United States Construction Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

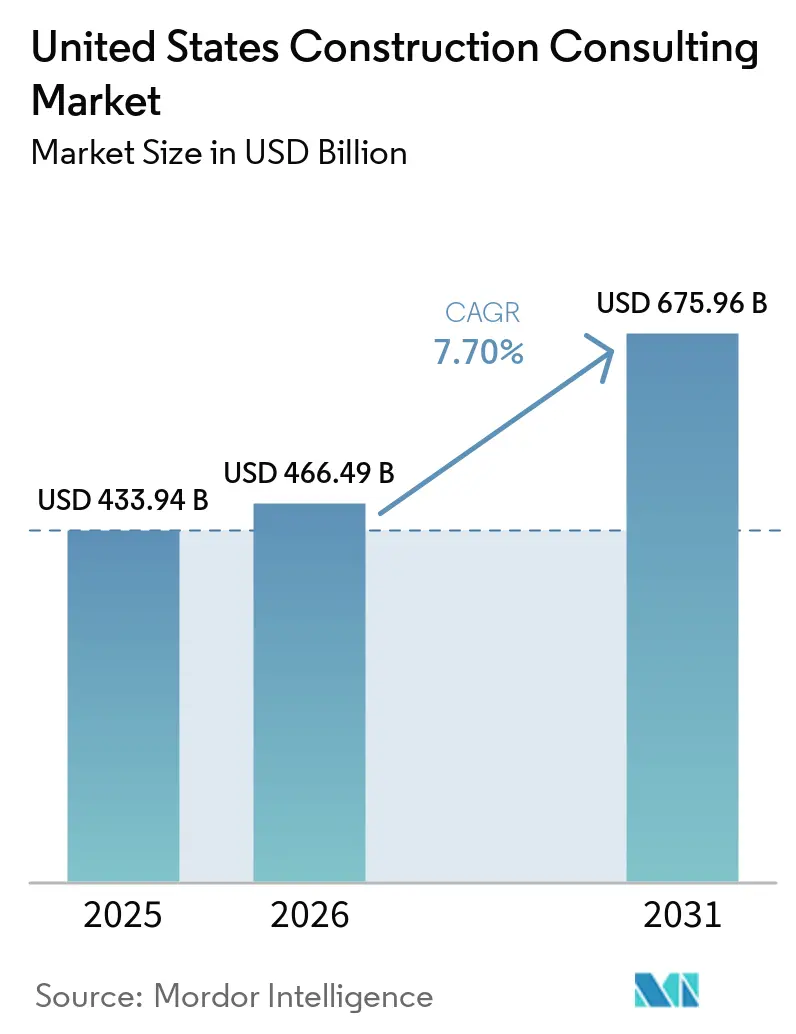

| Base Year Market Size (2025) | USD 433.94 Billion |

| Market Size (2026) | USD 466.49 Billion |

| Market Size (2031) | USD 675.96 Billion |

| Growth Rate (2026 - 2031) | 7.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Construction Consulting Market Analysis by Mordor Intelligence

The United States Construction Consulting Market size is projected to be USD 433.94 billion in 2025, USD 466.49 billion in 2026, and reach USD 675.96 billion by 2031, growing at a CAGR of 7.70% from 2026 to 2031.

Federal infrastructure stimulus, led by the Infrastructure Investment and Jobs Act (IIJA), is sustaining multi-year pipelines, while private hyperscalers are pouring record sums into artificial intelligence (AI) data center campuses. Consultants that can bridge traditional civil engineering with digital-twin advisory are capturing premium retainers as owners prioritize schedule certainty, resiliency, and technology enablement. Project Management Consultancy (PMC) keeps its foundational role, yet master-planning demand is rising as owners seek single-throat-to-choke accountability for feasibility, permitting, and ESG compliance. Labor scarcity, Buy America documentation burdens, and materials-cost volatility round out the opportunity-risk spectrum that underpins the United States construction consulting market.

Key Report Takeaways

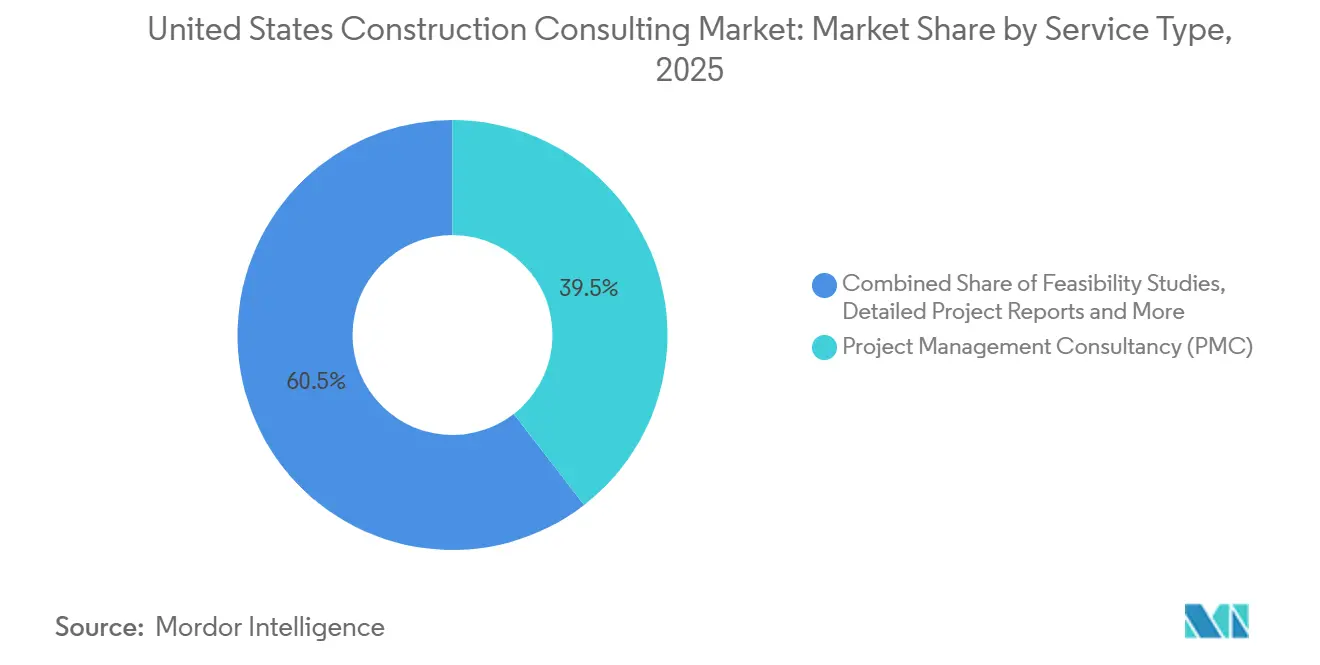

- By service type, Project Management Consultancy held 39.5% of the United States construction consulting market share in 2025, while Master Planning is projected to expand at an 8.3% CAGR through 2031.

- By sector, Infrastructure and Civil projects commanded 38.65% of the United States construction consulting market size in 2025, whereas the Commercial segment is expected to grow at an 8.4% CAGR between 2026 and 2031.

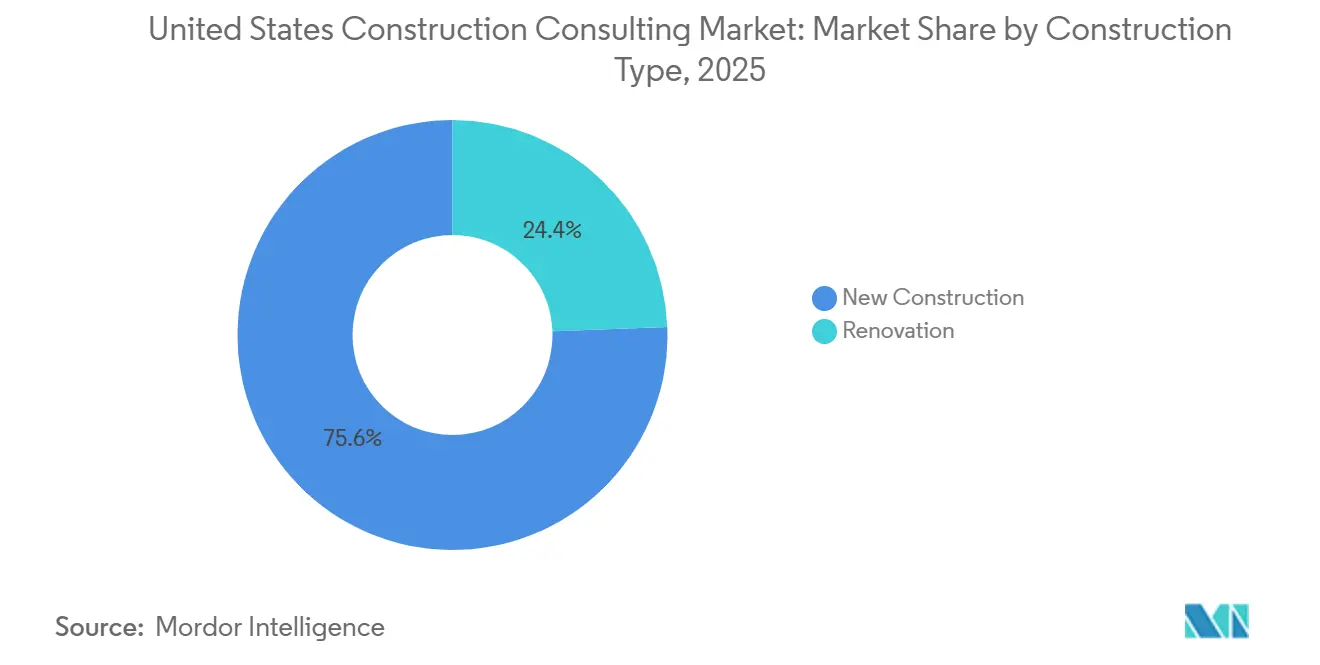

- By construction type, New Construction accounted for 75.6% of the United States construction consulting market share in 2025, but Renovation is forecast to rise at a 9.05% CAGR through 2031.

- By investment source, private funding accounted for 75.69% of the United States construction consulting market in 2025, while public funding is projected to grow at a faster CAGR of 8.55% during 2026–2031.

- By states, the Southeast led with 40.55% of the United States construction consulting market share in 2025, whereas the West is poised for the quickest 8.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Construction Consulting Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Private-sector AI data-center boom | +2.1% | West, Southeast, Southwest | Medium term (2–4 years) |

| Federal infrastructure stimulus keeps public-works pipeline robust | +1.8% | Nationwide, strongest in the Southeast and the West | Long term (≥ 4 years) |

| Rapid BIM and digital-twin adoption | +1.2% | Major metros in the West and the Northeast | Medium term (2–4 years) |

| ESG and decarbonization mandates | +1.0% | National, led by California and New York | Long term (≥ 4 years) |

| Mid-market owners outsourcing project management | +0.9% | National, early in the Sunbelt | Short term (≤ 2 years) |

| Buy America compliance complexity | +0.7% | States with high federal-aid highway outlays | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Private-Sector AI Data-Center Boom

Hyperscaler capital expenditures climbed to USD 443 billion in 2025 and are budgeted at USD 602 billion for 2026 as firms race to serve generative-AI workloads. Flagship campuses, such as the USD 50 billion Stargate complex, demand site selection, utility capacity, and cooling optimization expertise that few firms currently possess. AIA forecasts show data-center billings outpacing every other commercial sub-sector through 2027[1]American Institute of Architects, “Consensus Forecast July 2025,” aia.org . Consultants who can coordinate more than 100 subcontractors per campus while mitigating cyber-physical risks and land multi-year frameworks. Consequently, AI-linked workstreams are now the fastest-growing segment of the United States construction consulting market.

Federal Infrastructure Stimulus Keeps Public-Works Pipeline Robust

IIJA funnels USD 350 billion into highways and a USD 496 billion Department of Transportation budget, anchoring steady demand for roadway, bridge, and water-infrastructure consultants[2]Federal Highway Administration, “BABA Guidance Memorandum,” fhwa.dot.gov . Energy-security outlays under the CHIPS and Science Act further expand advisory scope to semiconductor and LNG megaprojects. Scope growth now includes climate-resiliency assessments and EV-charging networks, pushing consultants up the strategic value chain. Federal Emergency Management Agency (FEMA) Buy America Preference rules, effective 2026, increase documentation loads, making regulatory consultants indispensable. As appropriations flow over a decade-plus horizon, the stimulus offers durable visibility for the United States construction consulting market.

Rapid BIM and Digital-Twin Adoption

Owners insist on 4D scheduling, clash detection, and digital twins of asset lifecycles to compress delivery times and cut operating costs. The approach lowers rework yet introduces new cyber threats; more than 5,400 global attacks were logged in 2024, with some ransom demands topping USD 75 million. Consultants are embedding zero-trust network design and liability allocation during concept phases to safeguard connected devices. New York City’s combined sewer overflow tunnel, overseen by an AECOM-Parsons joint venture, showcases real-time digital monitoring as a procurement requirement. Digital-twin fluency is quickly becoming a gatekeeper credential for shortlisting on large contracts.

ESG and Decarbonization Mandates

The Environmental Protection Agency’s low-carbon concrete program steers USD 2 billion toward verified reduced-emissions materials, forcing consultants to integrate life-cycle assessments in bid packages[3]Environmental Protection Agency, “Low-Carbon Construction Materials”, epa.gov . The Department of Energy’s Clean Energy Rule mandates net-zero-ready federal buildings, driving demand for energy modeling and renewables integration. Federal contractor greenhouse-gas disclosure thresholds now apply to contracts above USD 50 million. Arcadis’ USD 1.7 billion Battery Park City resiliency award shows climate-adaptation consulting scaling from niche to mainstream. Collectively, ESG mandates add a predictable premium service layer within the United States construction consulting market.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-consultant labor shortages inflate fees | –1.3% | Nationwide, acute in fast-growing Sunbelt | Medium term (2–4 years) |

| Materials price volatility delays projects | –0.9% | National, most severe in the West | Short term (≤ 2 years) |

| Fragmented permitting regimes prolong timelines | –0.6% | Key coastal metros | Long term (≥ 4 years) |

| Cyber-liability risk deters smaller firms | –0.4% | Data-center and critical-infrastructure builds | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Skilled-Consultant Labor Shortages Inflate Fees

92% of firms reported hiring difficulties in 2025, and average craft wages reached USD 39.69 per hour, 8.9% above the private-sector mean. Smaller consultancies lack capital for AI scheduling tools or offshore drafting hubs, squeezing margins. Large players respond by acquiring talent en masse; WSP bought Power Engineers for USD 1.78 billion in 2024. Elevated labor premiums shave roughly 1.3 percentage points off the forecast CAGR for the United States construction consulting market.

Materials Price Volatility Delays Projects

Steel surged 11.9% in 2025, while regional inflation in the West rose to 4.55% from 4.41% nationally. Owners delay starts to re-price bids or embed escalation clauses, as seen in Bechtel’s USD 27 billion Woodside LNG contract. Consultants take on mitigation assignments, cost tracking, hedging, and value engineering, but prolonged bid cycles trim near-term revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Master Planning Builds Momentum

Project Management Consultancy secured 39.5% of the United States construction consulting market share in 2025, reflecting its centrality to cost, schedule, and contractor control. Master Planning and other advisory offerings, however, are projected to outpace the broader market at an 8.3% CAGR through 2031, as owners seek one-stop guidance on feasibility, zoning, and digital twin modeling. AECOM’s 2026 Sound Transit win illustrates how master plans can extend into multi-year program management retainers. Digital-twin simulations that test resiliency scenarios further raise entry barriers, enabling consultancies to lock in premium, recurring fees.

Feasibility Studies and Detailed Project Reports remain mandatory for public procurement, especially where IIJA dollars require rigorous vetting. Design and Engineering Services continue to underpin physical delivery, yet client demand is shifting upstream toward strategic insight. This dynamic expands the total addressable advisory spending and reinforces the value proposition of firms that blend regulatory savvy with data-centric design.

By Sector: Commercial Outpaces on Digital Demand

Infrastructure and Civil projects accounted for 38.65% of the United States construction consulting market in 2025. Still, the Commercial sector is set for the strongest 8.4% CAGR during 2026-2031, powered by data center, life science, and adaptive reuse initiatives. American Institute of Architects surveys cite 26.3% data-center billing growth for 2026, dwarfing every other commercial bucket. Office retrofits into mixed-use labs and residential units add a steady backlog, even as speculative office ground-breakings slow. Turner Construction’s Philadelphia arena joint venture showcases marquee commercial programs that blend design leadership with complex stakeholder management, further attracting consultants fluent in technology-enabled delivery.

Residential momentum in the Southeast sustains baseline consulting volumes, while CHIPS Act-funded semiconductor fabs in the West reinforce industrial backlogs. Public highways, water, and social infrastructure packages remain sizable. Yet, private AI-centric builds deliver higher fee intensity per dollar of capex, skewing overall growth toward the Commercial classification in the United States construction consulting market.

By Construction Type: Renovation Accelerates

New Construction comprised 75.6% of spending in 2025, but Renovation is forecast to climb at a 9.05% CAGR to 2031. A median housing-stock age of 41 years and mortgage-rate “lock-in” dynamics funnel capital into remodeling rather than new construction. Large-scale retrofits such as the 3.2 million-square-foot Las Vegas Convention Center overhaul completed in 2026 prove that renovation projects can rival the complexity of greenfield projects. Consultants offering phased-occupancy and historic-preservation know-how win outsized market share.

Greenfield projects tied to federal infrastructure and hyperscale data-center campuses keep New Construction dominant in absolute terms. However, the steeper trajectory of renovations shifts skill requirements toward existing-condition scanning, brownfield permitting, and operations-focused scheduling, thereby diversifying advisory firms' revenue sources.

By Investment Source: Public Dollars Gain Speed

Private investment delivered 75.69% of market outlays in 2025, yet Public funding is projected to expand faster at an 8.55% CAGR as IIJA, CHIPS, and climate-resiliency programs scale disbursements. California’s USD 15.2 billion highway allocation and Washington’s USD 3.3 billion share underpin steady consulting backlogs. Micron’s USD 15 billion Idaho semiconductor plant, supported by incentives, illustrates blended funding models that blur public-private lines and enlarge advisory scopes.

Private capital remains robust in AI data center builds, industrial logistics, and multifamily housing in Sunbelt metros. Yet, recession-sensitive office and retail pipelines remain tepid, making public appropriations an essential counter-cyclical stabilizer for the United States construction consulting market.

Geography Analysis

The Southeast retained 40.55% of the United States construction consulting market share in 2025, buoyed by warehouse, hospital, and manufacturing pipelines across Florida, Georgia, North Carolina, and South Carolina. North Carolina added 10,200 construction jobs, a 3.7% year-over-year lift, thanks to data-center, energy, and hospital builds, whereas Florida lost 8,800 positions as residential momentum cooled. Georgia’s 54% retail and 39% lodging growth highlights regional diversification, and South Carolina’s 70% hospital surge signals healthcare build-outs aligning with population inflows. Favorable business climates and labor-cost advantages cement the Southeast’s base-load consulting demand.

The West is forecast to have the fastest CAGR of 8.85% through 2031, helped by California’s USD 15.2 billion highway allocation, Washington’s USD 3.3 billion tranche, and megaprojects such as the USD 3.9 billion Sites Reservoir and the USD 15 billion Idaho semiconductor fab. Regional input-cost inflation at 4.55% above the 4.41% national level underscores the need for cost-control advisory. Meta’s USD 800 million Kuna (Idaho) data center and Micron’s fab underscore semiconductor-centric growth that hinges on consultants skilled in environmental and tribal permitting.

The Northeast, Midwest, and Southwest round out the national picture. New York’s USD 1.7 billion Battery Park City resiliency program exemplifies the demand for climate-adaptation consulting. Midwestern industrial investments like Fluor’s Virginia electrolyzer JV keep power and clean-energy advisories active. In the Southwest, Texas and Arizona absorb data-center and logistics capital, with HNTB’s Buck O’Neil Bridge replacement highlighting design-build traction. Collectively, these regions provide a diverse demand tapestry that underpins long-run market resilience.

Competitive Landscape

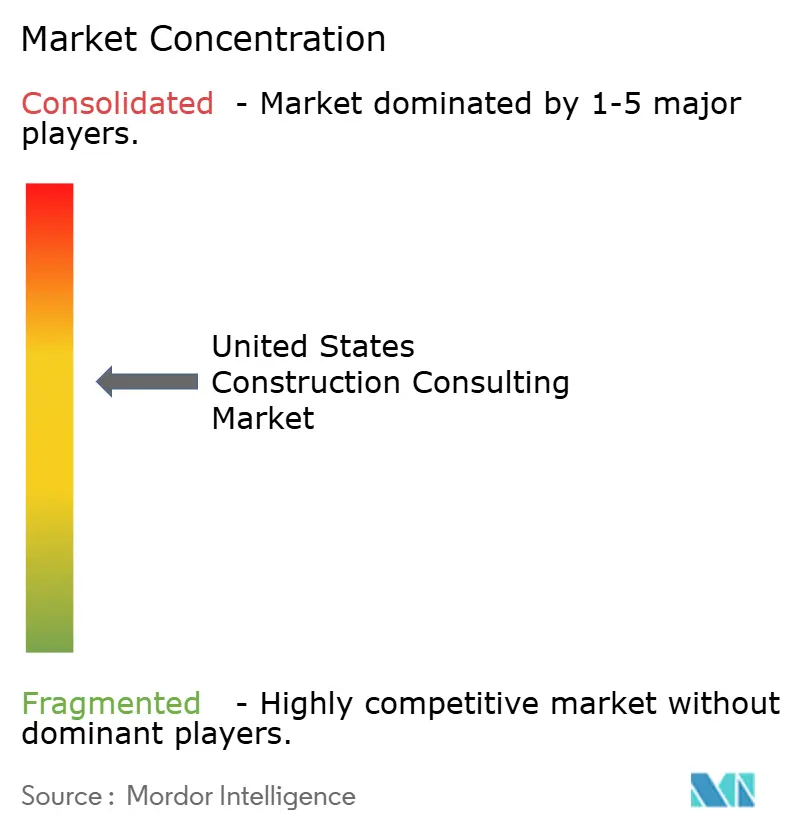

The United States construction consulting market is moderately consolidated, with global engineering majors commanding large-scale project delivery. Still, a diverse base of mid-sized specialists and technology-led entrants sustains competitive intensity and fragmentation across the advisory and mid-market segments. International majors AECOM, Jacobs, WSP, Bechtel, and Fluor anchor the top tier, leveraging global resource pools and end-to-end offerings that span design to commissioning. WSP’s USD 670 million Ricardo acquisition in 2025 broadened its environmental and rail toolkit, while Jacobs’ USD 1.6 billion acquisition of PA Consulting delivers strategy and digital acumen. Scale offers bidding leverage on federal mega-projects but does not preclude niche disruptors from carving specialized lanes.

Mid-sized and regional specialists thrive by claiming owner-representative and compliance niches. Terrapin Construction Group and YA Group differentiate with AI-powered estimating and zero-conflict models, serving USD 10-100 million project owners whom global EPCM outfits have historically overlooked. Buy America paperwork and ESG disclosures provide further fragmentation levers, as smaller players equip contractors with agile, purpose-built compliance teams.

Technology adoption is the decisive battleground. Firms that integrate BIM, 4D scheduling, and cyber-secure digital twins win higher-margin, multi-year mandates. AECOM-Parsons’ real-time monitoring of New York’s CSO tunnel and HDR’s data center cyber-risk services illustrate the role of technology in competitive differentiation. As AI workloads balloon, capital owners are increasingly comfortable granting consultants full life-cycle frameworks, planning through operations, to substantiate digital prowess.

United States Construction Consulting Industry Leaders

AECOM

Jacobs

WSP USA

HDR Inc.

Bechtel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AECOM and Parsons formed a joint venture for New York City’s combined sewer overflow tunnel supervision, embedding real-time BIM dashboards.

- February 2026: AECOM won a design and program-management contract for Sound Transit’s network expansion in Seattle.

- January 2026: Jacobs purchased the remaining stake in PA Consulting for USD 1.6 billion, boosting strategy and technology depth.

- January 2026: AECOM Hunt and PENTA delivered the 3.2 million-square-foot Las Vegas Convention Center renovation.

United States Construction Consulting Market Report Scope

| Project Management Consultancy (PMC) |

| Feasibility Studies |

| Detailed Project Reports (DPR) |

| Design and Engineering Services |

| Master Planning and Other Services |

| Residential | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Data Center | |

| Others - Institutional, Hospitality etc. | |

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Social Infrastructure | |

| Others |

| New Construction |

| Renovation |

| Public |

| Private |

| Northeast (New York, Massachusetts, Pennsylvania, etc.) |

| Midwest (Illinois, Ohio, Michigan, etc.) |

| Southeast (Florida, Georgia, North Carolina, etc.) |

| West (California, Washington, Colorado, etc.) |

| Southwest (Texas, Arizona, New Mexico, etc.) |

| By Service Type | Project Management Consultancy (PMC) | |

| Feasibility Studies | ||

| Detailed Project Reports (DPR) | ||

| Design and Engineering Services | ||

| Master Planning and Other Services | ||

| By Sector | Residential | |

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Data Center | ||

| Others - Institutional, Hospitality etc. | ||

| Infrastructure/Civil | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Social Infrastructure | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Northeast (New York, Massachusetts, Pennsylvania, etc.) | |

| Midwest (Illinois, Ohio, Michigan, etc.) | ||

| Southeast (Florida, Georgia, North Carolina, etc.) | ||

| West (California, Washington, Colorado, etc.) | ||

| Southwest (Texas, Arizona, New Mexico, etc.) | ||

Key Questions Answered in the Report

How large will the United States construction consulting market be by 2031?

Mordor Intelligence projects the market to reach USD 675.96 billion by 2031, growing at a 7.7% CAGR from 2026 to 2031.

Which service type leads to spending?

Project Management Consultancy captured 39.5% of the United States construction consulting market share in 2025, remaining the core fee generator .

What segment is growing the fastest?

The Commercial sector, fueled by AI data centers and adaptive reuse projects, is expected to expand at an 8.4% CAGR between 2026 and 2031.

Which region is forecast to grow the quickest?

The West region is set to achieve the highest CAGR of 8.85% to 2031, thanks to semiconductor and water-infrastructure megaprojects backed by IIJA funding.

How are Buy America rules impacting consultants?

The October 2025 and October 2026 phase-ins impose domestic-content documentation, creating steady demand for compliance advisory services and new recurring revenue streams.

Page last updated on: