowed with USD 125 million over five years, concentrate multidisciplinary expertise and foster public-private collaboration. The National Quantum Initiative Act’s reauthorization aligned NSF, DOE, and NIST mandates around applied research, while a novel equity-stake approach extends patient capital to strategically important startups. These initiatives narrow the investment gap with China and accelerate workforce development, thereby lifting demand for domestic hardware, software, and professional services over the medium term.

Rise of Quantum-Ready Cloud Developer Ecosystems

AWS Braket, Azure Quantum, and IBM Q collectively onboarded dozens of hardware partners in 2024, transforming quantum experimentation from a capital-intensive endeavor into a pay-per-use service.[2]Microsoft Azure, “Azure Quantum Development Kit,” azure.microsoft.com Enterprise developers can now prototype quantum algorithms through familiar SDKs, integrate them into classical pipelines, and iterate rapidly without acquiring dilution refrigerators or clean-room facilities. Cloud ecosystems produce a virtuous cycle: higher utilization yields richer telemetry, which feeds back into compiler optimizations and hardware refinements. Early commercial pilots in drug discovery, risk analytics, and supply-chain routing illustrate the pathway to quantum advantage, reinforcing near-term revenue visibility for platform providers.

Strategic On-Shoring of Cryogenic and Photonic Supply Chains for Defense Applications

The Defense Department earmarked USD 300 million in 2024 to localize manufacturing of dilution refrigerators, single-photon detectors, and photonic integrated circuits indispensable to quantum computers.[3]Department of Defense, “Department of Defense Announces Quantum Technology Initiatives,” defense.gov By mitigating dependence on European vendors, these measures compress lead times, improve ITAR compliance, and secure sensitive defense workloads. Colorado and New York cluster grants incentivize equipment makers to co-locate with quantum hardware firms, spawning regional supply-chain hubs. As domestic capacity scales, hardware vendors benefit from closer coordination with component suppliers, accelerating iterative design cycles and boosting production yields.

Corporate Demand for Post-Quantum Cryptography Migration Assessments

NIST’s finalized quantum-resistant encryption standards in August 2024 triggered industry-wide readiness audits.[4]National Institute of Standards and Technology, “NIST Releases First 3 Finalized Post-Quantum Encryption Standards,” nist.gov Leading banks budgeted multi-year migrations, with one top-three U.S. institution committing USD 200 million to quantum-safe infrastructure. Healthcare companies similarly expedite compliance paths to safeguard electronic health records, tying quantum adoption to clear regulatory milestones. Cyber-consultancies and specialized software integrators report full project pipelines, illustrating how security mandates can stimulate the United States quantum computing market even before large-scale fault-tolerant machines arrive.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of dilution-refrigerator manufacturing capacity inside the U.S. | -2.8% | National, affecting all quantum hardware deployments | Medium term (2-4 years) |

| Limited availability of ultra-pure helium-3 and other specialty isotopes | -1.9% | National, supply chain dependent | Long term (≥ 4 years) |

| Shortage of mid-career quantum algorithm engineers versus PhD-level theorists | -1.5% | National, concentrated in tech hubs | Short term (≤ 2 years) |

| Uncertain export-control regime for dual-use quantum hardware | -1.2% | National, affecting international partnerships | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scarcity of Dilution-Refrigerator Manufacturing Capacity Inside the U.S.

Only three domestic suppliers presently produce sub-10 millikelvin refrigeration systems, supporting roughly 50 machines per year versus projected demand surpassing 200 units by 2027. European dominance creates 12-18-month lead times, raising working-capital requirements for startups and extending pilot project timelines. DOE grants awarded in 2024 aim to quadruple U.S. capacity, yet complex brazing, vibration isolation, and cryogenic-plumbing competencies will take several years to mature. Defense customers face an added hurdle because ITAR restrictions forbid foreign cryostats in classified environments, further tightening supply.

Limited Availability of Ultra-Pure Helium-3 and Other Specialty Isotopes

Annual global helium-3 output remains capped near 15,000 liters, derived largely from nuclear weapons disassembly, making supply sporadic and politically sensitive. Quantum system builders compete with neutron detectors and medical-imaging applications for the isotope, inflating prices and adding procurement uncertainty. DOE’s tritium-decay program promises incremental supply increases post-2028, but until then, hardware vendors are investing in helium-3 reclamation and exploring alternative cooling schemes such as adiabatic demagnetization. These work-arounds add complexity, cost, and engineering risk, dampening near-term deployment momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Superconducting Leadership, Topological Disruption Brewing

Superconducting qubits delivered 47.83% of 2024 revenue in the United States quantum computing market, buoyed by rapid qubit-count scaling exemplified by IBM’s 1,121-qubit Condor processor. The United States quantum computing market size for superconducting platforms is projected to reach USD 800 million by 2030 as fabrication techniques inherited from conventional CMOS foundries continue to drive density gains. Yet the technology’s sensitivity to noise and cooling demands fuels interest in alternative modalities.

Topological qubits, though nascent, are forecast to expand at a 27.22% CAGR as Microsoft’s Majorana-based breakthroughs promise intrinsic error suppression. Trapped-ion architectures from IonQ and Quantinuum appeal to enterprises seeking high-fidelity gates for optimization tasks, while photonic qubits target quantum networking and secure communications. Quantum annealers remain niche, addressing combinatorial optimization in logistics and finance. Collectively, this diversity positions the United States quantum computing market to satisfy different performance, cost, and regulatory requirements as hardware matures.

By Deployment Model: Cloud Dominance, Hybrid Momentum

Cloud quantum services commanded 59.73% of 2024 spending, reflecting enterprises’ preference to rent rather than own exotic hardware. The segment’s United States quantum computing market size is on track to surpass USD 1 billion by 2030 as AWS, IBM, and Azure enlarge capacity, add hardware diversity, and extend developer tooling. Subscription-based access shortens proof-of-concept cycles and shifts capex to opex, attracting mid-market firms.

Hybrid classical-quantum solutions, the fastest-growing deployment model at 27.56% CAGR, integrate quantum kernels into HPC workflows, exploiting quantum speedups while retaining classical control logic. On-premises machines persist in defense and regulated sectors requiring air-gapped environments, but the cost premium confines demand to a narrow cohort. Over time, as error-rates fall and cryogenic form-factors shrink, hybrid architectures could displace pure cloud consumption, yet cloud will remain the default entry point for new adopters.

By Application: Finance Leads, Drug Discovery Accelerates

Financial optimization used quantum Monte Carlo and portfolio-rebalancing algorithms to secure 29.84% revenue share in 2024. Early pilots delivered run-time reductions in derivatives pricing, reinforcing BFSI’s first-mover posture. The United States quantum computing market share for finance applications is expected to contract gradually as other verticals scale, but absolute spending will still rise given expanding total demand.

Drug discovery and molecular simulation, expanding at a 26.99% CAGR, reflect pharma’s appetite for accelerating lead-candidate screening. Roche’s collaboration with IBM targets reducing protein-folding timeframes, a tangible business benefit that can translate into earlier clinical entry. Cybersecurity, logistics optimization, machine learning acceleration, and material science form a second wave of growth opportunities aligned with regulatory milestones and federal research grants.

By End-User Industry: BFSI Out-in-Front, Healthcare Ramping Fast

The BFSI cohort captured 28.73% of 2024 revenue as quantitative trading desks, risk managers, and compliance teams scrambled to derive even marginal speed advantages. Although its United States quantum computing market size dominance will taper slightly by 2030, incremental regulations like Basel IV and the SEC’s cyber-risk disclosures preserve spending momentum.

Healthcare and life sciences, rising at 27.07% CAGR, exemplify how quantum simulation compresses R&D timelines for biologics and small molecules. Government and defense segments prioritize quantum-safe communications, while automotive, aerospace, and energy industries experiment with materials design and supply-chain routing. Academic institutions, buoyed by NSF awards, continue to serve as crucibles for algorithm innovation that later migrates into commercial stacks.

Geography Analysis

California anchors more than 40% of company headquarters and research centers engaged in the United States quantum computing market, benefiting from proximity to cloud-service giants and a deep venture-capital pool. Google’s Santa Barbara lab, IBM’s Almaden facilities, and a constellation of startups provide a critical mass of talent, intellectual property, and pilot customers. Washington state supplements West-Coast leadership through Microsoft’s Redmond presence and robust university programs.

The Northeast advances through IBM’s quantum headquarters in New York and academic nodes at MIT, Harvard, and Yale. State-level incentives, including New York’s USD 100 million corridor initiative, attract hardware makers and software spinouts. Financial-services density in New York City supplies ready demand for quantum risk analytics, while Boston’s innovation ecosystem feeds a steady stream of post-docs into commercial roles.

Midwest and Southern states secure federal funding to diversify geographic participation. Colorado leverages NIST laboratories, Illinois taps Argonne National Laboratory for networked-quantum research, and Texas courts hardware suppliers through tax incentives. These programs emphasize workforce-development pipelines and specialized fabrication capabilities, broadening the United States quantum computing market’s talent and supply-chain base beyond legacy tech hubs.

Competitive Landscape

Competition spans technology behemoths, well-funded pure-plays, and niche software specialists, producing a moderately fragmented structure. IBM leads in installed superconducting capacity and operates the world’s largest quantum-cloud network, charging subscription fees and offering co-development partnerships. Google focuses on algorithm performance and public benchmarks, while Microsoft concentrates on topological fault tolerance, aligning its roadmap with Azure stack synergies.

Rigetti, IonQ, and Quantinuum pioneer differentiated hardware, superconducting, trapped-ion, and integrated photonics, respectively, aiming to leapfrog incumbents in error rates or gate connectivities. Patent filings exceeded 3,000 for IBM alone in 2024, signaling an escalating intellectual-property arms race. Vertical-software providers such as Zapata and QC Ware monetize algorithm toolkits and hybrid runtime environments, partnering with multiple hardware back ends.

Strategic moves in 2024 illustrate maturing commercialization: IBM hit a 1,000-qubit milestone, Google secured a USD 300 million pharma alliance, Microsoft demonstrated Majorana qubits, and AWS broadened Braket’s hardware roster. Defense contracts to Rigetti and national-lab collaborations for Quantinuum underscore government’s dual role as funder and first customer. Collectively, these developments heighten the pace of innovation while leaving room for new entrants to target unserved niches such as quantum networking and error-mitigation software.

United States Quantum Computing Industry Leaders

IBM Corporation

Google LLC

Microsoft Corporation

Amazon Web Services, Inc.

Rigetti and Co, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: IBM began beta access to its 1,121-qubit Condor system for select enterprise clients, marking the first commercialization phase of its quantum utility milestone.

- October 2024: IBM revealed quantum utility results on optimization workloads using the Condor processor, demonstrating tangible speedups for enterprise partners.

- September 2024: Google’s USD 300 million partnership with Roche advanced quantum-accelerated molecular simulation for oncology drug candidates.

- August 2024: Microsoft achieved reliable manipulation of Majorana fermions, a critical step toward fault-tolerant topological qubits.

United States Quantum Computing Market Report Scope

The United States Quantum Computing Market Report is Segmented by Technology (Quantum Annealing, Superconducting Qubits, Trapped-Ion Qubits, Photonic Qubits, Topological Qubits, Other Emerging Modalities), Deployment Model (On-Premises, Cloud-based Quantum-as-a-Service, Hybrid), Application (Drug Discovery, Financial Modeling, Logistics Optimization, Cryptography, Material Science, Machine Learning, Other Applications), End-user Industry (Healthcare, BFSI, Automotive, Chemicals, Energy, Government, Academia, IT, Other Industries), and Geography (Northeast, Midwest, South, West). The Market Forecasts are Provided in Terms of Value (USD).

| Quantum Annealing |

| Superconducting Qubits |

| Trapped-Ion Qubits |

| Photonic Qubits |

| Topological Qubits |

| Other Technologies |

| On-Premises Quantum Computers |

| Cloud-based Quantum-as-a-Service |

| Hybrid (Classical + Quantum) Solutions |

| Drug Discovery and Molecular Simulation |

| Financial Modeling and Portfolio Optimization |

| Logistics, Routing and Supply-Chain Optimization |

| Cryptography and Cyber-security |

| Material Science and Metallurgy |

| Machine Learning and AI Acceleration |

| Other Applications |

| Healthcare and Life Sciences |

| Banking, Financial Services and Insurance (BFSI) |

| Automotive and Aerospace |

| Chemicals and Materials |

| Energy and Utilities |

| Government and Defense |

| Academia and Research Institutes |

| IT and Telecommunications |

| Other End-user Industries |

| By Technology | Quantum Annealing |

| Superconducting Qubits | |

| Trapped-Ion Qubits | |

| Photonic Qubits | |

| Topological Qubits | |

| Other Technologies | |

| By Deployment Model | On-Premises Quantum Computers |

| Cloud-based Quantum-as-a-Service | |

| Hybrid (Classical + Quantum) Solutions | |

| By Application | Drug Discovery and Molecular Simulation |

| Financial Modeling and Portfolio Optimization | |

| Logistics, Routing and Supply-Chain Optimization | |

| Cryptography and Cyber-security | |

| Material Science and Metallurgy | |

| Machine Learning and AI Acceleration | |

| Other Applications | |

| By End-user Industry | Healthcare and Life Sciences |

| Banking, Financial Services and Insurance (BFSI) | |

| Automotive and Aerospace | |

| Chemicals and Materials | |

| Energy and Utilities | |

| Government and Defense | |

| Academia and Research Institutes | |

| IT and Telecommunications | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is the United States quantum computing market in 2025?

It is valued at USD 630 million in 2025 and is forecast to grow to USD 1.7 billion by 2030.

Which technology currently leads commercial deployments?

Superconducting qubits command 47.83% of 2024 revenue, sustained by rapid qubit-count scaling.

What is the fastest-growing end-user segment?

Healthcare and life sciences are expanding at a 27.07% CAGR through 2030 due to quantum-enabled drug discovery.

Why are cloud services critical to adoption?

Cloud-based quantum-as-a-service models remove capex barriers, capturing 59.73% of 2024 deployment spending.

What supply-chain challenge most constrains hardware scale-up?

Limited domestic dilution-refrigerator capacity imposes 12-18-month lead times and inflates project costs.

Page last updated on: