United States Facial Injectables Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

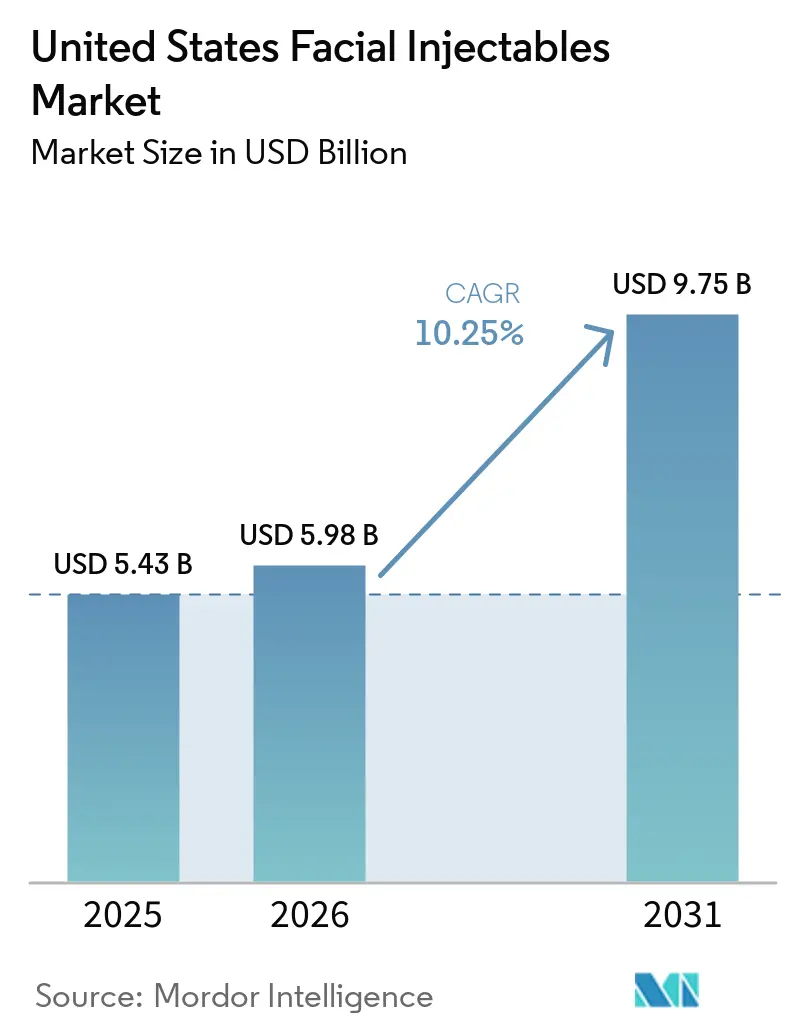

| Base Year Market Size (2025) | USD 5.43 Billion |

| Market Size (2026) | USD 5.98 Billion |

| Market Size (2031) | USD 9.75 Billion |

| Growth Rate (2026 - 2031) | 10.25% CAGR |

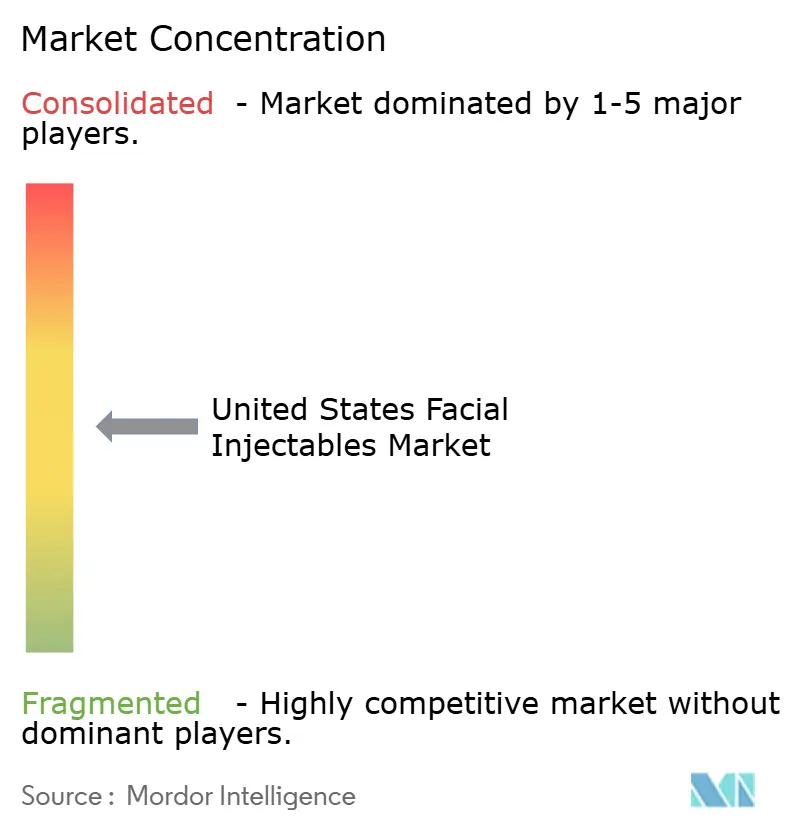

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Facial Injectables Market Analysis by Mordor Intelligence

The United States Facial Injectables Market size is projected to expand from USD 5.43 billion in 2025 and USD 5.98 billion in 2026 to USD 9.75 billion by 2031, registering a CAGR of 10.25% between 2026 to 2031.

The market is moving beyond a narrow cosmetic maintenance base because demand now comes from younger adults seeking preventive treatment, men entering the category more consistently, and patients seeking correction for facial volume loss after weight reduction. This wider treatment base is expanding addressable demand faster than treatment frequency alone, which supports recurring revenue for brands and clinic operators across the United States facial injectables market. Product innovation is also reshaping the commercial mix, as longer-duration toxins, regenerative fillers, and skin-quality injectables support higher-value protocols and more tailored treatment plans. Competitive behavior is becoming sharper as leading companies rely on injector education, indication expansion, loyalty platforms, and portfolio breadth, while newer entrants use differentiation and price positioning to gain traction. The largest near-term opportunity in the United States facial injectables market remains patient acquisition and protocol standardization for new treatment cohorts, while the key operational risk remains counterfeit and unsupervised injection activity that can damage trust in fast-growing outpatient channels.

Key Report Takeaways

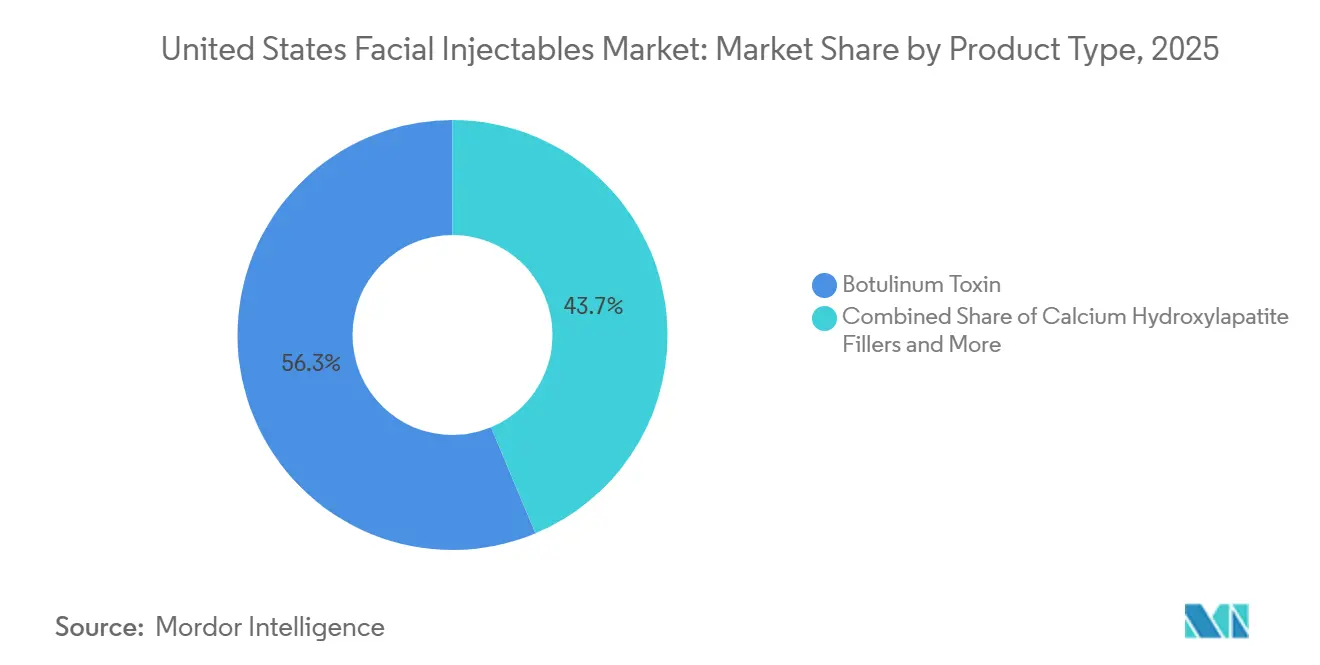

- By product type, botulinum toxin held 56.31% of United States facial injectables market share in 2025, while hyaluronic acid fillers are forecast to expand at 11.38% CAGR through 2031.

- By application, facial line correction accounted for 38.24% share of the United States facial injectables market size in 2025, while lip augmentation and perioral rejuvenation are forecast to expand at 11.52% CAGR through 2031.

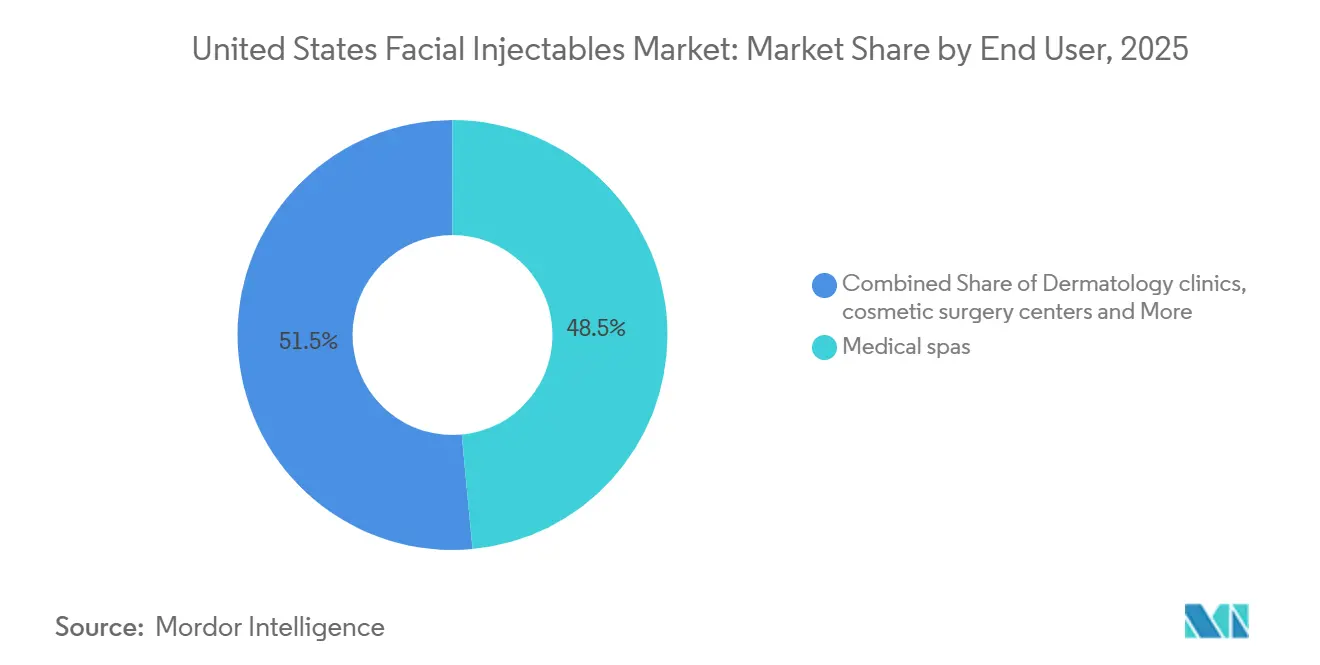

- By end user, medical spas held 48.52% of the United States facial injectables market share in 2025, while dermatology clinics are expected to record the highest CAGR at 11.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Facial Injectables Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Preference for Minimally Invasive Facial Aesthetics | +2.8% | National, highest procedural density in California, New York, Texas, and Florida | Short term (≤ 2 years) |

| Preventative Injectables Among Younger Adults | +2.0% | National, early concentration in coastal metro markets and college-adjacent cities | Medium term (2-4 years) |

| Broader Male-Patient Adoption | +1.1% | National, accelerating in urban professional corridors and Sun Belt markets | Medium term (2-4 years) |

| Longer-Duration Toxins and Regenerative Fillers | +1.4% | National, premium adoption concentrated in high-income ZIP codes | Long term (≥ 4 years) |

| GLP-1-Related Facial Volume-Loss Correction Demand | +1.0% | National, most acute in markets with high GLP-1 prescription density | Medium term (2-4 years) |

| Skin-Quality Injectables Expanding Treatment Occasions | +0.8% | National, driven by medspa and dermatology clinic penetration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Minimally Invasive Facial Aesthetics

The shift away from surgical facial procedures toward injectables reflects a durable change in how patients approach aesthetic care in the United States facial injectables market. Total cosmetic minimally invasive procedures exceeded 28.2 million in 2024, and neuromodulator injections alone reached 9.88 million, which shows how familiar these treatments have become for a broad patient base. Short recovery time, predictable outcomes, and the ability to adjust treatment gradually continue to make injectables more appealing than surgery for repeat maintenance. High procedure volume also teaches consumers to monitor facial aging more actively, which shortens the gap between noticing a concern and booking treatment. The medspa channel strengthens this pattern because it brings the category closer to consumers who may never have engaged a dermatologist or plastic surgeon before.

Preventative Injectables Among Younger Adults

Preventive treatment among Gen Z and younger millennials is changing the age profile of demand across the United States facial injectables market. A 2025 peer-reviewed analysis in the Aesthetic Surgery Journal found that the average age of first injection declines by 8.8 years with each successive decade of patients evaluated, which points to a strong cohort shift rather than a passing preference. This matters commercially because earlier treatment starts create a longer repeat-purchase cycle over the life of the patient. It also changes brand competition, because loyalty formed in the 20s can persist for many years if treatment outcomes remain consistent. Providers and brands that connect with this group early are better positioned to retain demand as these patients add new treatment areas over time.

Broader Male-Patient Adoption

Male demand is becoming a more meaningful contributor to the United States facial injectables market, even if it still trails the female patient base by volume. ASPS recorded 593,854 male neuromodulator injections and 106,665 male non-HA filler injections in 2024, representing 6% and 11% of their respective procedure totals, with year-on-year growth of 4.3% and 0.9%. Men often enter the category through jawline sculpting, masseter reduction, and chin contouring, which can support higher revenue per visit than standard forehead toxin sessions. Social media exposure and a stronger focus on professional image are also reducing stigma around male aesthetics. Companies that delay male-specific education, imagery, and injector training risk losing early loyalty to brands that already address this demand more directly.

Longer-Duration Toxins and Regenerative Fillers

Innovation in duration and mechanism is changing treatment economics across the United States facial injectables market. DAXXIFY showed a median clinical duration of 24 weeks in approval trials, compared with 16 to 18 weeks for standard botulinum toxin A, and more than 50% of patients maintained results at 6 months[1]Revance Therapeutics, “DAXXIFY Clinical and Product Information,” DAXXIFY, daxxify.com. In fillers, regenerative options such as PLLA biostimulators are attracting patients who want gradual collagen stimulation rather than immediate volume alone. Galderma reported positive 3-month interim data in January 2025 from a trial combining Sculptra with Restylane Lyft or Contour for patients experiencing GLP-1-related facial volume depletion. If treatment frequency falls because products last longer, providers need higher revenue per session, which supports premium pricing and combination protocols rather than simple volume growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-of-Pocket Repeat-Treatment Burden | -1.7% | National, most acute in price-sensitive suburban and rural markets | Short term (≤ 2 years) |

| Counterfeit and Unapproved Online Injectables | -0.8% | National, documented incidents across 11+ states | Short term (≤ 2 years) |

| Tighter Injector-Supervision and Delegation Rules | -0.6% | California, Texas, Florida, Georgia, expanding to Northeast and Midwest | Medium term (2-4 years) |

| Adverse-Event and Liability Sensitivity in High-Volume Settings | -0.5% | National, most material in high-volume medspa markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Repeat-Treatment Burden

The United States facial injectables market remains heavily exposed to patient spending because treatments are overwhelmingly self-pay. Neurotoxin sessions usually range from USD 300 to USD 600, while HA filler treatments typically range from USD 600 to USD 2,000 per area depending on product choice and injector profile. These costs build quickly for patients who maintain several facial areas or combine toxins with fillers in the same treatment cycle. That burden is especially important as the category expands into younger and more price-sensitive consumers, whose aesthetic budgets compete directly with routine household expenses. Providers that do not use membership models, treatment plans, or other retention tools face a greater risk of delayed visits, reduced frequency, and higher churn.

Counterfeit and Unapproved Online Injectables

Counterfeit and unapproved injectables have become a direct confidence risk for the United States facial injectables market, not just a fringe safety issue. The FDA issued a formal alert in April 2024 on counterfeit Botox circulating in multiple states. The CDC Health Alert Network then reported 22 adverse events across 11 states tied to injections by unlicensed individuals or to product from unverified sources. In 2025, the New York City Department of Health and Mental Hygiene documented 10 cases of severe illness linked to self-injected botulinum toxin bought through online marketplaces. These events are concentrated in unsupervised or loosely controlled settings, and they can weaken trust in fast-growing outpatient channels even when legitimate providers follow proper standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Entrenched Neurotoxin Leadership, Filler Acceleration Driven by Indication Expansion

Botulinum toxin held 56.31% of United States facial injectables market share in 2025, which confirms its position as the main entry point for new patients in the category. Its lead reflects broad use across glabellar lines, brow lifting, masseter reduction, and hyperhidrosis, along with repeat treatment patterns that support stable annual demand. The United States facial injectables industry also benefits from the category's familiarity, because many first-time patients begin with toxin before moving into more customized filler protocols. DAXXIFY adds another competitive layer by offering a median clinical duration of 24 weeks, which shifts the value discussion from simple session frequency toward efficacy per visit.

Calcium hydroxylapatite fillers and PLLA biostimulators are gaining momentum in regenerative treatment settings, where patients often want structural support and collagen stimulation rather than short-term volumization alone. Merz Aesthetics receives FDA approval in April 2026 for RADIESSE in the décolleté area, which expands the brand to four indications and strengthens its regenerative positioning across face and body. PMMA and collagen-based fillers continue to serve narrower but durable uses such as acne scar correction and chronic volume deficit management. HA fillers are the fastest-growing product segment at 11.38% CAGR from 2026 to 2031, supported by broader indication expansion, rising interest in skin-quality treatment, and active R&D directed at GLP-1-treated patients[2]ClinicalTrials.gov, “Assess Impact of Microdroplet HA Filler on Skin Quality in Patients on GLP-1 Agonists,” ClinicalTrials.gov, clinicaltrials.gov. FDA approval pathways remain a meaningful entry barrier in the United States facial injectables industry, which helps established brands defend share even as new entrants intensify competition.

By Application: Lip Augmentation Fastest-Growing as Patient Demographics Shift

Facial line correction accounted for 38.24% of the United States facial injectables market size in 2025, and it remained the largest application because it is still the most common first treatment. This application also supports strong recurring revenue because maintenance often requires 3 to 4 visits a year, which is more frequent than many volume-restoration procedures. In contrast, lip augmentation and perioral rejuvenation is the fastest-growing application at 11.52% CAGR from 2026 to 2031, driven by younger patient demand and better HA formulations suited to lip movement and tissue behavior. That growth profile matters because younger lip patients often become multi-category consumers later, which increases their long-term value within the United States facial injectables market.

Midface and cheek augmentation, chin and jawline contouring, and acne or atrophic scar correction are all expanding as injector training becomes more advanced and patient goals become more specific. The application mix is also changing because GLP-1-related facial volume loss creates a more urgent need for templated restoration protocols. A 2025 systematic review from the University of Washington and Emory University found that patients who lose 10% to 30% of body weight on GLP-1 agonists can show volume depletion in the cheeks, temples, tear troughs, lips, and jawline, changes that resemble accelerated facial aging. This creates a commercial gap because no branded standard protocol is yet established across the United States facial injectables market for this patient group. Established filler brands therefore have room to compete through treatment pathways, education, and combination regimens rather than product claims alone.

By End User: Medical Spas Dominant but Compliance Complexity Rising; Dermatology Clinics Fastest-Growing

Medical spas retained 48.52% of the United States facial injectables market size in 2025, which shows how far access has shifted from surgical settings toward high-volume outpatient environments. Their advantage comes from convenience, accessible pricing, membership models, and the ability to process a high number of repeat visits. This channel has become central to growth in the United States facial injectables market because it reaches consumers who prefer a lower-friction treatment experience. At the same time, the same high-volume model exposes medical spas more directly to scrutiny around injector supervision, delegation, and training standards.

Dermatology clinics are projected to grow at 11.25% CAGR from 2026 to 2031, the fastest pace among end users, because they can combine injectables with prescription skin care, energy devices, and physician-led assessment in one setting. That structure supports higher revenue per patient and stronger retention when cases are more complex or treatment plans span several modalities. The American Med Spa Association documented active 2025 legislative debates in states including Arizona, Illinois, and Colorado on APRN supervision requirements, which shows how operating rules are still evolving[3]American Med Spa Association, “Q1 2025 Med Spa Legislation Recap,” American Med Spa Association, americanmedspa.org. Plastic surgery and cosmetic surgery centers remain relevant for premium contouring and combination procedures, while hospitals and ambulatory surgery centers serve a narrower role in medically adjacent injectable use. The result is a channel mix where volume leadership stays with medical spas, but clinical complexity and regulatory resilience increasingly favor dermatology-led care.

Geography Analysis

California and the West Coast remain the deepest revenue pool within the United States facial injectables market because the region combines high disposable income, strong cultural acceptance of aesthetic procedures, and a dense supply of trained injectors. This regional base supports consistent demand across both neurotoxins and fillers, with a treatment mix that extends well beyond entry-level wrinkle correction. California also faces heavier operating scrutiny than many other states, which raises the bar for compliance among medspas and multi-site clinic operators. That tighter environment can slow poorly supervised expansion, but it also supports more disciplined provider behavior across the United States facial injectables market.

The Sun Belt, including Texas, Florida, Arizona, and Georgia, is the most active growth cluster for clinic expansion, new patient acquisition, and franchise-led medspa rollout. Population inflows, retiree spending, and strong aesthetic awareness keep these states attractive for new product launches and broader commercial distribution. At the same time, the region presents more execution risk because fast clinic growth can outpace the availability of well-trained and properly supervised injectors. That imbalance raises the importance of credentialing, oversight, and clinical protocol consistency for operators trying to scale. For the United States facial injectables market, the Sun Belt offers strong growth potential, but it also demands more disciplined compliance infrastructure than earlier expansion phases required.

The Northeast, led by New York and nearby affluent urban markets, remains important because patients in the region place strong weight on clinical credibility, innovation, and physician reputation. This supports faster adoption of differentiated products and combination protocols when new indications or treatment approaches reach the market. The Midwest presents a different opportunity because lower saturation and more accessible price points can support subscription-style growth and challenger brand entry. Together, these patterns show that the United States facial injectables market is national in scope, but regional success still depends on matching channel strategy, compliance capability, and treatment positioning to local demand conditions.

Competitive Landscape

The United States facial injectables market is moderately consolidated at the brand level, with AbbVie's Allergan Aesthetics and Galderma controlling the largest combined revenue pools across toxins and fillers. Their position comes from wide portfolios, strong injector education networks, and long clinical track records that are hard for newer players to replicate quickly. Allergan's BOTOX Cosmetic and JUVEDERM lines continue to support premium pricing, and its March 2026 presentation of the "Undetectable Era" framework at AMWC Monaco shows that natural-looking outcomes are a major competitive theme in 2026. Galderma also competes from a position of breadth through Dysport, Restylane, and Sculptra, and its January 2025 GLP-1-related combination trial gives it early visibility in an emerging use case. These two companies set much of the pace for premium brand positioning in the United States facial injectables market.

The second tier remains active and commercially relevant because it competes through targeted differentiation rather than pure scale. Evolus reported that Jeuveau captured more than 14% of the U.S. neurotoxin market and reached more than 50% clinic penetration, supported by a digital loyalty platform with nearly 1.5 million members. Revance competes on duration through DAXXIFY and extends its filler presence through the RHA Collection, including the March 2026 commercial launch of RHA Dynamic Volume for midface contour deficiencies. Merz Aesthetics remains important across Xeomin, Radiesse, and Belotero, with its April 2026 RADIESSE indication expansion showing how filings and label growth can build share without broad price competition. This leaves the United States facial injectables market open to challenger gains, but mostly in targeted niches rather than across the full portfolio spectrum.

The next competitive phase is likely to center on combination protocols, formulation technology, and indication breadth rather than basic volume promotion. That favors companies with stronger clinical development pipelines, better regulatory execution, and closer ties to injector education. White space remains visible in male-focused treatment pathways, GLP-1-related volume correction, and underserved non-coastal growth markets where branded loyalty is less entrenched. For the United States facial injectables market, this means scale still matters, but execution around emerging cohorts and protocol design matters more than scale alone.

United States Facial Injectables Industry Leaders

AbbVie (Allergan Aesthetics)

Galderma

Merz Aesthetics

Evolus

Revance

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Merz Aesthetics received FDA approval for RADIESSE for the treatment of décolleté wrinkles in patients 22 years and older, RADIESSE's fourth indication, making it the first and only regenerative biostimulator approved in the US for both face and body, and responding directly to growing patient demand for regenerative approaches to skin aging.

- March 2026: Revance and Teoxane commercially launched RHA Dynamic Volume, an HA filler for midface contour deficiencies engineered with adapted rheology for dynamic facial movement, and clinical data showed 98% of patients reported natural-looking results across clinical studies.

United States Facial Injectables Market Report Scope

As per the scope of the report, facial injectables are medical treatments used to enhance, restore, or alter facial features by injecting substances into the skin or underlying tissues. They are commonly used for purposes such as reducing wrinkles, adding volume, contouring, and improving skin appearance.

The segmentation for the United States facial injectables market is categorized by product type, application, and end user. By product type, the market includes botulinum toxin, hyaluronic acid fillers, calcium hydroxylapatite fillers, poly-L-lactic acid biostimulators, PMMA/collagen hybrid fillers, and other facial soft tissue fillers. By application, it covers facial line correction, lip augmentation and perioral rejuvenation, midface and cheek augmentation, chin and jawline contouring, acne scar and atrophic scar correction, lipoatrophy and volume restoration, and other applications. By end user, the market is segmented into dermatology clinics, plastic and cosmetic surgery centers, medical spas, and hospitals and ambulatory surgery centers. For each segment, the market size and forecast are provided in terms of value (USD).

| Botulinum Toxin |

| Hyaluronic Acid Fillers |

| Calcium Hydroxylapatite Fillers |

| Poly-L-lactic Acid Biostimulators |

| PMMA / Collagen Hybrid Fillers |

| Other Facial Soft Tissue Fillers |

| Facial line correction |

| Lip augmentation and perioral rejuvenation |

| Midface and cheek augmentation |

| Chin and jawline contouring |

| Acne scar and atrophic scar correction |

| Lipoatrophy and volume restoration |

| Other Applications |

| Dermatology clinics |

| Plastic surgery and cosmetic surgery centers |

| Medical spas |

| Hospitals and ambulatory surgery centers |

| By Product Type | Botulinum Toxin |

| Hyaluronic Acid Fillers | |

| Calcium Hydroxylapatite Fillers | |

| Poly-L-lactic Acid Biostimulators | |

| PMMA / Collagen Hybrid Fillers | |

| Other Facial Soft Tissue Fillers | |

| By Application | Facial line correction |

| Lip augmentation and perioral rejuvenation | |

| Midface and cheek augmentation | |

| Chin and jawline contouring | |

| Acne scar and atrophic scar correction | |

| Lipoatrophy and volume restoration | |

| Other Applications | |

| By End User | Dermatology clinics |

| Plastic surgery and cosmetic surgery centers | |

| Medical spas | |

| Hospitals and ambulatory surgery centers |

Key Questions Answered in the Report

What is the forecast for United States facial injectables through 2031?

The United States facial injectables market is projected to grow from USD 5.98 billion in 2026 to USD 9.75 billion by 2031 at a CAGR of 10.25%.

Which product type leads current revenue and which is growing fastest?

Botulinum toxin led with 56.31% revenue share in 2025, while HA fillers are the fastest-growing product type at 11.38% CAGR through 2031.

Why are younger adults becoming important to facial injectables demand?

Preventive treatment is starting earlier, and a 2025 peer-reviewed study showed the average age of first injection has been declining across successive patient cohorts.

Which application is expanding the fastest in the United States?

Lip augmentation and perioral rejuvenation is growing the fastest at 11.52% CAGR through 2031, supported by younger patient demand and improved soft HA formulations.

Which care setting dominates today and which one is gaining fastest?

Medical spas held 48.52% of revenue in 2025, while dermatology clinics are growing the fastest at 11.25% CAGR through 2031 because they can deliver more complex combination care.

What is the biggest operational risk for providers and brands?

Counterfeit and unapproved injectables remain a major risk, with FDA and CDC alerts and 2025 New York City illness cases showing how unsupervised use can damage consumer trust.

Page last updated on: