United States Digestive Health Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

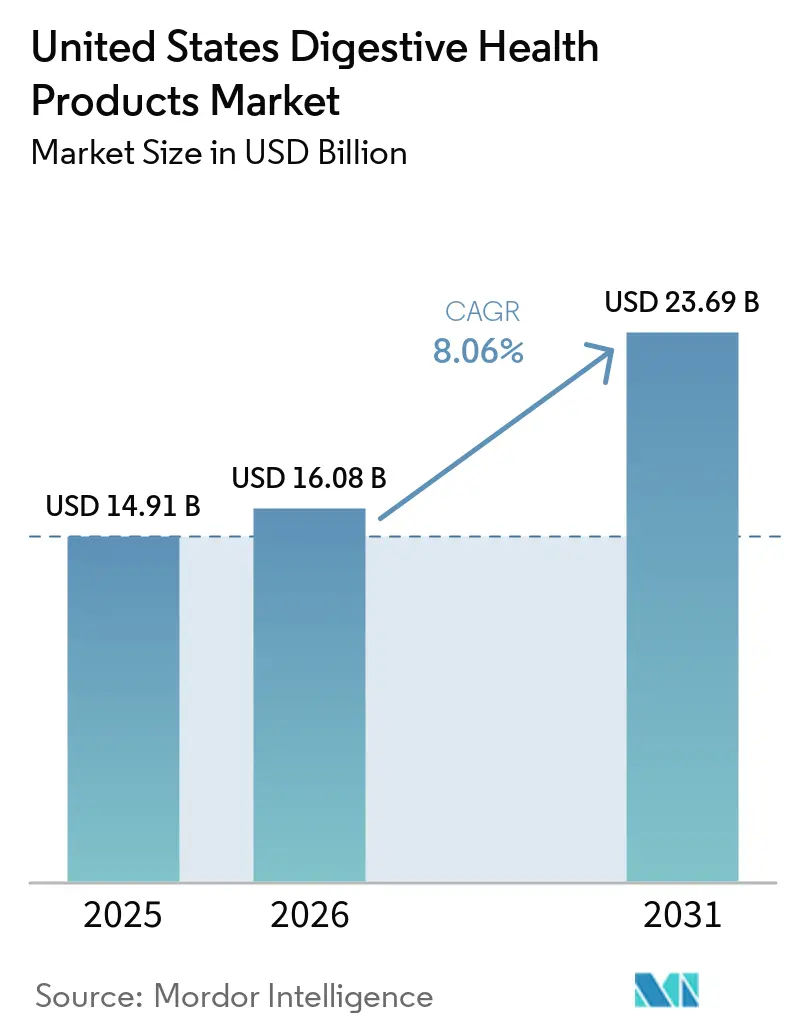

| Base Year Market Size (2025) | USD 14.91 Billion |

| Market Size (2026) | USD 16.08 Billion |

| Market Size (2031) | USD 23.69 Billion |

| Growth Rate (2026 - 2031) | 8.06% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Digestive Health Products Market Analysis by Mordor Intelligence

The United States digestive health products market was valued at USD 14.91 billion in 2025 and is projected to grow from USD 16.08 billion in 2026 to reach USD 23.69 billion by 2031, registering a CAGR of 8.06% during the forecast period from 2026 to 2031. This market is shifting from focusing solely on symptom relief to offering products that promote daily gut health. Consumers are increasingly turning to foods, beverages, and supplements to proactively maintain digestive wellness, rather than waiting for specific digestive issues to arise. Advancements in microbiome science are providing stronger scientific backing for products like probiotics, synbiotics, and similar formulations. This evidence is helping brands that prioritize science-based approaches to maintain premium pricing and build consumer trust. The competitive landscape is also changing. Traditional retail players are leveraging their large-scale shelf presence to maintain dominance, while direct-to-consumer brands are focusing on subscription models, consumer education, and unique product formulations to foster customer loyalty. Businesses that invest in advanced delivery technologies and establish clear brand credibility are likely to gain a competitive edge in this evolving market.

Key Report Takeaways

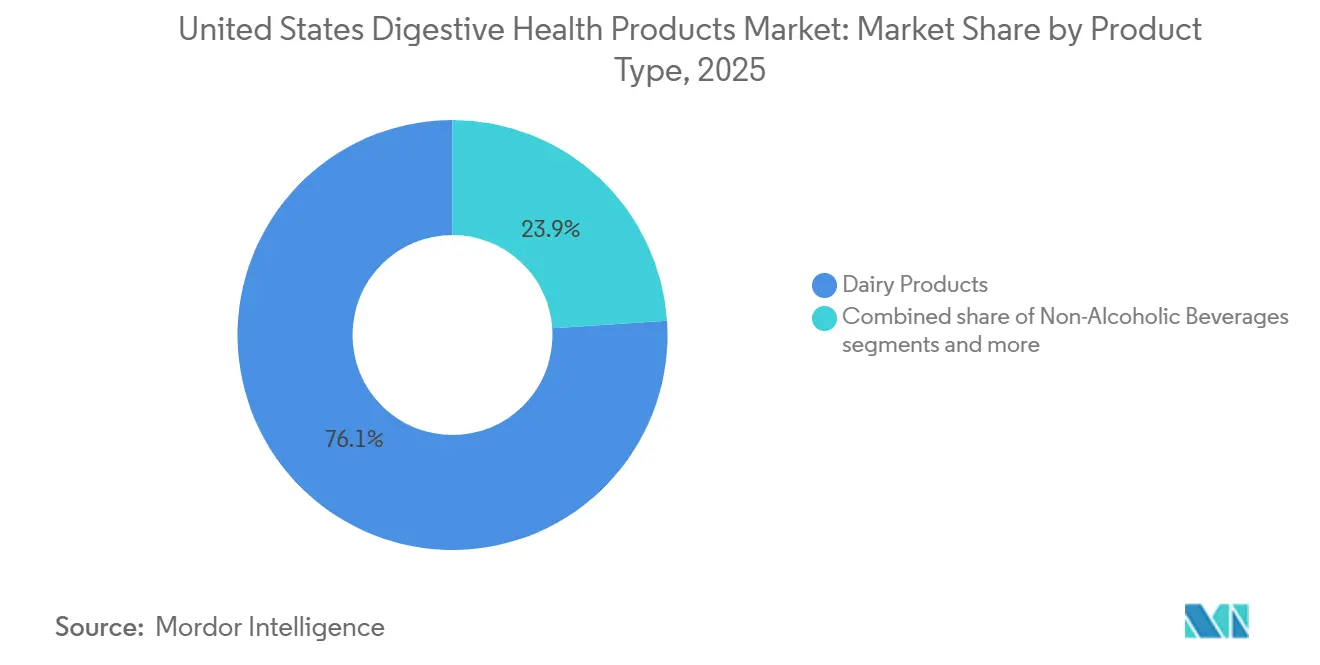

- By product type, dairy products held 76.06% share in 2025, while non-alcoholic beverages are projected to record the fastest growth at a 9.27% CAGR through 2031.

- By ingredient type, probiotics accounted for 88.15% share in 2025, while food enzymes are expected to expand at a 9.16% CAGR through 2031.

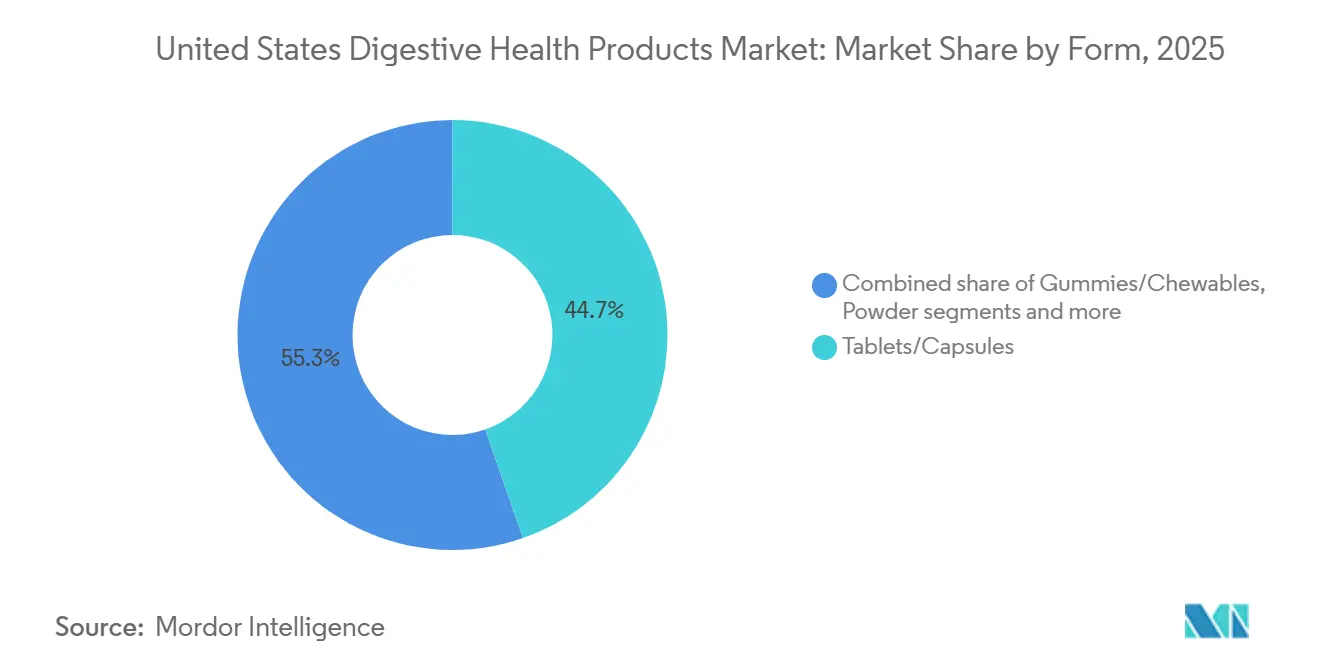

- By form, tablets and capsules represented 44.68% share in 2025, while gummies and chewables are forecast to grow at a 10.68% CAGR through 2031.

- By end user, adults captured 82.71% share in 2025, while the kids segment is projected to advance at an 8.84% CAGR through 2031.

- By distribution channel, supermarkets/hypermarkets held 43.67% share in 2025, while online retail stores are expected to grow at a 10.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Digestive Health Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of digestive disorders and gastrointestinal health concerns | +2.2% | National, with highest burden in the South and Northeast | Short term (≤ 2 years) |

| Growth in functional foods and beverages with digestive health benefits | +1.8% | National, with early adoption concentrated on the West Coast and Northeast urban markets | Medium term (2–4 years) |

| Expanding adoption of probiotics, prebiotics, and microbiome-supporting products | +1.5% | National, with strongest uptake in metropolitan health-conscious markets | Medium term (2–4 years) |

| Increasing consumer interest in holistic approaches to health and wellness | +0.9% | National, particularly strong among Gen Z and Millennials in urban and suburban markets | Long term (≥ 4 years) |

| Expansion of clean-label and natural ingredient trends in digestive health formulations | +0.8% | West Coast, Northeast; growing in Southeast | Medium term (2–4 years) |

| Increasing launches of plant-based probiotic and digestive health products | +0.7% | West Coast–led, with national e-commerce distribution | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Prevalence of digestive disorders and gastrointestinal health concerns

The digestive health products market in the United States is growing steadily, driven by the increasing number of people facing gastrointestinal (GI) issues. A survey conducted by Educated Patient in March 2026 revealed that half of Americans (50%) either have a diagnosed GI condition or suspect they may have one, underscoring significant demand for digestive health solutions[1]Source: Educated Patient, "Half of Americans Have Gut Issues (And Most Think That's Just Normal)", theeducatedpatient.com. Additionally, 52% of Americans view common digestive problems like bloating, constipation, and irregular bowel movements as a normal part of life, which points to a gap in awareness and preventive care. This growing awareness of digestive health has led to increased use of products such as probiotics, prebiotics, fiber supplements, digestive enzymes, and functional foods. Consumers are increasingly incorporating these products into their daily routines to address digestive issues and improve overall gut health.

Growth in functional foods and beverages with digestive health benefits

The digestive health products market in the United States is witnessing significant growth as consumers increasingly prioritize gut health as part of their overall wellness. People are now looking for convenient options like probiotic yogurts, fiber-enriched snacks, digestive wellness beverages, and gut-health supplements that can be easily incorporated into their daily routines rather than being used only when digestive issues occur. This shift is particularly evident among younger and health-conscious individuals who prefer preventive measures to maintain their well-being. Manufacturers are responding to this demand by introducing innovative products, such as Nature Made's SuperGreens and Digestive Enzymes, Pendulum Therapeutics' Gut Fuel powder, and Reckitt's Dulcolax Daily Digestive Wellness range, which go beyond traditional supplements to offer more diverse and accessible solutions for digestive health.

Expanding adoption of probiotics, prebiotics, and microbiome-supporting products

Microbiome-focused products are playing a significant role in driving the growth of the United States digestive health products market. Consumers are increasingly incorporating probiotics and prebiotics into their daily routines to enhance digestion, maintain gut health, boost immunity, and improve overall well-being. A 2025 report by the International Microbiota Observatory found that 53% of Americans use probiotics and 44% use prebiotics, surpassing global averages of 49% and 41%, respectively[2]Source: International Microbiota Observatory, "United States 2025: Knowledge And Behaviors About Microbiota", biocodexmicrobiotainstitute.com. This trend reflects a growing awareness among United States consumers about the importance of gut health and the benefits of maintaining a balanced microbiome. To meet this rising demand, manufacturers are actively expanding their product offerings with innovative formulations, including probiotics, prebiotics, and synbiotics, which is further fueling the market's growth and solidifying its position in the health and wellness sector.

Increasing launches of plant-based probiotic and digestive health products

The growing popularity of vegetarian and vegan lifestyles in the United States is driving significant demand for plant-based digestive health products. As reported by the Vegan Resource Group in August 2025, around 8–10 million United States adults identify as vegetarian, including vegans, and approximately 13 million Americans regularly consume vegan meals[3]Source: Vegan Resource Group, "How Many Vegetarians And Vegans Are There In The United States?", vrg.org. This shift in dietary preferences has led consumers to seek digestive health solutions that align with plant-based diets, such as dairy-free probiotics, plant-based digestive enzymes, fiber supplements, and clean-label gut health products. To meet this demand, manufacturers are developing innovative products tailored to vegan and vegetarian needs, focusing on natural ingredients and clear labeling. As plant-based eating becomes increasingly mainstream, demand for digestive health products tailored to these lifestyles is expected to play a key role in driving growth in the United States digestive health products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High product costs compared to conventional dietary supplements and food products | -1.2% | National, with pronounced sensitivity in rural markets and lower-income demographic segments | Short term (≤ 2 years) |

| Stringent regulatory requirements governing health claims and product labeling | -0.9% | National; applies uniformly under Food and Drug Administration jurisdiction | Medium term (2–4 years) |

| Increasing competition from traditional and natural digestive remedies | -0.6% | South and Midwest, where traditional herbal and home remedies retain cultural traction | Medium term (2–4 years) |

| Consumer skepticism regarding the effectiveness of digestive health supplements | -0.5% | National, particularly among older and less health-engaged demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High product costs compared to conventional dietary supplements and food products

The high prices of many digestive health products are a significant challenge for the United States' digestive health products market. Products like premium probiotics, digestive enzymes, synbiotics, and advanced gut health formulations are often much more expensive than regular dietary supplements. This is mainly due to the use of clinically tested ingredients, proprietary strains, and complex formulations. While some health-conscious consumers are willing to pay extra for these benefits, many price-sensitive households find it difficult to afford these products regularly. Additionally, since these products are usually purchased out of pocket and not covered by insurance, cost is a major factor in buying decisions. As a result, high prices limit the market's reach, making it harder for these products to gain widespread adoption among a broader range of consumers.

Stringent regulatory requirements governing health claims and product labeling

Regulatory restrictions on health claims pose a major challenge for the digestive health products market in the United States. Manufacturers are allowed to highlight general digestive wellness benefits through structure-function claims, but they cannot make claims about treating or preventing diseases without going through a lengthy and costly regulatory approval process. This limits their ability to clearly communicate the proven clinical benefits of products like probiotics, prebiotics, and digestive enzymes, even when backed by scientific research. As a result, consumers often struggle to assess the effectiveness of these products, which can erode trust and affect purchasing decisions. Additionally, companies, especially smaller ones, face higher compliance costs as regulations change, which can slow innovation and make it harder for them to compete in an already crowded market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dairy Dominates, but Beverages Rewrite the Growth Narrative

In 2025, dairy products made up 76.06% of the United States digestive health products market, making them the largest segment. This is because products such as yogurt, kefir, cultured milk drinks, and fermented dairy products are widely consumed for their probiotic benefits. These products are seen as an easy way to improve gut health and digestion as part of daily diets. Their strong presence in retail stores, high consumer trust, and ongoing innovations by major dairy companies have helped maintain their leading position in the market.

Non-alcoholic beverages are expected to grow the fastest among all product segments, with a projected CAGR of 9.27% from 2026 to 2031. This growth is driven by the rising demand for functional drinks that support digestive health in convenient, ready-to-drink formats. Companies are introducing products like probiotic beverages, kombucha, wellness shots, and fiber-enriched drinks to meet the needs of health-conscious consumers. Increasing awareness of gut health and a growing preference for preventive health solutions are key factors expected to drive this segment's expansion during the forecast period.

By Ingredient Type: Probiotic Supremacy Masks an Enzyme-Led Disruption

Probiotics were the leading ingredient type in the United States digestive health products market, accounting for 88.15% of total revenue in 2025. This dominance is due to increasing consumer awareness about the benefits of probiotics in maintaining a healthy gut microbiome, improving digestion, and supporting overall health. Probiotics are commonly used in dietary supplements, dairy products, functional foods, and beverages, making them a key component in digestive health products. Ongoing research and the availability of specialized probiotic strains have further boosted their popularity among consumers.

Food enzymes are projected to be the fastest-growing ingredient segment, with a CAGR of 9.16% during 2026–2031. The rising demand for products that aid the digestion of proteins, carbohydrates, fats, and lactose is driving this growth. Food enzymes are increasingly included in supplements and functional foods to address digestive issues and enhance nutrient absorption. Moreover, the growing interest in personalized nutrition and digestive health solutions is expected to further increase the adoption of enzyme-based products during the forecast period.

By Form: The Gummy Transition Reflects a Broader Supplement-to-Lifestyle Shift

Tablets and capsules made up 44.68% of the United States digestive health products market by form in 2025, making them the most popular choice. Their widespread use is due to their ease of consumption, accurate dosage, long shelf life, and familiarity among consumers. These formats are commonly used for delivering probiotics, prebiotics, digestive enzymes, and other supplements that support digestive health. Their affordability and availability in various retail outlets, including pharmacies, supermarkets, and online platforms, have helped maintain their leading position in the market.

Gummies and chewables are expected to grow the fastest among all forms, with a projected CAGR of 10.68% during 2026–2031. This growth is driven by the increasing demand for supplements that are easy and enjoyable to consume, especially among younger consumers and those who find it difficult to swallow pills. Gummies and chewables offer a fun, convenient alternative to traditional tablets and capsules. Manufacturers are also introducing a wider range of products, including gummies with probiotics, prebiotics, and digestive enzymes, which is further boosting the popularity of this segment during the forecast period.

By End User: Adults Drive Volume, but the Pediatric Segment Offers the Highest Long-Term Value

In 2025, adults made up 82.71% of the United States digestive health products market, making them the largest consumer group. This dominance is due to growing awareness of digestive health, rising rates of gastrointestinal disorders, and a shift toward preventive healthcare among adults. Products like probiotics, digestive enzymes, and fiber supplements are in high demand as they help improve gut health, boost immunity, and enhance overall wellness. The fast-paced lifestyles and changing dietary habits of adults have further fueled demand for these products.

The kids' segment is expected to grow at a CAGR of 8.84% during the 2026–2031 period. This growth is driven by parents becoming more aware of the importance of maintaining their children's digestive health and gut microbiome from an early age. To meet this demand, manufacturers are introducing kid-friendly options such as gummies, chewable tablets, and flavored probiotic supplements that are easier for children to consume. Concerns about digestive issues, immunity, and overall health in children are likely to continue driving the demand for digestive health products throughout the forecast period.

By Distribution Channel: Physical Retail Anchors Volume, Digital Channels Capture Value

In 2025, supermarkets and hypermarkets were the largest distribution channels for digestive health products in the United States, accounting for 43.67% of market share. These stores attract consumers by offering a wide variety of products, including probiotics, functional foods, beverages, and dietary supplements, all in one convenient location. Their strong brand presence and frequent promotional campaigns make them a preferred choice for shoppers. Their widespread availability across different regions ensures easy access for consumers, further solidifying their leading position in the market.

Online retail stores are expected to grow the fastest, with a projected CAGR of 10.56% from 2026 to 2031. This growth is fueled by the increasing preference for convenient shopping, where consumers can browse and purchase products from the comfort of their homes. Online platforms also provide detailed product information and customer reviews, helping buyers make informed decisions. The rise of e-commerce platforms and subscription-based wellness services has made digestive health products more accessible. Furthermore, the growing adoption of digital technologies and the demand for personalized health solutions are likely to drive continued expansion in online sales during the forecast period.

Geography Analysis

The South is the largest market for digestive health products in the United States. This is due to its large population, high rates of digestive health issues, and well-established retail networks. States like Texas play a major role in driving demand, supported by population growth and rising interest in products such as probiotics, prebiotics, and digestive enzymes. The region is a key manufacturing hub, providing a strong base for dietary supplements and functional foods. Growing consumer health awareness further solidifies the South’s leading position in this market.

The West is expected to grow the fastest among all regions, driven by rising interest in preventive healthcare and clean-label, plant-based digestive health products. States such as California are at the forefront, with consumers quickly adopting innovative solutions like dairy-free probiotics, microbiome-focused supplements, and functional beverages. For instance, in January 2026, Nature Made introduced a new line of digestive health products, including probiotics and fiber-based options, to meet the increasing demand for personalized gut health solutions. The West remains a hub of innovation in digestive health products and formats.

The Northeast and Midwest are also important markets for digestive health products in the United States. The Northeast benefits from high consumer awareness, strong pharmacy networks, and demand for premium, science-backed products, which supports the growth of trusted brands. In the Midwest, the adoption of digestive health solutions is increasing as e-commerce improves access and consumer education grows. Familiarity with probiotics and functional nutrition products is steadily rising, which is expected to drive consistent market growth in both regions during the forecast period.

Competitive Landscape

The United States digestive health products market is dominated by several major players, including Nestlé S.A., Danone S.A., Abbott Laboratories, The Procter & Gamble Company, and Reckitt Benckiser Group plc. These companies offer a wide range of products, including probiotics, digestive supplements, functional foods, and wellness solutions. Their strong brand reputation, extensive distribution networks, and partnerships with retailers help them maintain a significant market presence. However, the market remains competitive, as no single company has complete control, allowing opportunities for other players to grow.

Innovation and product variety are key factors driving competition in this market. Companies are investing in research and development to introduce advanced products like probiotics, prebiotics, postbiotics, and digestive enzymes. Many brands are also focusing on creating solutions that address specific digestive health concerns while ensuring convenience and effectiveness for consumers. This focus on innovation enables companies to stand out in a market that is becoming increasingly crowded with options, offering consumers more choices tailored to their needs.

The competitive landscape is constantly changing as both established companies and smaller, specialized brands work to expand their offerings. Increasing consumer demand for preventive healthcare, personalized nutrition, and clean-label products is pushing companies to diversify their product lines and improve their expertise in digestive health. To remain competitive, businesses are prioritizing investments in new ingredient technologies, product development, and consumer education. As a result, the market is expected to stay dynamic, with strong competition across both mainstream and premium product categories.

United States Digestive Health Products Industry Leaders

-

Nestlé S.A.

-

Abbott Laboratories

-

Danone S.A.

-

The Procter & Gamble Company

-

Reckitt Benckiser Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Dulcolax introduced a new Daily Digestive Wellness range to expand its digestive health product offerings in the United States. This range was designed to support regular gut health and improve daily digestion.

- March 2026: Nature Made introduced new products to its gut health range in the United States, including SuperGreens Powder, SuperGreens Capsules, and Digestive Enzymes. These products were designed to support digestion, boost energy, enhance immune health, and improve overall wellness.

- March 2026: Pendulum Therapeutics introduced Gut Fuel, a prebiotic fiber and polyphenol powder designed to support gut health, digestion, and metabolism in the United States. This product addressed the rising demand for digestive health solutions that support regularity, healthy blood sugar levels, and overall gut wellness.

- August 2025: Nature Made added new products to its digestive health range in the United States, including Probiotic + Prebiotic Fiber Gummies and Probiotics 1 Billion CFU Capsules. These products were designed to support digestion and immune health, meeting the growing demand for science-backed gut health solutions.

United States Digestive Health Products Market Report Scope

Digestive health products include foods, beverages, supplements, and functional ingredients designed to enhance gastrointestinal function, aid digestion, maintain gut microbiota balance, and support overall digestive health. The United States Digestive Health Products market comprises product type, ingredient type, form, end user, and distribution channel. Based on product type, the market is segmented into dairy products, bakery products, cereals, non-alcoholic beverages, and others. Based on ingredient type, the market is classified into probiotics, prebiotics, food enzymes, and others. Based on form, the market is classified into tablets/capsules, powder, gummies/chewables, and others. Based on end user, the market is classified into adults and kids. Based on distribution channel, the market is classified into supermarkets/hypermarkets, drugstores and pharmacies, online retail stores, and other distribution channels. The market forecasts are provided in terms of value (USD).

| Dairy Products |

| Bakery Products and Cereals |

| Non-Alcoholic Beverages |

| Others |

| Probiotics |

| Prebiotics |

| Food Enzymes |

| Others |

| Tablets/Capsules |

| Powder |

| Gummies/Chewables |

| Others |

| Adults |

| Kids |

| Supermarkets/Hypermarkets |

| Drugstores and Pharmacies |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Dairy Products |

| Bakery Products and Cereals | |

| Non-Alcoholic Beverages | |

| Others | |

| By Ingredient Type | Probiotics |

| Prebiotics | |

| Food Enzymes | |

| Others | |

| By Form | Tablets/Capsules |

| Powder | |

| Gummies/Chewables | |

| Others | |

| By End User | Adults |

| Kids | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Drugstores and Pharmacies | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the 2026 outlook for digestive health products in the United States?

The United States digestive health products market is estimated at USD 16.08 billion in 2026 and is forecast to reach USD 23.69 billion by 2031, projected to grow at an 8.06% CAGR.

Which product segment leads digestive health sales in the United States?

Dairy products lead by product type with 76.06% share in 2025, supported by long-standing consumer trust in yogurt and kefir-based digestive wellness formats.

Which product area is growing fastest through 2031?

Non-alcoholic beverages are the fastest-growing product segment, with a projected 9.27% CAGR, as digestive support becomes part of everyday beverage consumption.

Why do probiotics still dominate ingredient demand?

Probiotics held 88.15% share in 2025 because they have the strongest clinical familiarity, the broadest shelf presence, and the deepest consumer awareness in this category.

Page last updated on: