United States Enterprise Resource Planning Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

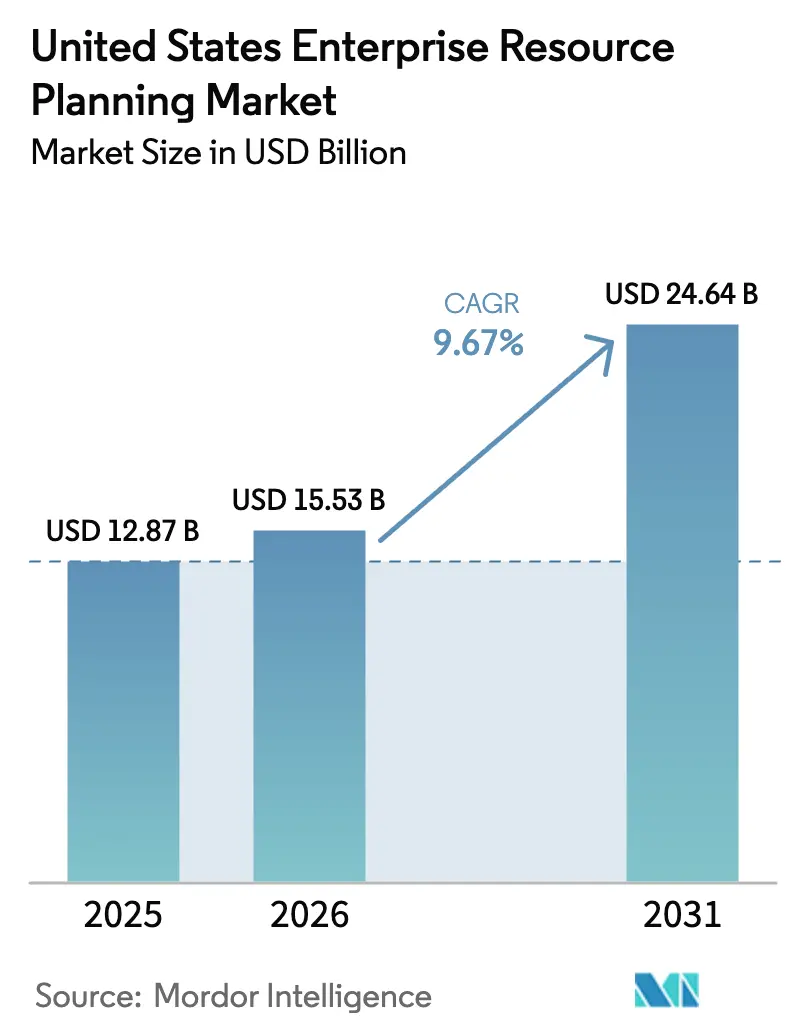

| Base Year Market Size (2025) | USD 12.87 Billion |

| Market Size (2026) | USD 15.53 Billion |

| Market Size (2031) | USD 24.64 Billion |

| Growth Rate (2026 - 2031) | 9.67% CAGR |

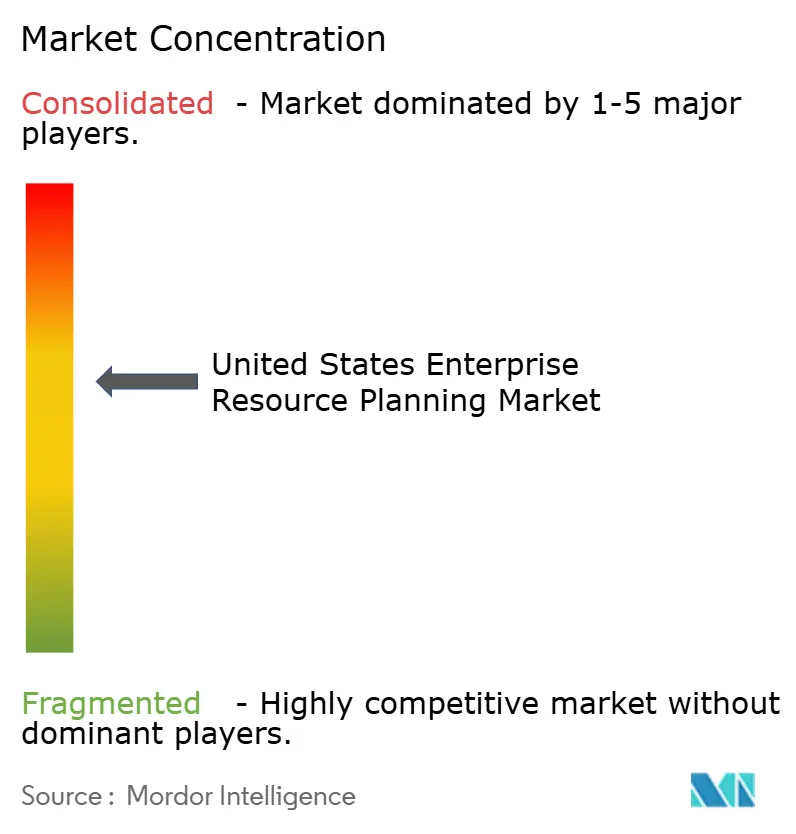

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Enterprise Resource Planning Market Analysis by Mordor Intelligence

The United States enterprise resource planning market size is expected to increase from USD 12.87 billion, and USD 15.53 billion in 2026 to USD 24.64 billion by 2031, growing at a 9.67% CAGR over 2026-2031. Shifts from capital-intensive on-premises suites to elastic cloud subscriptions are compressing payback periods, while embedded artificial intelligence automates finance, supply chain, and workforce tasks, elevating system value. Mid-market manufacturers and distributors that had long postponed upgrades are now migrating in waves because templated cloud offerings cut implementation cycles from 18 months to 9 and trim information-technology overhead by nearly one-third. Federal incentives tied to the CHIPS and Inflation Reduction Acts accelerate system replacements among semiconductor, clean-energy, and battery producers, whose subsidies require real-time traceability of energy, labor, and emissions data. Vendors that deliver quarterly feature releases, composable architectures, and zero-downtime updates gain share as decision makers prize agility, continuous compliance, and lower lifetime cost of ownership.

Key Report Takeaways

- By deployment model, cloud commanded 71.64% of the United States enterprise resource planning market share in 2025 and is expanding at a 10.67% CAGR through 2031.

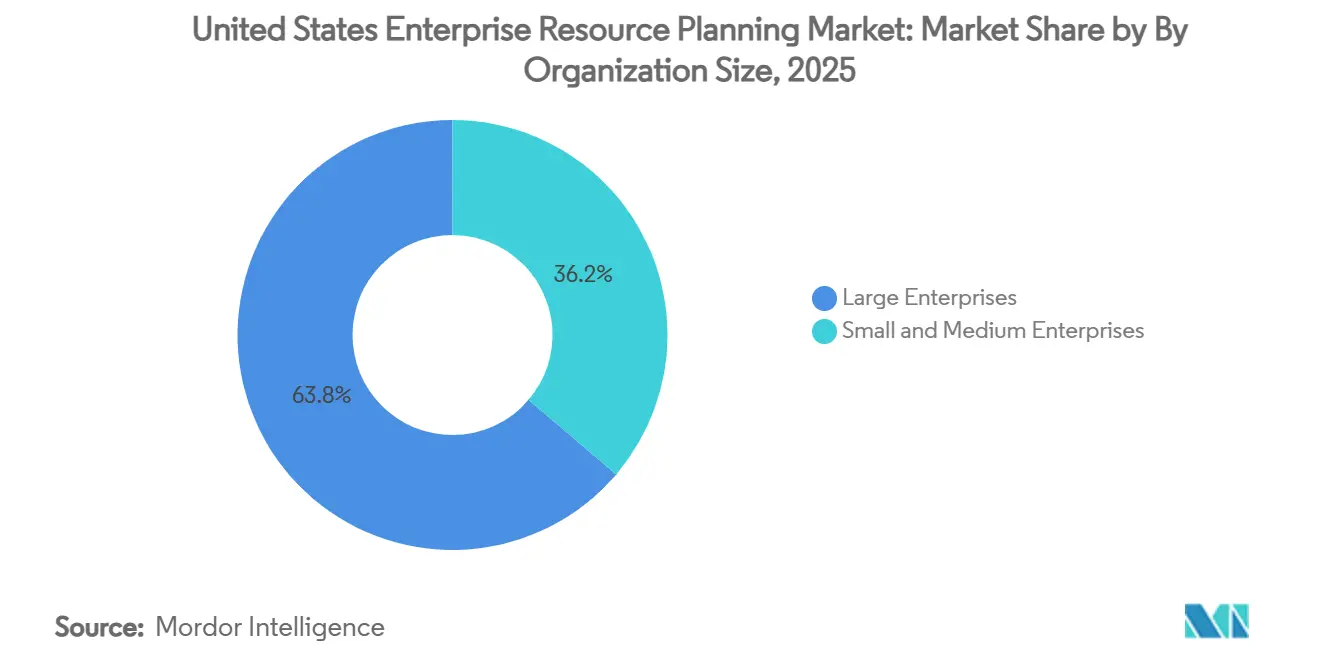

- By organization size, large enterprises led the United States enterprise resource planning market with a 63.77% share in 2025, while small and medium enterprises recorded the fastest projected CAGR of 11.35% through 2031.

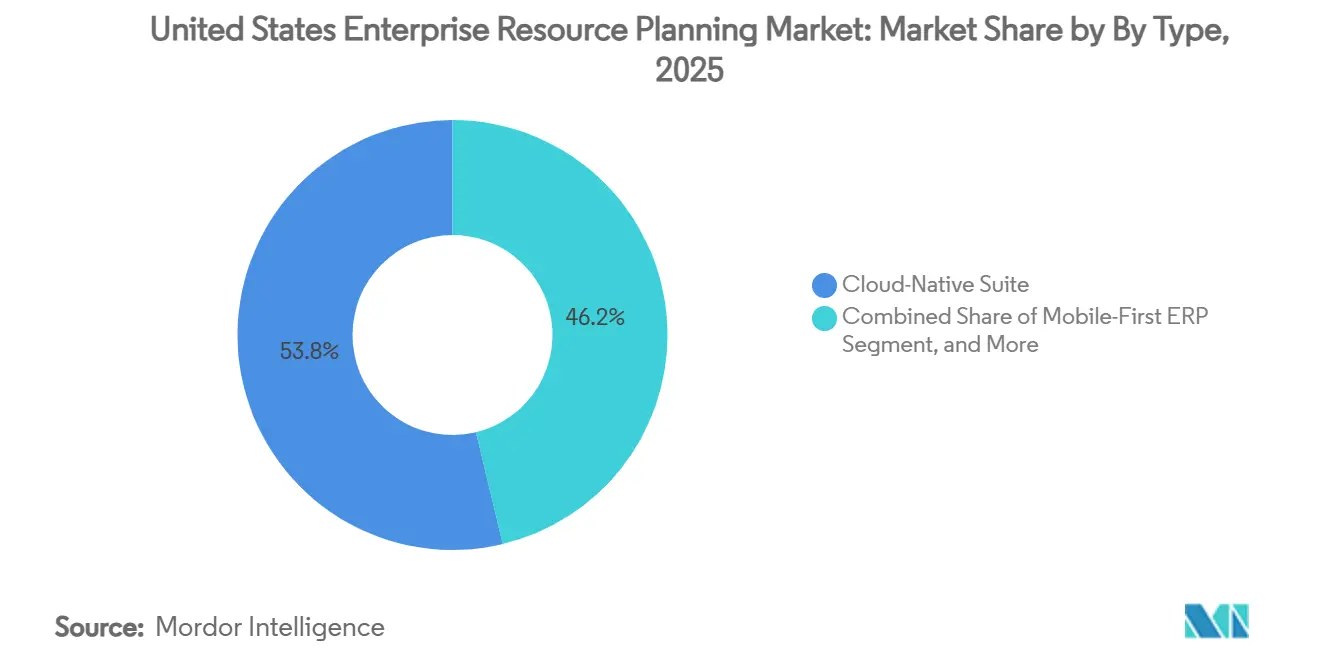

- By type, cloud-native suites captured 53.76% of the United States enterprise resource planning market size in 2025 and are projected to grow at a 10.41% CAGR over 2026-2031.

- By business function, finance and accounting accounted for 28.74% of the United States enterprise resource planning market in 2025 and is forecast to grow at a 10.56% CAGR to 2031.

- By industry vertical, manufacturing accounted for 21.83% of revenue in 2025 and is advancing at an 11.13% CAGR, the fastest among all tracked sectors.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Enterprise Resource Planning Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption Of Cloud ERP Among Mid‑Market Businesses | +2.4% | National, strongest in Texas, California, Illinois hubs | Medium Term (2–4 Years) |

| Integration Of AI‑Powered Analytics Within ERP Suites | +2.1% | Nationwide, early uptake in tech, finance, healthcare | Short Term (≤ 2 Years) |

| Demand For Real‑Time Supply Chain Visibility Post‑Pandemic | +1.7% | Nationwide, pronounced in automotive, pharma, electronics | Short Term (≤ 2 Years) |

| Government Incentives For Digital Transformation In Manufacturing | +1.2% | Midwest and Southeast manufacturing corridors | Medium Term (2–4 Years) |

| Emergence Of Composable ERP Architectures Enabling Modular Deployments | +1.0% | National, strong in multi‑subsidiary enterprises | Long Term (≥ 4 Years) |

| Shift Toward Subscription‑Based Pricing Models Improving ROI | +0.8% | National, sharpest in capital‑constrained SMEs | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Cloud ERP Among Mid-Market Businesses

Mid-market firms with USD 50 million to USD 1 billion in revenue migrate to cloud suites at a rate of more than 25% year-over-year because subscription pricing smooths cash outflows and eliminates hardware refreshes. One precision machining company in Texas cut IT overhead by 30% and lifted on-time delivery by 20% after replacing a 15-year-old system with an integrated cloud platform. Vendors preload connectors for Shopify, Amazon Marketplace, and third-party logistics providers, allowing distributors to synchronize sales, inventory, and finance without custom code. Private-equity owners now mandate cloud ERP at acquisition close to speed bolt-on integrations, further fueling demand. The momentum reduces the once-formidable switching barrier that kept legacy on-premise suites entrenched.

Integration of AI-Powered Analytics Within ERP Suites

Generative and predictive models embedded inside modern ERP platforms automate journal entries, supplier negotiations, and production scheduling. SAP’s Joule Copilot processed more than one billion transactions in 2025 and shortened month-end close cycles by 40% for early adopters.[1]Source: SAP, “Joule Copilot Processes One Billion Transactions,” SAP.COMMicrosoft Dynamics 365 Copilot drafts cash-flow alerts and inventory reorder recommendations, while Oracle Fusion automatically classifies ledger lines and reconciles intercompany balances.[2]Source: Oracle, “Fusion Cloud ERP AI Enhancements,” ORACLE.COM These capabilities reduce manual effort, speed decision-making, and bring project payback within 18 months. Adoption lags in healthcare and banking, however, because leaders demand model explainability to satisfy HIPAA and Sarbanes-Oxley audits.

Demand for Real-Time Supply Chain Visibility Post-Pandemic

Pandemic disruptions exposed the limitations of batch-oriented ERP systems, prompting 68% of supply-chain executives to prioritize upgrades that integrate IoT sensors and transportation systems. Automotive original-equipment manufacturers now require tier-1 suppliers to broadcast production status inside ERP portals, enabling just-in-sequence assembly and paring safety stock by up to 40%. Pharmaceutical distributors feed cold-chain telemetry into ERP inventory modules to protect drug integrity and comply with Drug Supply Chain Security Act serialisation requirements. Edge ERP deployments that transact locally and sync hourly with cloud hosts reduce latency and keep plants running during network outages, making the architecture a preferred blueprint for multi-site manufacturers.

Government Incentives for Digital Transformation in Manufacturing

The CHIPS and Science Act earmarked USD 52.7 billion for advanced manufacturing, and eligible digital infrastructure, including ERP, qualifies for 25% investment tax credits. A Midwest battery maker accelerated its ERP project by 12 months to capture USD 15 million in federal grants. States, including Ohio and Arizona, layer on matching funds that reduce net project costs by up to 40%, a critical lever for small and medium manufacturers adopting Industry 4.0. Subsidy recipients must document carbon intensity, labor productivity, and supply-chain provenance in real time, pushing many to retire paper or spreadsheet workflows and adopt integrated suites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Switching Costs From Legacy On‑Premise Systems | -1.5% | National, acute for SAP ECC and Oracle E‑Business Suite users | Medium Term (2–4 Years) |

| Cybersecurity Concerns Hampering Cloud Migrations | -1.2% | Nationwide, strongest in finance, healthcare, government | Short Term (≤ 2 Years) |

| Shortage Of ERP Implementation Talent In Rural Regions | -0.9% | Rural Midwest, Southeast, Mountain West | Long Term (≥ 4 Years) |

| Data Sovereignty And Compliance Complexities Across State Regulations | -0.7% | California, Virginia, Colorado, Connecticut | Medium Term (2–4 Years) |

| Source: Mordor Intelligence | |||

High Switching Costs from Legacy On-Premise Systems

Companies running highly customized SAP ECC or Oracle E-Business Suite face migration costs equal to 2-4% of annual revenue, with data cleansing alone consuming 40% of budgets and adding nine months to timelines. Consolidating multiple charts of accounts and customer masters inflates the scope, forcing many firms to phase migrations or accept costly customizations that compromise future upgrades. Mid-market enterprises, often short on change-management resources, feel the burden most acutely because they must rely on consultants billing USD 200-300 per hour.

Cybersecurity Concerns Hampering Cloud Migrations

The average cost of a United States data breach rose to USD 10.22 million in 2025, and cloud misconfigurations triggered 45% of incidents. [3]Source: IBM Security, “Cost of a Data Breach Report 2025,” IBM.COMA 2024 zero-day exploit in Oracle E-Business Suite reinforced fears that even mature platforms remain vulnerable. Finance and healthcare leaders worry that multi-tenant architectures cannot meet the Sarbanes-Oxley or HIPAA record-keeping requirements without costly compensating controls. The Cloud Security Alliance now recommends zero-trust frameworks and quarterly penetration tests, raising annual operating costs by 10-15% and requiring scarce cyber talent.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Cloud-Native Suites Unlock Agility and Modular Growth

Cloud-native suites segment commanded 53.76% in 2025 and will grow at a 10.56% CAGR through 2031, reflecting API-first architectures that enable finance or warehouse modules to be upgraded in isolation, ending weekend shutdowns and elevating uptime to 99.9%. Vendors such as Workday land with a core ledger and expand to an average of 3.2 modules within two years, proving the land-and-expand appeal.[4]Workday, “Financial Management Adoption Metrics,” WORKDAY.COM

Mobile-first ERP caters to field technicians and warehouse operators who primarily transact on smartphones, while social ERP embeds approvals and alerts within collaboration tools such as Teams and Slack. Two-tier or edge ERP synchronizes lightweight plant systems with a central cloud core, a strategy expected to achieve moderate penetration by 2027. Collectively, these patterns underline how composability helps organizations avoid lock-in and swap functionality without wholesale reimplementation.

By Business Function: Finance and Accounting Modernize First

Finance and accounting modules commanded 28.74% of spending in 2025 and will grow at a 10.56% CAGR through 2031, reflecting new tax, lease, and ESG disclosure rules that legacy systems cannot automate cost-effectively. Automated revenue recognition, intercompany eliminations, and multi-currency consolidation reduce audit fees and close cycles, making finance the entry point for many cloud migrations.

Supply-chain suites rank second, especially among manufacturers that need synchronized demand plans, procurement, and logistics. Human-capital tools now track skills inventories and pay equity metrics to comply with pay transparency laws. Customer and commerce modules unify digital and store channels, while manufacturing execution bridges shop-floor telemetry with financial ledgers, a necessity for lights-out automation programs.

By Deployment Model: Cloud Becomes Default Choice

Cloud deployments owned a 71.64% share in 2025 and are on pace for a 10.67% CAGR. Oracle froze innovation for on-premise E-Business Suite and PeopleSoft, pushing clients toward Fusion Cloud for new artificial intelligence and analytics. SAP extended support for ECC only through 2027, making S/4HANA Cloud the innovation lead. These policies, stitched to the economics of elastic scaling and quarterly releases, cement cloud as the default.

On-premise remains for defense or rural healthcare entities that require sovereign control or face weak connectivity, yet vendors now price perpetual licenses at two to three times comparable subscriptions and limit support hours. Hybrid footprints serve as transitional bridges but deliver diminishing returns as feature gaps widen.

By Organization Size: SMEs Accelerate, Large Enterprises Sustain Scale

Large enterprises held 63.77% of the United States Enterprise Resource Planning market share in 2025 and will grow at a 10.89% CAGR, driven by multi-entity compliance demands and two-tier strategies. They regularly invest USD 5-50 million to standardize hundreds of legal entities and dozens of currencies.

Small and medium enterprises hold a 36.23% share yet experience faster adoption because Acumatica, Sage Intacct, and Odoo cost USD 100-200 per user per month and go live within 6 months. Low-code customization and prebuilt Salesforce or Shopify connectors eliminate the historic need for expensive developers and make enterprise-class functionality affordable.

By Industry Vertical: Manufacturing Leads Through Traceability Mandates

Manufacturing accounted for 21.83% of revenue in 2025 and is expanding at an 11.13% CAGR, the fastest among tracked sectors. The United States Enterprise Resource Planning market in this vertical is growing because semiconductor and battery producers must document full material lineage to claim CHIPS subsidies. Automotive suppliers sync plant schedules with just-in-sequence assembly, trimming work-in-process by up to 40%.

Retail and ecommerce firms adopt unified commerce suites that merge point-of-sale, web, and mobile inventory data to prevent overselling. Banks modernize back-office ledgers to support real-time payments and Dodd-Frank stress testing. Government entities deploy cloud financials with citizen portals, while hospitals consolidate billing, supply, and clinical-trial data into a single suite to improve care coordination.

Geography Analysis

Federal incentives channel most manufacturing deployments to the Midwest and Southeast corridors, where semiconductor and electric-vehicle investments cluster. Plants in Ohio, Arizona, and Tennessee are pushing vendors to add localized tax and labor-compliance features, boosting regional professional services demand.

Coastal technology and healthcare hubs in California, Washington, and Massachusetts trail-blaze AI-infused ERP pilots. These early adopters influence product roadmaps and validate new workflows such as autonomous journal entries and supply-chain control towers, creating reference customers that accelerate nationwide rollouts.

Rural regions in the Mountain West and Deep South still lag due to broadband gaps and a deficit of certified consultants, yet state grants and low-orbit satellite connectivity programs are narrowing the divide. As high-volume manufacturers choose smaller towns for greenfield plants, vendors open regional implementation centers, seeding future cloud uptake.

Competitive Landscape

SAP, Oracle, and Microsoft still capture roughly 55-60% of new bookings, but share erosion is evident as Workday dominates large-enterprise human-capital deals, while vertical players such as Epicor, Infor, and Tyler Technologies exploit sector gaps. SAP’s cloud revenue surpassed license revenue in 2025, following its RISE migration program, which bundled services with subscriptions. Oracle folded Cerner into Fusion Cloud to blend clinical and financial data, signaling vertical convergence.

Smaller challengers win on cost and speed. Acumatica’s unlimited-user model attracts seasonal manufacturers, while Priority Software courts multilingual midsize exporters. Vendors with quarterly release cadences, open APIs, and 99.9% availability commitments gain net-new logos as switching costs fall.

Technology differentiation pivots on embedded AI, low-code extensibility, and data-residency transparency. Providers unable to guarantee sub-second latency, cyber resiliency, or composable deployments risk churn, especially as enterprises design ERP cores to be swapped in as modules rather than monoliths.

United States Enterprise Resource Planning Industry Leaders

SAP SE

Oracle Corporation

Microsoft Corporation

Infor Inc.

Workday Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Microsoft released Dynamics 365 Copilot for Finance, automating variance analysis and cutting close cycles by 35%.

- December 2025: Workday acquired Evisort for USD 1.8 billion, embedding AI contract intelligence into its financials and procurement systems.

- November 2025: Workday acquired Evisort for USD 1.8 billion, embedding AI contract intelligence into its financials and procurement systems.

- September 2025: Infor and Amazon Web Services unveiled industry templates that cut implementation timelines to nine months.

United States Enterprise Resource Planning Market Report Scope

The United States Enterprise Resource Planning Report is Segmented by Type (Cloud-Native Suite, Mobile-First ERP, Social or Collaborative ERP, Two-Tier or Edge ERP), Business Function (Finance and Accounting, Supply Chain and Operations, Human Capital Management, Customer Relationship and Commerce, Manufacturing Execution and Quality), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Industry Vertical (Manufacturing, Retail and E-commerce, BFSI, Government and Public Sector, IT and Telecom, Healthcare and Life Sciences, Other Industry Verticals). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud-Native Suite |

| Mobile-First ERP |

| Social / Collaborative ERP |

| Two-Tier / Edge ERP |

| Finance and Accounting |

| Supply-Chain and Operations |

| Human Capital Management |

| Customer Relationship and Commerce |

| Manufacturing Execution and Quality |

| On-Premise |

| Cloud |

| Large Enterprises |

| Small and Medium Enterprises |

| Manufacturing |

| Retail and E-commerce |

| BFSI |

| Government and Public Sector |

| IT and Telecom |

| Healthcare and Life Sciences |

| Others Industry Vertical |

| By Type | Cloud-Native Suite |

| Mobile-First ERP | |

| Social / Collaborative ERP | |

| Two-Tier / Edge ERP | |

| By Business Function | Finance and Accounting |

| Supply-Chain and Operations | |

| Human Capital Management | |

| Customer Relationship and Commerce | |

| Manufacturing Execution and Quality | |

| By Deployment Model | On-Premise |

| Cloud | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Industry Vertical | Manufacturing |

| Retail and E-commerce | |

| BFSI | |

| Government and Public Sector | |

| IT and Telecom | |

| Healthcare and Life Sciences | |

| Others Industry Vertical |

Key Questions Answered in the Report

How fast is adoption of cloud deployment among United States ERP users?

Cloud captured 71.64% share in 2025 and is growing at a 10.67% CAGR through 2031, making it the dominant deployment pattern.

Which business function upgrades first when United States firms modernize ERP?

Finance and accounting leads, holding 28.74% spend in 2025 and expanding at a 10.56% CAGR, driven by new tax and ESG disclosure mandates.

Why is manufacturing the fastest-growing vertical for ERP in the United States?

Manufacturers must document full material traceability to unlock CHIPS and clean-energy subsidies, lifting their ERP spend at an 11.13% CAGR.

What is the biggest barrier to ERP migration today?

Switching from heavily customized on-premise suites can cost 2-4% of annual revenue, delaying projects and inflating budgets.

Page last updated on: