United States Project Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

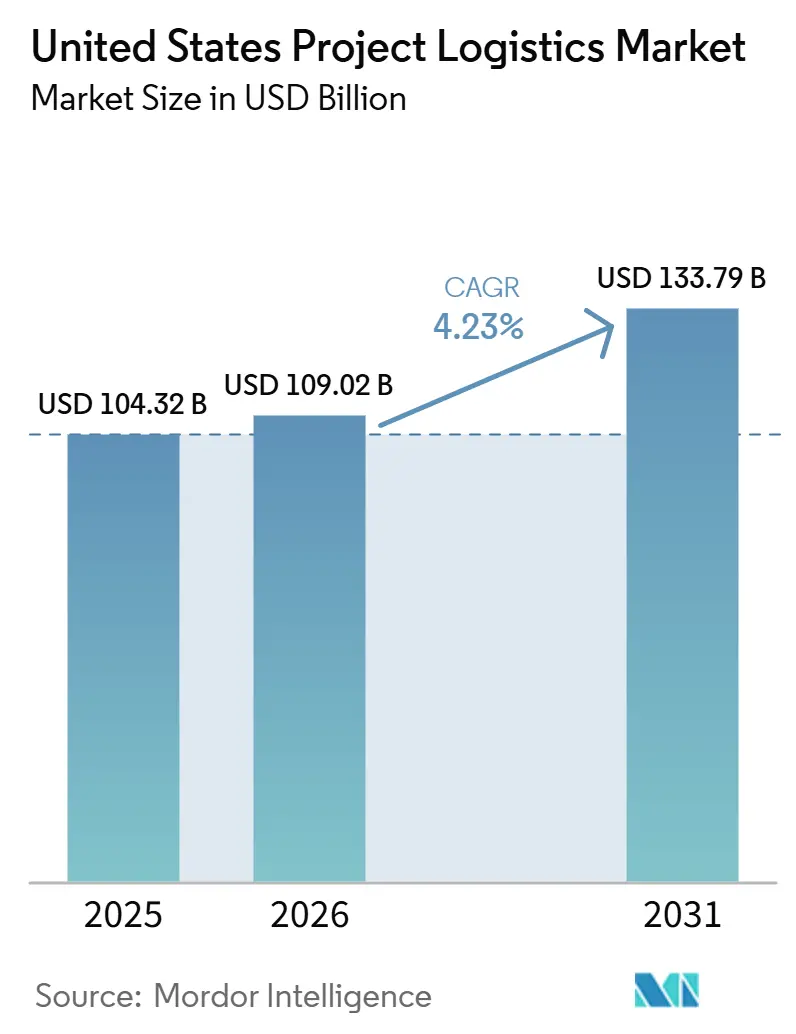

| Base Year Market Size (2025) | USD 104.32 Billion |

| Market Size (2026) | USD 109.02 Billion |

| Market Size (2031) | USD 133.79 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

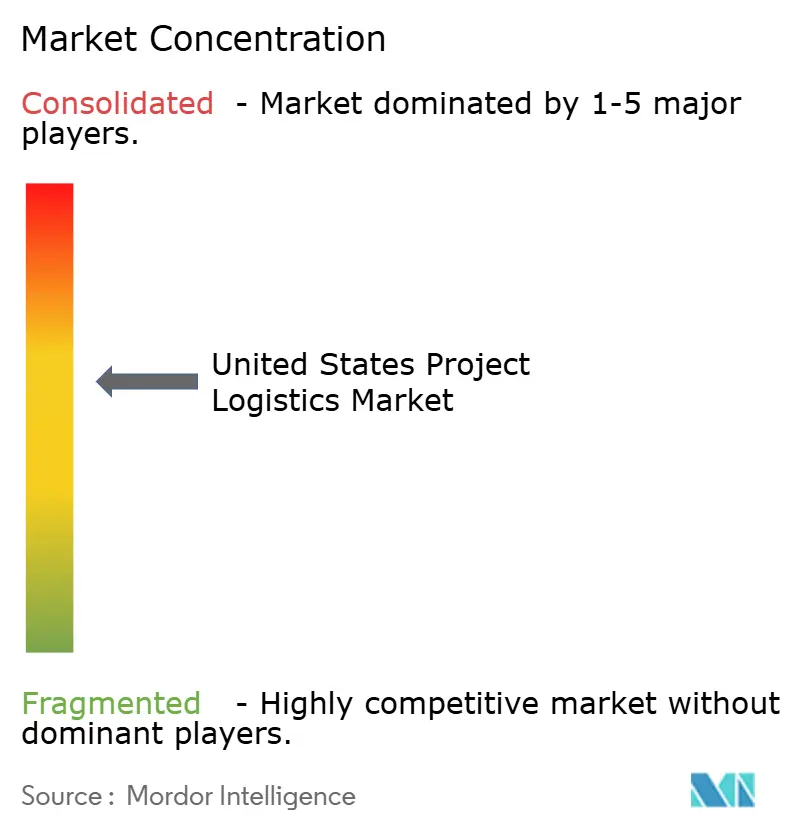

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Project Logistics Market Analysis by Mordor Intelligence

The United States project logistics market size was valued at USD 104.32 billion in 2025 and estimated to grow from USD 109.02 billion in 2026 to reach USD 133.79 billion by 2031, at a CAGR of 4.23% during the forecast period 2026-2031.

Growth in the United States project logistics market is being shaped by a visible shift in capital spending toward renewable energy, LNG infrastructure, semiconductor manufacturing, and AI-led data center construction. These projects rely on cargo that is oversized, route-engineered, permit-dependent, and often tied to narrow construction windows, which keeps the United States project logistics market distinct from standard freight activity. The United States project logistics market also remains more resilient than parcel or container logistics because much of the work centers on indivisible cargo, specialist lifting plans, and coordination across ports, roads, rail links, and project sites. Competition in the United States project logistics market is split between global multimodal providers with broad contract logistics reach and specialist heavy-lift operators with owned SPMTs, crane fleets, and deep route engineering. The strongest opportunities in the United States project logistics market lie with providers that can combine permitting, engineering support, warehousing, timed delivery, and equipment control within a single execution model.

Key Report Takeaways

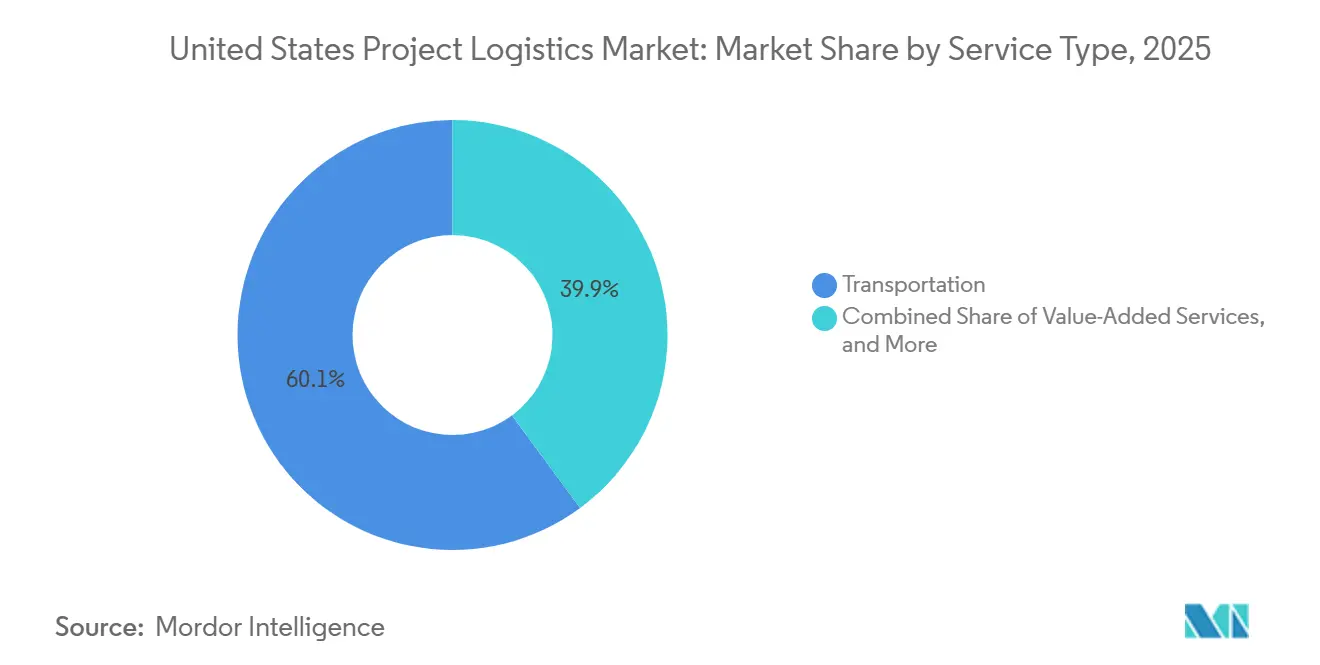

- By service, transportation led with 60.12% of the United States project logistics market share in 2025, while value-added services and others are forecast to expand at a 5.68% CAGR through 2031.

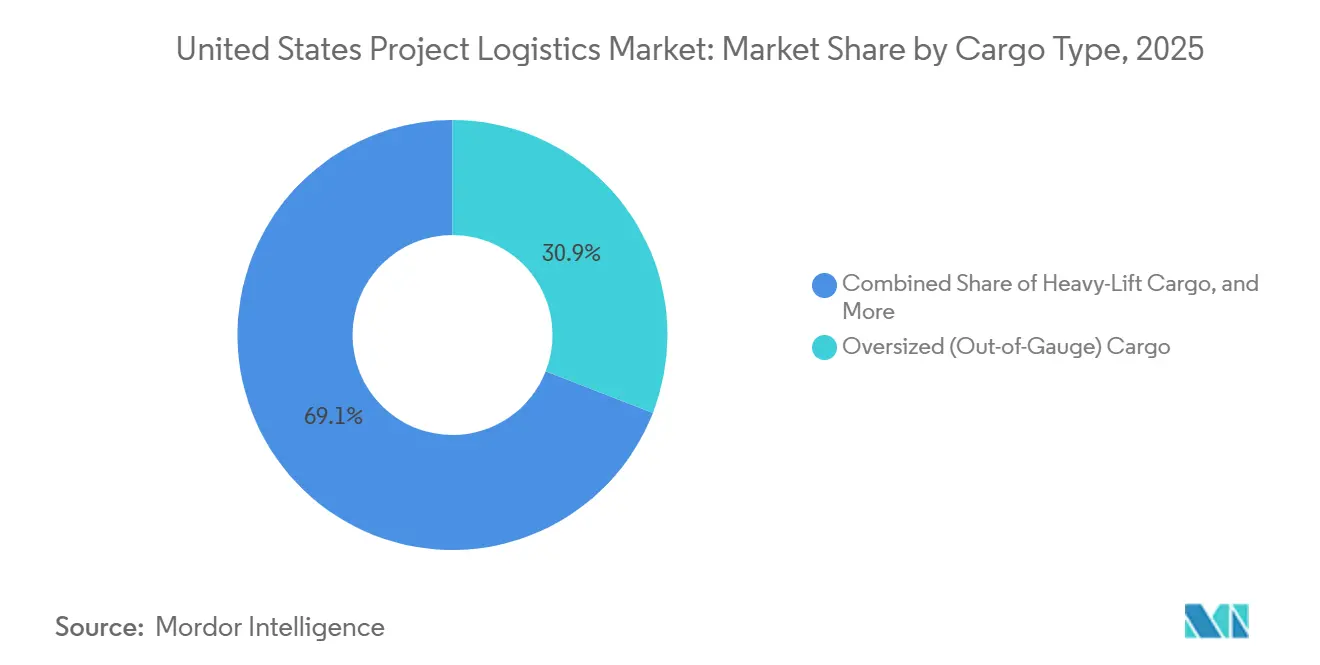

- By cargo type, oversized or out-of-gauge cargo held 30.85% share of the United States project logistics market size in 2025, while heavy-lift cargo recorded the highest projected CAGR at 5.12% through 2031.

- By end-user industry, oil and gas, mining, and quarrying accounted for 24.56% of of the United States project logistics market share in 2025, while energy generation and transmission, including renewable energy, is advancing at a 4.98% CAGR through 2031.

- By geography, the Southwest accounted for 37.32% of the United States project logistics market size in 2025, while the West is projected to grow at a 5.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Project Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Utility-Scale Renewable Energy Projects Supported by the Inflation Reduction Act (IRA) | +1.0% | National, with concentration in Southwest (TX, NM), Southeast (VA, NC), and West (CA, AZ) | Medium term (2–4 years) |

| Expansion of Gulf Coast LNG Export Terminals and Petrochemical Installations | +0.8% | Southwest (TX, LA); spill-over to Southeast port corridors | Medium term (2–4 years) |

| Accelerated Construction of Hyperscale Data Centers and AI Infrastructure | +0.9% | National; early gains in Southwest (TX), Southeast (LA), West (NV, CA), and Midwest (MI, OH) | Short term (≤ 2 years) |

| Federal Infrastructure Investments Upgrading Port, Rail, and Highway Connectivity (IIJA) | +0.6% | National; strongest in Southwest (TX, LA), West (CA, WA), and Midwest port corridors | Long term (≥ 4 years) |

| Reshoring Initiatives and Semiconductor Fabrication Plant (Fab) Construction (CHIPS Act) | +0.7% | West (AZ), Northeast (NY), spill-over to Southwest (TX) and Midwest (OH) | Medium term (2–4 years) |

| Increasing Demand for Specialized Multimodal Heavy-Lift Transport Solutions | +0.5% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Utility-Scale Renewable Energy Projects Supported by the Inflation Reduction Act (IRA)

Renewable energy projects continue to add steady volume to the United States project logistics market because large wind and solar sites depend on timed delivery of nacelles, transformer banks, tower sections, and other heavy components that cannot move through ordinary truckload networks. This cargo mix favors providers that can secure permits early, stage equipment near project sites, and line up escort, rigging, and crane support before field work reaches its peak delivery phase. Landstar reported heavy-haul revenue of nearly USD 170 million in Q4 2025, up 23% from Q4 2024, with wind and solar customers contributing to that acceleration in demand. Larger renewable energy components are also pushing more projects toward SPMT-led transport and engineered lift planning, which raises barriers for smaller operators without specialized assets or route expertise. Sarens completed the final onshore scope for the Coastal Virginia Offshore Wind project in 2026, after carrying out 740 SPMT operations and 382 heavy lifts, demonstrating the scale that renewable energy work now requires. As project schedules tighten around site readiness, grid connection, and construction sequencing, renewable energy work is driving stronger demand for bundled engineering, storage, and delivery coordination across the United States project logistics market[1]“Securing the U.S. Supply Chain for the Wind Energy Industry.” U.S. Department of Energy, 2026., energy.gov/cmei/systems/securing-us-supply-chain-wind-energy-industry.

Expansion of Gulf Coast LNG Export Terminals and Petrochemical Installations

LNG and petrochemical construction is supplying the United States project logistics market with a steady stream of modules, cryogenic equipment, pressure vessels, turbines, and fabricated assemblies that are heavy, oversized, and permit-intensive. Golden Pass, the 10th United States LNG export terminal, shipped its first cargo from Train 1 in April 2026, while Trains 2 and 3 remained scheduled for later commissioning phases, which kept Gulf Coast cargo activity elevated. Cheniere Energy’s Corpus Christi Stage 3 project reached substantial completion of Train 5 in March 2026, which supported continued movement of industrial cargo through Gulf Coast corridors. Cheniere Partners also signed a lump-sum, turnkey EPC contract with Bechtel in May 2026 for the first phase of the Sabine Pass expansion, covering Train 7 and supporting infrastructure, providing more than 6 million tons per annum of additional LNG capacity. Glenfarne’s Texas LNG and Kiewit executed a similar EPC contract in March 2026 for a 4-million-ton-per-annum facility at the Port of Brownsville, which added another large project to the same corridor. With multiple large builds progressing at once, the United States project logistics market is seeing tighter vessel availability, narrower labor buffers, and stronger pricing support in Gulf Coast heavy-lift lanes[2]“The 9th U.S. liquefied natural gas export terminal, Golden Pass LNG, shipped its first cargo.” U.S. Energy Information Administration, www.eia.gov/todayinenergy.

Accelerated Construction of Hyperscale Data Centers and AI Infrastructure

Hyperscale data center construction is creating a rapidly expanding cargo stream in the United States project logistics market, centered on large transformers, UPS systems, cooling units, switchgear, racks, and other high-value equipment that require controlled handling and precise delivery timing. DHL Supply Chain announced 10 dedicated North American data center logistics warehouse sites in 2026, totaling more than 7 million square feet, which reflects the need for specialized staging and warehouse-to-site execution. Meta expanded its Richland Parish campus in Louisiana in 2026 from a 2-gigawatt plan to a 5-gigawatt, USD 50 billion development, showing how quickly site scale is rising. Oracle and OpenAI also advanced the USD 16 billion Stargate campus in Saline Township, Michigan, in June 2026, which added another major project with synchronized construction and equipment schedules. These sites leave very little room for missed crane windows or late deliveries because mechanical, electrical, and commissioning trades often move in parallel once structures are ready. That operating rhythm is pushing the United States project logistics market toward more warehousing control, better tracking visibility, and tighter last-mile scheduling than many traditional industrial projects required.

Reshoring Initiatives and Semiconductor Fabrication Plant Construction Under the CHIPS Act

Semiconductor reshoring is adding one of the most demanding cargo categories to the United States project logistics market, as fab projects require extremely sensitive equipment, modular cleanroom systems, and high-purity utility infrastructure that cannot tolerate handling errors or unstable transit conditions. As of Q1 2026, the CHIPS Program Office had awarded more than USD 36 billion in direct grants and USD 12 billion in federal loans, supporting combined private-sector capital commitments of more than USD 450 billion through 2030. Micron’s USD 100 billion New York megafab began foundation construction in July 2026, marking the start of a major, long-cycle cargo program with large equipment and staged installation requirements. TSMC’s Arizona Fab 21 Phase 2 shell stands complete in 2026, with equipment installation beginning in Q3 2026, while Samsung’s Taylor, Texas facility also continues to advance toward operating status. Semiconductor projects place logistics planning on the critical path because route selection, vibration control, environmental protection, and timed site delivery all matter as much as pure transport capacity. As a result, the United States project logistics market is gaining more value from engineering-led execution than from basic freight movement alone.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent State-by-State Transport Regulations and Bridge Weight Limitations | -0.4% | National; most acute in Northeast, Midwest, and West corridors with aging bridge infrastructure | Long term (≥ 4 years) |

| Persistent Shortages of Specialized Labor and Experienced Heavy-Haul Drivers | -0.5% | National; highest vacancy rates in TX, FL, AZ, and CO | Medium term (2–4 years) |

| High Capital Expenditure and Maintenance Costs for Specialized Heavy-Lift Fleets | -0.3% | National; most pronounced for small-to-mid-tier operators | Long term (≥ 4 years) |

| Volatile Equipment Costs and Coordination Challenges Across Multi-State Jurisdictions | -0.2% | National; compound complexity on multi-state routes (Southwest to Midwest corridors) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent State-By-State Transport Regulations and Bridge Weight Limitations

State permitting remains a major operating restraint for the United States project logistics market because oversize and overweight transport still lacks a uniform national framework across all 50 states. The Federal Highway Administration sets an interstate legal vehicle weight limit of 80,000 pounds. At the same time, many project cargo superloads exceed that threshold and require route-specific approvals, engineering checks, and special designations. Bridge conditions in parts of the Northeast and Midwest make the issue harder because older infrastructure reduces the number of viable corridors for the heaviest equipment moves. That often forces longer routes, more escorts, and tighter sequencing between road carriers, rail links, and site teams, which increases costs and schedule risk. Operators without in-house permitting expertise are at a disadvantage because every state can apply different dimensional rules, review times, and routing conditions. When LNG, renewable energy, semiconductor, and public infrastructure projects run concurrently, the available route network within the United States project logistics market becomes even more constrained[3] “State Oversize/Overweight Load Permit Contacts.” Federal Highway Administration, ops.fhwa.dot.gov.

Persistent Shortages of Specialized Labor and Experienced Heavy-Haul Drivers

Specialized labor shortages are limiting execution capacity in the United States project logistics market because heavy-haul drivers, crane operators, riggers, and permit specialists take longer to train and replace than general freight labor. The labor gap is especially difficult in fast-growth states such as Texas, Florida, Arizona, and Colorado, where multiple capital projects compete for the same skilled workforce. The Specialized Carriers and Rigging Association launched its “40 Schools for 40 Years Workforce Challenge” in February 2026 to expand the talent pipeline, indicating that the shortage is serious enough to trigger organized industry action. Firms also need workers with experience in oversize-load handling, certification compliance, and jobsite coordination, which further narrows the pool. Hiring delays leave cranes, trailers, and staged cargo underused even when customer demand is present, reducing throughput and stretching mobilization timelines. This labor bottleneck matters across the United States project logistics market because technical project cargo cannot be scaled up as quickly as ordinary truckload capacity[4]“News & Media - SC&RF.” Specialized Carriers and Rigging Foundation, scr-foundation.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Anchors Revenue as Value-Added Offerings Scale

Transportation held 60.12% of the United States project logistics market share in 2025, confirming that physical movement remains the core revenue engine for heavy and oversized-cargo programs. Road-based heavy haul plays the largest role because it links fabrication yards, marine terminals, intermodal transfer points, and remote construction sites where rail or barge cannot complete the final leg. Flatbeds, multi-axle trailers, and SPMT configurations, therefore, remained central to execution across energy, manufacturing, defense, and infrastructure cargo flows. Rail and sea or barge modes still offered important corridor advantages on longer routes where bridge limits, highway height restrictions, or urban access constraints made over-road transport less efficient. Landstar reported USD 134 million in heavy-haul revenue in Q1 2026, up 18% year over year, with customers spanning data centers, energy, government, aerospace, and defense.

Value-added services and other services are projected to expand at a 5.68% CAGR through 2031, making them the fastest-growing service lines within the United States project logistics market. That growth reflects a buyer preference for a single provider that can manage feasibility reviews, customs coordination, rigging support, warehousing, and cargo visibility, rather than handing the same project to multiple firms. Warehousing, distribution, and inventory management are also becoming more important because project sites often face timing gaps between fabrication completion and field readiness. DHL’s 2026 rollout of 10 dedicated North American data center logistics warehouses shows how larger providers are building around staging, handling, and scheduled site delivery rather than only transport volume. The service mix in the United States project logistics market is therefore moving toward bundled execution, where engineering support and schedule control increasingly shape customer value.

By Cargo Type: Out-of-Gauge Leads Volume, Heavy-Lift Leads Growth

Oversized or out-of-gauge cargo accounted for 30.85% of the United States project logistics market size in 2025, reflecting the steady flow of wind nacelles, industrial process modules, transformer banks, structural sections, and other bulky components. This cargo group remains the largest because many project sites can still accommodate oversized pieces without the extreme lift planning required for the heaviest industrial loads. The operating challenge is that component dimensions keep increasing, placing greater pressure on highway clearances, bridge capacity, staging space, and escort planning. That dynamic gives route engineering, load distribution analysis, and early permit work a bigger role in the United States project logistics market than in more standardized freight categories. Providers that can prequalify corridors and plan around bottlenecks are in a stronger position when projects reach the final construction phase.

Heavy-lift cargo is estimated to grow at a 5.12% CAGR through 2031, making it the fastest-growing cargo category in the United States project logistics market. Growth is being driven by offshore wind foundation structures, LNG heat exchangers, offshore substation topsides, and other engineered loads that require purpose-built lifting systems and exact site coordination. Sarens completed the Coastal Virginia Offshore Wind onshore scope in 2026 after 740 SPMT transport operations and 382 heavy lifts, including topsides weighing close to 4,000 metric tons each. Breakbulk cargo and other project-specific configurations still serve an important role, especially on Gulf Coast industrial routes and mixed international equipment programs. Even so, the best margin support in the United States project logistics market remains concentrated in the technically hardest heavy-lift work, where equipment access and engineering credibility matter more than spot pricing.

By End-User Industry: Oil and Gas Anchors the Base, Renewables Define the Direction

Oil and gas, mining, and quarrying accounted for 24.56% of the United States project logistics market share in 2025, which kept the segment in the lead across end-user categories. The sector stayed strong because Gulf Coast LNG construction, Permian Basin midstream expansion, refinery maintenance programs, and industrial turnaround activity continue to create recurring project cargo demand. Sarens carried out heavy lifting operations at a petrochemical facility in Beaumont, Texas, in March 2026, underscoring the recurring nature of work associated with large industrial assets in this vertical. Phillips 66’s Iron Mesa cryogenic gas processing plant, under construction in Ector County, adds another source of module, vessel, and equipment transport demand in the Permian corridor. This recurring industrial base helps the United States project logistics market maintain equipment utilization even when project timing shifts in newer sectors.

Energy generation and transmission, including renewable energy, is forecast to grow at a 4.98% CAGR through 2031, giving it the fastest pace among end-user groups. Offshore wind, utility-scale solar, land-based wind, and grid equipment programs are expanding the list of transformers, switchgear, tower sections, foundations, and oversize structural components that must be moved under controlled schedules. Transmission and interconnection timing can delay equipment release, making flexible warehousing and hold-and-release capabilities more valuable for logistics providers serving these projects. Construction and infrastructure, manufacturing and industrial plants, and aerospace and defense continue to broaden the customer base. NASA’s Mobile Launcher 2 crane mobilization at Kennedy Space Center demonstrated that single-site programs in aerospace can still demand unusually large fleets, extended setup periods, and specialized coordination across the United States project logistics market.

Geography Analysis

The Southwest held 37.32% of the United States project logistics market size in 2025, the largest regional share. Its lead comes from the concentration of Gulf Coast LNG terminals, Permian Basin infrastructure, renewable energy installations, and semiconductor activity spread across Texas, New Mexico, Louisiana, and Arizona. Cheniere's Corpus Christi Stage 3 remained ahead of schedule in 2026, while the Texas LNG project at the Port of Brownsville moved forward after Glenfarne and Kiewit signed their EPC contract in March 2026. BNSF also began construction on a 350-acre intermodal facility at Logistics Park Phoenix in early 2026, adding rail-connected staging capacity to Arizona's fast-growing industrial corridor. A 600,000-pound transformer move for the Salt River Project in Pinal County showed how routine high-intensity heavy-haul work has become across the Southwest build cycle.

The West is projected to grow at a 5.27% CAGR through 2031, making it the fastest-growing region in the United States' project logistics market. Semiconductor investment and data center buildouts are the main drivers of demand, especially in Arizona, Nevada, and California. TSMC's Arizona Fab 21 Phase 2 shell is complete in 2026, with equipment installation beginning in Q3 2026, which supports a longer cycle of specialized equipment inflows and staging needs. Port and rail investments are also changing inland distribution from West Coast gateways, which should improve project cargo positioning for interior destinations over time.

The Northeast, Southeast, and Midwest made up the remaining regional base in 2025, each with a different project profile. The Northeast remains tied to offshore wind port logistics, and Sarens completed the final onshore scope at the Coastal Virginia Offshore Wind project in May 2026 after 740 SPMT operations and 382 heavy lifts. The Southeast benefits from automotive, aerospace, and power grid work, and South Carolina Ports completed a USD 55 million expansion of Inland Port Greer in March 2025 to strengthen inland rail connectivity. The Midwest is becoming more relevant for data center construction and heavy-lift terminal capacity, with the Stargate campus advancing in Michigan and Ports of Indiana securing a USD 32 million federal grant in July 2026 for Jeffersonville port expansion. Record port funding from the United States Department of Transportation in April 2026 also supported upgrades across multiple regions, although the pace beyond FY2026 may depend on future program direction.

Competitive Landscape

Competition in the United States project logistics market remains split between large multimodal integrators and specialist heavy-lift operators, keeping the field from consolidating around a single winning service model. Global providers bring scale in forwarding, contract logistics reach, and multinational customer relationships, while heavy-lift specialists compete through equipment ownership, engineering depth, and route knowledge. DSV completed its acquisition of DB Schenker in April 2025 for EUR 14.3 billion (USD 15.7 billion), expanding its project cargo footprint and broader logistics depth in North America. CMA CGM Group announced the acquisition of FedEx Supply Chain in July 2026 for an enterprise value of USD 1.4 billion, adding contract logistics and specialized transportation capacity in North America. C.H. Robinson also acquired DeSpir Logistics in June 2026 for USD 75 million, adding secure transportation and cargo escort capabilities for high-value, mission-critical freight.

Specialist operators continue to defend a significant share of the United States project logistics market because engineered lifting, SPMT deployment, and multi-night route execution are not easy to replicate. Mammoet completed six Terminal F module transports at Dallas Fort Worth International Airport in August 2025 using SPMTs, highlighting the execution premium available to firms with specialized heavy transport capability. Sarens showed the same advantage through its final Coastal Virginia Offshore Wind scope, where high-volume heavy lifts and repeated SPMT moves required both asset access and engineering discipline. Once lift plans, route approvals, and site sequencing are fixed, buyers have limited scope to switch providers, which helps specialists protect margins on the hardest jobs.

Technology and bundled support services are becoming a stronger competitive filter across the United States project logistics market, as customers increasingly demand visibility, staging, and schedule control for project cargo delivery. DHL’s dedicated data center logistics warehouse rollout in 2026 showed how larger operators are building repeatable service platforms around white-glove handling, rack configuration, and timed final delivery. Permitting remains a strategic differentiator as well, since major LNG expansions still depend on regulatory approvals and coordinated project sequencing, which directly affects bidding, fleet planning, and pricing assumptions. The United States project logistics market, therefore, favors providers that can combine engineering depth, warehouse control, access to specialized equipment, and the financial capacity to support long-cycle infrastructure programs.

United States Project Logistics Industry Leaders

DHL Group

Kuehne+Nagel

DSV A/S

CMA CGM Group

GEODIS

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: CMA CGM Group announced the acquisition of FedEx Supply Chain at an enterprise value of USD 1.4 billion, strengthening the group's contract logistics and specialized transportation presence across North America. The transaction is expected to materially expand CMA CGM's last-mile and warehousing capabilities in the United States, project cargo, and industrial logistics sectors.

- June 2026: C.H. Robinson Worldwide acquired DeSpir Logistics for approximately USD 75 million in cash, adding a specialized provider of secure transportation and cargo escort services for high-value, high-risk, and mission-critical freight across North America; the deal targets growth in aerospace, data center, and life sciences segments where precision execution and security compliance are key decision factors.

- May 2026: Cheniere Energy Partners signed a lump-sum, turnkey EPC contract with Bechtel for Phase 1 of the Sabine Pass Liquefaction Expansion, covering Train 7 and supporting infrastructure for more than 6 million tons per annum of additional LNG capacity; full construction is expected to begin in early 2027, generating sustained heavy-lift and module transport demand across the Gulf Coast corridor.

- March 2026: DHL Supply Chain announced the establishment of 10 dedicated North American data center logistics warehouse sites totaling more than 7 million square feet of capacity, set to go live in 2026, targeting hyperscale and colocation operators with white-glove handling, rack configuration services, and specialized warehouse-to-site transportation.

United States Project Logistics Market Report Scope

| Transportation | Road |

| Rail | |

| Air | |

| Sea/Barge | |

| Warehousing, Distribution and Inventory Management | |

| Value-added Services and Others |

| Oversized (Out-of-Gauge) Cargo |

| Heavy-Lift Cargo |

| Breakbulk Cargo |

| Others |

| Oil and Gas, Mining and Quarrying |

| Energy Generation and Transmission (Includes Renewable Energy) |

| Construction and Infrastructure |

| Manufacturing and Industrial Plants |

| Aerospace and Defense |

| Others (Maritime and Shipbuilding, Telecommunications, etc.) |

| Northeast |

| Southwest |

| West |

| Southeast |

| Midwest |

| By Service | Transportation | Road |

| Rail | ||

| Air | ||

| Sea/Barge | ||

| Warehousing, Distribution and Inventory Management | ||

| Value-added Services and Others | ||

| By Cargo Type | Oversized (Out-of-Gauge) Cargo | |

| Heavy-Lift Cargo | ||

| Breakbulk Cargo | ||

| Others | ||

| By End-User Industry | Oil and Gas, Mining and Quarrying | |

| Energy Generation and Transmission (Includes Renewable Energy) | ||

| Construction and Infrastructure | ||

| Manufacturing and Industrial Plants | ||

| Aerospace and Defense | ||

| Others (Maritime and Shipbuilding, Telecommunications, etc.) | ||

| By Geography | Northeast | |

| Southwest | ||

| West | ||

| Southeast | ||

| Midwest |

Key Questions Answered in the Report

What is the 2031 outlook for project logistics activity in the United States?

The United States project logistics market is forecast to reach USD 133.79 billion by 2031 from USD 109.02 billion in 2026, growing at a 4.23% CAGR over 2026-2031.

Which service area generates the most revenue in this space?

Transportation leads the revenue mix with 60.12% share in 2025, supported by heavy-haul road movements between fabrication yards, ports, and project sites.

Which cargo category is growing the fastest?

Heavy-lift cargo is the fastest-growing category, advancing at a 5.12% CAGR through 2031 as offshore wind, LNG, and other engineered projects require more specialized lifting.

Why is the Southwest the leading regional hub?

The Southwest held 37.32% share in 2025 because Gulf Coast LNG terminals, Permian infrastructure, renewable energy projects, and semiconductor investment are heavily concentrated there.

What is driving demand from data centers and semiconductor fabs?

Hyperscale data centers and semiconductor fabs require high-value transformers, cooling systems, cleanroom modules, and other sensitive equipment that must arrive on exact schedules.

What is the biggest operating challenge for providers?

State-level permitting complexity and shortages of specialized labor are major constraints because they reduce route flexibility, extend project timelines, and limit the rate at which capacity can scale.

Page last updated on: