United States Agricultural Tractor Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

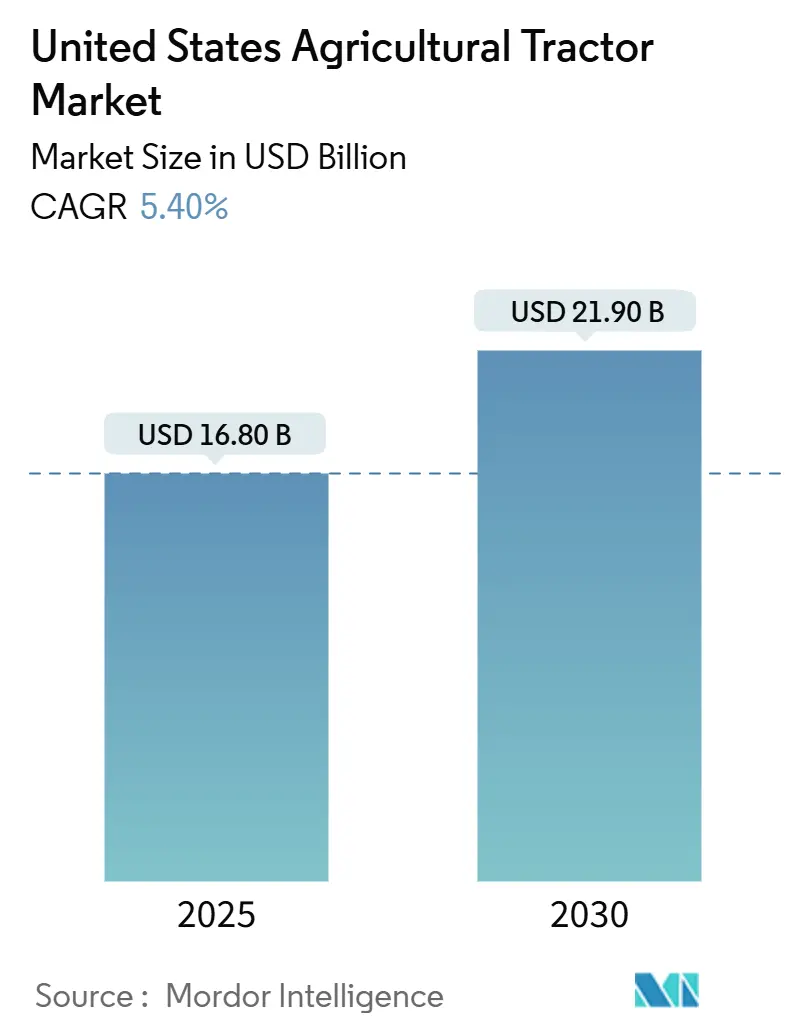

| Market Size (2025) | USD 16.80 Billion |

| Market Size (2030) | USD 21.90 Billion |

| Growth Rate (2025 - 2030) | 5.40% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Agricultural Tractor Market Analysis by Mordor Intelligence

The United States agricultural tractor market size is valued at USD 16.8 billion in 2025 and is projected to reach USD 21.9 billion by 2030, registering a 5.4% CAGR during the forecast period. Strong replacement demand, rapid electrification below 40 HP (rapid electrification of tractors below 40 HP), and embedded autonomy (embedded autonomous systems) are shaping the United States agricultural tractor market as growers look to offset rising labor costs and compliance spending. Real-time telematics, Farm Bill incentives, and carbon-credit monetization collectively enhance the return on investment, even as Tier 4 final engine costs pose headwinds. The interplay of regulation, connectivity gaps, and dealership consolidation signals a pivot toward integrated technology packages that promise quantifiable savings across multiple crop cycles.

Key Report Takeaways

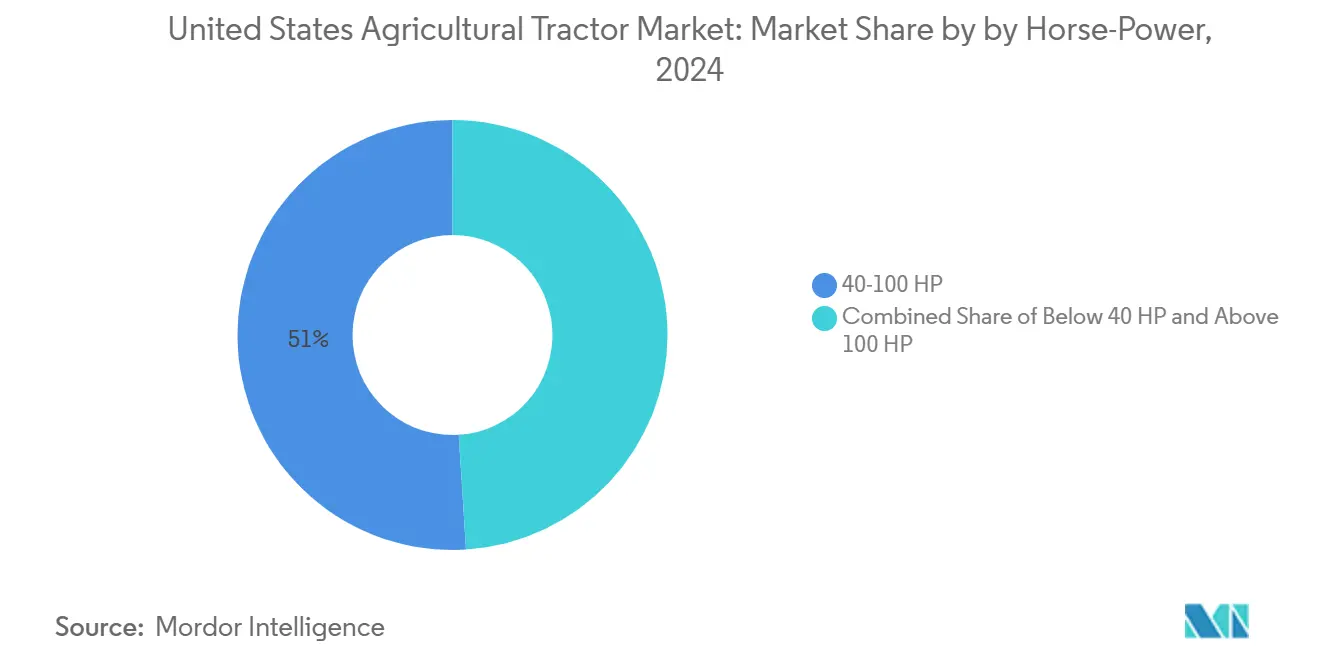

- By horsepower, the 40-100 HP category commanded 51% of the United States agricultural tractor market share in 2024, while the below 40 HP electric segment is forecast to grow at a 10.8% CAGR through 2030.

- By tractor type, utility tractors held 41% of the United States agricultural tractor market share in 2024, and the orchard and vineyard tractors are set to expand at an 11.4% CAGR to 2030.

- By drive type, two-wheel drive accounted for 77% of the United States agricultural tractor market share in 2024, yet autonomous/driverless platforms are primed for a 15.6% CAGR during the outlook period.

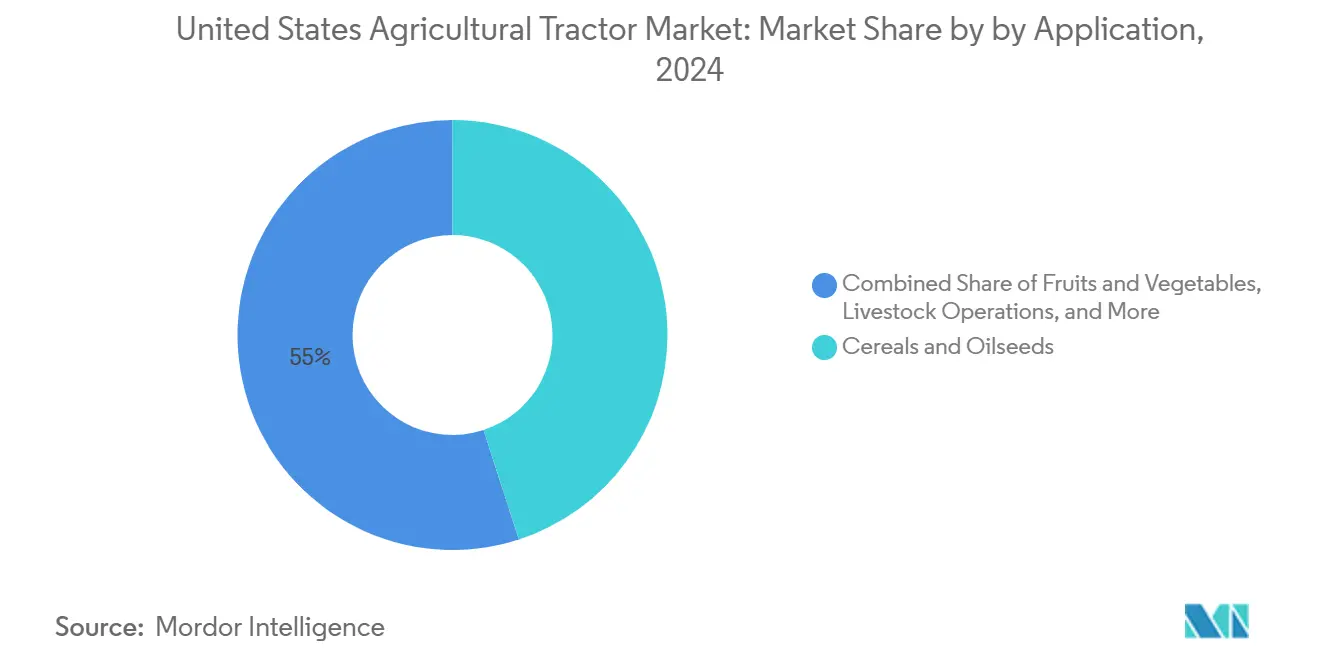

- By application, cereals and oilseeds held 45% of the United States agricultural tractor market share in 2024, and the fruits and vegetables are projected to post the strongest value growth at 5.9% CAGR through 2030.

United States Agricultural Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continuous electrification of sub-100 HP models | +1.2% | California, New York, and Vermont | Medium term (2–4 years) |

| Smart-implement compatibility boosts replacement demand | +0.9% | Midwest corn belt and Great Plains wheat regions | Short term (≤ 2 years) |

| Advanced telematics lower total cost of ownership | +0.8% | Nationwide commercial farming operations | Medium term (2–4 years) |

| Precision-Ag incentives in the 2023 United States farm bill | +0.7% | Nationwide, underserved producers in focus | Long term (≥ 4 years) |

| Autonomous retrofit kits reach commercial price points | +0.6% | Iowa, Illinois, and Nebraska large-scale farms | Long term (≥ 4 years) |

| Carbon-credit monetization for low-HP tractors | +0.4% | California and Northeast carbon-trading states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continuous Electrification of Sub-100 HP Models

Battery-powered tractors below 40 HP now offer meaningful payback because operating cost reductions offset up-front premiums within three to six seasons. John Deere’s E-Power prototypes and Solectrac’s compact lineup underline how early volume is clustering in vineyards, dairies, and greenhouse operations where low noise and zero tailpipe emissions carry premium value. Battery density still limits larger units, concentrating R&D on the compact range, yet component prices have fallen 14% since 2023, narrowing diesel price advantages. Dealer education and charging-infrastructure incentives remain gating factors, but Farm Bill climate allocations are catalyzing pilot deployments. With Deere’s commercial rollout slated for 2026, rivals face a shrinking window to lock in early adopters.

Smart-Implement Compatibility Boosts Replacement Demand

Implements are intentionally designed with limited backward compatibility, prompting farmers to trade in 6-8-year-old tractors rather than the historic 11-year cycle. The surge is most visible in the 40–100 HP class, where row-crop operations depend on sectional control. Consequently, the Original Equipment Manufacturers (OEMs) bundle guidance-ready wiring harnesses as standard to capture replacement share. This tailwind is projected to peak by 2027, once the installed base reaches a critical mass.

Advanced Telematics Lower Total Cost of Ownership

Predictive maintenance analytics prevent costly breakdowns and reduce idle fuel consumption, thereby trimming fleet costs by up to USD 25 per acre in yield-mapping applications. Yet, 65% of rural counties still lack FCC-grade broadband, which mutes benefits in mountain and delta regions [1]Source: Yaguang Zhang et al., “Challenges and Opportunities of Future Rural Wireless Communications,” NSF.GOV. National 5G projects promise relief within four years, and commercial farms are increasingly installing private LTE to bridge the gaps. As data subscriptions fold into equipment invoices, cost transparency improves, and adoption accelerates. The payback calculus strengthens further when insurers start offering telematics-linked premium discounts.

Precision-Ag Incentives in the 2023 United States Farm Bill

The USD 19.5 billion conservation allocation directs USD 8.45 billion to EQIP (Environmental Quality Incentives Program) and USD 4.95 billion to RCPP (Regional Conservation Partnership Program), rewarding GPS-guided variable-rate application that cuts input waste [2]Source: Natural Resources Conservation Service, “Inflation Reduction Act,” USDA.GOV . Eligibility rules favor underserved producers, widening the addressable base for guidance-ready tractors. Because contracts run up to 10 years, revenue visibility allows OEMs to finance in-house input-financing schemes tied to equipment bundles. FCC (Federal Communications Commission) recommendations for 100/100 Mbps field connectivity imply parallel infrastructure work, extending the driver’s impact to the end of the decade.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront and maintenance costs of Tier-4 final engines | −1.1% | Nationwide, small and mid-size farms | Short term (≤ 2 years) |

| Fragmented dealership coverage in mountain states | −0.7% | Wyoming, Montana, Colorado, and Idaho | Medium term (2–4 years) |

| Shortage of skilled technicians for sensor-laden models | −0.6% | Nationwide, acute rural shortfall | Long term (≥ 4 years) |

| Slow rural 5G rollout limits real-time data services | −0.5% | Remote agricultural counties nationwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Maintenance Costs of Tier-4 Final Engines

Tier 4 final compliance raises sticker prices by more than 15% and introduces exhaust fluid expenses that erode margins for family farms. While emissions of particulate matter plunge 95%, the payback period lengthens, motivating many growers to buy used pre-Tier-4 units or delay replacements. The strain is likely to moderate after 2026 once component suppliers scale production and secondary-market prices normalize.

Fragmented Dealership Coverage in Mountain States

Over 82% of Deere & Company's outlets are held by large chains, leaving swaths of Wyoming, Montana, and Idaho without convenient service. Repair trips can exceed 200 miles, resulting in harvest delays and increased downtime costs. Colorado’s landmark Right-to-Repair law aims to improve access, yet repeal provisions create uncertainty. Continued dealer consolidation suggests the service gap may widen before manufacturers deploy mobile support fleets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Horsepower: Electric Models Drive Sub-40 HP Growth

The below 40 HP electric tractor is forecast to advance at 10.8% CAGR, outpacing the broader the United States agricultural tractor market by nearly twofold, due to falling battery costs and municipal incentives. This segment benefits from greenhouse, dairy, and urban farming operations that prize zero-emission, low-noise performance. The 40–100 HP range retains 51% of the United States agricultural tractor market share in 2024 because of its versatility across row-crop and livestock tasks, anchoring long-term volume. Above 100 HP units serve large farms where diesel energy density still delivers the lowest dollar-per-acre cost.

Electric newcomers target cost-of-ownership metrics rather than environmental altruism, citing 60% fuel savings and 40% lower maintenance. Deere & Company’s 130 HP E-Power prototype underscores the manufacturer's shift toward scalable electrification, though battery mass keeps large-frame adoption in pilot mode. Solectrac’s revenue rose from USD 1.8 million in 2021 to USD 11 million in 2022, yet net losses show infrastructure hurdles remain. As lithium iron phosphate chemistry gains traction, pack costs could fall 20% by 2027, narrowing diesel’s upfront advantage.

By Tractor Type: Specialty Applications Lead Innovation

The utility tractors captured 41% of 2024 share, reflecting broad task compatibility across cattle, hay, and property maintenance. Still, orchard and vineyard tractors are set for an 11.4% CAGR through 2030, eclipsing the United States agricultural tractor market average. Their premium pricing stems from narrow chassis, autonomy-ready controls, and zero-emission powertrains that thrive in confined rows. Row-crop tractors hold stable demand linked to corn and soybean acreage, but margin pressure is steeper as OEMs balance high-horsepower features against price-sensitive growers.

Case IH's FieldOps platform includes a Connectivity Included offer that waives data-service fees for new orchard tractors, lowering lifetime costs and encouraging adoption. Premium fruit growers in California pay up because the margin per acre dwarfs commodity crops. Over time, technologies proven in specialty units such as LIDAR-guided sprayers should cascade into mainstream utility models once volumes cut component pricing, widening their appeal.

By Drive Type: Autonomous Systems Reshape Market Dynamics

Two-wheel drive machines still account for 77% of the United States agricultural tractor market, favored for affordability in moderate-traction applications. Four-wheel drive usage remains niche, focused on heavy tillage in the Great Plains states. Autonomous or driverless platforms, however, are projected to post a 15.6% CAGR, driven by chronic labor shortages and the promise of 24-hour operation windows.

AGCO Corporation’s retrofit kits lower entry barriers by fitting across competing brands and cost less than one-third of a new autonomous tractor, letting mixed fleets sample driverless technology before full transition. John Deere’s second-generation 9RX autonomy kit, featuring 16 cameras for 360-degree perception, targets commercial row-crop growers aiming to redeploy scarce labor elsewhere. Insurers and regulators will shape uptake speed, but economic advantages position autonomy as the fastest-growing slice of the United States agricultural tractor market.

By Application: Cereals Drive Volume, Specialty Crops Drive Value

Cereals and oilseeds held 45% of the United States agricultural tractor market share in 2024, capturing the largest portion of the market size as corn, soybean, and wheat operations rely on multiple mid-range units to cover expansive acreage. Their dominance is reinforced by strong adoption of 40–100 HP machines that pair easily with ISOBUS planters and sprayers, enabling variable-rate application that trims seed and chemical costs. Continuous crop rotation maintains high utilization rates, so farmers prioritize uptime and telematics for predictive maintenance. As broadband connectivity improves, cereal producers are projected to further enhance precision features, supporting steady equipment replacements. Collectively, these factors are projected to anchor a mid-single-digit growth path for the segment through 2030.

Livestock operations that focus on hay and forage account for higher demand, favoring utility tractors with loaders and PTO-driven balers for daily chores. Fruits and vegetables are projected to command a 5.9% CAGR of the market and post the fastest value expansion, as narrow-row orchard and vineyard growers invest in autonomy and electric drivetrains that reduce labor and emissions. Other specialty and miscellaneous crops, including nursery, turf, cotton, and emerging high-margin niches, make up the remaining 8%, yet they often justify premium technology packages to meet sustainability targets and capitalize on carbon-credit programs. Taken together, these diversified applications broaden revenue streams for manufacturers and cushion cyclical swings in any single crop segment.

Geography Analysis

The Midwest Corn Belt accounts for approximately half of the annual tractor shipments, driven by the prevalence of row-crop farming and the large farm sizes that predominantly utilize 40–100 HP models. Precision adoption here runs ahead of national averages because economies spread technology costs across thousands of acres. Great Plains wheat states tend to lean toward high-horsepower four-wheel drive units capable of making broad passes, but labor shortages are steering interest toward autonomous retrofits.

California and the Pacific Coast command premium value through orchard and vineyard business, adopting electric and narrow-track tractors early owing to stringent air-quality mandates and specialized crop rows. The FARMER Program offers grants topping USD 178 million for low-emission agricultural equipment, nudging growers toward electric or hybrid options [3]Source: California Air Resources Board, “FARMER Program,” ARB.CA.GOV. Northeast states mirror these trends in smaller volumes, boosted by established carbon markets where emission credits sweeten paybacks.

Mountain states face unique challenges, sparse dealer coverage forces ranchers to self-service or rely on distant repair hubs, prolonging equipment cycles. Right-to-repair legislation in Colorado could become a blueprint elsewhere if federal rules stall. Connectivity shortfalls are most severe here, stalling telematics value until infrastructure closes the gap. These factors collectively hinder near-term growth in the United States agricultural tractor market but create opportunities for accelerated adoption once the constraints are alleviated.

Competitive Landscape

The United States agricultural tractor market arena operates in a highly concentrated market, where the top five companies commanded a major share in 2024. Deere & Company alone holds a higher share, giving it command over pricing signals and technology roadmaps. CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Mahindra&Mahindra Ltd., collectively fill the rest of the leadership tier, anchoring scale efficiencies that smaller rivals cannot match. The dense concentration accelerates product refresh cycles because each leader must differentiate or risk share erosion in a market with limited room for newcomers.

Strategic moves in 2025 underscore the technology race. Deere & Company pledged USD 20 billion in domestic investment that targets autonomous production lines and battery plants, signaling confidence in local demand. CNH Industrial N.V. mapped out a plan to raise precision tech sales to roughly one quarter of agriculture revenue by 2030, backed by a full tractor lineup refresh. AGCO Corporation chose a retrofit-first approach, launching OutRun autonomy kits that bolt onto mixed fleets at under USD 55,000 and create subscription revenue streams. Kubota Corporation expanded its compact line with the MX4900, priced to attract cost-sensitive buyers who still want a cabbed machine and turbocharged power. These contrasting strategies show that competitive advantage is shifting from raw horsepower to software, data services, and total cost of ownership.

Dealer consolidation strengthens incumbents by tightening control over parts, financing, and data, yet it also fuels right-to-repair campaigns in states such as Colorado. Service capacity is further strained by a shortfall of more than 4,000 qualified technicians, an issue that costs dealers about USD 2.4 billion in lost labor annually. Retrofit specialists and software startups aim to capitalize on these gaps by offering open-architecture upgrades that promise faster repairs and reduced downtime. The leadership cluster leverages scale advantages, with growing customer demand for connectivity, uptime, and repair flexibility driving pressure and sustaining a rapid pace of innovation.

United States Agricultural Tractor Industry Leaders

CNH Industrial N.V.

AGCO Corporation

Kubota Corporation

Mahindra&Mahindra Ltd.

Deere & Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Kubota Corporation introduced the MX4900 utility tractor, which offers the lowest horsepower in the MX series. The tractor includes loader capabilities and hydraulic flow features, making it the most affordable model.

- February 2025: Deere & Company introduced two autonomous agricultural machines. The Autonomous 9RX Tractor uses 16 high-resolution cameras that provide a 360-degree view for unmanned operation in large-scale farming. The Autonomous 5ML Orchard Tractor uses Lidar sensors to navigate through orchard canopies while performing air blast spraying operations.

- January 2024: Doosan Bobcat launched the AT450X, an electric articulating tractor with autonomous capabilities. The tractor incorporates Agtonomy's software and embedded-computing technology, enabling remote-controlled operations in vineyards and orchards. The vehicle operates without emissions and features autonomous functionality for compact agricultural applications.

United States Agricultural Tractor Market Report Scope

A tractor is a farm vehicle used to pull farm machinery and provide the energy needed for the machinery to work. For this report, tractors used in agricultural operations, especially four-wheeled tractors, have been considered. The United States agricultural tractor machinery market is segmented by horsepower into below 40 HP, 40-100 HP, and above 100 HP, and tractor type into utility tractors, row crop tractors, garden & orchard type tractors, and other tractor types. The report offers the market size and forecasts for volume (units) and value (USD) for all the above segments.

| Below 40 HP |

| 40-100 HP |

| Above 100 HP |

| Utility Tractors |

| Row-Crop Tractors |

| Orchard and Vineyard Tractors |

| Other Tractor Types |

| Two-Wheel Drive (2WD) |

| Four-Wheel Drive (4WD) |

| Autonomous / Driverless |

| Cereals and Oilseeds |

| Fruits and Vegetables |

| Livestock Operations |

| Others |

| By Horsepower | Below 40 HP |

| 40-100 HP | |

| Above 100 HP | |

| By Tractor Type | Utility Tractors |

| Row-Crop Tractors | |

| Orchard and Vineyard Tractors | |

| Other Tractor Types | |

| By Drive Type | Two-Wheel Drive (2WD) |

| Four-Wheel Drive (4WD) | |

| Autonomous / Driverless | |

| By Application | Cereals and Oilseeds |

| Fruits and Vegetables | |

| Livestock Operations | |

| Others |

Key Questions Answered in the Report

How large is the United States agricultural tractor market in 2025?

It stands at USD 16.8 billion and is forecast to reach USD 21.9 billion by 2030.

What is driving demand for electric tractors?

Lower operating costs, Farm Bill incentives, and zero-emission compliance drive the surge in sub-40 HP electric units.

Which tractor segment grows fastest through 2030?

Autonomous/driverless platforms are projected to post a 15.6% CAGR as retrofit kits hit viable price points.

Why are dealers consolidating?

Rising inventory and training costs push smaller outlets to merge, resulting in 82% of Deere & Company locations now controlled by large chains.

How do Tier-4 Final engines affect equipment costs?

Compliance adds more than 15% to purchase price and introduces ongoing exhaust fluid expenses that squeeze margins for smaller farms.

Page last updated on: