United States Advanced Ceramics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

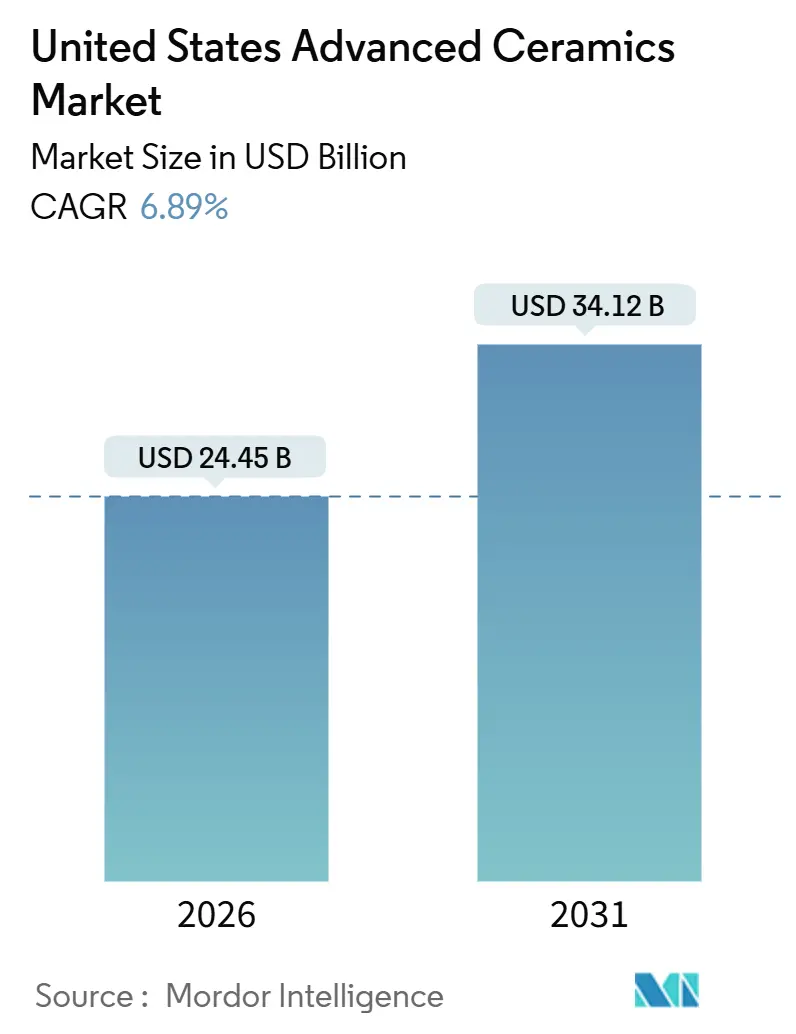

| Market Size (2026) | USD 24.45 Billion |

| Market Size (2031) | USD 34.12 Billion |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

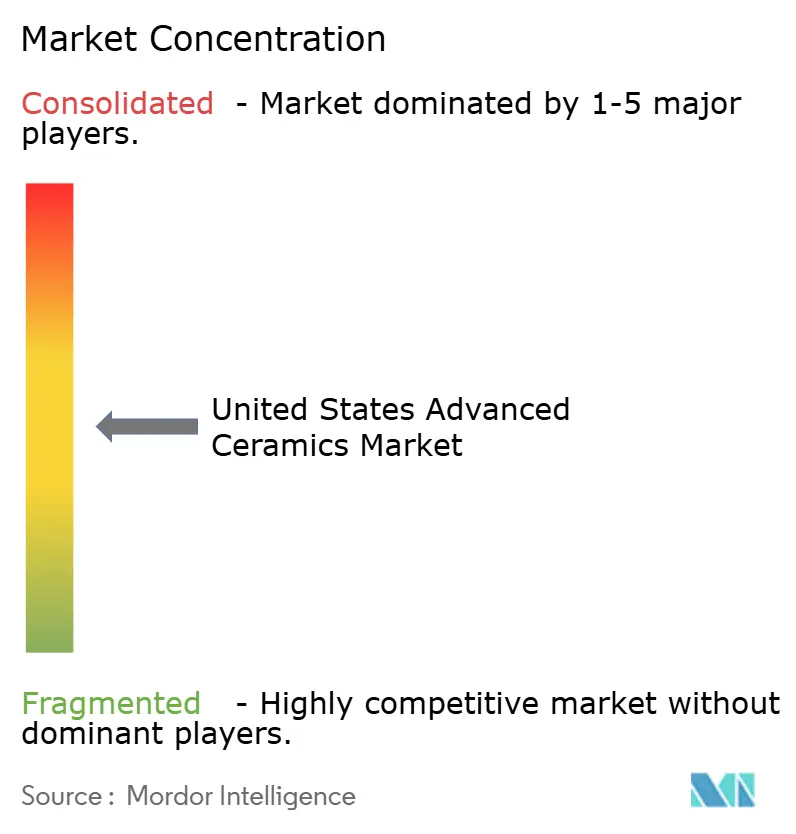

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Advanced Ceramics Market Analysis by Mordor Intelligence

The United States Advanced Ceramics Market size is estimated at USD 24.45 billion in 2026, and is expected to reach USD 34.12 billion by 2031, at a CAGR of 6.89% during the forecast period (2026-2031). Government incentives for semiconductor capacity, accelerating demand for battery-electric vehicles, and next-generation turbine platforms are expanding the customer base, while sustained military spending on hypersonic and space programs is converting niche research and development projects into serial production contracts. Suppliers are investing in vertical integration to secure critical minerals and near-net-shape forming technologies, trimming lead times for customized parts from months to days. Cost pressures remain the primary hurdle because diamond-tool machining and high-purity powders elevate component prices, yet binder-jetting and plasma-spray routes are beginning to compress the total cost of ownership, improving the economic case for designers in aerospace, defense, medical, and power-electronics applications. Capacity additions in silicon-carbide wafers, glass-ceramic interposers, and fine-grain zirconia powders point to a structural realignment away from commoditized alumina substrates toward higher-margin engineered solutions.

Key Report Takeaways

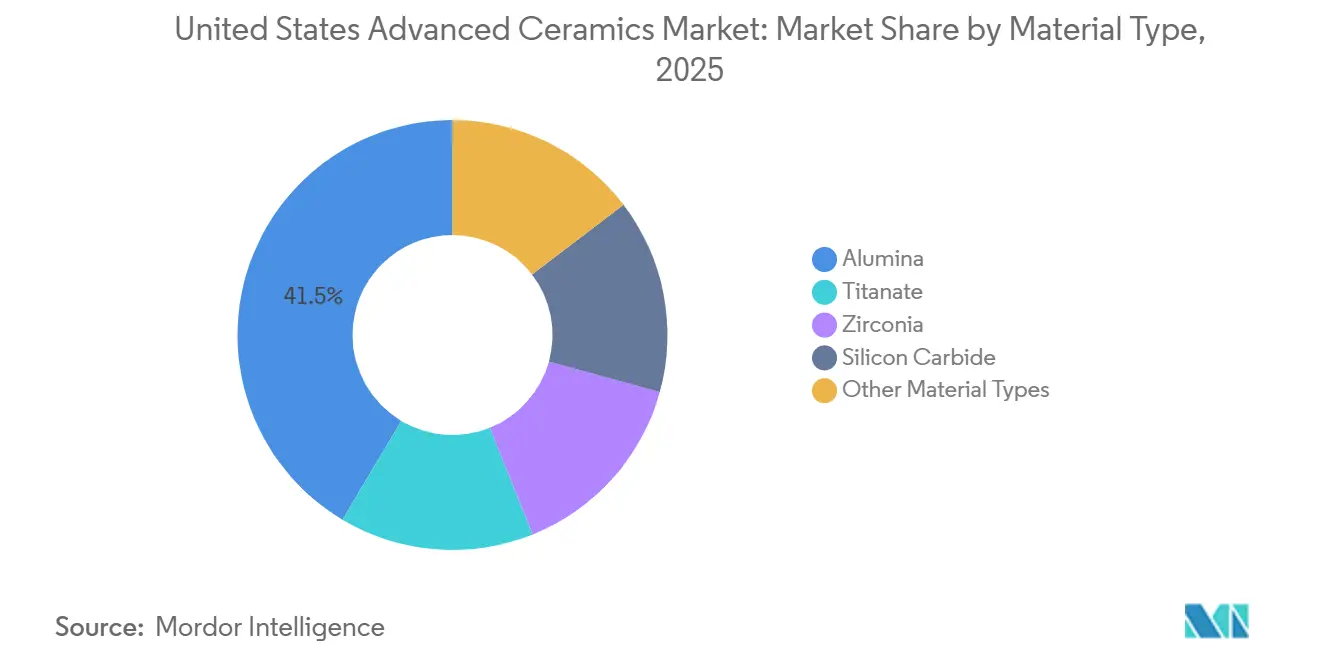

- By material type, alumina led with 41.46% of the advanced ceramics market share in 2025, while titanate ceramics are forecast to expand at a 7.82% CAGR through 2031.

- By class type, monolithic ceramics held 73.75% of the advanced ceramics market share in 2025; ceramic matrix composites are advancing at an 8.51% CAGR through 2031.

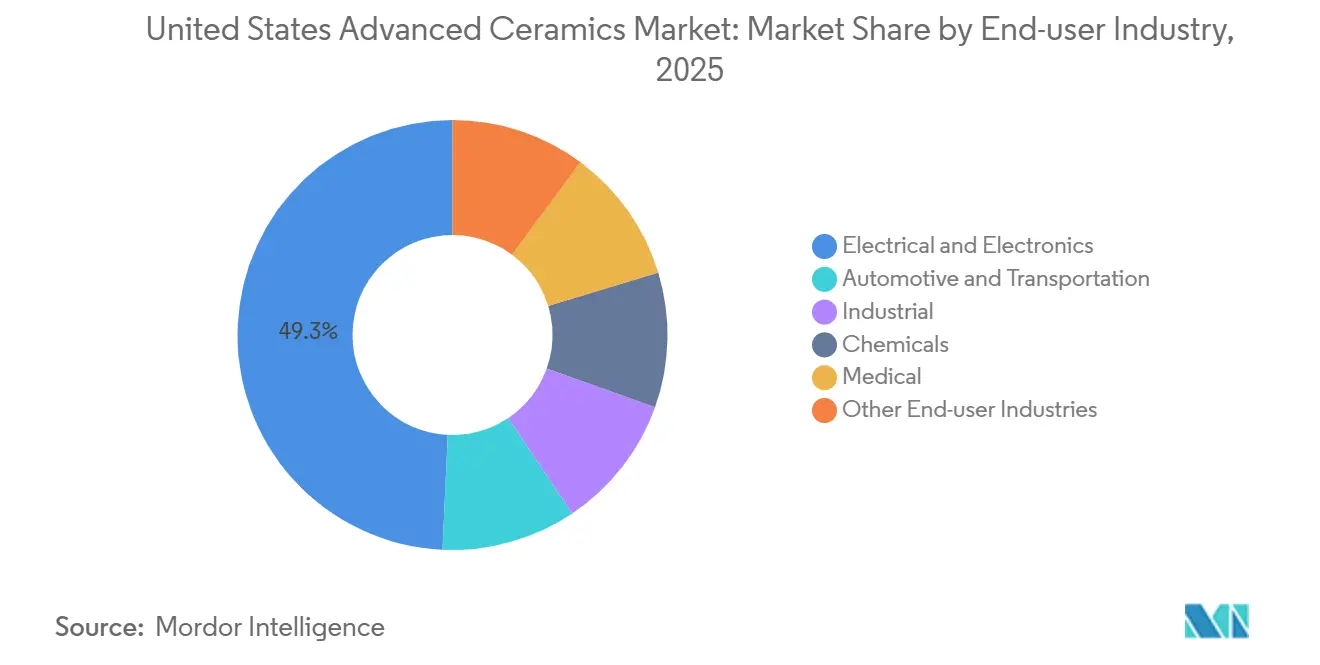

- By end-user industry, electrical and electronics captured 49.26% of demand in 2025, whereas medical applications are set to grow at a 9.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on advanced ceramics market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Advanced Ceramics Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strong Demand from Aerospace and Defense | +1.8% | National, concentrated in Arizona, California, Ohio, and Texas defense corridors | Medium term (2–4 years) |

| Electronics and Semiconductor Miniaturization Surge | +2.1% | National, with epicenters in Oregon, Texas, Arizona, and New York, fab clusters | Short term (≤ 2 years) |

| Rapid Deployment of 5G and Power-Electronics Infrastructure | +1.5% | National, led by metropolitan areas and EV manufacturing hubs in Michigan, Tennessee, and Georgia | Short term (≤ 2 years) |

| Federal Funding for Hypersonic and Space Programs | +1.2% | National, with concentration in Alabama (Huntsville), California (Edwards AFB), and Virginia (Wallops) | Long term (≥ 4 years) |

| Additive Manufacturing Adoption Reducing Lead-Times | +0.9% | National, early adoption in medical-device clusters (Massachusetts, California, Minnesota) | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Strong Demand from Aerospace and Defense

In 2024, the Pentagon inked MACH contracts, pushing the boundaries of ceramic matrix composite (CMC) procurement[1]Defense Advanced Research Projects Agency, “Materials Architectures and Characterization for Hypersonics,” darpa.mil . These contracts target operations at extreme temperatures, surpassing the limits of nickel superalloys. The Army's Extended Range Cannon Artillery project is leading the charge, specifying silicon-carbide liners that extend barrel life. This move is accelerating the adoption of reaction-bonded SiC components. Meanwhile, in the commercial aerospace arena, GE Aerospace's RISE demonstrator is leveraging CMC shrouds, achieving significant weight reduction per aircraft and translating to fuel savings. Further underscoring the military's commitment, a grant under the Defense Production Act Title III was announced in March 2025. This initiative aims to repatriate a portion of the military's ceramic supply, reducing dependence on foreign sources. Together, these initiatives are not only driving demand for advanced ceramics into mainstream production but also providing suppliers with a clearer, multiyear outlook.

Electronics and Semiconductor Miniaturization Surge

As logic scales down to 2-nanometer nodes and high-bandwidth memory stacks, ceramic consumption per chip package rises. Intel's Ohio megasite, set to commence volume production in late 2026, is projected to consume significant amounts of alumina substrates annually. The National Advanced Packaging Manufacturing Program is co-funding glass-ceramic interposers, which reduce signal loss at frequencies above 100 GHz. This advancement paves the way for chiplet architectures in AI accelerators. Presently, a single high-end accelerator boasts numerous multilayer ceramic capacitors, each handling transient currents at high levels, a significant increase from 2020 figures. Given that sub-micron delaminations can lead to latent field failures, there's a growing reliance on inspection regimes utilizing automated optical and computed-tomography systems. This surge in electronics not only fuels immediate volume growth but also drives up average selling prices for high-purity powders and substrate blanks.

Rapid Deployment of 5G and Power-Electronics Infrastructure

In 2025, each mid-band 5G base station will deploy ceramic filters and resonators, tripling the count seen in 4G macro sites. This increase is driven by the need for tighter selectivity due to broader carrier aggregation demands. Meanwhile, the Infrastructure Investment and Jobs Act's charging network program is boosting volumes of silicon-carbide modules. These modules utilize direct-bonded-copper alumina substrates, adept at dissipating thermal loads, especially in fast chargers. Wolfspeed's Mohawk Valley fabrication facility highlighted a significant shift: automotive bookings have risen notably in fiscal 2025. This underscores the strong correlation between the acceleration of electric vehicles (EVs) and the rising demand for substrates. Furthermore, as connected vehicles demand higher data throughput, this necessitates further upgrades to base stations, further amplifying the growth of ceramic content in both infrastructure pillars.

Federal Funding for Hypersonic and Space Programs

Contracts for the Artemis lunar lander mandate the use of zirconia-toughened alumina for thruster nozzles and protective tiles. These components must withstand the lunar cycle's temperature swing, ranging from −280 °F to +250 °F, underscoring the rising demand for durable, space-grade ceramics. The Space Force allocated funding for the development of reusable ceramic heat shields, aiming for an ambitious target of improved launch cycles. This marks a significant leap from the technology used during the Shuttle era. Test flights at the Arnold Engineering Development Complex utilized ultra-high-temperature ceramic composites. Additionally, the Department of Energy’s Critical Materials Institute invested in enhancing domestic supply chains, focusing on scaling hafnium- and tantalum-carbide powders for components rated above 3,500 °F. Collectively, these endeavors solidify the role of advanced ceramics as pivotal players in the quest for aerospace dominance.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Production and Machining Costs | -1.4% | National, most acute in low-volume custom applications and precision-machined components | Short term (≤ 2 years) |

| Brittleness and Design-Flexibility Constraints | -0.9% | National, particularly affecting automotive, consumer electronics, and structural applications | Medium term (2–4 years) |

| Critical Mineral Supply-Chain Vulnerability | -1.1% | National, with exposure to Asian and African rare-earth sources and alumina refining capacity | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Production and Machining Costs

Precision grinding with diamond tools incurs significant costs for material removal. This cost escalates for intricate geometries, especially when metal alloys are used. While ceramic turbocharger rotors offer efficiency benefits, they come with a premium over their nickel-based counterparts. This price difference confines their use to high-end vehicle trims. Producers face yield losses due to shrinkage variability. To counter this, they oversize green bodies and then machine them back to the desired tolerance, a process that extends production time. Although binder-jetting can significantly reduce the need for this secondary machining, the high cost of alumina and silicon-carbide powders hinders their widespread adoption for industrial parts. The cost challenges are expected to diminish as powder synthesis techniques advance and hybrid manufacturing processes become more refined.

Brittleness and Design-Flexibility Constraints

The inherent brittleness of ceramics restricts their use in load-bearing structures subject to impact or flexural stress, constraining automotive and consumer electronics designers seeking to down-cost housings or brackets. Advances in micro-architectured lattices and fiber-reinforced composites can mitigate crack propagation, but high scrap risk during early prototypes discourages experimentation. Design-for-ceramic principles require tight collaboration between OEMs and suppliers, stretching development timelines compared with metals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Alumina Anchors, Titanate Accelerates

Alumina accounted for 41.46% of the advanced ceramics market share in 2025, thanks to its cost-performance ratio, making it ideal for semiconductor chambers, ballistic armor, and wear-resistant plant components. As demand for EV inverters grows, the need for substrates with high heat dissipation capabilities has surged, propelling Wolfspeed to achieve substantial substrate revenue in fiscal 2025. Titanate-based dielectrics, though smaller in tonnage, are advancing at a 7.82% CAGR through 2031, powered by the densification of 5G base stations and automotive radar modules that need high-permittivity capacitors[2]IEEE, “Transactions on Components, Packaging and Manufacturing Technology,” ieee.org .

Under the tightening regulations of ISO 6474-2:2024, there's a new mandate for granular traceability in medical-grade alumina. This has led to a spike in compliance costs, particularly burdening smaller mills. Meanwhile, the emergence of binder-jettable silicon-nitride powders is revolutionizing the industry. These innovations are significantly reducing turbine-component lead times and achieving a notable reduction in material waste. Life-cycle assessments highlight the advantages of silicon-carbide pump seals, which are extending the mean time between failures in corrosive environments. This significant enhancement justifies the premium on material costs. As designers increasingly prioritize uptime and miniaturization, it's anticipated that while alumina will maintain its foothold in commodity substrates, its market share will wane post-2028, giving way to the rising volumes of titanate and silicon-carbide.

By Class Type: Monolithic Dominance, CMC Momentum

Monolithic ceramics captured 73.75% of 2025 due to their established manufacturing lines, which produce parts at a cost that composite alternatives have yet to match. Meanwhile, Ceramic matrix composites are growing at an 8.51% CAGR through 2031, driven by FAA-backed initiatives supporting SiC/SiC qualifications in commercial engines.

Although CMC prepreg sheets remain expensive, limiting their widespread adoption, GE Aerospace is optimistic about their potential. They anticipate significant fuel consumption reductions when CMC components replace nickel alloys in their forthcoming RISE engine. Additionally, innovations like functionally graded plasma-spray coatings are enhancing blade longevity. These advancements are helping monolithic substrates maintain their edge in medium-duty turbines. As a result, the market is evolving: while cost-effective monolithics focus on volume markets, CMCs and cutting-edge coatings are carving out lucrative niches in aerospace, defense, and energy sectors.

By End-User Industry: Electronics Lead, Medical Surges

Electronics absorbed 49.26% of U.S. consumption in 2025, largely fueled by wafer-processing equipment and multilayer ceramic capacitors tailored for AI servers. Thanks to the CHIPS Act's generous subsidies for fab construction, this demand surge is poised to persist until 2031. The automotive sector is increasingly leaning towards power-electronics substrates. Notably, silicon-carbide modules, adept at handling high thermal loads, now rely on alumina or aluminum-nitride blanks. These materials boast a performance that eclipses traditional silicon IGBT substrates.

Medical uses, though smaller, are climbing at a 9.68% CAGR to 2031. This growth is largely attributed to patient-specific implant clearances, which significantly reduce lead times and hospital stays. In industrial settings, ceramics are prized for their wear and corrosion resistance. For instance, in sulfuric-acid pipelines, ceramics can last significantly longer than stainless steel. This longevity comes at a cost premium but offers a substantial extension in service life. In 2024, Bloom Energy made waves by shipping solid-oxide fuel cells. Each megawatt's production consumed yttria-stabilized zirconia, underscoring the energy sector's steady growth. While electronics will continue to dominate the market share, both medical and energy sectors are emerging as lucrative avenues, providing suppliers a buffer against the volatility of commodity pricing cycles.

Geography Analysis

Five primary corridors in the United States, anchored by semiconductor, aerospace, defense, and medical-device ecosystems, create localized economies of scale that bolster supplier proximity. Integrated wafer-fab lines in Arizona, California, and Ohio consume alumina substrates, electrostatic chucks, and etch-chamber linings at scale. Meanwhile, turbine and jet-engine plants in South Carolina and North Carolina are adopting ceramic matrix composites.

Texas and New York are at the forefront of the advanced ceramics market, particularly in silicon-carbide wafers. In Austin, substrate and tooling suppliers are flocking around multiple logic-fab expansions. Huntsville, Alabama, and Edwards Air Force Base in California are hubs for hypersonic research and testing, utilizing ultra-high-temperature composites in experimental flight hardware. Boston, Minneapolis, and the Bay Area form a medical-device triangle, where US additive manufacturing capabilities are streamlining qualification loops, driving growth in medical ceramic consumption.

The Gulf Coast grapples with supply-chain vulnerabilities, especially with its import-dependent alumina refineries. However, Saint-Gobain’s plant in Baton Rouge is set to change the landscape. Once fully operational, it will produce high-purity alumina powder, reducing the nation's reliance on Asian sources. While strategic clustering offers a demand pull, it also heightens risks tied to single-node import routes for essential precursors. This underscores the urgency for vertical integration and mineral diversification strategies.

Competitive Landscape

The United States advanced ceramics market is moderately fragmented. HRL Laboratories’ hafnium-carbide additive-manufacturing license to a defense prime illustrates the rise of university spin-outs capable of leapfrogging legacy suppliers in ultra-high-temperature domains. Competitive intensity is therefore anchored in cycle-time reduction, quality control, and secured mineral supply rather than pure capacity scale.

United States Advanced Ceramics Industry Leaders

CoorsTek Inc.

Corning Incorporated

3M

Morgan Advanced Materials

CeramTec GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Kyocera boosted the aluminum-nitride substrate capacity 30% at Kagoshima to serve 800-V EV battery systems, investing JPY 8 billion (~USD 54 million). This will also affect the market in the United States.

- May 2024: Morgan Advanced Materials entered a USD 12 million collaboration with Pennsylvania State University to develop silicon carbide fibers for ceramic matrix composites, targeting aerospace turbine applications. The partnership will establish a chemical vapor infiltration reactor at Penn State's Materials Research Institute, with pilot-scale fiber production expected by 2027.

United States Advanced Ceramics Market Report Scope

Advanced ceramics are inorganic, non-metallic materials that are synthesized from highly refined, pure raw materials and processed with rigorous control over composition and microstructure. Unlike traditional ceramics (pottery, bricks), advanced ceramics are engineered for superior mechanical strength, high-temperature stability, wear resistance, and corrosion resistance.

The United States advanced ceramics market is segmented by material type, customer class type, end-user industry, and geography. By material type, the market is segmented into alumina, titanate, zirconia, silicon carbide, and other materials. By class type, the market is segmented into monolithic ceramics, ceramic matrix composites, and ceramic coatings. By end-user industry, the market is segmented into electrical and electronics, automotive and transportation, industrial, chemicals, medical, and other industries. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Alumina |

| Titanate |

| Zirconia |

| Silicon Carbide |

| Other Material Types |

| Monolithic Ceramics |

| Ceramic Matrix Composites |

| Ceramic Coatings |

| Electrical and Electronics |

| Automotive and Transportation |

| Industrial |

| Chemicals |

| Medical |

| Other End-user Industries |

| By Material Type | Alumina |

| Titanate | |

| Zirconia | |

| Silicon Carbide | |

| Other Material Types | |

| By Class Type | Monolithic Ceramics |

| Ceramic Matrix Composites | |

| Ceramic Coatings | |

| By End-user Industry | Electrical and Electronics |

| Automotive and Transportation | |

| Industrial | |

| Chemicals | |

| Medical | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current valuation of the U.S. advanced ceramics market?

The market is valued at USD 24.45 billion in 2026 and is forecast to reach USD 34.12 billion by 2031, registering a CAGR of 6.89%.

Which material dominates demand?

Alumina leads with a 41.46% share in 2025 due to its ubiquity in semiconductor and armor applications.

Which segment is growing fastest?

Titanate-based ceramics are expanding at a 7.82% CAGR, fueled by 5G infrastructure and radar modules.

How does additive manufacturing affect ceramics production?

Binder-jetting and similar methods can reduce lead times and scrap rates by half, though powder costs remain high.

What are the top risks to supply continuity?

High production costs and reliance on imported high-purity alumina and rare-earth oxides pose significant supply-chain vulnerabilities.

Page last updated on: