United States Dental 3D Printing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

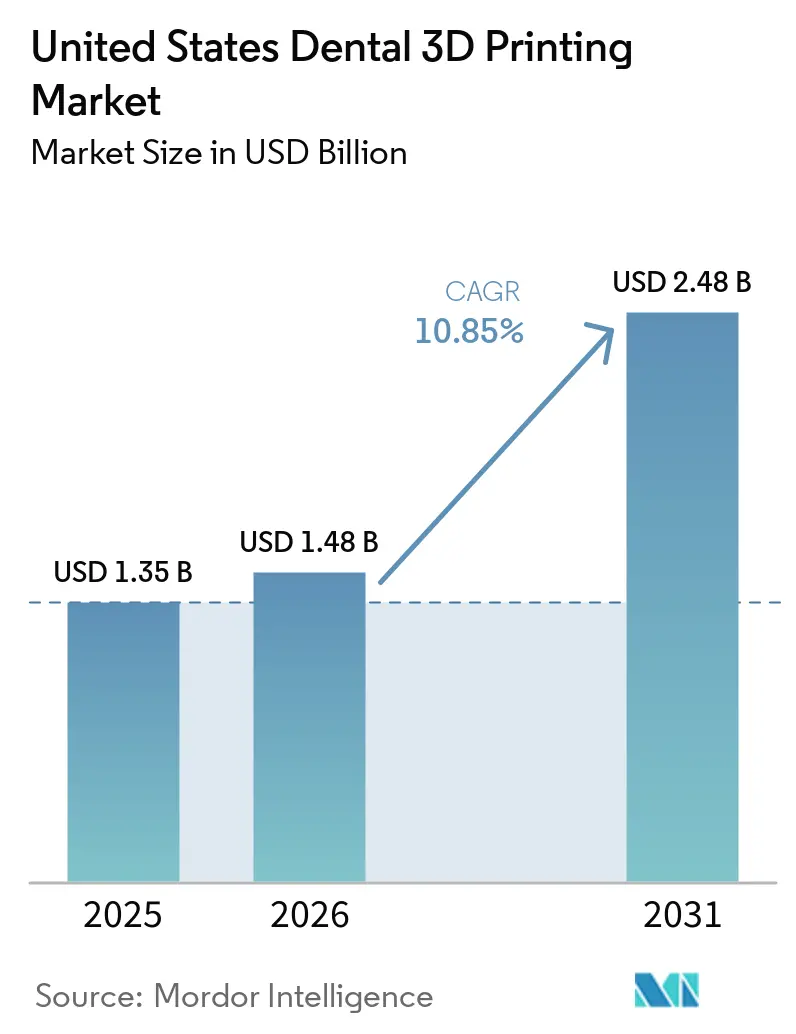

| Base Year Market Size (2025) | USD 1.35 Billion |

| Market Size (2026) | USD 1.48 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 10.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Dental 3D Printing Market Analysis by Mordor Intelligence

The United States Dental 3D Printing Market size is projected to expand from USD 1.35 billion in 2025 and USD 1.48 billion in 2026 to USD 2.48 billion by 2031, registering a CAGR of 10.85% between 2026 to 2031.

The United States dental 3D printing market is expanding because chairside manufacturing is moving from pilot use to routine clinical workflows, especially as practices seek faster restorative turnaround and tighter control over scheduling. Labor pressure is also reinforcing automation, as dental laboratory technician employment is projected to contract, and only 33,920 technicians were recorded nationally in 2024, which makes digital production more attractive for both labs and clinics. Competitive positioning in the United States dental 3D printing market is shifting toward validated ecosystems, with printer makers, materials companies, and workflow partners tying recurring resin demand and software usage to installed hardware. The United States dental 3D printing market is also benefiting from a broader FDA-cleared materials base that widens the number of indications a single platform can serve. Adoption still faces caution in definitive long-wear applications because the clinical evidence base remains stronger for guides and models than for long-term direct-printed appliances.

Key Report Takeaways

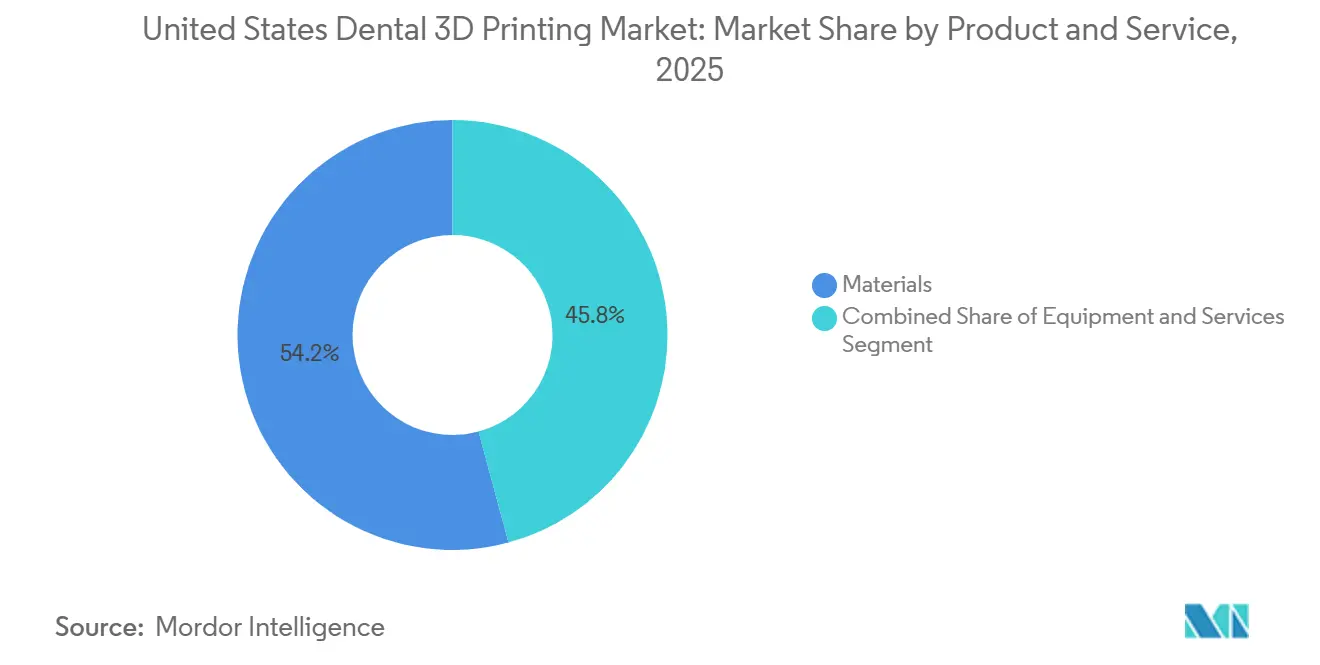

- By product and service, materials held 54.23% of the market in 2025, while services are projected to expand at an 11.91% CAGR through 2031.

- By technology, vat photopolymerization accounted for 32.38% of the United States dental 3D printing market size in 2025, while fused deposition modeling is forecast to grow at a 12.73% CAGR through 2031.

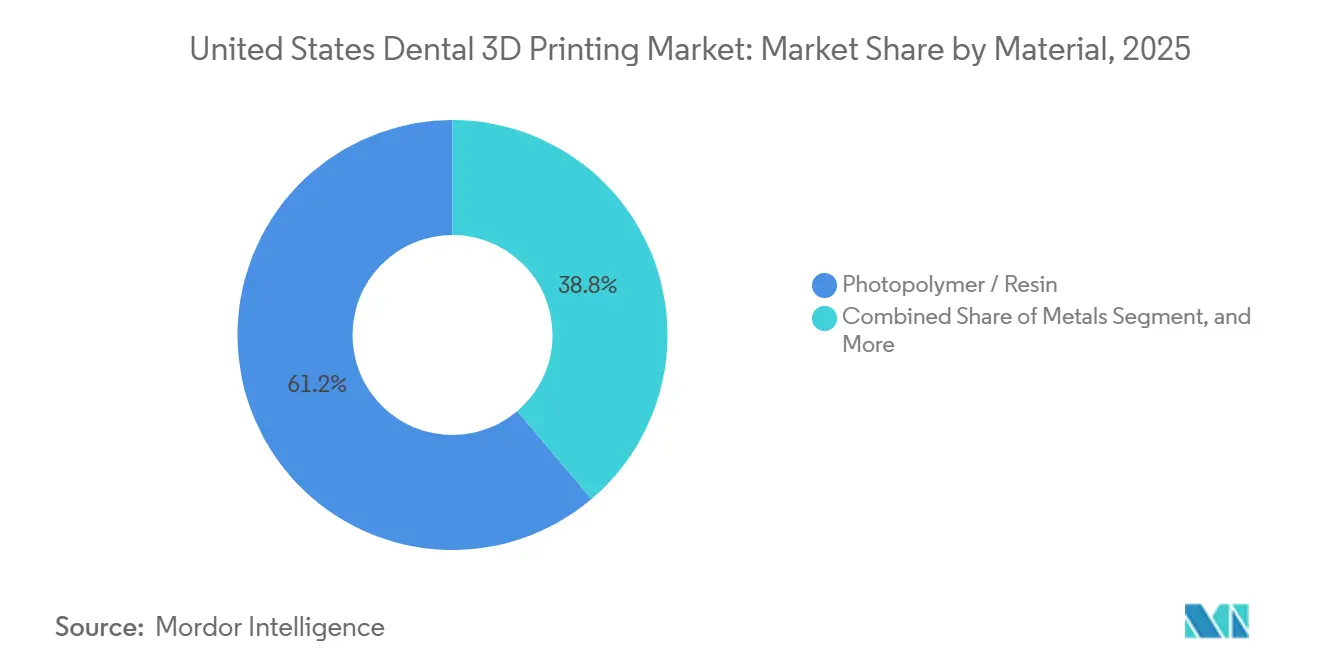

- By material, photopolymer resins captured 61.23% of the market in 2025, while metals are expected to advance at an 11.28% CAGR through 2031.

- By application, orthodontics represented 39.23% of the United States dental 3D printing market size in 2025, while implantology is set to grow at a 12.07% CAGR through 2031.

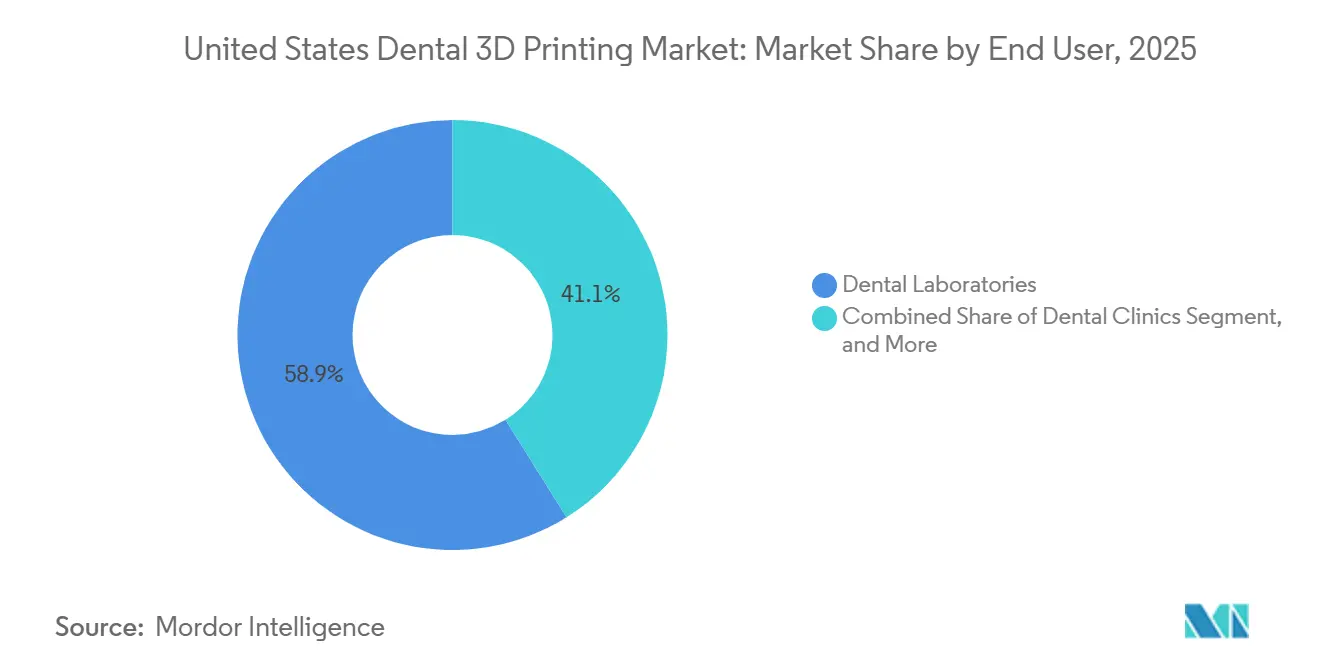

- By end user, dental laboratories held 58.86% of the United States dental 3D printing market share in 2025, while dental clinics are projected to record the highest CAGR at 11.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Dental 3D Printing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Customized Same-Day Appliances And Restorations | +2.1% | National, with early gains in metro DSO clusters such as New York, Los Angeles, Chicago, and Houston | Medium term (2-4 years) |

| Clear Aligner And Orthodontic Workflow Expansion | +1.9% | National, with high concentration in Sun Belt and suburban growth markets | Medium term (2-4 years) |

| Broader FDA-Cleared Printable Material Portfolio | +1.4% | National, shaped by the FDA 510(k) Class II premarket pathway | Short term (≤ 2 years) |

| Turnaround-Time And Per-Part Cost Reduction | +1.7% | National, with the strongest ROI in rural and semi-urban markets with limited lab access | Short term (≤ 2 years) |

| Dental Lab Technician Shortages | +1.2% | National, with acute pressure in smaller metros where training programs have closed | Medium term (2-4 years) |

| Direct-Print Appliance Workflows Reducing Thermoforming Steps | +0.8% | National, with early adoption in technology-forward orthodontic DSOs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Customized Same-Day Appliances and Restorations Driving Chairside Adoption

Same-day dentistry is becoming a more practical operating model for practices that invest in chairside 3D printing. SprintRay stated that its Midas Digital Press can produce up to 10 restorations in under 10 minutes, and its February 2026 Chicago Midwinter preview showed multi-unit molar capability, which signals a wider clinical scope than earlier chairside systems offered. That matters because the United States dental 3D printing market is moving beyond simple front-tooth use cases toward broader restorative workflows. Early adoption is still concentrated in DSO networks that can spread capital spending and training across many locations. Independent practices remain less represented, which means the next stage of expansion depends on making validated chairside workflows easier to adopt at smaller scale.

Clear Aligner and Orthodontic Workflow Expansion

Orthodontics remains one of the strongest demand engines in the United States dental 3D printing market because treatment planning requires high print volumes and repeatable digital workflows. Align Technology reported 2.6 million case starts in fiscal 2025, including 935,800 teen and pediatric starts, which confirms that case flow in orthodontics remains strong. LuxCreo secured FDA clearance for a direct-print clear aligner resin, which moves the workflow closer to full in-office production and reduces dependence on the conventional thermoforming path.[1]LuxCreo, “LuxCreo FDA-Cleared 4D Aligner, Direct-Print Clear Aligners for Same-Day Orthodontic Treatment,” LuxCreo, luxcreo.com. A 2025 study in Progress in Orthodontics found that certain direct-printed aligner materials delivered optical and microbiological performance comparable with thermoformed alternatives. As this model scales, resin demand will shift away from mold production and toward flexible direct-print polymers designed for active wear.

Broader FDA-Cleared Printable Material Portfolio

The United States dental 3D printing market is gaining from a wider pipeline of FDA-cleared materials that expands what a single printer can produce. Carbon launched FP3D in September 2025 as an FDA-cleared flexible partial denture resin, which added a new removable prosthetic indication to digital workflows.[2]Carbon, “Carbon Announces Commercial Availability of FP3D Resin,” Carbon, carbon3d.com. Formlabs received 510(k) clearance in February 2026 for Premium Teeth Resin for temporary crowns, inlays, onlays, veneers, and up to 7-unit bridges, while Rapid Shape announced FDA approval for its RS VIVO dental resin portfolio in the same month. This broader cleared portfolio means practices can support more indications without replacing their installed printer base. It also gives an advantage to suppliers that already have strong biocompatibility and compliance documentation across multiple resin families.

Turnaround-Time and Per-Part Cost Reduction

Turnaround time remains one of the clearest reasons practices and labs continue to add digital manufacturing capacity. The United States dental 3D printing market benefits when workflows shift from external lab queues toward in-office or near-office production because treatment scheduling becomes easier to control. Implantology has been one of the earliest beneficiaries, since digital planning and guide fabrication fit naturally into the same digital chain. The advantage is strongest in suburban, rural, and semi-urban settings where outside lab access is less convenient and delivery delays are harder to absorb. That is why the United States dental 3D printing market continues to attract interest from high-throughput clinics that want faster case completion and fewer workflow handoffs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost and Training Burden | -1.90% | National; disproportionate impact on solo and small-group practices outside major metros | Medium term (2–4 years) |

| Regulatory and Material-Validation Requirements | -1.30% | National; compliance factors tied to FDA 510(k) Class II pathway and ISO 10993 testing | Short term (≤ 2 years) |

| Limited Long-term Evidence for Long-Wear Direct-Printed Appliances | -0.80% | National; concentrated in prosthodontics and direct-print aligner clinical adoption | Long term (≥ 4 years) |

| External Lab Dependence Slowing Chairside Printer Conversion | -0.60% | National; most pronounced in rural markets with long-standing lab referral relationships | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Training Burden

The shrinking technician base is becoming a structural support for automation across the United States dental 3D printing market. State labor market data showed only 33,920 dental laboratory technicians nationally in 2024, and long-term employment is projected to decline through 2032.[3]Michigan Department of Career Development and Advancement, “Occupational Focus: Dental Laboratory Technicians,” Michigan.gov, michigan.gov. This staffing pressure is especially significant for smaller metros and lower-density markets where recruiting replacement talent is more difficult. As a result, labs and clinics are leaning more heavily on repeatable digital processes that reduce dependence on scarce manual skills. The labor shortage does not remove the need for training, but it strengthens the payback case for automated models, guides, and restorative production.

Limited Long-Term Evidence for Long-Wear Direct-Printed Appliances

Definitive prostheses, directly printed aligners, denture bases, and metal frameworks remain in early stages of adoption from a long-term clinical evidence standpoint. A 2025 narrative review in ScienceDirect confirmed that while surgical guides and diagnostic models have well-established reliability profiles, provisional restorations require longer-term validation before they can be deployed as definitive long-wear solutions. For direct-printed aligners specifically, the biocompatibility evidence base consists primarily of in vitro studies, with limited prospective clinical data on material performance under continuous intraoral wear over 12-month-plus treatment cycles. This evidentiary gap constrains reimbursement conversations and slows prescriber confidence in US orthodontic and prosthodontic practices that prioritise clinical conservatism. Until peer-reviewed multi-year outcome studies accumulate, the most clinically demanding applications — full-arch all-on-X restorations and long-wear definitive crowns in posterior positions — will retain higher procedural caution.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Materials Dominance Masks a Services Acceleration

Materials captured 54.23% of the United States dental 3D printing market in 2025, which reflects how strongly both chairside and lab workflows depend on recurring resin use. Each new printer placement can create a long tail of consumable demand, so suppliers have focused on expanding validated resin libraries rather than relying only on hardware sales. That pattern helps explain why materials remained the largest segment even as new printer launches continued across the market. Equipment still matters because it is the entry point that determines which software, resins, and post-processing steps a customer is most likely to keep using.

Services are forecast to grow at an 11.91% CAGR through 2031, which makes them the fastest-moving layer inside this segmentation. The shift matters because the United States dental 3D printing industry is moving toward recurring software, workflow support, and managed production relationships rather than one-time hardware transactions alone. Vendors are reinforcing that model through integrated workflows, training programs, and partnership-led material validation that keep users inside a preferred ecosystem. As adoption widens, services should capture more value from onboarding, design support, workflow optimization, and maintenance around installed systems.

By Technology: DLP and SLA Hold the Center While FDM Broadens Access

Vat photopolymerization held 32.38% of the United States dental 3D printing market size in 2025, which kept it at the center of orthodontic models, surgical guides, and crown provisional workflows. The technology remains entrenched because high-resolution output is still critical in dental use cases where fit, detail, and repeatability directly affect clinical acceptance. That position is reinforced by the breadth of cleared resin options now available on photopolymer-based systems. PolyJet and material jetting remain more specialized, but 3D Systems expanded its commercial relevance in 2026 by scaling its jetted denture platform through the NextDent 300 MultiJet printer.

Fused deposition modelling is projected to grow at a 12.73% CAGR through 2031, which makes it the fastest-growing technology segment in the United States dental 3D printing market. Its role is less about displacing vat systems and more about opening cost-conscious use cases such as educational models, custom trays, splints, and simple fabrication tasks. That matters for institutions and practices that need digital capability but do not always need the highest-end restorative resolution. Selective laser sintering keeps a place in the market for metal and nylon frameworks, though adoption remains concentrated in specialized laboratories with the process depth to manage it. The result is a technology mix where photopolymerization remains the clinical core, while FDM broadens the reachable base of users.

By Material: Resin Breadth Leads While Metals Raise the Performance Bar

Photopolymer resins accounted for 61.23% of the United States dental 3D printing market in 2025 within the materials segment, reflecting their broad use across models, guides, splints, dentures, and temporary restorative applications. This category has widened because new clearances continue to add sub-segments that can run on existing installed printers. Carbon added a flexible partial denture material in 2025, while Formlabs widened temporary restorative capability in 2026 with Premium Teeth Resin. Because of that breadth, resin remains the most important recurring revenue stream for much of the United States dental 3D printing market.

Metals are projected to grow at an 11.28% CAGR through 2031, which points to rising interest in cobalt-chrome and titanium applications where precision and strength are more important than broad accessibility. The segment remains narrower than resin because production quality, validation demands, and workflow complexity are all higher. Ceramics are also gaining relevance in selected aesthetic restorative uses, though they remain more limited in breadth. In practice, metals signal the next quality threshold for the United States dental 3D printing market, but they are still concentrated in laboratories that can support advanced process control and compliance. This keeps resin as the scale material, while metals continue to represent an important but more selective growth path.

By Application: Orthodontics Holds Scale While Implantology Advances the Fastest

Orthodontics held 39.23% of the United States dental 3D printing market size in 2025, supported by the heavy model output required in sequential aligner planning and appliance production. The segment remains large because even modest growth in clear aligner volume can translate into substantial print demand across models, retainers, and related digital steps. The workflow is also evolving, as direct-print aligner systems reduce reliance on the traditional model-and-thermoform process. Clinical support is still building, but published evidence suggests that selected direct-printed materials are narrowing the performance gap with conventional thermoformed options.

Implantology is forecast to grow at a 12.07% CAGR through 2031, making it the fastest-growing application segment in the United States dental 3D printing market. The main reason is the growing use of patient-specific surgical guides, which fit cleanly into digital planning and in-office production workflows. Prosthodontics remains the second-largest application block because crowns, bridges, and dentures continue to pull large volumes through both labs and chairside systems. Oral and maxillofacial surgery also offers a strong adjacent opportunity, though adoption remains more selective because anatomically complex cases require deeper design expertise. Across applications, the United States dental 3D printing market is balancing high-volume orthodontic demand with faster procedural growth in implant-led workflows.

By End User: Labs Operate at Scale While Clinics Set the Growth Path

Dental laboratories held 58.86% of the United States dental 3D printing market share in 2025, which reflects their established role in high-volume model, denture, framework, and restoration production. Labs remain the scale anchor because they can centralize hardware, trained staff, and quality control across a larger case base. That operating advantage is visible in multi-site investment activity, including ROE Dental Laboratory's deployment of multiple NextDent 300 MultiJet systems across several United States locations in 2026. The result is a United States dental 3D printing market in which labs still carry most production volume even as clinical use expands.

Dental clinics are projected to grow at an 11.45% CAGR through 2031, which makes them the most important structural growth engine in the United States dental 3D printing market. The main support is the widening range of FDA-cleared materials, which improves the case for printing more indications inside the practice rather than sending them out. DSOs are leading this conversion because they can standardize procurement, implementation, and staff training across multiple clinics. Academic and research institutes remain the smallest end-user group, but they still matter because they help train future users and support validation of emerging workflows. This keeps clinics as the growth path, even while laboratories remain the installed production base of the United States dental 3D printing industry.

Geography Analysis

The United States dental 3D printing market is the largest national market globally and operates within a dental system with a strong DSO presence, active materials development, and a comparatively dense digital dentistry infrastructure. Regional adoption inside the country is still uneven, which means the United States dental 3D printing market is shaped as much by local workflow maturity as by national demand. Metro corridors with strong DSO penetration, including the greater New York area, Los Angeles, Chicago, and Houston, have led chairside adoption because centralized procurement lowers the burden on each practice location. In these metro clusters, growth is moving from first-time printer installation toward broader platform consolidation. Practices are increasingly looking for systems that can handle restorative parts, surgical guides, and aligner-related workflows inside one validated operating environment.

The Sun Belt has a different profile inside the United States dental 3D printing market because population growth is creating demand faster than legacy lab infrastructure can absorb. Texas, Florida, Arizona, and Georgia are benefiting from suburban dental expansion, which makes in-office production more compelling for practices dealing with fast case flow. Dallas-Fort Worth, Phoenix, and Tampa have emerged as active chairside adoption markets for surgical guide and provisional crown workflows. Dentsply Sirona's restructuring plan in early 2026, which targeted USD 120 million in annualized savings, also signaled how strongly vendors are focusing on more cost-efficient digital operating models.

The Northeast and Midwest represent a different geography within the United States dental 3D printing market because they combine dense laboratory networks with many dental schools and academic centers. Adoption in these regions has leaned more toward laboratory-scale investment and multi-technology training environments than toward immediate chairside conversion alone. That matters because future practitioners entering the market from digitally equipped programs should face a lower learning curve. Rural and semi-rural Midwestern areas face a separate issue, as understaffed local labs strengthen the case for digital production, but access to technical support and infrastructure can still limit conversion speed. This gap creates room for service-led models that combine remote monitoring, maintenance, and material replenishment for lower-volume users. As a result, the United States dental 3D printing market continues to show one national growth story, but several different regional adoption patterns.

Competitive Landscape

The United States dental 3D printing market is moderately concentrated at the platform level, but it remains fragmented across materials, services, and workflow support. A limited group of major players, including Align Technology, Dentsply Sirona, 3D Systems, SprintRay, and other workflow-focused suppliers, compete by linking scanners, software, printers, and materials into tighter operating systems. This means the main competitive question in the United States dental 3D printing market is no longer just printer specification. It is increasingly about who controls the validated workflow and the recurring material relationship after installation. That shift is clear in partnerships that tie clinical materials science to chairside hardware and education infrastructure.

Strategic moves in the United States dental 3D printing market increasingly show that ecosystem depth matters more than commodity hardware pricing. SprintRay strengthened its position in September 2025 by acquiring the EnvisionTEC dental portfolio from Desktop Health, which expanded its patent base, trademarks, inventory, and material reach. Dentsply Sirona and Formlabs also aligned around Lucitone Digital Print Denture validation on the Form 4B, which illustrates how material-printer alliances are being used to widen installed-base value rather than only to sell new equipment. Carbon is pursuing a similar logic through workflow automation, and the company stated that its AO Backpack had processed more than 18,000 prints since its 2024 introduction. 3D Systems reinforced its own position in 2026 through multi-site NextDent deployment at ROE Dental Laboratory, which validated jetted denture production at scale.

Barriers to entry in the United States dental 3D printing market remain meaningful because cleared materials, biocompatibility evidence, and process quality systems are hard to assemble quickly. Suppliers with broader approval histories and stronger validation support can widen their lead as more practices prefer lower-risk workflow choices. This is why recurring resin sales, software integration, and training support are becoming more defensible than one-time hardware margins. Competitive pressure should therefore remain strongest around ecosystem lock-in, clinical validation, and workflow reliability rather than around standalone printer pricing alone.

United States Dental 3D Printing Industry Leaders

Align Technology, Inc.

Dentsply Sirona

Formlabs

Planmeca Oy

3D Systems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: 3D Systems announced that ROE Dental Laboratory deployed multiple NextDent 300 MultiJet 3D printers across several US locations, making it the leading domestic lab to scale the NextDent Jetted Denture platform at multi-site pace, validating the platform for high-volume clinical-grade denture manufacturing.

- April 2026: 3D Systems secured Class IIa EU MDR certification for its NextDent Jet Base and NextDent Jet Teeth materials, two months ahead of the targeted summer 2026 schedule, enabling full European commercial launch on May 4, 2026, and expanding the combined US and EU addressable edentulous patient population to over 60 million.

- March 2026: SprintRay announced the Midas World Tour, a global education programme across over 30 cities in partnership with the MOD Institute, GC America, Meisinger Dental, and Align Technology, designed to accelerate chairside multi-unit restoration adoption on the Midas Digital Press.

- March 2026: GC America and SprintRay formed a strategic R&D and commercialisation partnership to bring GC's dental materials science into the SprintRay Midas chairside ecosystem, enabling production of up to 10 restorations in under 10 minutes.

United States Dental 3D Printing Market Report Scope

The dental 3D printing market refers to the industry surrounding the manufacturing and sale of 3D printers, specialized software (CAD/CAM), and biocompatible materials used to produce highly customized dental appliances, prosthetics, and surgical tools.

The United States dental 3D printing market is structured across several well‑defined segments, covering the full value chain of products, technologies, materials, applications, and end users. By product and service, the market includes equipment, materials, and services that support dental 3D printing workflows. From a technology standpoint, the market spans Vat Photopolymerization, PolyJet/Material Jetting, Selective Laser Sintering, Fused Deposition Modelling, and a range of other emerging additive manufacturing technologies. In terms of materials, the industry utilizes photopolymers/resins, metals, ceramics, and other specialized dental materials tailored for clinical and laboratory use. The market also covers a broad set of applications, including orthodontics, prosthodontics, implantology, oral and maxillofacial surgery, and other dental‑specific uses. Finally, the end‑user landscape comprises dental laboratories, dental clinics, and academic and research institutes. Market forecasts across all these segments are provided in terms of value (USD), reflecting the financial outlook and growth potential of the United States dental 3D printing sector.

| Equipment |

| Materials |

| Services |

| Vat Photopolymerization | Stereolithography |

| Digital Light Processing | |

| PolyJet / Material Jetting | |

| Selective Laser Sintering | |

| Fused Deposition Modelling | |

| Other Technologies |

| Photopolymer / Resin | Model Resins |

| Guide and Tray Resins | |

| Splint and Guard Resins | |

| Denture Base and Tooth Resins | |

| Crown, Bridge, and Restorative Resins | |

| Metals | Cobalt Chrome |

| Titanium | |

| Ceramics | |

| Other Materials |

| Orthodontics | Aligner Models |

| Direct-Printed Aligners | |

| Retainers | |

| Indirect Bonding Trays | |

| Prosthodontics | Crowns and Bridges |

| Denture Bases | |

| Denture Teeth | |

| Try-In Dentures | |

| All-on-X and Full-Arch Restorations | |

| Wax-Ups | |

| Implantology | Surgical Guides |

| Implant Models | |

| Custom Abutment and Restorative Workflows | |

| Oral and Maxillofacial Surgery | |

| Other Dental Applications | Splints and Night Guards |

| Custom Impression Trays | |

| Gingiva Masks |

| Dental Laboratories |

| Dental Clinics |

| Academic and Research Institutes |

| By Product & Service | Equipment | |

| Materials | ||

| Services | ||

| By Technology | Vat Photopolymerization | Stereolithography |

| Digital Light Processing | ||

| PolyJet / Material Jetting | ||

| Selective Laser Sintering | ||

| Fused Deposition Modelling | ||

| Other Technologies | ||

| By Material | Photopolymer / Resin | Model Resins |

| Guide and Tray Resins | ||

| Splint and Guard Resins | ||

| Denture Base and Tooth Resins | ||

| Crown, Bridge, and Restorative Resins | ||

| Metals | Cobalt Chrome | |

| Titanium | ||

| Ceramics | ||

| Other Materials | ||

| By Application | Orthodontics | Aligner Models |

| Direct-Printed Aligners | ||

| Retainers | ||

| Indirect Bonding Trays | ||

| Prosthodontics | Crowns and Bridges | |

| Denture Bases | ||

| Denture Teeth | ||

| Try-In Dentures | ||

| All-on-X and Full-Arch Restorations | ||

| Wax-Ups | ||

| Implantology | Surgical Guides | |

| Implant Models | ||

| Custom Abutment and Restorative Workflows | ||

| Oral and Maxillofacial Surgery | ||

| Other Dental Applications | Splints and Night Guards | |

| Custom Impression Trays | ||

| Gingiva Masks | ||

| By End User | Dental Laboratories | |

| Dental Clinics | ||

| Academic and Research Institutes | ||

Key Questions Answered in the Report

What is the 2026 value of the United States dental 3D printing market?

The market stands at USD 1.48 billion in 2026 and is forecast to reach USD 2.48 billion by 2031 at a 10.85% CAGR.

Which product category leads dental 3D printing demand in the United States?

Materials lead the market with a 54.23% share in 2025 because recurring resin consumption supports both laboratory and chairside workflows.

Which technology is growing the fastest in dental 3D printing applications?

Fused deposition modeling is the fastest-growing technology segment, with a projected 12.73% CAGR through 2031.

Why are dental laboratories still the largest end users?

Dental laboratories held 58.86% of demand in 2025 because they remain the core production base for models, dentures, frameworks, and complex restorations.

What is driving faster growth in implant-related printing workflows?

Implantology is projected to grow at a 12.07% CAGR because digital planning and patient-specific surgical guides fit well with in-office production.

Page last updated on: