United States Cold Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

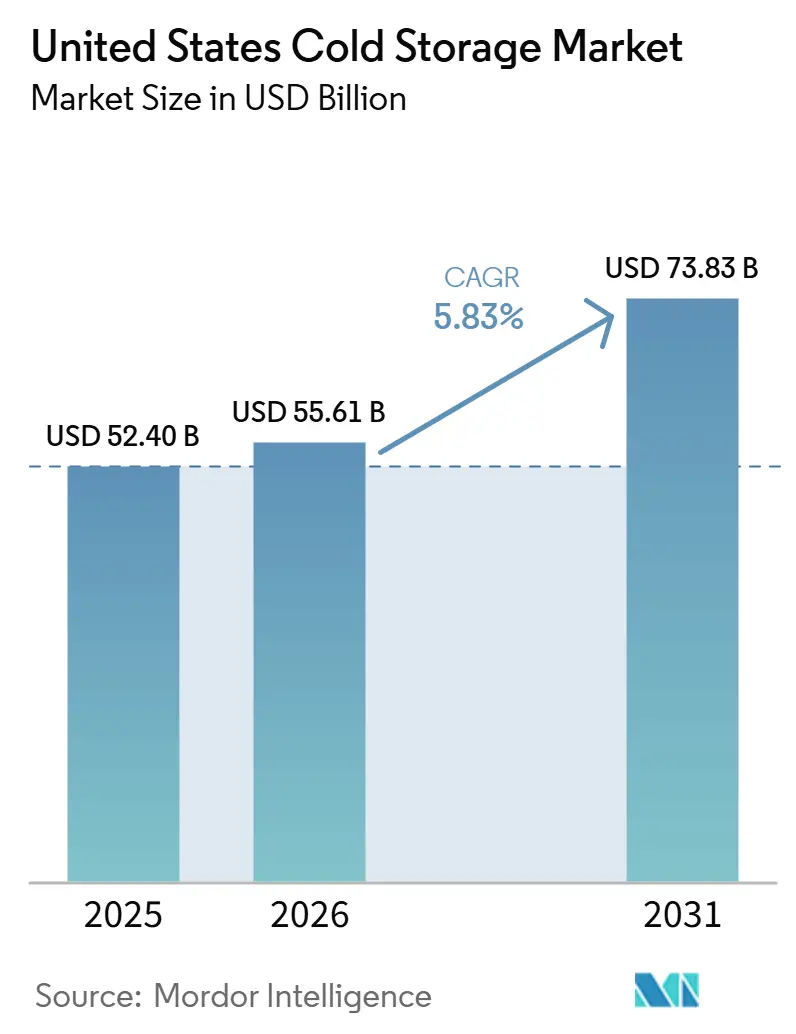

| Base Year Market Size (2025) | USD 52.40 Billion |

| Market Size (2026) | USD 55.61 Billion |

| Market Size (2031) | USD 73.83 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

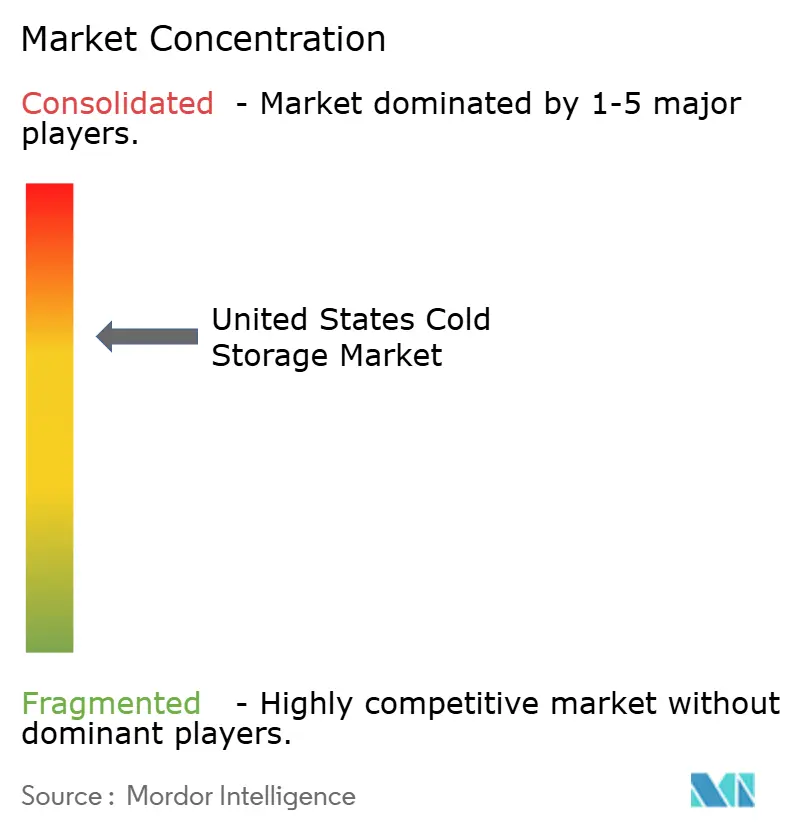

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Cold Storage Market Analysis by Mordor Intelligence

The United States cold storage market was valued at USD 52.40 billion in 2025 and is estimated to grow from USD 55.61 billion in 2026 to reach USD 73.83 billion by 2031, at a CAGR of 5.83% during the forecast period 2026-2031.

The current expansion of the United States' cold storage market reflects a wider shift in food distribution and pharmaceutical logistics toward regional temperature-controlled networks rather than short-cycle inventory additions. Demand is being shaped by longer lease commitments from food manufacturers, grocery retailers, and pharmaceutical distributors that want more reliable storage capacity and fewer supply chain disruptions. E-grocery fulfillment, pharmaceutical handling requirements, and higher facility design standards are pushing occupiers toward modern buildings with automation capabilities and stronger operational controls. Strategic activity in the United States cold storage market is also becoming more selective, with capital flowing toward large automated projects, energy upgrades, and facilities positioned near major trade, retail, and life sciences corridors. Regulatory pressure on refrigerants and the high energy load of refrigerated assets are also influencing investment decisions, which is widening the gap between advanced operators and aging facilities.

Key Report Takeaways

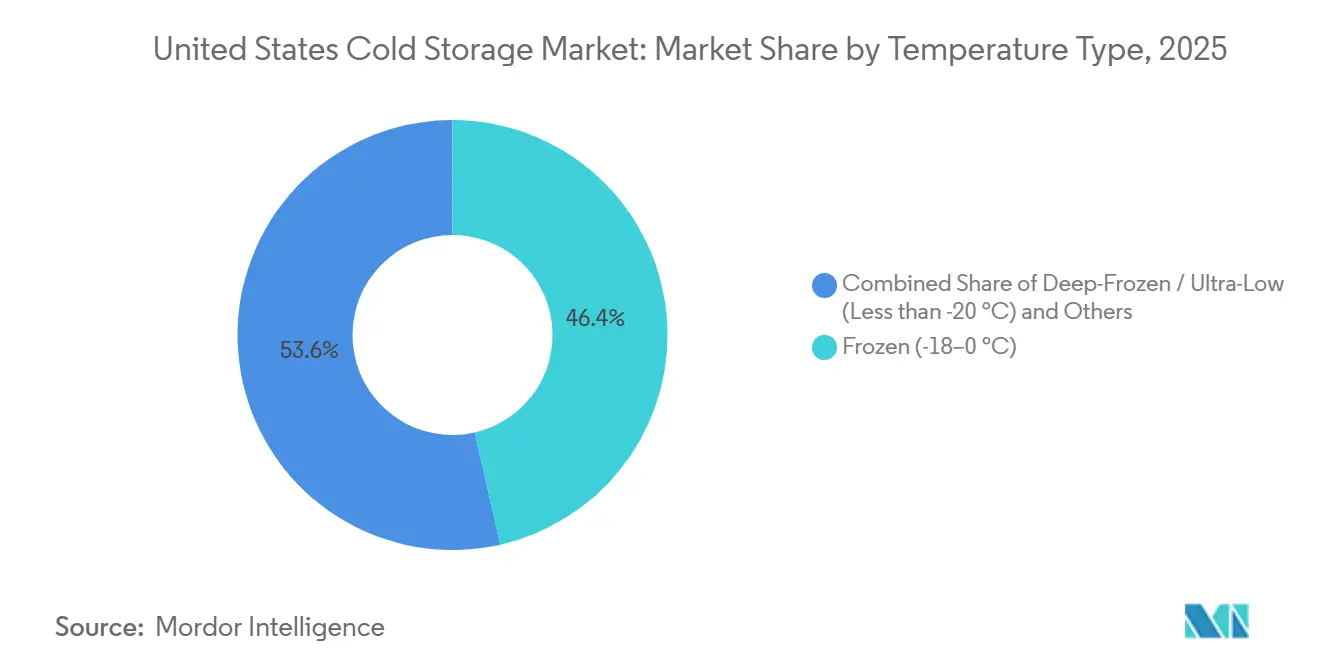

- By temperature type, frozen (-18–0 °C) held 46.44% of the United States cold storage market share in 2025, while deep-frozen/ultra-low (less than -20 °C) is projected to expand at an 11.09% CAGR through 2031.

- By automation level, conventional facilities accounted for 82.73% of the United States cold storage market size in 2025, while automated cold stores recorded the highest projected CAGR at 13.83% through 2031.

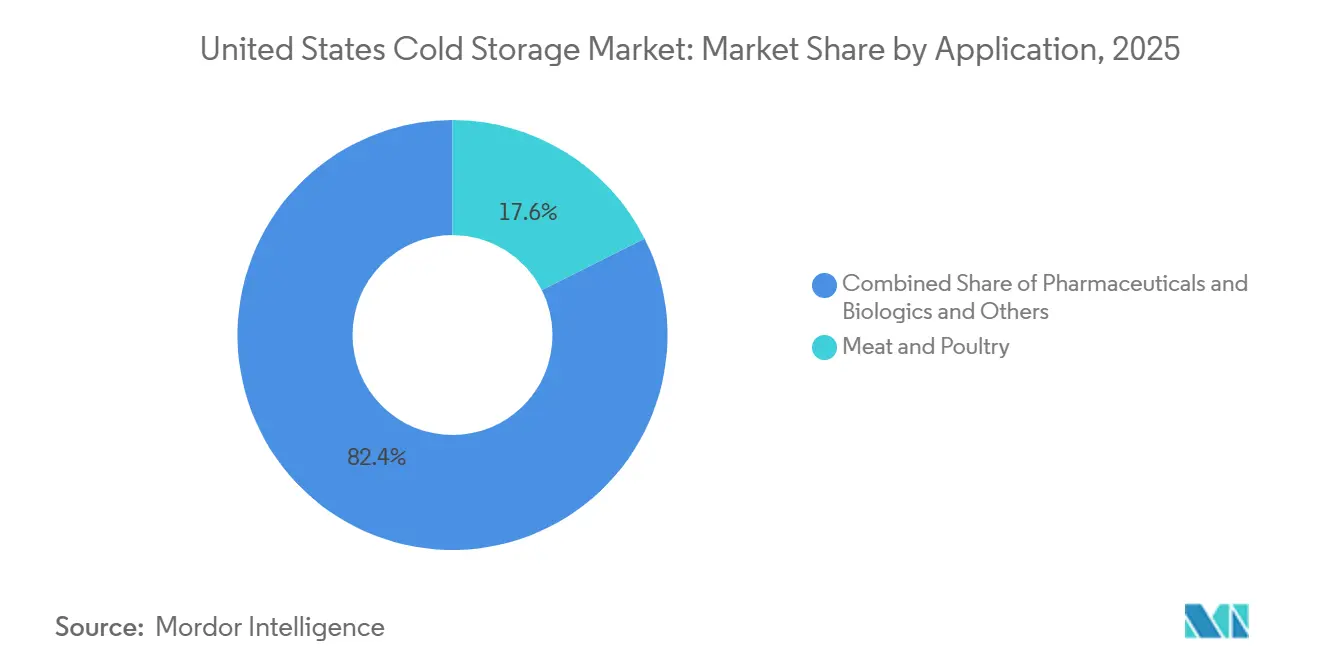

- By application, meat and poultry accounted for 17.59% of the United States cold storage market size in 2025, while pharmaceuticals and biologics are advancing at a 14.15% CAGR through 2031.

- By region, the West held 25.70% of the United States cold storage market share in 2025, while the Northeast recorded the highest projected CAGR at 10.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Cold Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Temperature-Controlled Grocery Fulfillment | +1.5% | National, concentrated in metro last-mile corridors across the Northeast, Sunbelt, and West. | Short term (≤ 2 years) |

| Pharmaceutical Cold Chain Expansion Beyond Food Logistics | +1.2% | Northeast, especially the New Jersey, Massachusetts, and Pennsylvania corridor, and the Sunbelt states such as Texas and North Carolina. | Medium term (2-4 years) |

| Automation-Ready Modern Facilities Capturing Occupier Demand | +1.0% | National, with strong new-build activity in Texas, Florida, Georgia, and Indiana | Medium term (2-4 years) |

| Energy-Efficiency Retrofits Improving Operating Economics | +0.7% | National, especially high-tariff states such as California and Texas | Short term (≤ 2 years) |

| Contracted Capacity as a Hedge Against Volatile Spot Inventory Cycles | +0.5% | Midwest, Southeast, and Southwest | Short term (≤ 2 years) |

| GLP-1 Driven Shifts in Food Mix and Cold-Chain Health Products | +0.8% | National, with spillover toward specialty pharmacy hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Temperature-Controlled Grocery Fulfillment

The United States cold storage market is benefiting from the steady buildout of refrigerated fulfillment infrastructure tied to online grocery and direct-to-consumer food delivery. Grocery retailers are reworking their distribution networks so that fresh, frozen, and prepared foods can move through more controlled handling points rather than general warehouse space. This raises the need for multi-temperature rooms, fast dock turnover, and urban cold nodes that can support repeat delivery cycles. NAIOP noted that the United States online grocery sales are on track to surpass USD 150 billion in 2026, supporting the case for continued investment in specialized refrigerated real estate[1]Source: NAIOP, “Cold Storage Investment: The Case for Temperature Controlled Real Estate,” NAIOP, naiop.org. As larger regional food distribution assets come online, the United States cold storage market is also seeing linked demand for smaller infill locations closer to dense metro delivery zones.

Pharmaceutical Cold Chain Expansion Beyond Food Logistics

The United States cold storage market is also being lifted by the rapid expansion of pharmaceutical logistics beyond the food-centered warehouse model. Biologics, biosimilars, and advanced therapies require tighter storage protocols, deeper validation, and more consistent chain-of-custody controls than typical food accounts. This pushes operators to invest in qualified chilled and ultra-low environments that can support higher-value products and stricter audit requirements. Demand remains concentrated in the Northeast, but the footprint is broadening as life sciences manufacturing activity grows in states such as Texas and North Carolina. This makes pharmaceutical handling one of the strongest quality-driven growth paths in the United States cold storage market, especially for operators that can combine temperature control, documentation, and modern infrastructure within a single network.

Automation-Ready Modern Facilities Capturing Occupier Demand

The United States cold storage market is moving toward automation as storage density, labor efficiency, and throughput become increasingly important in site selection. Automated storage and retrieval systems help operators use cubic space more effectively and reduce labor exposure in very cold environments where staff turnover is usually high. This is making automation a practical operating choice rather than a future concept for premium facilities. Lineage committed more than USD 740 million to develop 2 fully automated warehouses for Tyson Foods, and NewCold announced a USD 500 million-plus Phase 3 expansion in Lebanon, Indiana, with chilled and frozen zones and a 2D shuttle ASRS system[2]Source: Indiana Economic Development Corporation, “NewCold Plans Third Major Expansion in Lebanon, Growing Investment to $800M+,” Indiana Economic Development Corporation, iedc.in.gov. As a result, the United States cold storage market is rewarding operators that can deliver modern automation-ready facilities across frozen, chilled, and high-throughput formats.

Energy-Efficiency Retrofits Improving Operating Economics

The United States cold storage market is seeing stronger interest in retrofits because refrigeration remains the largest operating load in these facilities. Energy efficiency upgrades can improve margins while extending asset life in a segment where older buildings are becoming less competitive. Operators are focusing on controls, lighting, load management, and system design to reduce both baseline consumption and peak demand exposure. Americold reported more than USD 23 million of energy efficiency and facility improvement spending in 2025, including refrigeration controls and optimization projects across its network. The refrigerant transition under the AIM Act adds another reason for early upgrades, since operators who move sooner can align compliance planning with operating savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Refrigeration Power and Peak Load Exposure | -1.3% | National, with the sharpest pressure in California and Texas | Short term (≤ 2 years) |

| Very High Capital Intensity for New Build and Modernization | -1.0% | National, especially coastal and high-cost markets | Long term (≥ 4 years) |

| Shortage of Skilled Labor for Cold-Room and Automation Operations | -0.7% | National | Medium term (2-4 years) |

| Legacy Asset Obsolescence and Occupier Flight to Quality | -0.5% | Inland markets and secondary distribution corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Refrigeration Power and Peak Load Exposure

The United States' cold storage market faces persistent margin pressure from electricity costs, as refrigeration is the main power draw in most facilities. Operators in large demand centers also face high peak-load exposure, which can sharply lift bills during summer and high-utilization periods. This is especially difficult in regions where power pricing is already elevated and where demand charges punish short periods of load spikes. Central Valley Cold Storage showed PG&E commercial peak-period rates of USD 0.32 to USD 0.45 per kWh in 2026, underscoring the cost pressure major California operators must manage. The AIM Act transition adds another layer of cost because refrigeration system upgrades may improve long-run performance but require upfront spending before savings are fully realized.

Very High Capital Intensity for New Build and Modernization

The United States cold storage market is difficult for smaller operators because new development and modernization now require very large capital commitments. Conventional refrigerated projects already cost far more than ambient warehouses, and automated multi-temperature facilities require another major step up in spending. This narrows the developer pool to companies with access to institutional capital, infrastructure funding, or long-term tenant support. NewCold’s USD 500 million-plus Lebanon expansion and Igneo’s creation of ChillCo Logistics both show how large-scale capital is shaping the next build cycle[3]Source: Igneo Infrastructure Partners, “Igneo Announces Establishment of Cold Storage Platform With Acquisition of Mattingly Cold Storage,” Igneo Infrastructure Partners, igneoip.com. As funding becomes more concentrated, the United States cold storage market will likely continue to split into well-capitalized leaders and regional operators with limited conversion capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Temperature Type: Deep-Freeze Demand Accelerates as Frozen Storage Anchors Volume

Frozen (-18–0 °C) storage accounted for 46.44% of the United States cold storage market share in 2025, making it the largest temperature band by value. That position reflects the scale of protein processing, frozen meals, vegetables, and food service distribution across long-established supply chains. The segment also benefits from a deep installed base in the Midwest and Southeast, where manufacturers and processors generate steady throughput. Chilled storage remains important for fresh food, dairy, and some pharmaceutical flows, especially where retail replenishment requires faster cycling closer to demand centers. Ambient cold storage continues to serve narrower needs such as chocolates, wines, and temperature-sensitive materials that need control without full refrigeration.

Deep-frozen/ultra-low (less than -20 °C) is projected to grow at a 11.09% CAGR, giving it one of the most attractive expansion profiles in the United States cold storage market through 2031. The segment is being supported by cell and gene therapy storage, vaccine handling, and the broader need for validated ultra-low infrastructure. This is shifting investment toward facilities that can handle multiple temperature bands and maintain tighter monitoring standards. NewCold’s Lebanon Phase 3 project in Indiana shows how operators are building chilled and frozen capability together to improve flexibility across high-specification demand streams. In the United States, older deep-freeze capacity without automation or advanced controls is less likely to compete for premium biologics and specialty healthcare contracts.

By Automation Level (Storage): Conventional Stock Dominates, But Automation Capital Is Accelerating

Conventional facilities accounted for 82.73% of the United States cold storage market size in 2025, indicating that a significant share of the installed base still comes from older warehouse formats. This large share reflects decades of refrigerated construction that predated the current wave of dense automation and robotics. Many of these buildings continue to serve stable food accounts, especially in established processing corridors. Even so, customer expectations are changing as occupiers seek higher throughput, greater storage density, and reduced reliance on labor. This leaves conventional assets with a large base but a more selective future.

Automated cold storage is forecast to grow at a 13.83% CAGR, making it the fastest-growing format in the United States cold storage market. Higher labor costs, cold-room staffing challenges, and the value of cubic optimization are all supporting this shift. OPEX and Peltier also launched a multi-temperature automated cold storage solution in January 2026, showing that technology providers now see chilled and frozen automation as a practical commercial need rather than a niche product. In the United States cold storage industry, automation is no longer limited to the largest global players. However, access to capital still determines how quickly operators can convert plans into operating space.

By Application: Protein Anchors the Market While Pharma and Specialized Categories Outpace

Meat and poultry accounted for 17.59% of the United States cold storage market share in 2025, making it the largest application segment. Protein distribution remains a core demand base because it requires consistent frozen handling, large pallet volumes, and long-established distribution lanes across processors, retailers, and food service channels. The Midwest and Southeast remain especially important because they connect processing clusters to broad national consumption markets. Lineage’s acquisition of 4 Tyson Foods warehouses in Pennsylvania, Kansas, Illinois, and Arizona underscores the importance of protein infrastructure for leading operators and major food producers. Fish and seafood add another strategic layer, especially in port-linked corridors where imported and exported products need reliable temperature-controlled staging.

Pharmaceuticals and biologics are forecast to expand at a 14.15% CAGR, giving them the strongest growth profile among application categories in the United States cold storage market through 2031. Stricter handling standards, broader biologics pipelines, and the need for qualified chilled and ultra-low environments are lifting this segment. Vaccines and clinical trial materials also underscore the value of dedicated compliance infrastructure, as validated monitoring and traceability matter more in these flows than in standard food warehousing. Dairy and frozen desserts, bakery items, and ready-to-eat meals remain important but show more mature demand patterns tied to consumer distribution rather than regulatory specification. As a result, the United States cold storage market is likely to see a larger share of premium growth come from healthcare-linked categories than from volume-stable food applications.

Geography Analysis

The West accounted for 25.70% of the United States' cold storage market share in 2025, maintaining its position as the largest regional segment. This lead comes from major consumer demand centers, Pacific Rim produce and seafood flows, and agricultural output that needs year-round cold chain staging. Southern California remains especially strategic because it connects port activity, intermodal movement, and dense retail distribution. United States Cold Storage outlined plans for a Southern California automated facility with capacity for up to 200,000 pallets and direct access to an intermodal rail yard serving the Port of Los Angeles.

The Southwest is also attracting major investment within the United States cold storage market, especially in Arizona and Texas, where distribution access and development activity remain strong. Interstate Warehousing expanded its Kingman, Arizona, footprint in 2025, and Lineage began construction in 2026 with TGW Logistics on a large automated facility in Hutchins, Texas. The Northeast is the fastest-growing region at a 10.15% CAGR, supported by pharmaceutical logistics and dense urban food distribution. That combination gives the region a stronger premium mix than many other parts of the country.

The Southeast is absorbing a large share of new capacity because population growth, food manufacturing, and access to import-export continue to support warehouse demand. NewCold is completing its second automated frozen facility in McDonough, Georgia, in 2026, while Tippmann Group and Ahold Delhaize USA broke ground on a USD 860 million distribution center in North Carolina in the same year[4]Source: Tippmann Group, “Interstate Warehousing Expanding Kingman, Arizona Facility,” Tippmann Group, tippmanngroup.com. The Midwest remains a foundational operating region for the United States cold storage market because it still anchors protein processing and legacy food manufacturing volumes. Indiana now stands out as a major automation hub after NewCold lifted cumulative investment in its Lebanon campus to more than USD 800 million. Across both the Midwest and Southeast, demand is increasingly concentrated in newer facilities while older assets face weaker positioning if they lack automation, energy upgrades, and modern compliance standards.

Competitive Landscape

The United States cold storage market is moderately consolidated at the top tier, with Lineage and Americold controlling the largest institutional-grade refrigerated networks. Their scale matters because it supports national customer coverage, capital access, and the ability to invest in automation, energy systems, and specialized facility upgrades. This creates a clear advantage in large contracts that smaller regional providers may struggle to match. It also means that the leading operators can move faster when anchor tenants want new custom capacity.

Lineage has been one of the most active players in the United States cold storage market through acquisitions and long-term customer development. In April 2025, it acquired 4 Tyson Foods warehouses for USD 247 million and also committed more than USD 740 million to 2 automated greenfield projects for Tyson as anchor tenant. In May 2026, Americold announced a USD 1.3 billion joint venture with EQT, contributing 12 United States properties while retaining management control and using the structure to recycle capital. These moves show that leading companies are not only expanding their footprint but also changing how they fund growth.

Below the top tier, the United States cold storage market is becoming more competitive in selected corridors where automation-native and regional platforms are expanding. NewCold is building scale with high-density automated campuses, including the large Lebanon expansion in Indiana, and has added frozen capacity in Georgia. Igneo entered the space in April 2026 through the acquisition of Mattingly Cold Storage, which served as the founding asset of ChillCo Logistics, signaling growing infrastructure investor interest in platform-building. Technology is also becoming a separator, as automation software, warehouse execution tools, and higher energy efficiency can influence both operating costs and customer retention.

United States Cold Storage Industry Leaders

Lineage, Inc.

Americold Realty Trust

United States Cold Storage

Interstate Warehousing

FreezPak Logistics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Lineage, Inc. began construction on one of the largest automated cold storage distribution centers in the world in Hutchins, Texas, in partnership with TGW Logistics. The facility supports a major United States food producer and is expected to be completed by end-2027.

- May 2026: Americold Realty Trust and EQT announced a USD 1.3 billion North American cold storage joint venture. Americold contributed 12 United States properties, 124 million ft³, and more than 400,000 pallet positions.

- May 2026: Americold entered a multi-year agreement with Jeronimo Martins to manage storage and case pick fulfillment of 12 million cases of frozen products annually across 300 retail stores. The partnership created more than 80 new jobs and expanded Americold’s retail vertical in Europe.

- February 2026: NewCold announced its Phase 3 expansion at Lebanon, Indiana, a USD 500 million-plus investment for a new facility with chilled and frozen zones, the first North American 2D shuttle ASRS, and more than 200 permanent positions. Total campus investment exceeds USD 800 million.

United States Cold Storage Market Report Scope

| Chilled (0–5 °C) |

| Frozen (-18–0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (Less than -20 °C) |

| Conventional Facilities |

| Automated Cold Stores (AS/RS, Robotics) |

| Fruits & Vegetables |

| Meat & Poultry |

| Fish & Seafood |

| Dairy & Frozen Desserts |

| Bakery & Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals & Biologics |

| Vaccines & Clinical Trial Materials |

| Chemicals & Specialty Materials |

| Other Perishables |

| Northeast |

| Southeast |

| Midwest |

| Southwest |

| West |

| By Temperature Type | Chilled (0–5 °C) |

| Frozen (-18–0 °C) | |

| Ambient | |

| Deep-Frozen / Ultra-Low (Less than -20 °C) | |

| By Automation Level (Storage) | Conventional Facilities |

| Automated Cold Stores (AS/RS, Robotics) | |

| By Application | Fruits & Vegetables |

| Meat & Poultry | |

| Fish & Seafood | |

| Dairy & Frozen Desserts | |

| Bakery & Confectionery | |

| Ready-to-Eat Meals | |

| Pharmaceuticals & Biologics | |

| Vaccines & Clinical Trial Materials | |

| Chemicals & Specialty Materials | |

| Other Perishables | |

| By Region | Northeast |

| Southeast | |

| Midwest | |

| Southwest | |

| West |

Key Questions Answered in the Report

What is the 2031 value forecast for cold storage in the United States?

The United States cold storage market is projected to reach USD 73.83 billion by 2031, up from USD 55.61 billion in 2026, at a 5.83% CAGR over 2026-2031.

Which temperature segment leads revenue in the United States?

Frozen storage leads with 46.44% of the value in 2025, supported by protein processing, frozen foods, and foodservice distribution.

Which application is growing the fastest in refrigerated warehousing?

Pharmaceuticals and biologics are the fastest-growing application, with a projected 14.15% CAGR through 2031.

Why is automation becoming more important in temperature-controlled logistics?

Automated cold stores are projected to grow at 13.83% CAGR because they improve storage density, reduce labor exposure, and support higher throughput.

Which region offers the strongest growth outlook?

The Northeast is forecast to grow the fastest at a 10.15% CAGR through 2031, supported by pharmaceutical logistics and dense urban food distribution.

What are the main challenges facing operators?

Power costs, refrigerant compliance, and high capital spending remain the main constraints, especially for operators with older facilities or limited access to funding.

Page last updated on: