United Kingdom Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

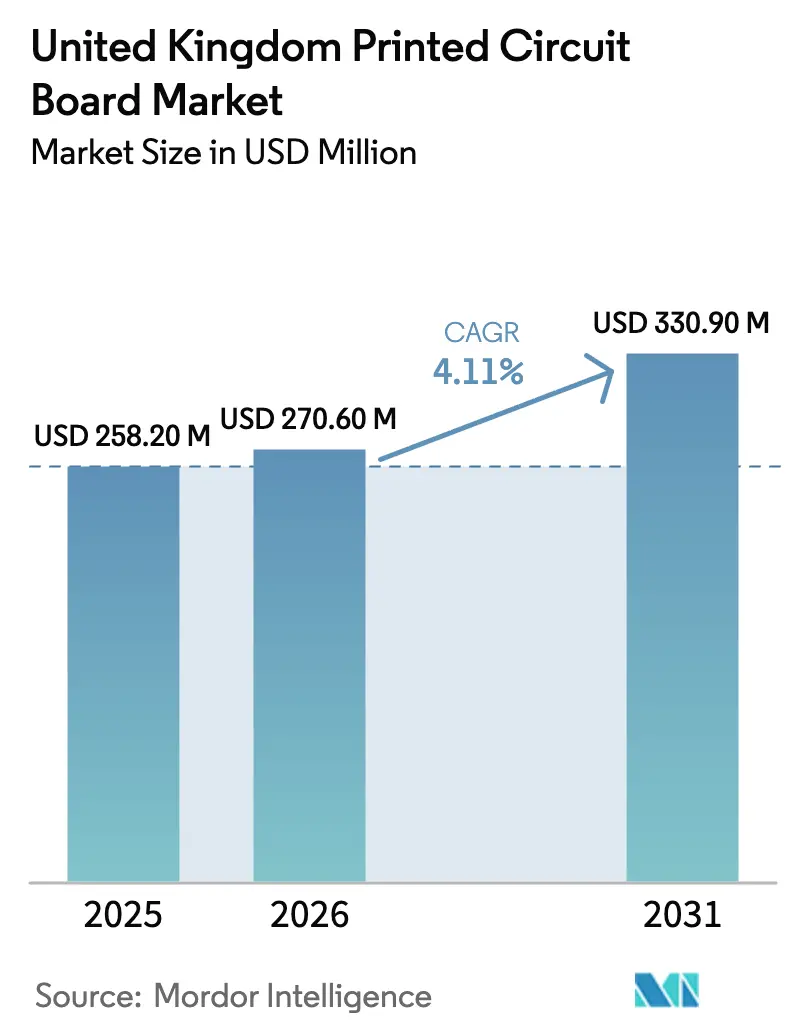

| Base Year Market Size (2025) | USD 258.20 Million |

| Market Size (2026) | USD 270.60 Million |

| Market Size (2031) | USD 330.90 Million |

| Growth Rate (2026 - 2031) | 4.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Printed Circuit Board Market Analysis by Mordor Intelligence

The United Kingdom Printed Circuit Board Market size is projected to expand from USD 258.20 million in 2025 and USD 270.60 million in 2026 to USD 330.90 million by 2031, registering a CAGR of 4.11% between 2026 to 2031.

The current market size reflects steady demand from aerospace, defense, data-center networking, and a selective reshoring trend that rewards high-reliability suppliers. Standard multilayer boards continue to anchor industrial controls and legacy telecom equipment, while flexible circuits expand in wearables and electric-vehicle (EV) battery harnesses. Government incentives, notably the Ministry of Defence’s munitions-plant program and Innovate UK grants, favor domestic fabricators that can meet AS9100 and NADCAP standards. At the same time, rising copper prices, talent shortages in high-density interconnect (HDI) design, and still-limited raw-board capacity constrain volume growth, keeping the sector oriented toward prototype and low-to-medium runs rather than mass production.

Key Report Takeaways

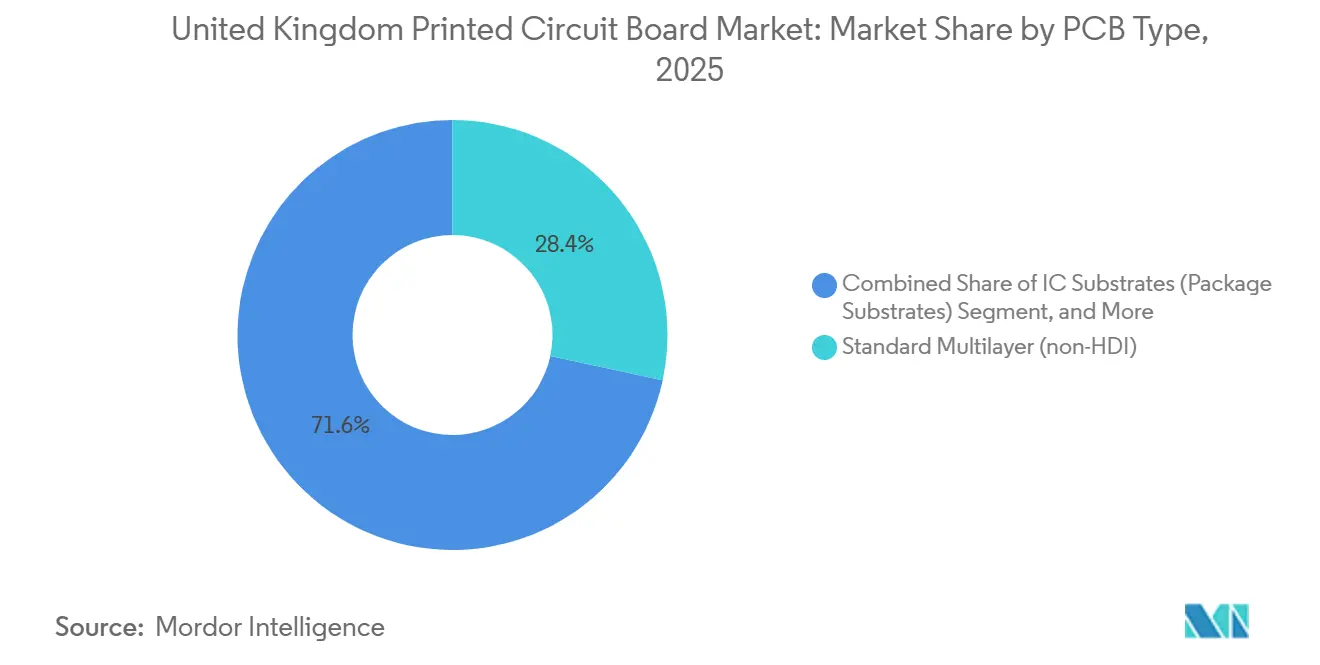

- By PCB type, standard multilayer boards led with 28.37% revenue share in 2025, while flexible circuits are on track for a 4.41% CAGR through 2031.

- By substrate material, glass-epoxy FR-4 accounted for 43.61% of the United Kingdom printed circuit board market size in 2025, yet high-speed low-loss laminates are forecast to expand at a 4.73% CAGR through 2031.

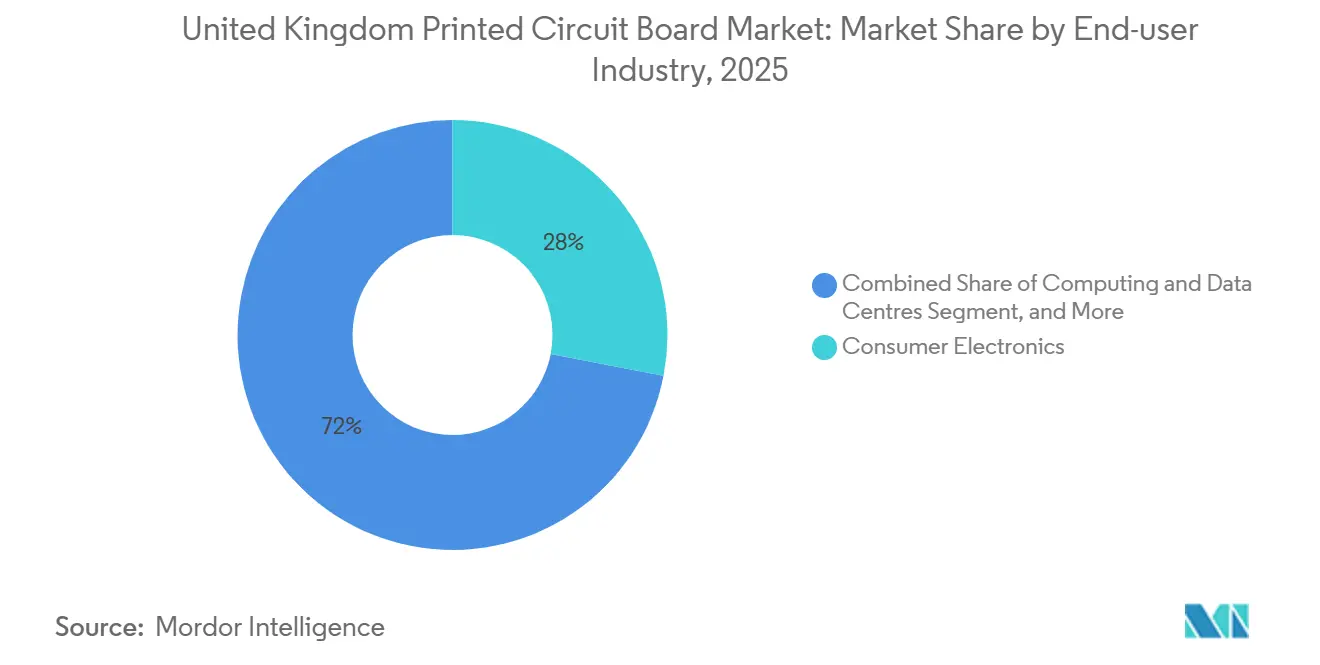

- By end-user industry, consumer electronics held 28.03% of the United Kingdom printed circuit board (PCB) market share in 2025, whereas automotive and EV applications are advancing at a 5.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reshoring of High-Reliability PCB Production for Defense and Aerospace Contracts | +1.0% | England (Bedlington, Fairford, Manchester), Scotland (Prestwick) | Medium term (2-4 years) |

| Proliferation of 5G Infrastructure Roll-outs Across Major UK Cities | +0.9% | England (London, Manchester, Birmingham), Scotland (Edinburgh, Glasgow) | Short term (≤2 years) |

| Growing Demand for Advanced Driver-Assistance Systems in UK-Made Vehicles | +0.7% | England (Sunderland, Bolton, West Midlands) | Medium term (2-4 years) |

| Expansion of Data-Center Footprint Driving High-Layer Server Boards | +0.5% | England (London, Manchester, Slough), Wales (Newport) | Short term (≤2 years) |

| Surge in Contract Manufacturing for Emerging UK Semiconductor Start-ups | +0.3% | England (Cambridge, Bristol, Manchester), Scotland (Edinburgh) | Long term (≥4 years) |

| Government Incentives for Sustainable Electronics Manufacturing | +0.1% | Nationwide, especially Made Smarter regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Reshoring of High-Reliability PCB Production for Defense and Aerospace Contracts

The Strategic Defence Review and a GBP 773 million (USD 1.07 billion) ordnance program announced in 2025 channel purchase orders to AS9100 and NADCAP qualified suppliers such as Amphenol Invotec and TT Electronics, shielding incumbents from low-cost Asian competition.[1]UK Ministry of Defence, “Strategic Defence Review and £773 million munitions factory investment,” GOV.UK Capital requirements for X-ray tomography, environmental stress screening, and full IPC-Class 3 traceability exceed GBP 5 million per line, which deters new entrants yet enables premium pricing that offsets the small production volumes. England’s Bedlington, Fairford, and Manchester clusters plus Scotland’s Prestwick aerospace hub now serve as preferred sourcing centers for BAE Systems and Thales, sustaining demand for multilayer boards exceeding 40 layers and specialized ceramic substrates. Lead-time advantages and intellectual-property control further justify local procurement even when unit costs run 25% higher than imports. These factors together elevate the United Kingdom printed circuit board market’s defense-aerospace segment above the overall market growth rate.

Proliferation of 5G Infrastructure Roll-outs Across Major UK Cities

Ofcom reported USD 12.6 billion (GBP 9.9 billion) in telecom infrastructure spend during 2025, with operators installing millimeter-wave small cells and massive-MIMO antennas that require controlled-impedance boards built on Rogers RO4000 and Isola I-Tera MT laminates.[2]Ofcom, “Connected Nations 2025,” ofcom.org.uk The high board count per square kilometer favors contract manufacturers that can rapidly iterate RF designs, such as TT Electronics’ Manchester site, which secured a USD 3.3 million (GBP 2.6 million) Innovate UK grant to scale RF module assembly. Short production runs and stringent phase-noise targets reward agile suppliers, pushing the United Kingdom printed circuit board (PCB) market toward higher technical content even as volumes remain modest relative to Asia-Pacific.

Growing Demand for Advanced Driver-Assistance Systems in UK-Made Vehicles

The GBP 2.5 billion (USD 3.4 billion) DRIVE35 program supports domestic ADAS electronics at Nissan Sunderland, Jaguar Land Rover, and Astemo’s Bolton facility.[3]Innovate UK, “DRIVE35 programme allocation,” innovateuk.ukri.org Automotive-grade boards qualified to AEC-Q200 endure -40 °C to 150 °C and intensive vibration, specifications that exclude most consumer-electronics fabricators. Trackwise Designs’ in-mold harness technology showcases flexible-circuit integration into structural parts, cutting wiring weight by 75%, although the company’s financial strain illustrates the capital intensity of automotive supply chains. As radar, lidar, and camera fusion penetrate mainstream models, domestic PCB suppliers able to co-locate with OEM engineering teams win design-in slots that sustain premium pricing and lift the United Kingdom printed circuit board market above baseline GDP growth.

Expansion of Data-Center Footprint Driving High-Layer Server Boards

London, Manchester, and Slough house 75% of the country’s hyperscale racks, and ongoing 400G to 800G switch upgrades demand 20-plus-layer backplanes on Megtron 6 or Astra MT77 material to maintain insertion-loss budgets below 28 dB at 56 Gbps PAM4. Concurrent Technologies’ plan to double assembly capacity by mid-2026, adding 14,800 square feet at its Colchester campus, underscores this pull-through effect. While land and power constraints limit mega-facility expansion in London, the pivot to edge nodes in Cardiff and Edinburgh diversifies geographic demand, giving Wales its fastest projected CAGR in the United Kingdom printed circuit board (PCB) market .

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper and Laminate Prices Eroding SME Margins | -0.6% | Nationwide, acute in Midlands and North England | Short term (≤2 years) |

| Talent Shortage in RF and HDI PCB Design Engineering | -0.4% | England (Cambridge, Bristol, Manchester), Scotland (Edinburgh) | Medium term (2-4 years) |

| Long Qualification Cycles in Medical and Defense Segments | -0.2% | National defense hubs and med-tech clusters | Long term (≥4 years) |

| Limited Domestic Fabrication Capacity Beyond Prototype Volumes | -0.2% | Nationwide structural gap | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper and Laminate Prices Eroding SME Margins

Copper climbed 21% from USD 9,173 per metric ton in Q4 2024 to USD 11,114 in Q4 2025 as Latin American supply disruptions converged with EV battery optimism.[4]International Monetary Fund, “Global price of Copper,” fred.stlouisfed.org Small UK fabricators lack hedge programs, so laminate suppliers pass cost hikes through within 60-90 days, compressing gross margins to low single digits. NCAB Group’s United Kingdom revenue dropped to SEK 207.1 million in 2024 after customer pushback on PCB price escalations, highlighting demand elasticity even in specialized segments. The absence of domestic copper-foil production removes any freight or currency advantage, locking SMEs into a price-taker role that slows the overall UK PCB market expansion.

Talent Shortage In RF and HDI PCB Design Engineering

A government workforce survey counted 27,245 electronics workers, with 39% nearing retirement and only 870 graduates emerging annually from relevant university programs. Apprenticeships fell 25% after further-education budget cuts, thinning the technician pipeline needed for HDI laser drilling, sequential lamination, and electromagnetic simulation. Competing semiconductor design houses lure RF specialists with higher salaries, leaving fabricators understaffed for complex stack-ups and substrate transitions. This talent gap lengthens design cycles, curbs adoption of any-layer via technology, and limits the United Kingdom printed circuit board market to less complex, lower-margin builds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Boards Accelerate In Wearables And EV Harnesses

Flexible circuits captured rising attention in 2025, yet standard multilayer boards still held a 28.37% share of overall shipments. The UK PCB market size for flexible products is forecast to grow 4.41% annually as Cambridge and Oxford med-tech firms embed flex substrates into clinical wearables, and EV makers specify lightweight battery-monitoring harnesses. Domestic innovators such as Trackwise Designs promote in-mold flex assemblies that cut cabling mass, although capital needs challenge smaller firms. Rigid one- and two-layer boards remain essential for price-sensitive consumer repairs, while HDI rigid-flex designs anchor aerospace avionics, a niche strengthened by the MOD’s supplier preferences. Low-volume, high-mix orders dominate, so suppliers invest in quick-turn setup rather than automated panel lines. In this environment, the United Kingdom PCB market favors agile shops that can shift between four-layer industrial orders and 30-layer satellite payload boards within the same shift.

A second driver comes from 5G millimeter-wave modules that require low-loss, high-frequency stack-ups. Although volumes are modest, their technical needs pull flex-rigid adoption forward. Conversely, large-screen consumer devices, once a growth engine for domestic EMS houses, rely on offshore producers, keeping local rigid volume muted. The next five years, of the United Kingdom printed circuit board (PCB) market, are thus marked by a gradual mix shift toward flex and rigid-flex, integrated battery harnesses, and HDI prototypes for automotive radar, collectively propelling segment value faster than unit counts .

By Substrate Material: Low-Loss Laminates Outperform FR-4 In Data-Center Builds

FR-4 retained a 43.61% share in 2025, anchoring power inverters, industrial controls, and legacy telecom gear. Yet the UK PCB market share for high-speed low-loss laminates is widening, underpinned by data-center backplanes that must hold insertion loss under 28 dB at 56 Gbps. Panasonic Megtron 6 and Isola Astra MT77, which cost 30%-50% more than FR-4, deliver dielectric constants below 3.5 and dissipation factors under 0.005, key parameters for 800G optical interconnects. In the United Kingdom PCB market, the domestic assemblers such as Concurrent Technologies leverage these materials in 20-layer builds shipped to London and Manchester hyperscalers.

Polyimide, ceramic, and metal-core substrates address high-temperature aerospace, RF power, and LED lighting respectively, but each remains under 10% of revenue. IC substrate production is negligible because the country lacks wafer-level packaging lines, a gap that the Custom Interconnect Andover project only partially fills. Certification demands from defense primes also spur ceramic adoption for thermal shock resistance, while eco-design mandates in the Design for Life roadmap push recyclability considerations into material selection. Together, these trends erode FR-4 dominance, raising the blended average selling price and boosting the United Kingdom printed circuit board market size despite constrained unit growth.

By End-User Industry: Automotive And EV Boards Outpace Consumer Electronics

Consumer devices commanded 28.03% of shipments in 2025, yet domestic smartphone assembly is minimal, so growth stays flat. Automotive and EV boards are forecast to post a 5.32% CAGR, the fastest of any sector, as DRIVE35 funding and Astemo’s Bolton ADAS plant lift demand for radar and camera processing PCBs qualified to AEC-Q200. Local supply is essential because design teams iterate firmware and layouts collaboratively with fabricators, reducing debug loops. Defense and aerospace maintain consistent order books, cushioned by the Ministry of Defence’s sovereign-supply stance, which shelters UK producers from offshore cost competition.

Data-center networking joins telecom infrastructure as a second growth node, fueled by 400G and 800G refresh cycles. Industrial automation remains stable, driven by retrofits inside Midlands and North England factories targeting energy savings. Medical devices, a high-value niche, benefit from ISO 13485 certified lines that deliver small quantities of respiration monitors and surgical robots. As circular-economy regulation tightens, med-tech OEMs reward modular board designs that facilitate end-of-life refurbishment, adding engineering revenue to the United Kingdom printed circuit board market.

Geography Analysis

England held 82.18% of United Kingdom PCB market revenue in 2025, anchored by Manchester, Sheffield, Bedlington, and Fairford facilities serving defense, telecom, and industrial clients. London’s hyperscale data centers ingest multilayer backplanes, while the West Midlands automotive corridor produces ADAS systems that rely on AEC-Q200 boards. The Made Smarter initiative funnels grants toward digital factories, yet most plants still specialize in quick-turn, low-volume work. Harwin’s Portsmouth expansion, a GBP 30 million (USD 38.4 million) project set for 2026 completion, illustrates how connector producers co-locate with board assemblers to shorten lead times and lower logistics emissions. TT Electronics’ Manchester site, buoyed by a USD 3.3 million Innovate UK award, will add RF module lines tailored for Ericsson and Nokia radio units, reinforcing England’s edge in microwave PCB know-how.

Wales, while starting from a smaller base, is projected to grow 5.07% annually through 2031. Newport’s emerging data-center cluster and supportive Welsh Government grants attract server board production as customers diversify away from London. The divestiture of TT Electronics’ Cardiff plant to Cicor in 2024 trimmed local headcount, but Cicor’s networked European footprint now feeds high-layer orders back into Welsh assembly. in the UK PCB market, sustainability incentives tied to the Design for Life roadmap steer PCB suppliers toward energy-efficient plating and water recycling, giving eco-certified plants a bidding advantage.

Scotland and Northern Ireland split the remainder. Edinburgh’s semiconductor design corridor and Prestwick’s aerospace park generate steady demand for HDI and ceramic boards. Yet many Scottish designs are still fabricated in mainland Europe due to limited local panel plating capacity. Northern Ireland has minimal board activity, sourcing prototypes from England and volume runs from Eastern Europe. Government semiconductor funds, earmarked largely for chip design, leave board fabrication under-supported, a gap that constrains regional supply resilience and caps the United Kingdom printed circuit board (PCB) market’s aggregate growth potential.

Competitive Landscape

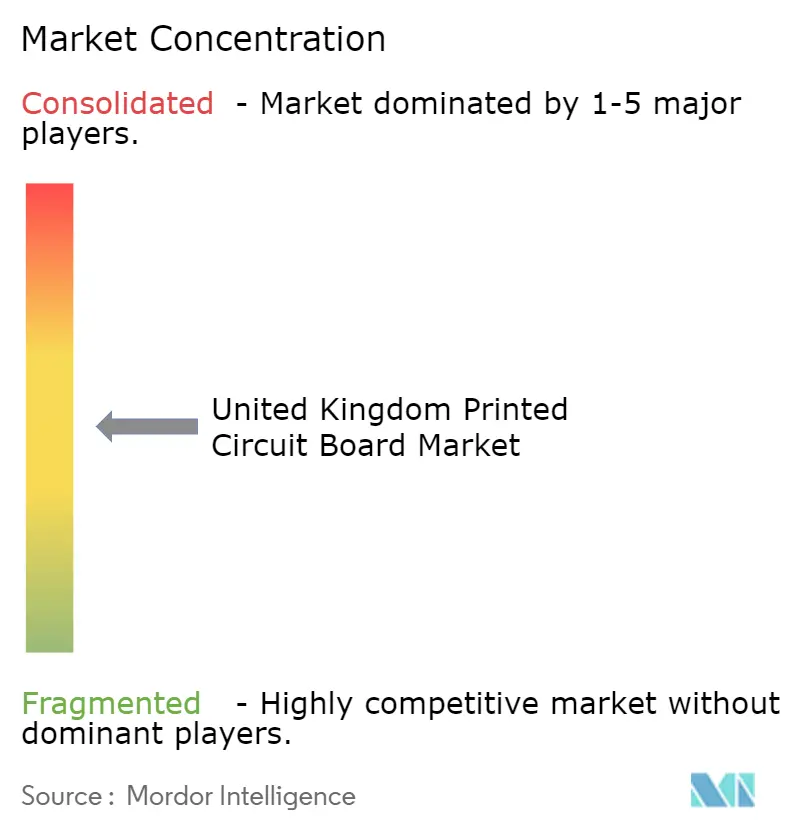

The UK printed circuit board market remains moderately fragmented as Europe-based EMS groups, niche domestic fabricators, and Asian contract manufacturers compete for high-mix orders. TT Electronics’ October 2025 acquisition of Cicor for GBP 287 million (USD 367.4 million) created a pan-European platform with vertically integrated fabrication, assembly, and box-build, elevating its share of defense and medical orders.[5]London Stock Exchange, “TT Electronics acquisition of Cicor,” londonstockexchange.com NCAB Group saw UK sales fall 24% in 2024, but its Q3 2025 European order intake rebounded 18% as data-center bids returned. ICAPE’s December 2024 purchase of ALR Services for GBP 2.5 million (USD 3.2 million) brought 300 active UK customers into its sourcing network, highlighting distributors’ role in bridging local design and offshore fabrication.

Smaller players invest in automation to protect margins. Incap UK upgraded its Newcastle-under-Lyme SMT line with Panasonic AM100 placement and NPM-GP/L printers, posting a 33% efficiency gain in 2025.[6]Panasonic Connect, “Operational efficiency at Incap UK,” eu.connect.panasonic.com MPE Electronics expanded Uckfield capacity by 2,064 square feet, adding floor space for conformal-coating and box-build stations. Custom Interconnect’s GBP 9 million (USD 11.5 million) Andover plant targets advanced semiconductor packaging, addressing a domestic gap in power-device assembly critical for EV chargers and renewable-energy inverters.

Barriers persist: AS9100, NADCAP, and ISO 13485 accreditations impose 18-36 month qualification cycles, deterring greenfield entrants. The lack of copper-foil and laminate factories inside the United Kingdom forces reliance on Japanese and Chinese suppliers, embedding foreign exchange risk. Nonetheless, white-space opportunities exist in flexible-hybrid electronics for medical wearables and rigid-flex battery harnesses. Firms that master design-for-sustainability and deliver rapid prototyping stand to capture incremental share as OEMs localize critical subassemblies.

United Kingdom Printed Circuit Board Industry Leaders

Trackwise Designs Plc

NCAB Group AB

TT Electronics Plc

Merlin Circuit Technology Ltd.

Eurocircuits NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Concurrent Technologies secured a 10-year lease on 14,800 square feet adjacent to its Colchester site to double PCB assembly capacity, targeting completion in H1 2026.

- October 2025: TT Electronics agreed to acquire Cicor Group for GBP 287 million (USD 367.4 million), expanding vertically integrated European PCB and electronics manufacturing.

- May 2025: Incap UK upgraded its first SMT line with Panasonic AM100 and NPM-GP/L equipment, achieving a 33% jump in throughput.

- February 2025: Harwin broke ground on a GBP 30 million (USD 38.4 million) multi-story facility in Portsmouth to double connector output, with rooftop solar expected to generate 244,000 kWh per year.

United Kingdom Printed Circuit Board Market Report Scope

The United Kingdom Printed Circuit Board (PCB) Market / United Kingdom Printed Circuit Board Market / UK PCB Market Report is Segmented by PCB Type (Standard Multilayer, Rigid 1-2 Sided, High-Density Interconnect, Flexible Circuits, IC Substrates, Rigid-Flex, Other PCB Types), Substrate Material (Glass Epoxy FR-4, High-Speed Low-Loss, Polyimide, Packaging Resins, Other Substrate Materials), End-user Industry (Consumer Electronics, Computing and Data Centres, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare Medical, Aerospace and Defence, Other End-user Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centres |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defence |

| Other End-user Industries |

| By PCB Type | Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centres | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defence | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the current value of the United Kingdom printed circuit board market?

The market is worth USD 270.6 million in 2026 and is on track to reach USD 330.9 million by 2031.

Which PCB segment is growing fastest in the country?

Automotive and electric-vehicle applications are projected to grow at a 5.32% CAGR through 2031, outpacing all other end-use sectors.

Why are low-loss laminates gaining share over FR-4?

Data-center upgrades to 400G and 800G Ethernet require tighter signal integrity, favoring materials like Megtron 6 that offer lower dielectric loss than standard FR-4.

How does copper price volatility affect UK PCB producers?

Many small and medium-sized fabricators cannot hedge raw material costs, so a 21% rise in copper prices during 2025 squeezed margins and delayed customer orders.

What makes defense and aerospace PCBs attractive for reshoring?

AS9100 and NADCAP certifications plus intellectual-property concerns drive buyers to domestic suppliers even at higher unit costs, securing premium pricing for qualified UK plants.

Which region outside England shows the highest growth potential?

Wales is forecast to expand at a 5.07% CAGR through 2031, fueled by new data centers in Newport and government support for sustainable electronics manufacturing.

Page last updated on: