United States HBM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

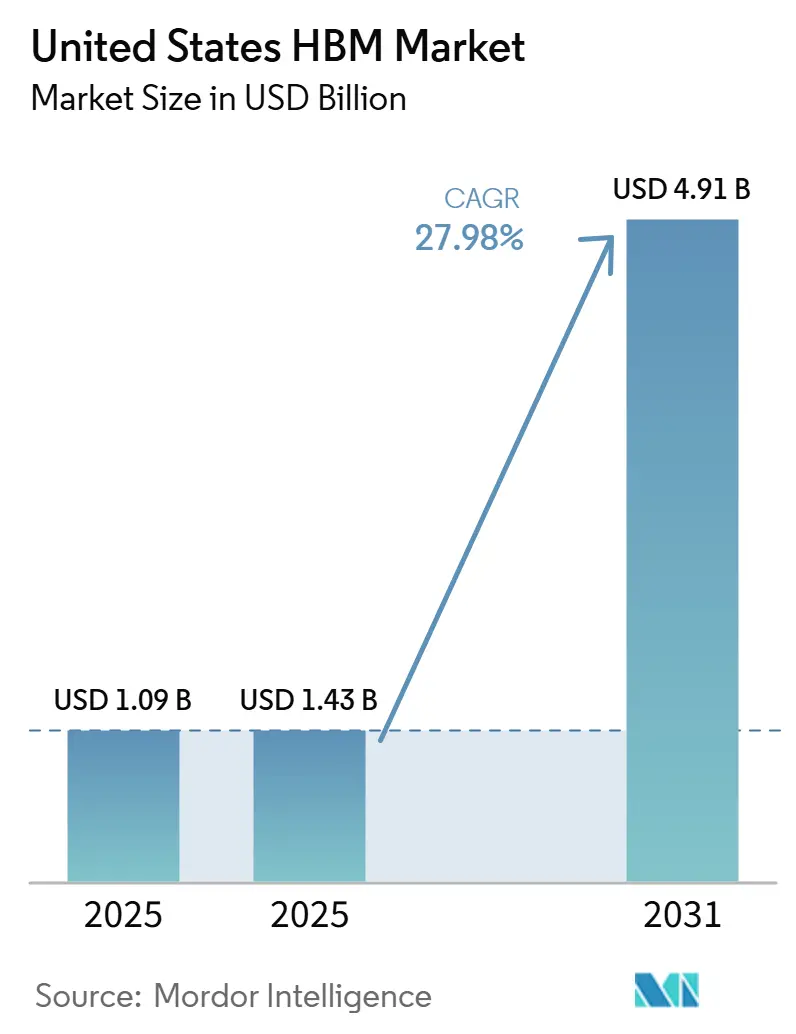

| Base Year Market Size (2025) | USD 1.09 Billion |

| Market Size (2026) | USD 1.43 Billion |

| Market Size (2031) | USD 4.91 Billion |

| Growth Rate (2026 - 2031) | 27.98% CAGR |

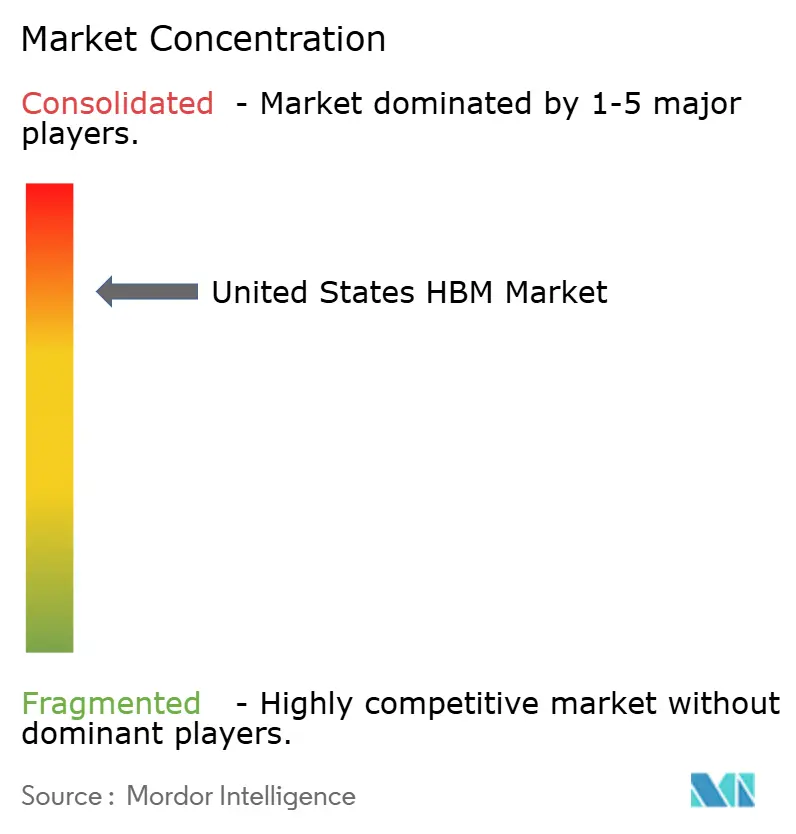

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States HBM Market Analysis by Mordor Intelligence

The United States HBM market size was valued at USD 1.09 billion in 2025 and estimated to grow from USD 1.43 billion in 2026 to reach USD 4.91 billion by 2031, at a CAGR of 27.98% during the forecast period (2026-2031). Growth is running well ahead of the broader DRAM cycle because AI accelerators now depend more on memory bandwidth than on raw capacity. The shift strengthened with the Blackwell platform cycle and is continuing as Vera Rubin enters production in 2026, which raises the number of advanced memory stacks needed in each accelerator and in each server rack. Supplier strategy is also changing because faster product qualification and tighter customer alignment now matter as much as wafer output. Supply remains concentrated at the memory level, which maintains pricing power and allocation discipline in a small group of suppliers, even though packaging and system integration involve a broader set of participants. Domestic investment programs are starting to reshape the long-term supply picture, although they do not remove the near-term pressure around advanced manufacturing and packaging capacity.

Key Report Takeaways

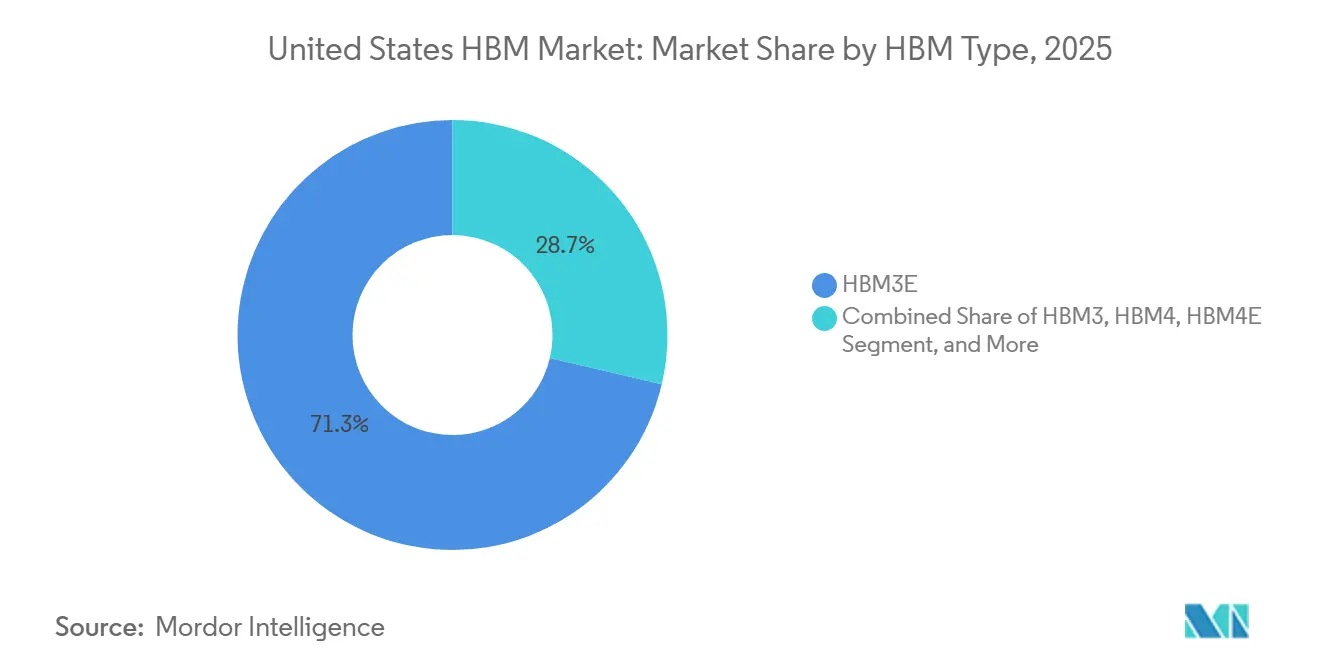

- By HBM type, HBM3E held 71.32% of the United States HBM market share in 2025, while HBM4E and later-generation HBM are projected to expand at a 28.94% CAGR through 2031.

- By technology node, advanced nodes below 1Z accounted for 49.94% of the United States HBM market size in 2025 and are projected to expand at a 28.69% CAGR through 2031.

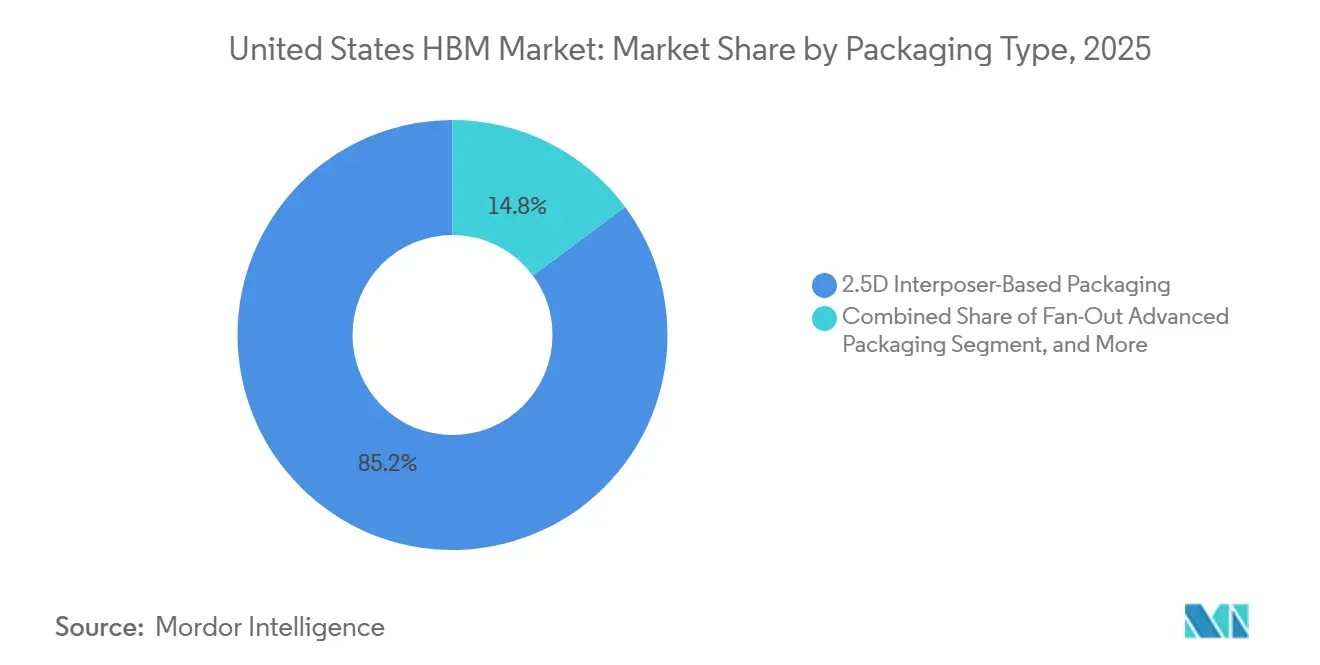

- By packaging type, 2.5D interposer-based packaging held 85.16% of the United States HBM market in 2025, while 3D stacking and hybrid-bonded integration are projected to grow at a 28.47% CAGR through 2031.

- By end-use industry, cloud service providers and hyperscalers held 44.73% of the United States HBM market in 2025, while internet platforms and AI model developers are projected to grow at a 29.11% CAGR through 2031.

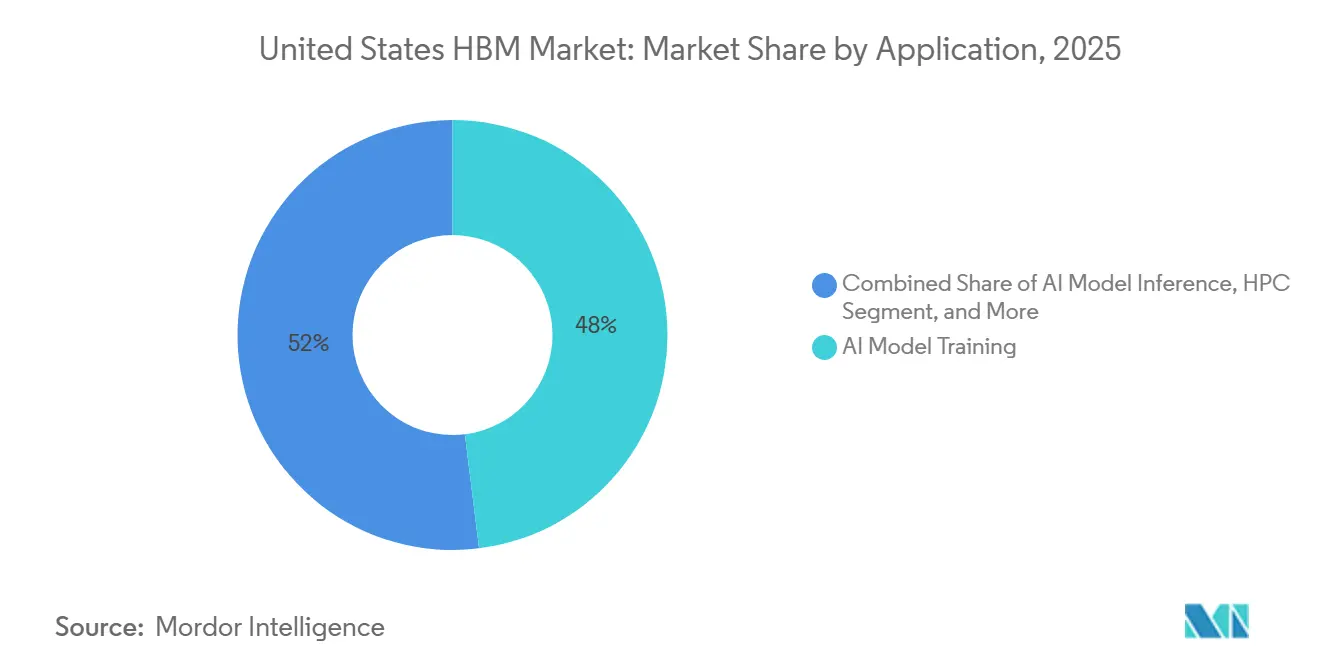

- By application, AI model training accounted for 48.03% of the United States HBM market size in 2025, while AI model inference is projected to advance at a 29.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States HBM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating AI Training and Inference Memory Intensity | +8.2% | National, with highest intensity in Northern Virginia, Silicon Valley, and Dallas–Fort Worth data center corridors | Short term (≤ 2 years) |

| Hyperscale GPU Cluster Expansion in United States Data Centers | +6.5% | National, concentrated in hyperscaler build-outs across Virginia, Oregon, Iowa, and Texas | Short term (≤ 2 years) |

| HBM Adoption in Advanced Packaging and Chiplet Architectures | +4.8% | Global supply chain with US demand pull, with packaging dependence centered in Taiwan-based interposer ecosystems | Medium term (2-4 years) |

| Domestic Memory Supply Chain Reshoring Incentives and CHIPS Act Support | +3.1% | National, with early-stage gains in Indiana, Idaho, New York, and Virginia | Long term (≥ 4 years) |

| HBM Demand Pull From Sovereign AI, Defense, and Secure Compute Programs | +2.3% | National, concentrated in defense and national laboratory compute clusters | Medium term (2-4 years) |

| HBM Qualification for Next-Generation Accelerators and Custom Silicon | +1.9% | National, with US hyperscaler custom ASIC programs as the primary demand node | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerating AI Training and Inference Memory Intensity

Per-accelerator HBM demand is rising faster than accelerator unit growth because each new platform uses more stacks and higher bandwidth per stack. NVIDIA stated that Vera Rubin ramped into full production in May 2026 and positioned the platform for agentic AI factories, which keeps memory bandwidth central to system design and deployment planning. Samsung said its commercial HBM4 reached 11.7 Gbps transfer speed and up to 3.3 TB/s per stack, which shows how memory roadmaps are being pushed to match more demanding AI workloads.[1]Samsung Semiconductor, “Samsung Electronics Begins Shipment of Industry-First HBM4E Samples,” Samsung Semiconductor Newsroom, news.samsungsemiconductor.com Micron entered high-volume HBM4 production for Vera Rubin, and AMD reported USD 16.6 billion in 2025 data center revenue, pointing to sustained demand for HBM-equipped compute platforms. Training clusters still consume large amounts of memory, but inference fleets add a steadier demand layer as they expand with live user traffic and service growth. That pattern supports the United States HBM market because memory content now rises with both new installations and ongoing platform refresh cycles.

Hyperscale GPU Cluster Expansion in United States Data Centers

Large AI data center build-outs keep pulling HBM volumes forward because accelerator deployment schedules are closely tied to memory availability. NVIDIA said Vera Rubin entered full production with 7 new chips across more than 350 supply chain partners in 30 countries, which signals the scale of systems moving toward deployment. Micron moved into high-volume HBM4 production for Vera Rubin in March 2026, and Samsung began mass production of commercial HBM4 in February 2026, both aligned with large customer rollouts. AMD’s 2025 data center revenue growth also points to a broader accelerator demand base, which matters because HBM demand follows platform adoption rather than stand-alone memory purchasing. As more buyers move from pilot clusters to production environments, supply allocations become harder to loosen and lead times remain sensitive. That shift gives the United States HBM market a broader and more durable demand base than a single procurement cycle would suggest.

HBM Adoption in Advanced Packaging and Chiplet Architectures

HBM adoption is now tied directly to advanced packaging choices because memory and logic must operate as a tightly integrated system in modern AI accelerators. Samsung’s HBM4 and HBM4E launches show that suppliers are lifting bandwidth and energy efficiency together, which is essential for dense accelerator packages with strict thermal and power limits. Micron’s 36 GB 12H HBM4 for Vera Rubin and SK hynix’s 12-layer HBM4 sample activity show that higher-layer designs are moving deeper into customer programs. IMEC found that 3D HBM-on-GPU stacking can push operating temperatures sharply higher without system-level cooling optimization, which explains why packaging now shapes both performance and reliability. In the United States HBM market, 2.5D interposer designs still lead current deployments because they remain the most established route for large AI packages. The move toward denser 3D and hybrid-bonded approaches will stay important over the medium term because bandwidth gains must come with better thermal control and better integration efficiency.

Domestic Memory Supply Chain Reshoring Incentives and CHIPS Act Support

Domestic policy support is starting to alter the long-run structure of the United States HBM market, even though it does not solve today’s supply tightness. NIST said SK hynix received up to USD 458 million in CHIPS direct funding for an HBM advanced packaging facility in West Lafayette, Indiana, tied to a total investment of USD 3.87 billion.[2]National Institute of Standards and Technology, “SK hynix, Indiana, West Lafayette,” CHIPS Program Office, nist.gov Micron said its domestic program totals USD 200 billion over 20 years and includes end-to-end HBM manufacturing, while CHIPS support spans facilities in Idaho, New York, and Virginia. These programs matter because future domestic capacity can improve supply assurance for buyers that value location, policy alignment, and security guardrails alongside price and performance. The build-out timeline is still long because SK hynix expects mass production in the second half of 2028, and Micron’s expansion is a multi-year manufacturing program rather than a short-cycle response. Over time, these investments should give the United States HBM market more domestic leverage in procurement and supplier negotiations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced Packaging Capacity Constraints Across CoWoS and Similar Flows | -4.5% | Global supply chain constraint, with the highest impact on US hyperscaler and custom ASIC programs reliant on qualified advanced packaging | Short term (≤ 2 years) |

| High Yield Loss Risk in Multi-Die, High-Stack HBM Manufacturing | -3.2% | Global, with yield risk concentrated at leading HBM production lines and demand impact felt most acutely in the United States | Medium term (2-4 years) |

| Thermal Management Limits in High Power Density AI Systems | -2.1% | National, most acute in high-density GPU clusters and secure compute installations | Medium term (2-4 years) |

| Heavy Concentration of Qualified Supply and Long Qualification Cycles | -1.6% | Global supply concentration with direct US demand implications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced Packaging Capacity Constraints Across CoWoS And Similar Flows

Advanced packaging remains a restraint because the United States demand still depends on a narrow set of qualified integration flows for frontier AI accelerators. NIST said SK hynix’s Indiana facility is expected to begin mass production only in the second half of 2028, meaning domestic relief will arrive after the current demand wave. Micron’s Idaho, New York, and Virginia plans are large, but they are part of a multi-year build-out rather than an immediate release of packaging capacity. This leaves the near-term United States HBM market exposed to schedule pressure whenever packaging availability and accelerator launch plans fall out of sync. The problem is structural because each new HBM generation also requires packaging validation and process tuning, not just more wafer output. Until more qualified capacity is in place, deployment timing will remain vulnerable even when end demand stays strong.

High Yield Loss Risk In Multi-Die, High-Stack HBM Manufacturing

Yield risk rises as more dies, more layers, and tighter tolerances are packed into each HBM unit. Samsung’s HBM4 and HBM4E launches show how quickly performance targets are advancing, but they also reflect the complexity of bringing new stack formats into sustained customer shipments. Micron’s 36 GB 12H HBM4 and SK hynix’s HBM4 development program push the same boundary, with tighter integration demands across memory, base die, and package design. Imec showed that 3D HBM-on-GPU architectures can reach 141.7°C before cooling co-optimization reduces temperatures to around 70.8°C, underscoring the link between thermal stress and manufacturing yield. Each generation, therefore, resets part of the learning curve, and early output can lag demand even when long-term roadmaps remain intact. That pattern moderates the speed at which new products can lift the United States HBM market through the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HBM Type: HBM3E Leads Near-Term Demand While HBM4 Moves Into Commercial Scale

HBM3E held 71.32% of the United States HBM market share in 2025, while HBM4E and later-generation HBM are projected to expand at a 28.94% CAGR through 2031. That lead came from the large procurement cycle tied to Blackwell-based systems, which made HBM3E the core memory choice for high-volume AI accelerator deployments. The generation delivered the bandwidth needed for the training-heavy build-out that defined the recent phase of the United States HBM market. Earlier generations, including HBM2E and HBM3, still served legacy HPC and professional visualization deployments where qualification cycles and installed platforms limited immediate migration. HBM4 entered meaningful commercial activity in early 2026 as suppliers shifted from development milestones to customer shipments.[3]Samsung Electronics Co., Ltd., “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung Global Newsroom, news.samsung.com

The fastest-growing part of this category is HBM4E and later-generation HBM, as customers now want higher throughput, greater capacity per stack, and stronger power efficiency within the same package footprint. Samsung said its commercial HBM4 reached up to 3.3 TB/s and improved power efficiency by 40% compared with HBM3E, giving the segment a clear performance case for future growth. Samsung also began shipping HBM4E samples in May 2026, with up to 3.6 TB/s bandwidth and 48 GB capacity, pushing the roadmap forward further that year. SK Hynix completed HBM4 development in September 2025, and Micron began high-volume HBM4 production for Vera Rubin in March 2026, confirming that the next cycle has moved from planning to execution. In the United States HBM industry, that change matters because demand growth now depends less on whether HBM4 arrives and more on how quickly suppliers can scale it across customer programs.

By Technology Node: Advanced Nodes Below 1Z Anchor Performance And Growth

Advanced nodes below 1Z commanded 49.94% of the United States HBM market size in 2025 and are projected to grow at a 28.69% CAGR through 2031. This is notable because the same node class is driving both current revenue and future growth, indicating that advanced process technology has already become a current requirement rather than a future option. The 1Z node underpinned the first HBM3E wave, while nodes below 1Z now support the shift to HBM4 and HBM4E products. SK hynix said its HBM4 uses the 1b nm process and the Advanced MR-MUF process, which ties next-generation HBM performance directly to more advanced manufacturing execution. Samsung said its commercial HBM4 combines a 4 nm logic base die with a 1c DRAM process, reinforcing the same-node trend seen with another leading supplier.

Advanced nodes matter because co-packaged memory must keep pace with faster AI accelerators, larger stack counts, and tighter power envelopes at the system level. Micron’s move into high-volume HBM4 production for Vera Rubin shows that below 1Z execution is now part of live commercial supply, not just a development benchmark. Legacy node families, including 1X, 1Y, and 1Z, still have demand in defense, research, and slower-qualification environments where continuity matters as much as peak performance. Those older nodes remain relevant when program lifecycles are long, and platform migration is managed cautiously. Even so, advanced nodes below 1Z accounted for 49.94% of the United States HBM market in 2025, as the United States HBM market now rewards bandwidth per watt and integration efficiency over other technical trade-offs.

By Packaging Type: 2.5D Interposer Leads Today While 3D Integration Gains Momentum

2.5D interposer-based packaging held 85.16% of the United States HBM market in 2025, while 3D stacking and hybrid-bonded integration are projected to grow at a 28.47% CAGR through 2031. The current lead reflects the maturity and manufacturing scale of interposer-based integration for large AI processors. This packaging route places HBM close to the compute die and supports the very wide interfaces that distinguish HBM from standard DRAM arrangements. In the United States HBM market, 2.5D remains the preferred format for most present deployments because it balances performance, manufacturability, and known qualification paths. Fan-out packaging holds the remaining share and is used mainly where cost, form factor, or deployment conditions do not support the full interposer route.

The faster-growing path is 3D stacking and hybrid-bonded integration, as customers seek higher bandwidth density without a larger lateral package footprint. SK hynix’s 12-layer HBM4 sample work and its iHBM thermal solution show that the company is pushing both stack complexity and cooling support in parallel. Samsung’s HBM4E sample shipments add another signal that denser and faster packaging paths are moving toward commercial relevance. Imec’s thermal work also shows why packaging will keep shaping the next phase of the United States HBM industry, because higher density must be matched by stronger system-level cooling and design control. Over the forecast period, the balance should shift gradually as customers pursue tighter integration without giving up reliability.

By End Use Industry: Hyperscalers Lead Demand While Internet Platforms Expand Faster

Cloud service providers and hyperscalers represented 44.73% of the United States HBM market in 2025, while internet platforms and AI model developers are projected to grow at a 29.11% CAGR through 2031. Hyperscalers lead because they secure supply early, influence platform qualification, and commit capital at a scale that smaller buyers cannot easily match. Their HBM demand is usually embedded in GPU and ASIC system procurement rather than in separate memory contracts, which keeps the relationship between compute platforms and memory supply tightly linked. NVIDIA said Vera Rubin entered full production in May 2026, and that supports continued HBM pull from large cloud deployments tied to next-generation AI infrastructure. In the United States HBM industry, the buying structure keeps the largest cloud customers close to the front of allocation decisions.

Internet platforms and AI model developers are growing faster because training and inference demand is spreading beyond the earliest hyperscaler-led wave. AMD reported USD 16.6 billion in 2025 data center revenue, pointing to a broader base of accelerator demand across the ecosystem and supporting wider buyer expansion. Government, defense, research, and academic institutions remain a persistent demand segment, though security requirements and long procurement cycles can constrain access to leading suppliers. Enterprise data centers and telecommunications operators add another layer of demand as inference workloads move closer to on-premises environments and network-side processing. This wider customer mix supports the United States HBM market because growth is becoming less dependent on a single buyer group.

By Application: AI Training Holds The Largest Share While Inference Gains Scale

AI model training accounted for 48.03% of the United States HBM market in 2025, while AI model inference is projected to grow at a 29.04% CAGR through 2031. Training led by hyperscalers spent the last several years building large GPU clusters designed to process increasingly large models at high throughput. Those workloads favor large HBM stack counts and sustained bandwidth across long compute runs, which kept training at the center of recent accelerator deployment plans. The result was a training-heavy demand pattern across the United States HBM market during the earlier stage of the current AI expansion. HPC and scientific computing continued to hold a stable place because HBM-equipped systems remain central to simulation, research, and national laboratory workloads.

Inference is growing faster because large models are moving from development into live services, and that change multiplies the number of deployed endpoints that need fast memory access. NVIDIA said Vera Rubin is designed for agentic AI factories and offers 3.5x training and 5x inference performance versus Blackwell, supporting the expected expansion of inference-oriented HBM demand. The distinction between training and inference matters because training values prioritize sustained throughput, while inference prioritizes bandwidth and latency under live service conditions. That difference is already influencing how suppliers position next-generation memory products within customer programs. As production AI becomes more distributed across applications and service layers, inference should continue to play a larger role in the United States HBM market.

Geography Analysis

The United States HBM market was valued at USD 1.09 billion in 2025 and is forecast to reach USD 4.91 billion by 2031 at a 27.98% CAGR, which keeps the country at the center of global HBM demand planning. That demand base is tied to the world’s highest concentration of large GPU clusters, foundation model training programs, and AI service deployments. The growth outlook keeps the United States HBM market near the front of supplier allocation, roadmap timing, and product qualification decisions. NVIDIA’s move to full Vera Rubin production, combined with HBM4 ramps at Samsung, Micron, and SK hynix, shows how closely supplier commercialization now tracks AI deployment needs linked to the United States. CHIPS-backed investment is also beginning to shift the country from a pure demand center toward a future supply participant through projects in Indiana, Idaho, New York, and Virginia. [4]National Institute of Standards and Technology, “Micron, Idaho, Boise,” CHIPS Program Office, nist.gov

Within the country, HBM demand is concentrated in the Northern Virginia and Washington, D.C. corridor, the San Francisco Bay Area and Silicon Valley, and the Dallas-Fort Worth and Phoenix metro areas. These clusters combine procurement leadership, hyperscale deployment, engineering talent, and access to power and data center real estate, making them the primary operating centers for the United States HBM market. Indiana is becoming a new memory-linked corridor through SK hynix’s West Lafayette project and its Purdue partnership, which adds a future packaging and research anchor in the Midwest. Defense and national laboratory locations add a smaller but specialized demand node where secure compute and long qualification cycles shape purchasing behavior.

The structural supply map serving the United States HBM market is still defined by geographic separation between wafer production, advanced integration, and final deployment. South Korean suppliers remain central to HBM wafer supply, Taiwan remains essential in the advanced integration flow, and United States sites remain the main end demand destination for large-scale AI systems. That structure creates several points of risk in logistics, policy, and scheduling because a delay in one layer can slow activity across the whole chain. Micron said it aims to produce 40% of its DRAM in the United States within two decades, which gives the country the clearest long-term localization target among current participants. CHIPS funding and related guardrails also raise the strategic value of domestic capacity, especially for customers that place weight on supply security and policy alignment. The geographic profile should therefore broaden over time, but the largest part of the United States HBM market will remain tied to existing data center and accelerator deployment clusters through most of the forecast period.

Competitive Landscape

The United States HBM market remains structurally oligopolistic at the supply level, as SK hynix, Samsung Electronics, and Micron Technology account for all production volume. SK hynix strengthened its position by completing HBM4 development in September 2025 and preparing for mass production ahead of the 2026 ramp phase. Samsung regained momentum by beginning mass production of commercial HBM4 in February 2026 and shipping HBM4E samples in May 2026, thereby improving its standing on the next-generation roadmap. Micron entered high-volume HBM4 production for NVIDIA's Vera Rubin in March 2026, reinforcing its role as the only United States-headquartered HBM supplier with a live next-generation program. Together, these moves keep the qualified supplier base narrow even though adjacent packaging and integration activities involve more companies.

Competition is now shaped as much by strategic partnerships and localization plans as by pure process technology. NVIDIA and SK hynix announced a multiyear technology partnership in June 2026 to co-develop memory for Vera Rubin systems, Vera CPUs, RTX Spark PCs, and Jetson Thor platforms, which deepens customer-supplier alignment beyond a single product cycle. Micron’s USD 200 billion domestic investment plan, backed by CHIPS support, is another major strategic move because it aims to pair long-term local manufacturing scale with end-to-end HBM capability. SK Hynix’s Indiana advanced packaging project adds a third clear move, linking future United States production with research and workforce development through Purdue University.

The next phase of rivalry will depend on which supplier can scale new stack formats quickly while meeting thermal and power limits. Samsung is using HBM4E sample shipments to demonstrate that it can transition from recovery to roadmap leadership in denser, faster parts. Micron is using early HBM4 volume production for Vera Rubin to strengthen its position with United States customers that value both performance and domestic alignment. SK hynix is combining early HBM4 development leadership with packaging and thermal work, including its iHBM solution, to support future high-density designs. Because only a few suppliers can meet these frontier requirements at scale, the United States HBM market remains concentrated even though downstream integration work is less tightly held.

United States HBM Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: NVIDIA and SK hynix announced a multiyear technology partnership to co-develop memory for NVIDIA's Vera Rubin AI supercomputers, Vera CPUs, RTX Spark PCs, and Jetson Thor robotic computing platforms, with SK hynix deploying NVIDIA CUDA-X libraries and NVIDIA PhysicsNeMo framework to accelerate semiconductor simulations and 3D factory digital twins, per NVIDIA's investor relations disclosure of June 2026. The agreement expands the HBM supply relationship beyond AI data centers into personal AI and physical AI markets.

- May 2026: NVIDIA announced that Vera Rubin entered full production on May 31, 2026, at GTC Taipei, with 7 new chips in full production across 350+ supply chain partners in 30 countries. The platform delivers 3.5x training and 5x inference performance versus Blackwell and is designed for agentic AI factory deployments, per NVIDIA's official GTC press release.

- May 2026: Samsung Electronics began shipping the industry's first 12-layer HBM4E samples to major customers on May 29, 2026, achieving 14 Gbps pin speed, scalable to 16 Gbps, 3.6 TB/s bandwidth per stack, and 48 GB capacity, representing a 20% bandwidth increase over HBM4 and a 16% energy efficiency improvement, per Samsung Semiconductor's global newsroom disclosure.

- March 2026: Micron Technology entered high-volume production of HBM4 36 GB 12H for NVIDIA Vera Rubin at GTC March 2026, achieving over 2.8 TB/s bandwidth and more than 20% power efficiency improvement over HBM3E, and simultaneously announced the industry's first PCIe Gen6 SSD in high-volume production, per Micron investor relations.

- February 2026: Samsung Electronics began mass production of the industry's first commercial HBM4 on February 12, 2026, shipping products with an 11.7 Gbps transfer speed, a maximum bandwidth per stack of 3.3 TB/s, and up to 36 GB of capacity, using a 4 nm logic base die and a 1c DRAM process. Samsung anticipates HBM sales will more than triple in 2026 compared with 2025, per Samsung Global Newsroom.

United States HBM Market Report Scope

The United States HBM Market Report is Segmented by HBM Type (HBM2E and Earlier, HBM3, HBM3E, HBM4, and HBM4E and Later Generation HBM), Technology Node (1X and Above, 1Y, 1Z, and Advanced Nodes Below 1Z), End Use Industry (Cloud Service Providers and Hyperscalers, Internet Platforms and AI Model Developers, Government, Defense, Research, and Academic Institutions, Enterprise Data Centers, Telecommunications Operators and Network Equipment Providers, Other Enterprise Verticals), Application (AI Model Training, AI Model Inference, HPC and Scientific Computing, Professional Graphics, Rendering, and Visualization, Network and Telecom Processing, Other High-Bandwidth Compute Workloads), and Packaging Type (2.5D Interposer-Based Packaging, 3D Stacking, Fan-Out Advanced Packaging). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2E and Earlier Generations |

| HBM3 |

| HBM3E |

| HBM4 |

| HBM4E and Later-Generation HBM |

| 1X And Above Legacy Nodes |

| 1Y Node |

| 1Z Node |

| Advanced Nodes Below 1Z |

| 2.5D Interposer-Based Packaging |

| 3D Stacking |

| Fan-Out Advanced Packaging |

| Cloud Service Providers and Hyperscalers |

| Internet Platforms and AI Model Developers |

| Government, Defense, Research, and Academic Institutions |

| Enterprise Data Centers |

| Telecommunications Operators and Network Equipment Providers |

| Other Enterprise Verticals |

| AI Model Training |

| AI Model Inference |

| HPC and Scientific Computing |

| Professional Graphics, Rendering, and Visualization |

| Network and Telecom Processing |

| Other High-Bandwidth Compute Workloads |

| By HBM Type | HBM2E and Earlier Generations |

| HBM3 | |

| HBM3E | |

| HBM4 | |

| HBM4E and Later-Generation HBM | |

| By Technology Node | 1X And Above Legacy Nodes |

| 1Y Node | |

| 1Z Node | |

| Advanced Nodes Below 1Z | |

| By Packaging Type | 2.5D Interposer-Based Packaging |

| 3D Stacking | |

| Fan-Out Advanced Packaging | |

| By End Use Industry | Cloud Service Providers and Hyperscalers |

| Internet Platforms and AI Model Developers | |

| Government, Defense, Research, and Academic Institutions | |

| Enterprise Data Centers | |

| Telecommunications Operators and Network Equipment Providers | |

| Other Enterprise Verticals | |

| By Application | AI Model Training |

| AI Model Inference | |

| HPC and Scientific Computing | |

| Professional Graphics, Rendering, and Visualization | |

| Network and Telecom Processing | |

| Other High-Bandwidth Compute Workloads |

Key Questions Answered in the Report

What is the size of the United States HBM market?

The United States HBM market reached USD 1.09 billion in 2025, is valued at USD 1.43 billion in 2026, and is forecast to reach USD 4.91 billion by 2031 at a 27.98% CAGR.

Which HBM type leads current demand in the United States?

HBM3E led with 71.32% share in 2025 because it was the main memory generation used in the recent AI accelerator build-out.

Which application is growing fastest for HBM in the United States?

AI model inference is the fastest-growing application, with a projected 29.04% CAGR through 2031 as large models move into live production environments.

Why are hyperscalers so important in this space?

Cloud service providers and hyperscalers held 44.73% of demand in 2025 because they secure supply early and buy HBM through large GPU and ASIC system programs.

What is driving the move from HBM3E to HBM4 and HBM4E?

Customers want more bandwidth, more stack capacity, and better power efficiency, which is why HBM4 and HBM4E are gaining attention in 2026 product ramps.

Page last updated on: