UK Frontline Worker Technology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

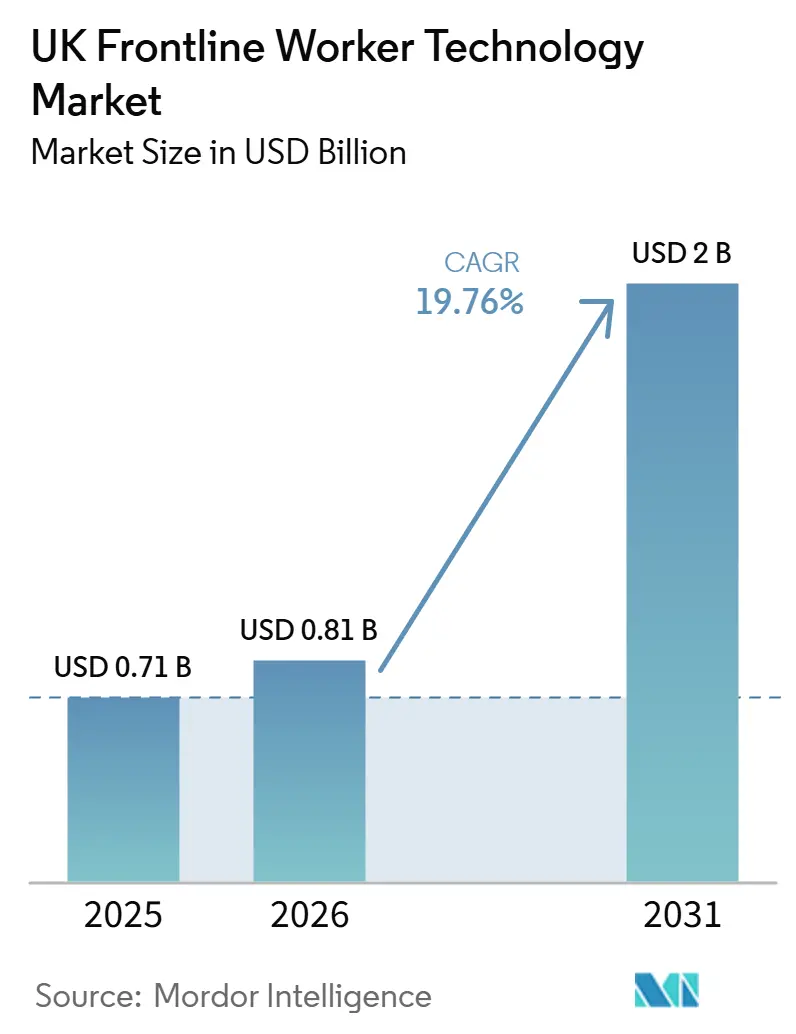

| Base Year Market Size (2025) | USD 0.71 Billion |

| Market Size (2026) | USD 0.81 Billion |

| Market Size (2031) | USD 2 Billion |

| Growth Rate (2026 - 2031) | 19.76% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Frontline Worker Technology Market Analysis by Mordor Intelligence

The UK frontline worker technology market size was valued at USD 0.71 billion in 2025 and estimated to grow from USD 0.81 billion in 2026 to reach USD 2.00 billion by 2031, at a CAGR of 19.76% during the forecast period (2026-2031). The United Kingdom frontline worker technology market is moving into a faster adoption phase because labor shortages continue to pressure employers in healthcare, logistics, retail, construction, and transport. The country also has a mature enterprise cloud base, which gives vendors a practical path to scale once pilot projects show clear operating gains. A large deskless workforce still relies on paper processes or older systems, so the room for digitization remains broad across multi-site employers. Buyers are increasingly looking for platforms that connect communication, scheduling, task execution, learning, and analytics in one environment, which favors vendors that can replace fragmented tools with a single operating layer. The United Kingdom frontline worker technology market is also being shaped by privacy, trust, and integration requirements, so suppliers with stronger governance controls and easier links to existing HR and ERP systems are better placed to turn initial deployments into larger contracts.

Key Report Takeaways

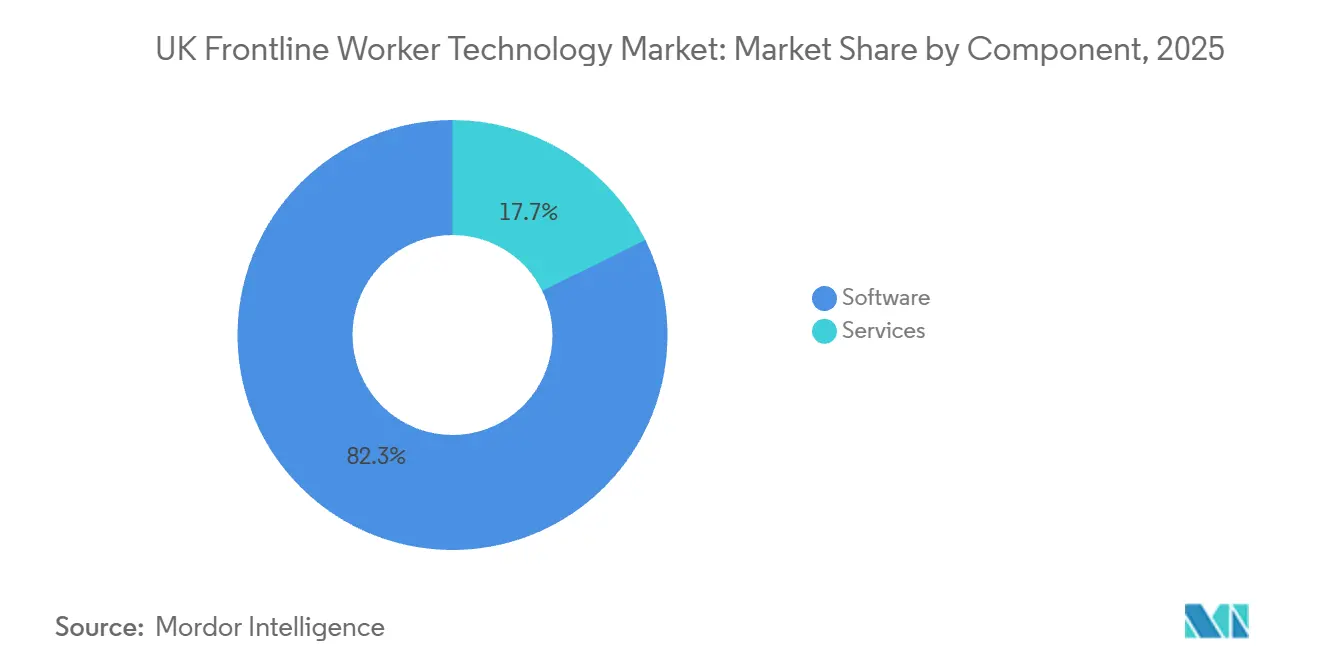

- By component, software held 82.28% of the UK frontline worker technology market in 2025, while services is projected to expand at a 22.31% CAGR through 2031.

- By deployment, cloud-based delivery accounted for an 80.41% share of the UK frontline worker technology market in 2025 and also recorded the highest projected CAGR at 20.38% through 2031.

- By organization size, large enterprises represented 70.58% of revenue in 2025, while SMEs are expected to grow at a 21.74% CAGR through 2031.

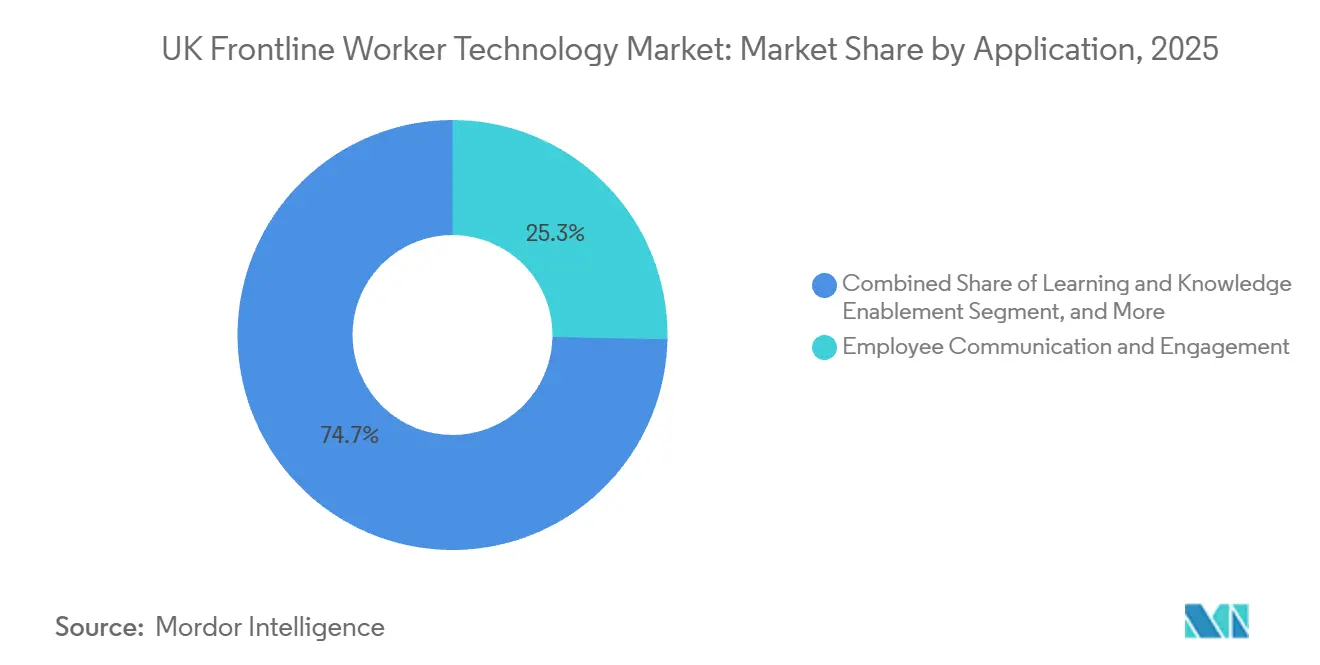

- By application, employee communication and engagement accounted for 25.32% share in 2025, while workforce analytics and performance management is projected to advance at a 22.86% CAGR through 2031.

- By end-user industry, retail and e-commerce captured 29.46% share in 2025, while healthcare and life sciences is forecast to grow at a 22.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UK Frontline Worker Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Need for Real-Time Task Orchestration Across Shift-Based Operations | +5.2% | UK-wide, with highest concentration in London, Midlands logistics corridors, and North West retail clusters | Short term (≤ 2 years) |

| Escalating Labor Shortages and Retention Pressure in Essential Frontline Sectors | +4.3% | UK-wide, most acute in England's NHS, Midlands and South East logistics, and London hospitality | Short term (≤ 2 years) |

| Broader Adoption of Mobile-First Workforce Applications and Wearable Devices | +3.6% | UK-wide, with stronger pull in London and the South East because of denser enterprise technology investment | Medium term (2-4 years) |

| Compliance Pressure for Safety, Auditability, and Training Traceability | +2.4% | UK national, elevated in construction, manufacturing, and healthcare under HSE oversight | Medium term (2-4 years) |

| Digital Work Instructions in Legacy Operational Workflows | +1.4% | UK national, with early use in large distribution and automotive manufacturing sites | Long term (≥ 4 years) |

| Unstructured Change Fatigue Among Supervisors and Frontline Teams | +0.6% | UK-wide, particularly visible in multi-site retail and large logistics networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Need for Real-Time Task Orchestration Across Shift-Based Operations

Shift-based operations in the United Kingdom frontline worker technology market now require faster coordination because e-commerce fulfillment, healthcare staffing pressure, and distributed store and site networks leave less room for manual task flow. Employers are increasingly moving away from separate apps for scheduling, communication, and learning, and toward a single frontline system that can manage activity across many locations. WorkJam’s March 2025 partnership with Rotageek showed this direction clearly by linking demand-driven scheduling with task management, communication, schedule self-service, and training in one workflow stack. Deputy and Geografia’s 2026 UK frontline study found that 88% of workers said AI made their jobs easier, yet only 42% said it reduced shift-related stress, which shows that speed gains do not automatically remove operational strain.[1]Deputy and Geografia, “The Big Shift Report 2026: State of the UK Frontline, Key Trends for Operations Leaders in 2026,” Deputy, deputy.com That gap matters because employers now want platforms that do more than push tasks; they want systems that help supervisors see bottlenecks early and adjust labor in real time. The United Kingdom frontline worker technology market, therefore, favors vendors that can turn task-level activity into usable managerial guidance without adding another tool for site teams.

Escalating Labor Shortages and Retention Pressure in Essential Frontline Sectors

Persistent labor shortages remain one of the strongest demand drivers in the United Kingdom frontline worker technology market because employers need to protect output with fewer available workers. The UK government’s 2025 occupational demand analysis identified 5.1 million workers, or 15.4% of total employment, in critical-demand occupations, while another 10.9 million workers were in elevated-demand roles. Adult social care alone had 111,000 vacant posts in 2024-25, and the sector is projected to need 470,000 additional workers by 2040 to meet rising demand from an aging population. These shortages increase the appeal of AI-assisted rostering, digital onboarding, and skills-matching tools because each of them reduces time spent on manual coordination. Employers are also using frontline systems to make existing teams more productive, which changes the buying case from basic digitization to workforce resilience. In this setting, the United Kingdom frontline worker technology market gives an edge to vendors that can show lower administrative burden and stronger retention support in healthcare, logistics, and hospitality.

Broader Adoption of Mobile-First Workforce Applications and Wearable Devices

Mobile access is becoming a core requirement in the United Kingdom frontline worker technology market because deskless workers need direct access to schedules, updates, tasks, and support during active shifts. A March 2026 YouGov survey commissioned by HIRSCHTEC and Flip found that 60% of deskless employees had no company-provided mobile app, and 1-third of those who did have an app had stopped using it because the tool did not deliver enough everyday value. The same study found that 85% of respondents considered secure single sign-on with direct access to all tools the most important app feature, which supports demand for unified platforms rather than scattered applications. This pattern helps explain why vendors are prioritizing mobile-first design, simpler onboarding, and fewer workflow steps for routine tasks. Wearables are also gaining relevance as employers look for safer hands-free workflows in industrial and healthcare settings. The British Safety Council noted growing attention to AI-powered wearables, including minister-level public support for such equipment in workplace safety settings, which adds policy visibility to this part of the market.

Compliance Pressure for Safety, Auditability, and Training Traceability

Compliance is becoming a stronger purchase trigger in the United Kingdom frontline worker technology market because paper processes create weak audit trails in safety-sensitive environments. Frontline employers in construction, manufacturing, and healthcare increasingly need digital records for checklists, incident capture, training completion, and task confirmation. Rapid Global’s UK research, released in October 2025, found that 18% of construction frontline workers still used paper-based processes for safety activities such as inductions, site sign-in, and incident reporting. That level of analog activity leaves a clear opening for software that can produce consistent records and reduce exposure from missing documentation. Compliance demand also supports the adoption of digital learning and work instruction modules because employers want proof that workers received and completed the required steps. As a result, the United Kingdom frontline worker technology market is seeing stronger interest in platforms that combine operational workflows with audit-ready records rather than offering one narrow compliance feature in isolation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy Systems Increase Integration Cost and Deployment Complexity | -2.2% | UK national, most pronounced in large manufacturing and retail chains with incumbent ERP infrastructure | Medium term (2-4 years) |

| Data Privacy, Worker Monitoring, and Employee Trust Concerns | -1.8% | UK-wide, elevated in financial services, healthcare, and the public sector under stronger privacy scrutiny | Short term (≤ 2 years) |

| Uneven Connectivity and Device Standardization Across Multi-Site Operations | -1.0% | UK national, most acute in rural logistics, offshore and remote construction sites, and dispersed care locations | Long term (≥ 4 years) |

| Budget Sensitivity Among Small and Mid-Sized End Users | -0.8% | UK-wide, most visible outside London and the South East where technology spending per employee is lower | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Systems Increase Integration Cost and Deployment Complexity

Integration remains one of the main restraints on the United Kingdom frontline worker technology market because many employers still run a mix of on-premises ERP systems, separate HR tools, payroll platforms, and older scheduling software. This fragmented stack raises implementation cost and extends rollout timelines, especially when internal IT teams cannot support complex interface work across several sites at once. The UK Department for Science, Innovation and Technology stated in its Technology Adoption Review, published in June 2026, that API interoperability and integration complexity were among the leading barriers to enterprise digital technology adoption, with the problem more pronounced outside London.[2]UK Department for Science, Innovation and Technology, “Technology Adoption Review 2025,” UK Government, publishing.service.gov.uk These conditions slow down return on investment because value from scheduling, communication, and analytics depends on clean links to workforce and payroll data. Vendors with pre-built connectors into widely used systems such as SAP SuccessFactors, Workday, ADP, and Sage are therefore better positioned to shorten deployment time and reduce buyer hesitation. The United Kingdom frontline worker technology market still has strong demand, but integration friction can delay purchase decisions even where the labor need is already clear.

Data Privacy, Worker Monitoring, and Employee Trust Concerns

Privacy and monitoring concerns remain a real brake on the United Kingdom frontline worker technology market because modern platforms often include task tracking, location visibility, behavioral data, and productivity metrics. Even when employers see value in these features, worker acceptance can weaken if the purpose of the data is not clearly explained. Deputy and Geografia reported in 2026 that 76% of UK frontline workers felt AI tools used by their employers lacked sufficient transparency. That trust gap matters because a technically successful deployment can still underperform if workers avoid or resist the system in day-to-day use. Vendors are responding by adding clearer permissions, visible data logs, and better communication around retention and oversight rules. This makes trust design part of product value in the United Kingdom frontline worker technology market, not just a legal check before deployment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads Platform Consolidation Across the UK Market

Software captured 82.28% share in 2025, which made it the dominant revenue base across the United Kingdom frontline worker technology market. That lead reflects a broad shift away from hardware-led point tools and toward cloud-based platforms that can coordinate communication, scheduling, tasks, learning, and analytics from a single control layer. Employers increasingly prefer one administrative environment because multi-site operations are harder to manage when each workflow sits in a different application. WorkJam’s March 2025 partnership with Rotageek supports this pattern because it joined demand-based scheduling with communication, training, and task execution inside one stack. The United Kingdom frontline worker technology market is, therefore, rewarding software vendors that can widen their functional reach without making site-level use more complex.

Services is the fastest-growing component, with a 22.31% CAGR through 2031, because complex deployments still need integration, training, configuration, and post-launch support. As platforms add more analytics and AI functions, the amount of governance and change management around each rollout also increases. This keeps services relevant even when software becomes easier to buy through SaaS models. Vendors that invest in certified partner networks and industry-specific templates can reduce implementation strain while preserving service revenue from optimization and support. That balance matters because the United Kingdom frontline worker technology industry still includes many large employers with older systems, and those employers need service depth before they can scale adoption across sites.

By Deployment: Cloud Consolidates as Hybrid and On-Premises Models Hold Select Positions

Cloud-based deployment accounted for 80.41% of the United Kingdom frontline worker technology market size in 2025 and is also the fastest-growing deployment model with a 20.38% CAGR through 2031. This position reflects the needs of retail, logistics, and healthcare operators that want centralized administration, faster updates, and less dependence on local infrastructure at each location. Distributed frontline teams cannot absorb downtime during shift changes, so reliability and remote support remain core reasons for cloud preference. The United Kingdom frontline worker technology market also benefits from a strong enterprise cloud base, which lowers the barrier for buyers who already use other hosted business systems. Cloud platforms are therefore becoming the default option when employers want quick expansion across multiple sites.

Hybrid deployment still keeps a place where employers want cloud usability, but retain tighter control over selected workforce records. This is especially relevant in environments such as NHS trusts, public bodies, and large financial services organizations where data handling choices remain sensitive. On-premises models also persist in large industrial sites where migration cost is still higher than the short-term gain from change. The DSIT review noted that cloud-technology expertise is less evenly distributed across UK regions, which suggests hybrid and on-premises demand will not disappear quickly outside the main digital hubs.

By Organization Size: Large Enterprises Lead Revenue While SMEs Set the Faster Growth Pace

Large enterprises represented 70.58% of revenue in 2025, which means the United Kingdom frontline worker technology market still rests on buyers that started deployments earlier and expanded across wider workforces. These employers had the scale to validate use cases in communication, scheduling, and task execution before smaller businesses moved in. Their current growth path is increasingly based on adding analytics, learning, safety, and AI layers to existing systems rather than starting from zero. This gives leading vendors a strong base for renewals and cross-selling in large accounts. The United Kingdom frontline worker technology market share of large organizations remains high because legacy complexity, compliance needs, and multi-site coordination problems are most acute in bigger enterprises.

SMEs are projected to grow at a 21.74% CAGR through 2031, which shows that platform economics are becoming more accessible below the large-enterprise tier. Modular SaaS pricing, easier deployment models, and simpler mobile-first workflows are opening the category to employers that could not previously justify full frontline software programs. The Employment Rights Act 2025 also supports adoption because better scheduling visibility and documentation have become more important for smaller employers that manage shift workers. This makes the SME segment an important expansion path for vendors that can deliver a shorter payback period without heavy IT involvement. The United Kingdom frontline worker technology industry is therefore broadening from enterprise-led adoption toward a more balanced customer base over the forecast period.

By Application: Workforce Analytics Accelerates While Communication Remains The Entry Point

Employee communication and engagement accounted for 25.32% share in 2025, which made it the largest application area in the United Kingdom frontline worker technology market. Communication remains the entry point because workers need a dependable daily channel before they can engage with scheduling, tasks, learning, or analytics in the same system. Platforms that cannot build routine app usage at this layer struggle to drive adoption of more advanced modules later on. This is why engagement tools still act as the anchor for broader workforce digitization in multi-site environments. The United Kingdom frontline worker technology market continues to treat communication as the base layer on which most later monetization depends.

Workforce analytics and performance management is the fastest-growing application, with a 22.86% CAGR through 2031, because employers increasingly want measurable labor intelligence rather than static performance summaries. As frontline platforms collect richer operational data, the analytics layer becomes the main route for proving return on investment through productivity, staffing, and retention outcomes. UKG’s June 2026 Workforce Intelligence Hub and Dynamic Workforce Operations launch fits this shift by placing real-time intelligence and execution tools on top of existing workforce management foundations.[3]Cisco and AI Workforce Consortium, “ICT in Motion: The Next Wave of AI Integration 2025,” Cisco, cisco.com Safety and compliance tools are also gaining weight as employers need better records, while learning and knowledge modules become more relevant when firms choose to upskill current workers faster rather than rely only on external hiring. The result is a stronger move toward unified application suites that reduce context switching for both workers and supervisors.

By End-User Industry: Healthcare Gains Momentum While Retail Holds the Largest Base

Retail and e-commerce captured 29.46% of the United Kingdom frontline worker technology market size in 2025, which kept the segment in the lead because of its high frontline headcount and constant need for schedule coordination, communication, and task execution. Retail operators run distributed site networks with daily labor variation, so the value of real-time mobile workflows is immediate and easy to test. This makes retail a natural early adopter for platform rollouts that begin with communication and extend into training, task tracking, and analytics. The United Kingdom frontline worker technology market has therefore built much of its installed base in retail and adjacent fulfillment activity. Even when other verticals grow faster, retail remains central because it offers scale and frequent operational touchpoints.

Healthcare and life sciences is projected to grow at a 22.58% CAGR through 2031, which makes it the fastest-growing end-user segment. NHS England reported in July 2025 that digital innovation programs in London were being used to improve productivity and free staff time across community and hospital settings. Deputy and Geografia also reported that UK healthcare employment in shift-based roles expanded 9% in 2025, which supports rising demand for tools that can manage labor across complex care settings. Construction is also gaining momentum as employers move away from paper safety processes, while logistics and manufacturing continue to invest where service continuity, compliance, and workforce visibility directly affect output. This leaves healthcare as the clearest growth engine within the United Kingdom frontline worker technology market over the forecast period.

Geography Analysis

London and the South East remained the main adoption center for the United Kingdom frontline worker technology market in 2025 because they hold the country’s densest mix of enterprise buyers, technology talent, and vendor access. Cisco’s AI Workforce Consortium reported that London accounted for 68% of UK technology sector jobs, which gives the region a stronger base for platform pilots, integration work, and scaling support.[4]UKG, “UKG Adds Agentic Orchestration to Its Workforce Operating Platform,” UKG, ukg.com That concentration also shortens the distance between frontline software vendors and enterprise decision-makers, which helps turn proof-of-concept projects into broader deployments. The Midlands and North West logistics corridors are emerging as secondary demand nodes because they support large distribution and fulfillment activity tied to omni-channel retail. These regions need real-time workforce tools to coordinate labor, tasks, and site communication across busy warehouse and store networks.

Scotland, Wales, and Northern Ireland contribute smaller absolute revenue today, but each carries sector-specific openings that support long-term demand in the United Kingdom frontline worker technology market. Scotland has a useful mix of NHS health boards and financial services employers, which supports demand for scheduling, compliance, and workforce communication tools. Northern Ireland’s cross-border logistics and agri-food operations create a practical use case for mobile task management in dispersed work settings. Wales offers a focused opening for safety and compliance applications because manufacturing and public sector employment remain important in its workforce mix. Public sector digital workplace initiatives also support this direction by raising interest in structured frontline workflows across government-linked organizations.

The United Kingdom frontline worker technology market still compares favorably with larger continental markets on frontline digitization, even though the adoption gap is not fully closed. A March 2026 YouGov study commissioned by HIRSCHTEC and Flip found that 60% of German deskless workers still lacked a company mobile employee app, which confirms that the digital gap in frontline roles remains a wider European issue. The United Kingdom frontline worker technology market benefits from lower language fragmentation than continental Europe, which makes implementation and support simpler for vendors serving multi-site employers. That combination, together with a more concentrated enterprise software environment, allows UK-focused vendors to move faster on rollout and local support than many multinational suppliers working across several language environments.

Competitive Landscape

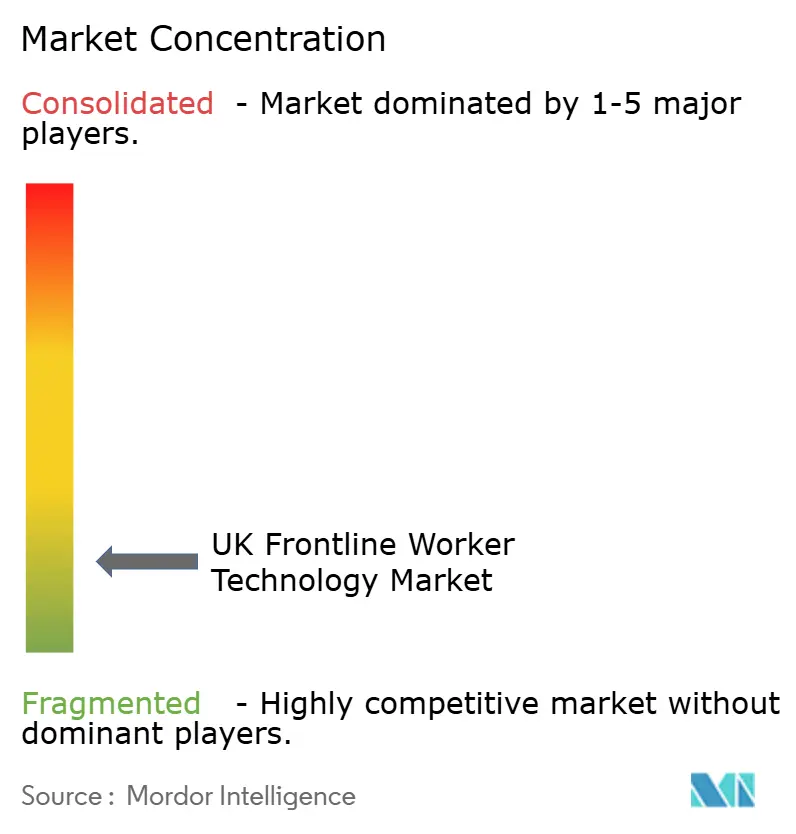

The United Kingdom frontline worker technology market is moderately fragmented, and no single vendor controls a majority across communication, scheduling, task management, analytics, learning, and safety. Competition is grouped into purpose-built frontline platforms, large enterprise suite vendors, and hardware-led suppliers that are adding software layers to their device businesses. Purpose-built vendors such as WorkJam, Quinyx, Zaptic, YOOBIC, and Beekeeper focus on frontline-specific workflows and faster operational deployment. Enterprise suite vendors such as Microsoft, SAP, ServiceNow, Oracle, and UKG extend existing collaboration or HCM systems into deskless use cases. Hardware-led suppliers such as Zebra Technologies and Honeywell are narrowing the gap between device provision and workflow orchestration by embedding more software and analytics around frontline activity.

Zebra strengthened this shift in June 2026 when it launched the Zebra Nucleus software platform and expanded its Workcloud suite with AI-powered operating tools for frontline environments. This move shows that hardware vendors want a larger share of workflow data and decision support, not only the device sales. Honeywell made a similar push in January 2026 with Performance+ for Guided Work, which combined voice-directed work with real-time analytics dashboards for connected workforce execution. Honeywell followed that direction in October 2025 with the CT70 mobile computer, which added AI-enabled processing and future RFID integration for frontline retail and logistics workflows. These launches reduce the old distinction between hardware specialist and software platform vendor in the United Kingdom frontline worker technology market.

Enterprise suite vendors are also raising the capability bar through automation depth rather than only feature expansion. ServiceNow’s February 2026 Autonomous Workforce launch added AI Specialists designed to resolve more than 90% of employee and IT service requests autonomously. ServiceNow and UKG had already signaled this direction in May 2025 through their agentic AI collaboration across scheduling, forecasting, absence management, and sourcing support for frontline teams. Purpose-built specialists still hold space where buyers want faster rollout, clearer workflow focus, or vertical-specific operating logic. The United Kingdom frontline worker technology market, therefore, remains open to both broad platforms and focused vendors, but win rates increasingly depend on local implementation strength, compliance readiness, and clear proof of productivity gains from real deployments.

UK Frontline Worker Technology Industry Leaders

Zebra Technologies Corporation

Honeywell International Inc.

Axonify Inc.

Legion Technologies Inc.

Panasonic Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zebra Technologies launched the Zebra Nucleus software platform and a major expansion of its Workcloud solutions at the ZONE 2026 customer conference in Nashville (June 1-4). The launch introduced AI-powered tools enabling IT leaders and frontline workers to convert real-time operational data into decisive action, marking a significant step in Zebra's transition from a hardware-first to a software-platform vendor.

- May 2026: UKG unveiled Pro Pay with Workforce AI at Payroll Congress 2026, incorporating agentic, assistive, and generative AI into its payroll platform. The solution detects, analyzes, and resolves payroll errors in real time, addressing a critical pain point for frontline and hourly workers, for whom payroll inaccuracy is a leading driver of voluntary turnover.

- April 2026: Zebra Technologies and Aiva Health announced a partnership to deploy hands-free nurse workflows combining Aiva's AI-powered clinical software with Zebra healthcare devices, the HC20/HC50 mobile computers, and the new WS101-H wearable badge. The solution targets frontline healthcare staffing efficiency amid persistent nursing shortages across UK and US hospital systems.

- February 2026: ServiceNow launched its Autonomous Workforce suite, simultaneously adding Moveworks to its AI platform. The update introduced AI Specialists capable of handling over 90% of IT service desk and employee service requests autonomously, extending ServiceNow's operational AI capability from back-office functions to frontline employee services across retail, healthcare, and manufacturing.

UK Frontline Worker Technology Market Report Scope

The UK frontline worker technology market comprises software platforms, connected applications, and associated services designed to digitally enable deskless and field-based employees across industries such as retail, industrial manufacturing, healthcare, transportation and logistics, hospitality, construction, and the public sector. These solutions improve frontline productivity, communication, task execution, workforce coordination, learning, operational visibility, safety, and compliance by integrating mobile devices, wearable technologies, artificial intelligence (AI), Internet of Things (IoT) sensors, cloud platforms, and enterprise business systems. The market includes revenue from software subscriptions and licenses, as well as professional and managed services supporting deployment, integration, customization, training, and ongoing support.

The UK Frontline Worker Technology Market Report is segmented by Component (Software, and Services), Deployment Mode (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Employee Communication and Engagement, Workforce Execution and Task Management, Workforce Scheduling and Coordination, Learning and Knowledge Enablement, Workforce Analytics and Performance Management, Safety and Compliance Management, and Other Applications), and End-user Industry (Retail and E-Commerce, Industrial Manufacturing, Healthcare and Life Sciences, Transportation and Logistics, Hospitality, Construction, Government and Public Administration, and Other Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Employee Communication and Engagement |

| Workforce Execution and Task Management |

| Workforce Scheduling and Coordination |

| Learning and Knowledge Enablement |

| Workforce Analytics and Performance Management |

| Safety and Compliance Management |

| Other Applications |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Healthcare and Life Sciences |

| Transportation and Logistics |

| Hospitality |

| Construction |

| Government and Public Administration |

| Other Industries |

| By Component | Software |

| Services | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Employee Communication and Engagement |

| Workforce Execution and Task Management | |

| Workforce Scheduling and Coordination | |

| Learning and Knowledge Enablement | |

| Workforce Analytics and Performance Management | |

| Safety and Compliance Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Industrial Manufacturing | |

| Healthcare and Life Sciences | |

| Transportation and Logistics | |

| Hospitality | |

| Construction | |

| Government and Public Administration | |

| Other Industries |

Key Questions Answered in the Report

How large is the UK frontline worker technology market in 2026 and what is the outlook to 2031?

The market stands at USD 0.81 billion in 2026 and is projected to reach USD 2.00 billion by 2031 at a CAGR of 19.76%.

Which component leads revenue in frontline worker technology across the United Kingdom?

Software leads the revenue base with an 82.28% share in 2025, reflecting the shift toward unified and cloud-native frontline platforms.

Why are UK employers investing more in frontline workforce platforms?

The strongest reasons are labor shortages, the need for real-time coordination, wider mobile adoption, and stronger compliance requirements for safety and traceability.

Which application area is growing the fastest through 2031?

Workforce analytics and performance management is the fastest-growing application, with a projected 22.86% CAGR as employers focus more on measurable labor intelligence.

Which end-user segment offers the strongest growth opportunity?

Healthcare and life sciences is the fastest-growing vertical, with a 22.58% CAGR, supported by staffing pressure and ongoing productivity-focused digital programs.

Are large enterprises or SMEs creating more growth momentum?

Large enterprises still hold the biggest revenue base at 70.58% in 2025, but SMEs are growing faster with a 21.74% CAGR as SaaS pricing and simpler deployment models improve access.

Page last updated on: