United States Grain Storage Silos Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 310.10 Million |

| Market Size (2031) | USD 380.90 Million |

| Growth Rate (2026 - 2031) | 4.20% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Grain Storage Silos Market Analysis by Mordor Intelligence

The United States grain storage silos market size is valued at USD 310.1 million in 2026 and is projected to reach USD 380.9 million in 2031, advancing at a 4.2% CAGR over the forecast period. Structural demand from farm consolidation, biofuel expansion, and shuttle-train terminals supports steady growth, while steel-price volatility and rising safety-compliance costs temper the pace. Federal cost-share incentives and rising labor expenses are nudging capital away from small on-farm bins toward large commercial complexes equipped with predictive-maintenance sensors that reduce spoilage losses and unlock insurance discounts [1]Source: USDA National Agricultural Statistics Service, “Grain Stocks," usda.gov. Composite and fiberglass designs are emerging as resilient alternatives to steel, especially in humid or coastal zones where corrosion undercuts service life. Meanwhile, automation suppliers are generating high-margin retrofit revenue by layering telemetry and analytics onto the installed base of manual silos, creating a data-driven ecosystem that reshapes aftermarket competition.

Key Report Takeaways

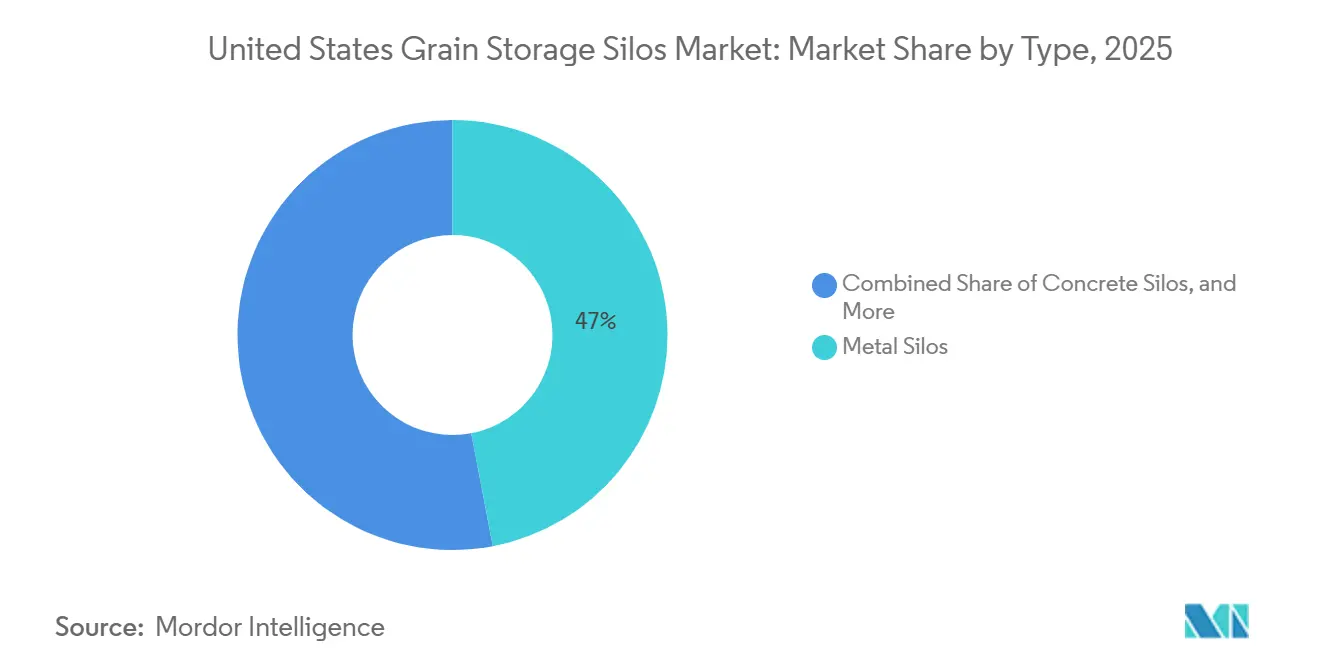

- By type, metal silos led with 47% of the United States grain storage silos market share in 2025, while composite/fiberglass silos are forecast to advance at a 7.5% CAGR through 2031.

- By product, flat-bottom silos accounted for 42.5% of revenue in 2025, whereas hopper-bottom designs are poised to grow at an 8.4% CAGR through 2031.

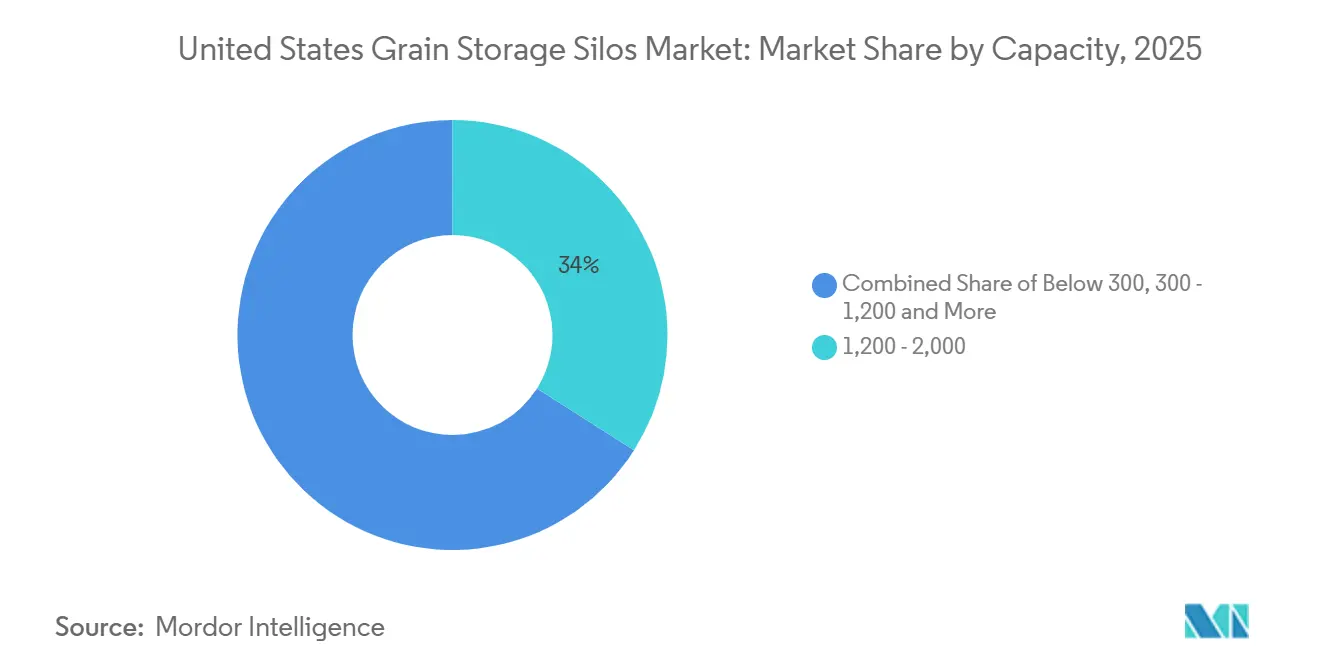

- By capacity, the 1,200–2,000 metric-ton band accounted for 34% of the United States grain storage silos market size in 2025, but the above-2,000 metric-ton segment is projected to expand at a 6.9% CAGR through 2031.

- By automation level, manual systems held 55% revenue share in 2025, while fully automated smart silos are projected to post a 9.2% CAGR to 2031.

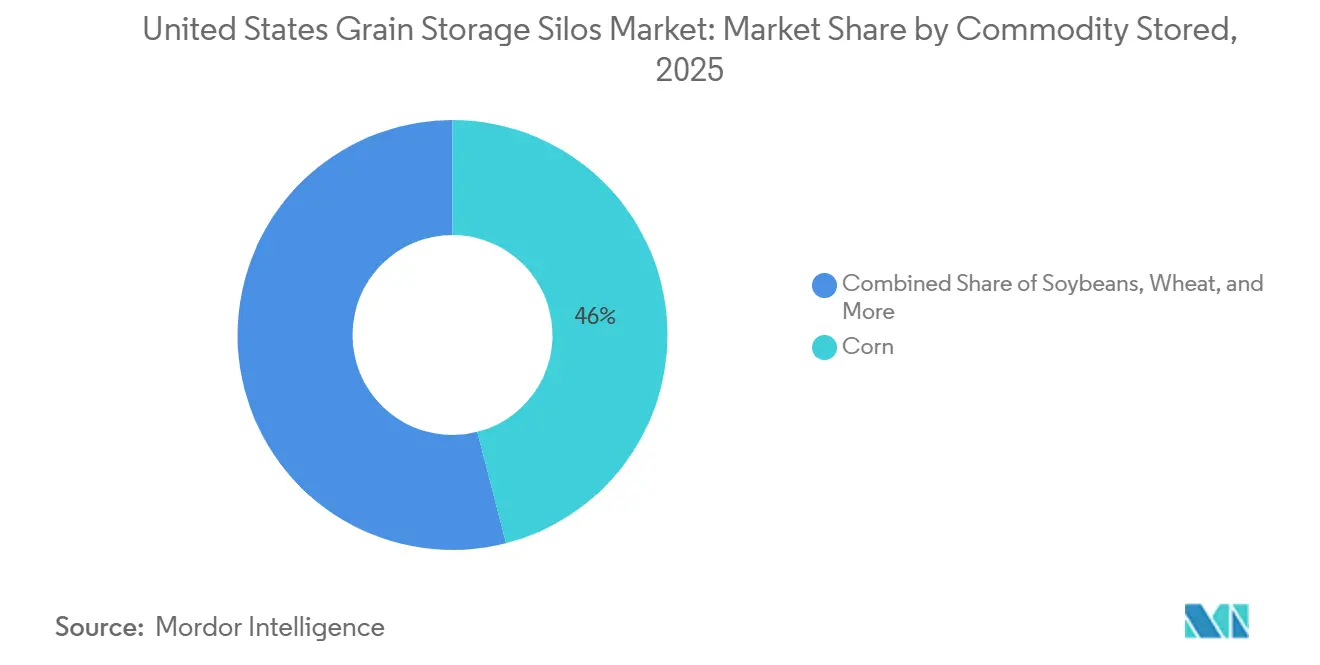

- By commodity, corn storage accounted for 46% of demand in 2025, yet rice and sorghum storage are forecast to grow at a 7.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on grain storage silos market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Grain Storage Silos Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for large-capacity commercial grain storage | +1.20% | Midwest and South | Medium term (2-4 years) |

| Volatility in farmgate prices incentivizing on-farm storage | +0.90% | National | Short term (≤ 2 years) |

| Federal cost-share programs for silo modernization | +0.70% | National | Medium term (2-4 years) |

| Midwest biofuel expansion driving corn storage additions | +0.80% | Midwest | Long term (≥ 4 years) |

| AI-driven predictive maintenance unlocking insurance discounts | +0.40% | National | Long term (≥ 4 years) |

| State-level carbon-credit schemes favor oxygen-limiting silos | +0.30% | California and Midwest pilots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for large-capacity commercial grain storage

Shuttle-train terminals and export-gateway elevators are increasingly utilizing silo complexes with capacities exceeding 50,000 metric tons to enhance rail freight efficiency and reduce per-unit handling costs [2]Source: USDA National Agricultural Statistics Service, “Grain Stocks,” usda.gov. Large-scale, single-structure projects, such as the 2021 Golden Grain Energy installation featuring a 2.2-million-bushel tank, have demonstrated significant land-use efficiency and lower operating costs compared to multi-bin layouts. This trend toward mega-scale storage benefits manufacturers with robust in-house structural engineering expertise and access to high-volume steel-forming capabilities, strengthening scale-driven competitive advantages within the commercial grain storage market.

Volatility in farmgate prices incentivizing on-farm storage

Basis spreads widened to USD 14.9 per metric ton during the 2024 harvest, prompting farmers to store corn and defer sales until local elevators boosted bids [3]Source: USDA Agricultural Marketing Service, “Grain Transportation Report,” ams.usda.gov. On-farm corn inventories climbed increasing as growers treated bins as price-risk tools. Producers with 5,000-10,000 bushels of storage captured seasonal lifts that paid for new capacity within four marketing cycles. The upside is offset by spoilage risk for operators without aeration or moisture controls, reinforcing demand for turnkey packages bundling fans, sensors, and remote monitoring.

Federal cost-share programs for silo modernization

The United States Department of Agriculture (USDA) Environmental Quality Incentives Program (EQIP) reimburses 50-75% of eligible upgrade costs, accelerating adoption of sealed-bin standards, variable-speed aeration, and moisture monitoring. Nebraska and Kansas report high uptake, whereas states with administrative backlogs see 12-18-month reimbursement lags. Manufacturers now bundle EQIP-compliant packages with documentation templates, lowering paperwork hurdles and expanding the pool of qualified applicants.

State-level carbon-credit schemes favor oxygen-limiting silos

California’s FARMER guidelines allocate funding for hermetic silos that curb fumigant use and grain respiration emissions, translating into 3-5% annual operating-cost offsets via carbon credits [4]Source: California Air Resources Board, “2024 FARMER Guidelines,” arb.ca.gov. Adoption is strongest among specialty-grain handlers and organic producers, where sustainability-linked pricing and certification premiums help offset higher initial investments. Despite a 20–30% capital expenditure premium, these operators are well-positioned to achieve returns through premium market access and compliance-driven incentives. Broader adoption depends on expanding carbon credit frameworks, incentive programs across more states, and standardizing verification mechanisms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety hazards from confined-space entry and explosions | -0.60% | National | Short term (≤ 2 years) |

| High steel-price volatility inflating capital costs | -0.80% | National | Short term (≤ 2 years) |

| Municipal height limits near railheads | -0.30% | Northeast and Midwest towns | Medium term (2-4 years) |

| Cyber-vulnerability of IoT-enabled silo controls | -0.20% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Safety hazards from confined-space entry and explosions

The Occupational Safety and Health Administration (OSHA) cited a Missouri cooperative in October 2024 after a fatal grain engulfment exposed gaps in rescue equipment and training [5]Source: OSHA, “Missouri Grain Engulfment Citation,” osha.gov. Purdue University’s 2024 injury report chronicled multiple preventable deaths tied to bridged grain and unlocked augers. Compliance upgrades can exceed USD 15,000 per bin, creating financial strain for small operators and shaping purchasing decisions toward designs that integrate retrieval anchors and dust-collection features.

High steel-price volatility inflating capital costs

The Producer Price Index for fabricated structural steel more than doubled from 2020 to mid-2022 before partially retreating, adding USD 25,000-35,000 to a typical 100,000-bushel bin and stretching payback periods to 12 years [6]Source: Federal Reserve Bank of St. Louis, “PPI Steel Structures,” fred.stlouisfed.org. Fabricators are utilizing pass-through clauses and hedging strategies to mitigate input cost risks. However, smaller manufacturers with limited financial flexibility continue to experience prolonged margin pressures. This situation is driving market consolidation, as factors such as scale advantages, procurement leverage, and financial resilience emerge as critical competitive differentiators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Metal Silos Dominate but Composites Gain Traction

Metal silos accounted for 47% of the United States grain storage silos market share in 2025, supported by established fabrication networks, standardized designs, and competitive pricing at scale. Their widespread use reflects installer familiarity and availability across both on-farm and commercial applications. Composite and fiberglass silos are anticipated to grow at a 7.5% CAGR through 2031, driven by their corrosion resistance and lightweight construction, which reduce foundation and installation costs. Concrete silos continue to cater to niche port and terminal applications requiring fire resistance and extended service life.

Steel remains the market leader due to standardized specifications and the availability of multivendor parts, which facilitate maintenance and upgrades. However, steel price volatility and concerns over corrosion are gradually shifting focus toward materials with lower life-cycle costs. Composite suppliers are enhancing resin formulations to improve impact resistance and ultraviolet stability. Broader adoption of composite silos will depend on achieving further cost reductions and expanding nationwide dealer and service networks to compete with the established steel silo distribution infrastructure.

By Product: Flat-Bottom Silos Lead but Hopper-Bottom Designs Surge

Flat-bottom bins accounted for 42.5% of revenue in 2025, reflecting their ability to maximize storage density for bulk commodities such as corn and soybeans. Their dominance is attributed to lower upfront capital costs and compatibility with existing sweep-auger infrastructure across on-farm and commercial facilities. However, hopper-bottom designs represent the fastest-growing segment of the United States grain storage silos market, projected to grow at an 8.4% CAGR. This growth is driven by faster discharge rates that reduce labor requirements, contamination risks, and operational downtime.

Despite the increasing adoption of hopper-bottom systems, flat-bottom silos will remain widely used for large-volume grain inventories, particularly where existing handling systems justify their economic advantages. Hopper-bottom silos typically command a 15–25% price premium, but this is increasingly offset by benefits such as reduced manual labor, faster cleanout cycles, and improved hygiene. These features are especially valued by feed mills, seed handlers, and specialty-grain operators, where traceability, cleanliness, and rapid inventory turnover are critical operational requirements.

By Capacity: 1.200-2000 Metric Tons Dominate but Above 2000 Metric Tons-Silos Drive Growth

Bins sized 1,200-2,000 metric tons captured 34% of the United States grain storage silos market size in 2025, aligning with typical large-farm and small-elevator requirements [7]Source: USDA Agricultural Marketing Service, “Grain Transportation Report,” ams.usda.gov. Installations with capacities above 2,000 metric tons, anticipated to grow at a 6.9% CAGR, are becoming integral to shuttle-train terminals capable of loading 110-car unit trains within shorter timeframes. These large-scale silo complexes provide notable logistics efficiencies by minimizing dwell time and facilitating high-throughput grain movement. Consequently, they can reduce per-bushel rail freight costs by up to 40%, enhancing their competitiveness and gradually replacing mid-sized country elevators that lack similar scale or rail connectivity.

Bins with capacities below 300 metric tons continue to address niche needs, particularly for seed storage and specialty crops where segregation and traceability are essential. However, growth in this segment remains constrained as industry consolidation reduces the number of small, independent producers. The 300–1,200-metric-ton capacity range faces increasing pressure from both flexible on-farm storage solutions and large unit-train terminals. Suppliers in this mid-range segment are compelled to differentiate through improved service offerings, financing options, and aftermarket support rather than relying solely on scale.

By Automation Level: Manual Systems Prevail but Smart Silos Accelerate

Manual silos accounted for 55% of revenue in 2025, reflecting the extensive installed base of legacy storage assets across the United States. These assets continue to depreciate slowly while remaining operationally viable. Many operators delay upgrades due to the long service life of existing infrastructure. In contrast, fully automated smart silos are projected to grow at a 9.2% CAGR through 2031, driven by benefits such as insurance premium reductions, lower spoilage losses, and operational efficiencies. These efficiencies can provide a payback period of three to five years for large installations, such as 500,000-bushel sites. Semi-automated systems are increasingly adopted as an intermediate solution, enabling gradual performance improvements without requiring a complete digital transformation.

Retrofit sensor and automation packages, offered by suppliers such as AGI (Ag Growth International Inc.), are targeting the extensive manual silo base by facilitating incremental upgrades instead of full asset replacement. These solutions typically include temperature and moisture sensors, cloud-based dashboards, and predictive analytics to support proactive grain management. Adoption is particularly appealing in regions with volatile moisture and weather conditions, where real-time monitoring and automated aeration adjustments provide immediate quality preservation benefits and measurable economic returns.

By Commodity Stored: Corn Storage Dominates but Specialty Grains Grow Faster

Corn accounted for 46% of demand in 2025, underscoring its dominant role in the United States grain production and its significance as a feedstock for ethanol and livestock feed, particularly in the Midwest. This strong position is supported by a well-established storage and handling infrastructure tailored to corn logistics. In comparison, rice and sorghum storage, projected to grow at a 7.8% CAGR, is benefiting from acreage expansion in states such as Texas and Oklahoma, alongside rising export demand for identity-preserved grains. These specialty crops often achieve pricing premiums that compensate for the higher per-bushel storage costs associated with segregation, quality preservation, and traceability.

Corn storage infrastructure is highly developed, limiting growth opportunities primarily to yield improvements and incremental increases in biofuel demand rather than significant capacity expansion. On the other hand, specialty-grain storage is driving new investments, as these crops require purpose-built silos with advanced contamination controls and dedicated material-handling systems. Manufacturers are increasingly incorporating specialized coatings, sealed transfer points, and separate conveying lines to meet organic and non-GMO (Genetically Modified Organisms) certification standards, creating distinct opportunities in higher-value storage projects.

Geography Analysis

The Midwestern United States holds the largest share of the nation’s commercial grain storage capacity, driven by robust agricultural output and a well-established rail and biofuel infrastructure. States such as Illinois, Iowa, Kansas, Nebraska, and Minnesota experience consistent demand for large-scale storage, supported by investments in shuttle-train logistics and ethanol production. Additionally, major agribusiness-led biofuel complexes contribute to sustained requirements for adjacent grain storage capacity in the United States grain storage silos market.

The Southern United States is experiencing growth from a smaller installed base, driven by increased rice and sorghum cultivation. Periodic production surges have highlighted storage shortages, prompting greater reliance on temporary solutions and boosting demand for permanent on-farm bins. The limited presence of large commercial terminals in this region creates opportunities for suppliers offering integrated, aerated storage systems that perform effectively in high-humidity environments.

The Western United States faces structural challenges, including water scarcity and zoning regulations that restrict silo height. Environmental incentive programs in states like California are promoting the adoption of sealed storage systems and electrically powered material-handling equipment to reduce emissions. Meanwhile, the Northeastern United States remains a relatively small market, primarily centered around import terminals and feed mills. Storage development in this region is constrained by proximity to residential areas and stricter land-use regulations.

Competitive Landscape

The United States grain storage silos market is moderately concentrated, with the top five players including Ag Growth International Inc., CTB Inc. (Brock Grain Systems), Sukup Manufacturing Co., AGCO Corporation, and Superior Grain Equipment LLC occupying major share. New entrants focus on smooth-wall hopper designs tailored to specialty grains, while regional steel fabricators differentiate by rapidly mobilizing field crews. Raw-material hedging, safety certification depth, and aftermarket service are emerging as key competitive levers in a market where project scale, rather than product novelty, often dictates supplier selection.

Emerging disruptors include concrete silo specialists such as Hoffmann Inc. and CST Industries, which are capturing market share in the super-sized segment above 50,001 metric tons by offering turnkey engineering, procurement, and construction contracts that bundle foundation work, slip-form concrete placement, and automated grain handling systems into fixed-price packages, thereby reducing project risk for operators.

Technology adoption is accelerating, with manufacturers integrating predictive maintenance algorithms, remote aeration control, and blockchain-based grain traceability into new silo designs to differentiate offerings and capture premium pricing from operators serving identity-preserved and organic supply chains.

United States Grain Storage Silos Industry Leaders

-

Ag Growth International Inc.

-

CTB Inc. (Brock Grain Systems)

-

Sukup Manufacturing Co.

-

AGCO Corporation

-

Superior Grain Equipment LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Sukup Manufacturing Co. introduced its Synk smart grain management system at the Farm Progress Show. This system features IoT-enabled monitoring and automation, showcasing the increasing adoption of smart technologies in the U.S. grain storage silos market.

- December 2023: Sukup Manufacturing Co. announces its acquisition of Ramco Innovations, a leading automation distributor in the Midwest. The strategic partnership brings together the expertise and resources of the two industry leaders. Sheffield-based Sukup is an innovator in reliable grain storage, drying, and handling solutions. That reputation for quality and reliability, combined with Ramco's deep understanding of automation technologies, will create a collaboration that drives innovation and enhances customer experiences in the industrial sector.

United States Grain Storage Silos Market Report Scope

Grain storage silos are large, specialized structures, typically cylindrical and made of metal or concrete, used to store bulk quantities of grain and other agricultural products. The United States Grain Storage Silos Market Report is Segmented by Type (Steel Silos, Metal Silos, and Other Silos) and by Product (Flat-Bottom Silos, Hopper Bottom Silos, Feed Hoppers, and Farm Silos). The Market Forecasts are Provided in Terms of Value (USD).

| Metal Silos |

| Concrete Silos |

| Composite/Fiber Glass Silos |

| Flat-Bottom Silos |

| Hopper-Bottom Silos |

| Other Silos |

| Below 300 |

| 300 - 1,200 |

| 1,200 - 2,000 |

| Above 2,000 |

| Manual |

| Semi-Automated |

| Fully Automated (Smart Silos) |

| Corn |

| Soybeans |

| Wheat |

| Rice and Sorghum |

| Other Grain Silos |

| By Type | Metal Silos |

| Concrete Silos | |

| Composite/Fiber Glass Silos | |

| By Product | Flat-Bottom Silos |

| Hopper-Bottom Silos | |

| Other Silos | |

| By Capacity (Metric Tons) | Below 300 |

| 300 - 1,200 | |

| 1,200 - 2,000 | |

| Above 2,000 | |

| By Automation Level | Manual |

| Semi-Automated | |

| Fully Automated (Smart Silos) | |

| By Commodity Stored | Corn |

| Soybeans | |

| Wheat | |

| Rice and Sorghum | |

| Other Grain Silos |

Key Questions Answered in the Report

What is the current value of the United States grain storage silos market?

The market stands at USD 310.1 million in 2026 and is projected to reach USD 380.9 million in 2031.

Which silo type holds the largest share?

Metal silos accounted for 47% of 2025 revenue driven by its competitive pricing.

Which product segment is growing the fastest?

Hopper-bottom silos are projected to grow at an 8.4% CAGR through 2031 due to rapid discharge and lower labor needs.

What role does automation play in new projects?

Fully automated smart silos, although holding a smaller base, are forecast to grow at 9.2% CAGR as sensors cut spoilage and earn insurance discounts.

Page last updated on: