United States Digital Denture Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

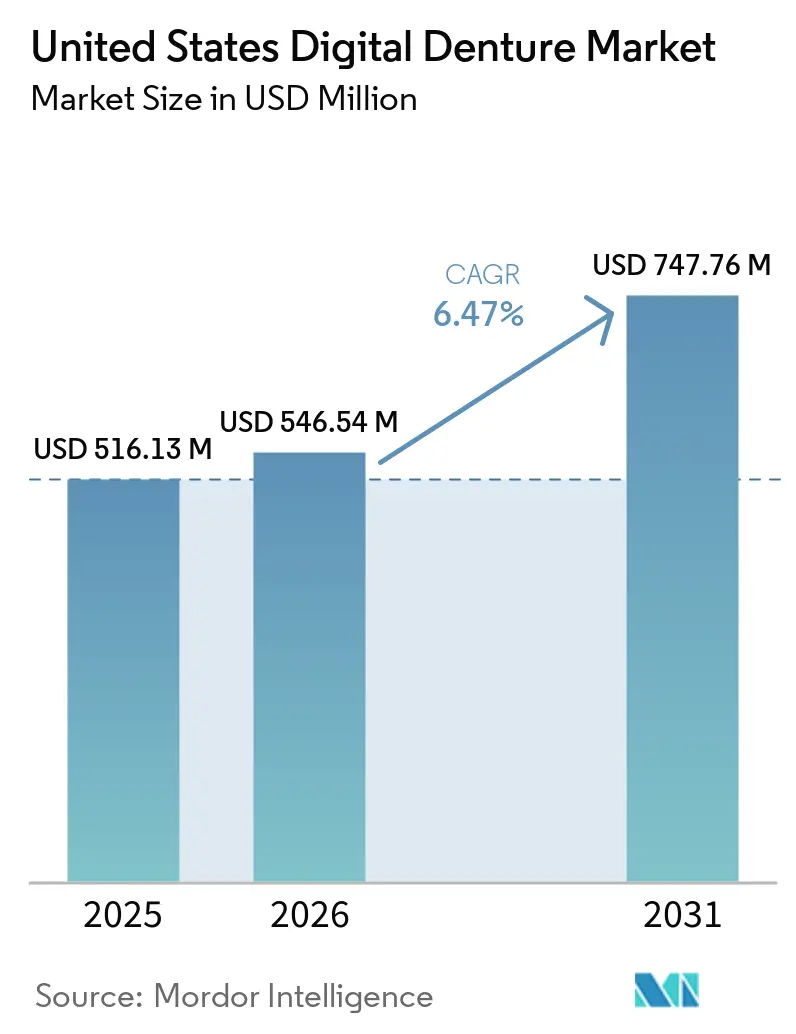

| Base Year Market Size (2025) | USD 516.13 Million |

| Market Size (2026) | USD 546.54 Million |

| Market Size (2031) | USD 747.76 Million |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Digital Denture Market Analysis by Mordor Intelligence

The United States Digital Denture Market size is projected to expand from USD 516.13 million in 2025 and USD 546.54 million in 2026 to USD 747.76 million by 2031, registering a CAGR of 6.47% between 2026 to 2031.

The digital denture market is being shaped by 2 structural shifts that are moving in parallel: a larger elderly patient pool with significant tooth loss and a steady move away from analog fabrication toward software-led design and automated production. The American College of Prosthodontics states that 36 million Americans are fully edentulous and 120 million are missing at least 1 tooth, which leaves a broad treatment base for removable prosthetics and related replacement cycles across the forecast window. The U.S. Census Bureau projects that the population aged 65 and older will reach 73 million by 2030, which means the age group with the highest denture need will continue expanding during the period under review. Competition in the digital denture market is also moving beyond hardware alone, as established suppliers push validated material and printer ecosystems while lower-cost entrants compete on access, workflow simplicity, and open architecture. This leaves room for growth where laboratories can raise throughput, where duplicate denture workflows reduce repeat visits, and where centralized purchasing groups standardize technology choices across multiple clinical locations.

Key Report Takeaways

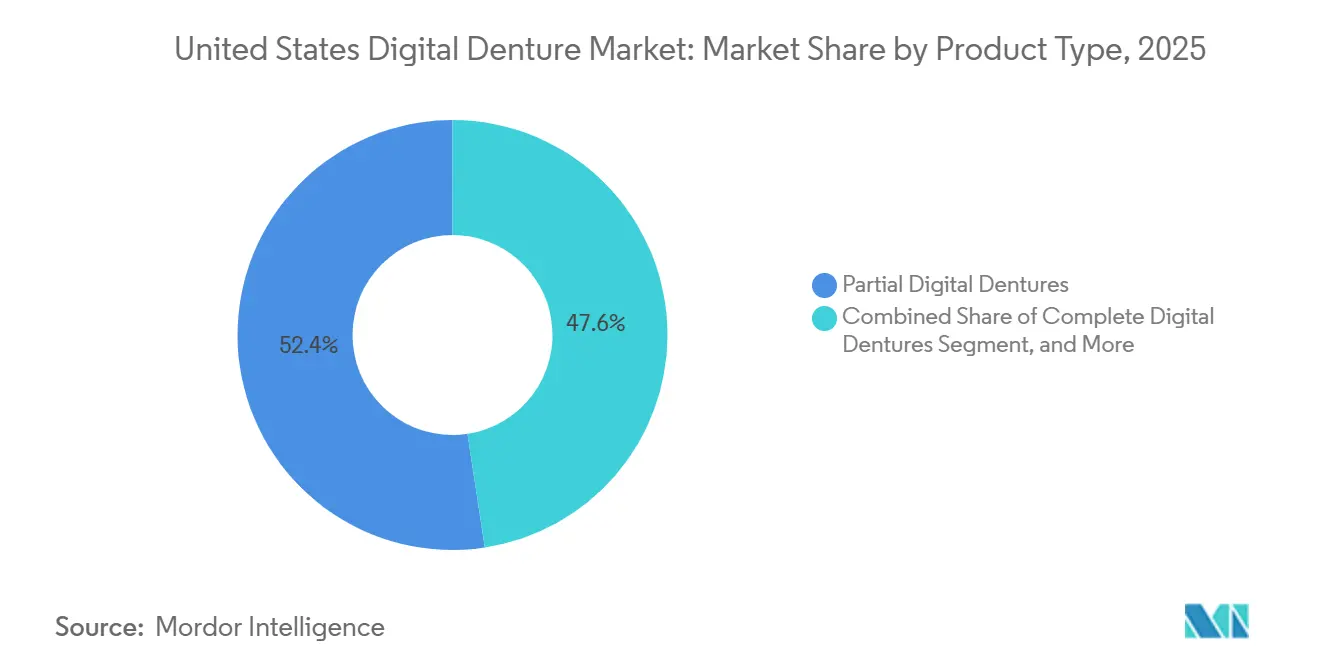

- By product type, Partial Digital Dentures held 52.39% of the digital denture market size in 2025, while Complete Digital Dentures are forecast to expand at a 9.28% CAGR through 2031.

- By manufacturing route, Vat Photopolymerization 3D Printing captured 47.23% of the digital denture market share in 2025, while Material Jetting and Multi-Material Monolithic Printing are projected to grow at a 9.92% CAGR through 2031.

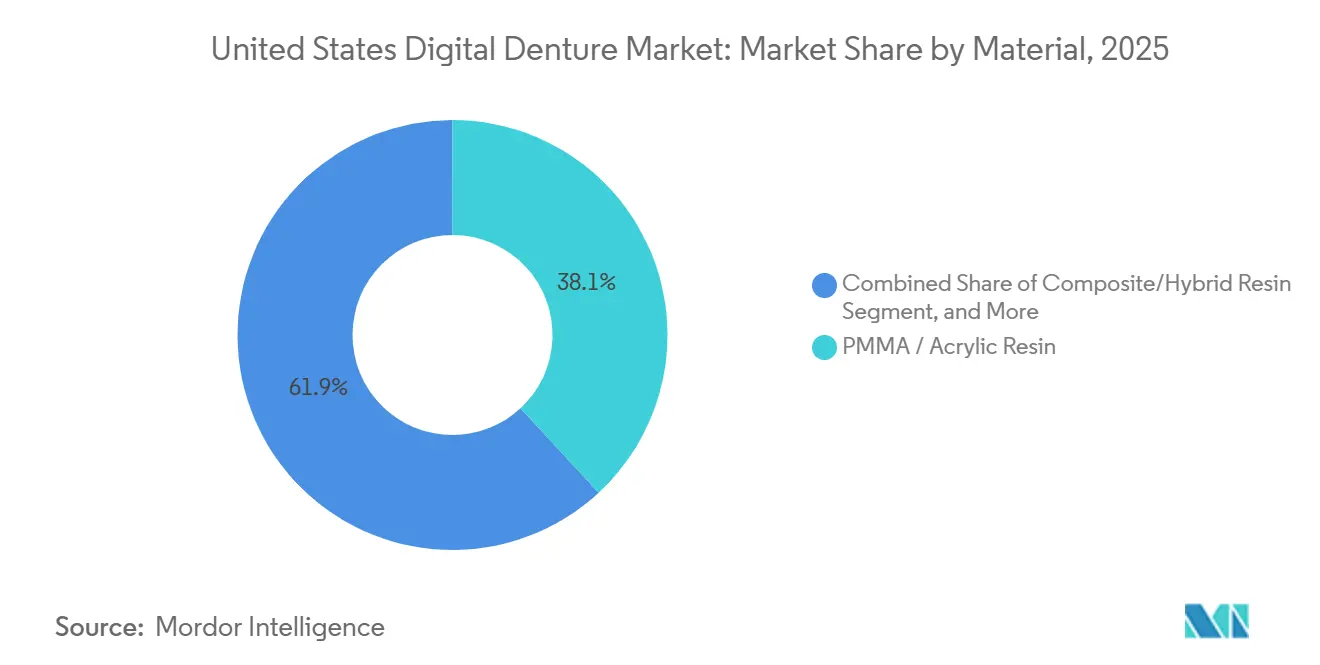

- By material, PMMA and Acrylic Resins accounted for 38.12% of the digital denture market size in 2025, while Composite and Hybrid Resins are expected to advance at an 8.79% CAGR through 2031.

- By application, Definitive Dentures represented 35.74% of revenue in 2025, while Immediate Dentures are set to grow at a 9.41% CAGR through 2031.

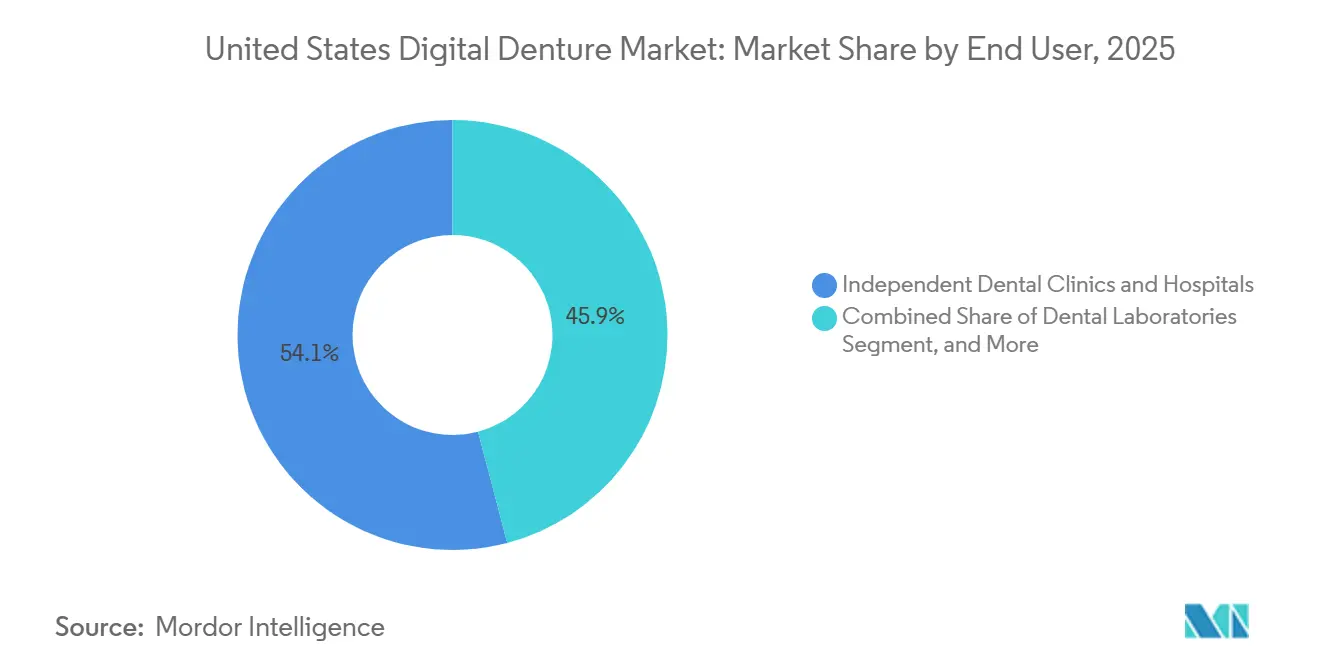

- By end user, Independent Dental Clinics and Hospitals held 54.09% of revenue in 2025, while Dental Laboratories are projected to grow at a 9.19% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Digital Denture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Edentulous Senior Base | +1.2% | National, with stronger intensity in Florida, Texas, Arizona, and southeastern states | Long term (≥ 4 years) |

| CAD/CAM and 3D Printing Adoption | +1.8% | National, led by metropolitan markets and DSO-dense corridors | Medium term (2-4 years) |

| DSO-Led Digitization and Procurement | +0.9% | National, concentrated in Southeast, Southwest, and Midwest DSO expansion zones | Short term (≤ 2 years) |

| Demand for Implant-Retained and Aesthetic Prosthetics | +0.7% | National, with premium uptake concentrated in coastal states | Medium term (2-4 years) |

| FDA-Cleared Monolithic and Antimicrobial Denture Materials | +0.6% | National | Short term (≤ 2 years) |

| Digital Archives Enable Duplicate Dentures and Fewer Visits | +0.3% | National, with early adoption in multi-location DSO networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

CAD/CAM and 3D Printing Adoption Redefines Laboratory Economics

The shift toward digital denture production has moved well beyond an early adoption phase in the U.S. laboratory base, because software-guided design and automated output now change labor use, remake rates, and turnaround times in the same workflow. Commercial laboratories are increasingly using digital case design to standardize tooth setup, preserve archived files, and reduce the variability that traditionally came from hand-built processes. Multi-material jetting is especially important because it turns the denture base and teeth into a single printed structure, which removes a manual bonding stage that often created both labor drag and quality risk. In July 2025, 3D Systems said beta customers using its NextDent 300 MultiJet platform achieved production speeds up to 300% faster than analog workflows and 120% faster than conventional 2-part printing, which shows why throughput has become a major purchase criterion.[1]3D Systems, “3D Systems Announces Major Milestone in Digital Dentistry With Full Commercial Release of New FDA-Cleared Denture Solution,” 3D Systems, 3dsystems.com At the same time, a 2025 meta-analysis in Scientific Reports found that milled PMMA denture bases still showed stronger flexural performance and hardness than many printed alternatives, which means additive workflows still depend heavily on material formulation and post-cure control to narrow the gap.[2]Amr Azab et al., “Systematic Review and Meta-Analysis of Mechanical Properties of 3D Printed Denture Bases Compared to Milled and Conventional Materials,” Scientific Reports, pmc.ncbi.nlm.nih.gov In the digital denture market, that balance between faster output and dependable mechanical performance is pushing vendors to compete on validated systems rather than on printer specifications alone.

Aging Edentulous Senior Base Provides Durable Demand Floor

The aging patient base remains the most durable source of case demand, but its importance goes beyond simple volume because it favors workflows that reduce visits, simplify remakes, and preserve design records over time. The American College of Prosthodontics states that 36 million Americans are fully edentulous, 120 million are missing at least 1 tooth, and 2.5 million Americans receive their first denture each year, which keeps the prosthetic replacement pool structurally large. The same organization also notes that 90% of fully edentulous Americans use dentures, which supports a stable installed base for relines, replacements, and duplicate prostheses.[3]American College of Prosthodontics, “Facts & Figures,” American College of Prosthodontics, prosthodontics.org This is where digital archiving becomes commercially important, because older patients, especially those with lower mobility, benefit when an exact-fit backup can be produced without repeating full impression and design steps. Research published in Frontiers in Dental Medicine in 2025 states that the U.S. population aged 65 and older is expected to reach 98 million in coming decades, while access gaps remain significant for low-income, rural, and minority seniors. For the digital denture market, that combination of aging demand and uneven access suggests long-term volume support, with the strongest upside likely where service delivery models improve convenience and affordability at the same time.

FDA-Cleared Monolithic and Antimicrobial Denture Materials Expand the Defensible Product Portfolio

Material innovation has become more defensible when it is paired with regulatory clearance, because clinicians and laboratories both place higher value on workflows that reduce liability and lower the risk of inconsistent outcomes. Between 2024 and 2025, the market saw a clear increase in clinically positioned digital denture materials, including monolithic solutions and newer antimicrobial or flexible options that expand use cases beyond standard removable appliances. In September 2024, 3D Systems received FDA clearance for its multi-material monolithic jetted denture solution, and the company followed that clearance with a full U.S. commercial release in July 2025, which gave laboratories a validated path to single-print denture production. Each such approval or clearance matters because it reduces adoption friction for clinicians who need stronger evidence on safety, repeatability, and workflow compatibility before changing treatment protocols. It also helps integrated vendors defend pricing, since validated material libraries and approved workflows are harder to replace with low-cost alternatives that lack the same documentation. In the digital denture market, this makes regulatory progress part of the product itself, not just a compliance step that sits in the background.

DSO-Led Digitization and Procurement Accelerates Technology Standardization

Dental service organizations are having an outsized effect on adoption because they do not need to change 1 practice at a time, and instead can set workflow rules, purchasing standards, and training plans across broad clinical networks. This has practical effects on the digital denture market because standardized scanners, design platforms, and laboratory partners reduce variation that otherwise slows case acceptance and remake control. Centralized procurement also improves equipment economics, since DSOs can negotiate volume terms that are not usually available to single-location clinics or small local groups. Once a network settles on 1 validated workflow, the same choice tends to shape laboratory relationships, material selection, staff onboarding, and support needs across many affiliated locations. That network effect matters because training an entire region on the same digital design environment lowers implementation friction and helps clinical teams move from physical impressions to scan-based case starts more quickly. The result is a wider operating gap between DSO-backed practices and independent operators, with the former better positioned to adopt the digital denture market at scale and the latter more exposed to capital and staffing constraints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Scanners, Printers, and Software | -1.3% | National, with disproportionate pressure in rural markets and single-operator independent practices | Short term (≤ 2 years) |

| Coverage Gaps and Out-of-Pocket Affordability | -1.0% | National, most acute in low-income Southern and Midwestern states | Long term (≥ 4 years) |

| Technician Pipeline and Digital Training Gaps | -0.7% | National, critical in mid-tier markets outside dental education hubs | Medium term (2-4 years) |

| Workflow Standardization and Material-Validation Gaps | -0.5% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Scanners, Printers, and Software Limits Independent Practice Adoption

The cost of a full digital setup still slows adoption among smaller operators, because the required investment often includes scanners, design software, printing or milling equipment, and post-processing tools rather than a single purchase. A complete chairside or laboratory system usually requires USD 50,000 to USD 150,000, which places many independent practices and smaller regional laboratories in a wait-and-see position. That cost pressure also changes market structure, because high-throughput production is more likely to concentrate within DSOs and large commercial laboratories that can spread equipment costs across a higher case count. Open-material systems and financing options are easing part of the burden, but software subscriptions, upgrade cycles, depreciation, and material validation costs still make payback harder to judge for lower-volume operators. The Osseointegration Foundation of North America has also described a broader laboratory challenge that includes a shrinking number of U.S. labs, older technician workforces, and weaker training pipelines, all of which make fresh capital commitments harder to justify. In the digital denture market, this means the economic barrier is not only the printer or scanner price itself, but also the uncertainty around staffing, volume, and the time required to build a reliable digital workflow.

Coverage Gaps and Out-Of-Pocket Affordability Suppress Clinical Conversion

Coverage limits continue to slow conversion from conventional dentures to digital options, especially for the senior population that accounts for a large share of denture needs in the United States. The Kaiser Family Foundation stated in November 2024 that traditional Medicare does not cover routine dental services such as dentures, and that recent policy expansions were limited to medically linked dental procedures rather than broad dental coverage. That leaves a large share of patients paying directly, which often shifts treatment choices toward lower-cost options even when digital workflows offer better fit management, file storage, or fewer return visits. Medicare Advantage plans do offer some dental benefits for many enrollees, but reimbursement scope and annual limits vary widely, which keeps affordability inconsistent across plans and geographies. In March 2025, Senator Bernie Sanders and Representative Lloyd Doggett introduced the Medicare Dental, Vision, and Hearing Benefit Act of 2025 to expand coverage for dentures and related procedures for 68 million beneficiaries, but passage remains uncertain. For the digital denture market, this keeps insurance reform in the position of a meaningful medium-term catalyst, but not a dependable near-term driver of immediate volume conversion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Full-Arch Digital Demand Accelerates as Population Ages

Partial Digital Dentures held 52.39% of the segment mix in 2025, while Complete Digital Dentures are projected to record the fastest growth at a 9.28% CAGR from 2026 to 2031. Partial dentures held the larger base because partial tooth loss remains the more common clinical presentation across the broad adult population that enters removable prosthetic care before full edentulism sets in. Laboratories also had a longer runway to digitize partial workflows, which gave this category an earlier commercial foundation than fully digital full-arch cases. Complete digital cases are now gaining speed because they align well with file-based design, repeatable tooth arrangement, and fewer manual production steps once the workflow is set. The 2025 expert consensus published in the International Journal of Oral Science described fully digital complete denture fabrication as clinically sound, more precise, and preferred by patients because it reduces chair time, which supports broader acceptance in routine practice.

These product lines still serve different economic roles inside the digital denture market. Partial dentures continue to anchor present revenue because they address a larger pool of partially edentulous patients and fit comfortably within existing laboratory and clinic habits. Complete dentures are expanding faster because the value of duplicate fabrication, digital storage, and full-arch efficiency becomes more visible once the full denture process is digitized from the start. Implant-Supported Overdentures sit in a more differentiated tier, since they combine removable prosthetics with implant planning and attachment-based workflows that are less exposed to basic price competition. Fixed Hybrid Full-Arch Dentures remain the highest value case type in many digital settings, and they reward laboratories that have already invested in advanced design software, guided planning, and tighter coordination with surgical teams.

By Manufacturing Route: Monolithic Jetting Challenges Photopolymerization's Installed Lead

Vat Photopolymerization 3D Printing led the route mix with 47.23% in 2025, while Material Jetting and Multi-Material Monolithic Printing are forecast to expand at a 9.92% CAGR through 2031. Vat photopolymerization led the way because SLA, DLP, and related systems had already spread across commercial laboratories, dental schools, and many digital prosthetic workflows before newer monolithic options reached full commercial readiness. Within this route, faster plate throughput and lower energy cost per arch are making DLP and LCD-style production more practical for mid-tier laboratories that need reliable volume without the capital profile of more advanced systems. Subtractive milling still keeps a meaningful role because mechanical performance remains a major concern in definitive prosthetics and premium applications. The 2025 Scientific Reports review found that milled PMMA bases delivered stronger flexural performance, better hardness, and stronger dimensional consistency than many 3D-printed alternatives, which continues to support milling in accuracy-sensitive cases.

The fastest momentum is now shifting toward monolithic output, which is why this part of the digital denture market is drawing so much attention from equipment suppliers. 3D Systems said its NextDent 300 MultiJet platform delivered production gains of up to 300% over analog workflows and 120% over conventional 2-part printing in beta settings, largely because it removes the bonding step between base and teeth. Hybrid print-and-bond workflows remain important during this transition because they let laboratories use digital production in stages without retiring existing equipment too quickly. That matters for operators who want better turnaround and workflow digitization but still need to manage capital exposure carefully. FDA 510(k) clearance also remains central across route choices, because it reduces the compliance risk that laboratories and clinicians weigh when choosing between a familiar system and a newer one.

By Material: Composite Resins Challenge PMMA's Incumbency on Performance and Innovation Rate

PMMA and Acrylic Resins retained the largest material position at 38.12% in 2025, while Composite and Hybrid Resins are projected to grow at an 8.79% CAGR during 2026 to 2031. PMMA kept the lead because it has decades of clinical use, established cost expectations, and compatibility with both milled and printed denture workflows. It also benefits from a large body of performance data, which makes it easier for laboratories and clinicians to compare outcomes and stay within familiar treatment standards. Composite and hybrid formulations are moving faster because they promise stronger aging resistance, better esthetic behavior, and material performance that better suits the needs of printed prosthetics. In the digital denture market, chemistry is a more important competitive lever than it was when hardware differences alone dominated supplier messaging.

The category is also becoming more layered as use cases diversify across the digital denture industry. Flexible nylon and polyamide materials continue to serve patients who want metal-free partials or who have specific comfort and esthetic preferences, though this sub-segment has digitized more slowly than rigid base materials. Metal-supported frameworks still matter in overdenture and fixed hybrid applications where structural rigidity and implant compatibility remain essential. The broader development path is visible in published materials research, since a 2025 Cellulose review reported that cellulose-nanoparticle-reinforced PMMA composites showed clear gains in impact resistance and flexural modulus across 28 in vitro studies. That type of work suggests the future balance between milling and printing will depend not only on machine speed, but also on how fast resin and composite systems improve on durability, comfort, and long-term clinical stability.

By Application: Immediate Dentures and Duplicate Workflows Redefine Service Offerings

Definitive Dentures held the largest application share at 35.74% in 2025, while Immediate Dentures are forecast to rise at a 9.41% CAGR from 2026 to 2031. Definitive cases remain the volume anchor because they are the core replacement prosthetic for both fully and partially edentulous patients across routine restorative care. Digital workflows improve this application by supporting better occlusal planning, more consistent esthetic customization, and stronger record retention for future adjustments or remakes. Immediate dentures are expanding faster because pre-surgical scanning and design let clinicians prepare prostheses before extraction or implant visits, which shortens the time between surgery and restoration. A 2025 case report in Prosthesis showed that fully digital immediate-loading workflows can use pre-surgical intraoral scans to support same-day provisional delivery, which helps explain the stronger growth rate of this category.

Duplicate and backup dentures are becoming more commercially important than their current size alone suggests. Once a patient has moved through a digital workflow, a stored file makes it far easier to reproduce an exact-fit backup without restarting the process from the beginning. This matters especially for frail seniors, homebound patients, and institutional settings where repeat visits are more difficult, and prosthesis loss creates immediate quality-of-life issues. Try-in and provisional dentures are also changing, because higher-performance printable materials are narrowing the old separation between trial appliances and definitive prosthetics. The digital denture industry, therefore, gains not only from new patient starts but also from the added service layers that digital storage, faster reproduction, and better printable materials make possible

By End User: Independent Clinics Lead Volume While Laboratories Drive Technology Advancement

Independent Dental Clinics and Hospitals held 54.09% of the demand in 2025, while Dental Laboratories are projected to expand at a 9.19% CAGR through 2031. Clinics and hospitals remain the largest end-user group because they are the point where patient diagnosis, scanning, extraction planning, and treatment acceptance occur. In many cases, however, these providers act more as scan-originators and care coordinators than as the final production site, since fabrication continues to move toward specialized laboratories. This leaves the digital denture market with a split operating model, where clinical demand is widely distributed but manufacturing capability is becoming more concentrated. DSOs and group practices still matter disproportionately because centralized procurement can shape scanner choice, laboratory partnerships, and platform selection across many locations at once.

Dental Laboratories are growing faster because automation directly addresses one of the hardest structural issues in the digital denture industry, which is a shortage of trained technicians alongside rising case complexity. As enrollment weakens in parts of the dental technology training pipeline, laboratories have a stronger reason to replace manual steps with digital design, standardized nesting, automated production, and archived case management. Academic and hospital-affiliated centers hold a smaller current share, but they influence adoption by generating the clinical evidence that practitioners and payers use when evaluating newer methods. The 2025 expert consensus on digital complete dentures in the International Journal of Oral Science is one example of how institutional research supports broader acceptance of fully digital workflows. A 2026 randomized clinical trial in Scientific Reports comparing CAD/CAM milled and 3D-printed implant-assisted mandibular overdentures adds to that evidence base and shows how institutional validation continues to shape equipment and workflow choices.

Geography Analysis

The digital denture market in the United States remains concentrated in geographies where aging demographics, laboratory density, and organized dental networks overlap most clearly. The Sun Belt, especially Florida, Texas, Arizona, and the Carolinas, stands out as the strongest demand corridor because senior population density is high and multi-location dental groups have expanded rapidly across these states. The U.S. Census Bureau projects that the 65+ population will continue rising, and Florida remains one of the most senior-heavy states in the country, which reinforces the region's role in removable prosthetic demand. These same markets also support faster workflow deployment because DSO activity and commercial laboratory infrastructure make it easier to standardize scanners, design files, and fabrication partnerships across many practices. States with very high edentulism rates, including West Virginia, Kentucky, and Arkansas, offer clear volume potential, although lower affordability and thinner commercial lab networks still limit the pace of premium digital conversion in some of these areas.

The Northeast corridor remains the premium tier within the digital denture market because household income, specialist density, and more complex restorative case demand are stronger than in many lower-cost regions. New York, New Jersey, Connecticut, and Pennsylvania support more implant-retained and fixed hybrid demand, which raises per-case revenue and favors providers with advanced design and planning capability. Academic and hospital-linked centers in Boston, New York, and Philadelphia also matter because they help validate protocols that later diffuse into routine commercial use. The West Coast, especially Southern California, shows a similar premium profile and adds deep commercial laboratory and innovation capacity. Regional clustering around large dental manufacturers, major laboratories, and software-driven workflow companies supports faster testing, adoption, and refinement of digital denture production methods.

Midwestern and rural geographies remain the hardest areas to penetrate, even though they offer a meaningful long-term opportunity if access barriers continue to ease. These regions often have more single-chair practices, fewer digitally trained technicians, and a stronger reliance on Medicare patients who are directly affected by denture coverage gaps. The Kaiser Family Foundation stated in 2024 that traditional Medicare does not cover routine dentures, which continues to weigh on treatment conversion in these settings. Remote design support and cloud-based prosthetic planning are beginning to reduce the skill gap by allowing clinics to originate scans without maintaining the same level of in-house design expertise. As those support models scale between 2026 and 2031, geographic barriers in underserved Midwestern and rural markets are likely to loosen, even if they do not disappear completely.

Competitive Landscape

The digital denture market covers linked competitive layers, large platform vendors that sell integrated hardware, software, and validated materials, and specialized denture design or fabrication companies that compete on execution, flexibility, and case-specific expertise. Dentsply Sirona, 3D Systems, and Straumann are among the most visible integrated names, while Glidewell, AvaDent, SprintRay, and DENTCA add competitive pressure through narrower workflow strengths or lower-cost access points. This keeps concentration moderate rather than high, because large suppliers do shape standards, but the operating field still includes several equipment makers, software ecosystems, laboratories, and specialist service providers. One important battleground is software interoperability, since dental CAD platforms often determine which printers, materials, and design libraries fit most smoothly into day-to-day lab production. Vendors that can secure validated compatibility and consistent workflow performance are better placed to hold recurring materials revenue over time.

Recent company moves show how competition is being built around workflow control rather than around a single device. In July 2025, 3D Systems commercially released its FDA-cleared NextDent jetted denture solution in the United States, which strengthened its position in monolithic multi-material production and highlighted speed as a key selling point. Straumann's 2024 annual report also emphasized an integrated digital strategy that links the SIRIOS intraoral scanner, coDiagnostiX planning software, and prosthetic services through its AXS platform, which shows how major vendors are trying to keep more of the workflow inside a connected ecosystem. Dentsply Sirona adds another competitive advantage through scale, since the company reports Q1 2026 net sales of USD 945 million with growth centered in CAD/CAM and digital dentistry, giving it more room to invest in clinical education, material validation, and distribution depth. Smaller challengers continue to compete on lower equipment cost, simpler adoption, and open-material positioning, which helps prevent the market from tightening too quickly around only 1 or 2 closed systems.

White space remains visible where digital methods are still becoming established. Flexible partial dentures and immediate-load hybrid workflows still offer room for suppliers that can solve material performance, design labor, and clinic-to-lab coordination more effectively than current options. Design automation is also becoming a sharper point of competition because once print speed improves, labor in tooth setup and case design becomes the next major cost bottleneck. Patent-protected geometries, validated resin libraries, and FDA-backed workflows therefore matter as both quality markers and practical barriers to entry. That combination explains why the digital denture market remains open enough for new entrants to matter, but structured enough that established platform companies still hold the strongest leverage over standards and repeat consumables revenue.

United States Digital Denture Industry Leaders

3D Systems, Inc.

Straumann Group

Ivoclar Vivadent AG

Dentsply Sirona Inc.

Dentsply Sirona Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Roland DGA Corporation has announced the launch of the Elevate Denture Solution, a patent‑protected digital denture kit designed to enable repeatable and accurate denture fabrication for dental laboratories, denturists, and clinicians. Developed in partnership with Ivoclar and FOLLOW‑ME! Technology North America, the solution integrates milling equipment, restorative materials, and CAM software into a streamlined workflow. The system emphasizes precision and consistency, supporting scalable production and advancing digital denture adoption across the dental industry.

- July 2025: 3D Systems announced the full commercial release of its FDA-cleared NextDent Jetted Denture Solution for the US market on July 29, 2025. The solution, the first commercially available monolithic, multi-material jetted denture system, uses the NextDent 300 MultiJet 3D printer and reported up to 300% faster production versus analog workflows in beta deployment.

- March 2025: Senator Bernie Sanders and Representative Lloyd Doggett introduced the Medicare Dental, Vision, and Hearing Benefit Act of 2025 (H.R. 2045), proposing expansion of Medicare to cover dentures, dental cleanings, fillings, and other procedures for 68 million American Medicare beneficiaries.

United States Digital Denture Market Report Scope

The digital Denture Market encompasses the global industry focused on designing, producing, and supplying dental prosthetics using advanced digital technologies like CAD/CAM, 3D printing, and AI-driven workflows, rather than traditional manual casting and molding methods.

The United States digital denture market report, presented in terms of value (USD), is segmented across several dimensions that define its scope and growth trajectory. By product type, the market includes complete dentures, partial dentures, implant‑supported dentures, and fixed hybrid solutions. In terms of manufacturing route, production methods encompass milling, vat photopolymerization, material jetting, and hybrid approaches. From a material perspective, key categories include PMMA/acrylic, composite and hybrid materials, flexible nylon, and metal frameworks. By application, digital dentures are used for definitive cases, immediate dentures, duplicates, and try‑in models. Finally, by end user, adoption spans dental laboratories, clinics, dental service organizations (DSOs), and academic centers.

| Complete Digital Dentures |

| Partial Digital Dentures |

| Implant-Supported Overdentures |

| Fixed Hybrid Full-Arch Dentures |

| Subtractive Milling | |

| Vat Photopolymerization 3D Printing | SLA-Based Workflows |

| DLP / LCD-Based Workflows | |

| Material Jetting / Multi-Material Monolithic Printing | |

| Hybrid Print-And-Bond Workflows |

| PMMA / Acrylic Resin |

| Composite / Hybrid Resin |

| Flexible Nylon / Polyamide |

| Metal-Supported Frameworks |

| Definitive Dentures |

| Immediate Dentures |

| Duplicate / Backup Dentures |

| Try-In and Provisional Dentures |

| Dental Laboratories |

| Independent Dental Clinics and Hospitals |

| DSOs And Group Practices |

| Academic and Hospital-Affiliated Centers |

| By Product Type | Complete Digital Dentures | |

| Partial Digital Dentures | ||

| Implant-Supported Overdentures | ||

| Fixed Hybrid Full-Arch Dentures | ||

| By Manufacturing Route | Subtractive Milling | |

| Vat Photopolymerization 3D Printing | SLA-Based Workflows | |

| DLP / LCD-Based Workflows | ||

| Material Jetting / Multi-Material Monolithic Printing | ||

| Hybrid Print-And-Bond Workflows | ||

| By Material | PMMA / Acrylic Resin | |

| Composite / Hybrid Resin | ||

| Flexible Nylon / Polyamide | ||

| Metal-Supported Frameworks | ||

| By Application | Definitive Dentures | |

| Immediate Dentures | ||

| Duplicate / Backup Dentures | ||

| Try-In and Provisional Dentures | ||

| By End User | Dental Laboratories | |

| Independent Dental Clinics and Hospitals | ||

| DSOs And Group Practices | ||

| Academic and Hospital-Affiliated Centers | ||

Key Questions Answered in the Report

What is the projected value of the United States digital denture space by 2031?

It is projected to reach USD 747.76 million by 2031, up from USD 516.13 million in 2025, at a 6.47% CAGR over 2026 to 2031.

Which product category is expanding the fastest?

Complete Digital Dentures are forecast to grow the fastest, with a 9.28% CAGR through 2031, while Partial Digital Dentures remained the largest category in 2025.

Which manufacturing route currently leads adoption?

Vat Photopolymerization 3D Printing led in 2025 with 47.23% of revenue, reflecting its broad installed base across laboratories and digital workflows.

Why are dental laboratories growing faster than clinics in this field?

Dental Laboratories are projected to grow at 9.19% CAGR because they are investing in automation to offset technician shortages and improve throughput.

How does Medicare policy affect denture adoption in the United States?

Traditional Medicare still excludes routine denture coverage, which keeps out-of-pocket costs high and slows conversion to higher-value digital options.

Page last updated on: