United Kingdom Self-Adhesive Labels Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 1.99 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 3.72% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Self-Adhesive Labels Market Analysis by Mordor Intelligence

The United Kingdom Self-Adhesive Labels Market size is estimated at USD 1.99 billion in 2026, and is expected to reach USD 2.39 billion by 2031, at a CAGR of 3.72% during the forecast period (2026-2031). Current expansion is shaped by Extended Producer Responsibility (EPR) rules that, from 2026, tie modulated fees to label recyclability scores, rewarding mono-material and linerless constructions while penalizing silicone-liner waste. Demand momentum clusters around five growth vectors: food and beverage allergen labeling, e-commerce parcel volumes, sustainability-driven adhesive conversion, RFID-enabled retail inventory programs, and premium craft-beverage aesthetics. Simultaneously, the sector absorbs headwinds from shrink-sleeve substitution, raw-material price spikes, and liner EPR compliance costs, prompting converters to invest in digital printing, waste-reduction platforms, and supply-chain visibility tools. Competitive intensity remains high as global label-stock suppliers streamline operations and regional converters leverage quick-turn capabilities to secure localized contracts.

Key Report Takeaways

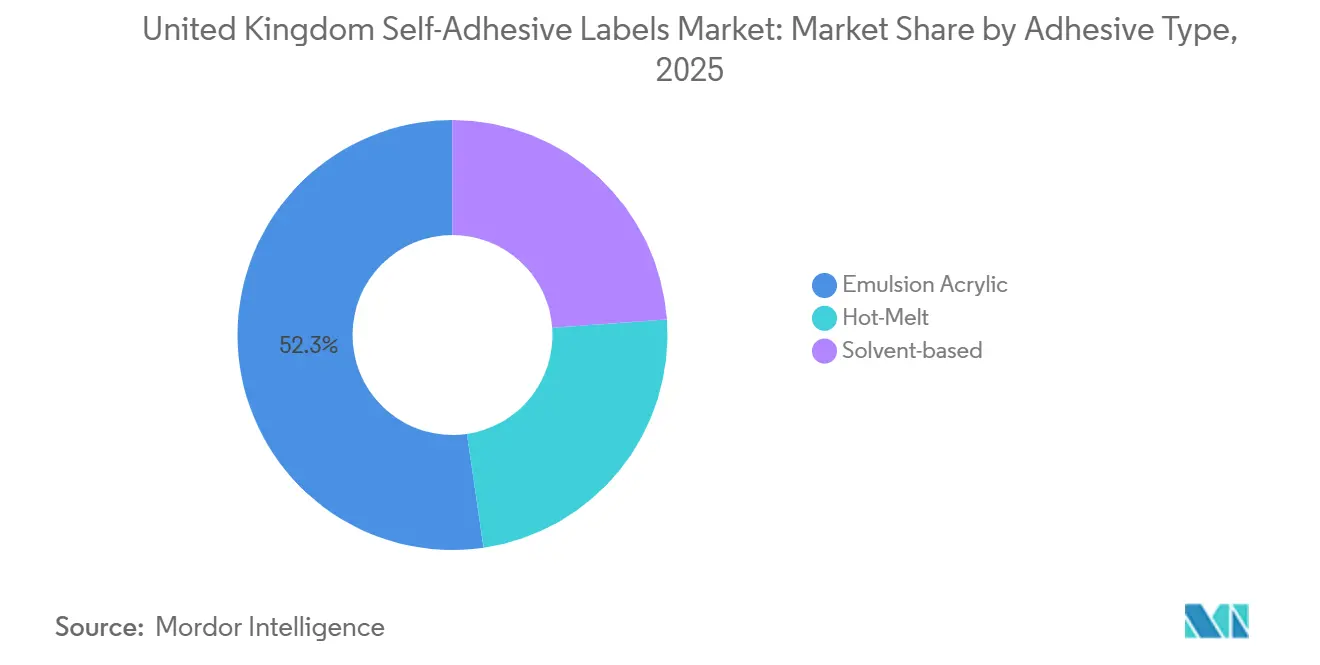

- By adhesive type, emulsion acrylic commanded 52.31% of the United Kingdom self-adhesive labels market share in 2025 and is on track to grow at a 4.34% CAGR through 2031.

- By face material, paper led with 61.20% share in 2025, while plastic substrates are forecast to expand at a 4.12% CAGR through 2031, supported by logistics automation and pharmaceutical durability requirements.

- By end user, food and beverage applications held 40.67% of the United Kingdom self-adhesive labels market size in 2025; the pharmaceutical segment is projected to rise at a 4.26% CAGR to 2031 on serialization and Braille mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Self-Adhesive Labels Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust demand from food and beverage sector | +1.2% | National, concentrated in Greater London, West Midlands, and Yorkshire food manufacturing clusters | Medium term (2-4 years) |

| E-commerce and logistics boom | +0.9% | National, with peak demand in South East England fulfilment hubs and last-mile delivery networks | Short term (≤ 2 years) |

| Sustainability-driven labelstock conversion | +0.7% | National, accelerated by EPR modulation starting 2026/27 | Long term (≥ 4 years) |

| RFID-enabled smart-label adoption in retail | +0.5% | National, early adopters in grocery multiples and fashion retail | Medium term (2-4 years) |

| Craft beverage premium-label surge | +0.4% | National, concentrated in Scotland (whisky), London (craft spirits), and regional craft beer clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Robust Demand from Food and Beverage Sector

Food and beverage labels account for 40.67% of 2025 demand, and the sector’s 1.2-point uplift to the overall CAGR derives from complex compliance rather than pure volume gain. Natasha’s Law obliges allergen disclosures on every prepacked item, multiplying SKU counts and pushing sandwich chains and bakeries toward same-day digital label updates[1]Food Standards Agency, “Prepacked for Direct Sale Allergen Guidance,” food.gov.uk. The “consistency-in-recycling” framework simultaneously restricts adhesives that impede PET and paperboard recovery, steering brand owners to wash-off or linerless options that carry lower modulated EPR fees. These twin pressures elevate revenue per square meter even as grocery unit sales level off. Converters that combine food-safe inks, quick-change digital presses, and recycling-compliant chemistries have leveraged this dynamic to win multi-year agreements with supermarket suppliers and contract packers.

E-Commerce and Logistics Boom

In 2025, the United Kingdom saw parcel volumes surpass billions of shipments, leading to a heightened demand for variable-length shipping labels in fulfillment centers. Linerless formats not only provide more labels per roll but also eliminate silicone waste, resulting in reduced downtime and lower EPR fees. The InNo-Liner platform, a collaboration between HERMA and cab Produkttechnik, activates the adhesive directly at the applicator head. This innovation boosts adhesion to corrugated cartons, all without the need for release liners. With the Border Target Operating Model implementing fully digital customs declarations, there's an amplified demand for labels that feature unique consignment references and 2D barcodes. This shift has added to SKU complexity. Fulfillment operators, while considering investments in linerless applicators, find that the savings from reduced waste hauling and enhanced throughput help offset these costs, contributing to the market's growth.

Sustainability-Driven Labelstock Conversion

According to the Recyclability Assessment Methodology color score, modulated EPR fees rise based on recyclability. This means that placing non-recyclable "RAM Red" labels on the market comes at double the cost. Avery Dennison's AD LinrSave and CleanFlake programs, which achieve weight reduction and enhanced wash-off adhesive performance, are strategically positioned to earn RAM Green ratings. UPM Raflatac's BEYOND THE LABEL initiative promotes Forest Action-certified facestocks and silicone liner take-back schemes, aligning with the UK's ambitious goal of achieving zero waste to landfill by 2030. Converters pivoting towards water-based chemistries and mono-material films are reaping advantages, as brand owners increasingly prioritize sustainability and seek relief from fees.

RFID-Enabled Smart-Label Adoption in Retail

By 2027, GS1 UK is pushing retailers to transition from EAN-13 to QR and DataMatrix codes. This shift is prompting upgrades to label hardware and the adoption of more data-rich designs. RFID tags, now costing under GBP 0.05 per inlay, are being paired with these graphics. This combination offers real-time stock visibility, addressing the issue of inventory shrinkage. While fashion chains are leading the charge, pilot programs in pharmacies and consumer electronics hint at a broader retail adoption. Under EPR rules, RFID antennas are classified as packaging components. This means converters must either ensure these antennas don't interfere with recycling or manage separate waste streams for tagged items. This added complexity tends to benefit larger firms equipped with certified QA labs. As the return on investment cases for RFID mature, the technology is contributing an additional 0.5 points to market growth.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Alternative labeling technologies | -0.6% | National, concentrated in personal care and beverage sectors adopting shrink sleeves | Medium term (2-4 years) |

| Raw-material price volatility | -0.5% | National, affecting converters with limited hedging or pass-through clauses | Short term (≤ 2 years) |

| Release-liner EPR compliance costs | -0.4% | National, impacting converters without liner take-back infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Alternative Labeling Technologies

As personal-care and beverage brands pursue 360-degree graphics and container conformity, shrink sleeves, in-mold labels, and direct-to-shape printing collectively trim the market CAGR. Shrink sleeves in European beverages saw annual growth, drawing in cosmetics firms with their tamper-evident seals and glossy finishes. In-mold labels, favored in household cleaners, eliminate the need for post-production decoration and resist dishwashing or chemical exposure. Direct digital printing, which completely removes adhesive waste, finds favor with cosmetics testers and seasonal craft beer runs. However, self-adhesive labels carve out niches for variable data, regulatory text, and swift design changes—areas where sleeves and in-mold formats face challenges, thus containing but not fully neutralizing this limitation.

Raw-Material Price Volatility

In April 2024, Northern Bleached Softwood Kraft pulp prices increased, marking a significant rise from the previous year. Meanwhile, in Q2 2024, low-density polyethylene film prices rose, driven by inflation in feedstock costs. Emulsion acrylic adhesives, dependent on petrochemical monomers, see their prices closely tied to energy input costs. Converters without hedging strategies or quarterly pass-through contracts face sudden cost spikes, leading to margin compressions. The UK's Critical Imports Strategy highlights that adhesives and films, primarily sourced from EU and Asian routes, are vulnerable to disruptions at the Suez and Malacca chokepoints[2]PackUK, “Operational Plan 2024-2025,” gov.uk . Despite this, contingency procurement efforts remain inconsistent. These price surges compel smaller converters to either hike prices—potentially alienating clients—or withdraw from low-margin segments, resulting in a reduction in the market's CAGR during turbulent periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Adhesive Type: Emulsion Acrylic Dominance Reflects Regulatory and Performance Convergence

Emulsion acrylics captured 52.31% of United Kingdom self-adhesive labels market share in 2025, outperforming solvent and hot-melt chemistries by expanding at a 4.34% CAGR through 2031 as converters prioritize low-VOC, wash-off formulations that satisfy EPR recyclability metrics. Water-based coatings avoid solvent-recovery investments, deliver cold-chain adhesion, and score RAM Green, gaining favored-supplier status in supermarket and pharmaceutical bids. Hot-melt grades persist in logistics where instant tack and rough-surface adhesion trump VOC concerns, while solvent acrylics decline in premium wines due to tightening emission limits.

The United Kingdom self-adhesive labels market size for emulsion acrylic constructions is projected to widen further as the Medicines and Healthcare products Regulatory Agency enforces tamper-evident serialization, a use case requiring freeze-thaw resistance and autoclave survival, both delivered reliably by advanced acrylics. Avery Dennison’s S2045LL and UPM Raflatac’s RP770M illustrate incremental gains—enhanced clarity and deep-freeze tack—without solvent residues. Although niche silicone-free hot-melts such as BioBond BioMelt offer renewable content, their higher cost confines them to environmentally branded SKUs. Overall, acrylic conversion signals regulatory and functional convergence, anchoring growth leadership inside the adhesive taxonomy.

By Face Material: Paper Retains Share Despite Plastic’s Functional Advantages

Paper facestocks held 61.20% of the 2025 volume, yet plastic films are forecast to grow 4.12% annually as logistics and pharmacy applications demand tensile strength and moisture-proof performance beyond coated papers’ ceiling. Polypropylene balances economics and clarity for durable goods, while PET excels where chemical resistance and dimensional stability matter. Vinyl faces gradual displacement due to chlorine content penalties within RAM scoring.

Despite plastic’s momentum, the United Kingdom self-adhesive labels market size for paper remains sizable because food and beverage brands favor tactile textures, renewable sourcing, and lower EPR fees. Consistency-in-recycling rules classify “sticky paper” as non-recyclable unless adhesives wash off during pulping, prompting converters to pair repulpable acrylics with FSC-certified papers to safeguard supermarket listings. Hybrid innovations—paper-film laminates that combine haptic appeal with moisture barriers—emerge as compromise solutions. Going forward, growth bifurcates: premium spirits and cold-chain pharma tilt toward multi-layer films, while grocery and personal-care refill schemes reinforce paper’s mainstream anchorage.

By End-User Industry: Pharmaceutical Growth Outpaces Food and Beverage Maturity

Food and beverage labels maintained 40.67% of 2025 demand, underscoring the United Kingdom self-adhesive labels market’s historic core; yet pharmaceutical volumes are set to climb fastest at a 4.26% CAGR to 2031 thanks to serialization, Braille legislation, and tamper-evidence. Pressure-sensitive formats enable variable-data printing and tactile embossing in a single pass, displacing wet-glue paper labels that cannot deliver patient-critical content at speed.

The United Kingdom self-adhesive labels market size tied to pharmaceuticals further benefits from hospital cold-chain protocols that demand labels survive -20 °C storage, steam sterilization, and solvent wipes. Meanwhile, mature grocery volumes plateau, but SKU proliferation—driven by allergen rule changes—keeps press utilization high. Personal care straddles both worlds: growth in vegan and refillable products raises label counts, yet shrink sleeves absorb shampoo and deodorant lines that chase 360-degree graphics. Logistics labels scale with e-commerce shipments but endure steep price erosion due to linerless automation. Overall, end-use diversification cushions the market against single-segment shocks, yet pharma clearly sets the velocity frontier.

Geography Analysis

In the United Kingdom, while a unified regulatory framework exists, regional clusters distinctly influence consumption trends. In Greater London and the South East, dense fulfillment hubs are propelling the adoption of linerless logistics labels. This shift is largely driven by automation in high-speed sortation lines at major players like Amazon and DPD. Meanwhile, the West Midlands and Yorkshire, home to food-manufacturing plants, are prioritizing rapid allergen label changeovers. These plants are opting for paper-based facestocks in tandem with wash-off acrylics.

Scotland, with its whisky distilleries and craft gin producers, is adding a premium touch. These producers are choosing embossed foils and tactile laminates, commanding prices several times higher than standard labels. This strategy, while on a modest volume, generates significant value. Northern Ireland, under the Windsor Framework, is navigating a complex regulatory landscape. Converters here must adhere to both the UK Extended Producer Responsibility (EPR) and the forthcoming EU Packaging Regulation. This dual compliance challenge tends to benefit larger converters equipped with cross-border compliance teams.

Despite the digital lodgment under the Border Target Operating Model, Brexit-related challenges remain. Specialty adhesives are grappling with REACH registration, customs pre-lodgment, and navigating port congestions, especially at critical choke points like Suez and Singapore. Highlighting the supply-concentration risk, converters are strategically positioning their plants near multimodal freight corridors such as M1, M62, and Felixstowe railheads. This strategy ensures a reliable influx of raw materials while maintaining close proximity to major brand owners. While geographic fragmentation persists, the complexities of EPR reporting and the capital demands of digital presses are pushing consolidation. This trend favors sites capable of spreading compliance and equipment costs over a larger throughput.

Competitive Landscape

The United Kingdom self-adhesive labels market is moderately fragmented. Multinational suppliers dominate label-stock feedstock, while more than 200 regional converters compete on turnaround and niche specialization, rendering the United Kingdom self-adhesive labels market moderately fragmented. Innovation white-space coalesces around RFID-enabled logistics labels, decorative linerless wraps, and mono-material paper-PP laminates. Direct-to-shape digital print bureaus and shrink-sleeve specialists loom as disruptive entrants, particularly in personal care. The Environment Agency’s 2026 component-level reporting mandate elevates the role of compliance officers and quality labs, tilting the playing field toward firms with in-house regulatory expertise. Strategic responses include joint ventures for liner recycling, investment in HP Indigo and EFI Nozomi presses, and subscription-based supply contracts that lock in raw-material pass-through clauses.

United Kingdom Self-Adhesive Labels Industry Leaders

Avery Dennison

UPM

CCL Industries

Fedrigoni Self-Adhesives

HERMA GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: BioBond Adhesives launched BioMelt pressure-sensitive hot-melt formulations using plant-based feedstocks targeting label and tape markets, with sampling beginning Q4-2025.

- August 2025: Henkel introduced Technomelt EM 335 RE, a hot-melt adhesive engineered for PET bottle labels that separates cleanly during recycling, aligning with European recycled-content mandates.

United Kingdom Self-Adhesive Labels Market Report Scope

Self-adhesive labels are defined as versatile, pre-glued labeling materials that adhere to surfaces using pressure, eliminating the need for moisture, heat, or additional glue.

The self-adhesive labels market is segmented by adhesive type, face material, and end-user industry. By adhesive type, the market is segmented into hot-melt, emulsion acrylic, and solvent-based. By face material, the market is segmented into paper and plastic. By end-user industry, the market is segmented into food and beverage, pharmaceutical, logistics and transport, personal care, consumer durables, and other industries (including chemicals and industrial goods, automotive components, electronics and electrical equipment, medical devices and diagnostics, retail and apparel such as price tagging and promotions, office supplies like A4 sheet labels, construction materials, and household DIY products). For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Hot-Melt |

| Emulsion Acrylic |

| Solvent-based |

| Paper | |

| Plastic | Polypropylene |

| Polyester | |

| Vinyl | |

| Other Plastics (PE (LDPE, HDPE), Polystyrene (PS), Polyolefin blends, Polyamide (PA), Polyimide (PI), Specialty bioplastics (PLA, cellulose films)) |

| Food and Beverage |

| Pharmaceutical |

| Logistics and Transport |

| Personal Care |

| Consumer Durables |

| Other End-user Industries (Chemicals and industrial goods, Automotive components, Electronics and electrical equipment, Medical devices and diagnostics, Retail and apparel (price tagging, promotional), Office supplies and stationery (A4 sheet labels), Construction materials, Household and DIY products) |

| By Adhesive Type | Hot-Melt | |

| Emulsion Acrylic | ||

| Solvent-based | ||

| By Face Material | Paper | |

| Plastic | Polypropylene | |

| Polyester | ||

| Vinyl | ||

| Other Plastics (PE (LDPE, HDPE), Polystyrene (PS), Polyolefin blends, Polyamide (PA), Polyimide (PI), Specialty bioplastics (PLA, cellulose films)) | ||

| By End-User Industry | Food and Beverage | |

| Pharmaceutical | ||

| Logistics and Transport | ||

| Personal Care | ||

| Consumer Durables | ||

| Other End-user Industries (Chemicals and industrial goods, Automotive components, Electronics and electrical equipment, Medical devices and diagnostics, Retail and apparel (price tagging, promotional), Office supplies and stationery (A4 sheet labels), Construction materials, Household and DIY products) | ||

Key Questions Answered in the Report

How big is the United Kingdom self-adhesive labels market in 2026?

It is valued at USD 1.99 billion and is forecast to reach USD 2.39 billion by 2031, rising at a 3.72% CAGR.

Which adhesive type leads sales?

Emulsion acrylic formulations held 52.31% of the United Kingdom self-adhesive labels market share in 2025 and remain the fastest-growing at a 4.34% CAGR through 2031.

What end-user segment is expanding the quickest?

Pharmaceutical labeling is projected to grow at 4.26% annually, outpacing food and beverage by leveraging serialization, Braille, and tamper-evident mandates.

How are EPR rules shaping material choices?

Modulated fees reward RAM Green constructions, driving adoption of linerless, wash-off adhesives and mono-material film or paper labels that simplify recycling.

Are linerless formats gaining traction?

Yes, logistics operators in the South East and Greater London adopt liner-free solutions to lower waste tonnage and speed label application, reinforcing demand momentum.

Page last updated on: