Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 14.01 Billion |

| Market Size (2026) | USD 14.45 Billion |

| Market Size (2031) | USD 16.91 Billion |

| Growth Rate (2026 - 2031) | 3.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Alfalfa Market Analysis by Mordor Intelligence

The United States alfalfa market was valued at USD 14.01 billion in 2025 and is estimated to grow from USD 14.45 billion in 2026 to USD 16.91 billion by 2031, at a CAGR of 3.2% during the forecast period from 2026 to 2031. Domestic livestock demand, driven by dairy and beef feeding systems, continues to provide the United States alfalfa market with a stable demand base, even as export conditions remain uneven[1]Source: USDA Economic Research Service, “Livestock, Dairy, and Poultry Outlook: August 2025,” ers.usda.gov. According to United States Department of Agriculture (USDA)- National Agricultural Statistics Service price data, alfalfa remained the United States' fourth most valuable field crop in 2025, with a farm gate value of approximately USD 8.5 billion and average prices near USD 171 per metric ton. These figures are sustaining supply investment across irrigated western states and expanding non-irrigated eastern belts. Export pressure, lower per-unit margins, and water constraints in western states are pushing the United States alfalfa market toward larger, more capitalized operators. These pressures are also encouraging a product mix shift toward pellets, cubes, and other higher-value formats that better align with domestic equine and specialty nutrition demand.

Key Report Takeaways

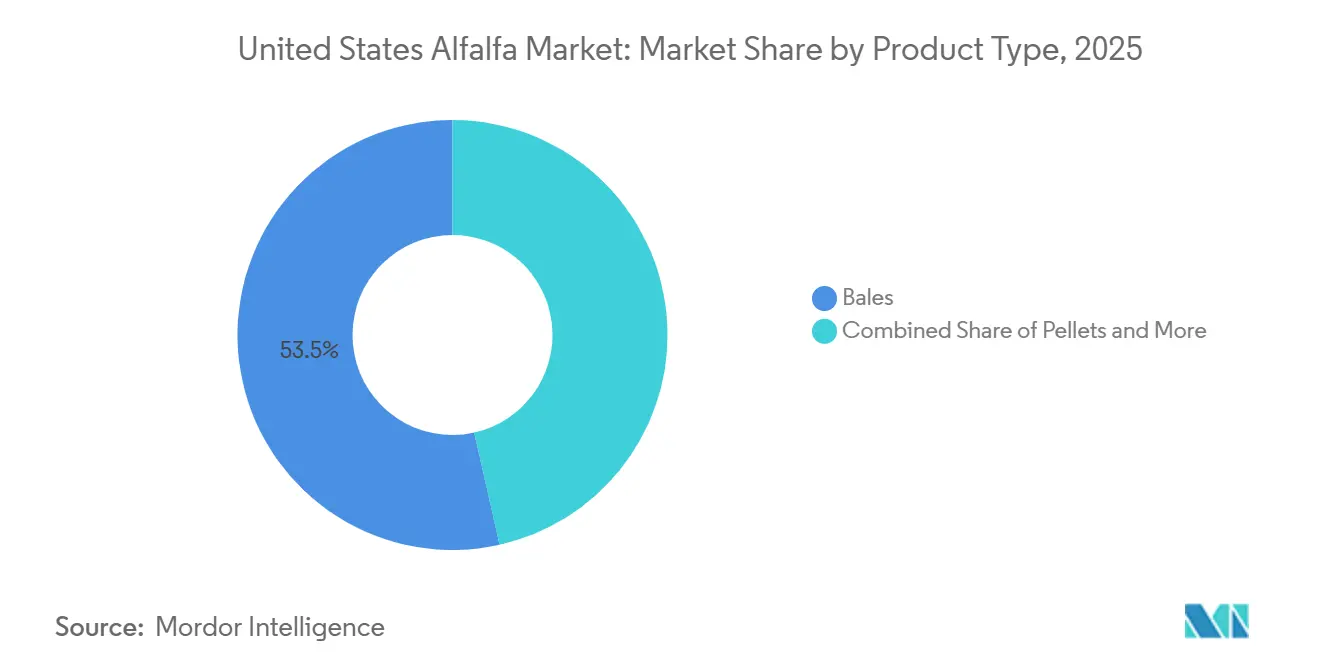

- By product type, bales is the largest segment in the United States Alfalfa Market, holding 53.5% of the market share in 2025, while pellets are the fastest growing segment, anticipated to expand at a 3.0% CAGR between 2026 and 2031.

- By application, dairy cattle feed is the largest segment, accounting for 80.4% of the market share in 2025, while equine feed is the fastest growing segment, anticipated to expand at a 4.6% CAGR between 2026 and 2031.

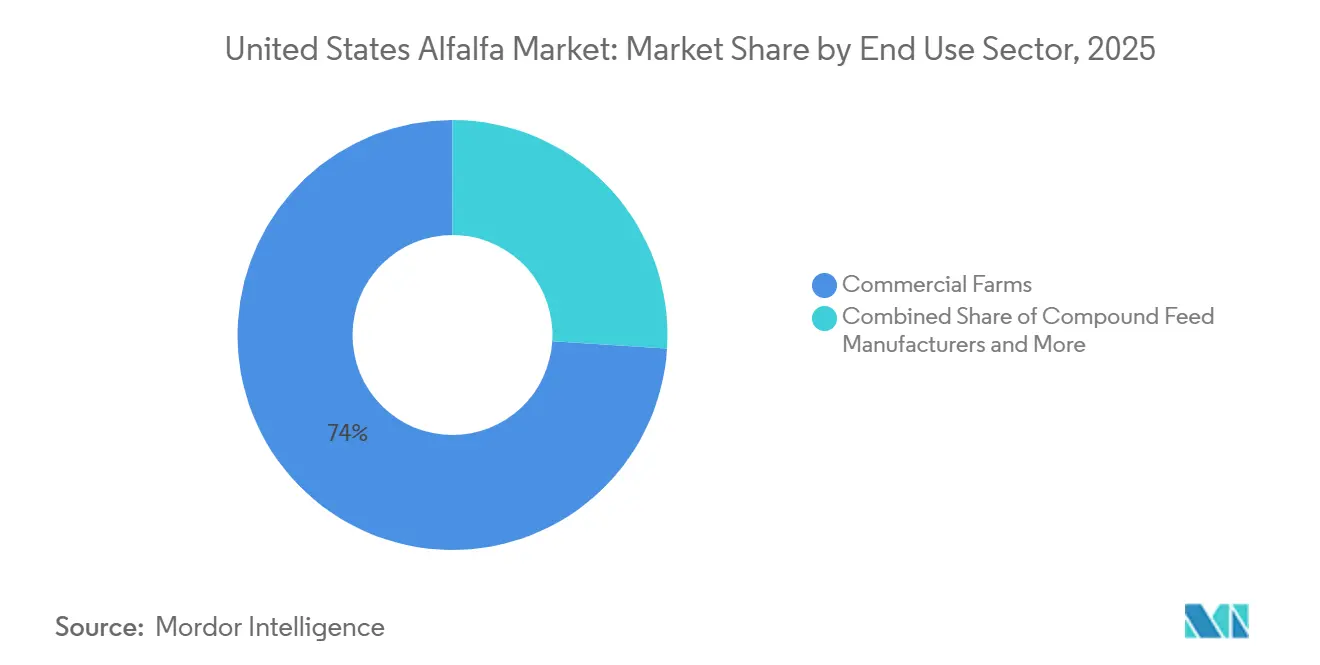

- By end use sector, commercial farms are the largest segment in the United States Alfalfa Market, representing 74.0% of the market size in 2025, while pet food and specialty nutrition is the fastest growing segment, anticipated to expand at a 9.0% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Alfalfa Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of irrigated alfalfa acreage in high-yield western corridors | +0.7% | United States, concentrated in California, Idaho, Washington, Arizona, and Nevada | Medium term (2-4 years) |

| Export pull from Asia-Pacific and Middle East feed buyers | +0.8% | United States exporters, with demand from China, Japan, South Korea, Saudi Arabia, and the United Arab Emirates (UAE) | Short term (≤ 2 years) |

| Shift toward higher-margin forage crops on water constrained farmland | +0.5% | United States, especially the Southwest and Pacific West | Long term (≥ 4 years) |

| Rising demand for high-protein dairy and beef rations | +0.6% | United States, concentrated in the Upper Midwest and western dairy states | Medium term (2-4 years) |

| Adoption of certified seed, heat-tolerant varieties, and precision irrigation | +0.5% | United States, with early adoption in California and Idaho | Long term (≥ 4 years) |

| Soil health value from alfalfa in rotation systems | +0.3% | United States, mainly the Midwest and Southeast grain belt | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Export Pull from Asia-Pacific and Middle East Feed Buyers

The market continues to benefit from structural import dependence in East Asian and Gulf dairy systems, despite weaker Chinese buying in 2025. Saudi Arabia and the United Arab Emirates (UAE) rely on imported forage, as water scarcity and food security policies limit local production, keeping offshore demand relevant for United States exporters[2]Source: United States Department of Agriculture, “Alfalfa Demand in Northern China - Market Trends Challenges and Outlook,” apps.fas.usda.go. In 2025, Japan imported 329,559 metric tons of United States alfalfa, South Korea imported 210,746 metric tons, and Saudi Arabia imported 277,987 metric tons, creating a broad alternative demand base as China reduced purchases. The shift away from China is reshaping trade relationships rather than reducing overall export demand, helping the United States alfalfa market maintain value in premium supply chains tied to established buyers. Producers with established export infrastructure in California and Washington are better positioned to capture this redirected demand than operators serving only domestic spot markets.

Rising Demand for High-Protein Dairy and Beef Rations

The United States alfalfa market continues to draw strength from dairy and beef feed systems, as alfalfa remains difficult to replace in high-performance rations. The United States Department of Agriculture Economic Research Service (USDA ERS) projected the dairy cow inventory at 9.45 million head in 2025 and annual milk yield per cow at 24,255 pounds (11,001.8 Kg), supporting continued demand for nutrient-dense forage[3]Source: USDA Economic Research Service, “Livestock, Dairy, and Poultry Outlook: August 2025,” ers.usda.gov. A 2025 Purina Mills study on beef-on-dairy crossbreeding showed that such breedings declined by 5% in 2024, prompting herd managers to focus more on milking efficiency and replacement heifers, both of which favor high-specification feed inputs. The National Animal Nutrition Research Association (NANRA) reported in 2025 that more than 60% of added feed ingredients went into dairy and beef cattle diets, confirming where feed demand is concentrated. This keeps the United States alfalfa market closely tied to large livestock systems where fiber digestibility and protein density are critical at the ration level.

Adoption of Certified Seed, Heat-Tolerant Varieties, and Precision Irrigation

Technology adoption is emerging as a long-term support factor for the United States alfalfa market, as growers facing water constraints seek to maintain yields with fewer resources. Research published in Crops and Soils on Precision Irrigation Technologies for Water-Wise and Climate Resilient Alfalfa Production in 2024 found that deficit irrigation at 25% below full irrigation maintained comparable yields across several western trial sites while also improving forage nutritive value. The same study found that low elevation sprinkler systems outperformed mobile drip irrigation across environments, indicating that equipment selection is a key productivity factor independent of irrigation volume. These developments support a more resilient production base for the United States alfalfa market, where operators can invest in improved seed varieties, irrigation systems, and field management practices.

Expansion of Irrigated Alfalfa Acreage in High-Yield Western Corridors

The United States alfalfa market remains heavily dependent on high-productivity western corridors, which benefit from irrigation access, scale, and export links. According to United States Department of Agriculture Crop Production Summary 2025, the total harvested acreage reached 14.7 million acres in 2025, up from 14.6 million acres in 2024. Record yields were reported in Iowa and Wisconsin, indicating that productivity gains are extending beyond the traditional western core. In Idaho's Magic Valley, California's Imperial and San Joaquin valleys, and Washington's Columbia Basin, margin pressure is encouraging larger operators to consolidate acreage vacated by smaller growers.The continued investment in water-efficient western acreage helps explain why the United States alfalfa market remains concentrated in these corridors despite tighter resource conditions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Water allocation limits in drought-stressed production states | -0.9% | United States, especially California, Arizona, Nevada, and Colorado River basin states | Short term (≤ 2 years) |

| High pumping, drying, and baling costs | -0.7% | United States, most acute in energy intensive irrigated western states | Medium term (2-4 years) |

| Freight and handling losses in long-distance export chains | -0.6% | United States export oriented producers in California, Washington, and Oregon | Medium term (2-4 years) |

| Quality downgrades from heat, dust, and inconsistent storage | -0.5% | United States, with higher risk in hot and arid southwestern states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Water Allocation Limits in Drought-Stressed Production States

Water access remains the most significant structural constraint on the United States alfalfa market, as western production is closely tied to drought-stressed basins and regulated groundwater systems. Arizona's agricultural allocation for Colorado River water was fully cut off in both 2023 and 2024, and central Arizona alfalfa cultivation declined by 48% between 2022 and 2024 in the affected farming areas. In December 2024, the Arizona Attorney General filed a lawsuit against Fondomonte LLC, a subsidiary of Almarai, over groundwater extraction in La Paz County, indicating that regulatory attention was shifting beyond general water policy toward direct enforcement. As the regulations tighten, larger operators that can more effectively manage compliance, water rights, and legal exposure are likely to gain an advantage over smaller farms in the United States alfalfa market.

High Pumping, Drying, and Baling Costs

Cost inflation is limiting earnings across the market even where demand remains stable. The American Farm Bureau Federation (AFBF) reported in 2026 that input costs for water, fertilizer, labor, fuel, and machinery had risen by 20% to 35% since 2020 across major producing states. Average full economic production cost reached USD 229 per metric ton in 2025, while the average farm gate price was USD 171 per metric ton, leaving a gap of USD 58 per metric ton and market losses of approximately USD 2.9 billion. Farm prices had fallen by 43% from the 2021 to 2022 peak of USD 288 per metric ton to USD 164 per metric ton by November 2024, and the 2025 recovery had still not restored break-even economics for most operators. This is pushing the United States alfalfa market toward larger and more mechanized farms that can absorb margin pressure for longer periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pellets Gaining Ground in Export-Ready and Specialty Formats

Bales held 53.5% of the United States alfalfa market share in 2025, maintaining their position as the leading product type by revenue due to their deep integration into large dairy and beef operations. Cubes continue to serve equine and specialty small animal demand where lower dust levels and controlled intake are priorities. Compressed formats remain important for export-oriented supply chains, as they are better suited to long-distance handling and container logistics than loose bulk movement. This has resulted in a market structure where commodity bales preserve the volume base while pellets and related processed formats capture a greater share of value growth.

Pellets are the fastest growing product type in the United States alfalfa market, with this segment forecast to grow at a 3.0% CAGR from 2026 to 2031. Demand is rising because pellets are well suited to commercial equine feeding, specialty animal nutrition, and export channels that value consistent density, easier handling, and lower storage risk. The broader shift toward precision feeding is also making standardized product formats more attractive to buyers seeking repeatable ration performance over bulk commodity variation.

By Application: Dairy Feed Dominates While Equine Feed Records Fastest Growth

Dairy cattle feed accounted for 80.4% of the United States alfalfa market share in 2025, reflecting the central role of dairy in demand. In high-yield herds, alfalfa contributes 18% to 22% of ration dry matter, a role closely tied to the 9.45 million dairy cows reported for 2025. Beef cattle feed is the second largest application, supported by continued use of alfalfa to balance concentrate-heavy diets amid tight cattle supplies. Poultry feed uses alfalfa primarily as a nutritional and pigmentation supplement, making it a smaller and relatively stable part of the United States alfalfa market.

Equine feed is forecast to expand at a 4.6% CAGR from 2026 to 2031, making it the fastest growing application in the United States alfalfa market. In June 2025, Standlee Premium Products LLC and Triple Crown Nutrition launched the Diamond Line, a six-product premium equine range combining alfalfa-based forage with a specialized nutritional formulation. This launch reflects rising demand for traceable, higher-specification forage in managed boarding facilities and organized sport settings where feed consistency is important. Small ruminant and camelid feed remain relevant niche applications, and their growth supports broader quality improvements in moisture control, dust reduction, and testing across the value chain.

By End Use Sector: Pet Food and Specialty Nutrition Emerging as a High-Growth Channel

Commercial farms held a 74.0% share of the United States alfalfa market in 2025, reflecting their procurement scale, integrated logistics, and long-term grower relationships. Their position is further supported by their ability to absorb cost fluctuations and secure supply across multiple states, which smaller buyers cannot consistently replicate. Compound feed manufacturers represent another significant organized buyer segment, purchasing meal and dehydrated pellets for balanced ration products tied to overall livestock production volumes. Household and hobby animal owners form a smaller but growing channel, increasingly purchasing cubes and pellets online in 20 kg to 40 kg packs, which supports higher unit pricing in the United States alfalfa market.

The pet food and specialty nutrition segment is forecast to grow at a 9.0% CAGR from 2026 to 2031, making it the fastest-growing segment in the United States alfalfa market. Oxbow Enterprises, Inc has established a notable position in premium small animal hay by applying quality standards for mycotoxins, heavy metals, and pesticide residues, which requires greater supplier discipline. In October 2025, Leaft Foods partnered with Meateor Pet Food Ingredients to distribute alfalfa protein concentrate in the United States pet nutrition channel, expanding alfalfa's application beyond forage into functional ingredient use. This channel is outperforming others because companion animal buyers are applying human food-style quality expectations to fiber and protein ingredients, creating a faster-growing premium outlet in the United States alfalfa market.

Geography Analysis

Harvested acreage in the United States alfalfa market reached 14.7 million acres in 2025, with a large share of premium and export-oriented production concentrated in irrigated western corridors. California's Imperial and San Joaquin valleys, Idaho's Magic Valley, and Washington's Columbia Basin remain central production areas due to their combination of scale, irrigation infrastructure, and export logistics. These regions are significant not only for production volume, but also for their ability to serve buyers requiring compressed, processed, or specification-based forage. Within this western core, operators with water security and logistics assets are gaining ground as smaller growers face tighter margins and higher compliance costs.

Non-irrigated eastern and Upper Midwest belts are becoming more important to the United States alfalfa market as productivity gains broaden the supply base. Iowa and Wisconsin reported record yields in 2025, reflecting improvements in crop genetics and field management outside the traditional export belt. This is significant because dairy demand is also concentrated in the Upper Midwest, which reduces freight exposure when forage can be sourced closer to herd locations. Rotation benefits further support eastern and Midwestern acreage, as alfalfa contributes soil health value in grain-oriented systems where producers require agronomic flexibility. As a result, the United States alfalfa market is no longer solely a western irrigation story, even as the west retains its premium export and processing role.

The Southwest remains the most stressed part of the United States alfalfa market, as Arizona and nearby basin states face hard water limits and increasing political scrutiny. Foreign-owned operations have also come under closer review, raising compliance requirements for groundwater use in Arizona. The geographic balance within the United States alfalfa market is therefore shifting toward water-secure operations and away from acreage dependent on increasingly contested water supplies.

Competitive Landscape

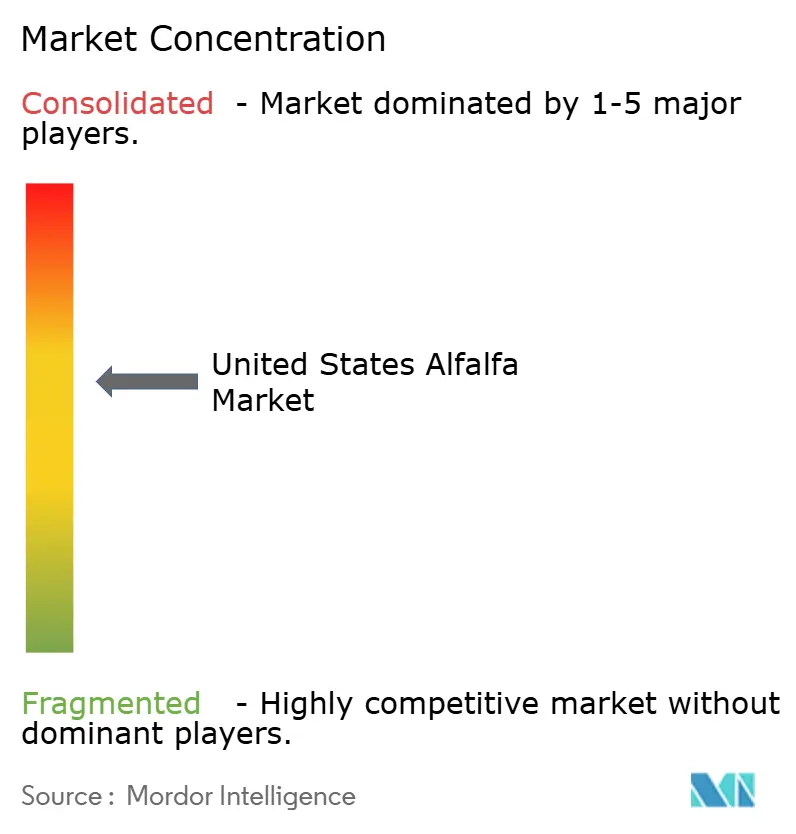

The United States alfalfa market is moderately concentrated, with the top five companies, such as Standlee Premium Products LLC, Al Dahra ACX Global Inc, Anderson Hay and Grain Inc., Green Prairie International Inc., and Border Valley Trading, holding a major share in 2025. This keeps the market concentrated at the top while remaining active among smaller players, supporting consolidation where scale, product processing, and branded distribution matter more than raw volume.

Strategic activity in 2025 and 2026 suggests that competition in the United States alfalfa market is evolving along several simultaneous trajectories. Anderson Hay & Grain Co., Inc. continued its Chapter 11 restructuring proceedings through 2026, with court actions pertaining to financing arrangements and asset sales reflecting an ongoing reorganization rather than liquidation. In response to the United States-China export disruption of 2025, Al Dahra ACX Global Inc. leveraged its diversified global sourcing network encompassing established sourcing operations in both Spain and the United States to reduce its dependence on any single trade corridor. Standlee Premium Products LLC pursued a distinct strategy, expanding its branded nutrition portfolio through the launch of the Diamond Line in June 2025. Collectively, these developments highlight a growing divergence within the United States alfalfa market between restructuring activity in commodity oriented businesses and brand building initiatives within specialty nutrition channels.

Mid-tier competition in the United States alfalfa market is increasingly tied to pelletizing, cubing, and other processing capabilities that serve equine, pet, and export customers with tighter specifications. A further strategic opening is emerging in western irrigated acreage, where financial stress and water regulation are driving ownership shifts. At the same time, foreign capital-backed operators with strong end-market links in Saudi Arabia and the United Arab Emirates face greater scrutiny over groundwater use in Arizona, adding regulatory risk to expansion plans. Overall, the United States alfalfa market remains competitive, with advantage shifting toward firms that combine scale, processing, customer access, and regulatory compliance.

United States Alfalfa Industry Leaders

Standlee Premium Products LLC

Al Dahra ACX Global Inc.

Green Prairie International Inc.

Anderson Hay & Grain Co., Inc.

Border Valley Trading, Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Standlee Premium Products launched Alfalfa Mini Cubes, extending its mini cubes forage format from timothy grass to alfalfa and giving horse owners a more convenient, dust-reduced option for stall and trail feeding. The new SKU strengthens Standlee’s strategy of converting bulk alfalfa bale buyers into higher-margin packaged forage consumers in the Western and Mountain states equine retail channel.

- June 2025: The United States Food and Drug Administration (FDA) completed its Plant Biotechnology Consultation Program review of Cibus' altered lignin alfalfa trait, clearing the way for S&W Seed Company to commercialize the first gene-edited alfalfa varieties in the United States. S&W Seed Company, headquartered in Longmont, Colorado, announced two initial commercial varieties, Fall Dormancy 5 and Fall Dormancy 7. These varieties were developed to improve ruminant digestibility and support more flexible harvest timing without increasing inputs per acre. This launch offers growers in the Southwest and Intermountain West improvements in yield potential and feed quality.

- June 2025: Standlee Premium Products LLC and Triple Crown Nutrition jointly launch the Diamond Line, a 6 product premium equine nutrition range combining Standlee’s alfalfa based Western forage with Triple Crown’s EquiMix nutritional formulation. The Diamond Line targets a higher specification equine feeding tier than either company had previously occupied independently.

United States Alfalfa Market Report Scope

Alfalfa is obtained from the alfalfa plant, also known as lucerne (Medicago sativa). It is cultivated as an important forage crop and is widely used in animal nutrition because of its high protein content and forage value.

The United States Alfalfa Market is Segmented by Product Type (Bales, Pellets, Cubes, and Compressed Bales), by Application (Dairy Cattle Feed, Beef Cattle Feed, Poultry Feed, Equine Feed, Small Ruminant Feed, Camelids and Other Livestock Feed), and by End Use Sector (Commercial Farms, Compound Feed Manufacturers, Household and Hobby Animal Owners, and Pet Food and Specialty Nutrition). The Market Size and Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Product Type

| Bales |

| Pellets |

| Cubes |

| Compressed Bales |

By Application

| Dairy Cattle Feed |

| Beef Cattle Feed |

| Poultry Feed |

| Equine Feed |

| Small Ruminant Feed |

| Camelids and Other Livestock Feed |

By End Use Sector

| Commercial Farms |

| Compound Feed Manufacturers |

| Household and Hobby Animal Owners |

| Pet Food and Specialty Nutrition |

| By Product Type | Bales |

| Pellets | |

| Cubes | |

| Compressed Bales | |

| By Application | Dairy Cattle Feed |

| Beef Cattle Feed | |

| Poultry Feed | |

| Equine Feed | |

| Small Ruminant Feed | |

| Camelids and Other Livestock Feed | |

| By End Use Sector | Commercial Farms |

| Compound Feed Manufacturers | |

| Household and Hobby Animal Owners | |

| Pet Food and Specialty Nutrition |

Key Questions Answered in the Report

What is the 2031 outlook for United States alfalfa demand?

The sector is forecasted to reach USD 16.91 billion by 2031 from USD 14.45 billion in 2026, at a 3.20% CAGR from 2026 to 2031.

Which product format is gaining the most momentum in the United States?

Pellets are the fastest growing product type, with a forecasted 3.0% CAGR from 2026 to 2031, supported by equine, specialty nutrition, and processed feed demand.

What is the biggest risk facing growers in western states?

Water allocation limits are the main constraint, especially in Arizona and other Colorado River linked areas where acreage and groundwater access are under pressure.

Which end use sector is expanding the fastest?

Pet food and specialty nutrition is growing the fastest at a 9.0% CAGR from 2026 to 2031, helped by premium small animal and functional ingredient demand.

Page last updated on: