United States Bulky Waste Collection Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

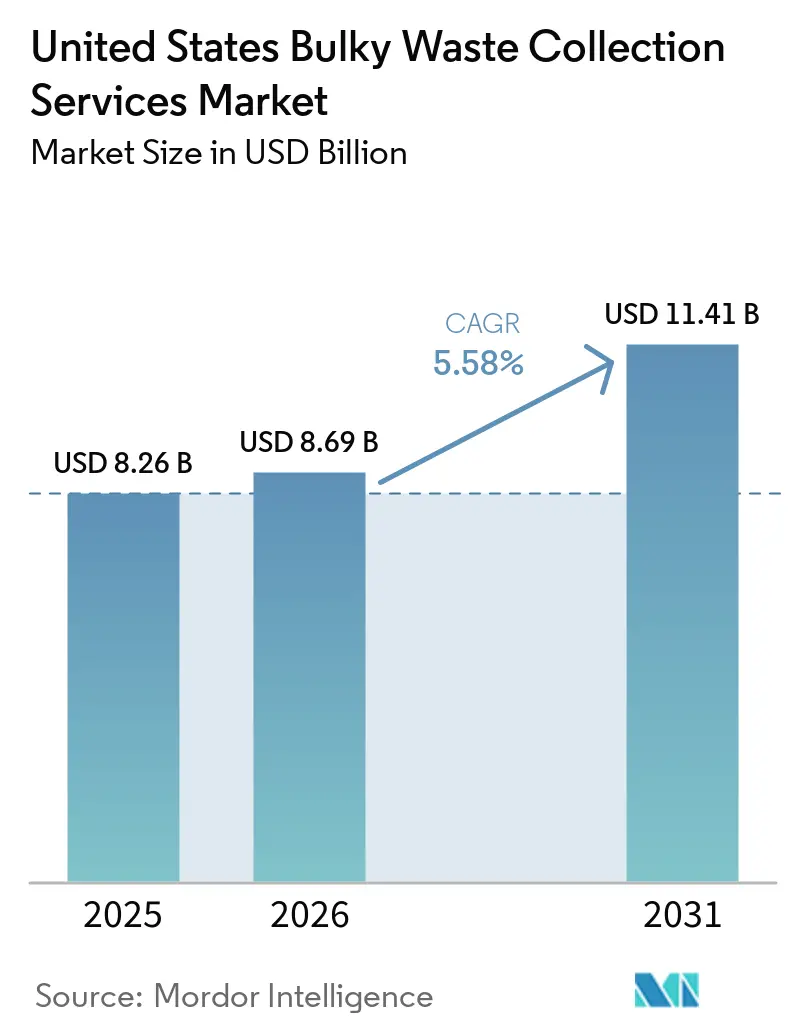

| Base Year Market Size (2025) | USD 8.26 Billion |

| Market Size (2026) | USD 8.69 Billion |

| Market Size (2031) | USD 11.41 Billion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Bulky Waste Collection Services Market Analysis by Mordor Intelligence

The United States Bulky Waste Collection Services Market size was valued at USD 8.26 billion in 2025 and is estimated to grow from USD 8.69 billion in 2026 to reach USD 11.41 billion by 2031, at a CAGR of 5.58% during the forecast period (2026-2031).

The growth outlook is steady and reflects an operational shift toward on-demand collection, tighter community rules on curbside placement, and recurring disaster recovery needs that create episodic surges in debris volumes. Competitive strategies center on disposal internalization, where integrated haulers protect margins by using owned landfills and transferring assets. At the same time, digital booking and same-day residential pickups increase consumer willingness to pay. Municipalities are renewing franchise agreements with larger operators that can bundle collection, transfer, and disposal under a single contract, aided by improved route optimization and customer-facing apps. The United States bulky waste collection services market also benefits from higher multifamily housing density in fast-growth corridors, which increases the frequency of furniture turnover and move-in discard events. Operator integration with emergency debris-removal protocols is widening the serviceable base by linking county-level programs with scalable private fleets.

Key Report Takeaways

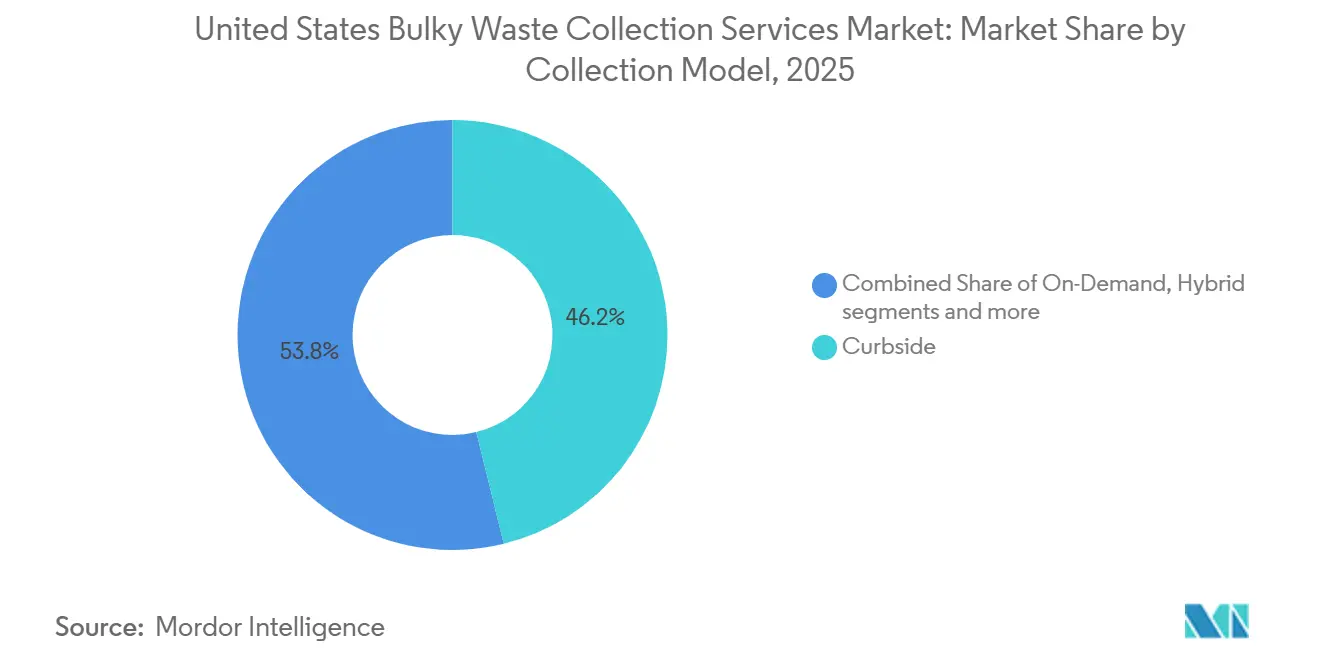

- By collection model, curbside led with 46.21% of the United States bulky waste collection services market share in 2025. The on-demand segment emerged as the fastest-growing, registering a 6.34% CAGR through 2031.

- By source, residential accounted for 60.12% of the United States bulky waste collection services market size in 2025 and is expanding at a 5.92% CAGR through 2031.

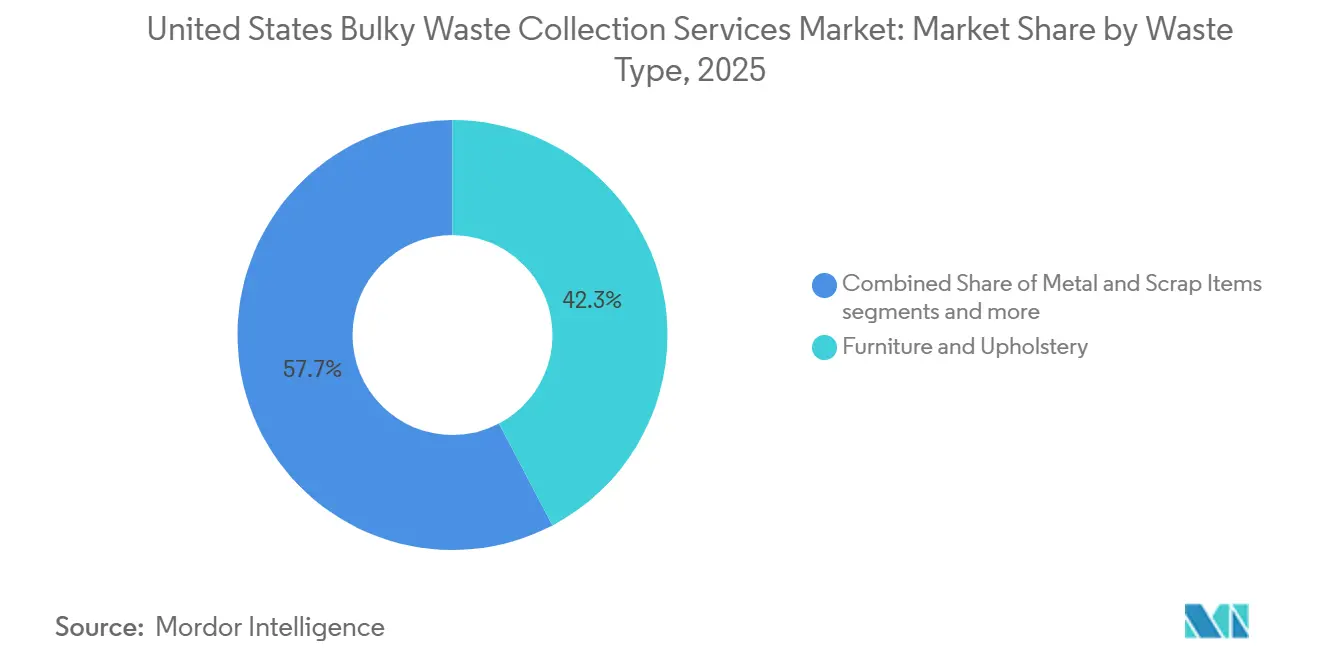

- By waste type, furniture & upholstery captured a 42.31% share in 2025 and is the fastest-growing, with a 6.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Bulky Waste Collection Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multifamily Housing Construction Boom in Sunbelt States | +1.2% | Texas Triangle, Phoenix metro, Atlanta metro, Charlotte metro | Medium term (2-4 years) |

| HOA Covenant Enforcement and Curbside Placement Restrictions | +0.8% | National, concentrated in Arizona, Nevada, Florida, Texas master-planned communities | Short term (≤ 2 years) |

| Hurricane and Wildfire Disaster Recovery Recurring Cycles | +0.9% | Gulf Coast and Atlantic seaboard, California wildfire zones | Short term (≤ 2 years) |

| Municipal Franchise Agreement Renewals Favoring Integrated Service Providers | +0.7% | National, with emphasis in regions facing landfill capacity constraints | Long term (≥ 4 years) |

| "Fast Furniture" E-Commerce Replacement Cycles Accelerating | +1.3% | National, strongest in last-mile dense metros | Medium term (2-4 years) |

| Junk Removal Franchising and Private Equity Consolidation | +0.6% | National, strongest in secondary metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Multifamily Housing Construction Boom in Sunbelt States

High-density multifamily projects increase furniture turnover and move-in discard events, leading to more on-demand bulky pickups and roll-off requests for property managers. New developments often use centralized enclosures that restrict oversized items and encourage scheduled or app-based removal instead of uncoordinated curbside placement. Minimum-service standards in large complexes favor operators that can respond quickly and provide digital confirmations for residents and leasing offices. The United States bulky waste collection services market benefits as these communities cluster in metros with sustained in-migration and active building pipelines. The resulting increase in service demand raises route density and reduces deadhead time for private fleets, supporting stable pricing over multi-year windows.

HOA Covenant Enforcement and Curbside Placement Restrictions

Homeowners associations commonly restrict bulk-item placement to narrow windows and assess fines for violations, which steers residents toward same-day or next-day removal booked through digital channels. This pattern is most visible in master-planned communities where design standards discourage curb piles and board rules convert occasional municipal pickups into recurring private calls. As a result, on-demand haulers expand into targeted ZIP codes with high HOA penetration and clear off-street pick-up requirements. The United States bulky waste collection services market is growing as households weigh the cost of a ticket and truck rental against the convenience of a scheduled garage-to-truck service. The enforcement environment aligns the incentives of residents, HOA boards, and haulers to meet short service windows while offering transparent pricing.

Hurricane and Wildfire Disaster Recovery Recurring Cycles

Recurring storms and wildfires generate debris surges that require rapid mobilization, staging, and final disposal, which expands demand for bulky collection, roll-offs, and transfer capacity. FEMA debris-removal missions and county-level emergency programs coordinate with private contractors, which raises volumes and operating hours during the recovery phase. These missions rely on multi-category sorting protocols and reimbursement frameworks that reward readiness and safety compliance. The United States bulky waste collection services market experiences these spikes as predictable seasonal patterns, especially along storm corridors and in fire-prone counties. Operators with existing municipal contracts, safety training, and scalable fleets are better positioned to secure task orders when emergency work begins.[1]Federal Emergency Management Agency, “Hurricane Debris Pick-Up a Priority for Florida Recovery,” FEMA, fema.gov

Municipal Franchise Agreement Renewals Favoring Integrated Service Providers

Cities with constrained landfill capacity prefer bidders that control disposal and transfer assets, which reduces exposure to spot tipping fees and contract disruptions. Contract scopes are broadening to include on-call bulky pickup modules that move ad hoc collections into a unified service plan for residents. Larger operators can bundle collection, transfer, disposal, and technology upgrades, such as customer portals and route optimization, thereby lowering total system costs. The United States bulky waste collection services market gains predictability as these renewals standardizes bulky-item response times and data reporting across neighborhoods. Global leaders demonstrate the model by expanding municipal portfolios and investing in integrated infrastructure that supports multi-service contracts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Illegal Dumping Epidemic on Federal and Rural Public Lands | -0.4% | Western states with extensive BLM holdings | Medium term (2-4 years) |

| Labor Shortage and Rising Insurance Costs for Manual Collection | -0.7% | National, most severe in tight labor markets | Short term (≤ 2 years) |

| State-by-State Mattress Recycling Infrastructure Gaps | -0.5% | 46 states without EPR programs, acute in large-population states | Long term (≥ 4 years) |

| Donation Center Capacity Saturation Post-Pandemic | -0.3% | Urban and suburban corridors with major thrift operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Illegal Dumping Epidemic on Federal and Rural Public Lands

Illegal dumping on public lands diverts funds to cleanup and weakens service expansion in rural counties, especially where distances to permitted sites are long. Cleanups range from modest efforts to complex projects involving hazardous materials, which can escalate costs and timelines. The visibility of dump sites then attracts more offenders, degrading property values and increasing enforcement demands. The United States bulky waste collection services market loses reportable volume when material bypasses formal channels and ends up on federal tracts. Federal agencies and cities document persistent costs, which reinforce the value of accessible legal options and resident education.

Labor Shortage and Rising Insurance Costs for Manual Collection

Operators face a constrained pool of commercial drivers and mechanics, which tightens route coverage and elevates overtime costs. Industry groups have called for stronger workforce development funding and training support to meet near-term hiring needs. Higher claim severities and reduced carrier appetite add pressure to insurance budgets, particularly for fleets that handle manual lifts and residential pickups. The United States bulky waste collection services market must absorb these costs through pricing and contract structures that reward operational safety and schedule reliability. Where labor is tight, larger operators with training programs and safety technology hold an advantage in municipal bids and private accounts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Collection Model: Curbside Dominates Market Demand

In 2025, curbside services captured a 46.21% market share, owing to their structured model that promises predictable collection schedules, clear placement guidelines, and dependable service for both residents and property managers. This segment benefits from HOA regulations and municipal frameworks that standardize waste placement and curbside collection processes. Regions with dedicated routes for bulky waste and adequate budget allocations have widely adopted municipal curbside programs, ensuring consistent service. Major players like Waste Management Inc. and Republic Services bolster curbside operations by focusing on route optimization and integration with disposal services. In summary, curbside services are a cornerstone of the United States' bulky waste collection market, especially in well-organized urban and suburban areas.

The United States bulky waste collection services market for on-demand collection is projected to grow at a 6.34% CAGR through 2031, supporting multi-truck franchise scaling and gains in route density in high-growth corridors. These patterns increase the addressable base for integrated haulers and franchise networks that coordinate through centralized dispatch and mobile driver tools.[2]Junk Rescue, “Understanding HOA Rules for Bulk Trash and Junk Pickup,” Junk Rescue, junkrescueaz.comGrowth in On-Demand is further reinforced by county emergency protocols and seasonal events that require rapid deployment of extra trucks, crews, and containers. Hybrid models that combine scheduled bulk days with on-demand pickups appeal to suburban municipalities, though adoption remains incremental in tight-budget areas. Contracted B2B agreements with multifamily communities and senior-living operators provide a stable base, but they grow more slowly than retail on-demand due to longer contract cycles.

Residential Leads on Share as Density and Turnover Lift Volumes

Residential sources accounted for 60.12% in 2025, reflecting higher move-in and move-out activity, furniture turnover, and HOA-driven compliance for visible curb placement. The segment captures episodic surges from storm and wildfire recoveries when debris removal becomes an urgent priority under emergency programs. These programs coordinate with private contractors and expand service hours and route coverage to clear neighborhoods and restore normal activity. The United States bulky waste collection services market benefits from predictable annual cycles that align crews, containers, and staging sites for short mobilizations and multi-week cleanups. Multifamily communities also drive recurring small-lot pickups that align well with on-demand booking and quick truck rollouts.

Commercial and municipal sources remain important in city centers and public facilities where planned renovations and periodic cleanouts occur on fixed schedules. Industrial sources grow with manufacturing and logistics expansions, although their share is smaller and tied to project timing. The United States bulky waste collection services market size for residential sources is expected to grow at a 5.92% CAGR through 2031, sustaining fleet utilization across suburban and urban routes. Integration with digital dispatch and customer notifications improves resident experience and reduces missed pickups, while owned disposal assets protect margins in capacity-constrained regions. These features help operators balance predictable residential baseloads with variable disaster-response assignments.

By Waste Type: Furniture & Upholstery Leads Share and Growth as Replacement Cycles Shorten

Furniture & Upholstery captured 42.31% share in 2025 and is the fastest-growing segment, with a 6.74% CAGR through 2031, supported by shorter replacement cycles and delivery models that simplify purchase and returns. Donation channels face capacity constraints in dense metros, leading to a higher proportion of collected furniture being sent to landfills when items are unsuitable for reuse. Operators with warehouse staging can triage for materials recovery and charitable partners, but quality and handling costs still limit diversions at scale. The United States bulky waste collection services market share for Furniture & Upholstery remains the largest within waste types, backed by recurring household updates and move-related dispositions. These characteristics raise average ticket values due to lift complexity and item size relative to other materials.

White goods and C&D debris maintain meaningful volume, with appliance pickups tied to replacement cycles and rebate-driven upgrades. Municipal contract scopes increasingly include on-call options for sofas and appliances, which channel ad hoc requests into baseline service levels for residents. The United States bulky waste collection services market's allocation of size to Furniture & Upholstery aligns with collection economics that reward operators for truck configuration, crew safety, and proper handling. Integrated haulers with transfer stations and landfill capacity can internalize tipping, while specialized franchise brands focus on fast response and customer service in residential neighborhoods. The balance of speed, safety, and diversion potential will define margin structures within this waste type across the forecast period.

Geography Analysis

The South holds the largest share of the United States bulky waste collection services market due to strong population growth, active multifamily development, and recurring hurricane-season debris surges. On-demand models are expanding in master-planned communities in Texas and Florida, where covenant enforcement narrows curbside placement windows and encourages garage-to-truck pickups. Emergency debris programs intensify activity during recovery periods, which increases roll-off demand and temporary staging needs for household bulky items. Cities and counties prefer service partners with disposal access and safety programs that can scale during peak weeks, which benefits integrated operators. These forces combine to lift baseline volumes and widen the addressable footprint of the United States bulky waste collection services market in fast-growth corridors.

The West shows elevated demand linked to wildfire recovery and urban density in major coastal metros. Counties with recurring fire seasons require rapid mobilization, hazardous-material handling, and coordinated staging that reward experienced contractors. Landfill access, transfer capacity, and engineered safety protocols are decisive in bid awards and task orders. The United States bulky waste collection services market is growing in these areas as local governments adopt on-call bulky pickup services and expand household coverage through app-based requests. The model reduces illegal curb placement and supports neighborhood quality-of-life goals during normal operations while retaining surge capacity for extraordinary events.

The Northeast and Midwest contribute a significant base for municipal and commercial contracts, with competitive renewals favoring disposal owners that can ensure long-term tipping. Urban density sustains steady curbside volumes and calls for consistent crew safety and predictable routing. Secondary metros across the Midwest attract franchise expansions where land costs and permitting timelines support fast openings. Rural corridors in the Mountain West continue to struggle with illegal dumping on public lands, which signals unmet demand for accessible, affordable collection in remote areas. These conditions shape localized strategies within the United States bulky waste collection services market, as operators match service tiers to regional needs.[3]Bureau of Land Management, “Protect Wyoming’s Public Lands from Illegal Dumping,” U.S. Department of the Interior, blm.gov

Competitive Landscape

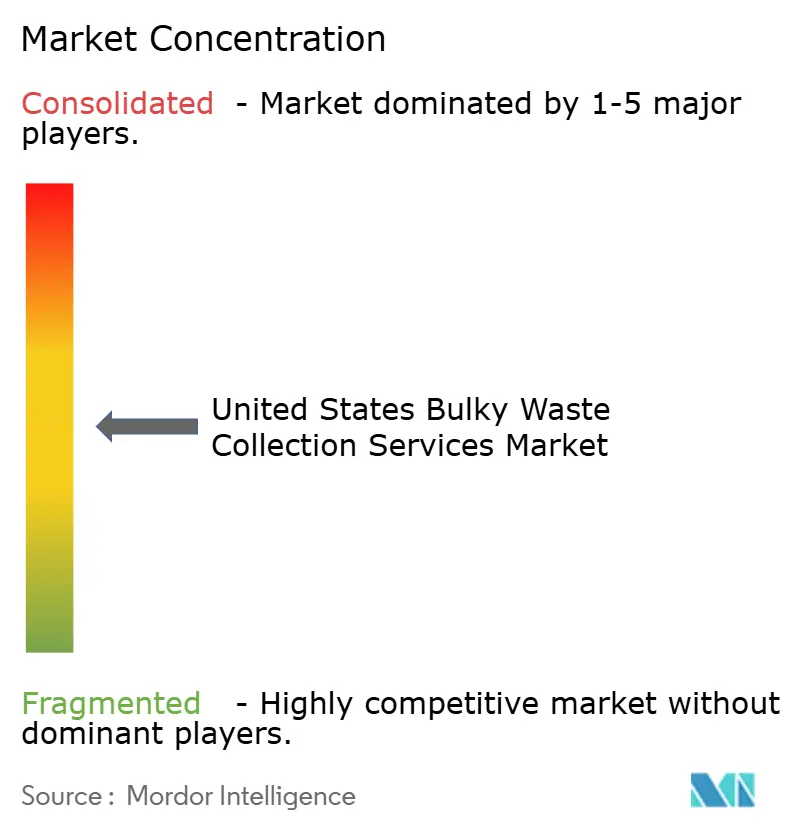

The United States bulky waste collection services market is moderately fragmented, with a few large integrated haulers with strong disposal assets alongside a broad base of regional operators, franchise networks, and independent service providers. The competitive field in the United States bulky waste collection services market is split between integrated haulers with disposal assets and a large tail of franchise brands and independents. Disposal internalization provides a cost advantage by avoiding third-party tipping and stabilizes margins in capacity-constrained regions. Integrated players have expanded in growth markets through acquisitions that densify routes and bring additional transfer and landfill capacity. Franchise networks compete on responsiveness, transparency, and customer service, with centralized booking and dispatch that enable same-day pickups. These differences have narrowed as integrated haulers launch consumer-facing portals and pilot on-demand pickup services to meet residential demand.

Strategic moves continue to reshape regional positions. GFL completed a large platform acquisition focused on industrial and municipal waste, adding sites, trucks, and disposal assets that improve internalization and operating leverage. In Texas, a tuck-in acquisition expanded GFL’s presence across the state’s growth triangle, with the acquired leadership team retained to maintain continuity. Casella expanded its New England footprint by acquiring Star Waste Systems, adding residential, commercial, and C&D processing capacity across multiple facilities that support route density and disposal access. These transactions reinforce the role of integrated networks within the United States bulky waste collection services market and highlight the premium on asset control.

Global leaders are also expanding specialty capabilities relevant to municipal and institutional contracts. Veolia’s agreement to acquire Clean Earth expands its hazardous-waste treatment and PFAS management capabilities, which can be important for public contracts involving complex materials. Veolia’s federal services arm secured a five-year DOE ordering vehicle for the treatment of specific low-level waste categories, reinforcing its technical depth to support complex cleanup tasks. In the United Kingdom, Veolia and SUEZ reported significant municipal renewals and new awards, reflecting an integrated model increasingly mirrored in United States city procurements. These moves support the United States bulky waste collection services market by diffusing technology, compliance expertise, and integrated operations across regions and service types.

United States Bulky Waste Collection Services Industry Leaders

Waste Management, Inc.

Republic Services, Inc.

GFL Environmental Inc.

Waste Connections, Inc.

Veolia Environnement SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GFL Environmental and SECURE Waste Infrastructure announced a transaction valued at approximately USD 6.4 billion that expands GFL’s footprint and is positioned to be accretive to adjusted free cash flow per share in year one, with expected cost opportunities and expanded facility coverage in North America. The combined network increases disposal optionality and densifies routes in energy and municipal waste corridors.

- April 2026: Casella Waste Systems completed the acquisition of Star Waste Systems, adding about USD 100 million in annualized revenue across residential, commercial, and roll-off services, along with a C&D processing and transfer site that strengthens its New England operations.

- November 2025: Veolia signed a definitive agreement to acquire Clean Earth from Enviri, positioning the company as a leading hazardous-waste player in the United States and expanding its PFAS treatment capabilities for municipal and industrial clients.

United States Bulky Waste Collection Services Market Report Scope

| Curbside |

| On-Demand |

| Hybrid |

| Contracted B2B |

| Others |

| Residential |

| Commercial |

| Industrial |

| Municipal/Government |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) |

| Furniture & Upholstery |

| Metal & Scrap Items |

| White Goods/Appliances |

| Construction & Demolition |

| Others |

| By Collection Model | Curbside |

| On-Demand | |

| Hybrid | |

| Contracted B2B | |

| Others | |

| By Source | Residential |

| Commercial | |

| Industrial | |

| Municipal/Government | |

| Others (Religious Institutions, Temporary Disaster Relief Camps, Film/TV Production Sets) | |

| By Waste Type | Furniture & Upholstery |

| Metal & Scrap Items | |

| White Goods/Appliances | |

| Construction & Demolition | |

| Others |

Key Questions Answered in the Report

What is the current size and growth outlook for the United States bulky waste collection services market?

The United States bulky waste collection services market size was USD 8.26 billion in 2025 and is projected to reach USD 11.41 billion by 2031, at a 5.58% CAGR over 2026-2031.

Which collection model is growing the fastest across the United States bulky waste collection services market?

On-Demand is the fastest-growing model at a 6.34% CAGR through 2031, supported by same-day pickup expectations.

Which source category leads the United States bulky waste collection services market by share?

Residential leads with 60.12% share in 2025, reflecting higher move-related discards, furniture turnover, and emergency debris removal volume during storm and wildfire recoveries.

What is the largest waste type within the United States bulky waste collection services market?

Furniture & Upholstery is the largest waste type, with a 42.31% share in 2025, and it is also the fastest growing, with a 6.74% CAGR through 2031.

How are integrated haulers competing in the United States bulky waste collection services market?

Integrated haulers focus on internalizing disposal through acquisitions and asset densification, stabilizing margins, and enabling competitive pricing in municipal and residential contracts.

What external events most influence demand swings in the United States bulky waste collection services market?

Hurricanes and wildfires create episodic debris surges that raise demand for bulky pickups, roll-offs, and temporary staging, coordinated through FEMA and county emergency programs.

Page last updated on: